Petron Corporation Case Presentation - CFA Institute

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

UNIVERSITY OF THE PHILIPPINES DILIMAN – VIRATA SCHOOL OF BUSINESS

Petron Corporation

Case Presentation

Michelle Therese Diaz | Christian Ernest Santos | Abigail Dy | Wilson Ramos | Christian Villar

1 December 2014

Contents

The Company ............................................................................................................................................. 2

1.1. Overview ...................................................................................................................................... 2

1.2. Ownership Structure .................................................................................................................. 2

1.3. Business Strategy ...................................................................................................................... 3

1.3.1. Expansion of regional presence in the Asia Pacific ............................................... 3

1.3.2. Leveraging on refining assets to achieve competitive advantage .......................... 3

1.3.3. Ensuring market dominance over the long-term .................................................... 3

2. The Oil Industry in the Philippines ................................................................................................... 4

2.1 The Philippine Economy ........................................................................................................... 4

2.2 The Oil Industry .......................................................................................................................... 4

2.2.1. Car Buying Boom .................................................................................................. 4

2.2.2. Market Share ........................................................................................................ 4

2.2.3. Global Oil Market .................................................................................................. 6

2.2.4. Industry-specific risks............................................................................................ 7

3. Financial Analysis............................................................................................................................... 8

3.1. Overall Financial Statement Analysis...................................................................................... 8

3.1.1. Financial Performance .......................................................................................... 9

3.1.2. Financial Position .................................................................................................10

3.1.3. Cash Flows ..........................................................................................................10

3.1.4 Industry Ratios .....................................................................................................11

3.2. Significant Accounts and Related Accounting Policies ...................................................... 12

3.2.1. Sale of Goods ......................................................................................................12

3.2.2. Accounts Receivable ...........................................................................................15

3.2.3. Trade Payables....................................................................................................17

3.2.4. Inventories ...........................................................................................................18

3.2.5. Property, plant and equipment .............................................................................19

3.3. Technical Analysis ................................................................................................................... 21

3.3.1. Stock price trend ..................................................................................................21

3.3.2. Sale of PCOR shares by PCERP .........................................................................22

4. Investment Recommendation and Justifications ......................................................................... 22

1The Company

1.1. Overview

Supplying almost 40% of the country’s oil requirements, Petron Corporation is the largest oil

refining and marketing company in the Philippines. The company operates an oil refinery in

Limay, Bataan, which processes crude oil into a full range of petroleum products. These include

gasoline, diesel, liquefied petroleum gas (LPG), jet fuel, kerosene, fuel oil, and petrochemical

feedstock benzene, toluene, mixed xylene, and propylene.

From the refinery, Petron transports its products mainly by sea to more than 30 depots and

terminals nationwide. The company supplies fuel oil, diesel, and LPG to various industrial

customers, as well as jet fuel to key airports for international and domestic carriers.

Petron retails its products in 2,200 service stations all over the country. These products include

Petron Blaze 100 Euro 4, XCS, Xtra Advance, Super Xtra Gasoline, Turbo Diesel, and Diesel

Max. The company’s LPG brands, Gasul and Fiesta, are sold to households through a wide

retail network and to industrial customers.

Petron also operates a lube oil blending plant at Pandacan Oil Terminal, where it manufactures

lubes and greases. These are also sold through Petron’s service stations and sales centers.

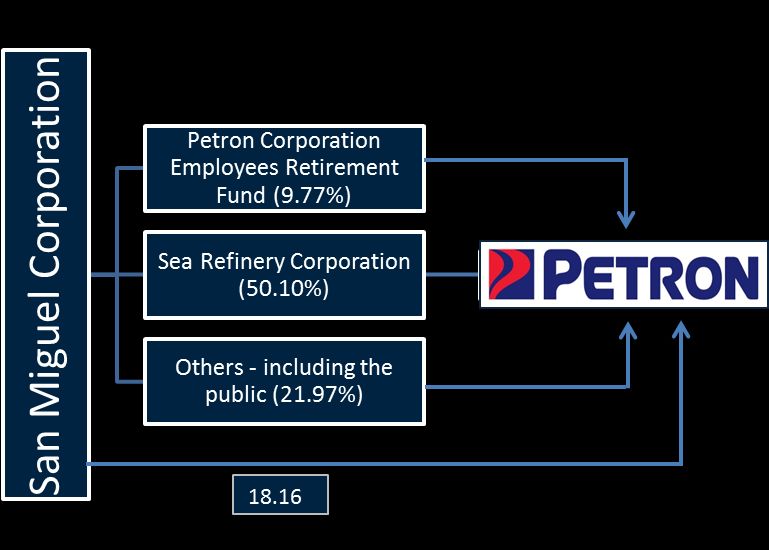

1.2. Ownership Structure

Petron is a public company listed in the Philippine Stock Exchange (PSE). Philippine food and

