Identifying Private Equity Opportunities in Indonesia, Vietnam and Thailand - Private Equity-Section AB - insead

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Identifying Private Equity Opportunities in Indonesia, Vietnam and Thailand Sponsored by: JL Capital Private Equity- Section AB Hill P., Matteo Ferrante, Neha Dodeja, Pratiksha Barasia, Uday Mehra (MBA Class of 2020 July)

⮚ Executive Summary

⮚ Opportunities in Fintech in Indonesia

⮚ Opportunities in Consumer Retail in Vietnam

⮚ Opportunities in Food Manufactoring in Thailand

2

Executive Summary

• JL Capital is looking to make its first investment in SEA by focusing on promising indsutries in specific

countries

• The shortlisted industries represent (i) easy to understand market dynamics and business models (ii) potential

JL Capital opportunities within the right ticket size (iii) underinvestment in the particular sector

• Fintech space is nascent but shows promise for a massive increase in TAM led by high TPV

• Payments is the entry point for consumers, paving the future for Lending; Fintech lending can bridge the gap

for unutilized financing capacity and access to credit in Indonesia

Indonesia • SME lending is attractive and presents opportunities for investment from JL Capital

• Consumer retail is a fast-growing investment space in Vietnam with strong sales growth

• E-commerce penetration is on the rise in Vietnam, however, retail players with offline presence are expected to

succeed in online channels

Vietnam • A potential investment target, market leader in baby retail, fits the relevant factors required for success

• Thailand is the kitchen of the world: Food processing contributes 23% of Thailand’s GDP

• Packaged food shows a strong demand forecast in APAC with a focus on ready meal in Thai market

Thailand • Recommend to target healthy ready meal, frozen fruits or halal food segment by local producers

3

Process

JL Capital to shortlist Deep-dive into Identify 1-2 potential

Identify 3-4 industries

3 industries based on selected industries to deals in total (only if

in target countries

interest and core understand growing possible, or else share

capabilities sub-sectors transcripts of

conversations)

First presentation to JL Second discussion to talk Final discussion to present

Capital about shortlisted industries final results and discuss next

steps

4

⮚ Executive Summary

⮚ Opportunities in Fintech in Indonesia

⮚ Opportunities in Consumer Retail in Vietnam

⮚ Opportunities in Food Manufactoring in Thailand

5

The Fintech space in Indonesia is nascent - but shows promise for a

massive increase in TAM led by high TPV1

E-Money is a small fraction of total electronic payments in Indonesia

Total Addressable Market (TAM) for the Fintech space in

Indonesia expected to grow by ~8x by 2025… 100%

90%

80%

US$ Bn 70%

8.15x 60%

50%

95.2

40%

30%

20%

10%

0% 1.8% 8.0%

10.4

2017 2018 2019 2020E 2021E 2022E 2023E 2024E 2025E

2019 2025E E-money Credit cards Debit cards

…mainly driven by 4 key consumer trends Fintech loans in Indonesia are only 0.2% of total outstanding loans

800 0.40

730

1• Massive promotional spend: Mostly by Fintechs, e-Commerce 700

690

0.35

625

platforms and ride-hailing (mostly Payments led) 600 560 580 595 570 0.30

• Rising smartphone penetration: Risen from 25% in 2014 to >60% in 500

2 500 0.25

2019 400

400 360 0.20

• Growing internet TAM: Driven by Indonesia’s young, hyper internet-

3 engaged population, increasing disposable incomes 300 0.15

• Burgeoning offline use cases: Rising Fintech adoption by shopping 200 0.10

4 malls, Co-funding by merchants 100 0.05

0 0.00

Dec-18 Jan-19 Feb-19 Mar-19 Apr-19 May-19 Jun-19 Jul-19 Aug-19 Sep-19

Fintech loans outstanding (US$ Mn) Fintech loans as % of total IDR loans

Notes: (1) Total Payment Volume 6

Sources: OJK, Goldman Sachs Global Investment Research, Bank Indonesia, Macquarie Research

Payments is the entry point for consumers, paving the future for Lending

Traditional Fintech service adoption cycle by

consumers

Payments & Transactions Lending Financial Products

41 companies hold an e-Money license (as on Feb’20) 164 lending companies registered with OJK (Dec’19) E-commerce platforms are main players

x Highly concentrated market: Top 4-5 players ✔ Fragmented market landscape: No clear ~ Small market: Very small market size and

control >90% of transaction market share; market leader; Long tail of companies own >1% growth due to low capital market penetration

High-ticket investments will be required to enter of total loan share and financial literacy

the market

✔ Under-penetrated market: Fintech loans in x Low interest-generating business models:

Evolving regulatory landscape: Bank Indonesia are only 0.2% of total outstanding In a typical Fintech lifecycle, value is generated

