Media Industry Accounting Group Annual conference 2017 - www.pwc.com/miag

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

www.pwc.com/miag

Media Industry

Accounting Group

Annual conference 2017

London

15 June 2017

Global entertainment and

media outlook 2017-2021

Phil Stokes

PwC UK

E: phil.stokes@pwc.com

PwC

Never Before

HAS CHANGE OCCURRED IN SUCH

SHORT PERIODS OF TIME.

PwC

Disruptive forces are

rapidly reshaping our world.

Five inescapable world trends are acting together and driving change.

Right now

Demographic Shift in global Accelerating Resource scarcity Technological

shifts economic power urbanisation and climate change advances

PwC 4

Disruptive forces are

rapidly reshaping our businesses.

Organizations must take actions now to prepare for the disruptive opportunities and

evolving platforms of the next few years.

Right now

Technology forces Societal Forces Regulatory Forces

Smart Device Proliferation and Consumerisation and Privacy and

Ubiquitous Connectivity Always On expectations Shifting Regulatory Landscape

PwC 5

The world is in beta.

Technologies, trends, markets and economies

are in a constant state of flux.

Right now

Competitive advantage is It is no longer about long- Organizations must have This may mean setting up

transient term strategies to sustain the agility, empowerment, new businesses and

a competitive advantage and the confidence to allowing outdated versions

PwC change to die

The business environment

is ripe for the disruptors.

Disruptors see the future, build scalable platforms, and experiment restlessly and boldly.

Right now

Disruptors do not More importantly, they They have an insatiable They see the future,

respect incumbent or are not held back by those focus on the customer build scalable

classical organizational structures platforms, and

structures

PwC experiment relentlessly

7

Organisations must innovate today.

Leaders who do not listen to their stakeholders and change will be

passed by as their markets and customers move without them.

Right now

Customers are Organisations can Market dominance can Siloed decision Innovation will drive

digital generate deeper insights quickly be lost to new making is a signal of success

than ever before entrants impending failure

PwC 8

From 2017 a new breed of customer will dominate - the Digital Natives

Enabling total customer centric business models

Digital now enables businesses to compete on the basis

of helping customers achieve their desired outcomes.There is an increasing need to build digital trust

The new trust dynamic: trust + opportunity = growth

OpportunityA roadmap for the biggest business challenges

Know Define Evolve Create Accelerate Protect

The new core competencies required to survive and thrive in the digital age

Know Define Evolve Create Accelerate Protect

your your your total sustainable time to market your assets from

customers , business business in value for through smart, the threats of

markets and strategy for response to customers and sustainable the digital age

ecosystem the digital digital shareholders delivery to build

age disruption through models stakeholder

innovation trustIn a world that’s in Beta…

…we believe successful companies

need to focus on three major

imperatives…

Trust

Speed and Agility

Constant Innovation

Global E&M Outlook 2017-2021For Entertainment & Media companies this translates

into three specific themes

Develop seamless consumer

relationships across

distribution channels

Put mobile (and increasingly video)

at the centre

Innovate around the product and

user experience

Global E&M Outlook 2017-2021The future of E&M is… fan-tastic!

Knowing what drives

‘fandom’ and who your Extending franchises

most engaged fans into experiences

really are

Becoming a

Fan-Centric

Company

Selling to fans

Building direct-to-

(not to “eyeballs”)

consumer destinations

wherever they may be

Aligning operations to

provide ‘value’ – invest

in what makes a

difference for fans

Global E&M Outlook 2017-2021Build businesses and brands around active, higher value communities of users Global E&M Outlook 2017-2021

User experience takes centre stage 4.2% in today’s global Projected industry multi-speed media growth 2017–2021 landscape

Focusing on the user experience creates growth

opportunities in a challenging economic environment

Global E&M Growth

2.54% Global E&M revenue as a

7.0% 2.53% share of global GDP

2.52%

6.0% 2.48%

2.44%

5.0% 2.39%

4.0%

4.2%

3.0% CAGR

2.0%

3.6%

1.0%

0.0%

2013 2014 2015 2016 2017 2018 2019 2020 2021

E&M excluding internet access Total E&M

Global E&M Outlook 2017-2021Internet video, internet ads, gaming and access are

the engines powering global E&M growth

CAGR minus GDP growth by segment

2016-2021 (% points)

