Markets Outlook RESEARCH - BNZ

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

RESEARCH

Markets Outlook

5 July 2021

July MPR Preview

• Case for rate hikes builds Market pushing the RBNZ hard

• Least regrets may mean sooner rather than later

• Capacity constraints and housing flash bright warning signs

• Market already pricing February move

• Can the RBNZ afford to green light this?

The RBNZ has been adamant that its decision-making

framework has been based on a policy of least regrets.

Those least regrets have largely entailed keeping monetary

policy as loose as possible to stave of the potential for

economic chaos that COVID has threatened. The problem

is that monetary settings broadly remain at the same levels

that were seen while experiencing the very worst of the

economic fallout from the COVID outbreak. No matter how

pessimistic you might be, it is hard to deny that conditions acknowledges recent strength in the domestic economy

are now better than at that time and should remain that while also continuing to highlights the Bank’s concerns

way even with further COVID outbreaks likely. On this with the economy’s residual risk.

basis, monetary conditions should be tighter than they are

now, and least regrets should be turning towards avoiding Nonetheless, we think it would be difficult for the RBNZ to

the threats imposed by an overheating economy. hold a straight face and repeat its May MPS comment that

meeting its employment and inflation requirements “will

Be that as it may, this is a very difficult road for the RBNZ necessitate considerable time and patience”. In our opinion

to travel. While it will be itching to adopt a tighter stance, the requirements have already been well and truly met.

it will also not want financial markets to get ahead of

themselves for fear of the dislocation that rapidly rising And, yes, there are a number of “temporary” factors

interest rates might cause. currently at play but once these factors wane we still think

inflation and employment conditions will warrant a return

It is worth noting that market pricing has already moved to more normal/neutral monetary settings which must

dramatically. At the time of writing, the market is fully mean significantly higher interest rates than is currently

pricing in a 25 basis point rate hike by the February 2022 the case.

MPS. A further hike is priced by August. With the domestic

data printing stronger and stronger the market even has a Even though we believe a hike in the cash rate now could be

more than 50/50 chance of a rate hike by the November easily justified, we are not forecasting one on the day of the

meeting this year. July 14 Monetary Policy Review. There is, however, a

reasonable chance that the RBNZ gives a strong nod that its

When the RBNZ produced its May MPS it had effectively LSAP problem might be culminated earlier than the June

assumed a first rate hike by August of next year. The data, 2022 deadline it currently faces. It doesn’t need to make any

and anecdote, flow since then must surely mean the formal announcement in this space as it can simply let its

Reserve Bank has either become more confident in that purchase programme slide away to nothing without causing

assumption or sees the need to tighten sooner. It simply any fuss and bother. However, the Bank might like to send a

can’t have gone the other way. Consequently, the RBNZ is gentle message as to its possible OCR track by formally

left with two options. Either it green lights the recent changing the date when it may cease purchasing new paper.

market move or it tries to push back against the recent This could act as a soft-signal as to when the RBNZ thinks it

drop in rates. The problem it faces is that if it does concur might want to have the option of raising the cash rate.

with current market pricing, and says so, the market will

inevitably tighten further. It is not clear the Reserve Bank In terms of the data the Bank has received since the MPS,

would be happy for this to occur just yet. This being the the Q1 GDP outturn was the game changer. At 1.6% it was

case, we think the RBNZ might produce a statement which miles above the RBNZ’s -0.6% assumption and the level of

www.bnz.co.nz/research Page 1

Markets Outlook 5 July 2021

GDP was further raised by upward revisions to previous On Tuesday morning NZIER delivers its June Quarterly

quarters’ activity. Prior to the release of these data the Survey of Business Opinion. This is a survey that the RBNZ

RBNZ had assumed the economy had a negative output watches with much interest. In our opinion, there is a very

gap of 0.5%. We can’t be sure what it’s current view is but high chance that it will provide strong supportive evidence

the bankers must almost certainly believe that output gap of the capacity constraints that have developed in the

analysis would now suggest that, all other things being economy, the desire for businesses to hire more labour

equal, that the Reserve Bank should be tightening now. than is available and the upward pressure on prices. As

such, it is highly unlikely to dissuade the RBNZ from

That perception will have been strengthened by recent becoming more hawkish.

labour market reports. Partial indicators have seen us

revise upward our employment growth expectation for If the QSBO doesn’t cause the RBNZ sleepless nights, this

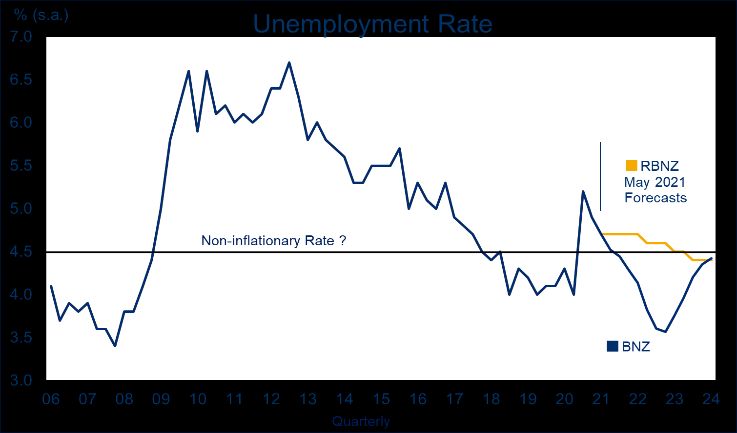

Q2 to 0.5% and revise down our unemployment rate morning’s Barfoot’s housing data will certainly do so. The

expectations to 4.5%. If we are right, the unemployment median average price in Auckland rose 3.4% in the month

rate will again be below the RBNZ’s expectations of June to be up 21.9% for the year. The volume of sales

(currently sitting at 4.7%) and will be very close to the for the month was nothing short of ridiculous. The annual

