Integrated Shield Plan riders: What you need to know - MoneySense

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

THE STRAITS TIMES

Premium

Integrated Shield Plan riders: What you

need to know

Income's Mr Andrew Yeo says that from April 1 next year, only riders with co-payment features can be bought from the

insurer.

PUBLISHED APR 15, 2018, 5:00 AM SGT

Ministry's move to incorporate a co-payment element should encourage rethink of

needs

Lorna Tan Invest Editor/Senior Correspondent (mailto:lornatan@sph.com.sg)

he soaring costs of healthcare are raising concerns among many of us, so the moves by the Health Ministry last month to try reining them in have been welcomed. The key measure is that sales of insurance riders that fully pay your portion of the hospital bill - this typically means the bill is covered from the first dollar - will cease from April 1 next year. That's when a new rider that will include a patient's co-payment for a hospital bill becomes available. Getting your bill fully covered is obviously a benefit but financial experts say the practice can end up with some patients being overcompensated while others may be given excessive treatment merely to generate fees, or are overcharged by some healthcare providers. The end result is escalating healthcare costs and higher insurance premiums for all. So the ministry's move to incorporate a co-payment element in a rider should encourage consumers to play an active role in choosing their medical providers and treatments. The Life Insurance Association says it will also help insurers manage claims and reduce the need for significant premium hikes, which will allow private hospital Integrated Shield Plans (IPs) and riders to remain sustainable options. Mr Daniel Lum, director of product and marketing at Aviva Singapore, says: "The escalating cost of healthcare is a challenge that requires multi-pronged efforts from various parties to overcome.

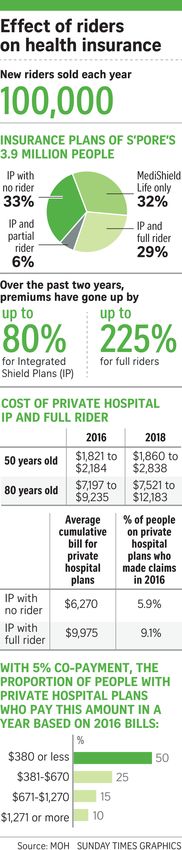

"The (ministry's) move encourages consumers to practise healthier lifestyle options and make more conscientious decisions when seeking treatment, as well as prompting healthcare providers to recommend medically-appropriate and cost-effective treatments." The changes will be introduced gradually. If you buy a full rider between March 8 this year and March 31 next year, you get some time before you switch to the new co-pay rider. You will move to the new IP rider from April 2021, which will have a co-payment element of at least 5 per cent of the hospital bill. The total amount a year that you have to pay for hospitalisation will be capped to ensure affordability. But the cap is subject to you being treated by doctors on the insurer's panel or having the insurer's pre- authorisation if seeking treatment from doctors not on the panel. If these conditions are not met, you will have to pay at least 5 per cent of your bill, with no limit on how much you need to pay each year. The new move does not affect the 1.1 million individuals who bought full riders before March 8 this year. The Sunday Times highlights what you need to know about the new IP riders. NEW RIDERS FROM APRIL 1, 2019 As part of the Health Ministry initiative, the six IP insurers - AIA, Aviva, Axa, Great Eastern (GE), NTUC Income and Prudential - are reviewing their riders. They will launch new riders with a co-payment feature of at least 5 per cent of the hospital bill by next April 1. The amount will be capped at a minimum of $3,000 a year if the policyholder seeks treatment from the insurer's preferred healthcare providers. Those who buy full riders from March 8 this year to March 31 next year will transition to the new riders with the co-payment feature upon their renewal from April 1, 2021. Mr Neil Frith, managing director, life at Axa Insurance, says premiums for the new co-pay riders are expected to be lower than for the existing full riders. REASONS FOR HEALTH MINISTRY'S MOVE Statistics show that people with IP riders have bills that are on average 60 per cent higher than those who have IPs without riders. The reasons include over-charging by doctors - a practice that increases premiums for all of us. Total IP and rider claims hit $1.05 billion in 2016, up from $858 million in 2015, and all six insurers suffered underwriting losses in 2016.

The ministry fears that if this continues, healthcare costs will rise for everyone, including those who are only

on basic MediShield Life.

IPs incorporate the basic MediShield Life, so higher IP bills also mean higher payouts from MediShield Life,

pushing up its premiums.

New rules for Integrated Shield Plan …

Posted by The Straits Times

178,718 Views

Unsure about the new rules for Integrated Shield Plan riders? Here's everything you

need to know. http://str.sg/oS2s

305 215 2.5K

EXISTING IP RIDERS

Besides full riders, IP insurers also offer partial riders where the policyholder pays a small part of the bill.

