Online Appendix (For Online Publication Only) - Census.gov

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Online Appendix (For Online Publication Only)

A Further Details and Results

A.1 Property Taxation and the Protesting Process

In this section we provide more details about the institutional context.

Section 25 of the Texas Property Code stipulates how property taxes are assessed and

collected. Property taxes must be computed according to several steps. First, the county is

responsible for estimating the “total market value” (i.e. value of the land plus any improve-

ments) for each of its residential and commercial properties. Note that we refer to this total

market value as “proposed value” in our paper. The Texas Property Code mandates each

estimated total market value must (a) accurately reflect the market value of the property

as of January 1st and (b) be “fair” insofar as being consistent with the estimated values

of comparable properties. A household may protest the proposed value it receives on the

grounds that (a) and/or (b) are not satisfied.

Second, the county calculates each household’s “appraised value”, defined as the lower of

total market value or the homestead cap (this homestead cap can apply only for properties

with homestead status, for more see Section 3, minus certain exemptions, such as agricultural

use “total” exemptions. Third, each property’s “taxable value” is computed by jurisdiction

as the household’s appraised value less certain additional exemption amounts applied by the

jurisdiction. These include any additional exemptions for which the household has been ap-

proved qualifying and submitting relevant paperwork, such as exemptions for homesteads,

over age 65, disability, veteran, low income, historic properties, and more. In Texas, Inde-

pendent School Districts are required (and other jurisdictions may elect) to “freeze” property

taxes for households with Over 65 or Disabled exemptions as of the year they qualified for

the exemption.

Finally, the taxes due to each jurisdiction are calculated by multiplying the jurisdiction’s

taxable value of the home by the jurisdiction’s tax rate. The household receives a bill for the

total taxes due for the year, which equals the sum of the taxes due across all jurisdictions

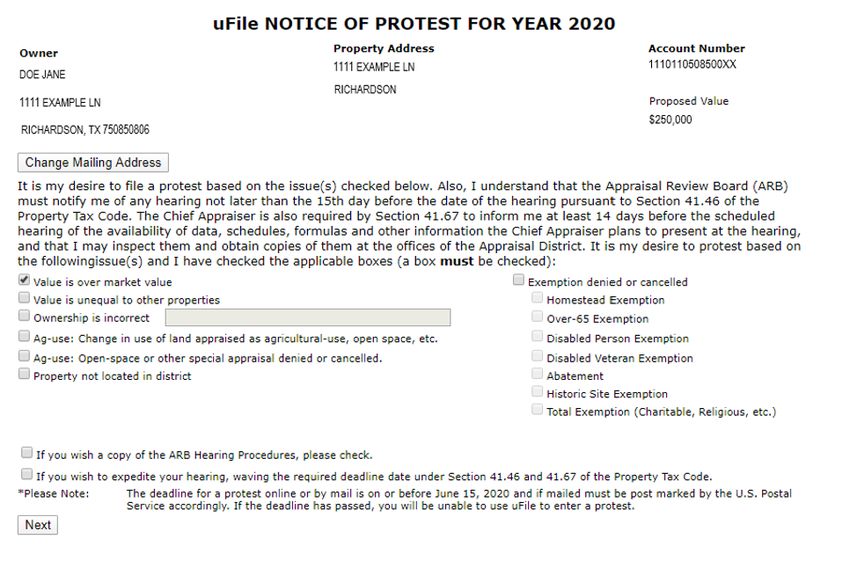

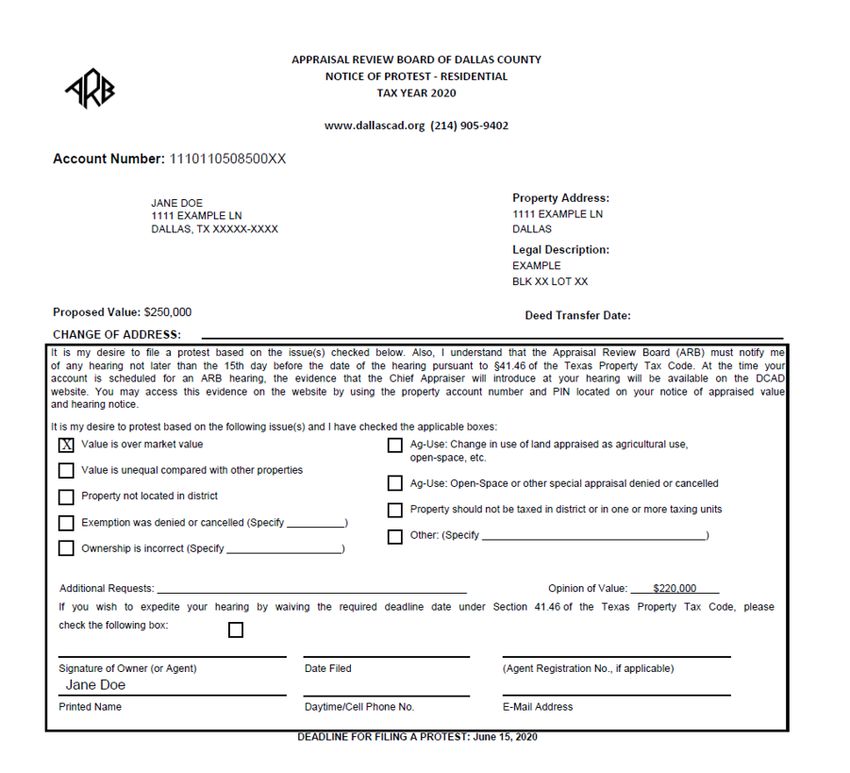

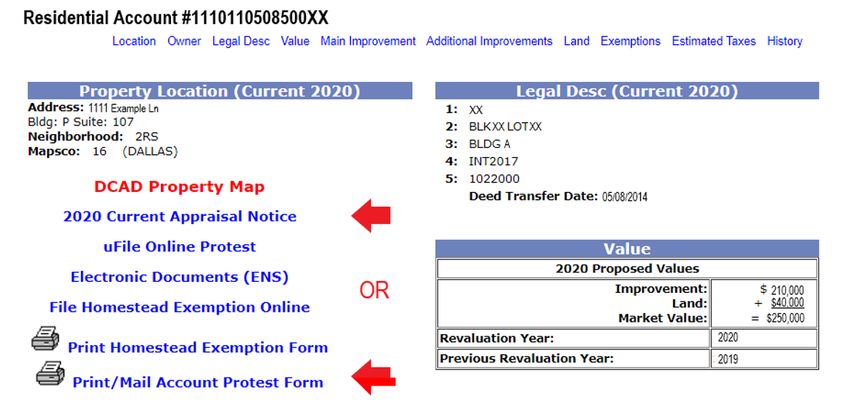

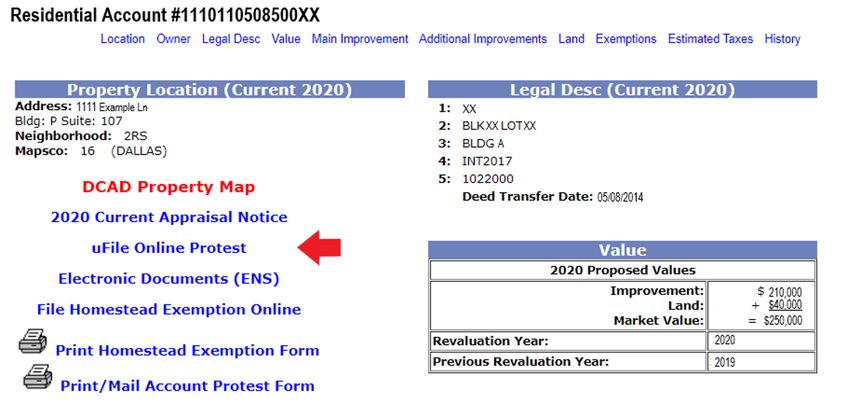

in which the home resides. See for example the sample DCAD notification in Appendix G,

which includes a break-down of the property tax calculation.