Internet video 6.0

four major

Internet advertising 4.3

growth

Video games drivers 2.7

Internet access 0.5

Cinema -1.2

OOH -1.7

Music -2.0

TV advertising -2.8

B2B -2.9

Radio -3.4

Traditional TV & video -4.2

Books -4.5

Magazines -6.0 E&M CAGR: 4.2%

Newspapers -8.3 GDP CAGR: 5.6%

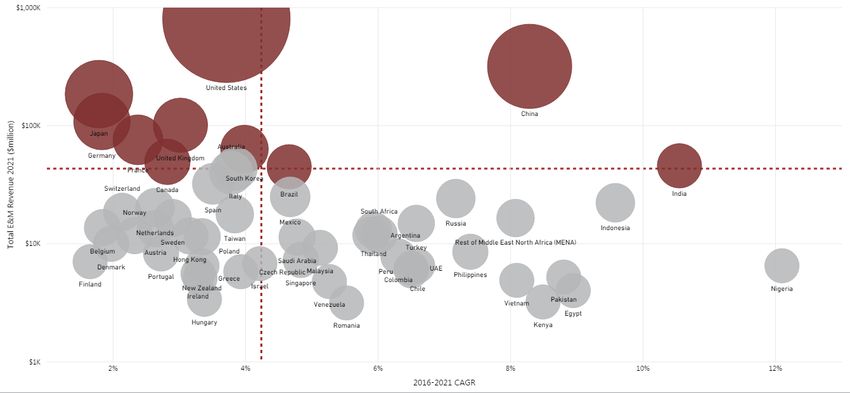

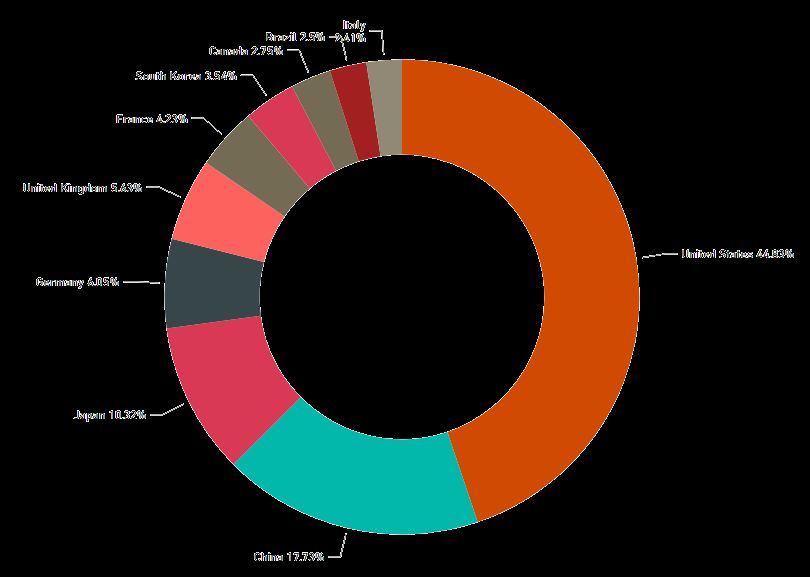

Global E&M Outlook 2017-2021Top E&M countries

The United States is projected to remain the largest E&M market through

2021, however the % of total E&M spend the US represents is declining

France 4%

United Kingdom 6%

Projected % of United States 45%

Germany 6% E&M Revenue in

2021

(top markets)

Japan 10%

China 18%

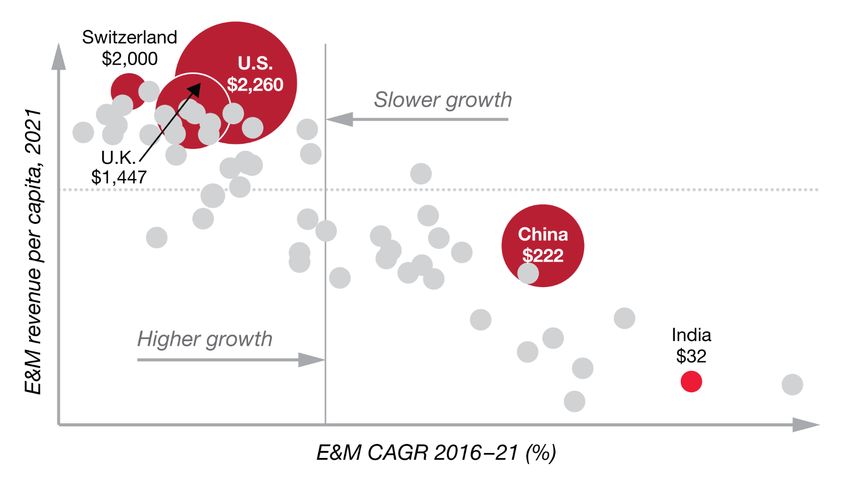

Global E&M Outlook 2017-2021Global E&M Markets

• Each bubble represents a country

• Size of bubble represents total E&M revenue

Total Global E&M Revenue Projections 2021

(USD Millions)

2017 – 2021 CAGR (%)Quadrants

5% CAGR

Mature Next Wave

Average Projected

Size Growth

2021 revenue ($US bn) 2016-2021 CAGR

US$10 bn $77.1 3.2%

$52.1 8.3%

$5.9 7.1%

Slow Up &

Growing Comers $6.6 3.1%

bigger

faster

Global E&M Outlook 2017-2021The most rapid growth rates are in newly emerged markets, where per capita spending is generally low Global E&M Outlook 2017-2021

Demographics – youth will be served… Global E&M Outlook 2017-2021

Technology and digital media have changed the way

younger generations experience and purchase content

US household spending by generation

(US$)

Millennials

spend

significantly

less on

entertainment

annually than

baby boomers

and

Generation X.