NAIRU. Moreover, job ads data, vacancies, employment increase was 52%. And, no, this is not a COVID bounce-

intentions and labour shortage surveys, and anecdotal back. The increase from June 2019 was 58%! Listings were

evidence all suggest the risk is that even we are relatively strong but not strong enough to keep pace with

continuing to underplay the strength in the labour demand. As a result, the month-end stock of homes

market. Recall, of course, that we have had a long-held available for sale was the lowest June reading in five years.

view the unemployment rate will fall sub 4.0% within

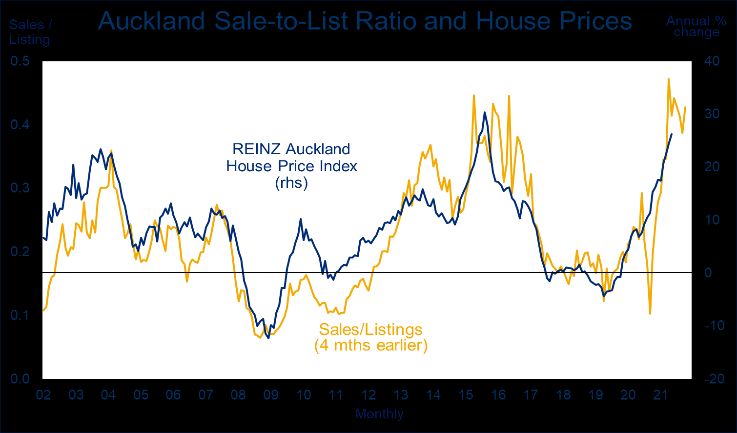

twelve months and that labour issues will become even Housing refuses to die peacefully

more substantive as the Australian labour market

similarly tightens.

Labour market tighter and tighter

It will take time for Government and RBNZ policy shifts to

fully impact the market but how long can the RBNZ wait

for confirmation of such. As we have said for a long time

now, if money costs next-to-nothing people will keep

But it doesn’t end here, in addition: borrowing it.

- It looks like annual CPI inflation will be well above the

RBNZ’s forecasts by the end of the September quarter; Other data due over the week is unlikely to have a marked

impact on our, or the RBNZ’s, general view of the world.

- Trading partner growth estimates are being revised

We already know that commodity prices are high and

higher (albeit that Australia may take a hit);

supportive of the broader economy. Today’s ANZ

- Oil and house prices look like they will end up higher Commodity Price Index is likely to report commodity prices

than the RBNZ had assumed. moving further into record levels while Wednesday’s GDT

- And the TWI is modestly lower than assumed. (dairy) auction is expected to reveal ongoing strength in

dairy prices albeit they are currently on a modest

All this being the case, the only real debate is when does downward trend.

the Reserve Bank start hiking and how aggressively does it

do so. The when and how much is of critical importance to Also on Wednesday, we get the working age population

financial market participants but the key message for all data that goes into the June quarter labour market

others is, simply, get used to the prospect of rising interest calculations. With net migration remaining very low the

rates, and probably sooner rather than later. growth in the potential labour force will stay similarly

dampened adding to labour supply constraints and helping

push the unemployment rate ever lower.

www.bnz.co.nz/research Page 2

Markets Outlook 5 July 2021

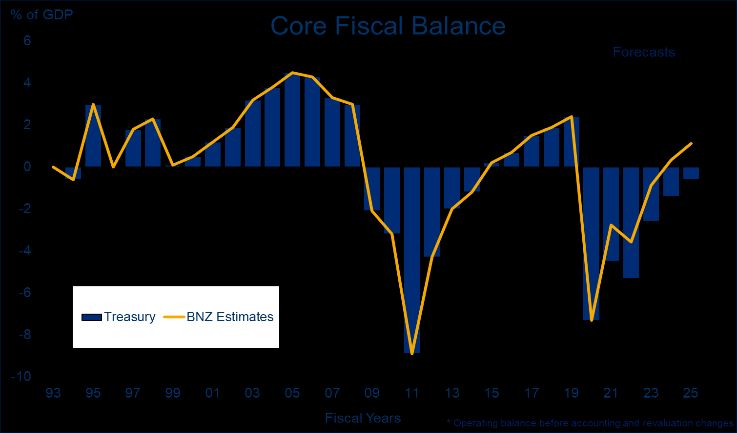

Labour supply constrained Fiscal windfall

And while much of the current focus is on monetary policy, was 31.2% of GDP as at end May. This is materially lower

and how the data might impact the Reserve Bank’s views, than the 33.1% projected by Treasury.

let’s not forget developments on the fiscal front where the

ongoing strength in the economy continues to deliver It is worth nothing that New Zealand’s core crown residual

revenue windfalls. Just two months after the Budget, the cash deficit for the June year 2021 looks like it will be at

deficit for the year ended June 2021 is already $5.8 billion least $6.3bn less than expected. All things being equal, this

less than Treasury forecast, with one month to go. means the Government will have “over-funded” its debt

programme by this amount. Unless the Government

If we assume the fiscal gains that have been made in the chooses to “recycle” this money, there is the opportunity

last two months are sustained then the fiscal deficit for the for future debt issuance to be further lowered. In turn this

June Year 2021 will fall to just 2.8% of GDP from Treasury’s means there will be even less need for the RBNZ to

4.5% of GDP estimate. If we then assume the change in the support the bond programme.

deficit for each year thereafter remains as currently

forecast then the books would be in surplus by June 2024. At face value, the fiscal position is fantastic news, and

highlights just how superbly placed the NZ Government is

Similarly, debt projections become that much better too. if it again needs to come to the rescue of the economy due

In this regard, New Zealand’s fiscal position is nothing to another shock or cyclical downturn. But with this

short of staggering, especially when you consider that not position also comes heightened pressure on it to relax

only have we faced a pandemic and financial crisis in the fiscal discipline. Right now, the last thing New Zealand

last 15 years but also a series of devastating earthquakes. needs is more fiscal stimulus. This is not to deny the

Based on our deficit projections, New Zealand’s gross requirement for targeted spending, as and where

government debt (ex settlement cash balances) will rise to necessary, but any devolution to a scattergun approach

a mere 35.6% of GDP by June 2025. This means New could prove economically damaging.

