India's Energy Sector: Pride and Prejudice

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

India’s Energy Sector:

Pride and Prejudice

T

he Indian energy sector people; wholesale price index gas will be sourced at interna-

and particularly the oil inflation hovers in the 8-9% tional prices. In today’s market,

and gas sectors is an area level, annual fuel subsidies are the long-term base price for LNG

of high personal and pro- in excess of US$20 billion and delivered to India would at a

fessional interest to us and to are primarily funded by the Gov- minimum be US$11-12/million

our company. ernment coffers. The fiscal defi- British thermal unit (mmBtu) and

We have had the pleasure to cit is estimated at around 5.9% quite possibly higher at say,

interact with Dr. Vijay Kelkar for 2012 and balance of pay- US$14-15/mmBtu at US$100/bbl

over a long period of time and ments deficit in the US$12.5- oil price. Prices below US$11-

have become his admirers. We 13.0 billion range during Q3 12/mmBtu are uneconomic for

have found his intellect, insights, 2012. All this is occurring in an new LNG production. India may

and sense of practical realities environment of the economy also need to pay some or all of the

an immense inspiration. Our being expected to grow at a so called “Asian Premium.” This

contribution to the festschrift is minimum of 8-9% annually for increment reflects the additional

a testimony of our respect and the next five years. price that some buyers—specifi-

admiration for him. India is not blessed with abun- cally East Asian countries—cur-

The purpose of this paper is to dant oil and gas resources. Find- rently pay to ensure supply

lay out directional concepts that ing and proving reserves have also security for both oil and gas. It is

are essential, possibly critical for been challenging. The country im- crucial to realize that the “Asian

India’s energy sector to perform ports more than 75% of the crude Premium” that is widely debated

efficiently. It is not to be viewed oil that is domestically processed today is not the differential be-

as a roadmap for deregulation, and this will increase in the com- tween the price that buyers are

but should help provide some ing years. At a time when crude asking for and Henry Hub prices.

guidance on how India can better prices have risen to the US$100- It is the difference between what

position itself in an increasingly 120/barrel (bbl) range, India’s is paid today and the long-term

competitive world where terms import bill is set to scale to new base price to justify new LNG

like ‘energy security’ and ‘re- heights. For all these reasons, supply investments.

source nationalism’ are funda- business as usual is not an option. The message is clear. It is un-

mental components of a national A growing base-load energy likely to see a large fall in oil

energy policy. requirement is guaranteed for a prices, thus, high energy prices

country with the second largest are here to stay and India in its

R Challenges That India Faces population in the world with a current state of play has no

but Cannot Do Much About per capita energy consumption choice but to import most of its

E The country has gone through that is one-third of the world energy requirements.

turbulent times in the last two average. Indigenous gas sup-

P years. A series of corruption plies have dropped and pipe- Challenges That India

Faces but Can Do

O cases and scams have rocked the

Indian Government and led to a

line gas imports from Iran or

Turkmenistan are probably ‘pipe- Something About

R shaky climate for investors: both

domestic and foreigners alike.

dreams’. India has latent demand,

but limited indigenous resources.

India is saddled with a combi-

nation of regulations, consumer

T India’s population continues to

increase from well over 1 billion

The fuel for growth will almost

certainly be imported gas, but this

resistance, bureaucracy, and

much misinformation.

Country

Focus 26 HYDROCARBON ASIA, JULY-SEPT 2013 Visit our website at: http://www.safan.com

India’s PSUs – Massive engines was to make the country self-reli- over national resources and to

that must lead and not follow! ant. It is therefore understand- develop them for the benefit of

A newly independent India in able that unlike the private sector its citizens. The performance of

1947 was struggling with eco- firms, profit making and retain- Indian NOCs (that are also PSUs)

nomic inequalities, high unem- ing market share or customer sat- in achieving the second of these

ployment rates, socio-economic isfaction were not the primary objectives has been poor.

problems, weak industrial base, objectives of a PSU. India needs to find a path to

inadequate investments, lack of The Indian government will enter the modern energy world,

infrastructure, and imbalances back its ‘ratnas’ at any cost and the PSUs and for the purpose of

across various states. The con- this leaves them with a sense of this paper, NOCs, need to lead

cept of Public Sector Undertak- security. However this also from the front. An ideal NOC

ings (PSUs) was developed to makes the enterprise subject to would be an:

stem these issues and to help the regular interference from minis- • Organization that is based

nation embark on self-reliant eco- tries, limited operational and on meritocracy

nomic growth. PSUs would then financial autonomy, inflexible • Organization that eliminates

lay the foundation for the coun- human resource policies, and or minimizes corruption and

try’s industrial development, conflicting operative procedures cronyism

maximize its long-term goals, that ultimately slow down the • Organization with financial

and contribute towards its socio- decision-making process. and operational autonomy

economic development. It is imperative that these PSUs • Organization that would ac-