Global E&M Outlook 2017-2021www.pwc.com/outlook

Consumer/end-user & 5 year historic &

54 Countries 17 segments

advertising spending 5 year forecast data

Access Read Watch Listen Play

Internet access Books Box office Music eSports

Data Traditional

B2B Radio Video games

consumption TV & video

Internet Virtual

Magazines

video reality

TV

Newspapers

advertising

Internet

OOH

advertisingSources of Global revenue growth

Size Growth

2021 share of revenue 2016-2021 CAGR

Advertising

30% 4.2%

$677 bn

Access spend

29% 6.0%

$647 bn

Consumer spend 41% 3.1%

$912 bn

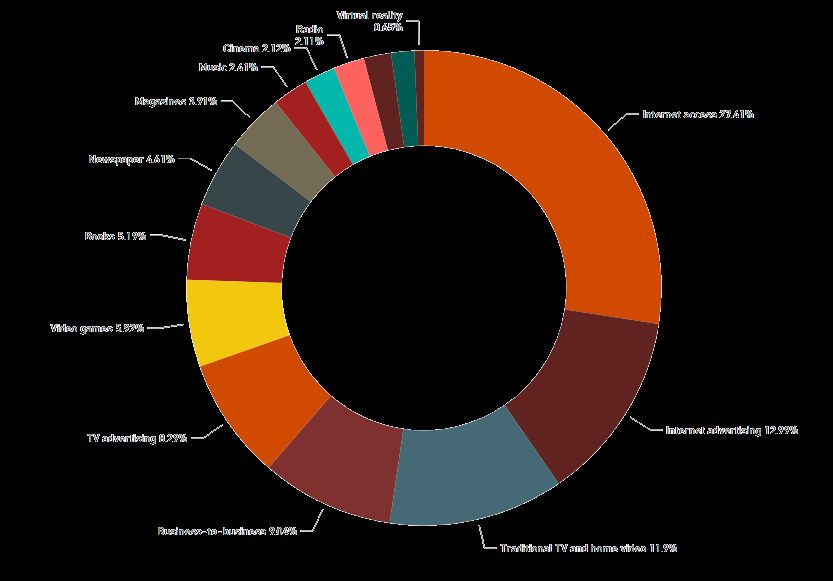

Global E&M Outlook 2017-2021Global revenue of $2.2 trillion by segment

Internet access 27%

Internet

Access

represents

the largest

percentage

(27.4%) of

global E&M

spend,

followed by

Video Games 6%

Internet

Advertising

and

Traditional

TV and

Home Video TV Ads 8% Internet ads 13%

Business-to-business 9%

Traditional TV & home video 12%

Global E&M Outlook 2017-2021Segment global growth rates

CAGR 2016-21

Radio 2.1% TV advertising 2.8% B2B 2.7%

OOH 3.8%

Video games 8.2% Internet access 6.0%

Newspaper -2.7%

Internet video 11.6% Music 3.5%

Magazines -0.5%

Traditional

1.3% Cinema 4.4%

TV/video

Internet

9.8% Books 1.1%

advertising

Global E&M Outlook 2017-2021Summary by consumer experience and segment

Global Revenue & CAGR Global Growth by Top Revenue

$700 Contributing Segments

Access 6.0%

(CAGR 2016-21)

$600

$350

$500

$300 Internet advertising 9.8%

Revenue US$ bn

TV and video 1.3%

$400 $250

Revenue US$ bn

Watch 2.5%

$200 B2B 2.7%

$300

Read 0.1% TV advertising 2.8%

$150

$200

Play 10.4% $100

Video games 8.2%

$100 Listen 3.5% $50 Internet video 11.6%

$0 $0

2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021

Note: Above summaries exclude B2B and all advertising.

Global E&M Outlook 2017-2021Internet access - $647 bn

Global internet access revenue Mobile internet subscribers, mn

APAC 1,648

2,455

EMEA 626

907

Latin America 244

381

North America 299

329

2012 2013 2014 2015 2016 2017 2018 2019 2020 2021

Mobile Fixed 2016 2021

Governments and regulatory bodies in many markets are taking steps to increase competition

as well as coverage through changes in law, regulation or by licensing new operators.

Global E&M Outlook 2017-2021Data consumption

Global data consumption, MB mn Data consumption CAGR 2016-21

1,200 31.7%

Smartphone

72.9%

1,000

800 17.6%

Fixed broadband

21.8%

600

16.6%

400 Other portable

38.6%

200

-8.2%

Non-smartphone

0 21.1%

2012 2013 2014 2015 2016 2017 2018 2019 2020 2021

Global India

Strong continued growth is expected in both mature

The single biggest driver of growth is the increased markets such as the US and less developed markets

adoption of smartphones and, in particular, the rise such as India and Brazil. India overtook the US as

of video viewing on smartphones. the world’s second-largest smartphone market in

2015.

Global E&M Outlook 2017-2021Internet advertising - $303 bn

Global advertising revenue & CAGR

$350

$300

Revenue US$ bn

$250 CAGR 9.8% Internet advertising: $303 bn in 2021

$200 TV advertising: $194 bn in 2021

$150 CAGR 2.8%

$100

$50

$0

2012 2013 2014 2015 2016 2017 2018 2019 2020 2021

Internet TV

Global internet advertising grew by 19% YOY to surpass TV in 2016. Its 2016-2021 CAGR of

9.8% makes it 40% of total advertising in 2021, versus 26% for TV.

Global E&M Outlook 2017-2021Internet advertising - $303 bn

Global internet advertising revenue Projected growth

CAGR 2016-2021

Wired 2.5%

Mobile 18.5%

2012 2013 2014 2015 2016 2017 2018 2019 2020 2021

Mobile Wired

Innovation including harnessing artificial

Mobile will overtake wired advertising in

intelligence to track ads across platforms and

2019 growing to account for 56% of internet

create personalised targeting, will be a

advertising globally by 2021.

significant long-term opportunity.

Global E&M Outlook 2017-2021Internet video - $37 bn

Global Internet video vs.

