Luxembourg Property market - Market Overview H1 2019

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Luxembourg

Property market

Research Report

Market Overview H1 2019

© Auchan / Promobe

Developer : Ceetrus

Economic

Background

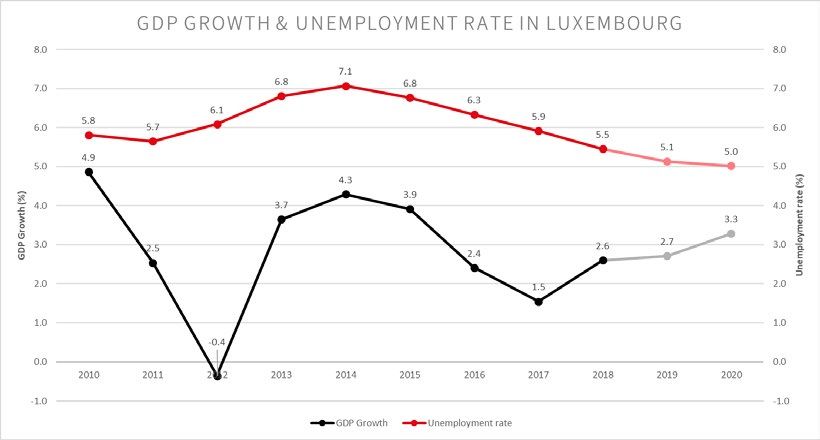

Beginning of 2019 numbers are confirming

the country’s sustained growth.

The global economic situation Luxembourg. A No-Deal Brexit will have favorable business environment. GDP

looks more volatile than ever from a very limited impact on Luxembourg growth is maintaining a good and

a business stand point. It would be economy if we compare to neighboring healthy rhythm at 2.6%, compared

foolish to think that we know what countries such as France and Belgium to the anemic 0.4% of the eurozone

2020 will bring. From Brexit chaos with both facing a -0.4% decrease area. On top of this, the Luxembourg

to a US/China trade war via possible forecast in their respective GDP. Government adopted six major policies

conflict in the gulf, the geological Luxembourg is viewed indeed as an (such as public transport gratuity)

situation doesn’t look very stable in alternative to London for investors and which will add an extra push on GDP

the short to medium term. companies in EU particularly in the and to employment. Unemployment

financial sector. The situation could stabilized at 5.5% this quarter and is

A Global Risks survey made by Oxford be very different for Luxembourg if forecasted to decrease by 0.5% by the

Economic on EU investors saw 13% a trade war intensifies because of its end of 2020.

of them viewing a No-Deal Brexit as trade exposure, a significant part of

a global economic risk. This number Luxembourg’s exports are directly Inflation experienced a significant

is growing as we get closer to 31st linked to global supply chain. decrease during the last 3 months

October 2019 (the current Brexit from 2.1% to 1.8% due to the 4.5% fall

deal deadline which the new British Despite the clouds on the horizon, of oil product prices. The public debt

Prime Minister has declared as final). fundamentals stayed positive in bottomed out at 21.3% of GDP, as ever

On top of this, 41% of respondents Luxembourg during the first half of far below the eurozone average of

see trade war as a major risk for the 2019. The stable political situation and 86.1% (Eurostat).

global economy for the next two years the government proximity to economic

and this is perhaps the biggest risk for actors helped Luxembourg maintain a

Sources: STATEC

Economic

Snapshot

Inflation Population

2018 H1 2019 2018 H1 2019

2,1% 1,8% 602.500 614.000

Structure of GDP

by output

Industry

Agricultural

11,6% 0,3%

Services

88,1%

€

GDP Increase Unemployment Rate

+ 2,6% 5,5%

Sources: STATEC

Office

Market

Speculative development remains

very limited this year.

We saw the total take-up reach 23,946 The average size per deal falls almost biggest completions are coming from

sq.m. for Q2, which brings the total H1 by half to 394 sq.m. compared to the extension of the European Court

take-up to 41,334 sq.m. On the 105 the first half of last year where we of Justice (39,750 sq.m. in Kirchberg),

transactions we listed, only six were reached 703 sq.m. If we remove the Casa Ferrero (30,000 sq.m in Airport

above the 1,000 sq.m. threshold. The IWG Group transactions from the list, district) and Royal Hamilius (10,000

biggest transactions were Spaces this number falls further to 320 sq.m. sq.m. in CBD).