~ Indonesia has launched QRIS to unify QR code loans through Payments & Lending first; Indonesia is

based cashless payments; Reduces barriers to not at a stage to generate meaningful returns

entry for new players Unaddressable market by traditional banks: from Financial Products

✔ Fintechs lending to SMEs are targeting invoice

Significant growth potential: Only 1.8%1 of financing; Traditional banks have lengthy credit Consumer behaviour not shifting: This

✔ electronic payments in Indonesia happen approval processes for this segment ~ sector is primarily dominated by banks in

through e-Money; ~8% e-Money transactions Indonesia; Despite e-commerce platforms, no

expected by 2025 shift seen in consumer behaviour

Notes: (1) 2019 estimates by Bank Indonesia 7

Sources: Goldman Sachs Global Investment Research, Bank Indonesia, Macquarie Research

Fintech lending can bridge the gap for unutilized financing capacity and

access to credit in Indonesia

Low percentage of loan disbursements to GDP1 indicate an Majority of SMEs, middle & lower income individuals still

unutilized financing capacity in Indonesia do not have access to credit in Indonesia2

Australia 122% Total MSMEs Total Individuals

63 Mn 186 Mn

South Korea 94%

New Zealand 92%

Thailand 78%

74% 71%

USA 78%

Japan 57%

China 49%

Low percentage of Debt wrt GDP is directly

26% 29%

Indonesia 17% attributed to lower access to credit for

SMEs and low/middle income individuals

India 11% MSMEs Middle/Lower Income

Individuals

Have access to credit No access to credit

Notes: (1) Ratio taken based on 2017 figures (2) As of 2018 end 8

Sources: International Monetary Fund, Asian Development Bank, Central Bureau of Statistics (ID), Ministry of Cooperative and MSME (ID), Central Bank of Indonesia, PwC

SME lending is an attractive business model generating higher

financing rates than traditional banks

Fintech lending market

in Indonesia

Short-term consumer loans P2P loans targeted at SMEs P2P microfinance

Avg. ticket size ($): 70 Avg. ticket size ($): 140,000 Avg. ticket size ($): 200-350

Avg. loan tenure: 1-3 months Avg. loan tenure: 0.5-6 months Avg. loan tenure: 3 months

Major players: Major players: Major players:

Platform1

• Major product offered by SME Outstanding credit (IDR Bn) 234 529 267

lenders is Invoice Financing Total credit underwritten (IDR Bn) 1,163 2,940 2,430

extending credit for up to 80% of

the receivable value. NPLs2 1.05% 2.30% 8.0%

• Traditional banks can’t engage in Active borrowers 1,776 1,193 15,436

this business due to lengthy credit Invoice financing rates (p. a.) 13-43% 12-20% 12-26%

approval processes, so they have

Borrower upfront fee 3-5% 3-5% 3%

started acquiring minority stakes

in SME lending platforms Banks having a minority stake -

Notes: (1) Numbers as of November 2019 (2) NPLs: Non-performing loans 9

Sources: OJK, Bank Indonesia, Macquarie Research, Company Reports

Only a handful of venture deals have taken place within the Fintech

SME lending space in Indonesia over the last 5 years

Mar’20: $23.5 Mn (C) Jun’19: $12 Mn (B) Feb’20: $10 Mn (B) Sep’19: $8.6 Mn (A)

Nov’19: $1 Mn (B) Aug’19: $10 Mn (B) Dec’18: $0.2 Mn (S)

Aug’18: $16.5 Mn (A)

Potential investment option1

Nov’18: $4.3 Mn (A) Apr’16: $1.2 Mn (S) Sep’19: $1 Mn (S)

Notes: (1) Investment recommendation based on industry, competitor and company analysis (not including financials) 10

Sources: PrequinModalku: A potential investment option in Indonesia for JL Capital

Indonesia Singapore, Malaysia

Present as

Dec’19: Undisclosed amount of Debt funding Apr’20: $40 Mn (C) by existing investors and

by Triodos Microfinance Fund, Triodos Fair an undisclosed bank

Share Fund Funding Rounds Apr’18: $25 Mn (B) led by SoftBank

Apr’16: $1.2 Mn (S) led by Alpha JWC Ventures, Sequoia India, Alpha JWC

Ventures and Singapore Press Holdings Ventures, Golden Gate Ventures

$900 Mn Total amount disbursed1 $948 Mn

52% loans greater than $10,000 Biggest ticket size segment 51% loans less than $11,000

8.0%3 Current default rate 3.36%

• Modalku is one of the 3 leading Fintech lending providers for SMEs in Indonesia, however it has not raised an equity round since 2016