Zealand’s gross debt will be lower than the net debt of

many developed countries and, indeed, lower than the stephen_toplis@bnz.co.nz

debt levels of most pre-COVID. As things stand, net debt

www.bnz.co.nz/research Page 3Markets Outlook 5 July 2021

Global Watch

• FOMC minutes to monitor for taper talk NAIRU. NAB sees the RBA lagging the Fed, BoC and RBNZ in

• China inflation and financing data due normalisation.

• ECB to adopt a more symmetrical 2% inflation target?

Dovish outcomes could include any of the following: (1)

• RBA meets; decision on YCC, QE expected

rolling the 3yr YCC to the November 2024 bond; (2) not

• G20 fin mins and central bankers meet next weekend

tapering QE and doing a full $100bn in six months. A push

back on market pricing of rate hikes as early as November

2022 would also be dovish and could incorporate retaining

Australia

the “at least 2024” guidance on when conditions for a rate

Tuesday’s RBA Board meeting will be closely watched with hike would be met.

the Bank having flagged this meeting as where it will make

Hawkish outcomes would be: (1) QE moving to a weekly

its decisions on whether to extend the 3yr YCC target, and

purchase schedule as that would enable a quick end to QE

how it will calibrate its ongoing QE program. NAB’s view is

that the RBA will not extend its 3yr YCC target and we also and thus potentially opening a shift to rate hikes earlier.

Communication thus will be key here should the RBA move

expect QE to be tapered (reduced to $75bn from $100bn for

to a weekly purchase schedule given hike implication; and

six months) in the third round to commence in September

(2) a shift in the RBA’s framework of wanting actual

2021. The consensus view is also that the RBA does not

extend 3yr YCC, but for QE a majority see a shift to a more inflation being sustainably within the band before raising

rates. The former is a possibility, while NAB does not think

flexible QE schedule without an immediate taper.

the RBA will shift from their maximum employment

By not rolling 3yr YCC, the RBA can continue to step away framework and detect no shifts internationally from other

from time-based forward guidance to be more outcomes central banks.

based, opening up the possibility of rate hikes earlier than

Finally, removing the “at least 2024” guidance NAB does

2024 if economic outcomes develop favourably. Markets are

not think would be much additional signal as not rolling 3yr

already there, fully pricing rate hikes to 0.25% by November

2022 and to 0.75% by March 2024. This week’s Board YCC already pivots forward guidance towards being

outcomes based. Dr Lowe has already shifted language

Meeting and post-Board remarks will also be important to

somewhat here, concluding his recent speech with the “for

see whether the RBA pushes back on market pricing.

inflation to be sustainably in the 2-3 per cent range, wage

NAB’s view on the cash rate is that while there is a increases will need to be materially higher than they have

probability of the RBA moving in H2 2023 and markets been recently. Partly for the reasons I talked about earlier,

should price in this risk, the RBA has given itself a high bar, this still seems some way off”.

assessing that 3%+ wages growth is needed to generate

inflation sustainably at target. 3% wages growth by 2022 is Regarding data this week, Retail Sales and Building

possible on wages models where NAIRU is assumed to be Approvals are due on Monday and Weekly ABS Payrolls on

Tuesday. None are likely to be market moving, especially

around 5.0%, given unemployment is now 5.1%. NAB’s

given the RBA meeting this week.

model-based NAIRU estimates are around 4.5% with

possible downside risks to this given international Building Approvals are likely to decline after a period of

experience that Governor Lowe has also previously cited. recent strength, driven by the HomeBuilder stimulus and

An eventual acceleration in wages growth may also take other government grants. NAB pencils in a -5.0% m/m

some time to feed through to sustainably higher inflation. outcome, which is where the consensus has now settled.

Accordingly, outside of 3yr YCC and QE, the markets focus Retail Sales are a final measure with NAB and the

will be on when the RBA expects to hike rates, and consensus at 0.1% m/m, matching the preliminary print.

whether the RBA pushes back on market pricing which

Virus numbers and the Sydney lockdown

currently has the first hike pencilled in by November 2022.

Any indication of how far the RBA assesses the economy is As for the recent Sydney virus outbreak, it is unlikely to

from full employment will also be in focus given weigh materially on July’s Board Meeting with the May

unemployment is back to pre-pandemic levels. SoMP having assumed sporadic outbreaks controlled via

short lived restrictions. There is the risk that Sydney’s

NAB thinks the RBA will push back on market pricing,

lockdown will go longer than two weeks with virus

coming across as dovish, with the virus outbreak another

numbers sticky.

reason to remain on the dovish side. The RBA’s recent

pivot to maximum employment also suggests the RBA will Given the recent virus outbreak has resulted in lockdowns in

be happy to lag wage/price developments and will wait four capital cities (Sydney, Brisbane, Darwin and Perth),

until actual inflation is sustained within the band before there is intense focus on what the vaccination threshold is

tightening, instead of hiking on a pre-conceived notion of to go from the current de-facto elimination strategy to living

www.bnz.co.nz/research Page 4Markets Outlook 5 July 2021

with the virus. NSW Premier Berejiklian said it would take Eurozone

around 75-80% of the population to be vaccinated before

News reports say the ECB is to hold an impromptu meeting

“you can start having conversations about what Covid

in Frankfurt during the week to wrap up the Bank’s

normal looks like”. NAB calculates Australia could get to 80%

strategy review. If agreement can be reached, that may

adult vaccination by November 2021. The outline of the

well turn out to be the focal point. A formal shift to a more

National Cabinet’s plan to transition Australia’s COVID-19

symmetrical 2% inflation target is likely. Datawise Retail

response also ties avoiding lockdowns to vaccinations, with

Sales for May are due on Tuesday as is the ZEW investor

specific targets to be developed. Until that point is reached,

survey for June; Final Services PMI for June is on Monday.

the risk of snap lockdowns will remain.

