Investor Presentation - NYSE:CRK - Comstock Resources, Inc.

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

NYSE:CRK

Investor Presentation

MAY 2021

Disclaimer

This presentation includes “forward-looking statements” within the meaning of Section 27A of the Securities Act of 1933 and Section 21E of

the Securities Exchange Act of 1934. Forward-looking statements give our current expectations or forecasts of future events. These

statements include estimates of future natural gas and oil reserves, expected natural gas and oil production and future expenses,

assumptions regarding future natural gas and oil prices, budgeted capital expenditures and other anticipated cash outflows, as well as

statements concerning anticipated cash flow and liquidity, business strategy and other plans and objectives for future operations.

Our production forecasts are dependent upon many assumptions, including estimates of production decline rates from existing wells and the

outcome of future drilling activity.

Important factors that could cause actual results to differ materially from those in the forward-looking statements herein include the timing

and extent of changes in market prices for oil and gas, operating risks, liquidity risks, including risks relating to our debt, political and

regulatory developments and legislation, and other risk factors, including the impact of the current COVID-19 pandemic, and known

trends and uncertainties as described in our Annual Report on Form 10-K for fiscal year 2020 and as updated and supplemented in our

Quarterly Reports on Form 10-Q, in each case as filed with the Securities and Exchange Commission. Should one or more of these risks or

uncertainties occur, or should underlying assumptions prove incorrect, our actual results and plans could differ materially from those

expressed in the forward-looking statements.

Reserve engineering is a process of estimating underground accumulations of hydrocarbons that cannot be measured in an exact way. The

accuracy of any reserve estimate depends on the quality of available data, the interpretation of such data and price and cost assumptions

made by reserve engineers. In addition, the results of drilling, testing and production activities may justify revisions of estimates that

were made previously. If significant, such revisions could impact Comstock’s strategy and change the schedule of any further production

and development drilling. Accordingly, reserve estimates may differ significantly from the quantities of oil and natural gas that are

ultimately recovered. These quantities do not necessarily constitute or represent reserves as defined by the Securities and Exchange

Commission and are not intended to be representative of all anticipated future well results.

Comstock owns or has rights to various trademarks, service marks and trade names that we use in connection with the operation of our

business. This presentation also contains trademarks, service marks and trade names of third parties, which are the property of their

respective owners. The use or display of third parties’ trademarks, service marks, trade names or products in this presentation is not

intended to, and does not imply, a relationship with, an endorsement or sponsorship by or of Comstock. Solely for convenience, the

trademarks, service marks and trade names referred to in this presentation may appear without the ®. TM or SM symbols, but such

references are not intended to indicate, in any way, that Comstock will not assert, to the fullest extend under applicable law, their rights

or the right of the applicable licensor to these trademarks, service marks and trade names.

2

Why Invest in Comstock?

Best-in-class capital efficiency creates industry-leading margins and return on capital employed

Conservative operating plan and best-in-class cost structure drives unparalleled free cash flow

for deleveraging

Basin leader in the Haynesville, a premier natural gas basin with geographical proximity to Gulf

Coast and attractive price differentials

> 1,900 high-return net drilling locations in the Haynesville and Bossier to support successful

program

Committed to environmental stewardship and a responsible energy future, with leadership on

low emissions in a prolific natural gas basin

Strategic relationship with successful Dallas businessman Jerry Jones, the company's largest

shareholder, whose investment to date in Comstock totals $1.1 billion

3

Leading Haynesville Operator

Comstock Resources overview Haynesville / Bossier shale

Haynesville Shale

• Significant Scale in the Haynesville Harrison

Bossier

• 323,000 Haynesville / Bossier net acres

(1)

Caddo

Bienville

• Robust inventory of de-risked, high-

return drilling locations

• > 1,900 net drilling locations Robertson

De Soto

Red

River

Panola

• ~73% of locations >5,000 ft. laterals

• Industry leading margins with

substantial free cash flow generation

Nacogdoches Shelby

Sabine Bossier

Shale

• Low-cost, flexible gas marketing

options San

• Limited basis risk due to proximity and Augustine

contracts tied to Henry Hub Company statistics

• Low gathering, treating and Net Acres

323,000(1) Q1 21 Production 1.3 Bcfe/d

transportation cost (Haynesville / Bossier)