• Modalku’s 2 main competitors – Investree and KoinWorks – have raised fresh funding in the last 1 year to increase their geographic

footprint in Indonesia and for expansion to other Southeast Asian countries

• Modalku raised debt in 2019, showing promise of using Leverage to boost Equity returns for the company’s business model

• Comparison of both geographies shows that Modalku will require an influx of capital in Indonesia to improve its infrastructure for bringing

down default rates and expanding its geographic reach in Indonesia

Notes: (1) As of Q2 2020 (Ongoing – Figures for 19 Apr 2020) (2) As percentage of overall loans disbursed (3) As per Macquarie Research 11

Sources: Modalku website, Funding Societies websiteExpanding the coverage for Indonesia’s “Credit Invisible” requires a tailored and innovative approach

1 • Since 2018, 70% of borrowers have been SMEs/individuals that had no prior credit access

• As Java gets saturated, innovation is required to reach out to SMEs outside of Java, and in sectors currently untapped

Credit worthiness verification is essential before NLPs start blowing up

2 • Debt refinancing is one of the top 3 loan purposes, indicating a potential “over-leveraged” debt behaviour

Things to • This behaviour might be more prevalent in conventional-to-online rather than purely online borrowers

keep in mind

before Important to monitor TKB901 along with NLPs for developing sustainable business models

• OJK is currently implementing TKB90 to ensure players disclose their loan performance

investing in 3 • This is an important measure to track irresponsible disbursement, and Fintechs should adapt their

the Fintech business models based on TKB90 metrics as well

Lending

space in Fintechs will need to collaborate with financial institutions for stable financing

4 • By collaborating with financial institutions, Fintechs will have a more stable source of funds

Indonesia • This also allows them to have wider use-cases within their loan portfolio

Indonesia’s Fintech Lending ecosystem is similar, but not comparable, to other countries

• Majority of underserved SMEs not only have limited data but also limited physical access to due Indonesia’s

5 topography

• Replicating business models of other countries will be ineffective compared to targeted business models

Notes: (1) TKB90 is a metric measuring debt repayment success rate over 90 days past due, the opposite of a Non-Performing Loan 12

Sources: Desktop Research⮚ Executive Summary

⮚ Opportunities in Fintech in Indonesia

⮚ Opportunities in Consumer Retail in Vietnam

⮚ Opportunities in Food Manufactoring in Thailand

13Consumer retail is a fast-growing investment space in Vietnam with

strong sales growth

Vietnamese retail sales growth remain robust through-out …underpinned by 4 key macroeconomic trends in the

economic cycles… country

Retail revenue and growth in Vietnam (2013-2020),

Revenue, USD Billion ; Growth, % 1• Strong economic growth: Vietnam’s GDP has

been increasing at 7% due to strong harvest and

surging manufacturing sector

180

180 30

27%

160

142 25 2• Rapid growth in consumer spending with higher

140

disposable income: Private consumption is 68% of

126 the overall GDP, highest in SEA, with a growing

120 115 20

103 middle class and heightened concerns about

100 85 94 hygiene and food safety

13% 13% 15

80 11% 11% 3

10% 10%

60 10 • Increase in foreign investment: 40% of

supermarkets currently owned by foreign investors

40

5 due encouragement by govt policies

20

4

0 0 • Free-trade agreements: Better FTAs and bilateral

2013 2014 2015 2016 2017 2018 2020

agreements have made international food

accessible to middle-classes

Notes: (1) Total Payment Volume 14

Sources: OJK, Goldman Sachs Global Investment Research, Bank Indonesia, Macquarie Research; Vietnam General Statistics OfficeVietnam’s modern grocery market is expected to grow at 25.8% p.a. over

the next 5 years, with a potential for further growth

Grocery is the largest retail category by value, fastest growing Modern segment grocery penetration is expected to grow as

in the SEA region GDP per capita increases

Breakdown of Vietnam retail market, %, 2018, 100% = USD 108 Bn

Other Modern grocery size, 40

Non-store USD bn, 2018

s 35

Apparel &retail

Footwear 6%

2% 30 Thailand

Leisure 5%

Goods 25

6%

Grocer

20 Indonesia

Health & Beauty 9% 44% y 15 Philippines

10 Malaysi

Vietna

5 a

m

Home & 11% 0

Garden 0 5 10 15 20 25 30 35

17% Modern grocery Growth

Electronic & 2018-2013 CAGR %

Appliances

• Vietnam is fast-growing retail market with grocery as the largest • Vietnam’s modern trade penetration is currently at 8% which is lowest

segment making up 44% of overall market amongst the SEA countries

• There are 4 key factors for this trend: • The market is on the verge of significant modernization and is likely to

1. Increased urbanisation coupled with increased awareness follow the S-curve of other developed Asian markets

2. Consolidation of top players (Satra acquired Auchan) • As GDP per capita rises, modern grocery retail market is expected to