Projected growth

physical home video revenue 2016-2021 CAGR

Internet 11.6%

-8.8% Physical

2012 2014 2016 2018 2020

Internet Physical

With the physical market continuing to There are a growing number of routes to the

decline, global Internet video revenue will audience due to the rise of Internet video,

overtake it for the first time in 2017 and shifting the emphasis towards content rights,

increase the gap over the forecast period. licensing deals and original productions.

Global E&M Outlook 2017-2021TV advertising - $194 bn

Projected growth Distribution of revenue

2016-2021 CAGR 2021

Online

12.4% Online 6%

Multichannel

4.6% Multichannel 28%

1.5% Terrestrial

Terrestrial

66%

Although advertisers in most markets still look to traditional TV for the largest audiences –

often live sporting events – there’s an increasing trend towards a multiplatform approach.

Driving consumers online to discuss TV content and advertising through social media, or

offering enhanced versions of advertising on video platforms like YouTube, ensures campaigns

connect with audiences more effectively.

Global E&M Outlook 2017-2021Traditional TV and home video - $277 bn

TV subscription revenue projected TV subscriptions

growth 2016

2016-2021 CAGR

Households

US 98

Global 2.3%

mn

India 154

Revenue

US $101

US$ bn

India $8

Investment in exclusive entertainment programming, original productions and sporting rights

is increasing each year. Companies in mature markets are responding with consolidation for

scale and content rights.

Global E&M Outlook 2017-2021Video games - $138 bn

Projected growth Distribution of consumer revenue

2016-2021 CAGR 2021

11.9% Social/Casual

PC

2.7% Console 25%

Social/casual

5.9% PC 56%

Consumer spending: $133 bn in 2021 Console

19%

Advertising: $5 bn in 2021

Social/casual gaming shows significant growth due to a huge global audience with increasingly

capable devices, low barriers to entry in terms of game costs and a business model that, if

successful, can propel a developer into the mainstream.

Global E&M Outlook 2017-2021Cinema - $50 bn

Box office revenue Box office projected growth

US$ bn 2016-2021 CAGR

2016 $37.1

Global Global 4.4%

2021 $46.0

Consumer spending: $46 bn in 2021

Advertising: $4 bn in 2021

APAC will experience the highest regional growth in box office revenue to US$20.4bn by 2021, a

CAGR of 7.9%. China and India will add a combined US$5.6 bn over the forecast period, or 63%

of global box office growth.

Global E&M Outlook 2017-2021Out-of-home advertising - $44 bn

Global OOH revenue Projected growth

2016-2021 CAGR

-0.3% Physical

Global

10.7% Digital

2012 2013 2014 2015 2016 2017 2018 2019 2020 2021

Digital Physical

Distinct advantages of digital OOH have enabled this format to be the main driver of revenue

growth through 2016, accounting for 82.3% of the increase in global OOH revenue since 2012.

Global E&M Outlook 2017-2021Music - $56 bn

Global digital music revenue Recorded music projected growth

2016-2021 CAGR

-11.6% Physical

Global

11.8% Digital

Recorded music : $27 bn in 2021

2012 2013 2014 2015 2016 2017 2018 2019 2020 2021

Live music: $29 bn in 2021

Downloading Streaming

Global music streaming revenue grew 65% YOY in 2016 to overtake downloading by a $3.2 bn

margin. Exploring alternatives such as strategic partnerships will be necessary for stand-alone

streaming providers in a highly competitive market.

Global E&M Outlook 2017-2021Business-to-business - $210 bn

Total B2B growth Business information projected

2016-2021 CAGR growth

2016-2021 CAGR

2.0% Non-Digital

3.7%

7.1% Digital

The business information sub-segment is the cornerstone of B2B revenue. The increasing

uncertainty from economic and geopolitical risks will contribute to continued global business

information growth to $118.4 bn by 2021.

Global E&M Outlook 2017-2021Radio - $49 bn

Digital music streaming Radio advertising projected growth

share of total radio 2016-2021 CAGR

15%

2016 Global 2.0%

35%

2021 Advertising: $37 bn in 2021

India

Licence fees: $6 bn in 2021

Satellite subscriptions: $6 bn in 2021

Traditional radio broadcasters and streaming music service providers are beginning to cross

over in terms of offering spoken word content and streaming on-demand services. This could

pave the way for a new business model for radio broadcasters.

Global E&M Outlook 2017-2021Books - $121 bn

Projected growth

2016-2021 CAGR

0.5% Educational Educational books: $37 bn in 2021

1.6% Consumer Consumer books: $63 bn in 2021

0.5% Professional Professional books: $21 bn in 2021

Pricing in consumer books continues to cause challenges. Bricks-and-mortar booksellers simply

cannot compete on price with online booksellers—nor can they offer the range of titles that an

online seller can.

Global E&M Outlook 2017-2021Magazines - $91 bn

Projected growth, Distribution of revenue

CAGR 2016-2021 2021

Trade Circulation 8%

-0.9% Consumer

1.5% Trade Trade Advertising 11%

Consumer Advertising 34%

Consumer Circulation 47%

Consumer magazines: $74 bn in 2021 Global

Trade magazines: $17 bn in 2021

Publishers are under pressure from changes in consumer content-consumption, specifically

video content. Consumer titles are looking for ways to reduce their reliance on Facebook and

YouTube now which now dominate ad revenue spend in most markets. Trade titles have had

success diversifying into events to drive revenue growth.

