Loomis Sayles Core Plus Bond Fund: Navigating Dynamic Markets with Tactical Flexibility - Natixis Investment ...

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Loomis Sayles Core Plus Bond Fund:

Navigating Dynamic Markets with

Tactical Flexibility

WRITTEN BY THE GLOBAL CREDIT CYCLE IS A PERPETUAL FORCE

INFLUENCING INTEREST RATES, CREDIT AVAILABILITY

THE LOOMIS SAYLES CORE PLUS AND CAPITAL MARKETS. FOR CORE PLUS MANAGERS

BOND TEAM WHO SEEK TO GENERATE TOTAL RETURN BY BALANCING

LIQUIDITY AND RISK, THESE UNDULATIONS POSE A

CLEAR CHALLENGE.

In our view, navigating dynamic market cycles demands

a flexible mandate and the ability to combine rigorous

macroeconomic insight with security-specific fundamental

research. The Loomis Sayles Core Plus Bond Fund is a

benchmark-aware product that seeks to add return in stable-

to-improving risk markets and preserve principal during

adverse markets using tactical portfolio allocations.

MANAGER

INSIGHT

JULY 2021 For Institutional and Investment Professional Use Only. Not For Further Distribution.

KEY TAKEAWAYS

• The Loomis Sayles Core Plus Bond Fund is a benchmark-aware product that seeks to add return in stable-to-

improving risk markets and preserve principal during adverse markets using tactical portfolio allocations.

• Our top-down assessment of the global macroeconomic environment is used to determine sector, security, yield

curve and duration positions within the core portion of the portfolio, as well as plus sector exposure.

• Relative and absolute risks are monitored continuously, and our ability to position similar to or away from the

benchmark is central to risk management efforts.

When market conditions are constructive and risk/return measures warrant, the fund typically pursues a yield

advantage over the Bloomberg Barclays US Aggregate Bond Index through allocations to “plus sectors,” such as

high yield credit and non-US dollar. During periods that call for more defensive positioning, the fund generally

adopts a higher-quality, more benchmark-like posture. The challenge lies in determining where to deploy

capital at any given time. As such, our investment process begins with a top-down assessment of the global

macroeconomic environment and capital market drivers—a view that we use to determine sector, security, yield

curve and duration positions within the core portion of the portfolio as well as exposure to the plus sectors.

With this nimble approach, the Loomis Sayles Core Plus Bond Fund has achieved strong returns through a

range of economic and market environments, as shown in the chart below.

LOOMIS SAYLES CORE PLUS BOND FUND CLASS Y SHARES

Average annual total returns as of 30 June 2021

Fund Bloomberg Barclays US Aggregate Bond Index

ONE YEAR THREE YEAR FIVE YEAR TEN YEAR

6.20%

5.34%

4.46% 4.66%

3.03% 3.39%

2.28%

-0.33%

Performance data shown represents past performance and is no guarantee of future results. Investment return and value will vary and you may have

a gain or loss when shares are sold. Current performance may be lower or higher than quoted. For most recent month-end performance,

visit www.loomissayles.com.

Performance for other share classes will be greater or less than shown based on differences in fees and sales charges. Performance for periods greater than one year is

annualized. Returns reflect changes in share price and reinvestment of dividends and capital gains, if any. You may not invest directly in an index.

Gross expense ratio 0.47% (Class Y). Net expense ratio 0.47%. As of the most recent prospectus, the investment advisor has contractually agreed to waive fees and/or

reimburse expenses once the expense cap of the fund has been exceeded. This arrangement is set to expire on 31 January 2022. When an expense cap has not been exceeded,

the fund may have similar expense ratios and/or yields. Class Y shares are available to certain institutional investors only; minimum initial investment of $100,000.

The Class Y inception date is 30 December 1994. Class Y shares are sold to eligible investors without a sales charge; other Classes are available for purchase.