3. Entry of international players like 7-eleven, Big C grow from $4 bn to $20 bn by 2025 (5X growth)

Sources: Deloitte report: Retail in Vietnam, Feb 2019; McKinsey report: Seizing the fast-growing retail opportunity in Vietnam, Sept 2019

15Consumer markets in Vietnam are still fragmented and there is ample

room for modern trade channels

Accelerating value contribution from modern trade channel... ...with smaller format leading the modern retail chain

emergence recently

Distribution of the retail sales from between Modern retail channels Average monthly shopping frequency of Vietnamese of modern trade

and traditional channels, %

25.2

2010

18.2 2018

25%

32%

45%

8.9 9.5

4.5 3.3 2.5

1.3 2.2 0.8 1.2

0.0

Wet market Traditional Convenient Minimarts Personal Supermarkets

Grocery Stores Case/ Drug

75% Stores Stores

68%

55%

2015 2017 2020

Modern Retail Tradtional

Channels Channels

Sources: Vietnam's Distribution and Retail Channels 2018 by EVBN; Nielsen, VCSC 2018 16There are six success factors that stand out as keys to making the most

of retail opportunities in Vietnam

Retail leaders exhibit 6 key success factors

▪ Ability to grow dense network of smaller stores in urban

areas Retail players are

1 Network and scale ▪ Require access to funding and dedicated team finding right

locations facing growing

competition from

Compelling value ▪ Successful retailers differentiate themselves by focusing on both local and

2

propositions

specific dimensions like price, assortment, experience etc. international

players.

Strong business ▪ Develop capabilities to tackle payment solutions, logistics,

3 proprietary products and loyalty programs Leveraging lessons

enablers

in innovative

▪ Strengthen brand equity through marketing and build loyal technologies and

4 Strong brand equity customer base

more advanced

▪ Local players have advantage over foreign

markets, players

▪ Extensive on-the-ground experience can achieve

5 Local knowledge ▪ Understand local tastes, rules and regulations and trends success

Innovation and ▪ Provide both offline and online channels to serve customers

6 ▪ Innovation into smart stores

omnichannel platforms

Sources: McKinsey report: Seizing the fast-growing retail opportunity in Vietnam, Sept 2019 17E-commerce penetration is on the rise in Vietnam, however, retail players

are diversifying to tap the entire ecosystem

Online retail sales make up only 5% of total online sales, Retail players are pursuing omnichannel strategy to capture

however it likely to grow with increase mobile penetration the market share in online

Online B2C sales vs online retail sales (2012-2020), Example 1:

Sales, USD Billion ; % total online sales

20 Online B2C sales 8 ▪ Korean supermarket chain, LOTTE Mart

Online retail launched SPEED LOTTE mobile app to

sales 7

combine traditional and online retail

15 6 ▪ The online version has more than 1000

5.0%

5 SKUs and delivers within 15kms

3.6% 10.0

10 4

2.8% 3.0%

6.2 3

1.8% 2.1% 5.0 Example 2:

5 0.7 4.1 2

2.2 3.0

0.7% 1

0 0 ▪ Bach Hoa XANH has 1000+ retail stores

2012 2013 2014 2015 2016 2017 2020 and has moved online with over 600

• Vietnam’s e-commerce industry is one of the fastest growing in the SKUs

region, growing at 27% CAGR ▪ Parent company Mobile World has

• E-commerce sector however is still in its early days with many players announced $43m investment to grow

operating at a loss the business

• Key success factors include overcoming logistics challenges and e-

payment solutions

Sources: Deloitte retail survey (2018) 18Vietnam Consumer Retail: Recent PE &VC Investment

Date Targets Acquirer ($US) Stake

Growth 2017 Vua Nem (Mattress company) Mekong Capital $6 mn. 57.5%

Stages 2019 VinGroup GIC Singapore $500 mn.

Investments

2008 Maison Mekong Capital $ 5mn.

IPO Notable acquisitions

Date Targets Acquirer ($US)

MM Mega Market Big C EUR 655

2016

Vietnam Supercenter mn.

Exits 2013 Ichiban Co. Berli Jucker $73 mn.

