Mid-Year Economic & Capital Markets Update July 20, 2021

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Mid-Year Economic & Capital Markets Update

July 20, 2021

1

MARKET UPDATE

MARKET THEMES

24

22.0

22 21.1

▐ Year-To-Date

20

QTD

18 17.5

16 15.0

14

Total Returns (%)

13.3

12 12.0

10.4

10 8.8

8.5 7.4

8

6.1 6.8

6

5.0 4.4

4 3.6 4.3

3.9 3.9

3.2

0.2 2.7 2.4

2 1.8

1.7 1.4

0.5 0.9

0

-2 -1.6 -1.8

-4 -3.0

TIPS Municipals 5- U.S. Core High Yield High Yield Foreign EM Debt U.S Large U.S. Small International Emerging U.S. Equity S&P Real Commodities Hedge

Year Bond Municipals Bond (Unhedged) Cap Cap Developed Markets REITs Assets Funds

*Hedge fund returns are lagged 1 month. Sources: FactSet, J.P. Morgan, Russell, MSCI, FTSE Russell, Alerian. Hedge Funds returns as of 5/31/21/21. All other returns as of 6/30/21.

Fixed Income Equity Real Asset / Alternatives

+ Interest rates moved lower at the longer end of the curve and + Optimism continued into the 2nd

quarter as vaccinations + REITs continued to benefit from increasing demand and low

were slightly higher inside of 5-years. continue to progress and many restrictions were lifted across the interest rates.

country.

+ Investment grade and high yield spreads compressed during - Emerging market equities lagged their developed market + Commodities benefitted most from large increases in energy,

the quarter. counterparts as many developing countries struggled to control namely oil, although strong performance was broad based

Covid-19 outbreaks. across sectors.

See disclosures for list of indices representing each asset class. Past performance does not indicate future performance and there is a possibility of a loss.

3FIXED INCOME MARKET UPDATE

U.S. Treasury Yields Curve Index Performance Attribution (2Q 2021)

U.S. Treasuries moved lower at the longer end of the curve with the 10-year and 30- In the U.S., both lower rates and spread compression drove fixed income performance.

year rates declining 29bps and 36bps, respectively. Dollar weakness provided a nice tailwind for foreign bonds.

Source: FactSet Source: FactSet

Credit Market Spreads – Trailing 5 Years

Credit spreads compressed during the quarter with investment grade and high yield spreads decreasing 11bps and 42bps, respectively.

Source: FactSet

Past performance does not indicate future performance and there is a possibility of a loss.

4EQUITY MARKET UPDATE

Equity Valuations (Trailing 15 Years) U.S. Equities – Contribution to Return by Sector (2Q 2021)

Valuations remain elevated when compared to historical ranges. Valuations were lower relative to U.S. equity performance was strong across sectors with technology contributing most to index

the first quarter despite strong equity performance, driven by strong underlying earnings growth. performance, although the real estate sector performed best on an absolute basis.

30 IT (27%) 2.9%

Range (+/- 1 Std Dev.)

Communications (10%) 1.1%

Sector (Avg Index Weight %)

Median

Current (6/30/2021) Health Care (14%) 1.1%

25

Trailing PE Ratio

3/31/2021 Financials (12%) 0.9%

Consumer Disc. (12%) 0.8%

20 Industrials (9%) 0.4%

Real Estate (3%) 0.4%

Energy (3%) 0.3%

15

Consumer Staples (5%) 0.2%

Materials (2%) 0.1%

10 Utilities (2%) 0.0%

U.S. International Dev. Emerging Markets

-0.5% 1.0% 2.5%

Source: FactSet Source: FactSet. Russell 1000.

Country Total Returns (%) – Top 10 Largest Economies

Strong equity performance was broad based across countries with China the noticeable laggard as Chinese technology and consumer companies continue to face regulatory pressures.

20 18.1 17.6

18

16 14.9

QTD ▐ Year-To-Date

14.5 14.1

Total Returns (%)

14 13.2

12 11.4 10.7

10 9.1

8.9 8.8 8.6 8.6

8

6 5.8

1.9

4 4.2 4.4

3.0

2 2.1

0 0.2

-2

US China Japan Germany United India France Italy Canada Korea

Source: FactSet Kingdom

Past performance does not indicate future performance and there is a possibility of a loss.

