Intu Shopping Centres: Development of a Public EV Charge Point Network - LEVEL Conference Pride Park Stadium, Derby, March 2018 - LEVEL Network

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

intu Shopping Centres: Development of a Public EV Charge Point Network LEVEL Conference Pride Park Stadium, Derby, March 2018 Dr Gareth Evans, Sustainable Travel Manager (North) Intu Properties plc

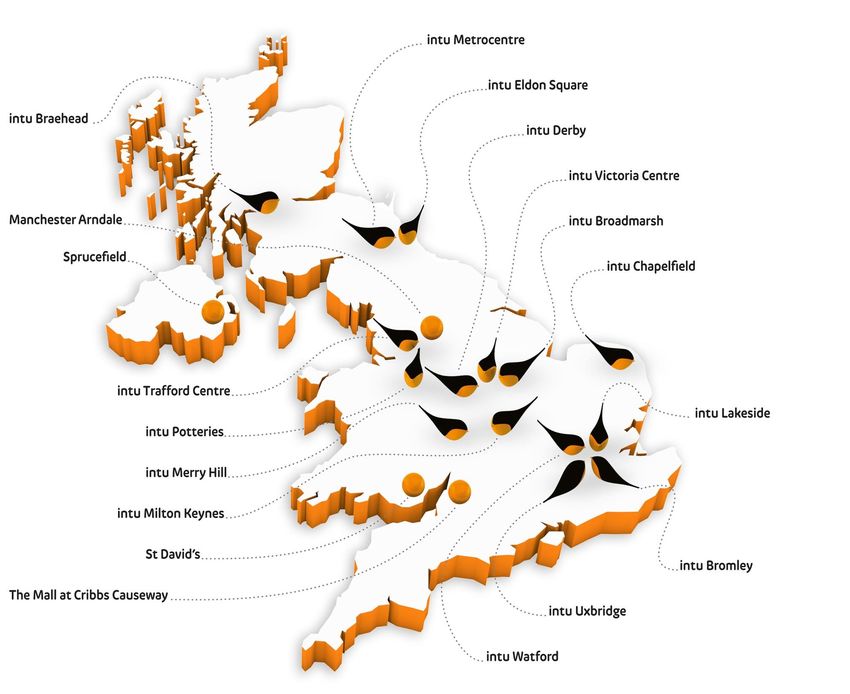

Who are intu? • British Real Estate Investment Trust (REIT) • Own or part-own 17 shopping centres across the UK (£9.8bn asset value) –Attract c.400m customer visits/year –Easy access for 2/3 of UK pop. •Ownership of three centres in Spain plus future development sites •Investing £600m+ in centre developments to 2020/21 • http://www.intugroup.co.uk

Super Regionals

Just off SRN

Large surface CPs +

some MSCPs

Free parking

Customer dwell ~2hr

Specific trip/visit

City Centres

Mostly MSCPs

40B (HO)

Paid-for parking

Customer dwell 1-2hr

Not necessarily

Page 3

visiting the centre

In the Beginning… • 2008: intu were one of the first shopping centre companies to introduce EV charging points across the entire portfolio… total cost = £120k! • First 50kW rapid chargers installed at UK shopping centres –intu Metrocentre (2011), NE PiP funding / ONE RDA –intu Braehead (2013), Transport Scotland grant funding

Continued Growth in EV Charging intu Braehead – YoY Growth but Starting to Plateau? Page 5

Current Demand for EV Charging

• On CYC (CPS/GMEV) network

–iBH – 1 rapid + 4 Type 2s: 2016: 3976; 2017: 4931; Growth = 24%

–iMC – 6 Type 2s: 2016: 4377; 2017: 4582; Growth = 5%

–iTC – 12 Type 2s: 2016: 6333; 2017: 5973; Growth = -6%

(NB. suspected comms. issues on two points for at least 1 qtr)

•On POLAR network

–iPO – 4 Type 2s. 2017: 185; 2018 (end Feb): 64 = 350-400 by end ‘18

–iLK – 2 rapids + 4 Type 2s: 676 (from Sept ‘17 to end Feb ‘18)

• On Plugged-in-Midlands legacy network(s)

–iDY – 6 Type 2s. 2016: 1193; 2017 (annual.): 1330; Growth: c.11%

Regional Variations in EVs and CP Availability

Shopping Centres & the EV Customer

• AA Populus Panel (Nov 2017) Q: More likely to buy an EV if charging

points existed at specific locations

–62% said supermarkets, shopping malls, leisure centres and car

parks [7kW/22kW Type2s better suited]

• Ensure EV charging facilities continue to be provided at our centres

•Supporting further growth in EV market through new developmentsRole of Shopping Centres in the EV Charging Mix

•Not all EV visitors to a centre will require a charge - destination charging is

a ‘nice to have’ where charging-for-charging is not unreasonable (TRL)

•Breakdown of demand across the EV charge point mix

–MyElecAve – Home: 66%; Workplace: 11%; Destination: 18%

–CM/POLAR – Home: c.70%; Workplace: c.10%; Destination: c.20%

–NewMotion – Home: 63%; Workplace: 10%, Destination: 27%

•More EVs on the road with larger batteries will increase charging times and

result in queuing on public infrastructure (TRL)

–Drivers forced to go elsewhere, leading to reduced utility of direct

investment in EV points

–Negative press and comments about lack of infrastructures, increase in

complaints to centres

Page 9Role of Shopping Centres in the EV Charging Mix

•Build it and they will come (TRL)

–EV drivers starting to accept charge points cannot go everywhere

–As long as there are enough points which work, in a safe and

convenient enough location, they don’t mind where these are placed

•Should we be looking to provide additional rapid chargers?

–Helps promote turnover of bays when Type 2s are in use

–Major financial outlay and power requirements versus extra Type 2s

–What is a suitable ratio of rapid:fast chargers?

–Automated & EV Bill - mandate for Motorway Services, could this

eventually be applicable to our super-regional centres?

–National Grid report - 50no super-rapid clusters across E&W will suffice

Page 10intu EV Steering Group • How many EV points are required? –Various future forecasts for EV growth to 2020/2025/2030 –Centre-by-centre reports based on 1hr drive time –Will there be a tipping point when all bays are EV-enabled? • Where should (can) they go? –‘Prominent but not Premium’ –Subject to available electrical capacity within existing centre supply –Competing demands from other services/facilities –Allocation and management of EV bays (ICEing, EVs over-staying) –Installation within MSCP (less civils) vs surface (more civils) –Potential H&S issues w.r.t. fire hazards in MSCPs? • Who pays for them?

Working in Partnership • Ensure consistency with wider regional strategies and networks –Simplicity for the customer (and our staff) is key • Local Authorities & Funding Programmes –NE Combined Authority – 2no rapid chargers at iMC –D2N2 GUL programme – 20no Type 2 chargers at iVC + iDY options –GMEV – exploring additional provision for iTC • Private/Industry Providers –Chargemaster POLAR network –350kW super-rapid charging station proposals • Concession-based Models –Elmtronics

EV – Helping Raise Awareness Page 13

In Conclusion - Electric Vehicles & intu • Strong recognition in the company of the ever-growing EV sector • Our centres are very suitable locations for EV charging points • Rapid versus standard/fast charging – meeting our commercial needs and those of the wider EV sector •Maintaining the existing EV infrastructure • Funding opportunities for further EV infrastructure • Partnership working with LAs, EV specialists – who is steering the future direction of the market?

Thank you for listening

You can also read