Money printing is not generating a lot of growth - Maurice Info

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

ISSN 1694-318X

www.pluriconseil.com Bilingual Journal of PluriConseil

Numéro 109 : Janvier-Février 2021

"Tout l’art de la politique est de se servir des conjonctures.” Louis XIV

Money printing is not generating a lot of growth

By Sameer Sharma

As we look forward to 2021 and to the prospect of vaccines allowing us to get our lives back in

order, from an economic standpoint at least, the world economy has recovered well and the

COVID impact is looking shallower than what was initially thought. When applying non-linear

machine learning ensemble models to a combination of both higher frequency economic data and

alternative economic data across regions as showcased in Figure 1, global economic activity has

largely recovered mainly led by East Asia and the United States. While a mild dip is likely during

the first quarter of 2021 given the partial curfews and partial lock-downs in some regions, global

economic growth is on pace to exceed 5% next year and has already mostly recovered to

previous levels of economic activity.

PAGE 5

Does velocity of money explain

growth and inflation?

By Eric Ng Ping Cheun

PAGE 8

The debt economy trap

By Mubarak Sooltangos

PAGE 12

Cette île doit être secouée

Par Amit Bakhirta

PAGE 15

Central bank digital currencies

and the war on cash

As global economic slack slowly begins to recede in By Kristoffer Mousten Hansen

the context of ultra loose monetary policies and PAGE 18

given the recovery, global inflation indicators have La portée du méga traité de

begun to rise. A simple de-noising of various

forward-looking market pricing of inflation in the

libre-échange asiatique

Par Riley Walters

United States and in Europe indicates that inflation

risks are once again rising. While global inflation is

likely to be at least 1% to 1.5% higher over the coming five years when compared to the previous

5-year average, shorter term inflation risks should not be dismissed especially as we head closer

to 2022.

The post COVID world (if the vaccines work as advertised and are distributed efficiently) will be

one where previous secular trends such as digitalization (e-commerce, Artificial Intelligence,

robots), inequality, de-globalization, US-China tensions and a focus on economic sustainability

(think ESG) will accelerate. This will be a tougher world where offshore tax jurisdictions will

increasingly be targeted by the usual tax authorities and where those who compete and innovate

will succeed while the rest will not find it as easy as before. When we think about Mauritius, the

solutions for the necessary transformational structural reforms are many and overdue, but the

An electronic journal published by PluriConseil Ltd

Director: Eric Ng Ping Cheun

Address: 38, Aldrin Street, Pointe aux Sables, 11128, Mauritius

Tel: +230 289 6719 Fax: +230 234 2761 Email: pluriconseil@intnet.mu

political willingness to engage in such reforms is sadly lacking because of what this could do to

the system that got politicians elected in the first place.

Figure 1: Index of Economic Activity Figure 2: Estimated Global Index of Forward

Looking Market Pricing of Inflation

Sources: Bloomberg, World Bank Open Data and

Various Open Source Indicators - Author

estimates (PCA + XGBoost Regressor) Data from Bloomberg and Author Estimates

The system of patronage will not take this economy to the next level

Before Mauritius can engage in meaningful structural reforms, it must decentralise economic

policy making away from the office of the Prime Minister, and it must revive technocracy and

chose meritocracy over loyalty and idol worship of the Prime Minister. To be fair, the system has

always been this way because the political system was designed that way at varying degrees, but

this system of nominating loyalists irrespective of competence (and more often than not

irrespective of relevant experience in the field prior to the nomination) who are then more than

happy to worship and allow their institutions to be remote controlled from elsewhere has not and

will not work any more.

Slogans that Mauritius was a “high-income

economy” may work with too many on the island, You need smart people who can

but whether you look at the quality of human take decisions rather than waiting

capital, the lack of productivity and innovation, on orders from elsewhere.

the depth of the capital markets, the dependence

on financial flows and tourist receipts which

helped keep skeletons under the carpet, rising debt, subdued private investment especially when

excluding bricks and mortar related investments, an increasingly unsustainable tax system given

the rising cost of the welfare state, demographic trends and stagnating pre-COVID economic

growth, the true picture is much more complicated.

Sure, the system of patronage may win elections but it will not take this economy to the next

level. You need independent and competent technocrats in key institutions of this country who act

independently but are accountable. You need smart people who can take decisions rather than

waiting on orders from elsewhere. Mauritians of course also get the system and the politicians

they deserve. Politicians love to be worshipped as demigods on the tiny island nation, but too

many like to engage in the worshipping too.

In a country where alternative job opportunities are few and living costs are ever rising, many will

play the “dance to the tune of the powers of the day” game and pick up the nominations even if

they are not qualified for the post. Many of us who have attended parties where recently elected

politicians suddenly get invited and become the canter of attention will laugh about it to some

others, but all of this tamasa is why Mauritius will struggle in the years to come. The notion that a

potential nominee would say “thank you but I have to refuse because this is not my field and I am

not qualified for this role” does not really exist in Mauritius.

Numéro 109 : Janvier-Février 2021 Page |2Over the past 40 years, all of us who live or have lived and worked in Mauritius have been

tempted to go on the “if we cannot beat them, let us join them” route and too many have done so.

Those who do not play such games typically stagnate or leave the country. Mauritius is a small

country with a small reservoir of competent technocrats, and the more it closes the inner circle of

those who make decisions, the worse it will be and has been.

A lot can be said about some in the private

sector too of course. This notion that we need

The rising number of Zombie diversified Jack of all trades but Master in none

companies post-COVID will have businesses despite poor free cash flow levels

longer term implications on and ROCE (Return on Capital Employed)

private sector investments, job versus WACC (Weighted Average Cost of

creation and potential output. Capital) metrics, the over-reliance on debt

rather than on optimal debt and equity funding

mix (long periods of excess liquidity in the

system distort credit risk pricing and behaviour), a passive shareholder base, the lack of

competitiveness, insular thinking by some captains, “quand la construction va, tout va” approach

and a saturated and small market are all factors which explain why the government has had to

step in with massive debt and grant funded public investments which have not always had strong

multiplier effects on the economy pre-COVID. Right now the Bank of Mauritius has provided

regulatory forbearance which has pushed the credit risk can down the road a bit further, but the

rising number of Zombie companies post-COVID will have longer term implications on private

sector investments, job creation and potential output. You can play with rules and make things

look better than they are on paper, but reality bites on all the same.

