NHS financial temperature check - Briefing

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

July 2015

NHS financial

temperature check

Finance directors’ views on financial

challenges facing the NHS

Briefing

Contents

Introduction 2

Introduction

Key findings 2

This is the third in a series of HFMA briefings setting

Financial performance 3 out finance directors’ views on financial issues facing

the NHS. Directors completed the survey during the

Quality 8

last two weeks of May 2015. It draws on the responses

What is the outlook? 9 of finance directors and chief finance officers1 (CFOs)

of 117 (47%) provider trusts and 79 (37%) clinical

Conclusion 12 commissioning groups (CCGs) from across the English

NHS. It also includes the views of five of the seven

(71%) Northern Ireland finance directors, four of the

nine (44%) Welsh finance directors and two of the 15

(13%) Scottish finance directors.

Key findings finance directors (59%), 42% of CCG

The 2015/16 financial performance CFOs, 60% of CFOs in Northern

of the NHS in England continues to Ireland and 50% of CFOs in Wales

deteriorate across all sectors. Acute told us they had made significant

trusts represent the majority of the changes to their 2015/16 financial

deficit. There is a deficit overall in plan from what was originally

local NHS organisations and the expected 12 months ago.

small underspend of £151m across In 2015/16 there is a clear

the 211 CCGs does not cover the distinction between the number of

net deficit of £822m in the English English trusts (63%), which are

provider trust sector. Financial plans forecasting a deficit, and the

for 2015/16 show a similar position. number of CCGs (83%), which are

NHS foundation trusts (FTs) reported forecasting a surplus. While the

a £349m deficit for the year-ending percentages look similar, as in

31 March 2015, compared with 2014/15 the CCG forecast net surplus

a planned net deficit of £10m2. is unlikely to be sufficient to cover the

The NHS trust sector reported an net deficit in trusts.

aggregate net deficit of £473m, Fewer than 20% of CCG and 10%

compared with a planned net deficit of trust finance directors think there

of £408m3. is a low risk to achieving their

financial plans for 2015/16.

Analysis of our survey shows: Finance directors are even less

confident about achieving their

Respondents in the majority of financial plans in 2016/17.

CCGs reported that 2014/15 The key risks identified to

year-end outturn was the same or organisations’ and health economies’

1 CCGs use the terminology of chief finance

officer (CFO), whereas NHS trusts and better than budget. But in the majority financial plans are slippage in cost

FTs generally use finance director. In of English provider trusts and Welsh savings, increased demand and

this briefing we sometimes use the term

finance director to mean both finance trusts and local health boards (LHBs) particularly increased emergency

directors and CFOs together, when it was worse. activity.

describing the views of all of our survey

respondents collectively In trusts the main drivers for this 66% of UK finance directors think

2 Performance of the foundation trust sector were an increase in agency staff quality will be maintained in 2015/16,

year ended 31 March 2015, May 2015, costs (72%) and under-achievement 26% think quality will improve, while

Monitor

3 NHS TDA Board meeting, 21 May 2015

of planned savings (55%). CCG 7% think quality will reduce.

Paper D: NHS Trust Service and Financial CFOs considered the main drivers of Respondents felt that within their

Performance Report www.ntda.nhs.uk/wp-

content/uploads/2015/03/Paper-D-Service-

variances to be acute contract organisation they probably have

and-Financial-Performance-Report-for- programme cost increases (66%) or sufficient levers to improve quality

March-2015.pdf for the period ending 31

March 2015

slippage on planned savings (53%). and financial performance, with the

More than half of English trust exception of Northern Ireland.

3

There is less confidence, however, the combined net deficit of £822m in

when asked whether they have the English provider sector, £599m

sufficient levers to effect change in is attributable to 54 acute FTs and

their local areas. £536m to 36 acute NHS trusts. The

Finance directors gave mixed aggregate acute sector deficit of

responses about whether they expect £1,135m is offset by surpluses in the

to see structural reconfiguration in the non-acute sector.

next 12 months, suggesting

reconfiguration will take place based However, there are 27 non-acute FTs

on local circumstances. and NHS trusts in deficit in 2014/15

The majority of finance directors compared with 6 in 2013/14, showing

responding to our survey do not that 2014/15 has been a challenging

believe the organisations in their area year across all sectors.

have sufficient resources to support

their long-term financial plans. Regionally there is little difference,

except in London, where there are

Financial performance proportionally fewer trusts in deficit.

