Income Investing in a Low-Yield World - Money Show Virtual Expo, August 2021 Marvin Appel, Ph.D., M.D - Signalert Asset Management

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Income Investing in a Low-Yield World

Money Show Virtual Expo, August 2021

Marvin Appel, Ph.D., M.D.

525 Northern Blvd, Suite 210, Great Neck, NY 11021

516-829-6444

Outline

• Investment landscape: low interest rates, high volatility, inflation risk.

• Introduction to high yield bonds

• Bond fund portfolio for long-term holding

• Fixed income investing to take advantage of higher yields

• High yield bond fund trading

• Floating rate funds

• High yield municipal bond fund trading

• Covered call writing—When is it worth doing?

• Tax-advantaged risk management with options and high yield municipal bond fund trading

Treasury Yields Are At Historic Lows

High yield corporate bond mutual funds

High yield bonds have been competitive

with equities 2000-2021

Consumer Staples

Sector SPDR (XLP)

7.8%/year, 36% max

drawdown

Merrill Lynch U.S.

High Yield Master II

6.9%/year, 35% max

drawdown

S&P 500 SPDR (SPY)

6.9%/year, 55% max

drawdown

Risk measure: worst drawdown

120 120

11722 on Jan. 14, 2000

115 115

110 110

2000-2002

105

37.8% 105

drawdown

100 100

95 95

90 90

Dow Jones

85 85

Industrial Average

80 80

75 75

7286 on Oct. 9, 2002

70 70

x100 x100

1999 2000 2001 2002 2003 2004 2005Bond fund portfolio for above-average yields • Put half of capital into the Vanguard Total Bond Market Index Fund (VBMFX) • Put the other half into the Wells Fargo Short-Term High Yield Bond Fund (SSTHX) • Historical return: 4.1%/year from 2001-2021 • Worst drawdown 8.7%. • For the funds separately: • VBMFX: 3.9%/year, 6.5% worst drawdown • SSTHX: 4.2%/year, 14.2% worst drawdown

Corp. High Yield Bonds Have Done Well When

Interest Rates Were RisingLosses in Monthly Growth

high yield bondsofhave

$10,000

been infrequent

Corporate Bond

but - High Yield

sometimes Obj. Avg

severe.

$

100,000

A

m 50,000

o

u

n 20,000

t

10,000

12/87 12/91 12/95 12/99 12/03 12/07 12/11 12/15 12/19

Final Amount

Corp. high yield bond average, growth of $10,000 1988-2021. Source: Steele Mutual Fund Expert, 6/30/20213% Buy and sell stops

Mutual fund value (including interest) 110

Sell

Buy

105

Buy

100

95

Sell

90

Share price

Your inves tm ent

85

1 2 3 4 5 6 7 8 9 10 11 12

Months

8/9/2021 Signalert Asset ManagementTime of sell (move to cash) Time of buy (move from cash to shares)

Floating rate bond funds • Hold adjustable-rate bank loans made to below-investment grade borrowers • Better collateralized than high yield bonds, so better recovery (>65%) in cases of default • Interest income tracks the prime rate, which rises and falls parallel to the Fed Funds Rate. But these loans usually have a minimum interest rate of 4% even when prime is below that. • No interest rate risk, but potentially significant credit-spread risk • Beware of potential liquidity problems (as in 2008). Read your fund’s prospectus regarding trading restrictions.

Floating rate funds are less volatile than

corporate high yield bond funds (2013-2020)

Total returns: 2018

HFLAX -4.6%

PGIM High Yield PBHAX -5.6%

(PBHAX)—

2015-2016 2020

3.5%/year

HFLAX -7.8% HFLAX -22.4%

2014

PBHAX -11.2% PBHAX -21.1%

Hartford Floating HFLAX -3.9%

Rate (HFLAX)— PBHAX -5.7%

1.6%/year

2013

HFLAX -1.4%

PBHAX -5.2%Summary

Taxable high yield bond funds.

• Low interest rates present a challenge to risk-sensitive investors.

• One solution is to use corporate high yield bond funds to take

advantage of their higher yields compared to the broad bond market.

• The simplest approach is to diversify risks with a portfolio of equal

allocations to Vanguard Total Bond Market Index Fund (VBMFX) and

Wells Fargo Short-Term High Yield Bond Fund (SSTHX).