A.2 Data Sources

In this section we presents further details about the data sources used in the paper.

i

Our main data source is made publicly available and easily accessible by the DCAD. Under

the Texas Public Information Act, all government information in Texas, with a few exceptions,

is available to the public.48 As of August of 2020, the raw data that we used in the paper

can be downloaded from the following links http://www.dallascad.org/DataProducts.

aspx and http://www.dallascad.org/TaxRates.aspx. Government information that is

not publicly available on the Internet, can be requested from any governmental body in

Texas for a fee to cover the cost of producing copies of the records. We requested data from

the DCAD on the “Opinion of Value” for all protests that were filed using the online system.

The protest dates recorded in the DCAD data correspond to the dates when protests

are recorded in the system. These recorded dates are an approximation of the dates when

protests are submitted. Specifically, protests submitted online are recorded every business

day (e.g., protests submitted on weekends are recorded the following Monday). The system

does not contain dates when protests are postmarked for protests submitted by mail, which

might create an small difference between the date when protests are submitted and recorded

in the system. For this reason, some protests that were received shortly after June 15th

may still have been filed by the June 15th deadline. To be conservative, in all the analysis

presented in the paper we include protests that were recorded as received by the DCAD

before July 15th .

We collected some complementary data from RedFin and Zillow. We use Redfin to

identify all houses sold in the county from October 1st , 2019 to May 9th , 2020, including

information on the sales price, address, and property characteristics. We used this data to

generate the information on comparable properties included in the letters we sent to subjects

in the extra aid treatment. We scraped RedFin estimates for subject pool households in

the field experiment to further validate the matches made by the comparison algorithm (see

Appendix A.5 for details). We found RedFin estimates for 95.8% of the households in the

subject pool. For the remaining households, we scraped Zillow’s estimates (a.k.a. Zestimates)

for the properties in lieu of the RedFin estimate, locating estimates for an additional 2.6%

of the subject pool. For the remaining 1.6% of the subject pool, we used a prediction model

to impute estimated home values, employing household characteristics predictors along with

zip code fixed effects.

A.3 Descriptive Statistics

In this section we provide some basic descriptive statistics for the different samples used in

the paper.

48

https://www.texasattorneygeneral.gov/open-government/members-public/overview-public-information-

act

ii

Table A.1 presents descriptive statistics for the key variables and for each of the samples

used in this paper. The table reports pre-treatment characteristics using data from 2019.

Column (1) corresponds to the sample used in the quasi-experiment. Column (1) shows that

the average home in this sample had 3.24 bedrooms, was assessed at $306,000, paid $6,150

annually in property taxes, or equivalent to a tax rate of 1.98%. Within this sample, 5.93%

owners protested directly in 2019 and 7.96% through an agent, and 74.24% had homestead

status. For this sample, we do not have information on demographics and partisan identity.

Column (2) of Table A.1 shows the average pre-treatment characteristics for the subject

pool used in the field experiment. Comparing columns (1) and (2) reveals that the samples

are similar but not identical in terms of observable characteristics. Properties included in

the field experiment are slightly more expensive than those in the quasi-experiment. The

differences between these two samples are explained by the filters listed in A.6.

We have information on demographics and partisan identity for the sample used in the

field experiment, and the last seven rows of Column (2) of Table A.1 present summary

statistics.

Column (3) of Table A.1 presents average characteristics for the sub-sample of survey

respondents associated with the field experiment. A comparison between columns (2) and

(3) of Table A.1 shows that survey respondents are not a random sample of the subject pool.

Specifically, the households selected to receive a letter that in turn answered the Field Survey

in column (3) own properties that are more expensive than those in column (2). In addition,

direct protests are substantially higher in column (3) than in column (2). Because column

(3) uses a subset of the households used in column (2), for this sample used in column (3)

we also have information on demographics and partisan identity. White and Republican

homeowners disproportionately answered the Field Survey.

Column (4) of Table A.1 presents average characteristics for the sample of 2,065 Mturk

respondents. A comparison of columns (2) and (4) of Table A.1 shows that the survey

respondents are certainly not identical to the subjects in the field experiment, but they are

not wildly different either. Property taxes are lower for this sample, which reveals that

property taxes in Texas are higher than in other states. For this sample, we do not observe

if respondents protested directly or through an agent nor the homestead status. In the

Mturk Survey we included questions on demographics and partisan identity, and the last 7

rows include summary statistics for these variables. Mturk Survey respondents are younger,

include a larger proportion of white homeowners, and a smaller proportion of Republicans

homeowners compared to both the subject pool sample in column (2) and the Field Survey

sample in column (3).

iii

A.4 Additional Falsification Tests

In the body of the paper, we present a number of falsification tests. In this section we provide

additional falsification tests.

One of the event-study falsification tests we conduct in the paper consists of estimating

the regression of interest but with pre-treatment outcomes as the dependent variable. For the

sake of brevity, the body of the paper presents results using the 2019 protest as the “placebo

outcome.” In this Appendix, we reproduce this analysis for each of the other pre-treatment

years for which we have data available: 2015, 2016, 2017, and 2018.

Figure A.1 corresponds to the results on the homestead cap presented in Table 1 and

discussed in Section 3. The rightmost coefficient (year 2020) corresponds to the results from

column (1) of Table 1, where the dependent variable takes the value 100 if the household

protested in 2020. The coefficient for year 2019 corresponds to the results from column

(2) of Table 1, where the dependent variable takes the value 100 if the household protested

in 2019. Likewise, the coefficients for each of the years 2018, 2017, 2016 and 2015 have a

dependent variable that takes the value 100 if the household protested in 2018, 2017, 2016 and

2015, respectively. As expected, the coefficients are consistently close to zero for each of the

falsification years (2015-2019), and always highly statistically different from the coefficient

for 2020. In two of the falsification years the coefficient is small but borderline statistically

significant, although that is expected: given the large number of falsification tests that we

conduct in this paper, a few of them a bound to be spuriously significant from time to time.

