RETIREMENT FUND PORTFOLIOS FOR THE 21ST CENTURY - Nedbank BettaBeta - Nerina Visser November 2013

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

RETIREMENT FUND PORTFOLIOS FOR THE

21ST CENTURY

Nedbank BettaBeta – Nerina Visser

November 2013

AGENDA

An introduction to…

– Traditional fund management in SA

– CPI+ Targeted Return Funds

etfSA Retirement Fund

– Portfolio range

– Back-testing results

– Features and benefits

Questions

Confidential 2HISTORICAL PERFORMANCE OF BALANCED FUNDS

- different large fund managers – 10 years

Very clustered –

herd effect Size affects

performance –

negatively!

Based on monthly total returns: Oct ‘03 – Oct ’13; Nedbank Capital calculations

Confidential 3CORRELATION STUDIES CONFIRM THE “HERD EFFECT”

Correlations vary from 0.89 between Sanlam and Old Mutual…

…to 0.74 between Investec and Allan Gray

Based on monthly total returns: Oct ‘03 – Oct ‘13; Nedbank Capital calculations

Confidential 4TRADITIONAL FUND MANAGEMENT

- what value does it add?

60% Equity, 30%

Bonds, 10% Cash

= better returns!

And the investor has to pay up to

2.5% for this “added value”…

Based on monthly total returns: Oct ‘03 – Oct ‘13; Nedbank Capital calculations

Confidential 5WHAT CAN BE ACHIEVED WITH ALLOCATION TO TRADITIONAL ASSET CLASSES?

Comparative performance of different asset classes – 10 years to Oct-13

Need low correlations to

counteract high absolute

risk

Beware the high risk of negative real

return of some “low risk” investments

Based on monthly total returns: Oct ‘03 – Oct ‘13; Nedbank Capital calculations

Confidential 6PRODUCT INTRODUCTION

Scope and Style

The etfSA Retirement Annuity Fund Range

– Preserve the purchasing power of assets over time

– Targeted real return p.a. (not guaranteed) measured over rolling three years (3%, 5%, 7% above CPI)

– Strategic allocations into a broad range of asset classes, incl.

Equities (Lower risk large cap, Green premium, High dividends, Listed property, Preference shares)

Interest-bearing instruments (Domestic Government and Inflation-linked Bonds and Cash)

International equities (Developed markets, Emerging markets and Africa)

Exchange Traded Commodities (Precious metals, Energy, Agriculture)

Investment style

– Passive, rules-based, optimised trading and investment strategy

– Momentum strategy – allow drift within tolerance limits

– Contrarian strategy – periodic rebalancing to optimised strategic asset class weights

– Minimise “churn” – trade frequency

– No on-going active decision-making

– Transparent and predictable – performs as expected

Confidential 7CONTRASTING PASSIVE TO ACTIVE MANAGEMENT

AND not OR

Index-tracking building blocks ≡ Passive

– ETFs / ETNs are all passively managed

– Advantages: low costs, efficiency, transparency, scalability, tax benefits

Strategic asset allocation ≡ Passive

– Designed to match liabilities / requirements at the lowest possible risk

– Focus is on risk management first, then (excess) return-seeking

– Tactical asset allocation overlays would be considered “active”

Periodic assessment of investment opportunities ≡ Active

– New passive building blocks represent new opportunities

E.g. International bonds, real estate; Corporate inflation-linked bonds, etc.

– Quarterly Trustee meetings to assess changes required to take advantage of these

However:

– NO forecasting

– NO stock-picking or selection of specific securities

Confidential 8WHAT ARE THE BENEFITS OF USING A PASSIVE INVESTMENT STRATEGY?