JULY 2021 For Institutional and Investment Professional Use Only. Not For Further Distribution. 2

The Importance of a Macro View

To confidently position the portfolio, we must first understand the macroeconomic

themes shaping the investment landscape. Drawing on Loomis Sayles’ deep

GLOBAL CREDIT CYCLE macroeconomic and sovereign research capabilities, we continuously assess key

global macro factors (GDP growth, monetary and fiscal policy, inflation, supply/

RECO

VER

demand dynamics of government bond markets, credit availability and politics),

Y

which are typically driven by the world’s major developed economies. Our view of

R

AI

the overall global credit cycle helps us determine a balance between the goals

EP

T R

CREDI

of return maximization and capital preservation and, accordingly, how to position

the portfolio relative to the benchmark (up or down in quality, liquidity and price

ANS EXP

transparency).

IO

N

to

LA

TE

While one or two major economies tend to lead the global credit cycle, individual

CY

RN CL

TU E

DOWN

economies do not progress through the cycle in lockstep. Our ability to identify

“mini cycles” and assess credit conditions in individual economies is critical. We

rely on insights from our sovereign research team, whose knowledge of local

markets helps us pinpoint where opportunities and risks may exist.

Tactical Sector Allocation

Once our macro and sovereign research groups have identified credit cycle themes, tactical use of sectors—

including out-of-benchmark exposure—allows us to target opportunities using what we believe are the right

instruments. The fund has the flexibility to invest up to 20% in high yield (including bank loans) and up to 10%

in non-US-dollar investments (including currencies and emerging markets debt).

When making sector allocations, we are mindful of a cycle’s idiosyncrasies: the best strategy for one period

of credit repair, for example, may not be optimal during the next phase of credit repair. To make informed

decisions, we draw on our own experience and firm resources, including specialized sector teams (asset

class strategy groups comprised of portfolio managers, traders and research analysts). We then implement

our sector strategy through fundamental bottom-up security selection. In partnership with Loomis Sayles’

credit, sovereign and securitized research analysts, we identify what we think are the best securities and

appropriate position sizes based on issuer volatility, relative valuation and liquidity.

JULY 2021 For Institutional and Investment Professional Use Only. Not For Further Distribution. 3

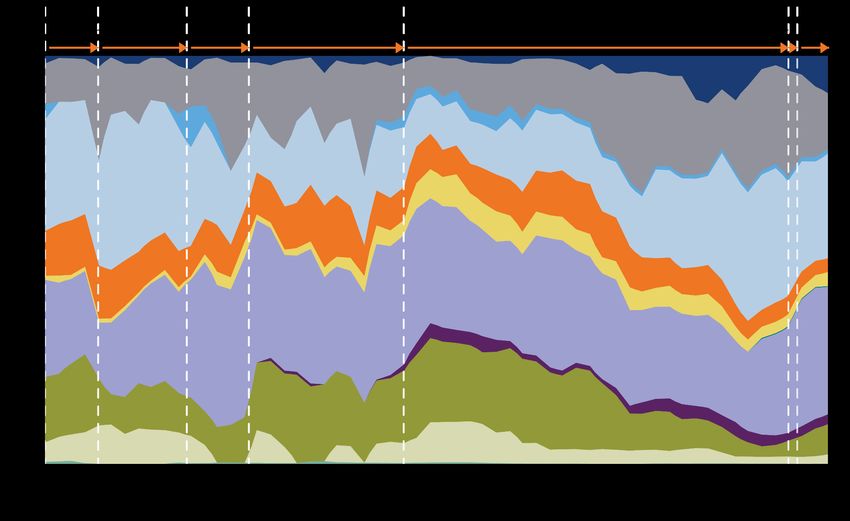

The chart below illustrates the Loomis Sayles Core Plus Bond Fund’s tactical use of sectors from 31 March

2006 until 31 December 2020. To help enhance total return potential and minimize risk, the fund is generally

positioned similar to the Bloomberg Barclays US Aggregate Bond Index during economic expansions and

downturns, while credit and non-dollar exposure is added during periods of repair and recovery.

