OCBC CREDIT RESEARCH Special Interest Commentary Wednesday, September 16, 2020 - OCBC Bank

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

OCBC CREDIT RESEARCH

Special Interest Commentary

Wednesday, September 16, 2020

Ticker:

OUECT

OUE Commercial REIT (“OUE-CT”)

OCBC Credit Research does not cover OUE-CT. We present this paper as a special interest

Seow Zhi Qi, CFA

commentary

+65 6530 7348

ZhiQiSeow@ocbc.com

Key Considerations

Acquisition driven growth: Since IPO, OUE-CT has grown through asset injection from its Sponsor,

OUE Limited (“OUE”, Issuer Profile: Neutral (5)) and the combination with OUE Hospitality Trust

(“OUE-HT”). The addition of One Raffles Place and OUE Downtown Office from its Sponsor has

brought total assets to ~SGD4.6bn as at 30 Jun 2019 from ~SGD1.7bn at IPO in 2014. Post-

combination with OUE-HT, OUE-CT’s total assets increased to SGD6.9bn as at 31 March 2020.

While the strategy of OUE-CT comprises acquiring assets from Sponsor and sourcing third-party

acquisitions on its own, we expect OUE-CT to continue to purchase assets from its Sponsor given

the track record.

Benefit from rental support and minimum rent from Sponsor: OUE-CT is receiving rental support

for OUE Downtown Office. Specifically, OUE will provide rental support of up to SGD60mn in total

or for a period from acquisition date (1 November 2018) up to 1 November 2023 (whichever is

earlier). Given SGD26.0mn of which has already been utilized and our base case assumption is that

OUE-CT will continue to benefit from the rental support, we estimate that this support will last till

2Q/3Q2022. In 2Q2020, rental support OUE-CT received was SGD5.4mn (+28.5%y/y). Without

rental support, total return before tax is estimated to fall by 18.8%y/y. OUE-CT also receives

minimum rent of SGD67.5mn p.a. for its hospitality assets from its Sponsor, the master lessor. With

international borders still closed for leisure travel, we expect OUE-CT to continue to benefit from

the minimum rent. Cumulatively, monies from OUE in 2Q2020 were SGD22.3mn (~32% of OUE-CT’s

adjusted total revenue). Overall, we think these highlight OUE-CT’s reliance on OUE especially in

tough times.

At risk of asset revaluation losses: We think OUE-CT runs the risk of its properties getting revalued

lower in the near term due to the poor economic outlook impacting occupancy rates and rent rates

or room rates for its hotel properties. OUE-CT’s aggregate leverage would be negatively impacted

because the denominator would become smaller as a result of a downward revaluation. Based on

figures as at 30 June 2020, a 5% decline in asset valuation would bring about a 2.1ppt increase in

aggregate leverage to 42.2% from 40.1% and a 10% decline would raise aggregate leverage to

44.6%, below the regulatory limit for aggregate leverage of 50% (if EBITDA/Interest as prescribed

by MAS is 2.5x or better). Management has estimated that asset values would need to correct by

~20% before regulatory limit of 50% is breached.

Over 50% of its investment properties have been pledged: OUE-CT’s secured borrowings of

SGD1.5bn are secured by investment properties with a total carrying amount of SGD3.5bn, leaving

OUE-CT with 48.6% of its total investment properties unencumbered (i.e. SGD3.3bn out of

SGD6.8bn). We think One Raffles Place (valued at SGD1,552mn at 31 December 2019), OUE

Downtown Office (SGD912mn) and Crowne Plaza Changi Airport (SGD497mn) remain

unencumbered. In the midst of COVID-19, we think the valuation of hotel properties could be at risk

but expect valuation of One Raffles Place and OUE Downtown Office to be relatively more stable.

While OUE-CT still has assets that it can pledge to banks for loans, the proportion of unencumbered

assets is low relative to the other S-REITs (~85% on average among REITs we officially cover).

Manageable credit metrics in the near term: As at 30 June 2020, aggregate leverage was 40.1%.

EBITDA/Interest based on our calculation is 2.1x, and better at 2.4x if we were to include rental

support into EBITDA. EBITDA/Interest as prescribed by MAS is 2.8x for OUE-CT. Given how interest

rates have come down, we do not expect debt cost to increase over time for OUE-CT from the

current rate of 3.1% p.a. OUE-CT has SGD64.9mn of cash on hand versus SGD576.3mn of debt

Treasury Research & Strategy 1

OCBC CREDIT RESEARCH

Special Interest Commentary

Wednesday, September 16, 2020

coming due in the short term. We think SGD426.3mn of which (a secured SGD loan) will be rolled

over. This would leave OUE-CT with SGD150.0mn of OUECT 3.03% ‘20s to refinance and ~SGD90mn

of capex for rebranding Mandarin Orchard Singapore commencing in 2Q2020. Management has

also shared that maturing debt will be refinanced ahead of maturity and it has sufficient liquidity to

meet its operational and financial commitments with available credit facilities to tap on where

necessary.

I) Company Background

OUE Commercial REIT (“OUE-CT”) is a REIT that invests in income-producing real estate used primarily

for commercial (e.g. office and retail) and hospitality. OUE-CT is listed on the SGX-ST with a market cap is

SGD2.0bn as at 18 August 2020, with total assets of SGD6.9bn as at 30 June 2020. OUE-CT has a portfolio

of seven properties across Singapore and Shanghai, China.

