Options to Build your Retirement Income - Who We Are

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Options to Build your

Retirement Income

Who We Are

The MoneySENSE-Singapore Polytechnic

Institute For Financial Literacy (IFL) is a

collaboration between Singapore Polytechnic

and MoneySENSE, a national financial education

programme for Singapore that is spearheaded

by the public-sector Financial Education

Steering Committee (FESC).

1

Objectives

Options to Build Your

Retirement Income

Benefits and Downsides of

These Options

IT’S NEVER

TOO EARLY OR

TOO LATE

TO START RETIREMENT

PLANNING

2

Building my

Retirement

Right-sizing Cash Top-up

your

Income to CPF

property SA/RA

Annuities

and

Insurance

Supplementary

Investment Retirement

Scheme

Key Life Stages

Wealth

Pre-Retirement Retirement

Wealth Accumulation Phase

Phase

• • Near

•Starting &

Established Retirement

Raising a

Career

Family

• Married • Golden

•Getting Married with Older Years

•Single Children

•Single with

•Young & Single Elderly

Parents Age

•Starting Work

Youth 20s 30s 40s 50s 65 80s

Copyright © 2017 Central Provident Fund Board. All rights reserved. Reproduction without prior written

consent by Central Provident Fund Board is strictly prohibited. Information is accurate as at January 2017.

3

• Comprises of principal, interest and

survivor benefits.

1a.

• A lump-sum payment is made in return

Annuities for promised future monthly payouts.

E.g. CPF IFEL.

Protects you from outliving your

savings during your retirement years

Downside

Benefits

You receive more by Some annuities do not factor in

living longer inflation into payouts; reducing

future purchasing power

• Whole life, endowment policies: Lump sum

cash value upon surrender or maturity.

1b. • Investment-linked products (ILPs): (a) Lump

Insurance sum cash value when surrendered, or (b)

Regular cash when units are withdrawn at

intervals.

ILP has features that ILPs have fees and charges that will

provide flexibility reduce the cash value of policy

Investment

Benefits risk Downside

Protection ceased Long term

Whole life and endowment

upon termination commitment

policies provide certainty

or maturity

4

2. Right-Sizing • Cash proceeds can be used for daily

To A Smaller expenses and investment.

Home • Can be done at one go, or in stages.

Cash proceeds that can be used for

daily expenses and investments

Downside

Benefits

Government

schemes e.g.

Larger space SHB

may not be Smaller living

Lower cost of space

needed maintenance

What are the factors that

will affect your decision

to monetise your

property?

5

Lease Buyback Scheme

(LBS)

Combined

No concurrent

monthly income

At least one owner is ownership of

of $12,000 or

Singapore Citizen property.

less.

All owners

have lived in

All owners at flat for at least

CPF Payout 5 years.

Eligibility Age

(currently 64) At least 20

or older. years of

remaining

lease.

LBS

2017 Top up Requirements

Sole Ownership Joint Ownership

Required to top up to Each co-owner is

adjusted prevailing Full required to top up to

Retirement Sum* (FRS) adjusted prevailing Basic

Retirement Sum (BRS)

CPF Payout $166,000 $83,000

Eligibility Age

(now 64) to

69

70 to 79 $156,000 $78,000

80 or older $146,000 $73,000

6

LBS

Bonus and Lease Retention

3-room or smaller HDB 4-room HDB

$1 cash bonus for every $3 $1 cash bonus for every $6

topped up to RA, up to $20K. topped up to RA, up to $10K.

Choice of Lease Retained

Age of Youngest Minimum Other Options

Owner

CPF Payout 30 35

Eligibility Age (now

64 to 69)

70 to 74 25 30, 35

75 to 79 20 25, 30, 35

80 or older 15 20, 25, 30, 35

2017

• 4-room paid-up HDB • Lims, aged 65

• valued at $450,000 • Sell 35-year lease for

• 65 years lease remaining $190,000

Cash Mr Lim (CPF RA) Mrs Lim (CPF RA)

Starting Balance $0 $20,000 $5,000

LBS Proceeds $49,000 $63,000 $78,000

LBS Bonus $10,000

Total $59,000 Lims topped up to $83,000 each.

CPF Life Payout ~ $900/month

Source: HDB Website - > Living in HDB flats -> Lease Buyback Scheme -> How it Works

7Silver Housing Bonus (SHB)

AGE & • At least one owner is a Singapore Citizen aged

CITIZENSHIP 55 or above.

INCOME • Gross monthly household income of $12,000 or

less.