2014 VinMart VinGroup $12 mn.

Mobile World

2017 An Khang Pharmacy

Investment

Sources: Tracxn June 2018 & CB Insights Jan 19 19Vietnam has seen exits to IPO from previous VC/PE backed deals

Business Description:

• Established in 1988, PNJ is the leading

jewelry manufacturer and retail in Vietnam

Year: 2007

Investor: Mekong and Reasons to invest:

Vina Capital • Increasing revenues: Revenues from retail

Amount: USD 8mn. jewelry store continuing to increase 28% YoY;

retail network grown from 330 to 370 in 2019

Growth envisioned from: • Large customer base: Large number of

(i) Revenue Growth customers over the last 30 years with high PNJ retail network

(ii) Margin improvement 370

switching costs for jewelry purchases

324

• Growing market: Jewelry retail sales likely to

Exits seen: grow as consumers rely on trusted brands 269

Mekong was able to • Established reputation in the jewelry 219

liquidate the investment business: Having been established 30 years 189

after 9 years with a gross back, PNJ has the reputation of being the

return multiple of 2.2x country’s leading jewelry brand with high-

quality, sophisticated products

• Continuous innovation: PNJ has been

continuously adapting to consumer trends and 2015 2016 2017 2018 2019

launching new collections

Sources: Pitchbook 20Citimart, a supermarket chain, was acquired by Aeon with the aim of

increasing to 500 stores by 2025

Business Description:

Year: 2015 • The company engages in operating

Investor: Aeon Company supermarket chains and offers groceries,

Amount: 49% acquired food products, clothes, housewares and other

products to its customers throughout Vietnam

Growth envisioned from:

(i) Revenue growth Reasons to invest:

(ii) Profitability increase • Significant room for revenue growth: Aeon

Citimart Revenue

will assist Citimart in building the new brand

Exit: and controlling product quality in the hopes of

(i) Acquisition by Aeon increasing the number of Aeon Citimart +15%

69

Group, one of the stores to 500 by 2025, which will have about 60

largest retailing groups 10,000 products

(ii) Similar supermarket • Increase in profitability: As supply chain

chains have a good improve and economies of scale kick-in, likely

chance being acquired to see increase in margins

by a larger company • Increase in customer loyalty: Customers

that is looking to likely to increase their loyalty to branded

increase its presence stores where they can find quality and

reasonable products 2015 2016

Sources: Pitchbook; DealstreetAsia, Desktop research, Mekong Capital presentation 21Pharmacity can expect increased profitability with investors seeing an

exit to another PE firm or straight as an IPO

Business Description: Number of stores

• Founded by 3 young entrepreneurs,

Pharmacity originally operated a chain of

Year: 2019 and 2020 pharmacy stores; expanded its store

Investor: Mekong and assortment to include health & beauty

undisclosed investors products from 2016

Amount: USD 30mn. • Currently, largest pharmacy retail chain in

Vietnam in terms of number of stores.

Growth envisioned from:

(i) Revenue Growth Reasons to invest:

(ii) Margin improvement • Increase in customer loyalty: Customer

(iii) Multiple expansion shopping from branded retail stores Number of customer loyalty card

might exist for those • Steady increase in number of stores: holders

that invested early- Pharmacity will expand from 1,000 stores by 1,660,000

stage in select 2021 and over 1,700 stores by 2025

companies • Improvement in store level profitability:

Average basket size has been increasing by

Exits envisioned: 14.8% CAGR from 2018-2025 and

(i) Sell to a late stage • Same store sales: Continuous growth in

VC/ PE firm average transaction/store/month by 5.4% 30,000

(ii) IPO CAGR

2017 2019

Sources: Pitchbook; DealstreetAsia, desktop research, Mekong Capital presentation 22BIBO MART, market leader in baby retail is identified as a potential

investment target in Vietnam

Bibo Mart is the market leader in baby stores in Vietnam with a BiBo Mart clearly satisfies all the success factors

large retail footprint and growth potential outlined that make it a solid potential target

Network and scale: Rapid growth with largest

number of stores in baby retail

Compelling value proposition: Speciality store

Name: Bibo Mart

for mom and baby products with only 1

international competitor

Description: Largest retail chain for mom and

baby products in Vietnam Strong business enablers: Strong partnerships

with international brands including Bubs Australia

Established in: 2006

Strong brand equity: Number 1 company in

Number of stores: 140 (as of Jan 19), across 22

Vietnam for selling high quality, branded products

cities, 15K SKUs

Valuation: $140 mn. (as of 2018) Local knowledge: Founder and CEO, Mrs Trinh Lan

Phuong has built company on local consumer trends

Investors: 80% owned by founder, 20%

investment from ACA Omnichannel platforms: Online platform, with call

centre to support online customers

Recommend to pursue Bibo Mart as a potential investment for JL Capital

Sources: Pitchbook; DealstreetAsia, Desktop research 23⮚ Executive Summary

⮚ Opportunities in Fintech in Indonesia

⮚ Opportunities in Consumer Retail in Vietnam

⮚ Opportunities in Food Manufactoring in Thailand

24Thailand is the kitchen of the world: Food processing contributes 23%

of Thailand’s GDP

Minimally processed Moderately processed Highly processed

Agricultural meat and seafood Canned and freeze-dried Packaged food (ingredients,

produces snacks and meals)