(IWG Group) in Impulse (Station) Transactions from Business Services

Speculative development remains

for 6,453 sq.m., Société Nationale companies are the lowest at 297

very limited at only 18,000 sq.m. in

de Crédit et d’Investissement in the sq.m. on average.

which we have considered Quatuor

Villa Servais (CBD) for 2,240 sq.m.

Despite the robust economic health (4,600 sq.m. in Cloche d’Or) and the

and Regus (IWG Group) in Oksigen

of Luxembourg, office take-up seems speculative parts of Naos (in Belval)

for 1,925 sq.m. (Kirchberg). Triton

to have slowed down in the first half and Zenit (in CBD) with respectively

International also moved into

of this year. The Global context is an 4,600 sq.m. and 4,500 sq.m.

Oksigen for the same amount of

important factor to consider, and

space. In terms of rents, we see an upward

companies might want to wait to see

pressure in the CBD where we see

Looking at details of occupant how the current chaotic situation will

some transactions approaching 52€/

types we see Banking and Finance evolve before taking any decisions

sq.m in the coming months. The

representing 46% of the transactions. to move offices. In other words, it

same upward pressure exists on the

Flex operators, also known as co- impacts negatively the decision

Cloche d’Or and Kirchberg where

working and business centers, are process and keeps take-up at a low

prime rents could increase again in

the second biggest type with 21% level, hopefully for a limited period

the next quarters. We will see in the

of all the transactions, boosted by

Vacancy rates are still very low despite second half of 2019 if this upward

both IWG Group transactions (8,378

increasing slightly from 3.4% to 3.6% trend is confirmed.

sq.m. in total). Co-Working is in an

thanks to two major completions:

evolving trend in Luxembourg and

Impulse in Station and Staccato in

we should see more and more similar

Kirchberg. For the second half of the

transactions in the coming months.

year, 165,000 sq.m. of the new offices

Business Services is the third category

should be completed where 88% of

with 5,786 sq.m. of transactions in H1

it is non-speculative. In this total, the

(representing only 14% of the total).

All rents quoted are exclusive of VAT.

Office

Snapshot

Take-up (in sq.m) Number of Deals

2017 2018 2019

& Average Size per Deal

300.000

2017 2018 H1 2019

250.000

200.000 245.561

218.368

150.000

143,400 Average Size: Average Size:

Average Size:

100.000

109,734 761 sqm 883 sqm 394 sqm

50.000

41,334 Volume: Volume:

0 287 278 105

H1 H2

Total Investment Prime rent (€/sq.m) Number of transactions

Volume Lux (€) (excl. V.A.T.) > 1.000 sq.m:

629 Mln 50 6

Stock (sq.m) Prime yield Office Vacancy rate

4 Mln 4% % 3.6%

Prime rents (€/sq.m) Take-up by sector

(excl. V.A.T.) Education, Health &

Insurance & Pension Funds Social

Periphery Kirchberg 3% 3%

22,5 36 Manufacturing

6%

CBD

Other

50 Station

7% Banking &

35

Finance

46%

City Belt

Business Services

28 Cloche d’Or/ 14%

Esch/Belval Gasperich/Howald

Real Estate Activities

24 30 21%

Retail

Market

The outlook for rents applicable to

prime locations remains stable, whilst

rents for secondary locations are under

downward pressure.

Total full take-up (Retail Warehouse, project of shopping centers and still available for in this giant retail

Shopping Center ad High Street malls during the last months, such complex located in the center of

included) for the first 6 months of as Auchan Cloche d’Or. Transactions Luxembourg.

2019 reached 14,261 sq.m., below the in Shopping Centers are on average

In terms of completion this year,

29,133 sq.m., of H1 2018. The average smaller in size compared to Retail

we saw the opening of Cloche d’Or

take-up over the last 5-years (H1 Warehousing. The Trafic transaction

Shopping Center in May, representing

only) stands at 21,513 sq.m. where in Belval Plaza II was the biggest at

more than 75,000 sq.m. of stores

Retail Warehousing represents 54% 1,876 sq.m. followed by Action in

on which 95% are already rented

of the total. The slowdown could the Boomerang Shopping Center in

and opening this year (Auchan,

be explained by the fact that Retail Strassen at 1,093 sq.m. and C&A in

AS Adventure, Namur, Sephora,

Warehousing is not as active as it Knauf Schmiede at 976 sq.m.