Of the seven assets, four are Grade A office properties. They are OUE Bayfront, 67.95% interest in One

Raffles Place, office components of OUE Downtown and 91.2% strata interest in Lippo Plaza. The first

three are located in Singapore while Lippo Plaza is located in Shanghai. OUE-CT also holds two hotels

and a retail property. They are 1,077-room Mandarin Orchard Singapore in Singapore’s Orchard Road

shopping belt, Mandarin Gallery (retail property) which is situated within Mandarin Orchard and the

563-room Crowne Plaza Changi Airport at Singapore’s Changi Airport. These assets were brought into

the OUE-CT structure following the combination with OUE Hospitality Trust (“OUE-HT”).

OUE-CT is managed by OUE Commercial REIT Management Pte. Ltd, a wholly owned subsidiary of OUE

Limited (“OUE”) who is the Sponsor. We hold OUE at Neutral (5) Issuer Profile as of writing. OUE is a

diversified real estate owner, developer and operator with a real estate portfolio located in Asia and the

U.S. OUE has a ~47.7% stake in OUE-CT as at 31 March 2020 and consolidates OUE-CT results.

OUE-CT has the right of first refusal (“ROFR”) over the Sponsor’s income-producing commercial,

hospitality and/ or integrated development properties.

At IPO in 2014, OUE-CT had an initial portfolio of just two assets – OUE Bayfront and Lippo Plaza.

Subsequently, the REIT has purchased new assets, thus far all from its Sponsor. These include a 67.95%-

interest in One Raffles Place (on 8 October 2015) and office components of OUE Downtown, both

located in Singapore. On 4 September 2019, OUE-CT completed the combination with OUE-HT, which

was similarly sponsored by OUE, though recorded as an associated company by the Sponsor.

OUE-HT, now an unlisted subtrust was once listed on the SGX-ST in 2013 with an initial portfolio of two

properties, Mandarin Orchard and Mandarin Gallery. OUE-HT then acquired Crowne Plaza Changi

Airport and its future extension on an adjacent site in June 2016 from a wholly-owned subsidiary of

OUE, its Sponsor for SGD495mn (total acquisition cost was ~SGD506mn). The property is master leased

to OUE till 27 May 2028, with an option for OUE to renew for two consecutive terms of five years each.

OUE will also provide rental income support for 3 years (which we believe to have ended on 1 August

2019) or totaling SGD7.5mn p.a., whichever is earlier.

Post the combination, OUE-CT has declined the offer to acquire Oakwood Premier OUE Singapore, a 268

room serviced residences which occupy the 7th to 32nd storey of OUE Downtown for SGD289mn under

ROFR. In July 2020, OUE-CT has also declined the offer to acquire USA Bank Tower, Los Angeles from its

Sponsor.

The issuer of OUECT 3.03% 20s and OUECT 4.00% 25s are OUE CT Treasury Pte Ltd. It is a wholly owned

subsidiary of OUE-CT and its principal activities are the provision of financial services for and on behalf of

OUE-CT. The bonds issued by OUE CT Treasury Pte Ltd are guaranteed by OUE-CT.

Treasury Research & Strategy 2

OCBC CREDIT RESEARCH

Special Interest Commentary

Wednesday, September 16, 2020

II) Ownership and Management

OUE, the Sponsor is the largest unitholder with a 47.68% deemed interest in OUE-CT. Followed by the

Tangs, Gordon and Celine Tang who has a deemed interest of 11.37% and 6.55% respectively. As at 9

March 2020, ~35.81% of OUE-CT’s units was held in the hands of the public.

Figure 1: Major Unitholders as at 9 March 2020

Unitholder Shares Deemed interest

OUE Limited 2,570,857,910 47.68%

Tang Gordon (Tang Yigang) 612,784,240 11.37%

Celine Tang (Chen Huaidan) 353,121,062 6.55%

Janet Yeo (Yang Chanzhen) 352,357,703 6.54%

Source: Annual Report

Mr Lee Yi Shyan was appointed as the Chairman and Non-Independent Non-Executive Director of the

Board of OUE-CT Manager on 17 September 2019. Mr. Lee joined OUE as an executive adviser to the

chairman of OUE in January 2016. He is the chairman of OUE Lippo Healthcare Limited and OUE USA

Services Corp, and was the chairman and non-independent non-executive director of the board of

directors of OUE Hospitality REIT Management Pte. Ltd. Prior to joining OUE, Mr. Lee was Singapore’s

Senior Minister of State for the Ministry of National Development, Ministry of Trade & Industry and

Ministry of Manpower. Mr. Lee is currently an elected member of parliament in Singapore for the East

Coast group representation constituency.

Ms. Tan Shu Lin was appointed as Executive Director of the Board of OUE-CT Manager on 31 October

2013. As Chief Executive Officer, she is responsible for the strategic management, growth and operation

of OUE-CT. She was with Ascendas Funds Management Pte Ltd, the manager of Ascendas REIT, as head

of Singapore Portfolio and Capital Markets and Transactions. Ms. Tan holds a Bachelor of Arts (First Class

Honours) in Economics from the University of Portsmouth, United Kingdom, and is also a Chartered

Financial Analyst.

Mr. Lionel Chua is the Chief Financial Officer of the OUE-CT Manager and is responsible for OUE-CT’s

financial management functions. Mr. Chua was the Chief Financial Officer of OUE Hospitality REIT

Management Pte. Ltd. He also has extensive finance and treasury experience at the Keppel Group and

the CapitaLand Group handling financial reporting, financing, cash management, tax and other finance-

related matters. Mr. Chua holds a Bachelor of Accountancy (Merit) degree from Nanyang Technological

University, Singapore. He is a Chartered Accountant of Singapore, or CA (Singapore), with the Institute of

Singapore Chartered Accountants.

Mr. Philip Mah is the Vice President, Asset and Investment Management of the OUE-CT Manager. Mr.