Net Undrilled Locations 1,930 Proved Reserves 5.8 Tcfe(2)

• No unmet minimum volume

commitments % Held-by-Production 93% % Gas 99%

% Operated 91% PDP PV-10 $2.2 bn(2)

% Working Interest 82% Total PV-10 $4.4 bn(2)

(1) As of December 31, 2020. (2) Based oil and gas prices of $50 WTI / $2.75 HH.

4

Recent Accomplishments and 2021 Outlook

• Successfully raised $1 billion of equity and debt throughout a volatile 2020

• $207 million common equity in May to redeem the Series A preferred, eliminated $21 million of

Prudently annual distributions

Managing the • Issued $800 million senior notes in 2020 to enhance liquidity and reduce reliance on bank facility

Balance Sheet • Refinanced $1,152 million of senior notes in March 2021 which saves $19.5 million in cash

interest payments per year and extends senior notes weighted average maturity from 4.9 years

to 6.7 years

Exceptional • Strong IP rates of 25 Mmcfe per day on average in 2020 and 2021

Drilling Results • Grew proved reserve base by 3% at a low, all-in finding cost of $0.66 per Mcfe in 2020

and Reserves • SEC Proved reserves grew to 5.6 Tcfe, replaced 159% of production

Growth • 1P PV-10 of $4.4 billion at flat $50 WTI / $2.75 HH

Consistently Low • Drilling and completion costs per lateral foot reduced by 17% since 2019

and Improving • Longer lateral wells averaged $1,010 per foot in 2021 Q1 versus $1,215 per foot in 2019

Costs

• Comstock’s focus continues to be capital discipline, producing free cash flow, and deleveraging

the balance sheet

Disciplined 2021 • Estimated production of 1.3 to 1.4 Bcfe per day

Plan and Outlook • Development capital expenditures of $510 to $550 million

• Expecting to generate substantial free cash flow in 2021 to pay down debt

5

Corporate Strategy Excels in Current Environment

Develop

Prudently grow free cash flow,

production and reserves

through development of high-

quality inventory

Protect Enhance

Manage commodity price

Enhance returns on capital

exposure through an active

through a focus on optimizing

hedging program to protect

full-cycle economics

our expected future cash flows

Finance Acquire

Evaluate and pursue strategic

Maintain disciplined financial acquisition opportunities to

strategy grow reserves, production,

and acreage position

6

Haynesville vs. Appalachia

Favorable differentials Lower midstream costs Superior full-cycle economics

2021 Q1 Differentials vs. Henry Hub 2021 Q1 Gathering & Transportation 2020 EBITDAX Margin / 3-Year F&D

($/mcfe) ($/mcfe)

Higher IRRs (1)

Faster payouts Ample in-basin demand

Basin Average Payback (Years)

IRR (%) Haynesville Appalachia

Basin Under-

Over-supplied

Demand supplied

Access to Open, More

Nearly Full ex

Premium Capacity in

MVP / ACP

Markets Process

Source: RSEG, Public filings. Appalachia includes AR, CNX, COG, EQT and RRC

(1) Based on RSEG type curves at $2.75 per Mcf.

7

Drilling Location Inventory

Extensive inventory of high return drilling locations

33 Years of inventory based on 2021 drilling program

As of March 31, 2021

Haynesville

Operated Non-Operated Total

(Gross) (Net) (Gross) (Net) (Gross) (Net)

up to 5,000 ft. 245 201 535 81 780 282

5,000 ft. to 8,000 ft. 372 280 206 40 578 320

> 8,000 ft. 518 372 228 35 746 407

1,135 853 969 156 2,104 1,009

Bossier

Operated Non-Operated Total

(Gross) (Net) (Gross) (Net) (Gross) (Net)

up to 5,000 ft. 238 190 371 53 609 243

5,000 ft. to 8,000 ft. 407 334 98 9 505 343

> 8,000 ft. 407 323 132 12 539 335

1,052 847 601 74 1,653 921

Total 2,187 1,700 1,570 230 3,757 1,930

8

Improving D&C Costs

17% decrease from 2019 to 2021 due to increased drilling efficiency and lower service costs

(Laterals > 8,000 ft.)