The financial performance of the NHS However, this masks the difference

in England continues to deteriorate between the largely financially

across all sectors. There is a deficit sustainable FTs in inner London and

overall in local NHS organisations the outer London NHS trusts that are

and the small underspend in CCGs struggling to balance their books.

does not cover the net deficit in the

English provider trust sector. In the local commissioning sector,

NHS England reports that CCGs have

The most recent reports from national underspent allocation by £151m in

agencies and regulators show: aggregate, but it was not split evenly

across the country7. According to

NHS FTs reported a £349m NHS England, the underspend in

deficit for the year ending 31 March CCGs includes £156m of planned

2015, compared with a planned net spending on continuing healthcare

deficit of £10m4. 77 of the 152 (51%) claims that was to be made in

FTs reported a deficit5. Acute trusts 2014/15 that has been moved to

represent the majority of the deficit future years, and payments to

but FTs in every sector reported CCGs under the Quality Premium

a deficit. scheme that were £66m lower

The NHS trust sector reported an than planned.

aggregate net deficit of £473m,

compared with a planned net deficit of Excluding these non-recurrent

£408m6. A total of 40 of the benefits, there was a small net

99 (40%) NHS trusts reported a overspend within the CCG sector.

deficit, with a combined gross For 2015/16, NHS England plans

deficit of £614m. to draw down £400m of prior

Across the 211 CCGs, there was a year surpluses in addition to the

small underspend of £151m7 announced 2015/16 allocations,

(0.2% of allocation). According to plus £179m of expenditure deferred

NHS England, ‘this position benefited from the final quarter of 2014/15. 4 Performance of the foundation trust sector

from significant one-off items that Year ended 31 March 2015, May 2015,

Monitor

have materially contributed to the The financial position of the NHS in

5 Year-to-date, unaudited, financial

underspend. Excluding these items, the devolved nations has not been information

there was a small net overspend reported publically yet. 6 NHS TDA Board meeting, 21 May 2015

within the CCG sector’. Paper D: NHS Trust Service and Financial

Performance Report www.ntda.nhs.uk/wp-

Performance against plan content/uploads/2015/03/Paper-D-Service-

The outturn figures reported by Analysis of our survey responses and-Financial-Performance-Report-for-

March-2015.pdf for the period ending 31

NHS England, Monitor and the Trust found that in most CCGs the 2014/15 March 2015

Development Authority (TDA) make it year-end outturn was the same or 7 NHS England Board Paper PB.150528/06,

clear that there is financial pressure better than budget. In the majority May 2015 www.england.nhs.uk/wp-

content/uploads/2015/05/item7-board-

across the NHS. The most severe of English provider trusts and Welsh 280515-upd.pdf

deficits are in the acute sector. Of trusts and LHBs it was worse.

4 NHS Financial Temperature Check

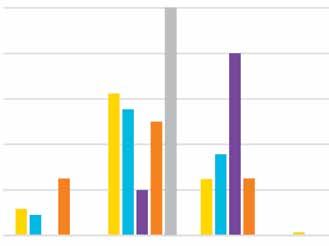

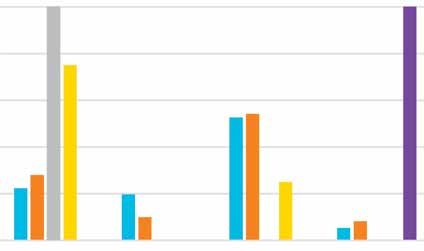

Chart 1: 2014/15 year-end outturn compared with the 2014/15 budget More than 50% of finance directors

in these organisations reported a

n better n same n worse worse year-end position than was

60 planned, as shown in Chart 1.