• A historically more powerful approach has been to utilize 3% buy and

sell stops to trade corporate high yield or floating rate bond funds

with the goal of reducing risks during the roughly 20% of the time

that market conditions are unfavorable, while benefitting from higher

interest income the rest of the time.High yield municipal bond funds • Federally tax-exempt (but not in most states) • May have AMT exposure • Less credit risk than taxable high yield bonds • Liquidity risk • Extremely long maturities—Much more interest rate risk than taxable high yield bonds

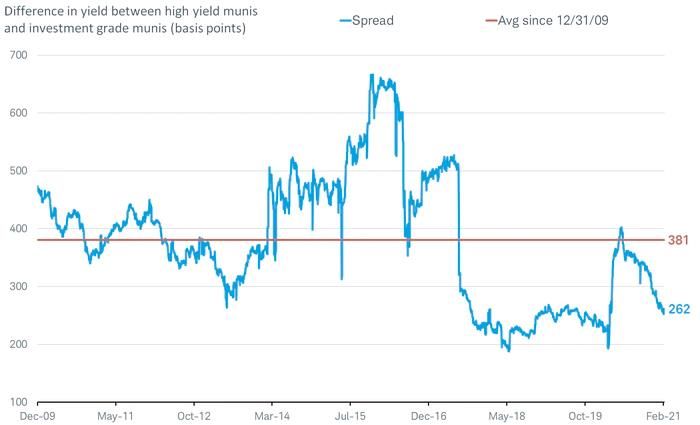

Taxable and muni high yield bond funds can usually diversify each other.

High yield muni spreads to

investment-grade are similar to

corporate bond spreads.

https://www.schwab.com/resource-center/insights/content/are-high-yield-muni-bonds-answer-to-low-yields, accessed 8/4/21Nuveen High Yield Muni Fund (NHMAX)

• Largest high yield municipal bond fund ($23 billion)

• SEC yield 2.73%

• 22 year average maturity, 9 year average duration

• 63% unrated, 10% BB

• 13% subject to AMT

• 3,416 positions

• 45% drawdown during financial crisis, 22% drawdown in 2020

• Underlying illiquid market ($144 billion total in Bloomberg Barclays index)

• Trade with the same system as corporate high yield bond funds but use

wider stops (6% to buy and sell)—five trades in 20 years.

https://www.schwab.com/resource-center/insights/content/are-high-yield-muni-bonds-answer-to-low-yields,

https://documents.nuveen.com/Documents/Nuveen/Default.aspx?uniqueId=9a5609f4-0d87-4967-a59b-28e99ca8ab70Trading rules originally published in “Higher Returns from Safe Investments” by Marvin Appel, FT Press, 2010.

An Option Strategy When Investors are Fearful

Introduction to options

• Call option

• Gives the owner the right but not the obligation to buy 100 shares at a pre-agreed price

(strike price) on or before an expiration date.

• Value of a call option rises when the underlying stock or ETF rises.

• Put option

• Gives the owner the right but not the obligation to sell 100 shares at a pre-agreed price

(strike price) on or before an expiration date.

• Value of a put option rises when the underlying stock or ETF falls.

• For every option bought there must be someone writing options on the other side of the trade

who must pay up if the buyer exercises the option.

• All else being equal, options are more expensive the longer until the expiration date and the

more volatile traders expect the underlying stock or ETF to be.How much does an option cost?

110

105

Time value

100

Stock price

95 Capital at risk

Intrinsic value

90 Strike price

85

80 Risk avoided

Capital at risk

75

70

65

60

Buy Stock Buy Call Option

Notional Value Intrinsic Value Time ValueCovered call position

• Buy 100 shares of stock 10

Profit / Loss on position at expiration

and sell one option on 8

the stock. Buy stock at $90

6 Sell covered call at $2

4

• Gain is likely to occur, 2

but is limited. 0

-2

• Losses are relatively -4

unlimited, but in a losing -6

Profit / loss on covered call position

month writing a covered

call always reduces -8 Profit / loss on ETF alone

losses compared to -10

owning the shares

81

82

83

84

85

86

87

88

90

91

92

94

95

96

97

99

80

89

93

98

100

alone.

Share Price at ExpirationPut-Call parity

Stock + dividends = call – put + cash

(cash earns risk-free interest)

As a result,

Stock – call = cash – put

In theory, covered call writing should return

the same as cash-secured put writing.Total Returns 1990-2020 Index Annual return Worst Drawdown Covered call (BXM) 7.5% -40% S&P 500 total return 9.3% -55% Put writing (PUT) 8.6% -37%

Implied volatility and VIX • “Implied volatility” is the level of volatility that a stock must demonstrate between now and expiration to make its stock options fairly priced. • VIX is an index that measures the average level of implied volatility (annualized) over the next 30 days built into S&P 500 Index options (puts and calls) expiring between 23 and 37 days from now. Its average value has been 19.5%. • The higher the level of implied volatility, the more expensive the same level of option protection. • Just because options are cheap (low VIX) doesn’t mean that they are a bargain.