Based on their profit churning rid themselves of the tarnished knowledge and reward a good

ability, these PSUs are granted image that is cast upon them. performance whilst penaliz-

some financial and operational The Government was on the right ing poor performance

powers and classified accord- track when it decided to divest • Organization that supports

ingly as ‘ratnas’ or crown jewels. its stake in some of the PSUs. By the social agenda of the

Accordingly these companies encouraging investments from government

are known as ‘Maharatnas’, the private sector, a public- The performance of PSUs (and

‘Navaratnas’, or ‘Miniratnas’. private partnership would be NOCs) in achieving the goals of

A Maharatna status empowers formed. This would not only strengthening India’s industrial

the PSU to take investment de- make the PSU more competitive, base, stimulate domestic produc-

cisions of up to US$0.9 billion1 but also bring it out of its isolation, tion, and achieve the social and

without seeking government ap- bring about more awareness of nation building objectives has been

proval. As this is the highest sta- the competitive forces, and even- massively sub-optimal. Much of

tus awarded to a PSU in India, it is tually enhance its profitability. the blame for this can be attrib-

also the highest level of autonomy Such a move would also: uted to failures to provide a regu-

a PSU can attain. Navaratna and • Help source funds to carry latory framework that rewards

Miniratna companies also enjoy out expansion plans rather good performance and penalizes

some autonomy, but to a lower than the Government having poor performance. The failure has

extent. Indian Oil Corporation Ltd. to shoulder the entire burden impacted both the upstream and

(IOCL) and Oil and Natural Gas • Make the shareholding pat- downstream sectors in India and

Corporation (ONGC) are both tern more diverse and thus fundamentally relates to:

Maharatna companies. bring in more transparency • NOCs not getting correct price

The intended purpose of these to the corporate governance incentives and signals

PSUs was to strengthen India’s structure • NOCs lacking autonomy

industrial base, develop domes- • Reduce the extent to which and being subject to politi-

tic production, and ensure growth the Government is involved cal interference

across all parts of the country in ‘less important’ matters • Bureaucracy based on in-

whilst meeting social commit- cumbency and cronyism

ments. At the inception stage, In an ideal world, how should a rather than merit

Government backing was crucial PSU perform?

as large sources of funds were National oil companies (NOCs) Upstream issues – unlocking of

required whilst returns would be including those in India were resources

minimal. The task at hand thus created to assert sovereign rights In 1997, the Indian Government

HYDROCARBON ASIA, JULY-SEPT 2013 27

approved the New Exploration at 825 million barrels of oil— (ICB) process. Successful bidders

and Licensing Policy (NELP) 30% of which is offshore. Among will then enter into a contract with

with the hope of accelerating the oil and gas discoveries in India the government and up to 100%

pace of domestic oil and gas ex- between 2006 and 2011, RIL tops participation by foreign compa-

ploration activities. India’s oil the list. A total of 223 discover- nies will be permitted. Simultane-

and gas exploration can thus be ies were made; 78 production ous exploration of oil, gas, CBM,

broadly classified into the pre- sharing contracts (PSCs) were tight gas, and shale oil and gas

and post-NELP era. The practice signed—41 gas and 37 oil. from the same contract area will

of auctioning_off oil and gas India’s coal-bed methane also be permitted. Thus, it looks

blocks under NELP commenced (CBM) reserves are estimated at like the government has learnt a

in 1999. It was in this round that some 168 trillion cubic feet (tcf). valuable lesson from its experi-

Reliance Industries Ltd. (RIL) bid In spite of 33 blocks offered to ence with CBM in that upon find-

and won the D6 block in the date, CBM has been discovered ing its first molecule of shale oil/

Krishna-Godavari Basin (KG-D6) only in five blocks. Four are gas, there would be no confusion

located off India’s eastern off- owned by private companies and about what to do next. The policy

shore. Some five years later, RIL one by an NOC. For many years, should be finalized by March 2013

discovered gas in this block and ambiguous government policy and then a date will be fixed

five years later commercial gas stymied CBM exploration be- for the ICB process. Realistically

production commenced. The cause simultaneous exploration though commercial exploitation

country hoped that RIL’s KG-D6 of CBM with oil and gas was pro- of shale reserves in India is still a

gas supply would effectively hibited. CBM commercialization few years away, material produc-

double India’s overall domestic to date continues to face delays tion is at least a decade away.

gas production from 2008 levels due to either refusal to award Regulatory approvals as well as

and minimize the country’s need clearance by the environmental statutory land clearances will need

for gas imports. However, de- ministry to the contractor or dis- to be acquired before a contractor

spite a successful ramp-up in putes between coal and petro- can start the drilling and then the

production that surpassed 2.15 leum ministries on issues relating ‘fracking’ process. There are other

billion standard cubic feet per to land acquisition. issues around water availability

day (bscf/d) in March 2010, KG- Commercial production has as well that need to fit within the