50

We asked respondents to cite causes

% of finance directors

40 for the main variances between

outturn and plan in 2014/15. Among

30 trusts, the main drivers were a

rise in agency staff costs (72%), in

20

many cases driven by Care Quality

10 Commission recommendations,

and underachievement of planned

0

CCG Trust Health and Local health Territorial savings (55%), leading to adverse

(England) (England) social care trust board board performance against plan.

(Northern Ireland) (Wales) (Scotland)

Some trusts improved their

performance against plan. The main

drivers for this include increased

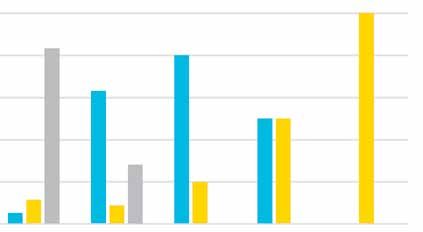

Chart 2: Main variances between 2014/15 outturn and plan in trusts activity and other non-recurrent

items, such as TDA funding, which

80 make it important to understand the

70 underlying financial position as well

as the reported position. Chart 2

60 summarises the main responses.

% of finance directors

50

The reasons remain consistent with

40

our previous surveys. In December

30 2014 we found: ‘Over 40% of provider

trust finance directors reported the

20

main drivers of the worsening year-

10 end financial forecast are unforeseen

0

increases in pay costs, allied with

lower than expected savings from

Rise in Underachievem’t Increase Increase in Increase in Increase in

cost improvement plans’8. The

agency of savings in turnover non-pay clinician other pay

costs plans costs pay costs costs proportion of finance directors

reporting these cost pressures has

increased since December 2014.

While most CCGs achieved or

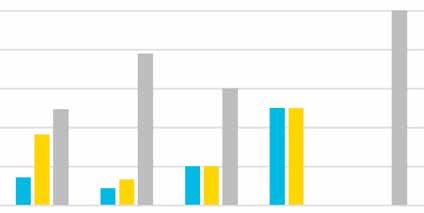

Chart 3: Main variances between 2014/15 outturn and plan in CCGs

improved on planned performance,

CFOs considered the main drivers of

70

variances to be programme cost rises

60

% of finance directors

(66%) or slippage on planned savings

50

(53%). CFOs also identified growth in

40

continuing care claims and contract

30 overperformance by provider trusts

20 in all sectors as additional costs.

10 Chart 3 summarises the responses.

0

Increase in Underachievement Increase in Increase in

These are consistent with our

programme costs of savings plans prescribing costs allocation

on acute contracts survey in December 2014 but the

proportion of CFOs reporting these

cost pressures has increased. In our

previous survey, the figure was 35%

8 NHS Financial Temperature Check for both drivers.

Results, December 2014, HFMA

www.hfma.org.uk/nhstemperaturecheck/

dec14/December 2014 The most common response from

CFOs in Wales and Northern

5

Table 1: Proportion of organisations’ contracts signed by CFOs

Were all contracts signed by Were all contracts signed by

date of survey response? 31 March 2015?

No Yes No Yes

CCG 68% 32% 93% 7%

Trust 58% 42% 90% 10%

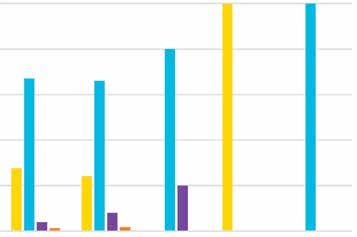

Ireland was underachievement of Chart 4: Forecast 2015/16 year-end financial position

savings plans. In Scotland, the two

n deficit n break even n surplus

respondents both highlighted an

increase in prescribing costs.

100

Contracts and financial plans

The majority of contracts between 80

commissioners and providers in the

% of finance directors

English NHS remained unsigned at

60

the time of our survey, as shown in

Table 1. Some respondents told us

that contracts had been agreed but 40

simply not signed. Other reasons

for not signing contracts included

20

disputes about activity levels, leading

to formal arbitration, or with agreeing

local tariff arrangements. 0

CCG Trust Health and Local health Territorial

In the majority of cases organisations’ (England) (England) social care trust board board

(Northern Ireland) (Wales) (Scotland)

financial plans have been submitted

to their regulator or national agency.