While some EZ countries are fearing more rapid

China transmission of the Delta variant, the EU’s digital travel

passport, is aimed at keeping the EU’s internal borders

CPI/PPI on Friday are the focus this week. The PPI is

open and should help the tourism sector.

currently running at 9.0% y/y indicating price pressure

within the industrial sector even as consumer prices

United Kingdom

remain subdued. The CPI in June is seen matching May’s

1.3% y/y outcome. Aggregate Financing figures are due The UK continues to stand out as a major economy with

anytime from now and will also be closely watched given high levels of vaccination and is seemingly on a path to

the deceleration seen in liquidity indicators. The Caixin fully reopen to ‘live’ with the virus mid-July. Datawise, May

Services PMI is due today. monthly GDP is due on Friday and should be relatively

strong. RICS releases its June house price indicator on

US

Thursday. Final services PMI activity for June is due on

The Public Holiday on Monday (Independence Day obs.) will Monday. BoE’s Bailey speaks with ECB’s Largarde on Friday

make for a quiet start to the week. Wednesday’s FOMC ahead of the finance ministers and central bankers G20

Minutes will be closely scrutinised for taper discussion, meeting next weekend.

particularly if the possible pace and MBS v. Treasuries was tapas.strickland@nab.com.au / doug_steel@bnz.co.nz

discussed. Tuesday’s ISM Services Index will shine more light

on growth momentum, while JOLTS on Wednesday should

be very strong and continue to point towards a sharp labour

market improvement over coming months.

www.bnz.co.nz/research Page 5Markets Outlook 5 July 2021

Fixed Interest Market Reuters: BNZL, BNZM Bloomberg:BNZ

After what had been a big move over the previous two risks are a little more balanced with the market already

weeks, there was some consolidation in short-term rates pricing a significant risk of a November hike.

last week. The market continues to fully price the first RBNZ

The RBA meeting tomorrow afternoon, and Governor

hike by February next year, with the Fed and RBA priced for

Lowe’s post-meeting remarks, will be key focus this week.

late 2022. Long-term interest rates fell last week and, in a

The firm consensus is that the RBA won’t extend its Yield

bigger picture sense, remain contained within broader

Curve Target bond to the November 2024, instead keeping it

ranges. We still see market positioning as the biggest near-

at the April 2024 for now (the market is clearly well ahead of

term obstacle to long-term rates heading higher as we have

the RBA, having priced around 30bps of hikes by the end of

in our forecasts. The key focus for this week is the RBA

2022). There is less consensus on what will happen with QE,

meeting tomorrow.

although our NAB colleagues think a taper is now priced in.

Last week saw further falls in long-term interest rates

Last week saw NZ bond supply step up, to $500m/week in

offshore, with the US 10-year rate ending the week at

nominal bonds from $300m/week in June. With the RBNZ

1.42%, its lowest close since early March. The nonfarm

keeping its QE bond buying pace at $200m, this left the

payrolls report revealed strong job growth in June but the

market needing to absorb more supply. The early signs are

market was seemingly unimpressed by the increase in the

encouraging, with no noticeable underperformance of

US unemployment rate, from 5.8% to 5.9%. Having been on

government bonds versus swaps or other bond markets. This

edge that a very strong payrolls report could bring forward

may give the RBNZ greater confidence that the market will

the timeline for the Fed to taper its bond buying, the market

adjust to the end of QE without major price adjustments.

reaction to the data, which saw interest rates decline and

Indeed, the RBNZ reduced the number of buyback operations

the USD weaken, suggested some relief among investors

this week from three to two (and the number of bonds it aims

that the Fed can take its time. The Fed minutes this week

to purchase from six to four), which arguably sets the scene

might provide some more clues around the timing and a

for future reductions to bond purchases.

more specific criteria for tapering.

While RBNZ staff continue to tinker with the week-to-week

The recent pullback in long-term rates might be a little

pace of bond purchases, we still think the Monetary Policy

surprising given the market has pulled forward the expected

Committee will want to sign off a decision to reduce

timing of rate hikes by most central banks. We think there

purchases to zero. We wouldn’t rule out such an

are a few factors contributing to this. First, it’s not unusual for

announcement at the RBNZ’s August MPS and it’s even

long-term rates to experience a period of consolidation after a

conceivable it could come as soon as July’s MPR.

big move, like that seen earlier in the year, especially when US

rate hikes still appear some time away. Second, market Long-term rates drifting lower

positioning still appears heavily weighted to ‘short’ positions

(i.e. bets on long-term rates increasing) which has acted as a

headwind for long-term rates increasing further. Often, when

investor positioning leans too far in one direction, the market

becomes resistant to moving much further and, indeed, often

moves the other way (the so-called ‘pain trade’). Third, the

hawkish Fed meeting in June has tempered some of the

optimism around the ‘reflation trade’, which has weighed on

long-term rates. We still think this is a short-term indigestion

issue and ultimately long-term rates, which remain extremely

low on a historical basis, will eventually head higher, both

offshore and in New Zealand. RBNZ bond buying falls further behind bond supply

There wasn’t much change in the expected timing of rate

hikes among the major central banks last week. The market

prices the Fed to start its rate hike cycle in December 2022,

a similar time to the RBA. For NZ, the market continues to

price a slightly better than even chance of a November 2021

OCR hike, with a 25bp move fully priced for February 2022.

The NZ 2-year swap rate ended last week at a 15-month

high of 0.8%.

NZ short-term rates are likely to keep moving higher ahead

of likely RBNZ OCR hikes. However, we think the near-term nick.smyth@bnz.co.nz

www.bnz.co.nz/research Page 6Markets Outlook 5 July 2021

Foreign Exchange Market Reuters pg BNZWFWDS Bloomberg pg BNZ9

The USD was broadly stronger last week, seeing NZD/USD Our short-term fair value model estimate rose to 0.7450

down 0.7% to 0.7030. This included a reversal of USD last week, its highest level since 2014, a reflection of high

strength Friday night following a mixed US employment risk appetite, record-high NZ commodity prices and a

report, helping the NZD rebound from a low of about higher NZ-US real short-rate spread.