EXISTING • No concurrent ownership of second property.

PROPERTY • HDB flat (met MOP for resale), or private

(SELL) property of Annual Value of $13,000 of less.

NEXT PROPERTY • Smaller HDB flat (up to 3-room) or Studio

(BUY) Apartment.

• Purchase price does not exceed selling price of

existing property.

HOUSING • Buy next property within 6 months

TRANSACTION o before selling existing property, or

o after completing sales of existing property

SHB

Top Up Requirement and Bonus

TOP UP

Up to $160,000 Required to use all net proceeds up to

cash proceeds $60,000 to top up into one or more owner’s

CPF RA.

Lessees can decide how to split the $60,000

top-up across their CPF RAs.

More than Required to make a further top-up into the

$160,000 cash CPF RA of the owner with the lowest RA

proceeds balance, up to the prevailing Full Retirement

Sum, after retaining $100,000 of proceeds in

cash.

Owners receive $1 cash bonus for every $3 top up to RA, up to

$20,000.

82017

Sell paid-up 4-room Buy Studio

@ $450,000 @ $100,000 Lims, aged 65

Cash Mr Lim (CPF Mrs Lim (CPF

RA) RA)

Starting Balance $0 $20,000 $5,000

Net Sale Proceeds (after $160,000 $80,000 $95,000

next purchase, refund of

RA and allowed

expenses)

Top-up RA ($60,000) $30,000 $30,000

Silver Housing Bonus $20,000 Top-up RA to $130,000 each

Total $120,000 CPF Life Payout ~ $1,400/month

3. Cash Top-Up • Cash top-up to his/her own and/or loved

To Special ones SA or RA under the CPF

Account (SA) Or Retirement Sum Topping-Up Scheme.

Retirement (*Terms and conditions apply)

Account (RA) • Automatic tax relief

Tax relief of up to $14,000

(*Terms and conditions apply)

Downside

Benefits

Top-ups cannot be withdrawn.

Interest is guaranteed Liquidity may be affected

and risk-free

94. • A voluntary scheme to supplement CPF

savings by saving cash into a SRS

Supplementary

account, capped at $15,300 for

Retirement

Singaporeans and $35,700 for foreigners.

Scheme (SRS) • Distributed upon death by way of a will.

Ad hoc

participation Penalty imposed when withdrawn

before statutory retirement age

Benefits Downside

Tax

incentives Savings in SRS

Impact of

account earns

Option to invest in policy changes

minimal interest

selected products

Source: www.iras.gov.sg

• SRS member has no taxable income.

• Prescribed retirement age prevailing at the time of his first SRS

contribution is 62 years old.

• Starts first penalty-free withdrawal at age 63.

• Amount in SRS account is $400,000.

YA 2016 2017 2018 2019 2020 2021 2022 202 2024 2025

3

Age 63 64 65 66 67 68 69 70 71 72

With- $40K $40K $40K $40K $40K $40K $40K $40 $40K $40K

draw Amt K

50% $20K $20K $20K $20K $20K $20K $20K $20 $20K $20K

taxable K

Tax $0 $0 $0 $0 $0 $0 $0 $0 $0 $0

Payable

No tax will be paid as the tax rate is zero for the first $20,000 of the

individual’s chargeable income.

Source: IRAS website – Tax on SRS Withdrawals

10• SRS member starts early withdrawal at age 61.

10 year penalty-free retirement withdrawal period starts from

age 62

YA 2016 2017 2018

Age 61 62 63

Withdrawal $40,000 $40,000 $40,000

Amount

Penalty (5%) $2,000 $0 $0

Withdrawal $40,000 $20,000 $20,000

Amount subject

to tax

Tax Payable $2,550 $0 $0

Source: IRAS website – Tax on SRS Withdrawals

SRS member has $400K balance, starts withdrawal at age 63 but

dies in 2015. All SRS monies shall be deemed to be withdrawn

on the date of his death.

YA 2012 2013 2014 2015 2016

Age 63 64 65 66 67

Withdrawal $40,000 $40,000 $40,000 $40,000 $240,000

Amount

Withdrawal $20,000 $20,000 $20,000 $20,000 Tax exemption*

Amount

subject to

tax

Tax Payable $0 $0 $0 $0 $0

*Tax exemption of up to $400,000 would be granted, based on number

of years remaining in the ten-year withdrawal period

11SRS member has $400K balance, withdraws at 63 – 64,

does not withdraw at 65-66 and dies in 2015.

All SRS monies shall be deemed to be withdrawn on the date of

his death.

