Section 12 L of the Income Tax Act - SANEDI ESCo Workshop

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Section 12 L

of

the Income Tax Act

SANEDI ESCo Workshop

22 January 2014

www.saneditax.org.za

Barry Bredenkamp

SANEDI

Old Chinese Proverb

“A journey of 1000 miles begins with

the

first step!”

The Act

Section 12L of the Income Tax Act, 1962, on the allowance for Energy Efficiency Savings,

as inserted by Act 17 of 2009, amended by Act 7 of 2010 and substituted by Act 22 of 2012.

www.saneditax.org.za

The ACT (1) For the purpose of determining the taxable income derived by any person from carrying on any trade in respect of any year of assessment ending before 1 January 2020, there must be allowed as a deduction from the income of that person an amount in respect of energy efficiency savings by that person in respect of that year of assessment. (2) The amount of the deduction must be calculated at 45 cents per kilowatt hour or kilowatt hour equivalent of energy efficiency savings. (3) A person claiming the deduction allowed during any year of assessment, must obtain a certificate issued by SANEDI, in respect of the energy efficiency savings for which a deduction is claimed in respect of that year of assessment.

The ACT … cont’d (a) the baseline at the beginning of the year of assessment; (b) the reporting period energy use at the end of the year of assessment; (c) the annual energy efficiency savings expressed in kilowatt hours or kilowatt hours equivalent for the year of assessment, including the full:- • criteria and methodology used to calculate the energy efficiency savings; and • any other information prescribed by the regulations. 4) A deduction must not be allowed in terms of this section if the person claiming the allowance receives any concurrent benefit in respect of energy efficiency savings.

The Regulations

Regulation No. R 971 in Terms of Section 12L of the Income Tax Act, 1962, on the allowance

for Energy Efficiency Savings.

www.saneditax.org.za

No. 37136 GOVERNMENT GAZETTE, 9 December 2013 GOVERNMENT/ REGULATION GAZETTE NATIONAL TREASURY No. 10080 9 December 2013 CONTENTS Government Notice R. 971. Income Tax Act, (58/1962): Regulations in terms of section 12L of the Income Tax Act, 1962, on the allowance for Energy Efficiency Savings, preceded by Notice 855 of the date upon which section 12L (deduction in respect of energy efficiency savings), as inserted by Act 17 of 2009, amended by Act 7 of 2010 and substituted by Act 22 of 2012 comes into operation on 1 November 2013. Printed by and obtainable from the Government Printer, Bosman Street, Private Bag X85, Pretoria, 0001

The Regulations Cover…… • Definitions • Procedure for Claiming the Allowance • Content Requirements of the Certificate • Baseline Calculation, ref. SANS 500 10:2011 • Concurrent Benefits; and • Limitations, (Exclusions)

The Big Question????

• 45 c/kWh OR 12c/ kWh?

Scenario 1 Scenario 2

R100.00 Profit R100.00 Profit

Less R28.00 (28% Tax) + 12L Rebate 45.00

= R72.00 = R145.00

+ 12L Rebate 45.00 Less R40.60 (28% Tax)

R117.00 R104.40

Note: Would have been R72.00 WITHOUT any INCENTIVE.

(*) Saving 100 kWh during the period of assessmentGuidelines

(in support of the 12-L Regulations)

www.saneditax.org.zaGuidelines, (in support of the Regulations) Provide more detailed explanations/ assistance to prospective Applicants & includes:- A basic calculation, to obtain an initial assessment of the feasibility for applying for the 12-L Tax Incentive; Project eligibility/ key criteria/ cost of M & V, to consider; Defining Load Shifting vs Energy Efficiency vs Energy Conservation projects in relation to 12-L eligibility; Highlighting specific exclusions from the Incentive; An explanation of the time limitations relating to this Incentive; A description of the various eligible Energy Carriers and Conversion Factors to kWh, for rebate purposes.

SANEDI

The South African National Energy Development Institute

A state owned Entity established under Section 7 of the National Energy Act 2008

(Act No.34 of 2008).

www.sanedi.org.zaThe South African National Energy Development Institute

mandate The National Energy Act, 2008 (Act No.

34 of 2008), Section 7 (2) provides for

SANEDI to direct, monitor and conduct

energy research and development, as

well as undertake measures to promote

energy efficiency throughout the

economy.