0.6950. The NZD was mixed on the crosses, rising to a one-

Recent price action confirms that decent support remains

month high against the AUD and closing the week at

for the NZD just under the 0.6950 mark, while the 0.71

0.9340, being flat against EUR, and down slightly against

level is the initial resistance level. Our current projections –

GBP, JPY and CAD.

which still see a pathway towards the NZD making fresh

The currency market remains focused on the US monetary year-to-date highs later in the year – are consistent with a

policy outlook at present. With the Fed’s reaction function view that the NZD remains at an attractive buying level.

dependent on “substantial further progress” towards its

Elsewhere this week, the RBA meeting tomorrow is a key

maximum employment goal being met, the market was

one for which the Bank will make a decision on its QE

sensitive to Friday’s employment report. In anticipation of a

programme. Markets consensus is that the RBA won’t

strong report, the USD strengthened in the days leading into

extend its Yield Curve Target bond to the November 2024,

the report but subsequently fell on a mixed result. While the

instead keeping it at the April 2024 (the market is well

monthly employment gain of 850k from surveyed

ahead of the RBA, having priced around 30bps of hikes by

businesses was ahead of expectations, the household survey

the end of 2022). There is less consensus on what will

showed weaker employment and an unexpected lift in the

happen with QE, although our NAB colleagues think a

unemployment rate to 5.9%. The shortfall of jobs from the

taper is now priced in. Thus, the market should be well

pre-pandemic level remains a chunky 6.7m people,

prepared for this announcement but there is always a

highlighting how slow the Fed is likely to be in normalising

small chance of a surprising AUD reaction.

monetary policy settings, with the market expecting rate

hikes to still be some 18 months away. Monetary policy not driving NZD/USD so far this year

In our view this market focus on US monetary policy looks 0.76 0.5

NZD/USD (lhs) NZ-US short rate* (rhs)

misguided. But as long as that remains the case, the USD

0.4

will be sensitive to the monthly employment reports and 0.74

outlook for US monetary policy. The NZD will be simply 0.3

taken for the ride.

0.72 0.2

Ironically, the rates market is moving towards seeing an

0.1

earlier start to the NZ monetary policy tightening cycle, but 0.70

the currency market isn’t paying attention. The run of *Expected tightening next 12 months,

0.0

strong NZ economic data means that the justification for NZ v US

0.68 -0.1

emergency policy settings has well passed. NZ house price Jan-21 Mar-21 May-21 Jul-21

inflation is running close to 30%, we think CPI inflation will Source: BNZ, Bloomberg

surpass 3% in the current quarter and by year-end it is

conceivable that the unemployment rate could have a 3-

handle. These are no appropriate conditions for a cash rate Cross Rates and Model Estimates

close to zero and the RBNZ still buying bonds at the rate of Current Last 3-weeks range*

$200m per week to suppress rates across the curve.

NZD/USD 0.7026 0.6920 - 0.7160

The OIS market prices a slightly better than even chance of NZD/AUD 0.9336 0.9250 - 0.9350

the RBNZ raising the OCR as soon as November. We can’t NZD/GBP 0.5082 0.5010 - 0.5100

argue against that view – a move to higher rates sooner NZD/EUR 0.5921 0.5840 - 0.5940

rather than later seems entirely appropriate. The message NZD/JPY 77.98 76.20 - 78.80

of the Quarterly Survey of Business Opinion due tomorrow *Indicative range over last 3 weeks, rounded figures

is likely to be intense pressure on economic resources –

high capacity utilisation and difficulty finding labour, for BNZ Short-term Fair Value Models

example – and intense pressure on costs and inflation.

Model Est. Actual/FV

With the NZD weaker than implied by economic NZD/USD 0.7450 -6%

fundamentals, the RBNZ should be much less concerned NZD/AUD 0.9010 4%

about any possible positive NZD reaction to tightening

monetary policy well ahead of other major central banks. Jason.k.wong@bnz.co.nz

www.bnz.co.nz/research Page 7Markets Outlook 5 July 2021

Technicals

NZD/USD

Outlook: Trading range

ST Resistance: 0.7100 (ahead of 0.7315)

ST Support: 0.6940 (ahead of 0.6800)

Recent price action reinforces the view that there is plenty

of support just below the 0.6950 mark. Prior support of NZD/USD – Daily

0.71 is the first level of resistance, ahead of 0.7315. Source: Bloomberg

NZD/AUD

Outlook: Trading range

ST Resistance: 0.9485 (ahead of 0.9600)

ST Support: 0.9135 (ahead of 0.9055)

The broader picture is one of directionless trading. We put

the support and resistance gap at a fairly wide 0.9135-

0.9485. NZD/AUD – Daily

Source: Bloomberg

jason.k.wong@bnz.co.nz

NZ 5-year Swap Rate

Outlook: Neutral

ST resistance 1.43

ST support 1.17

Still awaiting a break. Should 1.43 be breached, look

for move higher in yield. Alternatively, pay towards NZ 5-yr Swap – Daily

1.17 with a tight stop. Source: Bloomberg

NZ 2-year - 5-year Swap Spread (yield curve)

Outlook: Flatter

MT resistance 0.75

NZ 2yr 5yrSwap Spread – Daily

MT support 0.445 Source: Bloomberg

Should find some support around here around 0.54.