91% of CCG CFOs and 85% of trust forecasting a surplus in their plans,

finance directors told us they had as shown in Chart 4. Some 63%

submitted their plans, with similar of English trusts are forecasting a

levels in the devolved nations. This deficit at the 2015/16 year-end. The

does not mean the plans have been responses for the 2016/17 financial

approved however. In our December year show more trusts forecasting a

2014 survey we found that one in five surplus but the distinction between

trust finance directors told us they the financial position of CCGs and

had been asked to submit a revised trusts remains clear cut.

forecast by their regulator (either

Monitor for FTs or the TDA for NHS Among CCG survey respondents,

trusts), demonstrating the scrutiny 83% forecast a surplus, but it is

applied by regulators. important to understand the business

rules they are required to comply

Almost all organisations revised their with. CCGs are required by NHS

2015/16 financial plan from what was England’s financial planning business

originally expected 12 months ago. rules to make a minimum surplus

More than half of English trust finance equal to either 1% of allocation or

directors (59%), 42% of CCG CFOs, the 2014/15 surplus, less any agreed

60% of CFOs in Northern Ireland and drawdown, whichever is the greater9.

50% of CFOs in Wales told us they However, in the large majority of

had made significant changes. cases the surplus is brought forward

from the prior year, not generated

In 2015/16 there is a clear trend in-year. If CCGs reported on the

showing that, of our survey same basis as provider trusts, the 9 Supplementary information for

commissioner planning, 2015/16,

respondents, English trusts are large majority of CCGs would show a NHS England

forecasting a deficit and CCGs are break-even position.

6 NHS Financial Temperature Check

CCGs are not permitted to spend the surplus in CCGs is not cash-

brought forward resources without backed and so is unavailable for

a specific business case and spending. CCGs are only allowed to

approval from NHS England. submit a deficit plan in unavoidable

The business rules applying to circumstances, as determined by

CCGs mean that in many cases NHS England. However, after taking

these differences into account, the

Table 2: Analysis of forecast 2015/16 financial position by sector CCG sector would still appear to be

in better financial health than the

provider sector.

Sector Deficit Break-even Surplus

Acute 77% 9% 14% The forecast improvement in trusts’

Acute and 85% 0% 15% financial performance in 2016/17 may

community be attributable to finance directors’

expectations that financial recovery

Acute and 81% 8% 12%

plans will address financial difficulties

specialist

brought forward from 2014/15. But

Ambulance 33% 33% 33% trusts will often revise their medium-

Community 0% 0% 100% term financial plans closer to the

Community and 29% 21% 50% beginning of the actual financial year.

mental health

Most English trusts reporting a

Mental health 43% 0% 57% deficit are in the acute sector, while

Specialist 50% 25% 25% community trusts are relatively

financially sustainable, based on

our survey responses. Table 2

Table 3: Analysis of 2014/15 reported outturn by sector summarises the responses. For

(combined figures for NHS trusts and FTs) comparison, the reported outturn for

2014/15 is summarised in Table 3

Sector Deficit Break-even/ surplus showing an increase in the proportion

of forecast deficits across every

Acute (including specialist) 59% 41%

sector, apart from community.

Ambulance 20% 80%

Community 14% 86% In all sectors except the Welsh

Mental health 28% 72% NHS, most respondents told us their

organisation’s forecast 2015/16

Source: HFMA analysis of Monitor and TDA figures

year-end position is worse than the

2014/15 year-end position. Chart 5

Chart 5: Is the 2015/16 year-end forecast position better, the same or summarises the responses. Some

worse when compared with the 2014/15 year-end financial position? 78% of provider trust finance directors

and 50% of CCG CFOs forecast a

n better n same n worse worse financial position at the end of

2015/16 than their 2014/15 outturn.