beverage giant San Miguel Corporation (SMC) owns 68% of Petron’s shares--a 50% indirect

ownership through SEA Refinery Corporation and an 18% direct ownership. The public holds

the rest of the stakes. Presented in Figure 1 is Petron’s ownership structure.

Figure 1. Petron’s Ownership Structure

Source: Philippine Stock Exchange (2013)

21.3. Business Strategy

1.3.1. Expansion of regional presence in the Asia Pacific

The Company gained a foothold in the Malaysian oil market in 2012 through Petron Malaysia,

which has 16.6% share in the Malaysian oil market. In March 2012, Petron completed the

acquisition of 65% of Esso Malaysia Berhad, a publicly listed company, and 100% of

ExxonMobil Malaysia Sdn Bhd., and ExxonMobil Borneo Sdn Bhd. The acquisition included the

88,000 barrel-per-day Port Dickson Refinery (PDR), 550 service stations, and seven storage

terminals.

In 2012, Petron used provisionary fair values of the identifiable net assets in calculating the

goodwill as at the acquisition date. In 2013, Petron completed the purchase price allocation

exercise. As a result, Petron restated the amounts of net assets acquired, non-controlling

interest and goodwill recognized in 2012.

Table 1. Goodwill from Petron Malaysia Acquisition

Provisionary Final

In million Pesos Amounts Amounts

Total cash consideration transferred 25,928 24,790

Non- controlling interest measured at

proportionate interest in identifiable assets 3,584 5,445

Total identifiable net assets at fair value (18,873) (20,878)

Goodwill 10,639 9,357

Source: Petron’s Annual Report (2013)

1.3.2. Leveraging on refining assets to achieve competitive advantage

In 2011, Petron launched its $2-billion refinery expansion project – the Refinery Master Plan

Phase 2 (RMP-2), which is designed to transform Petron Bataan Refinery (PBR) into one of

Asia’s most modern refineries. Once completed, the project will give Petron greater flexibility to

process cheaper crude oil varieties from non-traditional sources. RMP-2 will also enable PBR to

convert most of its fuel oil production into higher value white products, such as gasoline and

diesel. At the same time, petrochemical production will significantly increase. The project also

equips Petron’s refinery with advanced technologies to produce Euro IV-standard fuels - the

global clean air standard.

In a disclosure to PSE, Petron reported that on September 30, 2014, it “oiled in” one of RMP-2’s

major units, the Vacuum Pipestill 2 (VPS 2), in preparation for full commercial operation in early

2015.

1.3.3. Ensuring market dominance over the long-term

In 2009, Petron launched the Bulilit Station Micro Filling Station Program to fulfill the fuel

demands of far flung, rural areas in the country. The Bulilit Station is an easy-to-build gasoline

station with a two- to three-product pump operation that can be easily expanded as demand

increases in growth centers. It is ideal for far-flung areas because of its low investment cost. As

part of Petron’s expansion program, these new micro-stations will reach more Filipinos. This

program also provides business opportunities for small entrepreneurs.

32. The Oil Industry in the Philippines

2.1 The Philippine Economy

The Philippines may have experienced an economic slowdown in the third quarter of 2014,

posting a 5.3% growth, compared to 7% in the same period in 2013 (NEDA, 2014). However,

the economic outlook for the country remains positive in 2015. The Asian Development Bank

predicts that the country’s gross domestic product will grow by 6.4% next year.While this figure

is slightly lower than the previous 6.7-percent economic outlook, it is still the highest among the

Southeast Asian nations (Bloomberg, 2014).

2.2 The Oil Industry

The oil industry is divided into two sectors – the upstream and the downstream sectors. The

upstream sector is involved in the exploration, development, and production of crude oil. On the

other hand, the downstream sector is the part of the industry involved in purifying crude oil and

refining it into different products. It also involves the transportation and marketing of crude oil

and its products. Petron belongs in the downstream sector.