Figure A.2 corresponds to the results on the effects of the letters presented in Table 2 and

discussed in Section 4. The rightmost coefficient (year 2020) corresponds to the results from

column (1) of Table 2, where the dependent variable takes the value 100 if the household

protested in 2020. The coefficient for year 2019 corresponds to the results from column (2)

of Table 2, where the dependent variable takes the value 100 if the household protested in

2019. And then each of the other coefficients reproduce the falsification exercise for each of

the other years with available data (2015-2018). As expected, the coefficients are consistently

close to zero and statistically insignificant for each of the falsification years (2015-2019).

Figure A.3 corresponds to the conditional cooperation results presented in Table 4 and

discussed in Section 5. The rightmost coefficient (year 2020) corresponds to the results from

column (1) of Table 4, where the dependent variable takes the value 100 if the household

protested in 2020. The coefficient for year 2019 corresponds to the results from column (2)

of Table 4, where the dependent variable takes the value 100 if the household protested in

2019. And then each of the other coefficients reproduce the falsification exercise for each of

the other years with available data (2015-2018). As expected, the coefficients are consistently

close to zero and statistically insignificant for each of the falsification years (2015-2019).

iv

A.5 Details about the Algorithm for the Comparison Properties

In this section we provide more details about the algorithm we used to find the values of

comparable properties that we included in the letters.

Although we identified one comparable property for all households in the subject pool, we

only displayed this information in the letter for the subjects randomly selected for the extra

aid letter. The algorithm begins by matching each household in our subject pool sample with

all houses listed on RedFin.com as sold between October 15th , 2019 and May 6th 2020, that

meet a list of criteria. Comparable properties were required to be within 0.75 miles of the

subject household, have the same number of bedrooms (or if the subject household has five or

greater bedrooms, then the comparison property must have five or greater as well), have at

least the number of bathrooms of the household minus one (or both must have five or greater

bathrooms), have a square footage between 95% and 120% of the subject household’s square

footage, and have an estimated sales price within 80% and 95% of DCAD’s 2020 proposed

value. Subject households were not permitted to be matched with themselves. Out of all

matches per the above criteria for a given subject household, we kept the single closest match

by distance.

Due to the fact lot size was only populated for about half of residential properties before we

performed our compables matching, we did not include lot size as part of our comparables

matching criteria, so as to avoid sample selection or generalizability concerns. A manual

review of matches found no perceptible difference in the quality of matches using either

approach.

We took random samples to manually inspect the quality of the comparable property, and

we found that the vast majority of the cases seemed reasonable. For a more formal assessment

of the quality of the arguments provided in the letter, we present some descriptive statistics

of the comparables identified by our algorithm.

Figure A.4 presents the distribution of “proposed savings” generated by the comparison

algorithm for all subject households in the field experiment. “Proposed savings” is calculated

as the household’s 2020 proposed market value minus the comparable home’s 2020 proposed

market value (i.e., the market value reduction the household would achieve if the household

placed the value of the comparable home in the “Opinion of Value” line on the protest

form and the DCAD settled for that value). Among other filters, the algorithm restricted

matches to homes with proposed market values in the range of 80% to 95% of the proposed

value of the subject household. The mean proposed savings was $37,973 (10.77%), while

the median proposed discount was $26,020 (10.01%)). Notably, households with comparison

homes valued 15%-20% cheaper are less frequent than those with comparison homes valued

5% to 10% lower. This suggests high overvaluation is less prevalent than lower levels of

v

overvaluation, as expected.

As an alternative method to verify our comparison algorithm, we can compare different

characteristics between the recipient’s property and the comparison property that we iden-

tified. The results are presented in Figure A.5. Figure A.5.a compares the estimated home

values according to a third party: we obtained estimates from RedFin (and when these were

unavailable, Zillow estimates) of the subject households’ and comparison homes’ market val-

ues. RedFin and Zillow estimates are not perfect and certainly have measurement error, but

on average they provide a reasonable proxy for home market values. Figure A.5.a shows

the the distribution of the %-difference between the value of the property and its compari-

son. The mean (median) difference is -1.66% (-2.17%), which indicates that our algorithm

identified a reasonable (if anything, slightly conservative on average) comparison property.

Figure A.5.b shows the distribution of the distance between the recipient’s own property

and the comparison property. On average, these pairs of properties are 0.38 miles from each

other, sometimes next door to each other, and at most 0.75 miles from each other. Figure

A.5.c shows the difference in square footage. Note that our algorithm selected comparison

properties that are, if anything, slightly larger than the recipient’s own property. That is,

the comparison property is conservative in this dimension. Last, Figure A.5.c shows that

most of the time the recipient’s property has the exact same number of bathrooms as the

comparison property, and the vast majority of the pairs are within half a bathroom of each

other.

A.6 Field Experiment: Design and Implementation

In this section we provide additional information about the design and implementation of

the field experiment.

We begin describing the filters used to arrive at the subject pool. We begin with the

universe of 423,607 residential single-family properties used for the analysis in Section 3.2,

and use various filters to arrive at 78,462 households in the final subject pool of the field

experiment. We exclude commercial real properties, non single-family residential homes (e.g.,

condos, townhouses, mobile homes, apartments, P.O. boxes, vacant lots), properties with

missing information such as the proposed value, taxable values, property address, owner’s

mailing address, households lacking data on characteristics used for the comparison algorithm

such as number of bedrooms, number of bathrooms, or year built (see Appendix A.5), or

where the Census geocoding did not yield an address match. We further exclude households

with proposed values lower than $50,000 or greater than $7.5 million and tax rates lower

than 1 percent.

We did not include non owner-occupied properties (i.e., where the owner’s mailing address

vi

was not the same as the property address), as those owners may take much longer to receive

the letter and/or are more likely to be investors. Properties with keywords in the owner field

that suggested it was a business operating out of a residential property (e.g., “LLC,” “corp,”

“realty”), was owned by a government body (e.g., “texas,” “city”), or that we could not

address our letter to an owner’s actual name (e.g., “estate,” “community”) were excluded.

We drop households where the owner had already filed a 2020 protest before May 21st .

Households without a comparison home match, an important input for the extra aid letter,

were dropped. After our letters were mailed, we excluded XX households which the mailing

company’s National Change of Address Verification (NCOAV) flagged as the owner(s) moved

or the property address was invalid.

All subject households in the field experiment were shown figures for their own proposed

market value and estimated tax amount in the table on the first page of the letter we mailed.

We cross-randomized whether in addition subjects were shown the “Average Dallas Home”

column and/or the “Estimated Tax Rate” row in the table (see Section 4.2 for a description

of the mailing design and see Figure 3 for the first page of a sample letter with red boxes

highlighting the parts that were randomized, for exposition purposes).

Since we cross-randomized two aspects of the tables, in total there were thus four possible

types of tables, which are summarized in Figure A.6. The first randomization (average tax

rate in the extra column), is central to the research design. The second randomization, about

whether the tax rate is made salient or not, is a minor aspect of the design that allows us to

establish whether the effects are sensitive to salience. In fact, the last row does not add any

new information: it is simply the ratio between the previous two rows, and thus its inclusion

should not matter for the results. Rejection of this null hypothesis would then mean that

households compare tax amounts or tax rates depending on what information was made more

salient to them, thus complicating the interpretation of our findings.