100

Most respondents reported the

80 degree of risk associated with

% of finance directors

achieving their organisation’s 2015/16

60 financial plan as high or medium,

as in Chart 6. In England, only 16%

of CCG and 10% of trust finance

40

directors reported there being a low

risk to achieving their financial plans.

20 The key risks to achieving financial

plans were identified as:

0

CCG Trust Health and Local health Territorial Slippages in cost savings (74%)

(England) (England) social care trust board board Increased demand (64%)

(Northern Ireland) (Wales) (Scotland) Emergency activity (55%)

Spending on agency staff (50%).

7

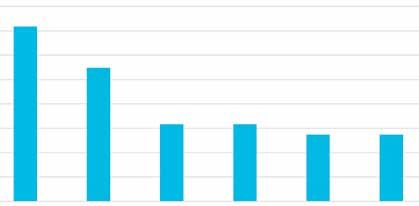

The perceived risk to achieving Chart 6: Finance directors’ estimated degree of risk to achieving their

financial plans increases for 2016/17, organisations’ 2015/16 financial plans

with the majority of respondents n low n medium n high

reporting having plans with a high

level of risk. We asked respondents 100

to identify the main risks to the overall

80

financial stability of their health

% of finance directors

economy. They were:

60

Increasing demand (76%)

40

Increasing emergency care

activity (65%) 20

Slippage on cost saving

schemes (54%) 0

The impact of social care financial CCG Trust Health and Local health Territorial

constraints – for example, delayed (England) (England) social care trust board board

transfers of care (49%) (Northern Ireland) (Wales) (Scotland)

Integration (46%).

We also asked respondents about the Chart 7: The main mechanisms CCGs are planning to meet the

achievability of their organisations’ financial challenges ahead

2015/16 financial savings plans.

Unsurprisingly, respondents were 80

more confident about achieving the

non-recurrent elements of their plans 60

rather that the recurrent savings.

% of finance directors

Some 69% of CCG CFOs and 72% 40

of trust finance directors are very or

quite confident their organisation’s

20

2015/16 non-recurrent savings plans

will be achieved. Respondents in

Scotland feel it is too early to say and 0

there is a mix of views in Wales and Integration/ Increased Investing in Investment Redesigning Reducing

redesigning integration community in primary pathways unnecessary

Northern Ireland. pathways bt health services care within acute clinical

across and social (eg to avoid sector variation

There is less confidence about community/ care/BCF hospital

achieving the recurrent elements of MH/acute schemes admissions)

savings plans. CCGs CFOs have

greatest confidence, with 46% feeling

very or quite confident – slightly Chart 8: The main mechanisms trusts are planning to meet the

higher than trusts, at 39%. financial challenges ahead

100

We asked finance directors about

the main mechanisms they plan on

using to meet the financial challenges 80

ahead. CCGs are planning

% of finance directors

integration of services with other NHS 60

organisations (80%), integration with

social care (76%) and investment in 40

primary care (68%). The responses

are summarised in Chart 7.

20

To meet trusts’ financial challenges,

finance directors plan to make 0

savings on agency staff (87%) and Reducing Procurement Reducing Estates Integration/ Redesigning

pay costs cost savings unnecessary rationalis’n redesigning jobs to cut

procurement costs (81%) and by spent on clinical MH/acute/ the cost of

reducing unnecessary clinical variation agency staff variation community/ non-clinical

(60%). Chart 8 shows the responses. pathways headcount

Respondents from Northern Ireland

8 NHS Financial Temperature Check

are primarily planning redesigned joint working. Some CCG CFOs feel

acute pathways (80%), procurement they have limited influence on the

savings (60%) and agency cost cost of unplanned demand in provider

savings (60%) to meet financial organisations. Some also feel that

challenges. In Wales, respondents provider trusts can become financially

are planning clinical standardisation challenged as a result of conflicting

(100%), investing in community priorities. For instance, national policy

services (75%), integration (75%), changes issued after local plans have

acute sector pathway redesign (75%), been agreed have caused uncertainty

and agency staff cost reduction (75%). in health economies.