But await a move towards medium support to take off

flattener at 0.445 level.

pete_mason@bnz.co.nz

www.bnz.co.nz/research Page 8Markets Outlook 5 July 2021

Quarterly Forecasts

Forecasts as at 5 July 2021

Key Economic Forecasts

Quarterly % change unless otherwise specified Forecasts

Mar-20 Jun-20 Sep-20 Dec-20 Mar-21 Jun-21 Sep-21 Dec-21 Mar-22 Jun-22

GDP (production s.a.) -1.5 -10.8 14.1 -1.0 1.6 0.7 0.6 0.7 0.5 1.1

Retail trade (real s.a.) -1.3 -14.8 27.7 -2.6 2.5 2.5 0.4 0.5 0.6 0.8

Current account (ytd, % GDP) -2.8 -1.8 -0.8 -0.8 -2.2 -3.5 -4.1 -4.4 -4.1 -4.2

CPI (q/q) 0.8 -0.5 0.7 0.5 0.8 0.7 1.2 0.6 0.3 0.3

Employment 1.0 -0.2 -0.7 0.6 0.5 0.5 0.3 0.4 0.5 0.7

Unemployment rate % 4.3 4.0 5.2 4.9 4.7 4.5 4.4 4.3 4.1 3.8

Avg hourly earnings (ann %) 3.7 2.9 3.9 4.6 3.0 3.3 2.3 2.4 3.3 3.5

Trading partner GDP (ann %) -2.4 -5.3 -0.9 0.7 6.3 9.5 5.5 4.6 4.8 4.7

CPI (y/y) 2.5 1.5 1.4 1.4 1.5 2.7 3.2 3.3 2.7 2.3

GDP (production s.a., y/y)) 0.0 -11.2 0.4 -0.8 2.4 15.6 2.0 3.7 2.6 2.9

Interest Rates

Historical data - qtr average Government Stock Swaps US Rates Spread

Forecast data - end quarter Cash 90 Day 5 Year 10 Year 2 Year 5 Year 10 Year Libor US 10 yr NZ-US

Bank Bills 3 month Ten year

2019 Dec 1.00 1.15 1.05 1.40 1.10 1.20 1.50 1.95 1.80 -0.40

2020 Mar 0.75 1.05 1.00 1.35 1.00 1.10 1.40 1.55 1.40 -0.03

Jun 0.25 0.30 0.40 0.85 0.25 0.40 0.80 0.60 0.70 0.15

Sep 0.25 0.30 0.25 0.65 0.15 0.25 0.60 0.25 0.65 0.02

Dec 0.25 0.25 0.25 0.70 0.15 0.30 0.75 0.20 0.85 -0.15

2021 Mar 0.25 0.30 0.75 1.40 0.40 0.85 1.50 0.20 1.30 0.09

Jun 0.25 0.35 1.00 1.75 0.55 1.20 1.90 0.15 1.60 0.17

Forecasts

Sep 0.25 0.35 1.60 2.20 0.90 1.65 2.25 0.15 2.00 0.20

Dec 0.25 0.35 1.85 2.45 1.05 1.85 2.45 0.15 2.25 0.20

2022 Mar 0.25 0.45 2.05 2.65 1.20 2.05 2.65 0.15 2.35 0.30

Jun 0.50 0.70 2.20 2.80 1.40 2.20 2.80 0.15 2.50 0.30

Sep 0.75 1.00 2.50 3.10 1.65 2.50 3.10 0.15 2.75 0.35

Dec 1.00 1.25 2.75 3.35 1.90 2.75 3.35 0.15 3.00 0.35

2023 Mar 1.25 1.50 2.90 3.40 2.10 2.90 3.40 0.15 3.00 0.40

Exchange Rates (End Period)