The benefit of printing money is fast eroding

Whatever I have said so far can be seen in the data too. Mauritius is already lagging. The Bank of

Mauritius is printing large sums of money, but the pre-COVID structural ills, the black listing and

the closed borders means that all this printing is having little effect so far. I supported and pushed

for unconventional monetary policies way back in February 2020 and still do but mainly when it is

driven towards the credit channel (not like what is being done with the Mauritius Investment

Corporation of course – a good idea gone bad by not having the right people at the right places

as usual) and more importantly when it is associated with clear policy guardrails.

Very few in Mauritius understand how complicated it will be for the central bank to efficiently

manage its balance sheet and be a credible inflation fighter in the coming years. The asset

liability management of its balance sheet in any rising inflation scenario would require an

amendment to the Bank of Mauritius Act in order to allow the central bank to go into negative

equity territory so that it can credibly focus on fighting inflation. Those who think otherwise have

simply not done the math.

Figure 3: Tax Revenues are not stagnating Figure 4: Revenues have a long way to go

Source: Statistics Mauritius, Author’s Calculations

Source: Company Quarterly Financials

Numéro 109 : Janvier-Février 2021 Page |3Mauritius, unlike the rest of the world as can be seen in Figure 3, is still struggling. Tax revenues

give us a good sense of what is happening to corporates and to the consumers, and this metric is

quite correlated to local growth. It is not rising!

The two largest conglomerates, namely IBL and CIEL, are diversified across multiple sectors of

the economy, and their quarterly revenue trends also offer us some insights about the pace of

any economic recovery as showcased in Figure 4 (note that GDP numbers in Mauritius lag and

are still stuck at second quarter of 2020 – you can all guess why it takes us longer than the rest).

With tourism earnings not expected to recover in December 2020 and with a weakened Mauritian

consumer (as showcased by tax revenues), one should not expect any meaningful recovery in

those topline numbers soon. More generally, the Mauritian stock market is in the last decile of the

worst performing stock markets in the world in 2020. The graph of the local market (Figure 5)

reflects the state of challenged corporate balance sheets and revenue declines and seems to be

one more higher frequency indicator which points to the still MIA recovery. The stock market is

certainly an imperfect indicator but it is well aligned to other indicators too (in a country where

sadly high frequency data is still not plentiful in 2020 given the politics around it).

Figure 5: A tough year for local equity Figure 6: More money is not creating more

investors units of output

Source: Bloomberg

Author’s calculations

From Figure 6, we can see that the velocity of money (the same trend is observed if you use base

money versus M3) decline has accelerated in recent quarters. We can print but it is not

generating a lot of growth because of our structural ills pre-COVID, the blacklist and the closed

borders. The only positive from this picture is that given low global inflation over the past decade

(imported inflation pressure was low), high growth in both base money and M3 did not lead to

higher domestic sourced inflationary pressures since the economy tended to operate below

capacity/potential. The significant slack still found in the Mauritian economy today means that

shorter term domestic sources of inflationary pressure are unlikely to play the spoil sport despite

all the money printing, but if we start getting more inflation from abroad or even if we begin to get

a more meaningful recovery after the opening of borders in the coming 2 to 3 years, then the

chart below will put the Bank of Mauritius in quite the conundrum.

A country can print all the money it wants for a time but if it cannot increase its capacity to

produce more goods and services with it, then it will turn against the country. How long can

Mauritius keep on printing money, pretend that it has near zero fiscal deficits given monetization

and not see growth pick up? It has been six months since Mauritius emerged from a successful

lock-down, and Figure 1 has shown that the world is already moving on, but it does not yet seem

clear to this author at least that policy makers have engaged in meaningful introspection about

why their policies are not working as the benefit of printing money is fast eroding.

Sameer Sharma is a chartered alternative investment analyst and a certified financial risk manager.

Numéro 109 : Janvier-Février 2021 Page |4Does velocity of money explain growth and inflation?

By Eric Ng Ping Cheun

Policymakers, in Mauritius as elsewhere,

have been pumping money into the

economy in a bid to mitigate the disastrous

impact of the Covid-19, let alone to restore

economic growth. Such a policy is based on

the monetarist assumption that more money

always leads to more spending. Still,

Mauritius’ real gross domestic product

(GDP) would contract by 7.0% in the fiscal

year 2020-2021, would rebound moderately

by 4.5% in 2021-2022 and would be back to

pre-pandemic level only in 2022-2023,

according to projections made in the national

budget.

Money and GDP

Jun-15 Jun-16 Jun-17 Jun-18 Jun-19 Jun-20

Gross Domestic Product (GDP) 400,565 422,084 446,401 469,744 490,557 457,863

(Rs million)

Year-on-Year Inflation (%) 0.4 1.1 6.4 1.0 0.6 1.7

End of month (Rs million)

Currency with Public 24,018 26,254 28,460 29,088 30,056 36,133

Monetary Base 71,594 70,420 80,702 109,049 105,730 148,347

Broad Money Liabilities (BML) 418,402 454,966 491,497 537,638 571,821 644,330

Monthly Average for year

ended (Rs million)

Currency with Public 23,350 25,760 27,804 29,563 29,698 33,340

Monetary Base 68,506 70,691 77,763 93,861 103,453 121,899

Broad Money Liabilities (BML) 397,079 437,190 476,601 518,398 552,770 605,520

Monetary Ratios

Velocity of Money Supply 1.01 0.97 0.94 0.91 0.89 0.76

(GDP/BML)

Velocity of Currency with Public 17.15 16.39 16.06 15.89 16.52 13.73

(GDP/Currency)

Average Broad Money Multiplier 5.80 6.18 6.13 5.52 5.34 4.97

(BML/Monetary Base)

BML to GDP 0.991 1.036 1.068 1.104 1.127 1.322

Currency with Public to GDP 0.058 0.061 0.062 0.063 0.061 0.073

(Sources: Bank of Mauritius & Statistics Mauritius)

Numéro 109 : Janvier-Février 2021 Page |5For policymakers, interest rates are an instrument of intervention in the economy, but central

banks cannot just change the policy interest rate: they must also manage the monetary base

(also known as high-powered money, reserve money or central bank money), which includes the

currency circulating in the public, the currency physically held in the vaults of commercial banks

and the reserves of banks held at the central bank. In Mauritius, the monetary base more than

doubled from Rs 71.6 billion end-June 2015 to Rs 148.3 billion end-June 2020. Yet, this drastic

increase led to a relatively subdued price inflation (an average year-on-year inflation of 2.2% in

that period) and to a mild economic growth (from +3.9% in 2015-2016 to -6.3% in 2019-2020).