Global E&M Outlook 2017-2021Newspapers - $107 bn

Global newspaper revenue Projected growth

$US bn CAGR 2016-2021

$127

Print

-4.02%

$8

Digital

6.13%

2012 2013 2014 2015 2016 2017 2018 2019 2020 2021

Circulation: $58 bn in 2021

Digital Print

Advertising: $49 bn in 2021

The global market is in long-term marginal decline. Consumers in Europe, North America and

Australasia continue to abandon print for digital channels. However, print consumption is still

growing strongly in Asia Pacific, now accounting for 60% of daily print circulation.

Global E&M Outlook 2017-2021Virtual reality - $15 bn

VR revenue Distribution of revenue

US$ bn 2021

App

$16 1%

$12

$8 Video

53% Gaming

$4 46%

$0

2016 2017 2018 2019 2020 2021

Global US China Japan

The end game for hardware companies will be Content will evolve into a market for video

attempting to become the standard platform for VR streaming, microtransactions and potentially a

and hence start to charge royalties or commission premium for VR video added to monthly pay-TV or

from content sales. OTT bills.

Global E&M Outlook 2017-2021Virtual reality

Global VR units Portable VR units

millions

240 240

180 180

120 120

60 60

0 0

2016 2017 2018 2019 2020 2021 2016 2017 2018 2019 2020 2021

Home Portable Dedicated Mobile

VR headsets based on smartphones are set to Interestingly, by 2021 we will also see enough

dominate in terms of usage numbers, and currently headsets in consumer hands to drive an advertising

this means a variety of implementations from market. VR video in particular will also benefit here

various phone manufacturers. given the immersive nature of the experience.

Global E&M Outlook 2017-2021Virtual reality

Virtual reality revenue is also poised for growth, with video and gaming

representing the majority of revenue

Virtual reality apps

(2%)

Virtual reality is one of

the most interesting Virtual reality video Virtual reality

(51%) gaming (47%)

media formats available,

offering highly engaging

content and an

immersive consumer

experience at an

increasingly affordable

price point Virtual reality revenue (size growth) by year

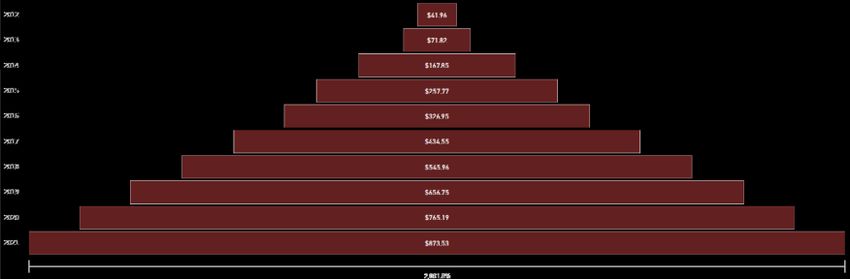

Global E&M Outlook 2017-2021E-sports - $0.9 bn

E-sports total revenue E-sports projected growth

US $ mn 2016-2021 CAGR

$750

Streaming

31.9%

advertising

$500

Consumer ticket

23.7%

sales

$250

Consumer

contribution 17.2%

$0

2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 Sponsorship 13.8%

Consumer Advertising

Total e-sports revenue has seen strong growth over

New games, a growing audience, and suitable

the historic period as interest rises worldwide,

infrastructure development worldwide will

tournaments and leagues become more

contribute to consumer ticket sales CAGR of 23.7%

sophisticated, and sponsorship and other

through 2021.

development money pours in to the discipline.

Global E&M Outlook 2017-2021E-sports

E-sports total revenue E-sports ad revenue

US $ mn US $ mn

$1,000 $450

$360

$750

$270

$500

$180

$250 $90

$0 $0

2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 2016 2017 2018 2019 2020 2021

Global US South Korea China Sponsorship Streaming advertising

South Korea was the largest market in the early Streaming advertising should rise strongly to

years of the historic period, but was overtaken by overtake sponsorship in 2018. The two streams

the US in 2015, with the latter due to extend its lead combined will account for nearly 75% of total

by the end of the forecast period. revenue in 2021.

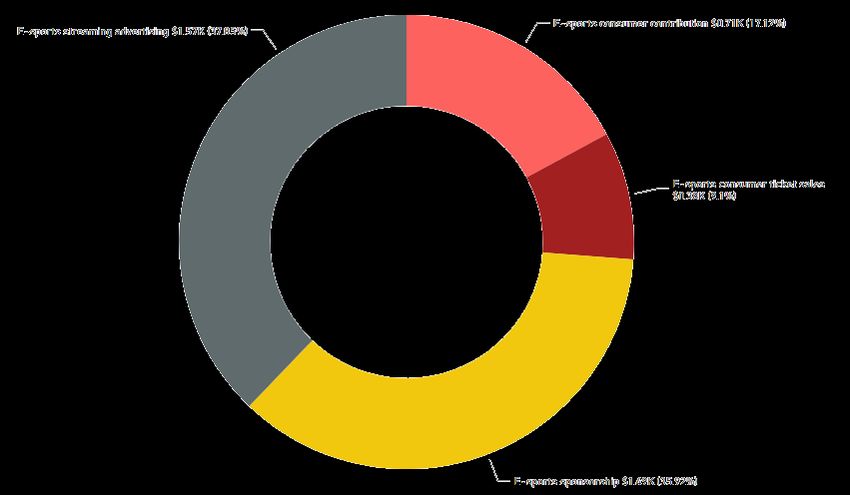

Global E&M Outlook 2017-2021eSports

eSports revenue is poised for dramatic growth, with advertising and

sponsorships enabling much of the growth

eSports streaming eSports consumer

adverts (38%) contribution (17%)