5REAL ASSET MARKET UPDATE

Real Assets Performance REIT Sector Performance

Energy drove real assets higher as May’s ransomware attack on the Colonial Most REIT sectors generated positive returns and continued to benefit from re-

Pipeline caused supply disruptions within the space. opening measures and low interest rates.

50

44.6 Residential 14.1%

YTD QTD 27.6%

40 Industrial 12.0%

19.1%

Retail 12.5%

32.8%

30

Data Centers 14.1%

11.4%

QTD

Total Return (%)

23.2 20.4 6.3% YTD

Health Care 13.3%

20 17.6

Office 9.5%

15.1%

12.8

10 9.4 Self Storage 23.6%

36.4%

3.9 Diversified 9.6%

18.9%

0

Specialty 12.0%

28.0%

-10

-5.7 Lodging/Resorts -0.6% 17.3%

Energy Industrial Precious Agriculture

Metals Metals -5% 5% 15% 25% 35%

Source: FactSet Source: FactSet

Total Return (%)

Past performance does not indicate future performance and there is a possibility of a loss.

6ECONOMIC EXPANSION

U.S. GDP PATH DURING PANDEMIC

• 2020 RECESSION AND REAL GDP GROWTH OFF PANDEMIC ECONOMIC ACTIVITY LOWS

+1.4%

-11.5% +14.6%

Source: https://fred.stlouisfed.org/series/GDP

8STRONG SECOND QUARTER 2021 REAL GDP GROWTH EXPECTATIONS

7.5% GDP GROWTH FORECAST FOR THE SECOND QUARTER OF 2021 (7/16/21 ESTIMATE).

7.5%

Source: https://www.atlantafed.org/cqer/research/gdpnow

9STRONG GLOBAL ECONOMIC GROWTH EXPECTATIONS

• 5.6% EXPECTED GROWTH FOR 2021*

• 4.3% EXPECTED GROWTH FOR 2022*

• IF ACHIEVED WOULD BE MOST RAPID RECOVERY FROM A CRISIS IN 80 YEARS

• FEDERAL RESERVE FORECASTS U.S. GDP GROWTH OF 7.0% FOR 2021 AND 3.3% FOR 2022**.

Historical Global GDP Growth and 2021/2022 Expectations*

8.0 100

90

5.6

6.0 World

4.5 80

4.3

4.0 3.4

2.8 3 3.1 2.8

3.3 3.2 70

2.6 2.5

60

2.0

50 Advanced economies

0.0 40

30

-2.0

20

-4.0 EMDEs

-3.5 10

-6.0 0

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

2021

2022

*World Bank. Note: EMDEs = emerging market and developing economies. Aggregate growth rates are calculated using GDP weights at average 2010-19 prices and market exchange rates. Data for 2020 are

estimates. Shaded area indicates forecasts.

** June 16, 2021 Fed release

10MONETARY POLICY

• FED FUNDS UPPER LIMIT TARGET RATE REMAINS AT 0.25% (SINCE MARCH 15, 2020)

• THE FED’S $120B ($80B TREASURIES & $20B MORTGAGES) MONTHLY BOND BUYING CONTINUES

• GLOBALLY, ON BALANCE, MONETARY POLICY REMAINS HIGHLY ACCOMMODATIVE AND STIMULATIVE

• 60% OF ECONOMISTS POLLED* EXPECT A TAPERING ANNOUNCEMENT IN THE THIRD QUARTER WITH TAPERING TO BEGIN IN EARLY 2022

3/15/20

20

*June 4-10, 2021 Reuters poll of over 100 economists.

Source of Fed Funds Target Range – Upper Limit Graph: https://fred.stlouisfed.org/series/DFEDTARU

11MONETARY POLICY

PROBABILITY OF FUTURE FED FUNDS RATES BASED ON FUTURES MARKET (7/13/21 ESTIMATE)*

100%

100%

93%

93%

100-125

Probability of Future Fed Funds Rate

82%

75% 79%

75-100

66%

62%

50% 21% chance of 50-75

rate hike by July

27, 2022 46%

54% chance of rate

hike by December 25-50

25% 14, 2022

0-25

0%

7/1/21 8/1/21 9/1/21 10/1/21 11/1/21 12/1/21 1/1/22 2/1/22 3/1/22 4/1/22 5/1/22 6/1/22 7/1/22 8/1/22 9/1/22 10/1/22 11/1/22 12/1/22

*Fed Funds Future Projections Source (Based on Futures contracts): https://www.cmegroup.com/trading/interest-rates/countdown-to-fomc.html

*Note: The above Estimate was post announcement of the (0.9%) June 2021 CPI estimate announced on July 13.