Similarly, broad money liabilities (BML), which comprise cash, deposits and debt securities,

jumped by a hefty 54% while nominal GDP rose by only 14%. Two reasons can explain why

national output grows much slower than money supply: the commercial banking sector transforms

only a part of the base money into money in circulation (maybe because of increased risk

aversion), hence a drop in the average broad money multiplier (BML/monetary base); and holders

of money, both physical and digital, reduce their frequency of transaction – what economists call

the velocity of circulation of money.

Velocity plummets when businesses and consumers spend less and hold their money assets for

a longer period of time. A fall in velocity may defeat the purpose of stimulus measures (which

push up the money supply) whereas its increase may raise expectations about future price

inflation. Now the question remains whether the speed with which money moves is a reliable

indicator of economic activity.

The equation of exchange

The idea of velocity is that the money a person spends for goods and services is used later by the

recipient of that money to purchase other goods and services. For example, a 100-rupee note is

used during a year as follows: a shoemaker pays the 100-rupees to a tomato farmer. The latter

uses the 100-rupee note to buy juice from a shopkeeper who uses the money to purchase bread

from a baker. The 100-rupees has thus served in three transactions: the velocity is 3. A 100-

rupee note circulating with a velocity of 3 finances 300 rupees worth of transactions.

Overall, the money stock is boosted by means of a velocity factor to establish the value of

transactions in an economy in a particular year:

Money supply (M) x Velocity (V) = Value of transactions

Value of transactions = Average prices (P) x Volume of transactions (T)

This gives the famous equation of exchange set out by Irving Fisher in 1911:

MV = PT.

Since T is a measure of the real GDP, it follows that money times velocity equals nominal GDP:

MV = GDP.

If velocity is assumed to be stable, then for a given stock of money, the nominal value of GDP

can be determined. Central banks track velocity (GDP/M) for several definitions of money, but the

Bank of Mauritius seems to focus on broad money liabilities. The velocity of BML dipped below

one in 2015-2016, which means that the average rupee was exchanged less than once in that

year. From 1.01 in 2014-2015, it trended lower to 0.76 in 2019-2020, despite aggressive cuts in

the Key Repo Rate. For currency with public, the velocity also tumbled, from 17.15 to 13.73,

reflecting to some extent the use of cash during the lockdown.

The decline in velocity is a matter of concern for those who, from the equation of exchange, view

money together with velocity as a source of funding: for a given stock of money, an increase in

Numéro 109 : Janvier-Février 2021 Page |6velocity helps finance a greater value of transactions than money can do by itself. In fact, neither

money nor velocity has anything to do with financing transactions.

Consider a shoemaker who sells a pair of shoes to a tomato farmer for Rs 100, and then

exchanges the Rs 100 to buy juice from a shopkeeper. How does the shoemaker pay the juice?

He has financed the purchase of juice not with money but with the shoes he produced. He has

used money to facilitate the exchange: money fulfils

The value of money originates here the role of the medium of exchange. The

number of times the unit of money (the rupee)

from humans’ subjective

changes hands (the velocity of circulation) does not

desire to maintain certain bear on the capacity of the shoemaker to fund his

cash balances. purchase of juice: shoes have been exchanged for

juice by means of money.

Money velocity does not have a life of its own. It is not an independent variable and therefore

cannot cause anything. Velocity is just PT/M and is dependent on the other terms to maintain the

balance of the equation of exchange. This mechanistic equation is not a truism but merely

represents a tautology: that the income and expenditure involved in all transactions must be

equal.

Demand for money

A crucial defect of the velocity concept is that it is an aggregate average that looks at the whole

economic system – a holistic concept that disregards the actions of individuals. From an

individual point of view, prices are determined in every transaction, each time money changes

hands, so an “average velocity of circulation” does not make sense. Moreover, while a “general

price level” can be considered at a certain point in time, it is absurd to measure prices over a time

period as goods and services vary in quantity and quality in time and space.

Everyone needs to keep an amount of ready cash on hand: this desire creates the demand for

money, i.e., the demand for cash holding. Changes in the purchasing power of the monetary unit

are brought about by changes arising in the relation between the demand for money and the

quantity of money available (money supply). The value of money originates from humans’

subjective desire to maintain certain cash balances.

No one ever has cash holdings more than he wants. If he thinks that his cash holdings are

excessive, he will invest the excess in buying goods and services or in lending it through bank

deposits, shares or securities. Cash holdings are not idle money (hoarding), but they render the

service of being ready for any future use. While money changes hands, it is always in someone’s

possession, in the cash balance of an economic agent.

In a weakening economy, people normally wish to

increase their cash holdings instead of spending their As soon as the

money. Recessions, let alone anxiety or uncertainty about pandemic ends,

the economy, tend to dampen the velocity of money by Mauritians will not go

making money as a store of value more attractive than on a spending spree

alternative investments. Since the Mauritian economy had

contracted during the first two quarters of 2020, it would

because the economy

be interesting to know whether domestic saving will recover only slowly.

subsequently shot up.

In any case, households are not flush with cash, and there is currently no glut of savings. As soon

as the pandemic ends, Mauritians will not go on a spending spree because the economy will

recover only slowly. Nevertheless, consumer demand may rebound, more money will change

hands, and this will contribute to the rise in inflation which has already started following the

monetary stimulus.