eSports includes eSports

consumer

consumer and ticket sales

advertising spending on (9%)

organized video game

competitions online and

offline across one-off

events and organized

leagues. This segment eSports sponsorships

(36%)

introduces a new brand

of entertainment that eSports revenue is projected to grow by over 2,000 percent

appeals largely to

younger audiences but

has a growing fan base

Global E&M Outlook 2017-2021Deep dive: Publishing

Publishing within the Outlook

Books Magazines Newspapers

Comprises revenue generated Comprises revenue from: Comprises revenue from:

from the sale of:

• Consumer-focused • Circulation (consumer

• Consumer books magazines spend on newspapers)

• Educational books • Trade magazines • Advertising in newspapers

• Professional books

Consumer only Consumer and advertising Consumer and advertising

Print and digital Print and digital Print and digital

Global E&M Outlook 2017-2021Key global themes and trends

Overall publishing is in a slow decline. However there are pockets of growth in

1 certain sub segments and markets.

Magazines and books will gain share of the global publishing market as they

2 transition to digital platforms more successfully.

Digital consumer magazine advertising will add more revenue over the

3 forecast period than any other sub segment of publishing, a total of $6.1 bn.

Trade magazine advertising is the only sub segment forecast to generate more

4 revenue from digital formats than print, reaching this tipping point by 2021.

As advertiser funding diminishes, income from newspapers’ primary customer

5 base, consumers, will become more important in publishers’ total revenue mix.

Global E&M Outlook 2017-2021Publishing macro trends

Publishing revenues, US$B Growth, CAGR 2016-21

$339 Newspapers -2.7%

2016

Magazines -0.5%

2021 $332

Books 1.1%

-0.7% $320

Growth, CAGR 2016-21

Print -2.7%

2012 2013 2014 2015 2016 2017 2018 2019 2020 2021

Digital 8.4%

Overall publishing is in a slow decline. However there are

pockets of growth in certain sub segments and markets.

Discounted pricing for print versions will help sustain overall

growth in books.

Global E&M Outlook 2017-2021Print vs digital

Publishing revenues, US$B Growth, CAGR 2016-21

$314

$283 7.6%

$246 Books

-0.6%

11.0%

Magazines

-3.5%

$73 6.1%

$49 Newspapers

$26 -4.0%

2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 Digital Print

Digital Print

Trade magazine advertising is the only

Increases in digital format revenues will not

publishing sub segment forecast to generate

be enough to make up for declines in print

more revenue from digital formats than

formats over the forecast period.

print, reaching this tipping point by 2021.

Global E&M Outlook 2017-2021Publishing mix changes

Share of publishing revenues Distribution of revenues, 2021

2016 35%

Books

2021 38% 72%

75%

84%

28%

Magazines

29%

25% 28%

16%

37%

Newspapers Books Magazines Newspapers

34%

Digital Print

Magazines and books will gain share of the global Books and magazines will generate about

publishing market as they transition to digital

platforms more successfully. Newspapers are

one-quarter of revenues from digital

having a harder time monetizing the shift to digital. platforms by 2021.

Global E&M Outlook 2017-2021Growth drivers in publishing

Revenues by sub segment Revenue added 2016 to 2021

US$ bn US$ bn

$16

Digital consumer books 6.9% CAGR Digital

$14 consumer

magazine $6.1

$12 advertising

$10 Digital consumer magazine

advertising 11.8% CAGR

$8 Digital

consumer books $4.3

$6

$4

Digital professional books 7.5% CAGR Digital

$2 professional $2.6

books

$0

2012 2013 2014 2015 2016 2017 2018 2019 2020 2021

Digital consumer magazine advertising will add

more revenue over the forecast period than any

other sub segment of publishing, a total of $6.1 bn.

Digital consumer books and professional books will

round out the top three growth sub-segments.

Global E&M Outlook 2017-2021Country ranking: books

Color legend

Top 10 largest books country

China & India rank in the top 10 among both

Top 10 fastest growing books country

the largest and fastest growing books markets,

making them attractive opportunities. Countries that sit in both lists

Global E&M Outlook 2017-2021Country ranking: magazines

Color legend

Top 10 largest magazine country

The US and China are the largest magazine

Top 10 fastest growing magazine country

markets in terms of revenue. These two

territories will account for 53% of the global Countries that sit in both lists

market by 2021.

Global E&M Outlook 2017-2021Country ranking: newspapers

Color legend

Top 10 largest newspaper country

India and Indonesia rank in the top 10 among

Top 10 fastest growing newspaper country

both the largest and fastest growing newspaper

markets, making them attractive opportunities. Countries that sit in both lists

Global E&M Outlook 2017-2021Deep dive: Internet video

Internet video within the Outlook

SVOD

Revenue from stand-

alone subscription video Revenue from

on demand (SVOD) transactional video on

services delivered over the demand (TVOD) services

open Internet, such as Internet Video (such as iTunes), that

deliver filmed

Netflix.

entertainment content via

the open Internet and

which do not require a

subscription.