Mah was an Investment Director at RGE Pte Ltd and was responsible for real estate investments in

China. Mr. Mah holds a Bachelor of Business Management (Cum Laude), majoring in Finance from the

Singapore Management University, and is also a Chartered Financial Analyst.

III) Portfolio Overview

OUE Bayfront

Located at Collyer Quay, Singapore, OUE Bayfront, comprises an 18-storey premium office building with

a rooftop restaurant and retail facilities, OUE Tower which is a conserved tower building currently

occupied by a fine dining restaurant and OUE Link, a link bridge with retail units. In total, OUE Bayfront

has a Net Lettable Area (NLA) of 37,144.9 square metre, with office and retail accounting for 94.7% and

5.3% respectively. OUE Bayfront is valued at SGD1,181mn as at 31 December 2019.

OUE Bayfront is on a 99-year leasehold title commencing 12 November 2007. As at 30 June 2020, the

property was fully occupied and continues to record positive rental reversion in 1Q2020 with committed

Treasury Research & Strategy 3OCBC CREDIT RESEARCH

Special Interest Commentary

Wednesday, September 16, 2020

rents above market rents. Nevertheless, we expect both occupancy and office rents to come under

pressure due to the business uncertainty posed by COVID-19 pandemic. OUE Bayfront has a Weighted

Average Lease Expiry (“WALE”) by NLA of 2.5 years and we will see 34.7% of leases by NLA expiring in

2021. The property generated SGD13.8mn revenue in 2Q2020 (21.5% of OUE-CT’s total revenue).

Lippo Plaza

Located in one of Shanghai’s core commercial districts, the property is valued at SGD571mn as at 31

December 2019. Comprising a 91.2% share of strata ownership in Lippo Plaza, it is a 36-storey Grade A

commercial building with a retail podium located at Huaihai Zhong Road, within the established

Huangpu business district in the Puxi area of downtown Shanghai.

Lippo Plaza has a 50-year land use right commencing 2 July 1994. As at 30 June 2020, the building’s

committed office occupancy declined 4.7ppt q/q to 81.1%. This could be due to the slowing office

leasing momentum in the Shanghai CBD Grade A market, amid worldwide business shutdowns. The

overall Grade A office occupancy was 85.4% for 2Q2020 in Shanghai, which was stable q/q. As of

2Q2020, the average passing rent was slightly lower (-0.62% q/q) at RMB9.64 per sqm per day. Putting

pressure on lease rates, Lippo Plaza will see 27.3% of its expiry leases by NLA expire in 2021 and a

further 42.2% expire in 2022. In a bid to cushion the business impact on the tenants, Lippo Plaza has

implemented support measures in line with relevant government advisories in Shanghai to all qualifying

tenants. In 2Q2020, Lippo Plaza generated total revenue of SGD6.4mn, contributing 9.9% to OUE-CT’s

total revenue.

One Raffles Place

The property consists of One Raffles Place Tower 1, a 62-storey Grade A office building, with a rooftop

restaurant and observation deck offering panoramic views of the city skyline, One Raffles Place Tower 2

and One Raffles Place Shopping Mall.

OUE-CT acquired a 67.95% interest in the property on 8 October 2015 from its Sponsor for

SGD1,145.8mn (total acquisition cost was ~SGD1,166mn) while the agreed value then was SGD1,715mn.

With an attributable NLA of 698,184 sqf (office 598,814 sqf and retail 99,370 sqf), the occupancy rate

was 91.4% (down 3.2ppt q/q) for the office component and 96.5% for retail (down 2.6ppt q/q) as at 30

June 2020. The property was valued at SGD1,862mn as at 31 December 2019 (based on OUB Centre

Ltd’s 81.54% interest in One Raffles Place, OUE-CT has an indirect 83.33% interest in OUB Centre Ltd

held via its wholly owned subsidiaries). One Raffles Place has a WALE by NLA of 2.1 years and bulk of the

expiry leases by NLA is in 2021 and 2022 (32.3% and 25.6% expiring in 2021 and 2022 respectively). In

2Q2020, One Raffles Place generated total revenue of SGD14.4mn, contributing 22.4% to OUE-CT’s total

revenue.

OUE Downtown Office

The office building includes the 35th to 46th storey of OUE Downtown Tower 1 and the 7th to 34th

storey of OUE Downtown Tower 2, offering ~530,000 sq ft of Grade A office space. It is part of the OUE

Downtown mixed-use development.

On 1 November 2018, OUE-CT purchased the office components of OUE Downtown for SGD908mn from

its Sponsor (total acquisition cost was ~SGD945mn). Property valuers had valued the property at

~SGD936mn. As part of the transaction, OUE would also provide rental support of up to SGD60mn in

total or for a period of up to 1 November 2023, whichever is earlier. We think there are SGD34mn

remaining as of 30 June 2020. Despite business shutdowns due to measures to contain COVID-19

spread, OUE Downtown Office saw its office occupancy rate fall by 2.9ppt q/q to 91.7% as at 30 June

2020, below average market occupancy rate of 97.1%. Due to consecutive quarters of positive rental

reversions, OUE Downtown Office’s average passing rate has increased to SGD7.39 psf pm from SGD6.94

psf pm at acquisition in 3Q2018. In 2Q2020, OUE Downtown Office generated total revenue of

SGD9.4mn, contributing 14.6% to OUE-CT’s total revenue.

Mandarin Orchard Singapore

Treasury Research & Strategy 4OCBC CREDIT RESEARCH

Special Interest Commentary

Wednesday, September 16, 2020

Located in the heart of Orchard Road, Mandarin Orchard Singapore is a renowned upscale hotel

featuring 1,077 rooms, five food and beverage outlets and more than 30,000 sq ft of meeting and

function space, with strong brand recognition given its long history of operations in Singapore.