($ per Lateral Foot)

$1,506

$1,446

$1,215

$1,026 $1,010

$941

$1,021

$764

$569

$645

$565

$425 $451 $457

$365

2017 2018 2019 2020 2021 Q1

Completion Drilling

9

Drilling Results

Bossier

Completed 285 operated wells since 2014

(average lateral length of 7,800 ft.)

with average IP rate of 24 Mmcf/d Caddo

6

5

12 11

First Quarter 2021: LL Turned To IP 13 Bienville

Well Name (feet) Sales (Mmcf/d)

1 Beaubouef 15-10 #3 7,477 03/07/2021 30 Harrison 1 4

2 Beaubouef 15-10 #4 5,431 03/07/2021 26 2 3

3 Beaubouef 15-10 #1 5,310 03/08/2021 25

4 Beaubouef 15-10 #2 7,444 03/08/2021 29

5 Roberts BF #1 11,132 03/10/2021 21 Red

6 Roberts TTB #2 13,043 03/10/2021 32 River

7 Adams 21-28-33 #1 10,573 04/12/2021 23 De Soto

8 Adams 21-28-33 #2 10,072 04/12/2021 26

8 9

9 Curry 28-33 #1 9,733 04/14/2021 23 7 10

10 Curry 28-33 #2 9,544 04/14/2021 23

11 Davis 7-6 #1 5,997 04/14/2021 25

12 Davis 7-6 #2 5,398 04/14/2021 21

13 Davis 7-6 #3 4,568 04/14/2021 19

8,132 25

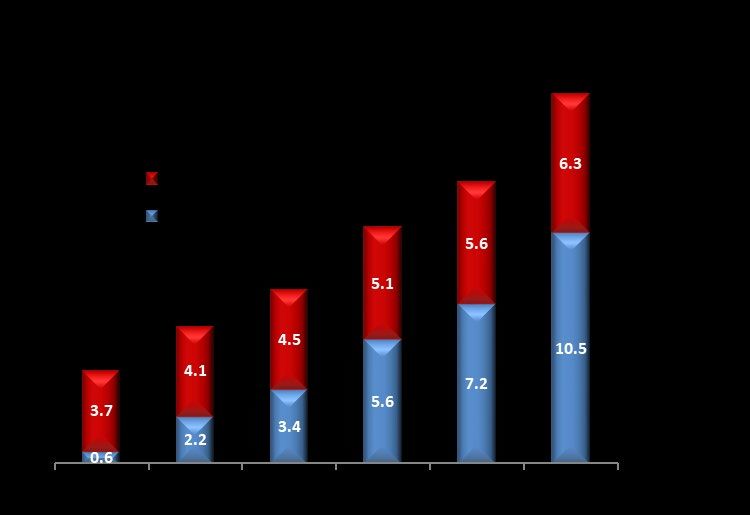

10Favorable Natural Gas Supply Demand Dynamics

• Long-term price support expected from

Natural Gas Storage (as of 5/7/21)

continued sector capital discipline,

increased power generation demand, long-

Favorable term industrial demand and continued

Supply & coal/nuclear retirements

Demand • Appalachian gas pipeline constraints limit

Fundamentals long-term growth prospects

• Natural gas storage levels are below average

as we enter summer demand season 378 Bcf 72 Bcf

below below

Last Year 5 Yr. Average

Natural Gas Exports

• LNG exports have reached record levels

Strong • Average of 10.5 Bcf/d for 2021 YTD,

Export with max flow rate of 11.6 Bcf/d

Markets • Mexican exports continue to grow

• 6.3 Bcf/d for 2021 YTD

11Gas Marketing Overview

Improving direct access to gulf coast demand centers Improving margins by…

• Having minimal firm transportation

agreements, at out-of-market rates

Carthage

Perryville • Entering into medium-term sales

agreements, which provide basis pricing

certainty at the Perryville hub

• Redirecting natural gas from Perryville

hub to gain direct access to high-growth

Gulf Coast demand (industrial, refining,

chemical and LNG)