Definitions for each of the variables disclosed in the table of the letter are summarized in

the notes below the table. Moreover, we discussed those definitions in more detail below:

Proposed Value for “Your Home”: The estimated market value of the property on

January 1st, 2020, as proposed by the DCAD. This is the market value included in

the Notice of Appraised Value mailed to homeowners by the DCAD around May 15th,

2020 if DCAD either proposed a change in the property’s market value or changed the

property’s homestead exemption status.

Proposed Value for the “Average Dallas Home”: The average market value for all single-

family residential properties, excluding condos, townhomes, and mobile homes in Dallas

County on January 1st, 2020, as proposed by Dallas CAD.

vii

Estimated Tax Amount for “Your Home”: This is the estimated total property taxes

due summed across all applicable jurisdictions for the 2020 tax year for the subject’s

household. We followed a similar process as the DCAD for estimating property taxes

due. That is, for each jurisdiction, the property’s estimated taxes due are calculated

as the jurisdiction’s estimated taxable value for the household (provided by DCAD)

multiplied by the jurisdiction’s 2019 tax rate.49 Each jurisdiction’s 2019 tax rate was

obtained from Dallas CAD’s website.50 In general, estimated current taxable values

are calculated as the appraised value (i.e., the lesser of (a) the household’s proposed

value and (b) homestead cap value, minus (c) agricultural-use exemption and (d) ab-

solute exemption) less any applicable Homestead, Over Age 65, Disabled, or Veteran

exemptions. For some jurisdictions (most frequently school districts), Over Age 65,

Disabled, and Veteran exemptions freeze the property’s taxable value at the taxable

value of the year in which the exemption started. To calculate estimated taxes due for

properties in jurisdictions where frozen tax amounts apply, we use the lower of (a) the

frozen tax value and (b) the current taxable value multiplied by the tax rate for that

jurisdiction.51 Estimated Tax Amount is calculated as the sum of the estimated taxes

due for each jurisdiction.

Estimated Tax Amount for the “Average Dallas Home”: This is the average 2020

estimated total property taxes due across all single-family residential properties in

Dallas County (excluding condominiums, town homes, and mobile homes). Estimated

Tax Amount was computed for all Dallas County households in the same way as for

subject households as outlined in “Estimated Tax Amount for ’Your Home’” above.

Estimated Tax Rate for “Your Home”: The estimated property tax rate for the subject’s

household. This is calculated as the household’s Estimated Tax Amount divided by its

Proposed Value.

Estimated Tax Rate for the “Average Dallas Home”: This is the average 2020 estimated

property tax rate for all single-family residential properties in Dallas County (excluding

condominiums, townhomes, and mobile homes). It is calculated as the average of

Estimated Tax Amount divided by Proposed Value for all Dallas County households.

49

Due to data availability, we did not include Special Districts in our calculation of estimated taxes due.

This makes little difference in practice, as these special rates account for less than 0.01% of the average

tax amount.

50

The tax rates by jurisdiction in 2019 were obtained from http://www.dallascad.org/TaxRates.aspx.

51

Note that the DCAD does not include the effect of “frozen” taxes in the estimated taxes due shown in

their letter. For the sake of accuracy, we do utilize the “frozen” tax amounts to calculate the estimated

taxes due shown in our letters.

viii

A.7 Field Experiment: Randomization Balance

In this section we show that the treatments are well-balanced in terms of observable charac-

teristics, demonstrating that the randomization was successful.

Table A.2 breaks down the average characteristics we used in the randomization by treat-

ment group. Column (1) correspond to the average characteristics for the whole subject

pool (which by construction is equal to column (2) of Table A.1). Columns (2) through

(4) present the pre-treatment characteristics by households that were randomly assigned to

receive no letters, letters with the basic aid message, and letters with the extra aid message,

respectively. Column (5) reports p-values for the null hypothesis that the average of each

characteristic is equal across these three treatment groups. The results show that, consistent

with successful random assignment, the observable characteristics are balanced across these

treatment groups. Columns (6) through (9) of Table A.2 present the pre-treatment char-

acteristics by households who received a letter and were randomly assigned to each of the

four treatment groups corresponding to the four types of tables. These four types of tables

result from the four possible combinations given by the inclusion or exclusion of an extra

column with the county average tax burden and the inclusion or exclusion of an extra row

with the calculated tax rates. Column (10) reports p-values for the null hypothesis that each

average characteristic is equal across these four treatment groups. Consistent with successful

random assignment, the results show that the observable characteristics are well-balanced

across these treatment groups.

A.8 Timing of The Letter Delivery, Visits to the Website and

Protests

In this section we present the timing of when subjects in the field experiment read the letters

we mailed and when subjects protested.

Following Perez-Truglia and Cruces (2017), Perez-Truglia and Troiano (2018) and Bottan

and Perez-Truglia (2020), we use the distribution of dates when the surveys included in

the letter were completed as a proxy for when the letters were actually read. This proxy

is conservative because some households may have read the letter and waited a few days

until responding to the survey. The results are presented in Figure A.7. The first survey

response was received on May 21st . This date coincided with the best guess provided by the

mailing company and the scan records from the Unites States Postal Service. This figure

suggests that a majority of the read-receipts happened in the first week after the start of

the letter delivery. The remaining read-receipts took place gradually until the last responses

were received on the deadline of the protest, on June 15th , 2020.

ix

We can also use the number of visits to the study’s website to infer when the letters were

received and read (the letters we mailed included the URL to the study’s website). We used

Google Analytics to track visits in an anonymous manner. Figure A.7.b shows the number

of visits by date. The evolution of the visits to the website tracks the survey responses very

closely. Note that this is not because the visitors were looking for the link to the survey: they

already had that link prominently displayed in the letter. The vast majority of the visitors go

to the website to find the step-by-step instructions on how to protest. Visits to the study’s

website began on May 21st and increased progressively until the tax filing deadline.52

For reference, Figure A.7 shows the timing of the protests in the subject pool. As ex-

plained in Appendix A.2 above, there might be differences between the dates when protests

are submitted and recorded in the DCAD’s system, and that in this paper we use recorded

dates since only these dates are available to us. Note that the vast majority of the direct

protests happened at least a week after our letters were delivered. Note also that there is a

quite similar gradual increase in the share of survey responses, the visits to the website and

the direct protests (Figures A.7.a, A.7.b and A.7.c, respectively). This probably means that

while most subjects received our letters shortly after May 20th , many of them held on to the

letter and used our website and responded to the survey weeks later. Indeed, in the survey

we asked households when they first saw our letter, and their responses confirm this view

(details in Appendix A.7).

Last, we would like to note that since we mailed the letters until the day we stopped

tracking protests (July 15th ), we performed several online searches on Google and social media

sites such as Facebook and Next Door and did not find any indication of contamination of

the field experiment due to public reports on this experiment while it was being conducted.

A.9 Effects from the Official DCAD Notifications

In this section we describe the official mail notifications sent by DCAD and present some

estimates of its effects on the probability of protesting.