The Philippine downstream oil industry has been deregulated since 1998. Currently, it is

dominated by two major oil refining and marketing companies: Petron and Pilipinas Shell. Shell

operates a plant capable of refining 110,000 barrels per day. It also owns a third oil refiner and

marketer, Caltex Philippines, which converted its refinery into an import terminal in 2003. Caltex

now operates as a plain marketing and distributing company under the name “Chevron” but

maintains its Caltex brand.

Shell, together with Chevron, jointly operates the Malampaya Deepwater Gas-to-Power Project.

2.2.1 Car Buying Boom

The level of car ownership in the Philippines is among the lowest worldwide. An estimated 47%

of Filipino households do not own their cars – the fifth lowest globally – according to a study by

Nielsen. However, the study also pointed to a more robust automotive demand in the coming

years as more households join the middle class and reach the financial means to make their

first car purchase. The study also revealed that 76% of Filipinos intend to acquire a car within

the next two years. Globally, the rate is at 65%.

Meanwhile, Malaysia posted the third highest level of car ownership globally at 93% and the

highest incidence of multiple car ownership globally at 54% of households who have more than

one car.

With the recent acquisition of Petron Malaysia, Petron is in a good position in both the Philippine

and Malaysian market.

2.2.2 Market Share

As of the end of the first half of 2014, Petron dominates the petroleum business in terms of

market share. The company holds 37% of the market share, as shown in Figure 2.

4Figure 2. Petroleum Products Market Share, H1 2014

29% Petron

37%

Shell

Chevron

8% Other Players

26%

Source: Department of Energy (June 2014)

Moreover, data from the Department of Energy show that small players have been eating up the

market share of major oil companies. These oil firms have collectively lost 11% of market share

to independent oil players since 2008. Petron was the least affected among the three major oil

companies. Chevron was significantly affected with a total drop in market share of 6%.

Figure 3. Market Share Trend

Source: Department of Energy (June 2014)

According to the Philippine Oil and Gas Report by Business Monitor International, the

Philippines will likely remain a small producer of both oil and gas. Due to faster consumption

growth than output increases, the Philippines will continue to be a net importer of crude oil and

oil products, as well as join the ranks of gas importers in the world.

5Competitive Landscape – Key Players in the Philippine Oil and Gas Sector

The main government upstream vehicle is the Philippine National Oil Company

Exploration Corporation (PNOC – EC), which is a partner of various international oil

companies (IOCs) in key projects, such as the Malampaya gas project, and accounts for

10% of upstream volumes.

Shell has a 25% refined products market share, with 920 retail outlets and 67,000

barrels per day (b/d) of net refining capacity. Together with Chevron, Shell jointly

operates the Malampaya Deepwater Gas-to-Power Project. Both have a 45% interest.

Chevron has around 800 fuel retail outlets and oil storage at the site of its former 72,000

b/d San Pascual refinery.

Although refining capacity will remain flat, upgrades to the country's two refineries will

help improve utilization rates and refined oil output.

Oil consumption will likely trend upwards over the long-term alongside the economic

growth.

2.2.3 Global Oil Market

Oil prices have been dropping sharply for the past three months, with Brent crude now hovering

at $70 per barrel. On November 28, a day after OPEC (Organisation of Petroleum Exporting

Countries) meeting to discuss the matter, prices went into a serious free fall.

The root cause of the decline in oil prices is oversupply, as the US added about 4 million new

barrels of crude oil per day to the global market coming from new drilling techniques like

fracking and horizontal drilling to extract oil from shale formations in North Dakota and Texas.

However, member countries could not agree on how to respond. Thus, OPEC decided to let

prices fall in the hopes that many of the newest drilling projects in the United States will be

unprofitable and will shut down.

Figure 4. Prices of Crude Oil, 2014 Trend

Source: New York Stock Exchange (2014)

62.2.4 Industry-specific risks

Petron follows an enterprise-wide risk management framework for identifying, assessing, and

addressing inherent risk factors that affect or may affect its business called Petron Risk

Management System (PRisMS).

The Group’s risk management process is a bottom-up approach, with each risk owner

mandated to conduct regular assessment of its risk profile and formulate action plans for

managing identified risks. As the Group’s operation is an integrated value chain, risks emanate

from every process, while some could cut across groups. The results of these activities flow up

to the Management Committee and, eventually, the Board of Directors through Petron’s annual

business planning process.