Mandarin Orchard Singapore is wholly-owned by OUE-HT.. It is under a master lease arrangement

entered into with OUE. The minimum rent is SGD45mn p.a. The hotel experienced a significant loss of

demand from tourist arrivals, business travels and social events as a result of strict travel restrictions to

contain COVID-19 spread, though there was replacement demand from people on self-isolation and

those affected by travel ban. Overall, the operating environment within the hospitality industry

remained weak in 2Q2020. As a consequence, Mandarin Orchard Singapore saw its 2Q2020 revenue per

available room (“RevPAR”) decline 79.5% y/y to SGD40mn (2Q2019: SGD196).

In a bid to capitalize on the uncertain business environment, OUE-CT announced in March 2020 that

Mandarin Orchard Singapore would be rebranded into Hilton Singapore Orchard with a capex of

SGD90mn (to be borne by OUE-CT) during this downtime. The refurbishment is expected to take place

from 2Q2020 and targeted to be re-launched in 2022.

Mandarin Gallery

The property is a four levels high-end retail mall situated along Orchard Road. The mall is complemented

by Mandarin Orchard Singapore, collectively providing an integrated hospitality and retail experience for

shoppers and hotel guests.

With the COVID-19 outbreak, Mandarin Gallery’s committed occupancy decreased by 3.4ppt q/q to

94.4% as at 30 June 2020, though average passing rent was higher (+2.04% q/q) at SGD22.47 psf pm

despite declines in foot traffic and tenant sales from April 2020 after stricter social distancing measures

being implemented.

Crowne Plaza Changi Airport

Managed by InterContinental Hotels Group, the property is a 563-room hotel situated near Changi

Airport. It is connected directly to Changi Airport Terminal 3 and via a pedestrian bridge from Terminal 3

to Jewel Changi Airport. The hotel is also located a short drive away from Changi Business Park and the

Singapore Expo.

Crowne Plaza Changi Airport is under master lease arrangement, where OUE is the master lessee. The

minimum rent is SGD22.5mn p.a. The hotel was valued at SGD497mn (SGD0.9mn/key) as at 31

December 2019. Due to the weak operating environment posed by COVID-19 pandemic, the hotel’s

2Q2020 RevPAR declined 56.2%y/y to SGD83 (2Q2019: SGD189).

Figure 2: OUE-CT’s Portfolio

Attributable Valuation2

1

Property Leasehold Type & Tenure NLA (sq ft) Occupancy (SGD’mn)

OUE Bayfront Multi-tenanted; 86 years Office: 378,692 100.0% 1,181

(except OUE Link – 5 Retail: 21,132

years)

3

One Raffles Multi-tenanted; Office: 598,814 91.4% 1862

Place Tower 1 & 25% of mall: Retail: 99,370

806 years

Tower 2 & 75% of mall: 62

years

OUE Downtown Multi-tenanted; 46 years Office: 530,487 91.7% 912

Office

Lippo Plaza Multi-tenanted; 24 years Office: 361,010 81.1% 579.3

Retail: 60,776

Mandarin Gallery Multi-tenanted; 36 years Retail: 126,283 94.4% 493

Mandarin Master leased; 36 years 1,077 rooms NA 1,228

Orchard (1.1mn/key)

Singapore

Crowne Plaza Master leased; 63 years 563 rooms NA 497

Treasury Research & Strategy 5OCBC CREDIT RESEARCH

Special Interest Commentary

Wednesday, September 16, 2020

Changi Airport (0.9mn/key)

Source: Company

1

Committed occupancy as at 30 June 2020

2

Valuation as at 31 December 2019

3

based on OUB Centre Ltd’s 81.54% interest in One Raffles Place, OUE-CT has an indirect 83.33% interest in OUB

Centre Ltd held via its wholly owned subsidiaries

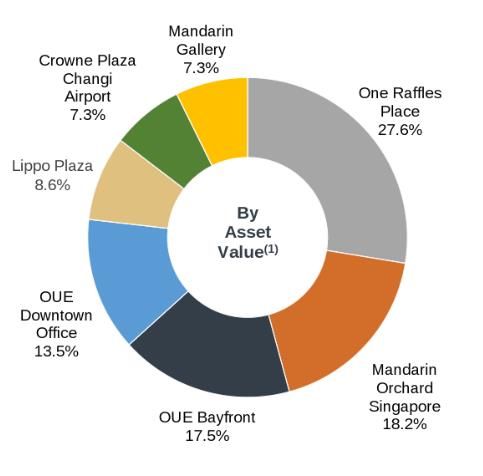

Figure 3: Portfolio Composition by Asset Value1 Figure 4: Portfolio Composition by Revenue1

Source: Company

1

as at 30 June 2020; asset values will only be revalued annually with the next valuation expected on 31 December 2020

IV) Business Analysis

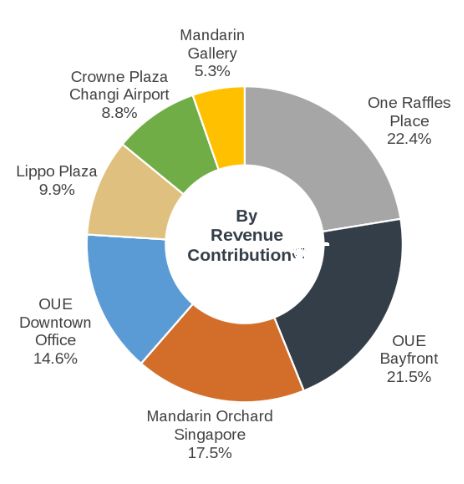

Diversified REIT; most exposure to Office: OUE-CT has three business segments and generates most

of its revenue from Office (62.6%), followed by Hospitality (26.3%) then Retail (11.1%). No single

asset contributed more than 22.4% of revenue in 2Q2020. Across lessees, Hospitality made up