CREDIT CREDIT

EXPANSION DOWNTURN REPAIR RECOVERY EXPANSION DOWNTURN REPAIR

LOOMIS SAYLES CORE

PLUS BOND FUND

SECTOR ALLOCATION

OVER TIME

Source: Loomis Sayles.

Data as of 31 December 2020.

Due to active management,

characteristics will evolve

over time.

Cash & Equivalents

US Treasury

US Agency

Agency MBS

CMBS

ABS / RMBS

Investment Grade Credit

USD $ Pay Emerging Market

Non-US Dollar (ex CAD) Pay

High Yield Credit

Bank Loans

Convertibles

Preferred / Equity

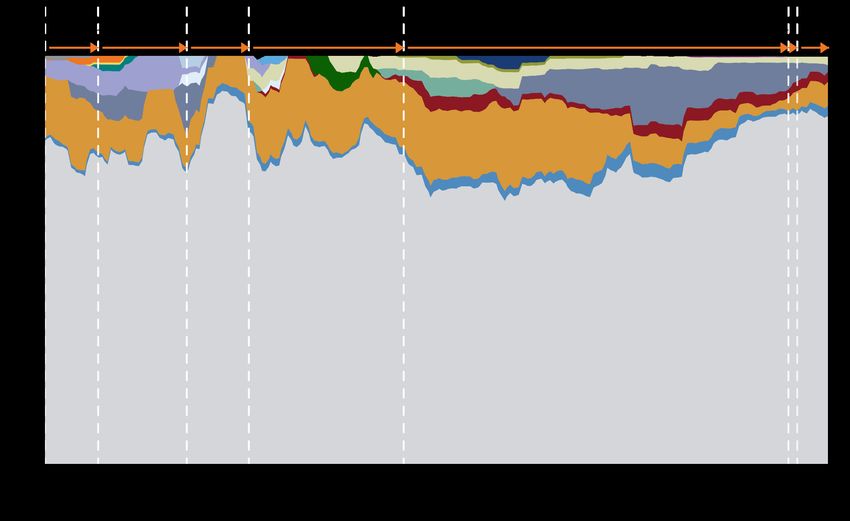

Plus Sectors: The Tool Kit

Though these sectors are often thought of as increased risk/reward areas, we think plus sectors can help reduce

portfolio risk. Overly constrained mandates can force managers to take less attractive positions because of

limited flexibility, thereby introducing unintended risk into a portfolio. Plus sectors allow us to scour a broader

opportunity set when seeking what we view as the best investment options for the fund. However, because these

sectors can introduce tracking error, we require a higher potential return per unit of risk before we will invest

out of benchmark. Allocations to plus sectors, detailed in the chart on the following page, have contributed

approximately 40% of the fund’s total return over a market cycle.i

JULY 2021 For Institutional and Investment Professional Use Only. Not For Further Distribution. 4

PRO-CYCLICAL AND

DEFENSIVE USE OF

PLUS SECTORS

Source: Loomis Sayles.

Data as of 31 December

2020.

Due to active management,

characteristics will evolve

over time.

Brazilian Real

Swedish Krona

Singapore Dollar

New Zealand Dollar

Australian Dollar

Norwegian Dollar

Icelandic Krona

Swiss Franc

Japanese Yen

Uruguay Peso

Philippine Peso

Mexican Peso We employ plus sectors to construct pro-cyclical, offensive portfolio positions

EURO

EURO (short position)

and to help defend against specific market risks, as described in the following

Canadian Dollar case studies.

TIPS

Bank Loans

High Yield Developed Market Debt

High Yield Corporate Bonds & Bank Loans: High yield can be attractive during

HY Emerging Market Deby periods of the credit cycle that we characterize as repair, recovery and expansion.