TVOD

Global E&M Outlook 2017-2021Key global themes and trends

Internet video’s growth has been underpinned by improving broadband

1 coverage and a wide range of OTT launches globally.

The internet video distribution ecosystem is diversifying, as old and new

2 media are building direct to consumer relationships as well new aggregators.

With an abundance of content delivery platforms new content will

3 increasingly be the differentiating factor.

Global expansion was the key trend in 2016 with the big international SVOD

4 players launching in the majority of markets.

Investment in original content is rising beyond major headline shows and

5 towards deals with local production houses to boost take-up in new markets.

Global E&M Outlook 2017-2021Internet video

Internet video revenues Growth, CAGR 2016-21

US$ bn

$40.0

SVOD 13.1%

11.6%

$30.0

$20.0

TVOD 7.4%

$10.0

$0.0

2012 2013 2014 2015 2016 2017 2018 2019 2020 2021

Global Internet video revenue reached US$21.2bn in 2016,

The Internet video market is exhibiting strong growth

having risen from US$6.3bn in 2012. The segment’s growth

worldwide as home video shifts from the purchase and rental

has been underpinned by improving broadband coverage

of physical goods such as DVDs, to the increasingly

and a wide range of OTT launches from pay-TV operators

competitive over-the-top (OTT) market.

and standalone services alike.

Global E&M Outlook 2017-2021Internet video mix changes

Distribution of revenue Internet video ecosystem

diversification

SVOD

TVOD 55%

45%

TVOD

24% Direct to

2012 SVOD Consumer

76%

2021

With many pay-TV providers launching OTT initiatives

Internet video growth has been dominated by SVOD, which

around the world, Internet video is becoming increasingly

accounted for 55% of Internet video revenue in 2012. This

core to service provider’s product portfolios. Many pay-TV

will rise to nearly three-quarters by 2021, with the remainder

OTT services are not primarily about taking on Netflix or

attributable to transactional VOD platforms such as Apple’s

Amazon, but monetising viewers who have previously

iTunes and Sky’s Sky Store.

avoided paying for content.

Global E&M Outlook 2017-2021SVOD

SVOD revenues by region Growth, CAGR 2016-21

US$ mn

$20,000 APAC 19.5%

$15,000

EMEA 13.1%

$10,000

$5,000 LatAm 11.5%

$0

2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 North America 10.9%

North America EMEA APAC LatAm

Global expansion was the key trend in 2016 with the big APAC exceeded EMEA in SVOD revenues in 2016. The

international SVOD players launching in the majority of number of domestic services offering local content and

markets. Companies are keen to market their exclusive original productions is spurring the market across this

content to the widest possible audience. region and is projected to reach $6.9 bn by 2021.

Global E&M Outlook 2017-2021Country ranking: SVOD

Color legend

Top 10 largest SVOD country

The US and China dominate the SVOD market

Top 10 fastest growing SVOD country

and, combined, will represent nearly two-thirds

of the global market by 2021. Countries that sit in both lists

Global E&M Outlook 2017-2021 69Country ranking: TVOD

Color legend

The US, UK, China, Japan, and Canada are Top 10 largest TVOD country

projected to experience the greatest revenue Top 10 fastest growing TVOD country

additions through 2021. Combined, these Countries that sit in both lists

markets will account for 74% of global TVOD

growth.

Global E&M Outlook 2017-2021 70Strategic questions PwC

Maximising the value of content: Blending data

and intuition

15-second download

With traditional measures of content performance having What role do ‘big data’ and

been thrown into flux by the explosion in digital channels data analytics play in content

and consumption data, new ways are emerging to value and marketing or purchasing

monetise content – Including measures of engagement such decisions in your business?

as ’attention minutes’.

What metrics are you using

While the content majors may appear to have been put at a today to measure content

disadvantage to the distribution players by the flood of performance, and are those

consumption ‘big data’, in fact their wealth of content metrics changing?

intuition and insights represents a huge differentiating asset

– and one they can blend with analytics-driven insights to

create a powerful hybrid.

This can unlock the user experience for the most engaged

‘fans.’Addressable advertising: On the road to ‘nirvana’

– But with more disruption yet to come

15-second download

Linear TV is now joining the move towards ‘addressable’ As an advertising inventory

advertising, targeting consumers though a blend of media owner, are you offering

usage data, demographic information and addressable advertising as

purchasing history. part of your portfolio? If not,

But questions remains for the three main stakeholders of why not?

advertisers, networks/publishers and consumers – With As an advertising agency, are

profound impacts, some of them unexpected, set to emerge you discussing the implications

along the advertising value chain as addressability of of addressable advertising with

ads advances. your clients as part of their

Two of the biggest hurdles to reaching the ‘nirvana’ of advertising mix?

addressable cross-platform ads are around improving the

precision of targeting, and gaining a deeper understanding

of individuals’ behavioural response to a given advert in a

given context.Audience measurement: Unlocking a treasure

trove of insight

15-second download

Online advertising has been winning market share from How do you currently measure

traditional broadcast advertising on the strength of its engagement, as opposed to

greater accountability and wealth of detailed data on user reach and frequency?

behaviour and engagement.

Would you be prepared to

But now TV is fighting back, with innovations in audience collaborate with others in the

measurement based around analysing return path data industry to drive greater

(where available), social listening, and new aggregated standardisation in audience

insights into agency spend. The new data also enhances Pay measurement?