Numéro 109 : Janvier-Février 2021 Page |7Money unevenly distributed

For sure, the expansion of money supply has not raised the general price level as proportionally

as monetarists would have us believe. This is because the velocity of circulation has not been

relatively constant over time, and the GDP has not approximated that of full employment (output

gap). It remains that inflation is a monetary phenomenon which, however, does not affect

uniformly all sectors and so disrupts the productive structure.

When more money is injected into the economy, an excess of spending over production results.

When spending grows faster than production, price inflation happens. The latter may also arise

without an expansion in money supply if the volume of goods shrinks (supply shock).

Variations in the quantity of money have also microeconomic effects on relative prices – effects

concealed by the equation of exchange – besides the fact that new money enters the economic

system at specific points (via public expenditure or credit creation) and at different moments (in a

sequential manner), favouring certain economic agents to the detriment of the rest. Thus begins a

process of income redistribution in which the first to receive the newly-created monetary units can

purchase goods at prices not yet affected by monetary growth, at the expense of late receivers

who find themselves buying goods at rising prices. Money unevenly distributed not only widens

income inequality but also distorts the structure of relative prices: money is not neutral.

Some economists make a distinction between cost-push inflation, of which exchange rates are a

key determinant, and demand-pull inflation. Actually the two types of inflation are two sides of the

same coin as, at the end of the day, it is effective demand that counts. That said, one cannot fully

understand inflation with the velocity of money. The process by which money comes into the

economy, the credit policy of the commercial banks, the central bank’s management of the

monetary base, the rates of change of the money supply and the discrepancy between demand

and supply of goods and services are all major factors of inflation.

Eric Ng Ping Cheun is the author of Fifty Economic Steps (2018), on sale at Bookcourt, Editions Le

Printemps, Editions de l’Océan Indien, Librairie Le Cygne and Librairie Petrusmok.

The debt economy trap

By Mubarak Sooltangos

The world is holding its breath. Have we found the

panacea that will defeat COVID-19? If we think that

vaccination will harness COVID-19 to manageable levels

or even eradicate it, enough damage has already been

done to national and world economies to rock the world’s

finances. We are probably at the start of an immense

financial crisis, the magnitude of which the world has

never seen.

The reason for this, setting aside the pandemic, is a

phenomenon, rather an evil called “debt-based economy”.

Everybody in this world is living on debt, from households

to companies and countries. Families cannot envisage

buying anything, from household appliances to furniture and cars on a cash basis, with savings

made over time. Companies live on the minimum possible shareholders’ funds and their worth is

constantly being measured by their debt: equity ratio rather than their profit generating potential.

Countries have tied the hands of their citizens and their children for decades to come by

borrowing intensively for investment in public infrastructure often not needed. Let us not talk of

borrowing to buy weapons, from huge credit providers where dirty money reigns supreme.

Numéro 109 : Janvier-Février 2021 Page |8All this denatured scenario has one name: easy credit obtained from third parties via banks and

debenture issues because the ultimate lenders earn interest on their loans. If not, nobody would

have lent money and holders of capital would have invested their money in equity-based

development projects, and we would have protected the world from the doom scenario we are in.

Borrowing on interest is essentially a speculative move, with the hope of earning sufficient profits

in a future full of uncertainty to service interest bearing loans, whose demands are very much

certain and already set in concrete in advance.

If most countries and corporates cannot survive financially a four-month lock down, cash flow

wise, this gives an idea of the magnitude of the debts which they carry on their shoulders to be to

this point crippled. We are all witnessing live the vulnerability of debt-based economy.

The magnitude of the debt economy in figures

• Economists all over the world talk about the necessity of containing national debt because its

repayment is tantamount to a tax on future generations. The International Monetary Fund and

the World Bank have fixed a reasonable maximum indebtedness of 65% of GDP in their

financial reform programmes for distressed countries. At the same time, total world’s debt

stands at USD 253 trillion against a world GDP of USD 79 trillion, and the debt is as high as

320% of GDP. Finally, every country seems to be outside IMF and World Bank’s

recommendations.

• The most indebted country in the world is America, with an explicit debt of USD 24 trillion,

i.e., 115% of its GDP. Explicit debt means all debts accounted for in national accounts. To

this, must be added its implicit debt (unaccounted for), namely financial promises, pensions

yet to be disbursed and obligations for medical insurance to be paid at a future date, which

makes a total of USD 103 trillion. Implicit and explicit debt together make a staggering USD

127 trillion, i.e. 570% of its GDP. As a comparison, America’s explicit debt after World War

Two was 120% of its GDP.

• As compared to America, China’s debt is 57% of its GDP and Russia, a surprising 18 %. This

makes us think twice before we swallow the oft repeated rhetoric that America is the most

powerful country in the world. It depends on what benchmarks we are using. GDP in dollars

and being the biggest economy in the world are not a measure of power because it depends

on what this GDP and wealth creation is built.

• National debt per capita is USD 60,000 in America, USD 1,400 in China and USD 3,700 in

Russia. Russia has the ninth lowest debt per capita in the world.

• Total explicit debt in America is USD 24 trillion, China USD 5 trillion and Russia USD 468

billion.

• GDP in America is USD 22 trillion, China USD 11,3 trillion and Russia USD 1.1 trillion.

• Expressed as a percentage of world GDP, America’s GDP is 27% and China 14.3%.

Some facts about the US Dollar

! America controls 18% of world trade but the proportion of the total world’s trade flux

conducted in US dollars is 57% (Euro 30% and GBP 5.5%). The amount of non-trade flux, in

the form of speculative, hot money is unrecorded, but may represent 25% of all US dollar

movements. This makes the US dollar by far, at over 80%, the most traded currency in the

world.

! 80% of the world’s energy transactions, mainly oil, is traded in US dollars, while America

exports only 2% of the world’s oil requirements.