D6 gas production has subse- commenced from two blocks framework of existing central and

quently declined and is currently with overall production esti- state government laws. It is also

estimated at 1.14 bscf/d. Hopes mated at a paltry 11 million worth noting that countries such

of virtual self-sufficiency have standard cubic feet per day as Australia and China are much

now been dashed. (mmscf/d). CBM production is ahead of India in their shale gas/

The disappointing performance thus at its nascent stages and a oil exploration and therefore se-

from KG-D6 highlighted the poor target production of 260 mmscf/ curing the necessary hardware will

record of results from India’s d by early 2014 is impossible! also be an issue for India. Explo-

NELP rounds. Since 1999 over nine With its massive revolutionary ration for shale oil and gas thus

rounds of NELP, a total of 257 success in the US, nearly every remains a wildcard for India and

blocks have been auctioned off. country is excited about its shale much depends on the position

Total discoveries are estimated at gas/oil prospects. As each goes that the government will take. If

107, of which, only 31 discoveries about looking for shale reserves, it can implement the policy at the

have been declared commercial. India too is no different. India’s earliest and lay out a clear and

Nineteen of these discoveries were recoverable shale reserves are es- structured process for the inves-

declared by Reliance India Ltd timated at anywhere between 6 tor and contractor, then the mol-

(RIL), eight by Gujarat State Pe- and 63 trillion cubic feet (tcf). These ecules may come into the market

troleum Corporation (GSPC), and are unofficial estimates. A draft before the end of this decade.

two by Niko Resources. Out of shale oil and gas policy was pre- Alternatively, shale exploration

these there is only one producing pared by the oil and gas ministries might go down the CBM route

asset. KG-D6 is the only produc- early this year. It is proposed that where even after a decade of

ing asset in the post-NELP era! blocks for shale exploration will exploration success, commer-

India’s overall balance of re- be made available via an open in- cial success remains evasive!

coverable reserves is estimated ternational competitive bidding Few general observations can

Country

Focus 28 HYDROCARBON ASIA, JULY-SEPT 2013 Visit our website at: http://www.safan.combe made with regards to In- fied into two regimes: adminis- incentive for a prospective pro-

dia’s upstream: tered price mechanism (APM) and ducer to invest. The risks are far

• Recent discoveries are mostly market price. APM gas was origi- greater than the rewards.

being made by private com- nally the gas sold from blocks that

panies and not NOCs. were awarded to two Indian NOCs Downstream retailing – A level

• High resource potential has on a nomination basis. The price playing field?

been identified but remains of this APM gas is regulated by In many countries, NOCs are

several steps away from com- the Government and was origi- required to service domestic de-

mercialization. nally sold at US$1.7-1.8/mmBtu. mand at prices determined by the

• Central government needs to It is this gas that spoilt the Indian Government, rather than the mar-

seek in-principle approval of market and especially the public ket. Exports are not permitted un-

the respective State govern- utility companies by creating un- less domestic demand is met.

ments before it can even put reasonable expectations! When Sellers are therefore forced to

up a block for exploration. RIL’s KG-D6 gas entered the In- forego higher prices (and profit!)

There are several clearances dian market, its wellhead price that may be available in the export

and approvals that the con- was fixed at US$4.2/mmBtu at market. This is the situation in the

tractor must obtain before the landfall and NOCs then began Indian market where LPG, kero-

drilling process can start. All lobbying for a higher price for the sene, diesel, and to a lesser extent

this can be cumbersome and APM gas. Consequently the APM gasoline are subsidized by the gov-

hold back the exploration gas price was raised to US$4.2/ ernment. Around 60% of these sub-

process by several months. mmBtu as well. Regasified LNG sidies (known as under recoveries)

India’s gas sector is fragmented (RLNG), CBM, as well as domes- are borne by the Government who

and current regulation lacks uni- tic gas sold from PSCs and NELP reimburses these state-owned oil

formity. The Directorate General rounds all fall in the “market price” marketing companies (OMCs) that

of Hydrocarbons (DGH) is the category and these are sold at are also refining companies (and

upstream regulator and the Pe- various other rates. therefore NOCs) with direct cash.

troleum and Natural Gas Regu- India is short of gas. As a conse- Around 30% of these under recov-

latory Board (PNGRB) oversees quence, the Government regu- eries are borne by upstream NOCs

the downstream activities. Some lates its use. The power and and the remainder is borne by the

policies and regulations are in fertilizer sectors are designated OMCs themselves. For the six

place but they concentrate more as priority sectors and these are months during April-September

on infrastructure, pipelines, and partially regulated by the Gov- 2012, these under recoveries are

gas transmission rather than pric- ernment. The government allo- estimated at US$15.6 billion and

ing and downstream gas mar- cates indigenous gas to these the Government has so far agreed

keting. New Delhi has made priority sectors at heavily subsi- to reimburse these OMCs for only

some cursory moves toward dized rates. Over time, private 35% of the total. This lag in the

deregulating India’s gas busi- investors have entered these sec- compensation mechanism is typi-

ness—these “policies,” for want tors, but the government retains cal and severely impinges the fi-

of a better word, are focused on strong control. The sectors repre- nancial liquidity of these OMCs.