According to the information posted in its official website,53 on May 15th all Notices of

Appraised Value for residential and commercial real properties became available on the Dallas

CAD website. Additionally, DCAD mailed the 2020 Notice of Appraised Value on May 15th

to those properties meeting the following criteria: an increase in the property appraised value,

an ownership change, a loss of homestead exemption, rendered property, or a new property.

52

We used Qualtrics for our survey and it is not possible to use Google Analytics to track visits the the

survey’s link included in the study’s website.

53

Source: http://dallascad.org/ViewPDFs.aspx?type=1&id=%5C%5Cdcad.org%5Cweb%5Cwebdata%

5Cheadlines%5CHEALTHALERTRecentHeadlines04032020.pdf.

xDCAD did not mail notices if the property value did not change or if the property value

decreased.

To estimate the effect of the DCAD mail notification, we exploit the discontinuity in the

rule used to decide who gets a mail notification and who doesn’t. Figure A.8 presents the

regression discontinuity results. The vertical axis measures the protest probability and the

horizontal axis measures the percentage growth in the proposed value between 2019 and 2020.

We restrict to a narrow band around 0%: i.e., between -5% and +5% growth in the proposed

value. The coefficient on the discontinuity (0.436) is positive, but small in magnitude and

statistically insignificant. This coefficient suggests that, if anything, receiving an official mail

notification from DCAD increases the probability of protesting directly by 0.436 pp. The

magnitude of this effect is much smaller than the effects of our letters reported in Section 4

above. This evidence supports the view that our letters in the field experiment did not

operate just as reminders.

A.10 Tax Amount versus Tax Rate

In the results on conditional cooperation, we focus on the belief about the average tax rate.

In principle, however, households could care instead about the average tax amount. In this

section we present some evidence supporting this specification choice.

The main motivation for this specification choice is data from the Field Survey indicating

that the vast majority of households think that the fair thing would be for all households to

pay the same tax rate.

The respondents are told that they can distribute a total tax burden of $10,000 between

two hypothetical households: Household A (whose home is worth $100,000) and Household

B (whose home is worth $400,000). The question provides a menu of six options to choose

from: Household A pays $0 (and thus Household B pays $10,000), $1,000, $2,000, $5,000,

$8,000, $9,000 or $10,000. The household is asked to report whatever allocation would be

most fair. If the respondent thinks that the fair allocation is for everyone to pay the same tax

rate, then he or she would choose the third option in which both households pay a tax rate

of 2%. If a respondent thinks that the fair thing is for everyone to pay the same tax amount,

then he or she should pick the middle option in which both households pay $5,000 (implying

a tax rate of 5% for Household A and a tax rate of 1.25% for Household B). The responses

to this question are presented in Figure A.9. A strong majority (76.5%) of households chose

the option that equalizes tax rates, while a minority of them (5.47%) chose the option that

equalizes the tax amounts and the rest chose a different option. This evidence suggests that

for a strong majority of households, the “fair” thing is for everyone to pay the same tax rate.

Last, we included a similar questions (whose parameters were randomized) in the Mturk

xiSurvey and the results are largely consistent.

A.11 Mturk Survey: Design and Implementation

In this section, we discuss more details about the design and implementation of the Mturk

Survey.

In the Mturk advertisement we explicitly noted that the survey was for homeowners.

However, some individuals who are not homeowners may miss that part of the advertisement

and click into the link to the survey anyways. For that reason, we included additional

screening questions at the beginning of the survey. We use these questions to exclude the

following categories: individuals who are not homeowners, respondents who were under age

18, or lived with their parents. For these respondents, as well as those that lived in counties

for which we did not have ACS data, the survey ended immediately after the screening

questions and they received the $0.25 base reward given to all participants. Respondents

that passed these filters were allowed to finish the survey. Those that completed the entire

survey were awarded a $0.50 bonus (on top of the $0.25 base reward).

We included a number of additional questions that we expected to be potentially useful

for descriptive statistics, robustness checks or heterogeneity analysis. For example, we asked

respondents whether they felt confident about their knowledge of their own property taxes,

how long they have lived in the current residency, how pays the property taxes and what is

the frequency of the payments. We asked them whether they thought that tax appeals of

property taxes were allowed in their county and whether they would consider appealing their

taxer or being late on their payments in the future. We included a question related to social

norms like the one included in the Field Survey (and described in Appendix A.10). And at

the end of the survey, we included a few additional questions about the individuals (such as

their age and political party) as well as their properties (e.g., number of bedrooms).

To create the feedback for the Mturk Survey, we utilized the latest data from the 2018

American Community Survey (ACS) to compute average home values and property taxes

for 3,210 counties across all 50 U.S. states. We used 2018 ACS one-year estimates, and for

counties where those were not available, 2018 ACS five-year estimates.54

The survey was advertised as a five-minute survey. The median respondent took about 7

minutes to complete the survey. Towards the end of the survey, there was an attention check,

similar to the one used in other studies (Bottan and Perez-Truglia, 2017; ?). A total of 99%

of the respondents passed the attention check. The payment scheme was on par with other

MTurk surveys (Bottan and Perez-Truglia, 2020). Participation in the Mturk Survey was

54

The ACS provides numbers of homes in different value ranges, so we used the number of households in

each range and the ranges’ midpoints to construct a weighted average home value by county.

xiirestricted to respondents located within the U.S. We created an additional restriction so that

each Mturk worker ID could only complete the survey once. We filtered out respondents who

did not complete the entire survey or for whom we were unable to confirm the validity of their

Mturk IDs. And to address potential concerns with outliers, we followed the standard practice

of filtering out the top and bottom 0.1 percentiles in prior beliefs as well as winsorizing the

top and bottom 0.1 percentiles in posterior beliefs (Fuster et al., 2018).

A.12 Salience of Tax Rate

In this section we discuss the role of salience of the tax rate.

In both the field experiment and the Mturk Survey, we cross-randomized whether the

tax rate was salient or not. We did this by cross-randomizing whether the table included a

third row with the tax rate. Since this third row does not add any new information (it is

simply the ratio between the previous two rows) its inclusion should not matter if agents are

rational, but might matter if they are salient. Rejection of this null hypothesis would then

mean that households compare tax amounts or tax rates depending on what information was

made more salient to them, thus complicating the interpretation of our findings. We will

report these results in a future version of the paper.

A.13 Partisanship Data

In this section we describe in more detail how we classified the households from the tax

records into likely Republicans and likely Democrats.

Based on the full name and address, the vendor provided a measure of whether each

owner of a household in the subject pool is Democrat (Republican). This was determined

either from the owner(s) self-reporting to be Democrat (Republican) in a survey (rarely

the case), or based on past voting behavior. In the latter case, households were assigned

to Democrat (Republican) if they voted in more Democrat (Republican) primaries than

they voted in Republican (Democrat) primaries since 2000. If the household did not have

any Democrat or Republican primary voting history, they were assigned to Democrat if

there is a record of a Democrat/liberal donation, the household has a "pro-choice" flag, or

if the household was an Affordable Care Act supporter. In turn, anyone with a record of a

past Republican/conservative donation, pro-life, or anti-Affordable Care Act is assigned to

Republican.