• Ranked 2nd largest exporter of

rice and sugar in the world • 1st as exporter of canned tuna • 6th food seasoning exporter and

• Top 5 for chicken and shrimp and canned pineapple 1st in Southeast Asia

exports • 11th ready meal exporter in the

• Major exporter of other seafood world, accounting for a 3.7%

products

Major players include both domestic and international conglomerates:

Sources: Thailand Board of Investment 25Packaged food shows a strong demand forecast in APAC with a focus

on ready meal in Thai market

Packaged food outperformed global market in Packaged food is expected to continue

APAC and Thailand outperforming global market

(Historical Growth 2015 to 2019) (Forecast growth 2020 to 2024)

In 2019, Ready meal

10.8%

sales was $613M in 9.8%

Thailand and $3B in

APAC

4.8%

3.4% 3.3% 3.6% 3.8%

2.9%

2.5% 2.3% 2.4%

1.5%

World APAC Thailand World APAC Thailand

Packaged Food Ready meal

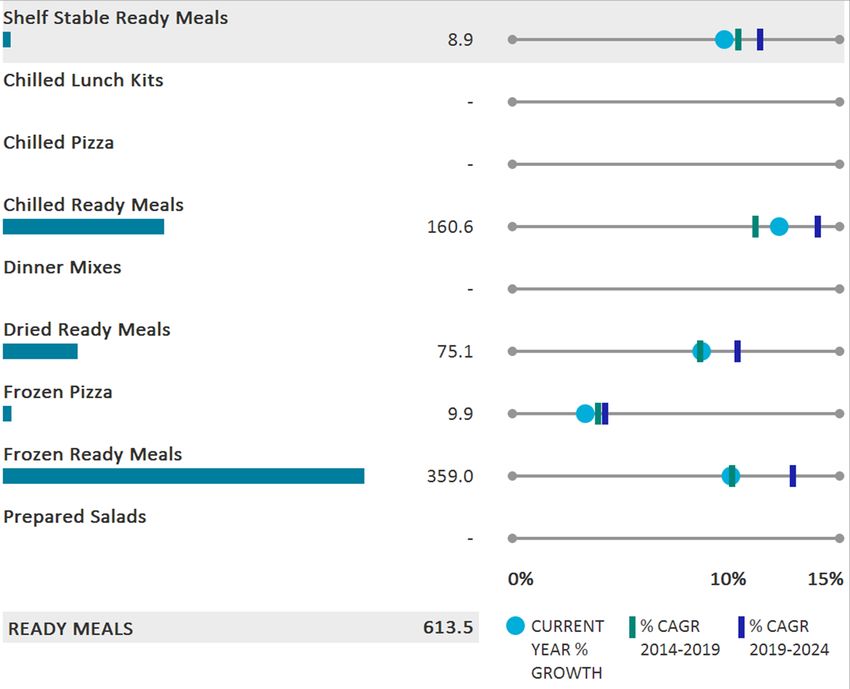

Sources: Euromonitor, Thai National Food Institute 26In 2019, market for packaged food in Thailand reached $14B, with ready

meals as the fastest growing sector

Dairy is the largest category, followed by rice, pasta and Ready meal shows the highest forecasted growth

noodle through 2024

Rice, Pasta Edible Oils Annual Consumption Growth from 2020 to 2024 (%)

and Noodles Ready Meals

Processed Sauces,

Meat and Dressings

Seafood and 12.0% 10.8%

Processed Condiments

Fruit and 10.0%

Vegetables Soup

8.0% 7.4%

Breakfast

Cereals Sweet

Spreads 6.0% 5.3%

Baked 4.8% 4.8%

Goods Baby Food 3.5% 3.8%

4.0% 3.0% 3.0% 2.8% 2.9%

2.5% 2.7%

1.8% 1.4%

Sweet 2.0%

Snacks 0.2%

0.0%

Savoury

Snacks

Ice Cream

and Frozen Dairy

Desserts Confectioner 25%

y

Sources: Euromonitor, Thai National Food Institute 27Packaged food industry is highly developed in Thailand with Frozen and

Chilled meals accounting for ~500m USD in sales in 2019

Frozen Ready Meal has the largest sales while Chilled Ready Four key trends explain the fast growth of Ready Meal

Meal is growing the fastest at 14.7% CAGR industry in Thailand

Sales of Ready Meals in Thailand by Category

Retail Value RSP – USD million 1• Rising middle- and upper-income consumers seek convenience

premium meal options that are both healthy and hygienic

• Both frozen and chilled ready meal is taking more market share

from instant noodles as consumers reach for more exotic

flavours and healthier options

2• Consumers seek fresher ingredients and less MSG in their meal

• Organic fruit and vegetable is still a niche segment but is growing

quickly

• Produces can also command 2x to 3x in price

3• Ready meal serving aging population present an untapped growth

opportunity

• CPRAM target elderly segment and hospital patients with easy to

chew meals such as boiled pork rice with low sodium

4• Halal meal export market also present a significant growth

opportunity

• Global market estimated to worth $1.6T in 2018 (16% of total

global food industry)