Most finance directors agreed Respondents also identified barriers

that their organisation’s stability to finding local solutions due to a

depends on working jointly with perceived lack of a coordinated

other organisations, as summarised approach to system management and

in Chart 9. Respondents provided sustainability by different regulators.

additional details about barriers to

Some provider trust finance directors

feel the scale of their funding can

Chart 9: Assessment by directors of whether their organisation’s determine the success, or otherwise,

stability depends upon working jointly with other organisations of their attempts to influence decision-

making in their health economy –

100 n CCG (England) they cannot effect change unless they

90 n Trust (England) are the largest organisation.

n Health and social

80 care trust (Northern Trust finance directors agreed with

% of finance directors

70 Ireland) their CCG counterparts that the lack

n Local health board of a single voice across the system

60 (Wales)

from regulators has a direct impact on

50 n Territorial board

local reconfiguration. Respondents

(Scotland)

40 recognised that improvement to

services requires joint working and

30

collaboration. However, the size of

20 deficits in some acute trusts can lead

finance directors to make decisions

10

that prioritise the interest of their

0 organisations above those of the

Yes No Don’t know

health economy, to avoid jeopardising

their own financial positions. One

Chart 10: Anticipated change in quality of patient services in 2015/16 respondent suggested the solution is

CCGs and trusts ‘breaking the rules

100 together’ to work more innovatively

n quality will

and address financial problems at

improve

health economy level.

n quality will

80 stay the same

n quality will

Quality

reduce Despite being pessimistic about the

% of finance directors

60 financial position of the NHS for the

n don’t know

current and future years, 92% of all

finance directors do not expect the

40

quality of services to deteriorate.

Some 66% think that quality will stay

20 the same and 26% think that it will

improve. Responses for each sector

are summarised in Chart 10.

0

CCG Trust Health and Local health Territorial

(England) (England) social care trust board board

This is consistent with the results

(Northern Ireland) (Wales) (Scotland) of our two previous surveys in June

2014 and December 2014.

9

But fewer finance directors now think to improve quality and financial

quality will increase. At the same performance – except Northern

point last year, 39% of respondents Ireland, as shown in Chart 11.

thought that quality would increase, Finance directors are much less

compared with 26% in our current confident about whether they have

survey. No respondents in Northern sufficient levers to effect change

Ireland expect quality to improve, in their local areas though – Chart

while in Wales all respondents are 12. There is an overall view that

expecting improvements. Overall 7% there is a weakness in strategic

of finance directors expect quality to system management, which echoes

deteriorate in 2015/16. findings from our previous surveys.

Some respondents felt there are

While the majority of finance directors multiple strategic influences in the

did not expect quality to deteriorate system, which increases the risk that

in their organisations, we asked organisations feel the need to work

them to identify which aspects of in silos. The regulatory regimes for

service quality generally are most CCGs and providers can also conflict.

vulnerable as a result of the current

financial challenges. Respondents

felt waiting times (60%), access to Chart 11: Do you feel you have sufficient levers to effect change that

services (57%), the range of services could improve quality and financial sustainability in your organisation?

offered (43%) and the interface

between NHS care and local authority 100

n CCG (England)

provided social care (40%) were

n Trust (England)

most vulnerable. This was consistent

80 n Health and

across the sectors. social care trust

(Northern Ireland)

% of finance directors

We asked finance directors what n Local

60

changes they anticipate in the quality health board

of patient services commissioned (Wales)

or provided by their organisations 40 n Territorial board

in 2016/17. In total, 84% felt quality (Scotland)

would stay the same or improve,

4% were not sure at this stage and 20

12% felt quality would reduce.

Finance directors reported that it 0

Yes definitely Yes probably No Don’t know

was increasingly challenging to

prioritise access to services and

service performance while maintaining

financial stability. Chart 12: Do you feel you have sufficient levers to effect change that

could improve quality and financial sustainability in your local area?

One said: ‘Patient safety and access

100

to services is not negotiable, so n CCG (England)

pressure on finances is getting worse n Trust (England)

rather than taking alternative courses 80 n Health and

of action. Pressure on finances longer social care trust

% of finance directors

(Northern Ireland)

term will have a detrimental impact

n Local

on the quality and safety of services 60

health board

provided.’ (Wales)

n Territorial board

What is the outlook? 40

(Scotland)

Finally, we asked respondents about

their outlook for their organisations

20

and local health economies.