Core

It generally offers a yield advantage over many other fixed income sectors and

can benefit from capital appreciation when credit spreads tighten. Because high

yield bonds generally have a yield cushion, they can exhibit reduced duration

sensitivity and may serve as a defensive hedge against rising rates. High yield

bonds are lower in the capital structure than bank loans, and their increased

credit and liquidity risk make them high-beta assets. Bank loans hold a senior

position in the capital structure, and while this can limit their upside potential

during recoveries, it is a valuable defensive credit feature in later-stage economic

expansions. Bank loans’ floating rate coupons can be beneficial when rates rise.

JULY 2021 For Institutional and Investment Professional Use Only. Not For Further Distribution. 5HIGH YIELD & BANK LOAN CASE STUDY: 2009-2013

2009: CREDIT REPAIR/RECOVERY 2010-2011: RECOVERY 2012-2013: LATE-STAGE RECOVERY

STRATEGY Maximize market exposure and favor Emphasize specific risk and credit- Seek to mitigate interest rate risk while

THEMES more defensive industries. sensitive industries that are typical still maximizing portfolio yield. Focus

late-cycle recovery stories. on late-cycle credits and industries.

STRATEGY Emphasized long duration, lower- Began moving up in quality. Used Increased bank loan allocation. Sought

IMPLENTATION quality HY. Focused on companies higher-quality HY issues with floating coupon as part of strategy

with stable, liquid balance sheets intermediate and shorter durations to seeking to maximize yield while

and sectors that appeared well help capture incremental yield while minimizing duration in anticipation of

positioned to benefit from recovery as reducing exposure to credit higher Treasury yields.

part of strategy to maximize duration and duration risk.

contribution, price appreciation

potential and yield.

Non-US Investments: Today, roughly 76% of global GDP comes from outside the US.ii Our guidelines allow

us to follow economic growth opportunities around the world and to take targeted exposure outside US

fixed income markets. When the risk/return prospects appear particularly compelling, we deploy non-US

investments offensively to emphasize directional themes within the global credit cycle. We can also use the

allocation defensively to offset or hedge against other risk exposures in the portfolio. The Loomis Sayles Core

Plus Bond Fund is able to invest directly in global currencies, non-dollar corporate or sovereign bonds, or

dollar-denominated bonds of non-US issuers (Yankee bonds).

– Currencies: Currencies can be utilized to express pro-cyclical or defensive views of global markets, to go

up or down in quality and liquidity, and to take advantage of price dislocations or perceived overreactions in the

market.

– Non-dollar-denominated bonds & dollar-denominated bonds of non-US issuers: We can use these

tools to invest in countries or companies whose balance sheets, bond yields, or bond market supply/demand

dynamics appear attractive.

NON-US CASE STUDY: 2004-2013

2004-2006: EXPANSION 2007-2008: DOWNTURN 2009-2013: RECOVERY

STRATEGY Gradually move away from US and into Assume a much more defensive Follow fiscal and monetary policy

THEMES markets still enjoying solid economic posture in both US and non-US portfolio responses around the globe. Focus

growth. holdings. on early-recovery stories (US) and

countries tied to cyclical recovery

(Canada and parts of Latin America and

Asia).

STRATEGY Began in US-dollar-denominated and Entered into long yen position as Sought currencies of growing

IMPLEMENTATION pro-cyclical non-US-dollar investments a partial hedge in anticipation of a economies tied to the global recovery

(Australian and New Zealand dollars, risk-off period. Yen was fundamentally (Mexican and Philippine pesos,

Swedish krona). Defensively moved into undervalued and had been used as a Canadian and Australian dollars). In

the Norwegian krone, euro and Swiss funding currency for carry trades. We later 2012 and early 2013, believed

franc as US economic fundamentals felt yen could rally sharply if investors European Central Bank support

deteriorated. unwound the carry trade. would be sufficient to help peripheral

European bond yields (Spain, Italy and

Portugal) compress toward those of

core Europe.