The vendor was able to match the data to 73.2% of owners in the sample. For properties

with multiple owners, we classify the household as Democrat if at least one of them is

Democrat, and Republican if at least one is classified as Republican. In the rare cases where

xiiithey are assigned to different groups, we pick the party of the person who is listed first in the

deed. Of the matched sample, 35.0% of households are identified as likely Democrat, 38.3%

are identified as likely Republican and the partisanship of the rest is unknown (i.e., there is

no sufficient data to classify them as Democrat or Republican). We can provide a validation

of this raw data on partisanship provided by the vendor. To do this, we use results from the

2012 presidential election at the voting precinct level.55 For each precinct, we compare the

share of households in our sample who were identified as Democrat (among those identified as

either Democrat or Republican) versus the actual voting share of the Democrat presidential

candidate (Barack Obama) among those who voted for either the Democrat candidate or

his Republican opponent (Mitt Romney). The results are presented in Figure A.10. The

dashed line is the 45-degree line, representing what a one-to-one relationship between inferred

democrats and democrat voting results would look like. Each grey dot corresponds to one

of the voting precincts, with a size proportional to the voting age population. The dark

dots correspond to a binned scatterplot. Note that the coefficient from the linear regression

(1.075) is very close to one, as expected. Moreover, the R2 of the regression (0.604) indicates

that the two variables are highly correlated.

We want to classify everyone, not just a subsample. For that reason, we build a simple

Logit model to predict whether you are Republican (or Democrat) based on the subsample

with a classification. The independent variables are the household’s proposed value, the

percentage of voters in the same precinct as the household that voted for Obama in the 2012

presidential election, a dummy for whether the home has multiple owners, a 2020 homestead

indicator, and fixed effects for each zip code and Independent School District. The model

is quite predictive, with an Area Under the ROC curve (AUC) of 78.1%. We then use

the predictive model to extrapolate to the subjects who were uncategorized. In the final

sample, 55% of the subjects are categorized as more likely to identify as Democrats and the

remaining 45% are categorized as more likely to be Republican. This narrow advantage for

the Democrats is consistent with recent electoral results from Dallas County. In the 2012

presidential election Barack Obama received 57% of the votes while Mitt Romney received

42% of the votes. In the 2016 presidential election, the Democrat advantage in Dallas county

was more pronounced, although this may be due to the unusual platform of the Republican

candidate: Hillary Clinton received 60.8% of the votes while Donald Trump received 34.6% of

the votes and Gary Johnson (a conservative candidate from the Libertarian party) received

3.2% of the votes.

55

This data was obtained Harvard’s Precinct-Level Election database, which is available at https://

dataverse.harvard.edu/dataset.xhtml?persistentId=hdl:1902.1/21919.

xivFigure A.1: Additional Falsification Tests: Effects of the 2020 Homestead Cap on the

Probability of Protesting

40

Protest Probability (p.p.)

20

0

−20

15

16

17

18

19

20

20

20

20

20

20

20

Year

Notes: The horizontal axis presents the year and the vertical axis the protest

rate. The blue dots represent the coefficient on τi from the Instrumental Variables

regression shown in equation 6 from Section 3.2, except the dependent variable is

an indicator variable that takes the value 100 if the owner protested directly in the

corresponding year between 2015-2020. The endogenous variable (τi ) corresponds

to the property tax rate (in percentage points) to which the household is subject.

The excluded instrument is the interaction between two variables: the difference

between the proposed value and the potential homestead cap, and an indicator

variable for whether that difference is positive. The regressions controls for the

difference between the proposed value and the potential homestead cap as well

as a host of additional variables – see Section 3.2 for the full list. Results based

on households with single-family homes, 2020 homestead status, and an absolute

difference between the proposed value and the potential homestead cap of less

than $15,000.

xvFigure A.2: Additional Falsification Tests: Effects of the two Letter Types on the Probability

of Protesting

Basic Aid Letter

Extra Aid Letter

3

Protest Probability (p.p.)

Start of

Intervention

2

1

0

−1

15

16

17

18

19

20

20

20

20

20

20

20

Year

Notes: The horizontal axis presents the year and the vertical axis the protest

rate relative to the control group. The blue dots and red diamonds represent

the average direct protest rate relative to the control group for the subjects who

received the basic aid and extra aid letter respectively.

xviFigure A.3: Additional Falsification Tests: Effect of the Information on Average Tax Rate

in the County on the Probability of Protesting

1

Protest Probability (p.p.)

0

−1

−2

15

16

17

18

19

20

20

20

20

20

20

20

Year

Notes: All results are based on households who received a letter in the field

experiment in 2020. The horizontal axis presents the year and the vertical axis

the protest rate. The blue dots represent the coefficient on the information shock

(Di · (τ − τi )) based on equation (10) from Section 5.5, except the dependent

variable is an indicator variable that takes the value 100 if the owner protested

directly in the corresponding year between 2015-2020.

xviiFigure A.4: Distribution of Proposed Savings Implied by the Extra Aid Message

4

3

Percent

21

0

5 10 15 20

Proposed Savings (%)

Notes: This figure shows the distribution of proposed savings, expressed as a

percentage of the home’s market value as notified by DCAD, for all households

in the subject pool of the field experiment. Proposed savings is defined as the

difference between the household’s proposed value (as notified by the DCAD) and

the sale price of the nearby, comparable home that was chosen by our algorithm.

Each household that was mailed the extra aid letter had the comparable home

included in the letter which could be used to support the household’s protest

(see Section 4.1). Details about the algorithm used select comparison homes are

contained in Appendix A.5.

xviiiFigure A.5: Differences between Subject’s Properties and their Comparable Properties

a. RedFin/Zillow Estimates b. Distance to Comparable

10

2.5

8

2

1.5

6

Percent

Percent

4

1

2

.5

0

0

00

5

0

5

0

25

50

75

0

0

5

.5

5

−7

−5

−2

10

.2

.7

−1

Household − Comparable RedFin Estimates (%−Difference) Distance to Comparable (Miles)

c. Square Footage d. Number of Bathrooms

60

4

40

3

Percent

Percent

2

20

1

0

.5

.0

.5

0

5

0

5

0.

0.

1.

1.

−1

−1

−0

0

>=May 15th, 2020 May 15th, 2020

Dear Jose E Alamillo, Dear Michael & Kim Walker,

We are researchers at The University of Texas at Dallas and we are reaching out to you as part of a We are researchers at The University of Texas at Dallas and we are reaching out to you as part of a

research study. You can lower your tax burden by protesting the taxable value assessment of research study. You can lower your tax burden by protesting the taxable value assessment of

your property. We want to share information that we hope will be useful. your property. We want to share information that we hope will be useful.