The etfSA RA Funds allow low cost exposure to indices via ETFs and ETNs – the fee savings are directly passed on to the

investor by way of enhanced performance

It allows for efficient and intelligent planning for retirement funds in developing a truly unique solution that is transparent

and non-emotional, and designed to meet the desired performance targets

No asset management fees (upfront or annually) or performance-based fees

35bps administration fee (excl. VAT) based on the NAV of the fund is accrued daily, deducted from cash / distributions in

arrears at month end (i.e. a reduction in yield, not a cash flow expense)

– This includes all intermediary services of trading, fund administration and custody

– It also includes the TERs of the underlying ETFs / ETNs

– This is all paid out of the administration fee

Confidential 9COMPARATIVE RISK AND RETURN PROFILES

of passive and active strategies

Significant reduction in risk,

for no sacrifice in return

AND it is fully scalable!

Based on monthly total returns: Oct ‘03 – Oct ‘13; Nedbank Capital calculations

Confidential 10STRATEGIC ASSET ALLOCATIONS

etfSA Retirement Annuity Fund Range

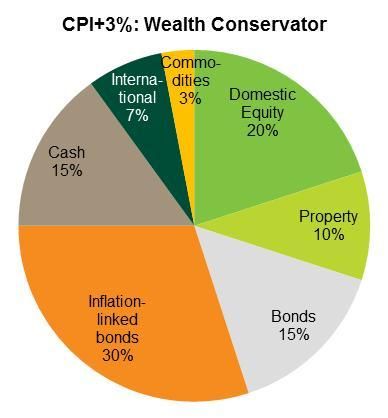

Confidential 11ETFSA WEALTH CONSERVATOR RETIREMENT ANNUITY FUND

CPI+3% return target; Focus on capital protection and income

Composite Benchmark Historical Performance – back tested to 2003

Strategic Asset Allocation

Nedbank Capital calculations; as at 31-Oct-13

Confidential 12ETFSA WEALTH BUILDER RETIREMENT ANNUITY FUND

CPI+5% return target; Balance income with moderate capital growth

Composite Benchmark Historical Performance – back tested to 2003

Strategic Asset Allocation

Nedbank Capital calculations; as at 31-Oct-13

Confidential 13ETFSA WEALTH ENHANCER RETIREMENT ANNUITY FUND

CPI+7% return target; Maximum capital growth

Composite Benchmark Historical Performance – back tested to 2003

Strategic Asset Allocation

Nedbank Capital calculations; as at 31-Oct-13

Confidential 14betta

WHAT CAN BE ACHIEVED WITH ALLOCATION TO TRADITIONAL ASSET CLASSES?

^

Comparative performance of different asset classes – 10 years to Oct-13

Based on monthly total returns: Oct ‘03 – Oct ‘13; Nedbank Capital calculations; Performance of strategic benchmarks for etfSA RA Funds

Confidential 15WHY IS BACK-TESTED PERFORMANCE ACCEPTABLE?

Passive investment strategies are implemented at two levels:

– Assets are allocated to index-tracking investment instruments, e.g. ETFs

– Asset allocation decisions are rules-based and defined upfront – no forecasts or valuations are used

The historic performance of index-tracking passive investments can be approximated by the performance of the reference

index less the total expense ratio (TER)

The asset allocation rules can be applied historically, e.g. rebalancing triggers etc.

The back-tested performance reflects the performance of both the asset allocation rules and the index-tracking investments

It merely has to measure the performance of a static set of rules as no active decisions are taken

Confidential 16ETFSA RETIREMENT ANNUITY FUND

How to choose the right fund for YOU

Identify your specific circumstances, requirements and goals, then match them to the appropriate fund

Conservator Builder Enhancer

Income / yield requirement

High Medium Low

(interest & dividends)

Balance between growth

Capital requirement Capital protection Capital growth

and protection

Time horizon (to expected

15 years

pay-out, not to retirement)

Risk appetite Conservative Moderate Aggressive

Confidential 17ETFSA RETIREMENT ANNUITY FUND

Features and Benefits

Investments are made into a range of ETPs to allow for maximum cost benefit to the investor, and to enhance transparency in

composition, pricing and performance

The portfolios target real returns and achieve risk reduction through diversified exposure to growth assets

Cost efficiency is further achieved through a flat annual administration fees and no initial fees