USD Forecasts NZD Forecasts

NZD/USD AUD/USD EUR/USD GBP/USD USD/JPY NZD/USD NZD/AUD NZD/EUR NZD/GBP NZD/JPY TWI-17

Current 0.70 0.75 1.19 1.38 111 0.70 0.93 0.59 0.51 78.0 74.1

Sep-21 0.75 0.81 1.28 1.48 108 0.75 0.92 0.58 0.51 80.7 75.3

Dec-21 0.76 0.83 1.30 1.50 110 0.76 0.92 0.59 0.51 83.6 75.7

Mar-22 0.76 0.83 1.32 1.52 110 0.76 0.92 0.58 0.50 83.6 75.3

Jun-22 0.75 0.82 1.34 1.54 112 0.75 0.92 0.56 0.49 84.0 74.2

Sep-22 0.75 0.82 1.32 1.52 112 0.75 0.92 0.57 0.49 84.0 74.6

Dec-22 0.74 0.80 1.31 1.50 110 0.74 0.93 0.57 0.49 81.4 74.6

Mar-23 0.73 0.79 1.29 1.48 110 0.73 0.92 0.57 0.49 80.3 74.2

Jun-23 0.72 0.77 1.27 1.45 110 0.72 0.93 0.57 0.50 78.9 73.8

Sep-23 0.71 0.76 1.26 1.44 110 0.71 0.93 0.56 0.49 78.1 73.3

Dec-23 0.69 0.75 1.25 1.43 110 0.69 0.92 0.55 0.48 75.9 71.5

TWI Weights

13.3% 19.2% 10.5% 4.1% 6.4%

Source for all tables: Statistics NZ, Bloomberg, Reuters, RBNZ, BNZ

www.bnz.co.nz/research Page 9Markets Outlook 5 July 2021

Annual Forecasts

Forecasts March Years December Years

as at 5 July 2021 Actuals Forecasts Actuals Forecasts

2020 2021 2022 2023 2024 2019 2020 2021 2022 2023

GDP - annual average % change

Private Consumption 2.9 -0.7 9.6 3.3 2.0 3.6 -1.9 10.7 3.2 2.4

Government Consumption 6.1 6.3 4.5 1.8 1.3 5.4 6.4 5.3 2.2 1.2

Total Investment 1.3 -4.7 13.8 4.2 -0.6 3.2 -7.4 14.6 5.0 0.1

Stocks - ppts cont'n to growth -0.5 -0.2 0.8 -0.1 0.0 -0.7 -0.8 1.6 -0.3 0.0

GNE 2.5 -0.5 10.2 3.1 1.3 3.0 -2.5 11.9 3.1 1.6

Exports -0.3 -15.9 3.8 10.7 8.1 2.3 -11.8 -4.5 9.4 10.7

Imports 1.2 -16.2 16.4 9.6 5.4 2.2 -16.4 14.0 8.7 7.2

Real Expenditure GDP 2.1 -0.4 6.0 2.8 1.6 3.0 -1.2 6.2 2.9 2.0

GDP (production) 1.7 -2.3 5.6 3.0 1.6 2.4 -2.9 5.6 2.9 1.9

GDP - annual % change (q/q) 0.0 2.4 2.6 2.9 1.6 1.8 -0.8 3.7 3.1 1.3

Output Gap (ann avg, % dev) 1.6 -2.1 0.7 1.4 0.7 2.0 -2.2 0.6 1.2 0.9

Nominal Expenditure GDP - $bn 322 325 351 371 385 319 322 345 367 381

Prices and Employment - annual % change

CPI 2.5 1.5 2.7 2.2 2.7 1.9 1.4 3.3 1.7 2.6

Employment 2.6 0.3 1.7 2.0 1.1 1.2 0.8 1.8 2.3 0.9

Unemployment Rate % 4.3 4.7 4.1 3.8 4.4 4.1 4.9 4.3 3.6 4.4

Wages - ahote 3.7 3.0 3.3 3.0 2.7 4.3 2.6 4.6 2.4 3.1

Productivity (ann av %) -0.3 -2.9 4.2 0.9 0.5 0.5 -4.1 4.6 0.9 0.6

Unit Labour Costs (ann av %) 3.5 5.3 -0.4 2.4 2.3 2.5 6.9 -1.0 2.5 2.3

House Prices 7.8 20.7 9.6 2.3 2.0 4.6 15.5 17.2 2.8 2.0

External Balance

Current Account - $bn -9.1 -7.2 -14.1 -16.6 -15.0 -10.6 -2.4 -14.8 -17.5 -15.6

Current Account - % of GDP -2.8 -2.2 -4.1 -4.6 -4.0 -3.3 -0.8 -4.4 -4.9 -4.2

Government Accounts - June Yr, % of GDP

OBEGAL (core operating balance) -7.3 -2.8 -3.6 -0.9 0.3

Net Core Crown Debt (excl NZS Fund Assets) 26.3 34.0 43.0 48.0 48.0

Bond Programme - $bn (Treasury forecasts) 29.0 45.0 30.0 25.0 25.0

Bond Programme - % of GDP 9.0 13.8 8.6 6.7 6.5

(1)

Financial Variables

NZD/USD 0.60 0.71 0.76 0.73 0.69 0.66 0.71 0.76 0.74 0.69

USD/JPY 108 109 110 110 110 109 104 110 110 110

EUR/USD 1.11 1.19 1.32 1.29 1.25 1.11 1.22 1.30 1.31 1.25

NZD/AUD 0.97 0.93 0.92 0.92 0.92 0.96 0.94 0.92 0.93 0.92

NZD/GBP 0.49 0.51 0.50 0.49 0.48 0.50 0.53 0.51 0.49 0.48

NZD/EUR 0.55 0.60 0.58 0.57 0.55 0.59 0.58 0.59 0.57 0.55

NZD/YEN 65.1 77.5 83.6 80.3 75.9 72.0 73.6 83.6 81.4 75.9

TWI 68.9 74.8 75.3 74.2 71.5 72.8 74.3 75.7 74.6 71.5

Overnight Cash Rate (end qtr) 0.25 0.25 0.25 1.25 2.00 1.00 0.25 0.25 1.00 2.00

90-day Bank Bill Rate 0.71 0.33 0.45 1.50 2.15 1.23 0.26 0.35 1.25 2.15

5-year Govt Bond 0.80 1.00 2.05 2.90 3.00 1.25 0.40 1.85 2.75 3.00

10-year Govt Bond 1.15 1.75 2.65 3.40 3.50 1.60 0.90 2.45 3.35 3.50

2-year Swap 0.65 0.50 1.20 2.10 2.30 1.25 0.28 1.05 1.90 2.30

5-year Swap 0.80 1.15 2.05 2.75 3.00 1.40 0.49 1.85 2.75 3.00

US 10-year Bonds 0.90 1.60 2.35 3.00 3.00 1.85 0.90 2.25 3.00 3.00

NZ-US 10-year Spread 0.25 0.15 0.30 0.40 0.50 -0.25 0.00 0.20 0.35 0.50

(1)

Average for the last month in the quarter

Source for all tables: Statistics NZ, EcoWin, Bloomberg, Reuters, RBNZ, NZ Treasury, BNZ

www.bnz.co.nz/research Page 10Markets Outlook 5 July 2021

Key Upcoming Events

Forecast ... Median -- Last Forecast ... Median --- Last

Monday 5 July Wednesday 7 July

NZ, ANZ Comdty Prices (world), June +1.3% NZ, Working-age Population, Q2 4.1019m

Aus, Building Approvals, May -5.0% -8.6% NZ, Dairy Auction, GDT Price Index -1.3%

Aus, ANZ Job Ads, May +7.9% NZ, Merchandise Trade, To 30 June 2021

Aus, Retail Sales, May final +0.1% +0.1%P Euro, EU Commission Forecasts

Aus, Services PMI (Markit), Jun 2nd est 56.0 Germ, Industrial Production, May -1.0%

Aus, Inflation Gauge (Melbourne Institute), Jun +3.3% US, JOLTS Job Openings, May 9,313k 9,286k

China, Services PMI (Caixin), June 54.9 55.1 US, FOMC Minutes, 16 Jun meeting

Euro, PMI Services, Jun 2nd est 58.0 Thursday 8 July

UK, Markit/CIPS Services, June 2nd est 61.7 NZ, Employment Indicators, Weekly as at 5 July

US, Holiday (obs), Independence Day Jpn, Eco Watchers Survey, June (Outlook) 47.6