Les Groupe H&M avec H&M, Cos,

has been historically. This category

A half-year volume of 4,746 sq.m. was Arket, &Other Stories, Weekday

represents only 15% of the H1 take-

recorded for the High Street category, and many others). More than 50%

up (or 2,003 sq.m.), very low if we

14% under its 5-year H1 average. The of these stores are new ones in the

compare to 2017 when it reaches

launches of a Delhaize Premium, Luxembourg retail landscape. We

30,900 sq.m.

a FNAC and a Galeries Lafayette have still in the pipeline for this year

Take-up in Shopping Centers grew inside the ROYAL-HAMILIUS project the Royal Hamilius (17,000 sq.m.) and

by 50% versus the last 5-year H1 in Q4 are bound to lead to a much infinity Shopping (6,500 sq.m.) both

average and represents 50% of the higher volume in the second part of planned for the end of the year.

total take-up. This trend is clearly 2019. Retail spaces from 30 to 630

linked to the completion of several sq.m. on single or double floors are

Royal-Hamilius, Luxembourg Infinity Shopping, Luxembourg

© Codic Group – Royal-Hamilius Retail © Immobel – Infinity Shopping

All rents quoted are exclusive of VAT.Retail

Snapshot

Yearly Take-Up (year-to-date)

2017 2018 H1 2019

Take-Up (sq.m) 48.200 37.650 14.261

Number

of Deals 70 74 35

Average Size

per Deal (sq.m) 680 509 407

Prime Rent (€/sq.m) Prime Rent (€/sq.m) Prime Rent (€/sq.m)

High Street Shopping Centres Retail Warehousing

(excl. V.A.T.) (excl. V.A.T.) (excl. V.A.T.)

2017 130 2017 110 2017 20

2018 130 2018 110 2018 20

Q1 2019 150 Q1 2019 110 Q1 2019 20

5Y H1 Take-Up (sq.m) 5Y H1 Number of Transactions

37.659

48

40.000

50

35.000

45

43

29.133 5 year

30.000 average 36 35 35

40

25.000 5 year

average

35

31

30

20.000

17.482 25

15.000 13.589 14.261 20

9.702 15

10.000

10

5.000

5

0 0

17

19

14

15

18

19

18

16

17

14

16

15

20

20

20

20

20

20

20

20

20

20

20

20

H1

H1

H1

H1

H1

H1

H1

H1

H1

H1

H1

H1Residential

Market

increasing demand for existing apartments

in comparison of new ones.

Sales of apartments 2014 and 2018. On the contrary, 29% to reach €1,542,371 on average

growth of existing apartment sales for a house (or €7,441/sq.m.). The

Sale price of existing apartment units

accelerated reaching +7.4% between average price for the whole country is

are booming across the country. If

2015 and 2018. The bank BIL in its last €784,162 for a house or €4,562/sq.m.

we compare 2017 to 2018 we see a

Immo-Index from May 2019 explained

growth of 14% for Luxembourg-city Districts where prices for a house

that the supply of existing apartments

ranging from €5,465/sq.m. to €11,173/ were the highest are in the north-east

for sale has increased along with

sq.m.. . The rest of the country is of Luxembourg-city in Niederanven

prices but that the supply of new

experiencing the same trend with for where the average price reached

apartments for sale has slowed down

example +15% in Bertrange (€7,479/ €1,837,880 (or €6,746/sq.m.). For this

along with a deceleration of price

sq.m.), +8% in Strassen (€7,367/sq.m.) district average house size is well

increases.

and +9% in Leudelange (€6,662/ above the average which is explains

sq.m.), So why do we see an increasing the high overall price, and the slightly

demand for existing apartment lower than average price per square

Sale price for new apartment units

instead of new ones? Taxation metre.