increasing competition between sent 70% of India’s gas consump- Private retailing firms such as

producers and distributors, de- tion. An increase in the domestic RIL, Essar, and Shell can adhere to

controlling gas prices, and so on. gas price raises the cost of input the government controlled prices

But since India lacks a cohesive to the power and fertilizer com- if they wish to but are not reim-

gas industry framework to begin panies that ultimately adds to the bursed. There is thus an obvious

with, New Delhi’s current nebu- Government’s subsidy burden. reluctance on their part to expand

lous reform plans will probably Thus from a contractor’s perspec- their retailing activities. The total

take a great deal of time to clarify tive—NOC or private company— number of retail stations owned

and implement. there is neither the freedom to by NOCs exceeds 38,000. This

sell the gas to a customer of their dwarfs the number of private re-

Gas pricing – penalty for discov- choice nor is it allowed to sell the tail outlets—estimated at just over

ering gas gas at a price that they believe 3,000. Private retail players hold

India has multiple gas prices, reflects the international market the government responsible for

but broadly, these can be classi- price. There is therefore limited their precarious state, as the gov-

HYDROCARBON ASIA, JULY-SEPT 2013 29ernment had invited private play- would result in the opposition However leaving those issues

ers and entry eligibility was sub- storming in! aside, there is a genuine crisis in

jected to a minimal US$0.36 billion India where the pool from where

investment in the infrastructure. Retaining manpower - India los- individuals can be chosen for oil

However, it has not yet ensured a ing out on a ‘class’ of leaders and gas jobs in the NOCs is shrink-

level playing field by controlling For the NOCs, the Public Enter- ing. India is at a stage where the

the retail prices. The retail market prises Selection Board (PSEB) is older generation is reaching re-

would turn competitive if the responsible for selection and place- tirement age and the younger gen-

prices are allowed to float in tan- ment of personnel in the posts of eration is coming to fill in those

dem with the international mar- Chairman, Managing Director, positions. Clearly, both genera-

ket, or private players were also and Functional Directors, as well tions have different mind-sets. For

reimbursed for selling products at as in posts at any other level as the older generation, working in

Government-controlled prices. may be specified by the Govern- the public sector was something to

Any expansion plan of the private ment. Getting the right person for be proud of, but the younger gen-

players in the retail sector would the top job is not easy especially eration prefers to work in private

be driven by a clear direction in when the job market has become sector. Thus India needs to think

the subsidy regime. increasingly competitive and em- about how this handover from one

Understandably, pricing, ployees have moved on from the generation to the other can be done

whether it is pricing of natural ‘one job for life’ attitude. With at- smoothly. The current age of re-

gas for sensitive sectors such as tractive pay packages, career ad- tirement is 60 years. After that, the

power and fertilizer or of sensi- vancement options, and better majority of those who held senior-

tive products such as gasoil, do- quality of life offered, it is a no level positions with more than 30

mestic LPG, and PDS kerosene, is brainer that private companies years of experience under their

a “red hot” political item for In- have successfully managed to belt are either snapped up by pri-

dia. A build up in subsidies puts poach manpower from NOCs. The vate companies or move on to start

a lot of pressure on the NOCs that problem is further exacerbated by their own consulting companies.

remain cash strapped until the two issues:

Government reimburses them ei- • Meritocracy is not strongly Philosophies That India Can

ther at the end of the quarter or adhered to – It is not uncom- Adopt

after six months. These are tough mon to see that the right can-

times for India—crude oil prices didate who may also be a top NOC model

remain well over US$100/bbl, the contender did not get the job As a rule, NOCs are infamously

country is struggling to bring because of intervention by a known for their incompetence,

down inflation rates, its own cur- Cabinet Minister. bureaucratic red tape, inefficiency,

rency is underperforming against • Cronyism is deeply en- and corrupt practices. They are

the dollar, and the subsidy situa- trenched in the system – A considered to be unreliable part-

tion continues to be worrisome. preferential treatment to an ners where a regime change could

Due to all this, as the country’s old friend is detrimental as it spell the end for contracts that

fiscal deficit mounts, it becomes not only disregards qualifica- were inked during the previous

increasingly challenging for the tion or merit, but also implies regime. In the oil and gas world,

Government to reimburse these that at some stage there could there are a few exceptions that

NOCs. Governments have an be a return of favor. have set themselves apart as be-

obligation to care for its people. NOCs have a deep connection ing well run, world-class opera-