12INFLATION FORCES

HISTORICAL ROLLING 12-MONTH INFLATION

Rolling 12-Month CPI vs. Average Annualized Inflation (1947 – June 30, 2021)

16.0%

March-80,

14.59%

14.0%

November-74,

12.20%

12.0%

April-51,

Consumer Price Index (CPI)

9.60%

10.0%

February-70, October-90, July-08, June-21,

6.42% 6.38% 5.50% 5.32%

8.0%

6.0%

4.0%

2.0%

0.0%

-2.0%

-4.0%

1948

1949

1950

1951

1952

1953

1954

1955

1956

1957

1958

1959

1961

1962

1963

1964

1965

1966

1967

1968

1969

1970

1971

1972

1974

1975

1976

1977

1978

1979

1980

1981

1982

1983

1984

1985

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2013

2014

2015

2016

2017

2018

2019

2020

Average Annualized CPI (3.5%) Rolling 1-Year Inflation

Data Source: https://fred.stlouisfed.org

14INFLATION FORCES: 10-YEAR BREAKEVEN INFLATION

• 10-YEAR BREAKEVEN INFLATION WAS 1.8% IN FIDUCIENT ADVISOR’S 2021 TO 2030 TEN-YEAR OUTLOOK (JANUARY 2021).

• BREAKEVEN INFLATION HAS RISEN BY 0.5% TO 2.32% AS OF JUNE 30, 2021 (SINCE THE JANUARY OUTLOOK).

• BREAKEVEN INFLATION PEAKED AT 2.54% IN ON MAY 10 DURING THE SECOND QUARTER AND HAS TRENDED DOWN SINCE.

Source: https://fred.stlouisfed.org/series/T10YIE

15CLASSICAL INFLATION THEORY

INFLATION DEPENDS ON MONEY SUPPLY GROWTH AND THE VELOCITY OF

MONEY.

• MONEY SUPPLY (M2) IS A MEASURE OF THE MONEY SUPPLY THAT INCLUDES CASH,

CHECKING DEPOSITS, SAVINGS, MONEY MARKETS, MUTUAL FUNDS AND CDS.

• VELOCITY OF MONEY IS AVERAGE NUMBER OF TIMES ONE DOLLAR IS USED TO

PURCHASE FINAL GOODS AND SERVICES PER YEAR.

16CLASSICAL INFLATION THEORY

While the M2 money supply expanded significantly, the velocity of money, or the rate at which money is

spent, slowed to its lowest level in 50 years.

U.S. Money Supply and Velocity

30 2.4

M2 Money Supply

25 2.2

2.0

20

Velocity

1.8

15

1.6

10

1.4

5 1.2

0 1.0

Jan-71 May-74 Sep-77 Jan-81 May-84 Sep-87 Jan-91 May-94 Sep-97 Jan-01 May-04 Sep-07 Jan-11 May-14 Sep-17 Jan-21

M2 Money Supply (YoY, left axis) Velocity (right axis)

Unemployment Rate Personal Saving Rate

16 40

14 35

Personal Savings Rate (%)

Unemployment Rate (%)

12 30

10 25

8 20

5.8

6 15

14.9

4 10

2 5

0 0

Sep-16

Jan-17

Jan-18

Jan-19

Jan-20

Jan-21

Sep-17

Sep-18

Sep-19

Sep-20

May-16

May-17

May-18

May-19

May-20

May-21

Nov-19

Dec-19

Nov-20

Dec-20

Apr-19

Oct-19

Oct-20

Jul-19

Apr-20

Jul-20

Apr-21

Jan-19

Jun-19

Jan-20

Jun-20

Jan-21

Aug-19

Sep-19

Aug-20

Sep-20

Feb-19

Mar-19

Feb-20

Mar-20

Feb-21

Mar-21

May-19

May-20

17ADDITIONAL INFLATION CONSIDERATIONS

• THE 2021 DEFICIT WILL LIKELY REACH ~$3.0T (ABOUT 13% OF GDP). OTHER THAN 2020 ($3.1T & 15% OF GDP), THIS IS THE LARGEST FISCAL DEFICIT AS A

PERCENTAGE OF GDP SINCE WORLD WAR II. BY COMPARISON, THE DEFICIT REACHED ~10% OF GDP DURING THE GREAT RECESSION (2008-2009).