The PRisMS considers incidences as major risks if it has a relatively high probability of

occurrence and has a material adverse impact to its financial performance.

Table 2. Major Business Risks

Major Risks Actions Taken

Financial risks due to interest and foreign Dollar-denominated liabilities

exchange fluctuations that may lead to hedging using forward, other

losses derivative instruments and

generation of dollar-denominated

sales.

Real-time awareness and response

by monitoring through an

enterprise-resource-planning

system

Commodity price volatility risks due to Commodity hedging activities to

changes in the price of crude oil products protect profit margins with the

authority to lock-in product and

refinery margins to protect

company profits

Effects of crude oil price changes

are passed to the market in a timely

manner as Petron operates in a

fully deregulated industry.

Operational risks due to disruptions that Effective maintenance practices

arise from accidents, processes or and inculcation of a culture of

machinery failures, human error, adverse continuous improvement

events outside of human control, and Corporate-wide health, safety, and

delays in major capital expansion projects environmental risk management

program

7Regulatory risks due to changes in the Actively maintaining lines of

policies of national and local government communications with the public,

government agencies, and other

stakeholders at both local and

national levels to identify and

respond to potential risk factors.

$100-million refinery facilities to

ensure compliance to the stricter

Clean Air Act restrictions

Scale down program to reduce

tankage capacities, joint operation

of facilities, and relocation plans to

address changes in zoning

ordinances by local governments

Source: Petron’s Annual Corporate Governance Report (2012)

3. Financial Analysis

3.1. Overall Financial Statement Analysis

Table 3. Financial Highlights

In Million Pesos

(Except per Share

and Sales Volume

Data) 2009 2010 2011 2012 2013

Net Revenues 176,531 229,094 273,956 424,795 463,638

Net Income 4,259 7,924 8,930 1,780 5,092

Fixed Assets 34,784 34,957 50,446 104,111 141,647

Total Assets 112,742 161,816 179,122 280,333 357,458

Earnings per Share 0.45 0.77 0.78 0.08 0.28

Sales Volume (in MB) 44200 48290 46700 74277 81545

Operating Margin

(ROS) 2.41% 3.46% 3.26% 0.42% 1.10%

Return on Assets 3.78% 5.77% 5.24% 0.77% 1.60%

Return on Equity 12.09% 17.51% 15.42% 2.55% 5.39%

Source: Petron’s Annual Reports (2011, 2012, 2013)

Common size analysis reveals that property, plant and equipment; trade and other receivables;

and inventories make up the bulk of Petron’s total assets in 2013. Property, plant and

8equipment comprise almost 40% of the company’s total assets, while trade and other

receivables are second to the largest contributor, with 18.93%. Inventories constitute nearly

15% of Petron’s total assets. The significant contributions of these assets were attributed to the

company’s major capital projects such as the RMP-2 and network expansion, as well as Petron

Malaysia’s rebranding of service stations.

Table 5. Common Size Analysis (Assets)

AMOUNT (IN %

MILLIONS)

Property, plant and equipment 141,647 39.63%

Trade and other receivables 67,667 18.93%

Inventories 51,721 14.47%

Source: Petron’s Annual Report (2013)

Petron’s liabilities, on the other hand, are composed mainly of short-term loans and long-term

debt. Short-term loans, which account for 28% of the company’s total liabilities, were used to

finance the importation of crude oil and petroleum products, and working capital requirements.

The company also funded its several capital projects by availing of additional long-term debt,

which is 16.23% of the total liabilities.

Table 6. Common Size Analysis (Liabilities)

AMOUNT (IN %

MILLIONS)

Short-term Loans 100,071 28%

Long-Term Debt 58,032 16.23%

Source: Petron’s Annual Report (2013)

3.1.1. Financial Performance

Full year 2013 consolidated revenues reached an all-time high of Php463.64 billlion, which is

9% higher than previous year’s level of Php424.80 billion. This was generated from total sales

volume of 81.5 million barrels (MMB), up by 7.2 MMB from 2012 due to the full consolidation of

Petron Malaysia. Cost of goods sold also increased but at a lower rate of 8% from Php406.80

billion in 2012 to Php440.48 billion in 2013.