Numéro 109 : Janvier-Février 2021 Page |9! Total foreign currency reserves of all countries in the world amount to the equivalent of USD

12 trillion, and 61 % of these reserves are in US dollars, i.e. USD 7.3 trillion. Hence, America

has a further debt of USD 7.3 trillion on its Treasury owed to other countries, and not

expressed in its national accounts. 20% of the world’s Central Bank reserves are in Euros, on

a decreasing trend since 2010 and 2.2% in Renminbi. Assuredly, the wisest

financial/monetary decision made by an American President is that of Richard Nixon, namely

stopping the convertibility of the US Dollar into gold in 1971, otherwise the equivalent of USD

7.3 trillion of America’s gold would, as of today, be the property of foreign countries, if ever it

does possess this amount of gold.

! Under the present circumstances, there is nothing that America can do, by buying or selling

its own currency, to influence the exchange rate of the dollar if it so wishes. The majority

chunk of US dollar exchanges is done by other countries. If the Federal Reserve decides to

use the other monetary policy tool, namely the interest rate, to raise the value of the dollar, it

would be the first loser. Being given that the national debt of America stands at USD 24

trillion, if the Fed hiked up its interest rate by one percentage point, this would cost the

American treasury USD 240 billion of additional interest payment per year.

Who are in the forefront to defend the US dollar?

Finally, the defence of the dollar lies in the hands of foreign central banks, and not the American

Federal Reserve. Any fall in the US dollar would pull downwards the value of the world’s

reserves, kept in dollars. This is an enigma for all economists to solve. The most powerful country

in the world and the first economy in size is the biggest debtor in the world, and it has no handle

on its own currency. Its economic fundamentals have no monetary significance, and it cannot

have a monetary policy of its own. It relies on the quantum of transactions conducted in the world

by other countries in dollars to keep its currency high, because the lower this quantum is, the

lower will be the dollar in value.

Additionally, and cynically, other countries as well want the US

The root cause of dollar to be high, because their national reserves are in

dollars. The dollar is perpetually kept high in China because its

our indebtedness is

central bank always buys the excess of its balance of trade

the financing of new generated by its exporting companies in dollars at a premium,

electoral promises. so as to keep demand for the dollar high. This suits China

admirably because in releasing more renminbi’s via this dollar

purchase on its domestic market than is necessary, it keeps its own currency plethoric and low to

favour its exports. The danger that this excess liquidity fuels inflation is kept at bay by quantitative

anti-inflation measures. If tomorrow another commercial and financial giant decides to embark on

a financial war with America, it has to find other means than destroying the US dollar, because it

has become the backbone of the world’s foreign trade and the lion’s share of all reserves of all

central banks in the world.

What is the nature of America’s debt?

The reason for all this American indebtedness is that its debt is in its own currency and there is

no urgency to repay them via a conversion in other currencies. The bulk of the Treasury bonds

issued by America to finance its budget deficit each year is bought by foreign central banks, and

since these bonds are in dollars, it is as if America will never repay them back, and will keep on

issuing new Treasury bonds to repay old ones as they come to maturity. The only thing that can

spell doom for America is if its creditors convert their dollars in other currencies. But if America

cannot by itself keep its dollar strong, because it cannot have a monetary policy of its own, it

deals violently with all countries which try to make a move to conduct their trade in other

currencies and to get rid of the hegemony of the dollar. Ghaddafi has paid with his life his

“impropriety” of trying to establish his “Gold Dinar”, backed by Libyan gold reserves, as a new

monetary standard to finance trade within the African continent. We can bet that any country

trying to convert its dollar reserves into other currencies will meet the same fate as Libya.

Numéro 109 : Janvier-Février 2021 P a g e | 10Why is America constantly at war?

This is the law of the financially weakest but militarily the strongest, made possible by easy

money being available because of the interest factor, a deadly evil at its core. Besides this,

America has to be perpetually at war to satisfy its demands of all sorts on other countries, and

these demands are so outrageous that they cannot be discussed around a negotiation table. As

an example, cheap Middle East oil prices would place American industries at a disadvantage with

regard to China, Japan, India, South Korea and Malaysia, who buy their oil from the Middle East

when America has its own oil, but with a higher extraction cost. There can no doubt be ways to sit

down with Middle East oil producers to negotiate a reduction in their output which will drive their

price higher. But this will involve inviting Iran to the negotiation table, and Iran would impose its

own conditions which America does not want to hear of. So, the preferred American scenario is to

keep the Middle East perpetually at war to drive its oil prices up because of the uncertainty of

war. This gives oxygen to American oil producers and manufacturing industries with a cheaper oil

extracted on their own soil.

Where does Mauritius stand?

Mauritius does not currently have a foreign currency availability problem because its central bank

has a comfortable cushion of foreign reserves of Rs 300 billion. However, these reserves are

likely to deplete month by month because of the country’s chronic balance of trade deficit, which

will not be bailed out, as is usually the case, at least in the foreseeable future by a surplus of

invisible trade (mainly tourism). Mauritius is also not in a position, right now, to measure the

magnitude of its eventual loss in foreign currency earnings of its financial sector resulting in its

inclusion in the European black list.

The solace we have, in the face of decreased exports of

goods, and probably also reduced financial sector earnings, Heavy investment in

is that with the depreciation of the rupee of around 10%, our infrastructural projects

imports of consumption items will also decrease, but to an of dubious usefulness

extent that we cannot presently measure with any degree of

accuracy. Our other lifebuoy could be an increase in

is a largely unjustified

incoming foreign currency for investment in real estate if financial burden.

these assets depreciate to an extent that will make them

attractive for foreign buyers.

The financing situation of the national budget

Mauritius’ real problem is the financing of its national budget, and in this context, we already had,

even before Covid-19, a very stretched situation because of our national indebtedness which had

reached the limit of reasonableness. The alarming point is that if money has to be injected in the

economy to prevent business failures and destruction of jobs, the budget deficit will have to

increase substantially, especially in a phase where reduced activity in all sectors will result in a

substantial loss of tax revenue. A reality which has for long remained unnoticed is that for years,

our budget deficit of around 3% of GDP (Rs 16 billion) has not gone into measures to boost

economic activity, but into financing a chronic debt servicing burden of about Rs 13 billion yearly.