Improving quality/financial stability 0

Respondents said they probably had Yes definitely Yes probably No Don’t know

sufficient levers in their organisations

10 NHS Financial Temperature Check

Some CCG respondents felt that, sustainability in their local area.

despite having enough levers, Northern Ireland respondents said

national and local guidance can fixed pay scales for medical staff,

conflict, which can remove their nursing staff and fixed staffing

ability to do things differently. For numbers generally are a key element

instance, the national payment of system-wide cost, making it hard to

system can provide disincentives influence financial performance.

for organisations to work together.

One trust finance director felt CCGs Respondents in Wales feel they have

do not have the levers necessary to sufficient levers but do not have

implement plans and that Monitor enough clarity about how service

protects the foundation trust sector reconfiguration will be funded.

from system change.

Long-term plans and policy

Our survey found that only 4% of Most finance director respondents

respondents from CCGs felt they do not believe the organisations in

definitely have mechanisms to their area have sufficient resources

improve the quality and financial to support their long-term financial

plans, particularly in England (92%)

and Northern Ireland (80%) – Chart

Chart 13: Do organisations in your area have enough baseline financial 13. The picture in Scotland was

resources to implement the Five-year forward view or other long-term different – both respondents believe

financial plans without the need for additional support? they have enough resources.

100 n CCG (England)

The key financial challenge is a lack

n Trust (England)

of pump-priming investment funds

80 n Health and social

and that all extra funds are already

care trust (Northern

Ireland) committed to the better care fund

% of finance directors

60 n Local health board (BCF) in England. Some respondents

(Wales) felt the senior management capacity

n Territorial board committed to the BCF would also

40 (Scotland) affect their ability to deliver long-

term financial plans. Respondents

20 also highlighted problems with their

organisations’ funding allocations.

0 Finance directors expressed concern

Yes No Don’t know

about the timing of the £8bn promised

by the government and whether it

Chart 14: Do you support the integration of health and social care in would be enough to meet demand

the format envisaged under the ‘devo Manc’ proposals in England? and new quality initiatives, such as

seven-day services.

n CCG (England)

100

n Trust (England) A major policy development in the

n Health and social care trust (NI) English NHS has been proposals for

80 n Local health board (Wales) integrating health and social care in

n Territorial board (Scotland) the Manchester area – ‘devo Manc’.

Welsh and Northern Irish respondents

% of finance directors

60 generally supported this, English

respondents less so – Chart 14.

40

Specific concerns about the

proposals include possible additional

20 bureaucracy and local politics,

especially where organisations are

not co-terminous. There are also

0 concerns about whether budgets are

Yes No Too early to say Don’t know held in the NHS or transferred to local

authorities and whether the priorities11

of NHS organisations and local Chart 15: Do you expect structural reconfiguration of organisations in

authorities are sufficiently aligned. your area in the next 12 months?

Many respondents are simply waiting

to see whether the changes in 100 n CCG (England)

Manchester are successful or not.

n Trust (England)

80 n Health and social

Alongside integration of health and care trust (Northern

social care we asked respondents for Ireland)

% of finance directors

their views about whether there would 60

n Local health board

be structural reconfiguration of the (Wales)

organisations in their area over the 40 n Territorial board

next 12 months. Chart 15 shows that (Scotland)

opinion is split, suggesting a degree 20

of uncertainty.

0

Action required Yes No Don’t know

We asked respondents to tell us

what actions would be of most help

to meeting the financial challenges in and collaboration, in particular

their areas. The responses covered to reduce demand, especially

national and local issues. emergency admissions.

Recognising that organisations are Finally, finance directors continue

struggling to achieve savings, many to call for honesty from politicians

finance directors felt more realistic with the public about services that

savings targets would be required can be provided within the financial

to help avoid further deterioration in settlement agreed for the NHS.

organisations’ finances. Respondents

felt savings could be achieved in part In a separate question we also asked

by actions to reduce agency staff finance directors to tell us the most

costs and staff costs in general. effective actions they were taking

to improve efficiency in 2015/16.

