MOBILE BANKING Financial inclusion and economic empowerment for the low income population and women in Vietnam - Nguyen Thi Ngoc Anh May 25, 2017

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

MOBILE BANKING Financial inclusion and economic empowerment for the low income population and women in Vietnam Nguyen Thi Ngoc Anh May 25, 2017

Presentation outline § Financial Inclusion: Introduction § Financial Inclusion in Vietnam: A Snapshot § Mobile Banking Project Overview – A shared value concept § Implementation challenges

Financial inclusion

introduction

Financial inclusion means that individuals and

businesses have access to useful and affordable

financial products and services that meet their

needs – transactions, payments, savings, credit and

insurance – delivered in a responsible and

sustainable way

(World Bank)

Financial inclusion

Pillars of financial inclusion

§ Payment system _ key enabler of FI

§ Innovative distribution channels: Financial products / services are provided through both

traditional and innovative channels, focusing on new technology-based distribution

channels (e.g. mobile banking, agent banking)

§ Diversification of financial services providers: including MFIs, non-financial companies.

§ Banks for Social Policy/ Development financial Institutions: still play an important role in

providing the poor with financial services in many countries.

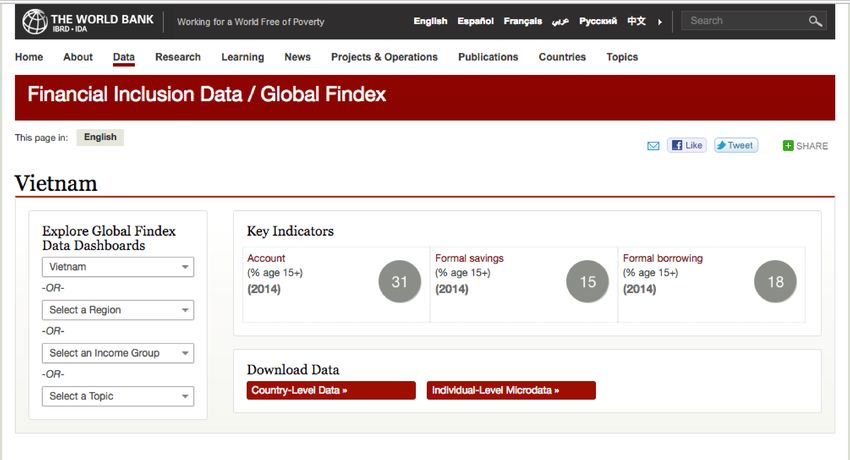

Financial inclusion Vietnam: Snapshot

Financial inclusion

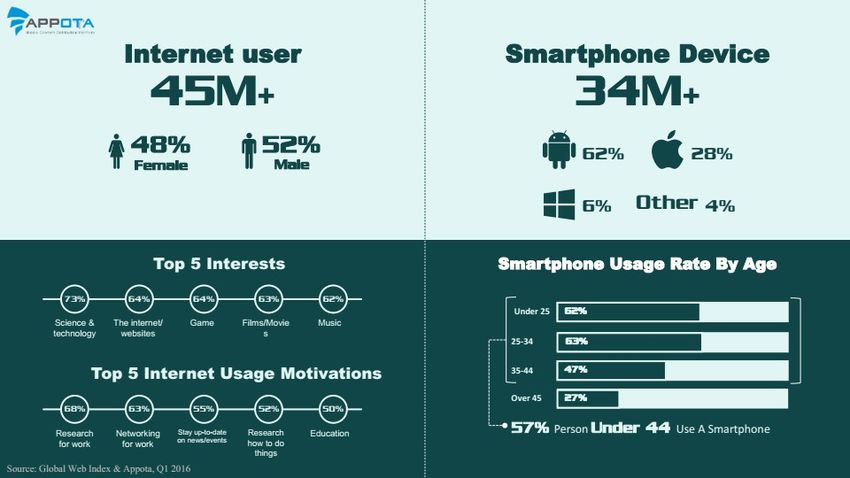

Vietnam: a rapid growth in Telecom network

Population: 91.71 mil. with over 60

mil. in rural areas (2015)

•

Fixed line Subscribers: 5.9

millions

•

Mobile Subscribers: 120.32

millions (3G: 35.78 millions)

•

Broadband Internet

Subscribers: 10.23 millions

•

Internet Users: ~45.5 millions

•

Mobile Signal Coverage: 94%

Source: GSO, MIC 2015 Appota, Vietnam Mobile Report, Q1 2016

Financial inclusion

Vietnam: new players

•

In MF subsector: 02 state-owned financial institutions

(Agribank, VBSP), a Coop Bank and 1,147 PCFs, 3

licensed MFIs (SBV) and about 50 semiformal MF

providers supported mostly by mass orgs, social funds

and donors (MFWG).