So, whatever economists may say about budget deficits being a financial tool to boost activity,

this is absolutely not the case for Mauritius because we also have been living chronically on debt

at national level. I am not in the same line of thought as the IMF and their assumption that above

65% of GDP, a country exceeds the upper safety limit, because many other developed countries

are still thriving with a debt of 120% of their GDP. However, we must all admit that, contrary to

well managed economies, our national debt has no useful and productive corollary. If we give

some thought to the reason why we are so heavily indebted, the implacable reality is that the root

cause of our indebtedness is the financing of new electoral promises made at each election

campaign, which, like old age pension, free bus fares and others become permanent items of

expenditure. Heavy investment in infrastructural projects of dubious usefulness, for whatever

Numéro 109 : Janvier-Février 2021 P a g e | 11reason, is also a largely unjustified financial burden. Enough to say that we are living under

crippling debts conditions as well.

Matters can become worse if we have to borrow in foreign currency in a durable balance of

payment deficit situation to keep our reserves at a level which is necessary to keep our country’s

credit rating still attractive for foreign lenders. The other aspect that nobody comments on is the

fact that our published foreign reserves figures are expressed in Mauritian rupees, and our rupee

has suffered a 10% depreciation in one year, albeit for justified reasons. But this also forms part

of management of public opinion.

Mubarak Sooltangos (msooltangos@gmail.com), a consultant, is the author of Business Inside Out (2018)

and World Crisis - The Only Way out, just published this month.

Cette île doit être secouée : le besoin de rêver

Par Amit Bakhirta

« Inventez-vous, puis réinventez-vous. »

Charles Bukowski

L’année 2020 a

indubitablement été une

année qui a ramené

notre monde à une

réalité oubliée mais aussi

brutalement réelle : celle

de la supériorité de la

nature sur l’humanité.

Elle nous a très

certainement rappelé

que nous restons

humblement vulnérables

à son évolution, à sa

mutation. Notre planète

reste suspendue dans

l’infinité de cet univers

dont nous connaissons et

comprenons si peu. Aussi

délicate, sublime et

harmonieuse qu’est la planète Terre, aussi impitoyable qu’elle puisse être : ainsi est le concept

métaphysique du paradis et de l’enfer – l’équilibre universel. Une terre en évolution dicte

l’évolution naturelle d’une économie, peu importe la directionnelle. Ainsi donc, une évolution de

son tissu socio-économique fondamental est inévitable si une nation rêve de prospérité. Elle se

doit.

Si l’évolution est restreinte, l’économie et ses participants ont souvent un besoin urgent d’un

secouement. Un shake qui shake vraiment ! Maurice, à notre humble avis, à ce carrefour de son

histoire socio-économique, en a cruellement besoin. Cette île doit être secouée.

Relier l’Asie à l’Afrique

Pourquoi ? Alors que nous entamons cette décennie, nous ne pouvons que réaliser la suprématie

économique, technologique et militaire de la Chine dans le monde moderne d’ici à 2035 (avec

prudence). La géopolitique internationale n’a pas été aussi cruciale depuis la fin des première et

deuxième guerres mondiales lorsque la suprématie mondiale a changé de mains. La Chine

Numéro 109 : Janvier-Février 2021 P a g e | 12dépassant le PIB des États-Unis d’ici à 2035 pourrait vraisemblablement être la transition

macroéconomique la plus importante que la planète connaîtra au XXIe siècle. La montée du

système socio-économico-politique hybride du communisme-capitalisme par rapport à la réalité

démocratique-capitalisme d’aujourd’hui aura des implications énormes sur les générations à

venir. Beaucoup d’entre nous ne le verront pas. Certains si. Certains auront ainsi la fortune de

vivre une transition mondiale si puissante que la future politique mondiale, la macroéconomie

mondiale et les structures monétaires et financières mondiales seront remodelées.

Pour cette seule raison, Maurice se doit de renforcer ses relations diplomatiques avec la Chine,

l’Inde, la Russie, le Brésil et surtout l’Afrique. L’avenir sera probablement dicté par l’énormité

d’une consommation interne dans ces pays. Nos décisions stratégiques géopolitiques dicteront

donc l’île Maurice de demain. Nous ne pouvons que lui consacrer des ressources adéquates.

Nos liens géopolitiques, notre roue économique et nos marchés financiers doivent être innovés

de telle sorte qu’ils relient véritablement la puissante Asie à la frontière de la croissance, l’Afrique.

L’économie mauricienne ne peut plus se permettre ce neuf à cinq obsolète. Nous devons ramer

24/7, et cela vers l’Afrique, patrie des opportunités. Des opportunités qui peuvent

vraisemblablement conduire Maurice vers une prospérité socio-économique de 1 000 milliards de

roupies de PIB.

Comment ? Jusqu’à ce que nous, en tant que peuple, nous entendions sur une destination socio-

économique aussi spécifique, propulsés par des bons dirigeants à la servitude altruiste de notre

nation et qui nous bénissent avec l’intellect requis et un environnement propice pour atteindre cet

objectif quantifiable avec des multiplicateurs socio-économiques sensibles, nous resterons sans

direction !

Des décisions et réformes politiques publiques et privées difficiles et importantes doivent

alimenter notre réinvention économique ; nonobstant cela, Maurice risque avec le temps de

perdre tout avantage concurrentiel.

Si le navire socio-économique mauricien n’a pas de destination socio-numérique claire, le pays

naviguera alors à l’aveugle, étant semblable à sourire à une belle femme ou bel homme dans

l’obscurité totale.