Figure A.6: Sample Information Tables

Some people

THE may choose to OF

UNIVERSITY protest

TEXASbecause they feel they are paying more than their fair share. Find

AT DALLAS Some people may choose to protest because they feel they are paying more than their fair share. Find

below some information

Naveen about

Jindal the estimated

School 2020 taxes for your home at 7117 Christie Ln (Dallas, TX)

of Management below some information about the estimated 2020 taxes for your home at 1320 Amsbury Dr (Desoto,

in Dallas County: a. Average:No & Rate:No TX) in Dallas County: b. Average:Yes & Rate:No

YOUR HOME YOUR HOME AVERAGE DALLAS HOME

May 15th, 2020

Proposed Value Proposed Value

Dear Robert Kevin &Tax

Estimated Becky Francis Drew,

Amount Estimated Tax Amount

We are

Source: Dataresearchers

provided by DallasatCentral

TheAppraisal

University

Districtof Texas

(CAD). at Value

Proposed Dallas andCAD's

is Dallas weestimate

are reaching out

of the home's to value

market youasasof January

part of1st,a Source: Data provided by Dallas Central Appraisal District (CAD). Proposed Value is Dallas CAD's estimate of the home's market value as of January 1st,

research

2020. study.

Estimated Youis our

Tax Amount can lower

estimate your

of taxes tax

due this yearburden by tax

using the latest protesting

rates available the

(some taxable value

exemptions might assessment

not be included). of 2020. Estimated Tax Amount is our estimate of taxes due this year using the latest tax rates available (some exemptions might not be included). Average

your property. We want to share information that we hope will be useful. Dallas Home values are based on all single-family homes in Dallas County, excluding condos, townhomes, and mobile homes.

The deadline to protest is June 15th, 2020. You can fill out a short form online or mail it in. You can

Some people may choose to protest because they feel they are paying more than their fair share. Find The deadline to protest is June 15th, 2020. You can fill out a short form online or mail it in. You can

find instructions on how to do this on the study's website:

below some information about the estimated 2020 taxes for your home at 317 Meadowcreek Rd

c. Average:No & Rate:Yes find instructions on how to do this on the study's website:

d. Average:Yes & Rate:Yes

(Coppell, TX) in Dallas County:

https://www.utdallas.edu/taxproject/

https://www.utdallas.edu/taxproject/

YOUR HOME

If you would like to help us with our study, we kindly ask you fill out the following confidential

Proposed Value If you would like to help us with our study, we kindly ask you fill out the following confidential

survey. It only takes a couple of minutes, and we would greatly appreciate your participation:

Estimated Tax Amount survey. It only takes a couple of minutes, and we would greatly appreciate your participation:

xx

Visit http://www.utdallas.edu/taxsurvey/

Estimated Tax Rate and enter validation code AACLFY

Visit http://www.utdallas.edu/taxsurvey/ and enter validation code AABBMJ

Source: Data provided by Dallas Central Appraisal District (CAD). Proposed Value is Dallas CAD's estimate of the home's market value as of January 1st,

2020. Estimated Tax Amount is our estimate of taxes due this year using the latest tax rates available (some exemptions might not be included).

Estimated Tax Rate is the estimated tax amount divided by Proposed Value.

The deadline to protest is June 15th, 2020. You can fill out a short form online or mail it in. You can

find instructions on how to do this on the study's website:

Notes: Each panel corresponds

800 W. Campbell Road to the hypothetical table

Website: https://www.utdallas.edu/taxproject/ that a 800

Please

recycle

given household

W. Campbell Road would receive under the different treatment

Website: https://www.utdallas.edu/taxproject/ Please

recycle

Richardson, TX 75080 Richardson, TX 75080

https://www.utdallas.edu/taxproject/

groups. The table was placed in the middle of the first page of the letter, within the red frame with dashed lines in Figure 3

43294 22598

If you would like to help us with our study, we kindly ask you fill out the following confidential

208672 - May 2020 - UTD Letter.indd 1 5/15/2020 208672 AM

9:40:41 - May 2020 - UTD Letter.indd 1 5/15/2020 9:40:41 AM

survey. It only takes a couple of minutes, and we would greatly appreciate your participation:

Visit http://www.utdallas.edu/taxsurvey/ and enter validation code AAARMX

800 W. Campbell Road Website: https://www.utdallas.edu/taxproject/ Please 800 W. Campbell Road Website: https://www.utdallas.edu/taxproject/ Please

Richardson, TX 75080 recycle Richardson, TX 75080 recycle

17245

208672 - May 2020 - UTD Letter.indd 1 5/15/2020 9:40:41 AMFigure A.7: Timing of Survey Responses, Visits to the Website and Tax Protests

a. Cumulative Share of Survey Responses

100%

Start of Filing

90%

Share of Letters Read (Proxy)

Letter Delivery Deadline

80%

70%

60%

50%

40%

30%

20%

10%

0%

−2

−1

+1

+2

+3

+4

+5

+6

+7

+8

+19

+10

+11

+12

+13

+14

+15

+16

+17

+18

+29

+20

+21

+22

+23

+24

+25

+26

+27

+28

+39

+30

+31

2

+ Days Since Start of Letter Delivery

b. Unique Visitors to the Project’s Website

3,000

Unique Visitors to Project’s Website

Mail Walkthrough

2,500 Online Walkthrough

2,000 Filing

Deadline

1,500 Start of

Letter Delivery

1,000

500

0

−2

−1

+1

+2

+3

+4

+5

+6

+7

+8

+19

+10

+11

+12

+13

+14

+15

+16

+17

+18

+29

+20

+21

+22

+23

+24

+25

+26

+27

+28

+39

+30

+31

2

+

Days Since Start of Letter Delivery

c. Cumulative Share of Subjects who Protested

15%

Share of Subjects who Protested

Through Agent Filing

Direct Deadline

10%

5% Start of

Letter Delivery

0%

−2

−1

+1

+2

+3

+4

+5

+6

+7

+8

+19

+10

+11

+12

+13

+14

+15

+16

+17

+18

+29

+20

+21

+22

+23

+24

+25

+26

+27

+28

+39

+30

+31

2

+

Days Since Start of Letter Delivery

Notes: The first red line indicates the date when the first letter was delivered (May 21st , 2020), and

the second line denotes the deadline for filing a protest (June 15th , 2020). Panel (a) shows the cumulative

fraction of the 1,888 responses to the survey included in the field experiment. Panel (b) shows the cumulative

number of unique visitors to the website, by the type of activity. Panel (c) shows the cumulative fraction

of the 78,462 subjects in the field experiment who protested, by type of protest.

xxiFigure A.8: Effect of Official DCAD Mail Notification: Regression Discontinuity Design

15

14

13

12

11

Direct Protest Rate (%)

10

9

8

7

6

5

4

3

2

1

0 RD Coefficient: 0.436 (1.174)

−5

−4

−3

−2

−1

0

1

2

3

4

5

%−Growth in Market Value, 2020−2019

Notes: This figure features a binned scatterplot of the relationship between the

growth in the proposed value from 2019 to 2020 and the direct protest rate in

2020. The lines on each side of the threshold of zero corresponds to separate OLS

regressions. The RD coefficient corresponds to the difference in intercepts from

the two regression lines, with robust standard errors in parentheses. The sample

includes 40,111 households, 5,432 with negative change in proposed value and

34,679 with positive change in proposed value.