•

Among MFIs, VBSP has largest market share (67%) of

total microfinance clients (ADB).

•

Increasing application of modern technology solutions

by banks to expand their products/services in effective

manner. However, not much seen among MF service

providers.

•

FI ecosystem is evolving. Besides financial services

providers, new players like mobile providers and e-

money operators.Financial inclusion

Vietnam: Direction

§ FI is considered as one of key socio-economic development areas. The

Govt. is formulating NFIS.

§ Legal framework is developed to boost financial and technological

infrastructure; diversify financial products/services, set up mechanism for

consumers protection and financial education. SMEs, poor people and

women are priority groups.

§ Policies directly promote FI:

• National Strategy and Plan for Microfinance Development in Vietnam by 2020

(Dec.2011);

• Master plan on development of non-cash payment in Vietnam during 2016-

20 (Dec. 2016): Development of modern means and methods of payments at

rural and far-reaching areas, promotion of financial inclusion; At least 70% of

over 15-year-old people will have banking accounts by 2020.Project overview

Vietnam Bank for Social policies (VBSP)

A public not-for-profit policy bank, serving poor

and near-poor households and other priority

groups.

§ 63 provincial branches, 629 district

transaction offices, and nearly 9,000

employees nationwide.

§ 7 mil. borrowers, nearly 200,000 SCGs at

11,000 communes. Monthly transactions at

MTUs at community nationwide.

§ VBSP’s IT infrastructure upgraded with the

Intellect Core-banking system in all 63

branches.

§ Facing with high operational costs, limited

products/services, ineffective communication

and transparence etc.Project overview Feasibility Study: in 2015, shown positive level of acceptation among VBSP’s clients and operational readiness of relevant service providers, together with positive environment to launch mobile banking services.

The partnership: PPP The partnership: • TAF facilitates VBSP-MC partnership to development of VBSP’s first- ever mobile banking platform for the poor and low-income population. • Shared value concepts: bring both social and business returns Project goal: increase and improve access to a full range of financial services for low-income households, especially women-led microenterprises, and also promote cost-effectiveness and sustainability at VBSP

The partnership:

Shared Value

Increase competitiveness, -

Minimize up-front investment by VBSP

business while improving -

Increase operational efficiency – save time

access to financial and costs

services for the -

New services to clients and reinforce Trust

underserved population. Image of VBSP.

-

Future business opportunities for MC for

market penetration in Vietnam.

-

Greater access to financial services with

increased security and convenience.

-

Economic empowerment, par. for women –

improved ICT knowledge/use, opportunity

-

Promote FI - policy inputs, rep. model

time, increase financial literacy.

-

Support reduction of cash transaction -

Contribute to MC’s financial inclusion

in economy

commitment for 500 mil. people by 2020

-

Enhance operational efficiency in

social development policy lending to

support poverty reduction.Development roadmap

Track 1 Track 2

VBSP sends account-

related information via

SMS text to clients:

- repayment

schedules,

reminders

- Inf. account

balances.

- VBSP new policies

To make the system and

clients familiar with SMS

notification on their

mobile phone and

improve transparency.Challenges

§ Building trust between partners. § Resistance to changes among

§ Partnership building take longer bank staff at HO and branches.

time than expected due to many § Resistance from group leaders

considerations and negotiations in before the threat of losing power.

making investment decisions, § Difficulty faced in reviewing and

getting related approval. verifying phone number of clients

§ Internal procedures for MOUs, in track 1.

contracts take time. § Training group leaders and clients

§ Multi-actors (Polaris, Collega, to get use of the service.

Viettel) involvement in the § Adoption rate is not expected due

process of system configuration, to related telecom infrastructure

planning and operate the FI problems (smartphone users,

platform and Mobile Services. internet system…)Thank you

You can also read