22.3% of OUE-CT’s revenue, followed by the banking, insurance and financial services sector at

20.1% and the retail (excluding F&B) sector at 10.5%. Occupancy rate at its office properties was

91.3% as at 30 June 2020, dragged by Lippo Plaza in Shanghai whose occupancy rate was 81.1%,

below the market average for office properties in Shanghai of 85.4%. In Singapore, OUE Bayfront is

100% occupied, while One Raffles Place and OUE Downtown Office are both at 91% handle when

the market average occupancy in Singapore core CBD office is 97.1%. As at 30 June 2020, expiring

leases at its office properties for 2020 was 11.1% of gross rental income, with the bulk coming from

OUE Downtown Office. Seemingly, OUE-CT has managed to renew some of these leases post 30

June 2020, bringing the expiring leases by gross rental income at the OUE Downtown Office down to

8.6% from 35.0%.

Growth via acquisition of properties from Sponsor: OUE-CT has grown since IPO through asset

injection from its Sponsor and the combination with OUE-HT. As at 31 March 2014, shortly after

IPO, OUE-CT was a REIT with ~SGD1.7bn total assets. The addition of One Raffles Place and OUE

Downtown Office from Sponsor has brought total assets to ~SGD4.6bn as at 30 Jun 2019. Post-

combination with OUE-HT, OUE-CT’s total assets was SGD6.9bn as at 31 March 2020. While the

strategy of OUE-CT comprises both acquiring assets from Sponsor as well as sourcing third-party

acquisitions on its own, we continue to expect OUE-CT to purchase assets from its Sponsor given

the track record.

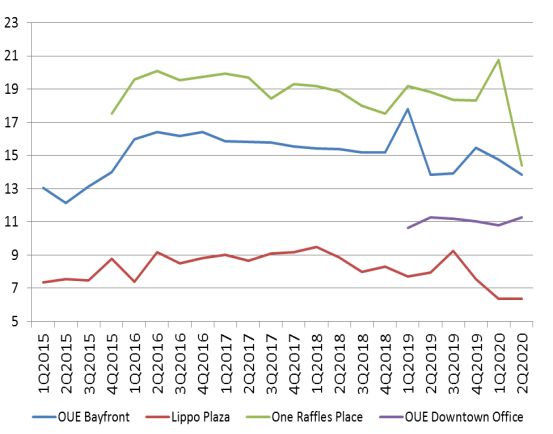

Stable until recently: Excluding Hospitality assets which are on master lease and on a same store

basis (i.e. excluding OUE-HT which combined with OUE-CT in 3Q2019), overall revenue in 2Q2020

was down 15.3%y/y and 16.5%q/q (comparing 1Q2020 with 2Q2020) to SGD44.0mn. While the dip

in 2Q2020 performance of the properties was mainly due to provision for rental rebates to be

extended to qualifying tenants to cushion the impact of business disruption due to COVID-19, we

Treasury Research & Strategy 6OCBC CREDIT RESEARCH

Special Interest Commentary

Wednesday, September 16, 2020

note that in 1Q2020, overall revenue on a same store basis was down 4.7%y/y and up 0.7%q/q.

Broadly, as seen in Figure 6, there is no clear trend on the revenue front for these properties.

Looking ahead, office occupancy and rents are expected to remain under pressure. Therefore, we

think muted organic growth will persist.

Figure 5: Revenue by Property (SGD’mn) Figure 6: Revenue by Property (SGD’mn)

Source: Company

Rental support for OUE Downtown Office already one-third utilized: Rents at the property was

(~SGD7.00 psf pm) lower than average of peers (~SGD8.43 psf pm) when OUE-CT acquired it in 2018

from its sponsor. Therefore, OUE provided rental income top up if actual rental income falls below

the target rent. The rental support is capped at SGD60mn in total or for a period of up to 1

November 2023 (i.e. 4Q2023), whichever is earlier. Based on Figure 7, rental income top up was

utilized every year since acquisition. We estimate that SGD26.0mn of rental support has been

utilized, leaving a balance amount of SGD34.0mn. Given that occupancy rate at OUE Downtown

Office remains below the market average and the economic outlook is weak, we expect OUE

Downtown Office to continue to qualify for rental support and draw down on the full amount

before 1 November 2023. We estimate that the balance rental support will last OUE-CT for another

7 to 8 quarters (i.e. until 2Q/3Q2022). As at 2Q2020, average passing rent is SGD7.39 psf pm, ~20%

below the target rent of SGD9.25 psf pm. Therefore we think rental support running out is a

significant downside risk for OUE-CT as we do not expect OUE Downtown Office to be able to see a

cumulative ~20%+ increase in rents over the next 1.5 years given current market conditions.

Consequentially, total return before tax is estimated to fall by ~19%y/y.