YA 2012 2013 2014 2015 2016

Age 63 64 65 66 67

Withdrawal $40,000 $40,000 $0 $0 $320,000

Amount

Withdrawal $20,000 $20,000 ($320K – (6 x $40K) x

Amount 50% = $40K

subject to

tax

Tax Payable $0 $0 $0 $0 $550*

*Tax payable on 1st $40,000 Chargeable Income is $550.

5. • Choose products that are suitable for

Shares, Bonds, your risk profile.

Unit Trusts and • Rebalance your portfolio with lower-

Other financial risk investments when nearing

products retirement.

Provides potentially

higher returns than fixed Market fluctuations

deposits.

Downside

Benefits

Possibility of

losing capital

Impact of policy

More likely to beat changes Requires constant

inflation monitoring

12RISK AND RETURN

TRADE-OFF

Investments that have potentially higher returns will

have higher risk of losing all or part of the capital.

Stocks Highest Risk And

Potentially

Highest Return

Bonds

Cash Lowest Risk And

Lowest Return

Singapore Savings Bonds

• To provide a safe and flexible way to save for

your long‐term financial goals

• Complement CPF and other options already

available

Singapore Savings Bonds

Exchange Traded Funds

Corporate Bonds

http://www.sgs.gov.sg/savingsbonds.aspx

13Main Features of SSB

LONG-

SAFE FLEXIBLE

Fully backed by TERM Exit any month,

the Government Interest steps up with no penalty

over 10 years

Tax-exempt Start with $500

18 years

Non-transferable

and above

http://www.sgs.gov.sg/savingsbonds/Your-SSB/This-months-

bond.aspx

Consider Before Investing

Time Risk

Horizon Tolerance

Liquidity

Objectives

Needs

Transaction How Return is

Cost Generated

Diversify your investment portfolio to

reduce risk.

14Your personal circumstances will change as your life

stage changes. Re-balance your investment portfolio

accordingly.

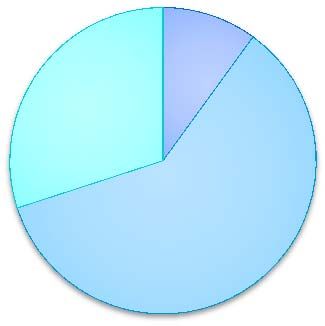

An Illustration of Asset Allocation According to Life Stages

Accumulation Savings

(20s to early 30s) (early 30s to mid 40s)

High

High Risk

Risk 20%

Medium 30% Medium

Risk Risk

50% 50% Low

Low Risk

Risk

30%

20%

High Low Medium

High Low Medium

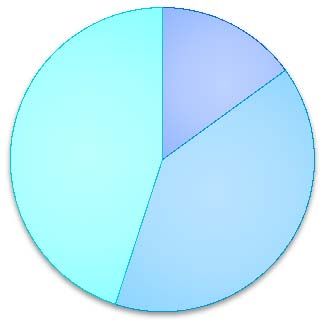

When a person is nearing retirement, he should adjust

his portfolio progressively to focus on capital

preservation.

Pre-Retirement Retirement

(mid 40s to late 50s) (late 50s onwards)

High

High Risk

Risk

15% Medium 10%

Medium Risk

Risk 20%

45% Low

Risk Low

40% Risk

70%

High Low Medium High Low Medium

15REVIEW YOUR PLAN

REGULARLY

Interest Rates Health

Inflation Rate

Factors that can

change during the pre-

retirement years and

can have an impact on

your plans

Personal Market

Circumstances Government Conditions

Policies

ACTIVITY

• Sam, 40, needs about $4,000/month to retire at 65.

• He owns a 4-room flat with his wife of the same age who is

not working.

• They have 2 children aged 8 and 10.

• If CPF Life payout grows according to inflation rate of 3%,

expected payout is $2,000/month.

$2,000 x 12 Median Life Expectancy (84) –

Retirement Age

X =

Annual

No. of Years in Gap to fill in

Retirement

Retirement cash

Income Gap in

cash

What options can Sam consider to boost his retirement income?

161. It’s never too late to start retirement planning

2. Considerations when applying age-appropriate

options

3. Be extra prudent when investing your

retirement savings.

USEFUL WEBSITES

The MoneySENSE-Singapore Polytechnic

Institute for Financial Literacy: www.finlit.sg

MoneySENSE: www.moneysense.gov.sg

www.cpf.gov.sg

www.moh.gov.sg

www.iras.gov.sg

www.sgs.gov.sg

1718

You can also read