xxiiFigure A.9: Social Norms about the Fair Distribution of Taxes

80

60

Percent

4020

0

}

K}

K}

K}

K}

K}

}

0K

$0

$9

$8

$5

$2

$1

$1

B

,H

B

B

B

B

B

H

H

H

H

H

B

,H

0K

K,

K,

K,

K,

K,

$0

$1

$1

$2

$5

$8

$9

A

A

A

A

A

A

A

{H

{H

{H

{H

{H

{H

{H

Preferred Tax Distribution

Notes: This figure shows the distribution of social norms based on a question

included in the Field Survey regarding the fair tax burden distribution. The

horizontal axis presents the options given to respondents on how to distribute a

total tax burden of $10,000 between Household A which is worth $100,000 and

Household B which is worth $400,000. The vertical axis presents the share of the

responses choosing each option.

xxiiiFigure A.10: Validation of Partisan Identity Data: Inferred Democrat Identity vs. Voting

Results by Precinct

100

80

Inferred Democrats (%)

40 20 60

Slope: 1.075 2(0.030)

R : 0.604

N= 555

0

0 20 40 60 80 100

Democrat Votes (%)

Notes: This figure features the relationship between inferred Democrat identity

and the percentage of votes for Obama in the 2012 presidential election. Each

light dot correspond to a different precinct, while the dark dots denote the corre-

sponding binned scatterplot. The dashed line is the 45-degree line, representing

what a one-to-one relationship between inferred democrats and democrat voting

results would look like. The slope (and R2 of the relationship is shown in the

note.

xxivTable A.1: Descriptive Statistics: Quasi-Experiment, Field Experiment and Mturk Samples

Dallas County Mturk

(1) (2) (3) (4)

QE FE FE-S SE

Home Value ($1,000s) 306.91 343.91 394.98 294.12

(0.56) (1.15) (6.99) (5.70)

Number of Bedrooms 3.24 3.31 3.41 3.08

(0.00) (0.00) (0.01) (0.02)

Property Tax Amount ($1,000s) 6.15 7.17 8.22 3.50

(0.01) (0.02) (0.14) (0.07)

Property Tax Rate (%) 1.98 2.10 2.11 1.28

(0.00) (0.00) (0.01) (0.02)

Owner-Protest in 2019 (%) 5.93 5.95 10.33

(0.04) (0.08) (0.70)

Agent-Protest in 2019 (%) 7.96 4.64 5.67

(0.04) (0.08) (0.53)

2020 Homestead Exemption (%) 74.24 83.81 92.80

(0.07) (0.13) (0.60)

Age 52.29 52.68 42.69

(0.06) (0.34) (0.28)

Democrat (%) 55.07 45.55 38.64

(0.18) (1.15) (1.07)

Republican (%) 44.93 54.45 31.57

(0.18) (1.15) (1.02)

White (%) 65.12 75.17 82.95

(0.21) (1.14) (0.83)

African-American (%) 8.55 6.57 4.84

(0.12) (0.66) (0.47)

Hispanic (%) 20.39 12.03 4.50

(0.17) (0.86) (0.46)

Observations 423,607 78,462 1,888 2,065

Notes: Average pre-treatment characteristics (i.e., prior to the letter delivery) with standard errors in parentheses.

Column (1) corresponds to the Quasi-Experiment (QE). Column (2) is the subsample of the subjects from column (1)

who were selected to participate in the Field Experiment (FE). Column (3) is the subsample of the subjects from column

(2) who responded to the survey included in the letter (FE-S). Column (4) corresponds to the individuals recruited

from Amazon Mechanical Turk who participated in the Survey Experiment (SE). Home Value is the notified assessed

value; Property Tax Amount is the estimated amount of property taxes based on the notified value; Owner-Protest

and Agent-Protest indicate whether the subject protested directly or through an agent, respectively; 2020 Homestead

Exemption indicates effective homestead exemption. In columns (1)–(3), the first seven variables are obtained from the

county’s administrative records and the rest are provided by a private company (and obtained only for the households

in the field experiment). Column (4) is based on survey responses.

xxvTable A.2: Randomization Balance Test

By Letter Type By Table Type

(1) (2) (3) (4) (5) (6) (7) (8) (9) (10)

All No Letter Basic Aid Extra Aid P-value No/No Yes/No No/Yes Yes/Yes P-value

Home Value ($1,000s) 343.910 345.253 342.616 343.700 0.637 340.086 345.895 337.883 344.581 0.181

(1.148) (1.982) (1.960) (2.014) (3.377) (2.497) (3.329) (2.433)

Number of Bedrooms 3.305 3.307 3.304 3.304 0.781 3.306 3.306 3.307 3.300 0.785

(0.002) (0.004) (0.004) (0.004) (0.007) (0.005) (0.007) (0.005)

Property Tax Amount ($1,000s) 7.166 7.188 7.162 7.145 0.748 7.085 7.216 7.028 7.188 0.088

(0.023) (0.039) (0.040) (0.040) (0.067) (0.050) (0.067) (0.049)

Property Tax Rate (%) 2.103 2.104 2.106 2.099 0.239 2.107 2.104 2.093 2.104 0.252

(0.002) (0.003) (0.003) (0.003) (0.005) (0.004) (0.005) (0.004)

Owner-Protest in 2019 (%) 5.954 6.135 5.833 5.874 0.279 5.831 6.032 5.549 5.837 0.492

xxvi

(0.084) (0.143) (0.148) (0.148) (0.254) (0.184) (0.252) (0.180)

Agent-Protest in 2019 (%) 4.642 4.721 4.610 4.586 0.731 4.597 4.707 4.822 4.380 0.352

(0.075) (0.127) (0.133) (0.131) (0.227) (0.164) (0.236) (0.158)

2020 Homestead Exemption (%) 83.809 83.896 83.592 83.926 0.529 83.318 83.593 84.139 83.963 0.400

(0.132) (0.219) (0.234) (0.231) (0.404) (0.286) (0.402) (0.282)

Observation 78,462 28,068 25,012 25,382 8,506 16,761 8,253 16,874

Notes: Average pre-treatment (i.e., before the start of letter delivery) characteristics of subjects, with standard errors in parentheses. Column (1)

corresponds to the entire sample. Columns (2)–(3) break down that sample into households assigned to no letter, basic aid letter and extra aid

letter, respectively. Column (4) reports the p-value of the test of equal means across the three treatment groups. Columns (6)–(9) break down

the subjects assigned to letters by whether the table in the letter included the additional column (i.e., the county averages) and/or the additional

row (i.e., the explicit tax rate). Column (10) reports the p-value of the test of equal means across the last four treatment groups. Home Value is

the proposed assessment value; Property Tax Amount is the estimated amount of property taxes based on the proposes assessment; Property Tax

Rate is the ratio of Property Tax Amount over Home Value; Owner-Protest and Agent-Protest indicates whether the subject protested directly or

through an agent, respectively; 2020 Homestead Exemption indicates an effective homestead exemption.You can also read