Figure 7: OUE Downtown Office Target Rent vs Average Passing Rent

Average Passing Target Rent Rental Support Top up

Rent (SGD psf pm) (SGD psf pm) (SGD’mn)

Nov & Dec 2018 6.94 8.90 ~2.56

2019 7.16 9.10 ~14.45

Jan to Jun 2020 7.31 9.25 ~8.98

2021 to 2023 - 9.40 -

Total ~25.99

Source: Company

Note: Total NLA is 530,487 sq ft; assumes rental support top ups to full occupancy

Hospitality assets are master leased to Sponsor: The hotels OUE-CT hold via a sub-trust is leased to

the master lessee who will appoint the hotel manager to manage day-to-day operations and

marketing. Mandarin Orchard Singapore’s master lessee is OUE and the master lease agreement is

subject to a minimum rent of SGD45mn per year until July 2028 with an option to extend for

another 15 years. Crowne Plaza Changi Airport is master leased to OUE Airport Hotel Pte Ltd and

the minimum rent is SGD22.5mn per year until May 2028 with the option to extend for two

consecutive 5 year periods. OUE Airport Hotel Pte Ltd is a wholly owned subsidiary of OUE. Given

the COVID-19 pandemic which led to travelling restrictions, minimum rent is especially useful. In

2Q2020, OUE-CT received the full amount of minimum rent from OUE. We note that RevPAR has

Treasury Research & Strategy 7OCBC CREDIT RESEARCH

Special Interest Commentary

Wednesday, September 16, 2020

fallen significantly by 79.5%y/y to SGD40 for Mandarin Orchard Singapore and 56.2%y/y to SGD83

for Crowne Plaza Changi Airport. Assuming travelling remains curtained for the rest of 2020, our

worst case assumption is that revenue from the Hospitality segment for OUE-CT will fall to the

minimum rent amount i.e. SGD16.9mn per quarter. The worst case also alters the scenario to

counterparty risk for OUE-CT where whether OUE-CT will receive the minimum rent amount is

dependent on OUE’s ability to make the payment. We have OUE at Issuer Profile of Neutral (5) as of

writing.

Rebranding to Hilton Singapore Orchard: OUE-CT announced on 26 March 2020 that it is

rebranding Mandarin Orchard Singapore to Hilton Singapore Orchard, which would be the largest

Hilton hotel in the Asia-Pacific region when completed. Works commenced in 2Q2020 and is

expected to be completed in 2022. The capex required is ~SGD90mn. We note that downside

protection from the minimum rent embedded within the hotel master lease arrangement will

continue throughout the phased renovation and ramping-up period. OUE-CT expects a 10% return

on investment on a stabilized basis. It is still too early to say though when international travel would

resume, which would impact on when this stabilized return on investment can be achieved. In the

short term we do not expect material changes to the reopening of international borders in the near

term. Discussions between governments have been protracted while countries facing second waves

have re-imposed restrictions on mobility. The International Air Transport Association (“IATA”) in its

latest views dated 28 July 2020 expects that air travel will not recover to pre-COVID-19 levels until

2024.

Pipeline of assets at Sponsor: Sponsor, OUE, has Downtown Gallery, a ~150,000 sq ft shopping

space spread over six levels. It has a prominent 262 metre wide frontage. Downtown Gallery has

lease tenure of 46 years remaining and was valued at SGD270mn as at 31 December 2019. OUE-CT’s

debt headroom is ~SGD323mn and ~SGD653bn for the regulatory limit of aggregate leverage of 45%

and 50% respectively. While we think OUE-CT is theoretically able to fund an acquisition of the

properties via a mix of debt and equity, we do not expect these properties to be injected into OUE-

CT in the near term. That said, the possibility remains that should Sponsor be in need of cash,

pumping its assets into OUE-CT is a viable route, especially if OUE-CT’s balance sheet is able to

accommodate asset growth.

V) Financial Analysis

Acquisitions drive debt higher: The increase in debt from 3Q2015 to 4Q2015 was due to the

acquisition of One Raffles Place. That next increase in 4Q2018 was due to the acquisition of OUE

Downtown Office and the biggest jump in 2Q2019 was due to the combination with OUE-HT. Since

IPO, OUE-CT has not paid down much debt. Figure 9 depicts strong correlation between debt and

revenue over time. We think this suggests that growth in revenue has been largely fuelled more by

debt though OUE-CT had in late 2018 raised ~SGD588mn of equity. Given organic growth has been

somewhat muted, we think it would be difficult for OUE-CT to pay down its debt in the near term.

Therefore, we expect debt to fluctuate around current levels, with aggregate leverage of ~40%.

Figure 8: Debt and Net Debt over Time (SGD’mn) Figure 9: Debt and Revenue over Time

(SGD’mn)

Treasury Research & Strategy 8OCBC CREDIT RESEARCH

Special Interest Commentary

Wednesday, September 16, 2020

Source: Company

51% of its investment properties have been pledged: OUE-CT’s secured borrowings of SGD1.5bn

are secured by investment properties with a total carrying amount of SGD3.5bn, leaving OUE-CT

with 48.6% of its total investment properties unencumbered (i.e. SGD3.3bn out of SGD6.8bn). We

think One Raffles Place (valued at SGD1,552mn at 31 December 2019), OUE Downtown Office

(SGD912mn) and Crowne Plaza Changi Airport (SGD497mn) remain unencumbered. In the midst of

COVID-19, we think the valuation of hotel properties could be at risk but expect valuation of One

Raffles Place and OUE Downtown Office to be relatively more stable. While OUE-CT still has assets

that it can pledge to banks for loans, the proportion of unencumbered assets is low relative to the

other S-REITs. For the S-REITs under our official coverage, the average unencumbered assets are

90% for Office REITs, 88% for Retail REITs and 83% for Hospitality REITs.

At risk of asset revaluation losses: We think OUE-CT runs the risk of its properties getting revalued

lower in the near term due to the poor economic outlook impacting occupancy rates and room

rates for its hotel properties. OUE-CT’s aggregate leverage would be negatively impacted as well

because the denominator would become smaller as a result of a downward revaluation. Based on

figures as at 30 June 2020, a 5% decline in asset valuation would bring about a 2.1ppt increase in

aggregate leverage to 42.2% from 40.1% and a 10% decline would raise aggregate leverage to

44.6%, below the regulatory limit for aggregate leverage of 50% (if EBITDA/Interest as prescribed

by MAS is 2.5x or better). Management has estimated that asset values would need to correct by

~20% before regulatory limit of 50% is breached.