• New lateral in service in Q2 which

allows up to 250 Mmcf/day to flow

from Logansport to Acadian

• Entered into agreement to be major

shipper on new Haynesville Acadian

Extension for 1 Bcf/day (expected to

Gillis be in service by 4Q in 2021)

• Expect regional basis to tighten as ~4 Bcf

HSC LNG & Industrial Henry Hub of new North-to-South pipelines are

Demand Centers

projected to come on-line through 2022*

*BTU Analytics’ Gas Basis Outlook

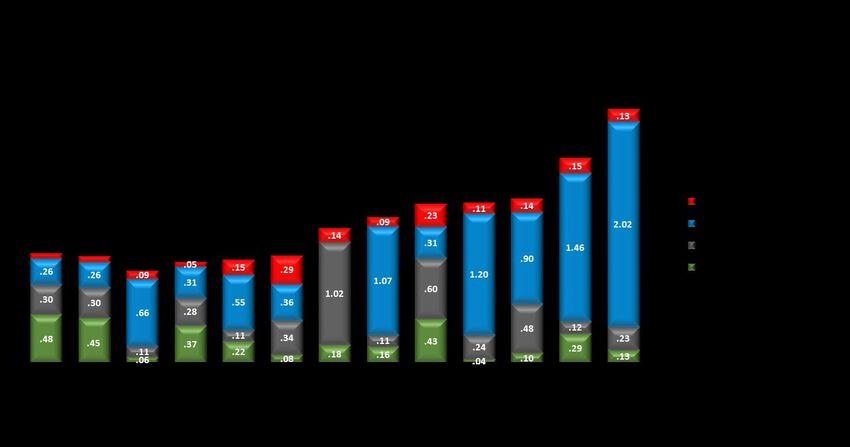

12Cost Structure Drives Best-in-Class EBITDAX Margin

$ / Mcfe

Best-in-class cost structure of gas producers

Leading margins compare favorably to both Permian and gas-weighted names

Unhedged EBITDAX(1)

Margin (%)

Oil Peers

Gas Peers

Source: Public filings. Based on Q1’21 reported actuals. Gas peers include: AR, CHK, CNX, COG, GDP, GPOR, EQT, RRC, SBOW, SWN and VEI (Pro Forma). OIL peers include: FANG, LPI and PXD.

(1) See non-GAAP reconciliation in appendix.

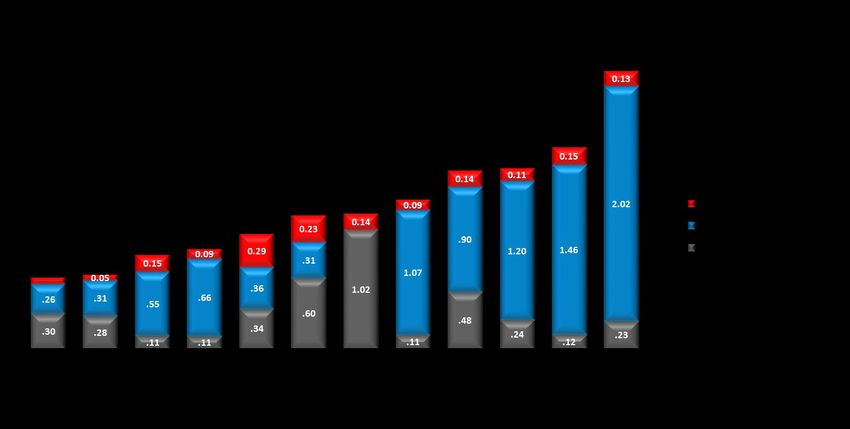

13Operating Cost Structure Offsets Legacy Interest Cost

Cost structure of gas producers including interest

$ / Mcfe

Source: Public filings. Based on Q1’21 reported actuals. Gas peers include: AR, CHK, CNX, COG, GDP, GPOR, EQT, RRC, SBOW, SWN and VEI (Pro Forma).