• In Thailand, there are more than 8,000 factories and over

150,000 products that received halal certification

Sources: Euromonitor, Thai National Food Institute 28Thailand Packaged Food Manufacturing: Recent PE & VC Investments

Date Targets Acquirer ($US) Stake

09-09-2019 Srithai Daily Foods Navis Capital Partners N/A N/A (Minority)

Minority

Dusit Thani PCL

Investments 03-02-2018 NR Instant Produce Co Ltd $21,06M 25,98%

09-08-2011 S&P Syndicate PCL Minor International PCL (MINT) $11.51M 5.04%

IPOs Valuation Notable acquisitions

Date Targets Acquirer ($US)

Thai Foods

Exits 17-06-2019

Group

$9.26M

$40.16m raised $4.8m raised

corresponding corresponding

to 26.09% of to 20% of Nippon Pack

equity equity 21-07-2016 $2.5M

PCL

Sources: Euromonitor, Pitchbook 29Recommend to target healthy ready meal, frozen fruits or halal food

segment by local producers

Ride the domestic ready meal boom

⮚ Seek small to medium sized manufacture catering to premium urban consumers

⮚ Products offering should focus on premium healthy ingredient that are low in MSG

▪ It is important to identify point of differentiation from market leader such as CP, who offers various selections of

ready meal through a strong network of owned convenience stores (7-eleven)

⮚ Consider alternative channels to serve consumers

▪ Several “clean food” players utilize deliver directly to home and offices

▪ Alternatively vending machine at residential condominium is an emerging route to reach young urban consumers

Focus on businesses that export halal, fruits and ingredients to APAC

⮚ Help halal certified manufacturers expand their export market and geography

⮚ Identify processed fruits business with strong distribution partners in China and domestic supply chain with

growers

▪ Differentiate produce through different processes such as freeze drying, baking or steamed sulfuring

▪ Mango, durian, mangosteen and coconut are the primary exports to China

⮚ Identify manufacturer of ingredients such as seasonings and condiments that are in demand in APAC

• Thailand has significant cost advantages as raw materials such as sugar, chilies and spices are locally produced

Sources: Euromonitor, Desktop research 30Potential target: JM Food, a major frozen and chilled ready meal

provider captures both domestic and export market

JM Food provides ready-to-eat Thai meal and ingredients including chilled and frozen meals & fruits, stir-fried

kits, sauce, and bakery. The company also offers food catering services and operates food court stalls

Product selection: Diverse product selections

that include chilled and frozen meal and fruits.

Potential to increase selection of healthy options

Certification and safety standard: Facilities are

Name: JM Food Industry Halal and HACCP certified; FDA registered

Business line :

Distribution network: Strong domestic

1) Manufacturer of chilled and frozen meal

distribution through large discount supermarket.

2) Provide catering services to event and banquet

Well known OEM capability for importers. Potential

3) Operate food stalls (food court)

to leverage owned-brand for exports and direct

distribution to local urban consumers

Market: Export 20%/ Domestic 80%

Market potential : JM Food can leverage the

Established in: 1982 strong growth trend of domestic healthy meal and

international demand of halal food

Sources: JMFthailand.com; Bangkokcompanies 31Backup

32Manufacturing is seeing recent growth given global trade wars; Large

retail stores are stealing market share from traditional stores

1 2

Manufacturing Large retail stores

Macro factors: Macro factors:

• Improvement logistics and real estate; increase consumption • Rapid urbanization; rapid growth of middle-class population

due to growing middle class • Wtinessing 11% growth since 2016; ranked 6th best destination

• Given current trade wars with China, increased emphasis on for retail investment

manufacturing locally for value-added products • Heightened concern factors for food safety and hygiene

• International companies (e.g. Samsung) shifting to Vietnam for • 75% still owned by mom and pop stores – ripe opportunity for

manufacturing to diversify supply chains growth of chains

Business model factors:

Business model factors:

• High investment multiples in the retail (MobileWorld divested

• Risks: Finding qualified professionals to work in the

for a 57x return)

manufacturing space

• Risks: Uncerntainity of government regulations impacts import

of food; US products still expensive to middle class HHs because

high high import duties

Past deals: Past deals:

• 2019: VinaCapital Group (USD 21.4 mn.) invested in Ngoc • 2008: Mekong and Vina Capital (USD 8 mn.) invested in Phu

Nghia Industry Nhuan Jewelry

• 2016: AIF Capital (USD 15mn.) invested in Rochdale Spears • 2019 and 2020: Mekong and undisclosed investors (USD 30 mn.)