are also increasing but at a lower

changes in 2015 could be one of the

pace than the existing ones. The Mobility problems around

reasons. The VAT rate change from

growth between 2017 and 2018 Luxembourg-city also add another

3% to 17% on investments combined

is +9% reaching €8,846/sq.m. in point of pressure on prices. Citizens

to a lower rate on renovation projects

Luxembourg-city. Country-wide we of Luxembourg want to be in areas

redirected investors towards

see +12% in Bertrange (€8,675/sq.m.), with easy access to their workplace

existing apartments and mainly

+9% in Hesperange (€7,655/sq.m.), and are more and more willing to pay

in Luxembourg-city where the

+ 9% in Bettembourg (€6,044/sq.m.) the price for this. We see a consistent

concentration of apartments in prime

and +8% in Mersch (€6,364/sq.m). growth in house prices in all the

locations is the highest.

districts surrounding the capital city.

So what can explain this growth

discrepancy between new and

existing apartment growth? Sales of houses

If we look closer at the STATEC House sales have experienced the

data, we see that the growth of new strongest growth if we compare

apartment sales decelerated these 2019 to 2018. Luxembourg-city

last year’s reaching +4.8% between house prices jumped more than

Sources: Observatoire de l’habitat

Sources: BIL IMMOindex, May 2019

All rents quoted are exclusive of VAT.Residential

Snapshot

Sales of Apartments Sales of Houses

Average price per sq.m Average price per house

6.332

6.143

5.741

5.576

4.965

4.729

2016 3.795

Country Country 2017 4.029

2016

2017

2018

2016

2017

2018

2018 4.308

Existing New

8.846

8.122

8.099

7.731

7.074

Luxembourg Luxembourg

2016 6.062

5.590

City City 2017 6.325

2018 7.085

2016

2017

2018

2016

2017

2018

Existing New

Average selling price of existing apartments

(based on announced prices)

country average:

5,576 €/sq.m

Junglinster

Lorentzweiler

insuffisant sales volume

Steinsel

Kopstal

Walferdange Niederanven

less than 4 000 €/sq.m

Mamer

Strassen Sandweile

Luxembourg r

Bertrange Ville Lenningen from 4 000 to 4 499 €/sq.m

Contern

Hesperange

Leudelange

from 4 500 to 4 999 €/sq.m

Roeser

from 5 000 to 5 999 €/sq.m

more than 6 000 €/sq.m

Sources: Observatoire de l’habitat

Sources: Paperjam Plus, Real Estate, July/August 2019Investment

Market

Office transactions stay the main

driver of growth in Luxembourg

While 2019 started slowly, we saw If we dive into the detail of the the market growth potential in

the third biggest Q2 ever in terms different types of transactions, we Luxembourg are attracting more and

of transaction volume with €445 see that Core type represents 65% of more investors from the southern

Mln invested. In total, we reached the total volume (from 58% in 2018). neighbour. Belgians and domestic

€629 Mln for the first half of the year. The focus on low risk assets (such investors close out the podium with

Total investments are 21% above the as single-tenant in most premium respectively 16% and 14% of the

5-year H1 average, an optimistic sign locations) remains. The Deloitte investments.

for the second part of 2019. Office transaction is the best testimony of

Good economic conditions, low

transactions stay the main lever of this trend. Next to Core, Value Added

financial rates and the growth of the

growth for 2019 accounting for 99% is the second favorite with 24% of the

proportion of Core type investments

of the total amount, a record.. Offices total.

are keeping yields at a historically

are still the asset class enjoying the

Luxembourg market is attracting all low level. Prime office buildings in

most liquidity.

range of investors from all around the strong locations are trading at a 4%

The biggest transaction accounted world. La Française did the biggest yield for short term lease, with the

for almost 40% of the total volume transaction by investing in D-Square same pressure in the City Belt and

by reaching approximatively €250 building for Korean money. This is the Periphery. We didn’t notice any

Mln. The French investor La Française the first time a Korean investor (and change for Logistic and Retail yields

acquired the Deloitte building in the an Asian one to a larger extend) is because of the lack of transactions in

Cloche d’Or. The second largest is by entering in the Luxembourg property the first half of 2019.

Fidelity Investment that acquired the market. French investors are staying

K2 Allegro in Kirchberg for €125 Mln. the biggest players. Proximity and

5Y Half-Year Investments Volumes and Yields

900 6%

800

5%

700

600 4%

604

500

3%

400

170 175 445

300 2%

397

200

1%

100

0 0%

2015 2016 2017 2018 2019

Q1 Q2 YieldInnovation

Focus

How technology is driving

transparency in real estate

Big data and the technology driving it, are promising

huge leaps forward for the real estate industry.