* Pro Forma for the March 4th Refinancing Transaction.

14Best-in-Class Margins Deliver Strong Returns

EBITDAX Margin (2020)

Comstock’s Margin Advantage

Operational Scale as Haynesville Basin’s

Largest Producer

U.S. E&P

Universe

Higher Realizations due to Favorable Gulf

Coast Market

Favorable Midstream Rates due to No Above Return on Capital Employed (2020)

Market Contracts

Low and Efficient Corporate Overhead

(Lowest of All E&P Companies)

U.S. E&P

Universe

Low Haynesville Lifting Costs

(No Treating/Compression)

Source: Public filings. Note: EBITDAX Margin reflects hedged margin. ROCE calculated as NOPAT / Average Capitalization.

15Oil & Natural Gas Reserves

(1)

Oil Gas Total

MBbls Bcf Bcfe

Proved Reserves as of 12/31/19(1) 16,747 5,342 5,442

Production (1,508) (451) (460)

2020 Additions 2 366 366

Price Revisions (2,858) (68) (86)

Performance Revisions (1,383) 375 367

Proved Reserves as of 12/31/20 (SEC)(1) 11,000 5,563 5,629

SEC PV 10 Value (million $) $1,991

8.2

PV 10 Value (million $) at $2.75/$50 $4,357

*Based on NYMEX prices of $2.75 per Mcf for natural gas and $50 per barrel for oil.

Reserves by Type PV-10 by Type Reserves by Commodity Reserves by Region

Total: Total:

Total: Total:

16

5.6 5.6

$2.0 Bn 5.6

Tcfe Tcfe

Tcfe

(1) Proved Reserves are based on SEC Pricing.

16Drilling Program

First Quarter 2021

Average

Lateral Gross WI Net

($ in millions) $ (feet) Wells Wells

2020 wells turned to sales $ 49.3 9,356 10 9.0

2020 wells completion In process 26.5 10,072 9 8.4

2021 wells drilled 61.1 7,351 21 19.0

2021 wells drilling 13.4 7,500 7 6.4

2021 non-operated and other 12.7

Total Development Costs $ 163.1

Exploratory Leasing $ 5.8

2021 Drilling Program Overview

Developmental Capital Expenditures $510 million to $550 million

Leasing Program $7 million to $10 million

Wells Drilled to Total Depth - Operated 67 Gross / 56.0 Net

Wells to Sales - Operated 55 Gross / 49.0 Net

Year-End Drilled Uncompleted Wells 31 Gross / 24.4 Net

Wells Drilling at Year-End 6 Gross / 5.7 Net

17Balance Sheet

Bank Credit Facility Capitalization

($ in millions) 3/31/2021

Cash and Cash Equivalents $77

Senior Secured Revolving Credit Facility: Revolving Credit Facility $550

7.50% Senior Notes due 2025 244

• $1.4 billion borrowing base

9.75% Senior Notes due 2026 873

reaffirmed on April 16, 2021 6.75% Senior Notes due 2029 1,250

• Maturity date July 16, 2024 Total Debt $2,917

• Pricing of L+225 to 325 bpts Preferred Equity (at face value) $175

Common Equity 1,130

• Key financial covenants: Total Capitalization $4,222

• Leverage Ratio < 4X, Current Ratio >1.0

Liquidity $927

Debt Maturity Profile

$1,250

$850 $873

$244

$550

2021 2022 2023 2024 2025 2026 2027 2028 2029

RBL Outstanding RBL Availability 7.50% Senior Notes 9.75% Senior Notes 6.75% Senior Notes