Manageable credit metrics in the near term: As at 30 June 2020, aggregate leverage was 40.1%.

EBITDA/Interest based on our calculation is 2.1x, and better at 2.4x if we were to include rental

support into EBITDA. EBITDA/Interest as prescribed under MAS’ calculation is 2.8x for OUE-CT.

Given how interest rates have come down, we do not expect debt cost to increase over time for

OUE-CT from the current rate of 3.1% p.a. OUE-CT has SGD64.9mn of cash on hand versus

SGD576.3mn of debt coming due in the short term. We think SGD426.3mn of which (a secured SGD

loan) will be rolled, leaving OUE-CT with SGD150.0mn of debt to handle (i.e. OUECT 3.03% ‘20s due

in September 2020). OUE-CT has another SGD90mn for the Hilton capex. Management has shared

that these maturing debt will be refinanced ahead of maturity and it has sufficient liquidity to meet

its operational and financial commitments with available credit facilities to tap on where necessary.

OUE-CT has also retained SGD13.8mn of distribution (comprising tax-exempt income and capital

distribution) in 1H2020 to preserve financial flexibility. While we expect OUE-CT to be able to meet

its near term financing needs, we note that it has SGD796mn maturing in 2021 (~30% of total debt)

and SGD674mn maturing in 2022 (~25% of total debt). The term of debt for OUE-CT is somewhat

short at 1.9 years.

Treasury Research & Strategy 9OCBC CREDIT RESEARCH

Special Interest Commentary

Wednesday, September 16, 2020

The Credit Research team would like to acknowledge and give due credit to the contributions of Zhou

Ziqi.

Treasury Research & Strategy 10OCBC CREDIT RESEARCH

Special Interest Commentary

Wednesday, September 16, 2020

OUE Commercial REIT

Table 1: Sum m ary Financials Figure 1: Revenue breakdow n by Segm ent - 1H2020

Year Ended 31st Dec FY2018 FY2019 1H2020

Incom e Statem ent (SGD'm n) Hospitality

26.3% Retail

Revenue 176.4 257.3 142.0 11.1%

EBITDA 127.2 187.9 102.0

EBIT 121.7 182.4 99.4

Gross interest expense 51.7 71.9 45.2

Profit Before Tax 150.4 150.7 65.5

Net profit 117.5 118.7 56.1

Balance Sheet (SGD'm n)

Cash and bank deposits 37.1 59.4 64.9

Total assets 4,571.1 6,888.2 6,913.4

Office

Short term debt 2.0 575.5 577.3 62.6%

Gross debt 1,713.3 2,687.1 2,707.5

Net debt 1,676.2 2,627.7 2,642.7

Offi ce Hospita lity Retail

Shareholders' equity 2,640.7 3,928.2 3,900.8

Cash Flow (SGD'm n)

CFO 132.7 160.9 116.9 Source: Company

Capex 3.6 7.9 3.1

Acquisitions 936.0 0.0 0.0 Figure 2: Revenue breakdow n by Property - 1H2020

Disposals 0.0 0.0 0.0 Crowne Mandarin Mandarin

Plaza Changi Gallery Orchard

Dividends 80.7 111.2 61.2 OUE Airport 5.3% Singapore

Downtown 8.8% 17.5%

Interest paid 43.3 66.5 38.6 Office

14.6%

Free Cash Flow (FCF) 129.0 153.0 113.8

Key Ratios

EBITDA margin (%) 72.11 73.01 71.80

Net margin (%) 66.61 46.15 39.48

Gross debt to EBITDA (x) 13.47 14.30 13.28

Net debt to EBITDA (x) 13.18 13.99 12.96

One Raffles

Lippo Plaza

Gross Debt to Equity (x) 0.65 0.68 0.69 9.9%

OUE Places

Bayfront 22.4%

Net Debt to Equity (x) 0.63 0.67 0.68 21.5%

Gross debt/total asset (x) 0.37 0.39 0.39 One Raffles Places OUE Bayfront

Net debt/total asset (x) 0.37 0.38 0.38 Lippo Plaza OUE Downtown Office

Cash/current borrow ings (x) 18.61 0.10 0.11 Crowne Plaza Changi Airport Mandarin Gallery

EBITDA/Total Interest (x) 2.46 2.61 2.25 Mandarin Orchard Singapore

Source: Company, OCBC estimates Source: Company

Figure 3: Debt Maturity Profile Figure 4: Gross Debt to Equity (x)

Am ounts in (SGD'm n)

(SGD'mn) As at 31/12/2019 % of debt

900

792.0

800 ount repayable in one year or less, or on dem and

Am

700 644.0 0.68 0.69

Secured 0.0 0.0% 0.65

575.0

600

Unsecured 210.9 6.0%

500

210.9

403.0 6.0%

400

Am ount repayable after a year

300

Secured 0.0 0.0%

200 130.0

Unsecured 3334.2 94.0%

100.0

100

3334.2 94.0%

FY2020 FY2021 FY2022 FY2023 FY2024 FY2025 FY2018 FY2019 1H2020

Total As at 30 June 3545.2

2020 100.0% Gross Debt to Equity (x)