They also suggested more realistic Responses covered clinical, process,

expectations for reducing activity be local and national issues.

set out in BCF plans and other plans

for integrating services across health Many finance directors described

and social care organisations. local schemes to redesign clinical

pathways and models of care.

As with previous surveys, many Examples include work to improve

finance directors suggest changes case management of patients’

and improvements to the national care across organisational

payment system in England would boundaries, particularly through

help alleviate financial pressure. using neighbourhood-based multi-

Some suggest addressing the disciplinary teams. In addition to this,

purchaser-provider split in England some finance directors are planning

and the system of regulation that to invest in seven-day primary care

surrounds it. services to improve the management

of patient pathways.

Finance directors also called for

greater integration of services, Underpinning clinical developments

specifically more progress on the in their organisations, finance

BCF in England. This is a slight shift directors told us they are planning

in position from our previous survey, to develop their organisations’

when we found that some finance information management and

directors were questioning the technology strategies to improve

feasibility of the BCF as potentially staff mobile working, supporting

too high risk to achieve its objectives. multi-disciplinary teams. Some were

Allied to this, finance directors saw also planning to invest in electronic

the need for improved joint working patient record systems.12 NHS Financial Temperature Check

Finance directors are also planning but many do not feel they have

back-office efficiencies. Examples sufficient levers to make changes

include strengthening the programme they believe are necessary in their

management office in their health economies.

organisation, to help achieve savings

plans, including through reducing In addition, many finance directors

management costs. do not consider they have sufficient

resources for their organisation’s

Allied to this are finance directors’ long-term financial plans. The

plans to make savings through government has made it clear it is

improved procurement. Other extremely unlikely that there will be

measures suggested are to develop additional money beyond the £8bn

innovative contracts and better previously announced to support the

deployment of staff. Five-year forward view in England,

but finance directors feel increasingly

Finance directors also mentioned impeded by barriers to joint working

some plans to improve or safeguard and making changes at health

income streams. For instance, one economy level.

finance director intends to only tender

for contracts that are appropriately Faster progress is needed to achieve

funded, while another plans to the changes outlined in the Five-year

increase non-health income such as forward view in England, but some

from car-parking, retail opportunities areas will need financial support to

and commercial deals such as make this happen.

bedside TV screens.

Finance directors have ambitious

Conclusion plans to achieve savings through

The 2014/15 financial year was more improving their organisations’

challenging than finance directors efficiency, from procurement savings

expected at the beginning of the year. to supporting staff to work in different

Draft accounts show the provider ways. These savings will help to

trust sector overspent significantly protect and maintain services but

and the local NHS organisations in finance directors will not be able to

England in overall deficit. rely on these measures alone to

solve the longer term financial

Finance directors have told us problems due to increasing demand

2015/16 is looking even worse, for services and an ageing

with increasing numbers of population.

organisations forecasting deficits.

Many organisations with plans to

achieve financial balance report

significant risks to their plans and that

the financial risk is not being shared

equally with commissioners.

Across the UK, in spite of the

The authors of this briefing were Richard Edwards

financial challenges, the quality of

(consultant) and Paul Williams (HFMA research

services is largely being protected

manager), under the direction of Emma Knowles

and prioritised. But there are already (HFMA head of policy and research)

signs of pressure, particularly in

waiting times. Although the vast © Healthcare Financial Management

majority of finance directors believe Association 2015. All rights reserved

quality will not deteriorate, they have

concerns that patient safety and Any enquiries should be sent to the publishers at

patient outcomes are vulnerable. info@hfma.org.uk or posted to the HFMA at:

1 Temple Way, Bristol BS2 0BU

Finance directors understand well t: 0117 929 4789

f: 0117 929 4844

the challenges they face and can

e: info@hfma.org.uk

make changes in their organisations,

w: www.hfma.org.ukYou can also read