18Improving Credit Profile

Significant Combination of Comstock and Covey Park created the Haynesville leader with

Scale deep Tier 1 drilling inventory and peer-leading cost structure

Sustainable,

Expect to generate meaningful Free Cash Flow to reduce revolver borrowings

Low Cost,

and Hedged Industry leading margins and returns on capital employed

Business ~69% hedged in 2021

Model

Maximizing Focused on capital discipline and deleveraging the balance sheet

Free Cash

Equitized $210 million of convertible preferred stock and refinanced $1,152

Flow million of senior notes which reduced annual fixed charges by $40.5 million

Favorable Bank facility matures in 2024

Maturity

Weighted average senior note maturity of 6.7 years

19

Runway

Improved Financial liquidity of $900+ million

Liquidity Clear line of sight to reducing leverage

19Strong Focus on ESG

Comstock strives to maintain sustainable and safe business practices and is committed to

conducting business in a responsible manner that protects the environment along with the health,

safety and security of employees, contractors and the communities where it operates.

Environmental Social Governance

We utilize natural gas fueled rigs Our Employee Health & Safety

Despite being a controlled

in our drilling operations. Using Management System is designed

company, we maintain a

cleaner burning natural gas to achieving our goals of

majority of independent

rather than diesel fuel allows us operational excellence and

directors who comprise our

to reduce emissions. maintaining an injury free

three oversight committees –

workplace. Components include

Audit, Compensation and

Our active leak detection and intensive employee training,

Governance/Nominating.

repair program uses optical gas periodic audits and inspection

imaging technology to detect and scorecards to measure our Our bonus incentive plan no

leaks so they are repaired success. longer focuses on absolute

immediately. growth metrics and instead has

We hold our contractors

performance measures for

We have improved our accountable to the highest

Return on Equity, Free Cash Flow

completion designs to reduce performance standards for

Generation, Well Cost Efficiency,

our freshwater use volumes for employee safety programs,

Operating Efficiency and Reserve

hydraulic fracturing by policies and procedures,

Replacement as its primary

approximately 30%. including training and we

performance metrics.

monitor compliance with a third

We utilize multi-well pad party management service.

locations and strive to extend We have strong governance

the lateral lengths of our wells to policies in place over stock

Our OSHA Total Recordable

minimize our above-ground ownership, non-discrimination,

Incident Rate was 0.00 in 2018

footprint. anti-harassment and bribery.

and 2019 and 0.45 in 2020.

20Lowering GHG Intensity

Emission Intensity

Emission Intensity

(kg CO2e / boe)

2019 data includes operations of Covey Park Energy for the full year.

21Natural Gas Powered Completions

Comstock has partnered with BJ Energy Solutions to deploy BJ’s next generation fracturing fleet which is fueled by

100% natural gas in its Haynesville shale development program in early 2022

BJ’s TITAN solution will make a substantial contribution toward Comstock’s CO2e and Methane reduction goals while

also improving well economics

BJ’s TITAN Fleet supports the reduction of greenhouse gas emissions while also creating efficiencies including reduced

operating costs, improved mobility, smaller well pad sites, and improved operational reliability

Carbon emissions (CO2e) are reduced by 25% compared to conventional diesel-powered fracturing equipment

This technology allows Comstock to reduce Methane emissions by ~60% compared to diesel only powered equipment, and by

greater than 95% compared to dual fuel options

The TITAN Fleet is comprised of only 8 pumps versus the 18 conventional pumps required for a typical Comstock completion today,

representing a +30% reduction of pad space required

The TITAN Fleet meets the most stringent noise requirements across North America

The three year contract with BJ locks in current completion cost while providing additional cost saving efficiencies, all