Source: Company Source: Company, OCBC estimates

Treasury Research & Strategy 11OCBC CREDIT RESEARCH Special Interest Commentary Wednesday, September 16, 2020 Explanation of Issuer Profile Rating / Issuer Profile Score Positive (“Pos”) – The issuer’s credit profile is either strong on an absolute basis, or expected to improve to a strong position over the next six months. Neutral (“N”) – The issuer’s credit profile is fair on an absolute basis, or expected to improve / deteriorate to a fair level over the next six months. Negative (“Neg”) – The issuer’s credit profile is either weaker or highly geared on an absolute basis, or expected to deteriorate to a weak or highly geared position over the next six months. To better differentiate relative credit quality of the issuers under our coverage, we have further sub-divided our Issuer Profile Ratings into a 7 point Issuer Profile Score scale. Please note that Bond Recommendations are dependent on a bond’s price, underlying risk free rates and an implied credit spread that reflects the strength of the issuer’s credit profile. Bond Recommendations may not be relied upon if one or more of these factors change. Explanation of Bond Recommendation Overweight (“OW”) – The bond represents better relative value compared to other bonds from the same issuer, or bonds of other issuers with similar tenor and comparable risk profile. Neutral (“N”) – The represents fair relative value compared to other bonds from the same issuer, or bonds of other issuers with similar tenor and comparable risk profile. Underweight (“UW”) – The represents weaker relative value compared to other bonds from the same issuer, or bonds of other issuers with similar tenor and comparable risk profile. Other Suspension – We may suspend our issuer rating and bond level recommendation on specific issuers from time to time when OCBC is engaged in other business activities with the issuer. Examples of such activities include acting as a joint lead manager or book runner in a new issue or as an agent in a consent solicitation exercise. We will resume our coverage once these activities are completed. Withdrawal (“WD”) – We may withdraw our issuer rating and bond level recommendation on specific issuers from time to time when corporate actions are announced but the outcome of these actions are highly uncertain. We will resume our coverage once there is sufficient clarity in our view on the impact of the proposed action. Treasury Research & Strategy 12

OCBC CREDIT RESEARCH Special Interest Commentary Wednesday, September 16, 2020 Treasury Research & Strategy Macro Research Selena Ling Tommy Xie Dongming Wellian Wiranto Terence Wu Head of Strategy & Research Head of Greater China Research Malaysia & Indonesia FX Strategist LingSSSelena@ocbc.com XieD@ocbc.com WellianWiranto@ocbc.com TerenceWu@ocbc.com Howie Lee Carie Li Dick Yu Thailand, Korea & Commodities Hong Kong & Macau Hong Kong & Macau HowieLee@ocbc.com carierli@ocbcwh.com dicksnyu@ocbcwh.com Credit Research Andrew Wong Ezien Hoo Wong Hong Wei Seow Zhi Qi Credit Research Analyst Credit Research Analyst Credit Research Analyst Credit Research Analyst WongVKAM@ocbc.com EzienHoo@ocbc.com WongHongWei@ocbc.com ZhiQiSeow@ocbc.com Analyst Declaration The analyst(s) who wrote this report and/or her or his respective connected persons did not hold financial interests in the above-mentioned issuer or company as at the time of the publication of this report. Disclaimer for research report This publication is solely for information purposes only and may not be published, circulated, reproduced or distributed in whole or in part to any other person without our prior written consent. This publication should not be construed as an offer or solicitation for the subscription, purchase or sale of the securities/instruments mentioned herein. Any forecast on the economy, stock market, bond market and economic trends of the markets provided is not necessarily indicative of the future or likely performance of the securities/instruments. Whilst the information contained herein has been compiled from sources believed to be reliable and we have taken all reasonable care to ensure that the inform ation contained in this publication is not untrue or misleading at the time of publication, we cannot guarantee and we make no representation as to its accuracy or completeness, and you should not act on it without first independently verifying its contents. The securities/instruments mentioned in this publication may not be suitable for investment by all investors. Any opinion or estimate contained in this report is subject to change without notice. We have not given any consideration to and we have not made any investigation of the investment objectives, fin ancial situation or particular needs of the recipient or any class of persons, and accordingly, no warranty whatsoever is given and no liability whatsoever is accepted for any loss arising whether directly or indirectly as a result of the recipient or any class of persons acting on such information or opinion or estimate. This publication may cover a wide range of topics and is not intended to be a comprehensive study or to provide any recommendation or advice on personal investing or financial planning. Accordingly, they should not be relied on or treated as a substitute for specific advice concerning individual situations. Please seek advice from a financial adviser regarding the suitability of any investment product taking into account your specific investment objectives, financial situation or particular needs before you make a commitment to purchase the investment product. OC BC and/or its related and affiliated corporations may at any time make markets in the securities/instruments mentioned in this p ublication and together with their respective directors and officers, may have or take positions in the securities/instruments mentioned in this publ ication and may be engaged in purchasing or selling the same for themselves or their clients, and may also perform or seek to perform broking and other investment or securities-related services for the corporations whose securities are mentioned in this publication as well as other parties generally. This report is intended for your sole use and information. By accepting this report, you agree that you shall not share, communicate, distribute, deliver a copy of or otherwise disclose in any way all or any part of this report or any information contained herein (such r eport, part thereof and information, “Relevant Materials”) to any person or entity (including, without limitation, any overseas office, affiliate, parent entity, subsidiary entity or related entity) (any such person or entity, a “Relevant Entity”) in breach of any law, rule, regulation, guidance or similar. In particular, you agree not to share, communicate, distribute, deliver or otherwise disclose any Relevant Materials to any Relevant Entity that is subject to the Markets in Financial Instruments Directive (2014/65/EU) (“MiFID”) and the EU’s Markets in Financial Instruments Regulation (600/2014) (“MiFIR”) (together referred to as “MiFID II”), or any part thereof, as implemented in any jurisdiction. No member of the OCBC Group shall be liable or responsible for the compliance by you or any Relevant Entity with any law, rule, regulation, guidance or similar (including, without limitation, MiFID II, as implemented in any jurisdiction). Co.Reg.no.:193200032W Treasury Research & Strategy 13

You can also read