• 2016: Stellus Capital Management (USD 6 mn.) invested in T.F invested in Pharmacity

Hudgins • 2019: GIZ (USD 500 mn.) invested in WinGroup

33Education and logistics are growing segments in Vietnam given the high

rate of urbanization and shift to middle class

3 4

Logistics Education

Macro factors: Macro factors:

• E-commerce is growing rapidly and being dominated by • 3rd largest young population; rapid urbanization; 41% population less

international players allowing for local companies to help with than 24 years old ‘golden demographic’

logistics • Rising middle class who desire to send kids to international school; new

• E-commerce logistics and the industry expected to reach an average decree accepts 50% locals in international schools

growth of 42 percent every year until 2022 • Strong desire to excel in the English language

• Logistics accounts for 18% of GDP (higher than most countries) with • State-owned universities and colleges only have capacity for 600,000 of

scope for improvement the 1.8 million candidates who undertake the national university

Business model factors: entrance examination

• 100% foreign owned logistics company not allowed under the laws Business model factors:

of Vietnam giving room to local players • Lean and capital efficient business models for some of the more

• 75% of e-commerce happening in two ciites allowing for focused innovative education platforms

logistics opportuniteis • Raised investment level for foreign investors decreasing compeititon of

• A series of M&A deals in the logistics industry took place in 2019 investors

reflecting consolidation in the industry • Focus areas: International schools, private schools, testing centres,

• Risks: Primairly cash-based economy limiting use of online logistics online education platforms

platform; • Risks: High taxation; complicated entry barriers for investors

Past deals: Past PE deals:

• 2016: Mekong invested in ABA Cooltrans • 2017 and 2019: Mekong (USD 4.9 mn.) and Kaizen (USD 10 mn.)

• 2016: Bravia Capital invested in Bac Ky Logistics invested in Yola

• 2017: Mekong invested in Nhat Tin Logistics • 2017: LBO by TPG in Vietnam Australia International School

• 2019: Navis Capital buyout of Than Than Cong education platform

34Opportunity for Thai food manufacturer to serve the growing Asia Market;

Rising middle class and tourists drive F&B demands

1 2

Manufacturing (especially in food) Food & Beverage & Hotels

Macro factors: Macro factors:

• Rich natural resoruces and raw material (80% of raw material • Tourism has been the fastest growing sector with revenue from

is locally produced) forist tourist representing a CAGR of 16.5% from 2009 to 2018

• Supportive skileld labor resource • Food Retail has experienced a tremendous growth

• $45B governemnt investment in Eastern Economic Cooridor.

$15B is dedicated to transforming manufacturing industries • Large active corporate accquirers such as Thai Beverage and

Minor international

Business model factors: Business model factors:

• Producing of healthy, functional (eg high-fiber) or specialty food • Tap into rising urban consumer spending power: upper end

(halal) coffeeshop and restaurants, driven by western food trend

• Production of high valued added food such as organic fruits,

dried/frozen fruits

• Target facilitates for foreign food corporates for expansion in SE

Past deals:

Asia.

• 2019: Bonchon (Chicken Time) was acquired by Minor

International for $63 M

• 2019: Santa Fe Steakhouse was aqquired by Boonrawd Brewerly

Past deals: for $50 M

• 2019: BTM Thailand was acquired by Breaktalk for $5.14M • 2019: MK Restaurant Group acquired in early September a 65%

• 2018 Mighty International was acquired by Frutarom stake in Laem Charoen Seafood for ~700M

Industries for $20M to expand capabilities in Asia • 2017: Express Food (Restaurant operator) received $15M from

• Other startup:… Lombard capital (PE firm)

• Other startup: Hungry Hub (A), Happy Fresh(C) ,Eatigo (B) 35Internet-based businesses have the highest potential in Indonesia,

market not saturated yet

1 2

Fintech lending (specifically B2B) Online Gaming (specifically mobile)

Macro factors: Macro factors:

• E-Payments market has grown at 15-20x over last 5 years • Increasing time spent by people on social media

• CC penetration is quite low • Rising internet penetration outside of Java

• Regulatory environment is becoming more favorable

Business model factors: Business model factors:

• Fintech loans are quite low in terms of overall transaction volume • Content/development side of gaming has high potential; high

• Fintech ecosystem is broken for B2B – not many lenders margins

• Small gaming revenue relative to population, low penetration

Past deals: Past deals:

• 4 major players exist in the e-money space right now: Ovo, • xx

Gopay, Dana, Linkaja. ShopeePay is emerging as the 5th player

• 100+ Fintech players for B2B lending, no clear leader

36You can also read