• AMBITIOUS SPENDING PROPOSALS EARLY IN THE BIDEN ADMINISTRATION (UPWARDS OF $6 TRILLION) SEEM UNLIKELY TO PASS CONGRESS WITHOUT MEANINGFUL

MODERATION, TEMPERING FUTURE INFLATION SHOCK RISKS.

• THE UNIQUE NATURE OF THIS PANDEMIC-LED RECESSION AND RECOVERY HAVE CREATED SOME UNUSUAL DISTORTIONS WE BELIEVE ARE LARGELY TEMPORARY IN

NATURE AS THE DISCONNECT BETWEEN A POST-PANDEMIC PRODUCTION RAMP-UP AND THE PENT-UP CONSUMER DEMAND WILL NORMALIZE OVER THE

INTERMEDIATE TERM.

18INFLATION: DIVERSIFICATION AND REAL ASSETS

• Real Assets have historically provided an effective hedge against rising inflation.

• Equities have generated positive real returns over the long-term, while fixed income provides good diversification in

periods of economic stress and recessions.

• During periods of rising inflation, while traditional asset classes may see challenging short-term performance, real

assets have produced strong returns.

• Inflation inflection points are difficult to project and time. We advocate for maintaining a strategic allocation to both

traditional and real assets.

Returns on Investments (%) During Various Inflation Environments

Falling Inflation Frequency 18% Stable Inflation Frequency 65% Rising Inflation Frequency 17%

23.2

25

20

14.5

15 10.6 11.8

9.6 8.4 7.9

10 5.5 6.8 6.2 5.4

3.1 3.0 4.5

5 2.3 1.3 1.7 2.7 2.0 1.1

0

-5

-3.5 -3.2 -3.7

-10

-15

-13.4

Stocks US Bonds US TIPS REITS Energy Stocks Metals Stocks Prec Metals Commodities

Period analyzed is January 1973 through December 2020. Real Estate: MSCI World Real Estate Index since January 1993 | Energy: MSCI World Energy Index since January 1995; DataStream World Energy Index from January 1973 to December 1994 |

Metals & Mining: MSCI World Metals & Mining Index since January 1995; DataStream World Metals & Mining Index from January 1973 to December 1994 | Commodities: Equal Sector Weighted S&P Goldman Sachs Commodities Index | Precious Metals:

70% MSCI World Gold Mining Equity Index/30% S&P GSCI Precious Metals Commodities Total Return Index since January 2005; 70% DataStream World Gold Mining Index/30% S&P GSCI Precious Metals from January 1973 to December 2004 | Rising

inflation: any month when Y/Y US CPI rose by +0.3% or more relative to the previous month; Stable inflation period is defined as any month when Y/Y US CPI was between -0.3% and +0.3% relative to the previous month; Falling inflation: any month when

Y/Y US CPI fell by -0.3% or more relative to the previous month.

Past performance does not indicate future performance and there is a possibility of a loss

19CAPITAL MARKET ASSUMPTIONS AND PORTFOLIO POSITIONING

PORTFOLIO POSITIONING

“REAL ASSETS REMAIN AN IMPORTANT DIVERSIFIER AS THE EVENTS OF 2020

HAVE LIKELY PLANTED SOME SEEDS FOR RISING FUTURE INFLATION.”

- FIDUCIENT ADVISORS’ JANUARY 2021 OUTLOOK

6/30/21 YTD (2 QTR 2021) Returns:

Financial Assets

• Global Stocks: MSCI ACWI: +12.3 (+7.4)

• Investment Grade U.S. Bonds: Barclays US Aggregate Bond Index: -1.6 (+1.8)

Real Asset Categories

• Real Estate: FTSE NAREIT Index: + 22.0 (+12.0)

• Commodities: Bloomberg Commodity Index: +21.2 (+13.3)

• Natural Resources: S&P Natural Resources Index: +19.9 (+7.3)