From buildings filled with sensors But significant change is on the Long-term promise, short-term

tracking employees, to software that horizon. In the last two years, $6 problems?The path to greater

monitors reams of lease documents, bn has been raised by so-called transparency nevertheless has its

new technologies are rapidly being proptech start-ups – companies hurdles.

incorporated across the commercial developing technologies dedicated to

Accurately monitoring real estate

real estate industry. No two tools are the property industry. More than 250

markets requires high-quality insights

the same, but they share a common start-ups are developing and rolling

from strong data sets. However, the

output: data. out proptech around the world. New

rapid expansion of proptech tools

technology platforms and services

While broad-based data collection has provoked concern around the

will give investors, tenants and

requires requisite caution, the consistency and reliability of some

property managers access to more

eventual outcome is likely to be of the data, a natural side effect when

easily-manageable datasets, allowing

greater transparency, especially in some of the new data providers rely

for better-informed decision-making

markets where information remains on scraping online sources.

processes.

tightly held, according to JLL and

The ownership of information is also

LaSalle’s Global Transparency Index. At the other end of the spectrum,

a key concern. Property owners and

Luxembourg scored 32nd, not bad blockchain technology could lead

managers can collect vast amounts

but still some room for improvement. to greater global standardization in

of data on tenants through sensors,

all areas relating to property, from

“Property is in the midst of a internet-linked devices, and video

city planning to environmental

technological leap,” says Jeremy feeds. If the information is tightly-held

reports. Trials have already started.

Kelly, global research director at JLL. among operators however, it could

Dubai plans to record all real estate

“The adoption of new technology limit the broader benefits of new

transactions on blockchain by 2020.

platforms generates new and more tools on wider market transparency.

Estonia is also using the technology

easily-accessible market data, Privacy and confidentiality concerns

to authenticate property registries.

which is key for overall real estate are also clearly pertinent with much

transparency.” tighter regulation and corporate

policies heading firmly in the

opposite direction .

Publicly-shared data may expand the

size of the market and make it more

efficient. Proptech data may have

this potential, but this outcome is

not guaranteed unless the firms who

control the data are willing and legally

able to choose to take this path.

As real estate becomes a mainstay

allocation for almost every

institutional investor, access to

consistent and reliable information

is a priority, but remains very difficult

to fulfill.Offices Luxembourg

Atrium Business Park

41 Rue du Puits Romain

L-8070 Bertrange - Luxembourg

T: + 352 - 46 45 40

www.jll.lu

Contacts

Angélique Sabron Lotfi Behlouli

HEAD OF MARKETS DIRECTOR OFFICE AGENCY

LUXEMBOURG LUXEMBOURG

+352 46 45 40 72 +352 46 45 40 58

Angelique.Sabron@eu. jll.com Lotfi.Behlouli@eu. jll.com

Robby Cluyssen Vincent Van Brée

SENIOR CONSULTANT HEAD OF CAPITAL MARKETS

RESIDENTIAL AGENCY LUXEMBOURG

LUXEMBOURG + 352 46 45 40 35

+352 46 45 40 52 Vincent .VanBree@eu. jll.com

Robby.Cluyssen@eu. jll.com

Stéphane Colle Dimitri Collignon

SENIOR ANALYST DIRECTOR RETAIL AGENCY

RESEARCH BELUX LUXEMBOURG

+352 46 45 40 + 352 46 45 40 57

Stephane.Colle@eu. jll.com Dimitri.Collignon@eu. jll.com

www.jll.lu / Jones Lang LaSalle

© 2019 Jones Lang LaSalle IP, Inc. All rights reserved. The information contained in this document is proprietary to Jones Lang LaSalle and shall be used solely for the purposes of evaluating this proposal.

All such documentation and information remains the property of Jones Lang LaSalle and shall be kept confidential. Reproduction of any part of this document is authorized only to the extent necessary

for its evaluation. It is not to be shown to any third party without the prior written authorization of Jones Lang LaSalle. All information contained herein is from sources deemed reliable; however,

no representation or warranty is made as to the accuracy thereof.You can also read