13SANEDI’s “Value Add” • Must provide an ‘Assurance Function’ to SARS. • Must consolidate, analyse and report to DoE, National Treasury and SARS. • Must assist wherever possible, to ‘make it happen’! • Provide and maintain the on-line database, to streamline the process. • Develop and improve the Guidelines. • Integrate current fragmented basket of activities into a ‘workable’ solution!

Conclusion

and the

Way Forward

www.saneditax.org.zaConclusion & the Way Forward Continue the ‘walk’, to resolve any misunderstandings, relating to interpretation of the Act and Regulations. implementing and refining/ improving the system and all supporting documentation. Conduct ‘Information Sessions’ throughout the country, to inform and educate all constituents about the incentive. Independently commission a bi-annual review of the functionality of the system, as well as the overall energy-and-economic impacts of the 12-L Tax Incentive. Unlike most other incentive schemes, severe penalties DO apply in the case of the Income Tax Act!

Access to some clever people

and ………….www.saneditax.org.za

Content of Presentation 1. The Act 2. The Regulations 3. Guidelines, (in support of the Regulations) 4. SANEDI’s “Value Add” 5. Conclusions & ‘The Way Forward’

Important Component of the Regulations

For the purpose of this regulation—

• “co-generation” means combined heat and power;

• “combined heat and power” means the production of electricity

and useful heat from a fuel or energy source which is a co-

product, by-product, waste product or residual product of an

underlying industrial process;

• “energy from waste” means waste or under-utilised energy in the

form of process furnace off-gas from an industrial process;

• “renewable sources” means—

(a) biomass;

(b) geothermal;

(c) hydro;

(d) ocean currents;

(e) solar;

(f) tidal waves; or

(g) wind.Important Component….cont’d

“waste heat” means heat that is—

(a) produced directly by an industrial process or

machines or equipment utilised in that industrial

process; and

(b) regarded as a waste by-product that is not utilised

for any useful application; and

“waste heat recovery” means utilising waste heat or

underutilised energy generated during an

industrial process.Important Component….cont’d • SANAS-accredited M & V mandatory • No minimum or maximum project size - 1 GWh/ p.a. appears to be an economically viable threshold

Regulation Limitations A person may not receive the allowance in respect of energy generated from renewable sources or co- generation, other than energy generated from waste heat recovery. A person generating energy through a captive power plant may not receive the allowance, unless the kilowatt hours or the equivalent kilowatt hours of energy output of that captive power plant in respect of a year of assessment is more than 35 per cent of the kilowatt hours or the equivalent kilowatt hours of energy input in respect of that year of assessment.

Basic On-line System

Functions

www.saneditax.org.zaSystem SECURITY The 12-L Energy Efficiency TAX On-line System has been developed, using the concept of (WAMP) Windows-Appache-PHP-MySQL DataBasE and is currently hosted by Hetzner. In order to professionally secure this website, it was decided to apply for a SSL certificate for the current (to be revised), saneditax.org.za domain and this certificate has already been issued by Hetzner.

Basic Functions System layout and

domain are

currently being

revamped, to

include all logos!

Figure 1. Home PageBasic Functions Figure 2. Log-in Page

Basic Functions Figure 3. Claimant Registration Page

Basic Functions Figure 4. M&V Inspection Body Registration Page

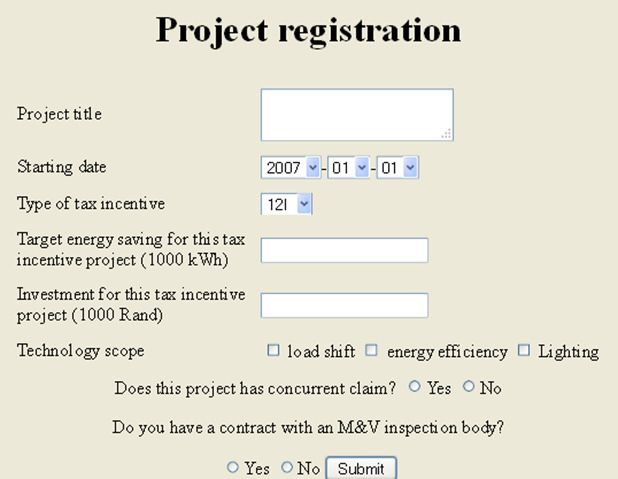

Claimant Functions Figure 5. Project Registration Page

SANEDI Administrators Functions

Figure 12. Project Assignment PageAdditional Functions Figure 15. Technology List Page

You can also read