JULY 2021 For Institutional and Investment Professional Use Only. Not For Further Distribution. 6Risk Management

When managing a benchmark-aware strategy with the goals of preserving principal in adverse markets

and adding excess return in stable-to-improving environments, risk control and downside protection are

paramount. Relative and absolute risks are monitored continuously, and our ability to position similar to or

away from the benchmark is central to risk management efforts. While we do not manage to tracking error,

we are very mindful of the benchmark and add to tracking error only when we feel we are being compensated

to do so. The fund typically targets a minimum 20% allocation to the US government sector. This positioning

helps deliver a source of liquidity and also provides a directional link to interest rate movements, which

informs how we manage portfolio duration and yield curve exposure. In volatile environments, we typically

favor high-quality liquid government securities. During periods of economic repair and recovery, credit

and non-US-dollar exposure can be used to help shorten duration and hedge interest rate risk given their

traditionally low correlation with US Treasurys and agency mortgage-backed securities.

USING TACTICAL FLEXIBILITY TO NAVIGATE RISING RATES

Not all fixed income securities will react the same to changes in US Treasury yields, and we recognize that each bond in a portfolio contributes “sources

of duration” due to its individual characteristics. One way we assess the fund’s interest rate sensitivity is by monitoring its US Treasury holdings’

contribution to duration (Treasury CTD). During periods when we believe interest rates are headed higher, we will tend to shorten Treasury CTD by

underweighting government sectors and overweighting sectors that offer incremental yield. When we believe interest rates are approaching a peak

and may begin to decline, we typically increase Treasury CTD. The chart below shows how the fund’s Treasury CTD changed relative to the 10-year US

Treasury yield over a 18-year period.

3.0 6

-188 bps YTM

2.5 5

US Treasury CTD (LHS) 2.29 years to 2.10 years CTD

10-Year Treasury YTM (RHS) 2.0 4

1.5 3

+75 bps YTM

Source: Loomis Sayles. .38 years to 2.29 years CTD

Data as of 31 December 2020. 1.0 2

0.5 1

- 0

Dec-02

Dec-03

Dec-04

Dec-05

Dec-06

Dec-07

Dec-08

Dec-09

Dec-10

Dec-11

Dec-12

Dec-13

Dec-14

Dec-15

Dec-16

Dec-17

Dec-18

Dec-19

Dec-20

Our tactical approach in managing the Loomis Sayles Core Plus Bond Fund allows us to take advantage of changing market environments.

The chart below shows the Core Plus Bond Fund’s performance during rising rate environments since the fund’s Class Y inception.

20%

16.93%

Core Plus Bond Fund (Class Y) 15

Barclays US Aggregate Bond Index

10

10-Year Treasury Bond

5.93%

Yield Change

5 3.27% 3.52%

2.01% 1.98% 2.43%

0.48%

0

-0.61% -1.14% -0.27% -0.94%

-1.91% -1.91%

-3.24% -3.24%

-5

2.25% 1.68% 1.69% 1.62% 1.56% 1.33% 1.16% 0.65%

30-Sep-98 to 30-May-03 to 31-Jul-16 to 31-Dec-08 to 31-Jul-12 to 29-Dec-95 to 31-Oct-01 to 31-Mar-08 to

31-Jan-00 28-April-06 31-Oct-18 31-Dec-09 31-Dec-13 31-Mar-97 29-Mar-02 30-May-08

Past performance is no guarantee of future results.

The ten worst periods of rising rates have been defined as the non-overlapping periods of worst cumulative rise in 10-year US Treasury yields (Source: Bloomberg)

from the trough in yield (using a 3-year look-back period) during the period of analysis (31 December 1990 to 31 January 2021). Periods that predate the fund’s

Class Y inception of 30 December 1994 have been excluded from this exhibit. Performance for periods less than one year is cumulative, not annualized.