In India’s case, this means the with the Government. It is there- tors that deliver on their fiscal,

government has to be quasi-so- fore only natural that some of that social, and sovereign commit-

cialist. The complicating factor political culture would flow into ment. India could learn from the

is that India is a democracy. Gov- the NOC culture too. The philoso- performance of these NOCs.

ernments have to focus on their phy of the Indian political culture

electoral prospects. is such that sycophancy would PETRONAS

A removal of subsidies in en- help one go a long way. A compe- PETRONAS is the state oil com-

tirety and implementation of tent strong willed person who pany of Malaysia. It was founded

market-based pricing would in- correctly says ‘no’ would be sacked in 1974 and was ranked 68 in the

vite the wrath of the public and at the very next opportunity. Fortune Global 500 list of compa-

Country

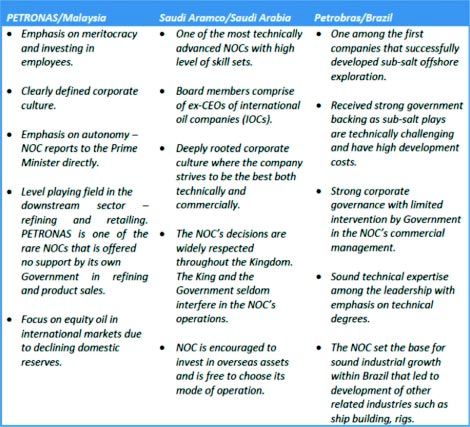

Focus 30 HYDROCARBON ASIA, JULY-SEPT 2013 Visit our website at: http://www.safan.comnies for 2012. The company was discovery of oil and natural gas eral government has control of

initially set up to manage and that led to the growth of Saudi around 56%, whilst private own-

regulate Malaysia’s upstream oil Aramco and eventually trans- ers hold 30% of the voting share.

sector. It then worked on pro- formed the desert kingdom into a The company started to focus on

duction-sharing contracts with modern nation state. The Saudi exploration in the late 1970s and

ExxonMobil, Shell, and developed Arabian Oil Company or Saudi was one of the first companies to

the know-how as an independent Aramco was founded in 1933 as engage in sub-salt and deepwater

operator. The company though California Arabian Standard Oil offshore exploration. These sub-

wholly owned by the Government Company and renamed Saudi salt plays are economically less

of Malaysia, operates like a pri- Aramco in 1988. Today, Saudi attractive because they are techni-

vate sector entity. Being an NOC, Aramco handles the largest crude cally challenging and develop-

it is empowered with sole owner- oil reserves in the world and is one ment costs are high. Over time,

ship and rights of oil and gas ex- of the most technically advanced Petrobras has developed tech-

ploration and production in companies in the world. The King nologies that allow the company

Malaysia. Thus, in the upstream has absolute authority over en- to tap into these reserves and thus

sector, all foreign and private ergy policy and there are no for- is one among the few companies

companies have to work with mal means set up to either modify that successfully developed sub-

PETRONAS. In the downstream or appeal against that policy. It is salt plays. Petrobras has a strong

sector however, PETRONAS com- the King who ultimately makes corporate governance structure. It

petes without favor from the gov- major decisions and the NOC is accountable not only to its own

ernment. There is no energy has to implement them. However, employees, but also to the Brazil-

minister to monitor the energy is- it is very rare that either the King ian populace. In spite of being

sues and instead it is the Prime or the Government would inter- an NOC, the intervention by the

Minister’s Economic Planning fere in the operation of the NOC. government is minimal. The gov-

Unit, and Implementation and Co- This is a big factor for a company ernment firmly believes that by

ordination Unit that are responsi- that has such major implications doing so the NOC can be more

ble for energy policies. This has in the international market and a efficient that in turn would yield

simplified the decision-making major political profile that politi- the country more profits and ben-

structure of PETRONAS. As Ma- cal interference in the NOC’s efits. Prior to the passing of the Oil

laysia faces declining indigenous business processes is relatively Law in 1997, Petrobras directors

crude oil, condensate, and natural infrequent. Saudi Aramco’s busi- were appointed by the President

gas production, and the reserves ness strategy matches that of a of Brazil. With the passing of the

have also declined, one route that private firm of a similar size. Law came a change in governance

PETRONAS has adopted is to in- Saudi Aramco is encouraged to and that brought in responsibil-

crease its international upstream buy and develop assets overseas ity, profitability, and a marked

activities. PETRONAS currently and it has the autonomy to choose increase in efficiency. Petrobras’

has assets worldwide in excess of whether it should enter into joint top executives and directors are

US$75 billion and is comparable ventures or take up sole propri- known to have sound technical

to many IOCs in terms of its in- etorship or perhaps just enter expertise which places them on

vestments. Its revenue from inter- into supply arrangements. par with the best energy compa-

national operations accounts for nies in the world (private or NOC).