Distributions received from underlying investments are re-invested into the portfolio immediately when received to maximise

total returns and optimise tax efficiency

It is ideal for investors who are self-employed or already contributing to an employer’s retirement fund and would like to

make additional savings for retirement

Investors can contribute to the fund at any time, on a regular or ad hoc basis

Investors can claim contributions to the fund as a tax deductible expense

Although the portfolios are recommended for long term investment, no exit penalties are charged

In the case of a withdrawal (or payment of benefit), the underlying investments are liquidated at the prevailing market prices

and the total proceeds paid to the investor

In the case of withdrawals from the fund, there may be a tax implication – individual investors need to get their own tax

advice

Confidential 18IN CONCLUSION

What this is not

– A “sexy”, “hip-and-happening” product chasing the latest fad

– A herd-hugger, modelling itself on the peer group

– A promise to always be the top performing fund

– A boom-bust investment profile

What it is

– An independent, optimised, strategic solution that will stick to its targeted mandate and investment style

– A proven dependable methodology

– Transparent holdings and performance

– Low cost – both investment and trading (direct benefit to the client)

Confidential 19THE BETA SOLUTIONS TEAM

Nerina Visser

– BSc, MBA, CFA

– 17 years experience in investment analysis and management

– Top 5 industry (FM) ratings in Quantitative Analysis (#1 in 2006), Risk Management and Innovative Research

Tawuya Nhongo

– MSc in Statistics, CFA

– Six years experience

Mteteleli Sapuka

– BComm, CFA level II candidate

– Six years experience

Contact us BetaSolutions@nedbank.co.za www.bettabeta.co.za

For regular educational insights and news, follow on Twitter: @Nerina_Visser

Confidential 20Questions?

Thank You

Confidential 21DISCLAIMER © 2013 Beta Solutions (Proprietary) Limited This document has been approved by Beta Solutions (Proprietary) Limited (“Beta Solutions”). It should not be considered as an offer or solicitation of an offer to sell, buy or subscribe for any securities or any derivative instrument or any other rights pertaining thereto (“financial instruments”). Some of the information contained herein has been obtained from public sources (including but not limited to data vendors such as I-Net and Bloomberg and the internet) and persons who Beta Solutions believes to be reliable. This document is not guaranteed for accuracy, completeness or otherwise. It may not be considered as advice, a recommendation or an offer to enter into or conclude any transactions. Securities or financial instruments mentioned herein may not be suitable for all investors. Securities of emerging and mid-size growth companies typically involve a higher degree of risk and more volatility than the securities of more established companies. Beta Solutions recommends that independent tax, accounting, legal and financial advice be sought should any party seek to place any reliance on the information contained herein or for purposes of determining the suitability of the products for the investor as mentioned in this document. Beta Solutions and its officers, directors, agents, advisors and employees, including persons involved in the preparation or issuance of this document, may from time to time act as manager or co-manager of a public offering or otherwise deal in, hold or act as market-makers or advisors or brokers in relation to the financial instruments which are the subject of this document or any related derivatives. Unless expressly stipulated as such, Beta Solutions makes no representation or warranty in this document. Neither Beta Solutions nor any of its officers, directors, agents, advisors or employee accepts any liability whatsoever, howsoever arising, for any direct or consequential loss arising from any use of this document or its contents. The information contained in this document may not be construed as legal, accounting, regulatory or tax advice and is given without any liability whatsoever. Past performance is no guarantee of future returns. Any modelling or back-testing data contained in this document should not be construed as a statement or projection as to future performance. This document is being made available in the Republic of South Africa to persons. All trademarks, service marks and logos used in this report are trademarks or service marks or registered trademarks or service marks of Beta Solutions. Nedbank Capital is a division of Nedbank Limited Reg No 1951/000009/06, an authorised financial services provider (licence number 9363), 135 Rivonia Road, Sandown, Sandton, 2196, South Africa. We subscribe to the Code of Banking Practice of The Banking Association South Africa and, for unresolved disputes, support resolution through the Ombudsman for Banking Services. We are a registered credit provider in terms of the National Credit Act (NCR Reg No NCRCP16). Confidential 22

You can also read