TV service providers ability to’ cross-sell and upsell services

to subscribers.

Going forward, future innovations in audience measurement

will depend increasingly on industry collaboration, to

provide advertisers with credible, comparable data for

buying decisions.OTT: Disruption for the industry, choice for

the consumer

15-second download

An expanding flow of OTT content services are being rolled How should incumbent

out in markets worldwide, both from new ‘pure-play’ OTT broadcasters and content

entrants and traditional broadcasters adding an OTT service providers respond to – And

to their portfolio. Players that achieve relevancy can join the reach – The growing ranks

consumer’s ‘inner circle of trust’. To stay there, they’ll need of ‘cord-cutters’ and

to apply innovation and agility ‘cord-nevers’?

As entrants and incumbents jostle for position, the How can E&M groups best

disruptive frenzy of activity is creating a complex, engage with customers

fragmented patchwork of often-overlapping content through digital channels to

services, using a diverse array of business, operating and drive their own innovation and

pricing models. adoption by customers?Reaching the next five billion consumers

15-second download

Mobile Internet connections worldwide are growing apace. What opportunities has your

They already outnumber fixed connections by three to one, company identified springing

and are projected to rise by over 5 billion to 7.6 billion in the from the next five billion

next four years. consumers joining the global

This is a bigger global disruption than the Industrial mobile Internet ecosystem?

Revolution, and presents entertainment and media Which emerging markets do

companies with a massive new audience for content in you feel you could target most

emerging markets – albeit at much lower ARPUs than effectively and profitably with

they’re accustomed to in the developed world. consumer offerings?Contextual awareness and data responsibility

15-second download

The mobile device is now the digital extension of the What opportunities has the

individual, sitting at the heart of their personal proximity growing ubiquity of mobile

network and constantly monitoring their activities devices opened up for your

and surroundings. business – and how do you

The wealth of data from the handset opens the way to anticipate these expanding in

contextual awareness of the consumer’s behavioural patterns the future?

and environment, enabling companies to anticipate their Before targeting consumers,

needs and address them with context-relevant choices, do you consider whether you

content and messaging. should do this – or just

But consumers in some contexts find this targeting intrusive whether you can?

– And there’s a risk this unease may grow as addressability

increases. So providers need to behave responsibly with

data, and put the consumers in control of what data they

share, and what value they get in return.Four forces reshaping the digital

advertising landscape

15-second download

‘Digital’ and ‘traditional’ advertising are not mutually As a marketer, are you

exclusive or in competition with each other – But all part of ‘running to where the ball is

the evolving mix of advertising options and revenue streams going to be’ with respect to

being targeted across the industry. media planning by having a

As the division between online and mobile ads blurs, and clear mobile and video

consumers’ attitudes to mobile advertising evolve, four strategy?

forces are reshaping the ads landscape: mobile, video, and Are you investing in creating

native and programmatic advertising. experiences that support your

users’ video and other needs?Entertainment and media deals: Beating a path to

the door of the connected consumer

15-second download

Entertainment and media megadeals have been a major Are you seeing different deal

feature of the M&A landscape in the US and Europe in rationales at play within – and

recent years, with several blockbuster transactions, mostly between – Different segments

by cable and satellite operators. of E&M? and with other non

What really links these deals is not their size, but their focus E&M segments?

on building scale in infrastructure and customers. These To what extent is your

goals play to two strategic aims: one defensive, in fending off market or markets

the advance of the over-the-top players; the other offensive, experiencing a blurring

in positioning to gain the upper hand in the ‘connected of traditional boundaries

home’/connected consumer? between media,

With the shift to maximising user experience, will the next communications

wave of deals be different – connecting innovative customer and technology?

focussed technology with existing customer brands?The shifting industry value chain

15-second download

With the debate still ongoing about net neutrality – often How do you believe differing

seen as a battle between telcos and content, especially online net neutrality rulings will

video, providers – the status of such regulation in markets affect the provision of internet

across the world varies widely. infrastructure in the long run?

Operators globally are undertaking a diverse array of As the next billion people in

initiatives in different markets to boost the value and returns emerging markets become

on their networks, through additional services and connected, what are the

innovations enabled by their networks. implications for the

distribution and consumption

of media content?The tax agenda: Reputation risk – Or an

opportunity for differentiation?

15-second download

Progress towards rewriting the international tax rulebook Do you feel the changes being

has continued during the past year, as governments have made to the international tax

begun to follow up their rhetoric about ‘tax morality’ with regime represent the right

hard legislation. responses to the

The changes in the tax environment are especially requirements and realities

relevant to entertainment and media companies, given of ‘digital’ business?

their heavy dependence on their reputation and brand Has your business carried out

among consumers. a total tax contribution study

across its markets?This publication has been prepared for general guidance on matters of interest only, and does not constitute professional advice. You should not act upon the information contained in this publication without obtaining specific professional advice. No representation or warranty (express or implied) is given as to the accuracy or completeness of the information contained in this publication, and, to the extent permitted by law, PwC does not accept or assume any liability, responsibility or duty of care for any consequences of you or anyone else acting, or refraining to act, in reliance on the information contained in this publication or for any decision based on it. © 2017 PwC. All rights reserved. “PwC” refers to the PwC network and/or one or more of its member firms, each of which is a separate legal entity. Please see www.pwc.com/structure for further details. 160613-095853-AG-OS

You can also read