more than 40% of its total revenue. Petrobras For Q1 2012, market capitalization

Petroleo Brasileiro S.A. or of Petrobras was estimated at

Saudi Aramco Petrobras is the state oil company US$120 billion and the company

Saudi Arabia is highly depend- of Brazil and was launched in 1953. ranked 23 among the Fortune

ent on oil income. Saudi Aramco The federal government owns Global 500 companies for 2012.

operates the country’s oil and gas 32% of the NOC, 40% is private PETRONAS, Petrobras, and

reserves and pays royalties and ownership, and the remainder by Saudi Aramco are good examples

taxes on the income earned. It is Brazil’s National Bank of Social of NOCs where the respective

allowed to retain the remainder of and Economic Development, the country is dealing with issues simi-

its income for future investments. Social Labor Fund, and other mi- lar to those faced by India—a

The country has the largest oil re- nority shareholders. When it young and growing population,

serves in the world and it was the comes to voting though, the fed- issues around corruption, regional

HYDROCARBON ASIA, JULY-SEPT 2013 31disparities, and promoting in- nical knowhow, but also have the China National Petroleum Cor-

dustrialization. While Saudi Ara- organizational capacity to match poration (CNPC)/PetroChina,

bia and Malaysia benefited by it with world-class operators. China Petrochemical Corpora-

being net exporters, Brazil was Though their main priority is to tion (Sinopec), and China Na-

significantly short. Fossil fuel secure the energy requirements tional Offshore Oil Corporation

subsidies were introduced in their of their respective nations, they (CNOOC)—exerts great influ-

countries to achieve social goals saw the need to also focus on ence on the oil and gas industry.

and these NOCs have had to assets overseas in an increasingly Chinese NOCs dominate the en-

shoulder the responsibility. Gov- competitive and challenging land- tire industry chain ranging from

ernments have empowered these scape. These companies have upstream exploration, develop-

NOCs so that they have room to worked together with the IOCs ment, and production to down-

expand and make rapid deci- to develop their own expertise stream refining, and marketing.

sions. Considering the regula- and their biggest advantage is The country is still a long way

tory and business environments that they have had the support away from achieving full liberali-

under which these NOCs oper- of their government and au- zation of its oil and gas industry

ate, they seem to do an excellent tonomy to make decisions. and markets, but has managed to

job in being efficient. Their focus Key attributes of these NOCs make more progress than India.

is on resource monetization; im- that have contributed towards China began investing in over-

prove revenue generation from their success are summarized in seas upstream oil and gas areas in

existing inputs whilst also hav- Table 1. the 1990s and intensified its efforts

in the latter part of the decade.

Since 2000, Chinese state oil com-

panies have made a bigger push to

expand overseas, which is favored

and encouraged by the Chinese

government. The Chinese state oil

companies have thus been taking

advantage of the central govern-

ment’s growing concern over po-

tential disruptions to their energy

supplies to realize their desires of

having larger business operations

around the world. “Going out”

has become part of the overall in-

vestment strategy for every state

oil company in China. All the ma-

jor Chinese oil and gas companies

have become very aggressive in

making direct acquisitions after

the global financial crisis in 2008.

In addition to gaining overseas

assets via corporate acquisition

and bid rounds, China has taken

advantage of the financial crisis’

limited and expensive commer-

Table 1 cial credit by offering tens of

ing to adhere to the internal oil Country Models billions in loans to several oil

and gas allocation and pricing and gas producing countries.

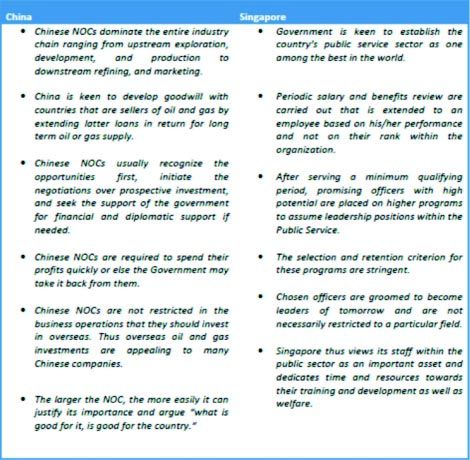

policies. These NOCs understand China – Quick turnaround with Venezuela, Kazakhstan, Brazil,

that in order to be competitive decision making as NOCs drive Turkmenistan, Bolivia, Ecuador,

with their IOC counterparts such the overseas investments and Ghana are countries that

as ExxonMobil, Shell, or Chevron, Similar to India, China through China has signed loan agree-

they must not only have the tech- its state-owned oil companies— ments with in exchange for long-

Country

Focus 32 HYDROCARBON ASIA, JULY-SEPT 2013 Visit our website at: http://www.safan.comterm oil or gas supply. By provid- three NOCs (CNPC/PetroChina, that factor in changes in eco-

ing these countries with the much Sinopec, and CNOOC) and other nomic conditions

needed capital, China is keen to players (Sinochem and a few • Individual’s annual increment

build goodwill with these nations. others) justify their existence in is adjusted based on his/her