Tuesday 6 July Germ, Trade Balance, May +€15.5b

NZ, QSBO, Q2 -13 US, Jobless Claims, week ended 03/07 364k

Aus, RBA Policy Announcement 0.10% 0.10% 0.10% Friday 9 July

Jpn, Household Spending, May y/y (real) +13.0% NZ, ANZ Truckometer Index, June -4.8%

Euro, Retail Sales, May -3.1% China, CPI, June y/y +1.3% +1.3%

Germ, ZEW Sentiment, July 79.8 China, PPI, June y/y +8.7% +9.0%

Germ, Factory Orders, May -0.2% UK, Industrial Production, May -1.3%

US, ISM Non-Manuf, June 63.5 64.0 UK, Trade Balance, May -£0.9b

US, Markit PSI, June 2nd est 64.8 64.8 UK, GDP monthly, May +2.3%

US, Wholesale Trade Sales, May +0.8%

Historical Data

Today Week Ago Month Ago Year Ago Today Week Ago Month Ago Year Ago

CASH AND BANK BILLS SWAP RATES

Call 0.25 0.25 0.25 0.25 2 years 0.79 0.79 0.58 0.23

1mth 0.27 0.26 0.27 0.28 3 years 1.02 1.04 0.85 0.25

2mth 0.31 0.30 0.30 0.30 4 years 1.20 1.24 1.09 0.31

3mth 0.35 0.34 0.32 0.31 5 years 1.34 1.41 1.30 0.38

6mth 0.38 0.37 0.33 0.33 10 years 1.81 1.94 2.00 0.79

GOVERNMENT STOCK FOREIGN EXCHANGE

04/23 0.50 0.52 0.28 0.34 NZD/USD 0.7028 0.7034 0.7230 0.6555

04/25 0.91 0.95 0.78 0.48 NZD/AUD 0.9338 0.9303 0.9319 0.9400

04/27 1.20 1.27 1.21 0.68 NZD/JPY 78.00 77.84 79.00 70.37

04/29 1.48 1.59 1.58 0.86 NZD/EUR 0.5923 0.5901 0.5929 0.5796

05/31 1.70 1.83 1.85 1.00 NZD/GBP 0.5081 0.5068 0.5099 0.5247

04/33 1.88 2.01 2.06 1.09 NZD/CAD 0.8662 0.8684 0.8733 0.8875

04/37 2.21 2.34 2.39 1.31

05/41 2.51 2.64 2.70 TWI 74.1 74.1 75.0 72.4

GLOBAL CREDIT INDICES (ITRXX)

Nth America 5Y 47 48 50 71

Europe 5Y 46 46 49 61

www.bnz.co.nz/research Page 11Markets Outlook 5 July 2021 Contact Details BNZ Research Stephen Toplis Craig Ebert Doug Steel Jason Wong Nick Smyth Head of Research Senior Economist Senior Economist Senior Markets Strategist Senior Interest Rates Strategist +64 4 474 6905 +64 4 474 6799 +64 4 474 6923 +64 4 924 7652 +64 4 924 7653 Main Offices Wellington Auckland Christchurch Level 4, Spark Central 80 Queen Street 111 Cashel Street 42-52 Willis Street Private Bag 92208 Christchurch 8011 Private Bag 39806 Auckland 1142 New Zealand Wellington Mail Centre New Zealand Toll Free: 0800 854 854 Lower Hutt 5045 Toll Free: 0800 283 269 New Zealand Toll Free: 0800 283 269 National Australia Bank Ivan Colhoun Alan Oster Ray Attrill Skye Masters Global Head of Research Group Chief Economist Head of FX Strategy Head of Fixed Income Research +61 2 9237 1836 +61 3 8634 2927 +61 2 9237 1848 +61 2 9295 1196 Wellington New York Foreign Exchange +800 642 222 Foreign Exchange +1 212 916 9631 Fixed Income/Derivatives +800 283 269 Fixed Income/Derivatives +1 212 916 9677 Sydney Hong Kong Foreign Exchange +61 2 9295 1100 Foreign Exchange +85 2 2526 5891 Fixed Income/Derivatives +61 2 9295 1166 Fixed Income/Derivatives +85 2 2526 5891 London Foreign Exchange +44 20 7796 3091 Fixed Income/Derivatives +44 20 7796 4761 This document has been produced by Bank of New Zealand (BNZ). BNZ is a registered bank in New Zealand and is only authorised to offer products and services to customers in New Zealand. Analyst Disclaimer: The Information accurately reflects the personal views of the author(s) about the securities, issuers and other subject matters discussed, and is based upon sources reasonably believed to be reliable and accurate. The views of the author(s) do not necessarily reflect the views of the NAB Group. No part of the compensation of the author(s) was, is, or will be, directly or indirectly, related to any specific recommendations or views expressed. Research analysts responsible for this report receive compensation based upon, among other factors, the overall profitability of the Global Markets Division of NAB. NAB maintains an effective information barrier between the research analysts and its private side operations. Private side functions are physically segregated from the research analysts and have no control over their remuneration or budget. The research functions do not report directly or indirectly to any private side function. The Research analyst might have received help from the issuer subject in the research report. New Zealand: The information in this publication is provided for general information purposes only, and is a summary based on selective information which may not be complete for your purposes. This publication does not constitute any advice or recommendation with respect to any matter discussed in it, and its contents should not be relied on or used as a basis for entering into any products described in it. Bank of New Zealand recommends recipients seek independent advice prior to acting in relation to any of the matters discussed in this publication. Any statements as to past performance do not represent future performance, and no statements as to future matters are guaranteed to be accurate or reliable. Neither Bank of New Zealand nor any person involved in this publication accepts any liability for any loss or damage whatsoever which may directly or indirectly result from any advice, opinion, information, representation or omission, whether negligent or otherwise, contained in this publication. USA: If this document is distributed in the United States, such distribution is by nabSecurities, LLC. This document is not intended as an offer or solicitation for the purchase or sale of any securities, financial instrument or product or to provide financial services. It is not the intention of nabSecurities to create legal relations on the basis of information provided herein. www.bnz.co.nz/research Page 12

You can also read