while reducing the environmental impact of Comstock’s future well completions

5,000 HHP direct drive natural gas fired turbine

pumping units – 8 units delivering 40,000 HHP

22Appendix

Guidance

Guidance 2021 2

Production (Mmcfe/d) 1,330 - 1,425

% Natural Gas 97% - 99%

Development Capital Expenditures ($MM) $510 - $550

Leasing Program ($MM) $7 - $10

Expenses ($/Mcfe) -

Lease Operating $0.21 - $0.25

Gathering & Transportation $0.23 - $0.27

Production & Other Taxes $0.08- $0.10

DD&A $0.90 - $1.00

Cash G&A $0.05 - $0.07

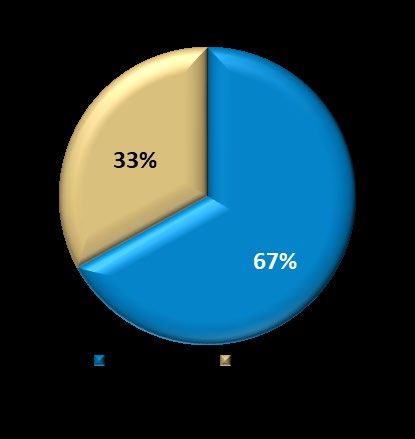

24Strong Hedging Program

Comstock has ~69% of its oil and gas production hedged in 2021

Natural Gas (Mmbtu/d) Oil (Bbl/d)

Period Swaps Collars Total 1 Swaptions 2 Collars

2021 1Q 607,271 $2.56 270,000 $2.45 / $2.88 877,271 $2.52 1,328 $41.23 / $51.10

2021 2Q 592,184 $2.54 330,000 $2.46 / $2.99 922,184 $2.51 1,500 $41.67 / $51.67

2021 3Q 585,000 $2.53 400,000 $2.47 / $3.03 985,000 $2.51 1,500 $41.67 / $51.67

2021 4Q 560,000 $2.53 400,000 $2.47 / $3.03 960,000 $2.50 1,500 $41.67 / $51.67

2021 FY 585,981 $2.54 350,493 $2.46 / $2.99 936,474 $2.51 1,458 $41.57 / $51.54

2022 1Q 190,000 $2.62 180,000 $2.51 / $3.27 370,000 $2.57 120,000 $2.51

2022 2Q 130,000 $2.68 120,000 $2.50 / $3.17 250,000 $2.59 120,000 $2.51

2022 3Q 130,000 $2.68 70,000 $2.50 / $3.10 200,000 $2.61 120,000 $2.51

2022 4Q 130,000 $2.68 70,000 $2.50 / $3.10 200,000 $2.61 120,000 $2.51

2022 FY 144,795 $2.66 109,589 $2.51 / $3.19 254,384 $2.59 120,000 $2.51

(1) Weighted average price is calculated using the long put price for collars.

(2) The counterparty has the right to exercise a call option to enter into a price swap with the Company on 120,000 MmBtu/d in 2022 at an average price of $2.51.

The call option expires for 100,000 Mmbtu/d at an average price of $2.52 in October 2021 and 20,000 Mmbtu/d at an average price of $2.50 in November 2021.

25Non-GAAP Financial Measure

Reconciliation of Adjusted EBITDAX

In thousands 1Q 2021 1Q 2020 2020 2019

EBITDAX:

Net Income (Loss) $ (134,125) $ 42,028 $ (52,417) $ 96,889

Interest Expense 63,811 52,810 234,829 161,541

Income Taxes (29,967) 11,391 (9,210) 27,803

Depreciation, Depletion and Amortization 109,128 110,425 417,112 276,526

Unrealized Loss (Gain) from Hedges 13,072 (16,483) 124,545 949

Exploration - 27 27 241

Stock-based Compensation 1,690 1,430 6,464 4,020

Loss on Early Extinguishment of Debt 238,539 - 861

2

-

Covey Park July 2019 Hedging Settlements - - - 4,574

Transaction Costs - - - 41,010

Loss (Gain) on Sale of Properties (70) - (17) 25

Total EBITDAX $ 262,078 $ 201,628 $ 722,194 $ 613,578

26You can also read