Although high profile oil diplo- many ways, including maintain- potential and performance

macy has helped Chinese NOCs ing size through continuous ex- assessment

to clinch deals, the Chinese NOCs pansion. Simply put, the larger • The public service sector is

usually recognize the opportuni- the company, the more easily it moving away from a senior-

ties first, initiate the negotiations can justify its importance and ar- ity-based system of fixed an-

over prospective investment, and gue “what is good for it, is good nual increment

seek the support of the govern- for the country.” In the quest to • Personnel are posted across

ment for financial and diplomatic outdo the others, the Chinese various jobs within a par-

support if needed. The Chinese NOCs may not make their invest- ticular Ministry or via

government allows these NOCs ments entirely based on commer- secundments to other Minis-

to keep their profits as long as cial reasons. China’s crude oil tries, Statutory Boards, or ex-

the companies are investing production based on equity in ternal organizations. This is to

them regularly. The net profits overseas assets is estimated at 1.7 facilitate wider exposure and

of these NOCs (US$56 billion in mmb/d for 2012 and forecast to career development by under-

2011) are comparable to that of increase to 3.8 mmb/d by 2020. taking different assignments.

the international majors. This is After serving a minimum quali-

despite Chinese NOCs bearing Singapore – A knowledge based fying period, promising officers

the responsibility to absorb the economy that is globally-oriented with high potential can be placed

subsidy burden of government shaped by an interventionist and on one of the programs to assume

set domestic prices. active government leadership positions within the

If the NOCs do not spend their Singapore’s public officials are Public Service:

profits quick enough, it is possible entrusted to manage multimillion • The High Potential Program

that the government may claw dollar projects and known to be (HiPo) – Opportunities are

back those earnings. Hence, given extremely committed to the task at provided for officers to par-

the huge amount of cash they hand. The country is known to be ticipate in training exercises

earned every year and the ur- clean of corrupt practices and is and forums on leadership and

gency to spend it, the NOCs ag- known internationally for its tough policy formulation. Personnel

gressively expand to overseas stance on corruption. The country are encouraged to enhance

markets and they also demand a prides itself in declaring that in- their leadership skills and

lower rate of return (than the IOCs) corruptibility is ingrained in the nurture a whole-of-govern-

for their investments. Further- psyche of its public service sector. ment perspective.

more, compared to the domestic This is primarily because the coun- • The Management Associates

energy business, there is no pre- try adheres to a performance- Program (MAP) – Personnel

scribed limit to the kinds of busi- based reward system for its are exposed to fundamentals

ness operations the NOCs or the officials in the public sector. Sala- of public governance and im-

Chinese private oil companies ries and benefits offered are com- parted with skills required for

like Yanchang Oil or Brightoil can parable with an employee from public administration. These

invest in overseas. Thus, with both the private sector with similar ca- candidates are rotated within

the freedom to maneuver and op- pabilities and skill sets. The Gov- various Ministries of the Gov-

portunity to grow bigger, oil and ernment is keen to establish the ernment that gives them ex-

gas overseas investments are ap- country’s public service sector as posure to the workings of

pealing to many Chinese compa- one among the best in the world. various sectors during their

nies. It is also usually easier to get To ensure that it is able to attract training and development.

the central government to approve and retain the right share of na- The selection and retention

overseas investment plans than tional talent and as a means to criterion for these programs are

it is for new domestic proposals. motivate good performance: stringent. Officers chosen are

The internal competition among • Periodic salary and benefit/ groomed to become leaders of the

the Chinese NOCs also shapes bonus reviews are carried future who are trained and

their overseas investments. The out with timely adjustments branded capable of heading other

HYDROCARBON ASIA, JULY-SEPT 2013 33disciplines and not necessarily ment interference can result in Manpower approach should

restricted to a particular field. stalling of reforms and policy be based on professionalism and

Indian NOCs need to look at its making within the NOC, disrupt domain expertise. India can look

staff as its most precious asset. corporate governance, and result at the Singapore model where of-

This is essential in order to create in concentration of power in the ficials in the public sector are re-

a unique identity for the com- hands of a few that results in warded well and are known to

pany and to steer its growth. The favoritism, and eventually poor function efficiently. There should

Indian Government must pro- progression of the NOC. be zero tolerance towards corrup-

vide incentives to its NOCs to Effective governance of the tion and cronyism. A smoother

develop a talented and motivated energy industry is crucial. Energy transition from the older genera-

workforce who not only remain policy is a fundamental compo- tion to the younger generation

loyal to the task at hand, but also nent of the Government’s social should be looked into. One way

to the establishment. and economic agenda. It should of doing this is by either holding

Key attributes of these coun- be “above politics.” Formulation on to the existing workforce yet

tries that have contributed to- and management of the energy to retire or by finding a way of

wards the development of their policy should be taken from the bringing back those who have

PSUs are summarized in Table 2. authority of the oil ministry. En- retired into some form of service.