L’Afrique reste notre panacée

Nous devons nous asseoir, briser cette économie, et déterminer comment nous ferons évoluer

notre structure économique, pour une croissance durable et inclusive qui nous amènera cet

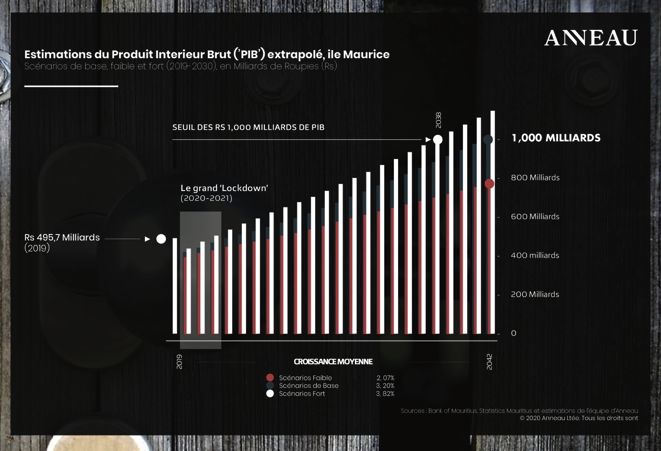

objectif numérique. D’un PIB d’environ 496 milliards de roupies en 2019, nous atteindrons au

mieux ce chiffre de 1 000 milliards de roupies en 2038 (après 18 ans et en supposant un taux

nominal de croissance moyen pondéré du PIB de 3,8%). Doubler le PIB d’un pays n’est certes

pas une tâche facile, mais la taille insignifiante de Maurice à l’échelle mondiale nous aide. La

Chine et l’Afrique étant deux économies de consommation super massives, nous ne pouvons que

vouloir nous en nourrir.

L’industrie mauricienne doit être réinventée, doit être « africanisée » ; autant que stratégiquement

possible. Ne réinventons pas la roue mais polissons-la. Nous avons besoin des meilleurs

cerveaux que ce petit morceau de terre au milieu de l’océan Indien puisse produire. Nous avons

également besoin des meilleurs Africains (il existe déjà un vivier incroyable de jeunes hautement

talentueux, intellectuels, qualifiés et non qualifiés en Afrique ; l’intellect certes ne connaît pas de

frontières).

Les chasseurs locaux sentent toujours les « proies » locales différemment et surtout

distinctement. Et l’Afrique a 54 territoires de chasse si différents pour notre petite économie. Vous

ne pouvez pas rêver de chasser dans la jungle africaine sans les bons outils de chasse et une

connaissance approfondie du terrain. Pourtant, de nombreux grands conglomérats locaux ont

essayé et échoué. Cependant, l’échec fait partie de l’apprentissage, partie intégrante de

Numéro 109 : Janvier-Février 2021 P a g e | 13l’éducation, de l’innovation, de la croissance, du progrès et de la prospérité. Pourtant, au niveau

national, notre culture en décourage.

Pourquoi la culture américaine est-elle si

Nos décisions stratégiques entrepreneuriale ? Parce qu’elle honore,

géopolitiques dicteront l’île séquentiellement, ceux qui essaient, échouent et

Maurice de demain. apprennent de leurs erreurs, repartent et réussissent.

Des gens partout, malgré des cultures socio-

économiques, juridiques et politiques variées, sont

souvent confrontés aux mêmes besoins et désirs, et l’Afrique reste donc notre panacée. Leurs

marchés restent raisonnablement sous-desservis (pour 1,2 milliard de consommateurs, peut-être

3 milliards d’ici 2030). Un alignement privé-public des intérêts à long terme sera très

probablement la base de ce « grand rêve ». Mais on ne peut aimer la mer des tropiques sans

aimer la chaleur !

Nous avons besoin d’une voix économique forte à la table de l’Union africaine. Une voix qui

reflète l’ambition socio-économique de notre nation. Maurice doit à nouveau oser de rêver grand.

Nonobstant, sans plan, un rêve reste un rêve.

Opportunité de levier unique

Nous entamons un nouvel ordre de cycle d’investissement. La pandémie de Covid-19 a accéléré

de profonds changements dans le fonctionnement des économies et des sociétés. Nous voyons

des transformations à travers la durabilité, les inégalités, la géopolitique et la politique

macroéconomique. Cela se reflète dans nos thèmes d’investissement en 2021, celui-ci devenant

de plus en plus intellectuellement difficile. À ce stade socio-économique, les taux d’intérêt

globalement bas couplés à la faiblesse des taux de croissance économique dans les pays

développés obligent les entreprises mauriciennes à être pleinement et intelligemment pompées

de dettes jusqu’au cou !

La structure du capital de nos entreprises locales doit donc, autant que possible, être imprégnée

d’une dette libellée en roupies et en devises étrangères historiquement peu coûteuse mais

productive (expansionniste) et se concentrer sur la croissance. Les activités de fusions et

acquisitions ainsi que les restructurations de capital devraient être en plein essor ; le marché,

dans de nombreux espaces, est mûr pour une consolidation suivie d’une expansion régionale

stratégique. C’est le moment de s’endetter, par des dettes massives (mais sachez en utiliser à

bon escient avec des opportunités d’entreprise inorganiques raisonnables et importantes ; les

rachats d’actions, même ceux avec effet de levier, sont plus sensés que jamais).

Avec une forte hausse des niveaux d’endettement public et privé à l’échelle mondiale et une ère

inflationniste mondiale faible, la croissance restera probablement anémique dans un avenir

prévisible. Les bons du Trésor ont un rendement négatif à moins de 1% dans les pays

développés. Dans le grand monde émergent, elles s’en tirent nord de 3% à 6% tandis que les

euro-obligations africaines en devises fortes rapportent au nord de 4% à 12%, attrayants vis-à-vis

des taux d’inflationnistes nationaux supérieures et donc des opportunités d’arbitrages. Par

conséquent, dans cet environnement actuel, nous prévoyons une croissance inférieure à la

normale à Maurice, à moins des réformes indispensables, ce qui prend malheureusement du

temps.

Les marchés des capitaux en feu en 2021

Chez Anneau, nous maintenons notre instant plus pro-risque tactiquement en 2021 en ajoutant

une surpondération et une concentration des actions nationales alors que nous voyons la

plausible reprise économique s’accélérer (des bas de 2020). La prime de risque sur les actions

nous paraît raisonnable et la baisse des taux réels pourrait lui permettre de se comprimer

davantage, soutenant les valorisations sélectivement – localement et internationalement.

L’accent doit donc être mis sur la valeur avec une inflexion pour la qualité et les noms robustes,

Numéro 109 : Janvier-Février 2021 P a g e | 14en particulier dans les marchés émergents à haut rendement qui, selon nous, connaîtront le

changement tactique mondial tant attendu dans les prochaines décennies. Nous voyons de telles

expositions fournir une résilience au début de la nouvelle

année, en particulier si le soutien budgétaire déçoit aux Que les crises soient

États Unis ou si le déploiement des vaccins est retardé. excellentes pour des

Nous favorisons donc également certaines expositions réformes audacieuses

cycliques que nous considérons comme florissantes à

et intelligentes.

mesure que le calendrier du déploiement généralisé des

vaccins avance.