Market returns under

high versus low volatility

16.00%

Annualized Returns 1990-2020

14.00%

13.70%

12.20% 11.60% BXM

12.00%

10.00% PUT

7.80%

8.00% S&P 500

6.00% 5.20%

4.30%

4.00%

2.00%

0.00%

VIX >= 19 VIX < 19Take advantage of VIX to guide your strategy:

write options when VIX > 19

Total Returns 1990-2020

12.00%

10.20%

10.00% 9.30% 9.60%

8.60%

8.00% 7.50%

6.00%

4.00%

2.00%

0.00%

S&P 500 Covered call Put writing BXM and SPX PUT and SPXThese are not conservative strategies

Worst Drawdowns 1990-2020

S&P 500 Covered calls Put writing BXM and SPX PUT and SPX

0%

-10%

-20%

-30%

-40%

-37%

-40% -40%

-50%

-44%

-60% -55%This is the best environment for

covered calls in years.

4100 4100

S&P 500 Index

4000 4000

3900 3900

3800 3800

3700 3700

3600 3600

3500 3500

3400 3400

3300 3300

3200 3200

3100 3100

3000 3000

2900 2900

2800 2800

2700 2700

2600 2600

2500 2500

2400 2400

2300 2300

2200 2200

2100 2100

2000 2000

1900 1900

90 90

80 80

70 70

60 VIX 60

50 50

40 40

30 30

20 21 20

10 12 10

2016 2017 2018 2019 2020 2021Poor risk management during market crashes

Poor Risk Management in 2020

There are other covered call indexes

available from CBOE

• Dow Jones Industrial Average (BXD, 1997-2017)

• Russell 2000 Index (BXR, 2001-2017)

• Nasdaq 100 Index (BXN, 1995-2017)

Beware:

Not all ETF covered call strategies are created

equal.Conclusions on using

covered calls for income

• This strategy works best with SPY rather than other index ETFs.

• Covered call writing has been more successful when option implied

volatility (the cost of option hedging) has been at or above average

(ie: VIX at or above 19).

• My experience in general is that covered call writing works best with

low-moderate volatility stocks and indexes but not with more volatile

underlying securities.

• Not a conservative strategy.Tax-advantaged strategy • Trade high yield municipal bond mutual funds. • Gain stock market exposure by holding in-the-money S&P 500 Index options that are 1256 contracts. • Result: Close to S&P 500 performance to the upside with downside risk reduced to the cost of the option plus the risk of high yield municipal bond funds. • The lower VIX, the better this strategy is.

Why use in-the money S&P 500 Index options?

Solid areas = capital at risk

Striped areas:

Risk avoidedSample tax-advantage trade for

S&P exposure

(8/5/21, S&P 500 at 4416) for every $441,600 in your account:

• Buy SPX 06/17/2022 4100 call at 493.80 ask (notional value $441,600). This position

will underperform the S&P 500 total return by 5.2% if the S&P 500 is flat or higher

between now and 6/17/2022 (4% time value plus 1.2% dividends missed). Maximum

stock market risk is 11.2% of the notional value (the cost of the option as a fraction

of $441,600).

• Trade the remaining $392,200 in high yield municipal bond funds. Need to make

5.9% on the funds for this portfolio to match the S&P 500. I project making half that.

• Can implement with mini-S&P index options ($XSP), each option representing

$44,160.Conclusions: • If option prices are too cheap for covered call writing, consider buying long calls and using bond fund trading to compensate for the cost of the option’s time value. • This type of strategy can garner you stock market exposure to the upside with potentially below-market risk during major declines.

Books by Marvin Appel (published by Prentice-Hall)

Disclaimers • Past results do not guarantee any future performance. • Results are based on data and calculations believed reliable, but are not audited or guaranteed. • Results are hypothetical. They are not the experience of any actual client. • Expenses such as taxes or transaction costs are not accounted for in the historical illustrations. • The strategies presented here may not be suitable for every investor. • Historical mutual fund total return data are from Investors FastTrack.

For more information

• Money management by Signalert Asset Management:

www.signalert.com, mappel@signalert.com

• Investment newsletter: Systems and Forecasts

• High yield bond timing signals

• US equity timing signal

• Relative strength between US and foreign equity timing signals

• Free newsletter trial (Sign up at www.systemsandforecasts.com)

• For a copy of these slides, email me at mappel@signalert.comYou can also read