Rather than raising the manda-

tory age of retirement, it is better

to give the NOCs the discretion

to retain and utilize older employ-

ees provided the employee is able

to function effectively. Even be-

yond that, NOCs should look to

retain that person in an advisory

role or a ‘chief mentor’ role. Pres-

ently when the PESB shortlists a

total of 15 candidates for a role

within the NOC, it is based on

the guidelines in Table 3.

There should be more room in

the above guidelines for the NOCs

to be able to absorb external candi-

dates and not just candidates from

other NOCs or PSUs.

For the upstream sector, there

must be an acknowledgement

that exploration involves high

risk of failure. To attract healthy

competition and involvement of

world class operations and op-

Table 2

erators, rewards must reflect this.

The Time Has Come For the ergy policy should reside with a There is no doubt that low

Indian Government to Take group comprising of the Prime prices received on domestic sales

The Bull By The Horns and Minister, Treasurer and Finance of gas impacts the performance of

Face the Consequences Minister, or some similar author- the NOC that also impacts their

Indian NOCs have their gov- ity grouping. The Vijay Kelkar and motivation to invest further. In

ernment’s backing and this is Rangarajan Committees are steps India’s case, the NOCs and other

their greatest strength. However, in the right direction, but it needs investors have decided to adopt a

they need to be empowered. The to be empowered more to take ‘wait and watch’ approach to see

Chinese model of empowering quick and bold decisions. This will how the Government deals with

NOCs is something that India provide greater assurance to the RIL. By end-2013, the Government

can consider. Too much Govern- investors in India’s energy sector. will review the KG-D6 gas price

Country

Focus 34 HYDROCARBON ASIA, JULY-SEPT 2013 Visit our website at: http://www.safan.comInvestments have also been forth-

coming in India’s natural gas sec-

tor and that is primarily due to

changes in the natural gas mar-

ket—formation of Petroleum and

Natural Gas Regulatory Board

(PNGRB), expansion of LNG ter-

minals, construction of new ter-

minals, granting licenses for new

city gas networks, regulatory

changes, and authorization of de-

velopment of new trunk pipelines.

India’s Foreign Direct Investment

(FDI) Policy allows for investment

of up to 100% in infrastructure

related to natural gas, marketing

of natural gas, natural gas/pipe-

lines, and LNG regasification in-

frastructure. Thus the system is

set up to grow and now needs to

draw in investors who will stay.

To do this, Government regula-

tion must be designed to promote

“risk taking, world-class, socially

responsible” organizations.

Table 3 As stated at the beginning, the

and realistically this will serve as say five years, which gives purpose of this paper is to lay out

a benchmark for natural gas sensitive sectors such as the power directional concepts for India’s

produced from domestic assets. and fertilizer companies and the energy sector to propel itself in the

A market-based pricing at arm’s end-consumers enough time to modern world. Business as usual

length needs to be arrived at adjust. It should be noted though is not an option for India—the sec-

which will not only draw in inves- that an end to a controlled-pricing ond most populous country in the

tors, but will also be beneficial to regime should be visible to all world—which has set itself a

the Government and Indian soci- stakeholders. This will also pro- growth target of 9% per annum

ety. Existing gas production is vide the much needed impetus and where the average age is well

likely to remain flat or decline with for raising production. Industry below 30 years. India must recog-

support from marginal fields of sources suggest that 10 tcf of gas nize that the world will not change

existing producers. New fields has been discovered but currently for India, but it is the other way

with over 10 tcf of discovered re- is undeveloped due to unattrac- around. Thus, reforms are critical

sources are waiting to be commis- tive financial terms. Exploration in the ailing energy sector. A fail-

sioned and can add to the existing would almost certainly identify ure to recognize the same and re-

production. However, the timeline more, but the current financial fusal to make changes will result

of these new additions will de- terms provide a disincentive. in stalling of this massive growth

pend on the abovementioned price India suffers from infrastruc- engine of the 21st century. HA

review and regulatory changes ture constraints, confusing multi-

introduced by the Government ple pricing of domestic gas and

to incentivize gas producers. imported gas, and often lacks This publication thanks

However, the onus will be on policy coordination amongst Fereidun Fesharaki and

the Government to ensure that a various government sectors. Praveen Kumar of FACTS

transition to a market-based pric- However, it is a huge market in Global Energy, headquartered

ing mechanism is smooth. A mar- the making. The city gas, indus- in Singapore for providing

ket-linked pricing should be trial, fertilizer, and power sectors this article.

arrived at over a period of time, are all poised for rapid growth.

HYDROCARBON ASIA, JULY-SEPT 2013 35You can also read