En 2021, nous prévoyons que la Banque de Maurice fera plausiblement face à des temps

difficiles à venir, car elle devra équilibrer la nécessité de maintenir des taux d’intérêt bas pour

stimuler cette reprise économique et elle fera face à un besoin de resserrement à mesure que

l’inflation s’accélère (2,4% reste probablement le décollage), avec une roupie sensiblement plus

faible, surtout si nous ne transformons pas la Mauritius Investment Corporation en un inducteur

de croissance nette de l’inflation – les yeux sur nos réserves et la roupie.

2021 verra réduire le risque d’une hausse rapide des taux d’actualisation affectant les

valorisations dans presque toutes les classes d’actifs. Nous aimons les actifs durables, car le

virage tectonique vers la durabilité ne fait probablement que commencer. Nous voyons

également un plus grand rôle pour les actifs exposés sur le marché chinois et les actifs du

marché privé pour le rendement, l’appréciation potentielle et l’exposition à des tendances de

croissance uniques.

L’économie mauricienne ne peut pas se caser à cinq heures dans ce monde moderne ! Nous

devons réinventer ce moteur pour que nous passions à un modèle économique 24/7 et devenir le

« Monaco » africain. Que les crises soient excellentes pour des réformes audacieuses et

intelligentes. Cet objectif de 1 000 milliards de roupies de PIB doit être humblement fixé et

respecté. Mais par qui ?

« Les lèvres de la Sagesse sont closes, excepté aux oreilles de la Raison. » (Le Kybalion)

Amit Bakhirta est le fondateur et CEO de la firme Anneau (www.anneau.co), une société de services

financiers à Maurice.

Central bank digital currencies and the war on cash

By Kristoffer Mousten Hansen

Twenty twenty is a year dominated by bad

news. While governments around the world

have imposed extremely destructive

restrictions on economic life and promise a

“Great Reset” that amounts to a great leap

forward into the socialist future, central

bankers have advanced plans for

implementing central bank digital currencies

(CBDCs). These may arrive as early as next

year. Yet what is the motivation behind this

innovation?

Reports recently published by the Bank for

International Settlements (https://www.bis.org/publ/othp33.htm) and the European Central Bank

(https://www.ecb.europa.eu/euro/html/digitaleuro-report.en.html) provide part of the answer.

Numéro 109 : Janvier-Février 2021 P a g e | 15These publications provide fascinating insight into the theories and ideologies driving central

bankers in their pursuit of CBDCs.

Monetary policy? Moi?

One perhaps surprising theme in both reports is the disavowal of any monetary policy behind

plans for introducing CBDCs. The BIS report claims that “monetary policy will not be the primary

motivation for issuing CBDC” (p. 8) and the ECB report notes that a “possible role for the digital

euro as a tool to strengthen monetary policy is not identified in this report” (p. 3). One might first

of all suppose that introducing a new form of money would by definition amount to monetary

policy, at least in a broad sense, and secondly perhaps find it a tiny bit weird that institutions

dedicated to researching and implementing monetary policy would not have considered the

potential effects of a new form of money in light of its effects on policy. But what is really striking

is that both reports – and especially the one issued by the ECB – at great length detail the

implications for monetary policy of CBDC. True, they say they don’t, but looking beyond the

executive summary and paying attention to what is written in the report itself puts the lie to that

claim.

In order to see this, we only need to look at the key features the central bankers identify as

desirable in a CBDC: it should be interest bearing, and it should be possible to cap how much

each individual can hold. Both measures are clearly aimed at supporting monetary policy. The

cap on holdings forces people to spend their money, driving either price inflation or investment in

financial assets, and by making the CBDC interest bearing (or remunerated, in the language of

the ECB) it becomes a tool of setting and passing on policy rate changes, including negative

interest rates.

The ECB’s Report on a Digital Euro (October 2020) in particular goes on at great length about the

need to limit or disincentivize “the large-scale use of a digital euro as an investment” (p. 28). The

reasoning behind this position is crystal clear: since monetary policy has driven interest rates into

negative territory, the ECB should not allow large-scale holding of digital euros, since investors

would then, quite sensibly, chuck their holdings of negative-yielding bonds and seek a safe haven

in digital euros – that is, if they can hold them at no cost.

Similarly, the ECB is averse to letting people convert their bank deposits into digital euros (p. 16),

which would reside in their individual wallets rather than in a bank account. Indeed, the horror of

what the BIS and ECB reports call “financial disintermediation” looms large in the minds of central

bankers: if people keep their money outside of banks, these will have less money to lend out,

thereby increasing borrowing costs. In the words of the BIS report, they are concerned that “a

widely available CBDC could make such events [i.e., bank runs] more frequent by enabling

“digital runs” toward the central bank with unprecedented speed and scale. More generally, if

banks begin to lose deposits to CBDC over time they may come to rely more on wholesale

funding, and possibly restrict credit supply in the economy with potential impacts on economic

growth.” (p. 8)

Of course, Austrian economists, since Ludwig von Mises’ The Theory of Money and Credit

(1912), understand that “financial disintermediation” can really be a blessing. In the context of

digital euros, all it means is that people would hold the amount of cash they deemed desirable

outside the banks. They would only make true savings deposits in banks, i.e., they would only

surrender money that they did not want instant access to.

Under such circumstances, banks would be incapable of expanding credit by issuing unbacked

claims to money; they could only make loans out of the funds their customers had explicitly made

available for that purpose. This would not only result in a leaner or sounder financial system, it

would also avoid the problems of the perennially recurring business cycle. And contrary to what

the central bankers fear, the supply of credit would not be restricted, it would simply be forced to

correspond to the supply of real savings in the economy. This, unfortunately, is an understanding

of economics completely alien to central bankers.

Numéro 109 : Janvier-Février 2021 P a g e | 16You can also read