As part of its review, Mr Andrew Yeo, Income's general manager for life and health insurance, says that from

April 1 next year, only riders with co-payment features can be bought from Income while its Plus and Assist

riders will be withdrawn. This will not affect customers who bought these riders before March 8.Income's Plus rider is a full rider while customers with its Assist rider do not need to pay deductible or co-

insurance. They pay only 10 per cent of the claimable amount, subject to a maximum co-payment each policy

year.

If they stay in a ward that is lower than their entitled ward, they will get a daily hospital cash benefit.

INDIVIDUALS WHO OWN FULL RIDERS BEFORE MARCH 8

If you already owned a full rider before March 8, the new rules do not apply. You can continue to enjoy first

dollar coverage for your hospital bills.

Related Story

askST: What should I know about the new riders

of MediShield-linked Integrated Shield Plans?

Related Story

What caused healthcare costs to spiral? And will

MOH's move on riders arrest the trend?

Related Story

Managing your healthcare costs well

However, insurers are allowed to change their products and features. For instance, if they had bad claims

experiences with customers with full riders, they may decide to change their product offerings.

You would likely be given the option to switch to the new rider with the co-payment feature - that will have

lower premiums - when it is rolled out by next April.

Prudential Singapore's head of medical Agnes Choy says it will not make changes for customers who bought

its full rider - PRUExtra Premier - before March 8. This product offers first dollar cover for private and public

hospitals.

She notes that the plan comes with a claims-based pricing feature that encourages more prudent use of

medical services.

Prudential customers on claims-based pricing enjoy lower premiums when they claim less, and a 20 per cent

saving on their premiums when they do not make a claim during the review period.

SELECTING A RIDER IP

riders help to reduce out-of-pocket expenses, so if you want a smaller cash outlay when hospitalised you

should consider buying one. However, affordability is a key factor to consider, says Ms Choy."As riders cannot be paid for using Medisave and have to be settled in cash, one needs to ensure that one can afford to pay the premiums in the long term," she adds. Another factor is the kind of hospitals for your treatment. Riders for public hospitals will be more affordable than those for private hospitals, says Ms Choy. Rider premiums have soared by up to 225 per cent over the past two years while IPs have risen by up to 80 per cent or so, according to the Health Ministry. Other factors to consider include your age and health. If you already have a full rider and would like to consider switching to the new co-pay rider, see how much premium savings you would enjoy a year and consider the number of years you expect to require few major healthcare treatments. Based on 2016 bills, 5 per cent co-payments came to $670 or less for 75 per cent of the people who made claims that year. SELECTING AN IP Individuals should take this chance to review their insurance portfolio, including assessing if their existing insurance coverage is in line with their current needs, as it is important to understand the coverage under your current plan before making any adjustments, says Mr Lee Swee Kiang, GE's head of group product management.

Any decision to buy, replace or terminate a policy should only be taken after careful consideration. Ms Choy warns that if you surrender your policy or switch insurance providers, you will no longer be able to enjoy first-dollar coverage for life from any new insurer. While first-dollar coverage plans are available up to March 31 next year, customers who buy during this period must transition to alternative riders with features that meet the new guidelines from April 1, 2021. They may also have to go through a health assessment and may not be covered for existing medical condition, Ms Choy adds. So it is recommended that you speak with a professional financial adviser to fully understand the impact of any decision, says Aviva's Mr Lum. He notes: "Having an IP is still important as it gives you the option of staying in private hospitals or a higher class ward of public hospitals, higher annual claim limits, choice of doctor, shorter waiting time and features such as coverage for emergency hospitalisation outside of Singapore - which could make a significant difference in one's recovery journey." Ms Choy says: "If affordability is a concern for customers, they can consider downgrading to a more economical plan that meets their needs. For instance, they could consider switching to a public hospital plan, or to a co-pay plan." PREFERRED PANEL OF DOCTORS All six IP insurers have a preferred panel of doctors except for Income and Prudential, which will have them in place by next April. Having a panel is the way to go as doctors' fees vary widely, even for the same treatment. AIA and some other insurers treat all public-sector doctors as approved medics on their panels. PRE-TREATMENT APPROVAL This varies with insurers. Some require customers to call a hot line or complete a form to seek approval before treatment. These approvals offer peace of mind that medical expenses will be paid for. In some cases, a letter of guarantee is provided by the insurer on approval at the hospital. GE launched Health Connect in March last year. It's a call-in service that lets customers access a pre-selected panel of doctors. It allows for appointment booking, pre-authorisation of hospitalisation expenses and direct claim settlement. This is how the proposed change in rider coverage might work Effect of riders on health insurance

You can also read