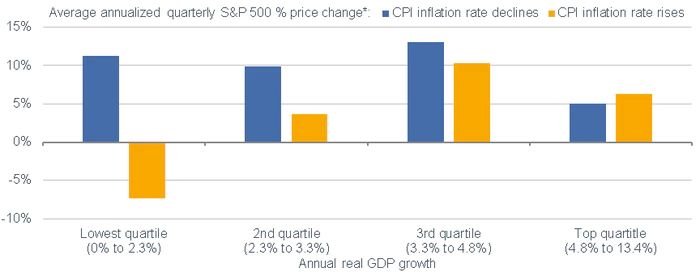

21INFLATION FORCES WITH STRONG ECONOMIC GROWTH (1950 – MARCH OF 2021)

• WHEN INFLATION ROSE, BUT ECONOMIC GROWTH WAS IN ITS HIGHEST QUARTILE, STOCKS NOT ONLY ROSE; THEY ROSE AT A FASTER

CLIP THAN WHEN INFLATION WAS FALLING IN THAT SAME GROWTH ZONE.

• ABOVE TREND INFLATION IS NOT NECESSARILY DETRIMENTAL TO STOCK MARKET RETURNS IF ALSO ACCOMPANIED BY STRONG ECONOMIC

GROWTH

Low Growth High Growth

AND Higher AND Higher

Inflation. Inflation

Source: Charles Schwab, The Leuthold Group, 1950-3/31/2021. *Based only on economic expansions (all quarters when trailing y/y real GDP growth rate was positive). Past performance is no guarantee of future results.

22EVOLVING TEN-YEAR CAPITAL MARKET ASSUMPTIONS (AS OF JULY 1, 2021)

• THE FOLLOWING IS A HIGH-LEVEL SUMMARY OF OUR 10-YEAR CAPITAL MARKET (NOMINAL) FORECASTS IF THEY WERE TO BE

REVISED FOR JULY 1, 2021 (SINCE OUR JANUARY 1, 2021 OUTLOOK).

➢ US INVESTMENT GRADE BONDS: 1.5% (+0.35% SINCE JANUARY).

➢ GLOBAL BONDS: 1.26% (+0.47% SINCE JANUARY).

➢ US EQUITY (5.7%), INTL DEV EQUITY (7.0%) & EM EQUITY (8.3), WHICH ARE GENERALLY WITHIN +/-0.16% OF JANUARY 2021 FORECASTS.

➢ INFLATION EXPECTATIONS: 2.3% (+0.5% SINCE JANUARY)

• FORWARD-LOOKING INVESTMENT GRADE BOND MARKET (NOMINAL) RETURN EXPECTATIONS GENERALLY ROSE WITH RISING

INTEREST RATES AND INFLATION EXPECTATIONS.

• EQUITY RETURN EXPECTATIONS, WHILE GENERALLY UNCHANGED NOMINALLY, HAVE DECLINED ON A REAL BASIS DUE TO RISING

VALUATIONS AND HIGHER INFLATION ASSUMPTIONS.

• DESPITE OUR VIEW THAT ACCELERATING INFLATION IS LIKELY TRANSITORY, INFLATION TAIL RISKS REMAIN. REAL ASSETS REMAIN

AN IMPORTANT STRATEGIC DIVERSIFIER.

• BROAD FINANCIAL ASSET CLASS VALUATIONS ARE ELEVATED CONSTRAINING LONGER-TERM RETURN EXPECTATIONS, BUT THE

CURRENT ROBUST ECONOMIC RECOVERY COUPLED WITH ACCOMMODATIVE FISCAL POLICY AND MONETARY POLICY MAY

PROVIDE A MEANINGFUL INTERMEDIATE-TERM TAILWIND FOR RISK ASSETS.

• OUTLOOK AND GENERAL PORTFOLIO POSITIONING REMAINS CONSISTENT WITH JANUARY 2021.

23Apollon Wealth Management, LLC (Apollon) is a registered investment advisor This document is

intended for the exclusive use of clients or prospective clients of Apollon. Any dissemination or

distribution is strictly prohibited. Information provided in this document is for informational

and/or educational purposes only and is not, in any way, to be considered investment advice

nor a recommendation of any investment product or service. Advice may only be provided after

entering into an engagement agreement and providing Apollon with all requested background

and account information. Please visit our website for other important disclosures.

http://apollonwealthmanagement.comYou can also read