JULY 2021 For Institutional and Investment Professional Use Only. Not For Further Distribution. 7Conclusion Today’s ever-evolving credit cycles and complex global markets demand flexibility. Our benchmark-aware, research-intensive investment style combines macroeconomic insight, changing tactical allocations and security-specific expertise to meet this need. As a portfolio management team, we have managed through multiple global credit cycles and have experienced the dynamic behavior of bond duration, yield curves, currencies and sectors. Drawing on this experience and Loomis Sayles’ research arsenal, we seek to populate the portfolio with what we believe are the best ideas for each unique market environment and deliver principal protection and solid risk-adjusted returns to our investors. This report was originally published in November 2013. We have updated the content as necessary and otherwise believe the information is correct and relevant. About Risk Fixed income securities may carry one or more of the following risks: credit, interest rate (as interest rates rise bond prices usually fall), inflation and liquidity. Mortgage-related and asset-backed securities are subject to the risks of the mortgages and assets underlying the securities. Other related risks include prepayment risk, which is the risk that the securities may be prepaid, potentially resulting in the reinvestment of the prepaid amounts into securities with lower yields. Below investment grade fixed income securities may be subject to greater risks (including the risk of default) than other fixed income securities. Foreign and emerging market securities may be subject to greater political, economic, environmental, credit, currency and information risks. Foreign securities may be subject to higher volatility than US securities due to varying degrees of regulation and limited liquidity. These risks are magnified in emerging markets. Currency exchange rates between the US dollar and foreign currencies may cause the value of the fund’s investments to decline. Inflation-protected securities move with the rate of inflation and carry the risk that in deflationary conditions (when inflation is negative) the value of the bond may decrease. JULY 2021 For Institutional and Investment Professional Use Only. Not For Further Distribution. 8

One Financial Center Boston, MA 02111 www.loomissayles.com

AUTHORS Endnotes

i

Loomis Sayles attribution; data from 1 January 2016–31 December 2020. Market cycle

defined as a three- to five-year period.

ii

Bloomberg Pro; 2019 World Bank data.

Disclosure

Bloomberg Barclays US Aggregate Bond Index is an unmanaged index of investment

grade bonds with one- to ten-year maturities issued by the US government, its agencies and

US corporations. Indexes are unmanaged and do not incur fees. It is not possible to invest

directly in an index.

PETER PALFREY, CFA

VP, Portfolio Manager This paper is provided for informational purposes only and should not be construed as

investment advice. Any opinions or forecasts contained herein reflect the subjective judgments

and assumptions of the authors only and do not necessarily reflect the views of Loomis, Sayles

& Company, L.P. Investment recommendations may be inconsistent with these opinions.

There can be no assurance that developments will transpire as forecasted and actual results will

be different. Data and analysis does not represent the actual or expected future performance

of any investment product. We believe the information, including that obtained from outside

sources, to be correct, but we cannot guarantee its accuracy. The information is subject to

change at any time without notice.

Past market experience is no guarantee of future results.

Before investing, consider the fund’s investment objectives, risks, charges, and

RICK RACZKOWSKI expenses. Please visit www.loomissayles.com or call us at 800-862-4863 for a

EVP, Portfolio Manager prospectus and a summary prospectus, if available, containing this and other

information. Read it carefully.

This information is intended for institutional investor and investment professional use only.

It is not for further distribution.

Natixis Distribution, LLC (fund distributor, member FINRA|SIPC) and Loomis, Sayles &

Company, L.P. are affiliated.

LS Loomis | Sayles is a trademark of Loomis, Sayles & Company, L.P. registered in the US

Patent and Trademark Office.

CFA® and Chartered Financial Analyst® are registered trademarks owned by the CFA

Institute.

LSWP43-0621

Exp. 10/31/21

MALR027319

1044618.29.1

For Institutional and Investment Professional Use Only. Not For Further Distribution. 9You can also read