Sales and Administrative Expenses amounted to Php11.48 billion in 2013, Php1.34 billion more

than the Php10.14 billion expenditures in 2012.

Petron closed 2013 with a consolidated net income of Php5.09 billion, which is a significant

improvement from its 2012 results of Php1.78 billion.

In 2012, Petron’s operating margin dropped to 0.42% from 3.26% the previous year. This was

due to volatility in crude and product prices in the global market.

9Figure 5. Financial Performance.

1,000 10%

800 8%

Operating Expense

600 6% Cost of Goods Sold

Net Revenues

400 4%

Gross Margin

200 2% Operating Margin

- 0%

2009 2010 2011 2012 2013

Source: Petron’s Annual Report (2011, 2012, 2013)

3.1.2. Financial Position

Petron’s consolidated assets, as of December 31, 2013, amounted to Php357.46 billion. This is

28% higher than the Php280.33 billion level at end of December 31, 2012 due largely to the

increases in property, plant and equipment, as well as cash and cash equivalents. Property,

plant and equipment surged by 36% from Php104.11 billion to Php141.65 billion because of the

company’s major capital projects and network expansion, as well as Petron Malaysia’s

rebranding of service stations.

Cash and cash equivalents rose by 87% or Php23.43 billion to Php50.40 billion essentially

sourced from internally generated funds and proceeds from loans.

Total liabilities increased by 21% from Php203.43 billion to Php245.57 billion traced to trade

payables to crude suppliers and contractors of ongoing capital projects. The company also

availed of additional long-term debt to fund various capital projects.

3.1.3. Cash Flows

Petron had better cash flows in 2013, which helped finance working capital requirements and

capital projects.

Table 7. Cash Flows

In Million Pesos 2013 2012 2011

Operating activities 33,752 1,854 790

Investing activities (43,329) (63,321) (22,637)

Financing activities 32,539 65,407 1,658

Effects of Forex 471 (438) 28

Net Cash Inflow (Outflow) 23,433 3,502 (20,161)

Source: Petron’s Annual Report (2013)

103.1.4. Industry Ratios

Petron bested its main competitor, Shell, and other companies in the industry in terms of growth

rate. Petron’s sales grew by 9% in 2013, compared to Shell’s 4.58% and the industry’s 4.36%.

Moreover, because of Petron’s various capital projects, its capital expenditure is more than four

times larger than the industry, dwarfing Shell’s -26.88-percent capital spending.

From a financial standpoint, Petron is generally less risky than Shell. In financing its growth with

debt, Petron is less aggressive compared to Shell and other companies in the industry, as

evident in its relatively low debt to equity ratio of 2.34 (compared to Shell’s 5.27 and industry’s

84.7).

Petron’s quick and current ratios are also above the industry benchmark. This means that

compared to other companies within the industry, Petron is more able to pay its short-term

obligations (using its liquid assets, in the case of quick ratio). However, the Petron’s current ratio

is still below Shell’s 1.2 and the ideal ratio of 2:1.

While greater than Shell’s, Petron’s interest coverage ratio of 1.27 is way below the industry’s

37.81. This means that Petron may be hardly meeting its interest expenses.

In the efficiency department, Petron’s turnovers are greater than Shell’s and the industry

average. However, Shell collects its receivables almost twice faster than Petron.

In terms of management effectiveness, Petron fared better than Shell. This means that Petron

manages its assets and shareholders’ money to generate profits better than Shell. However,

Petron’s ratios are still below the industry benchmark. The ratios of Petron, Shell, and industry

are presented in Table 8.

Table 8. Petron, Shell, and Industry Ratios

PETRON SHELL INDUSTRY

Growth rates (2013 vs

2012)

Sales 9% 4.58% 4.36%

Capital Spending 23% -26.88% 5.58

Financial Strength

(MRQ)

Quick ratio 0.76 0.63 0.73

Current ratio 1.07 1.20 1.03

LT Debt to Equity 71% 130.04% 45.91%

Total Debt to Equity 2.34 5.27 84.7

Interest coverage

(2013) 1.27 -0.30 37.81

11PETRON SHELL INDUSTRY

Efficiency

Receivable turnover 7.39 13.55 4.72

Inventory turnover 8.70 6.74 8.58

Asset turnover 1.45 0.51 1.02

Management

Effectiveness (2013)

Return on Assets 1% -1.19% 3%

Return on Equity 5% -6.91% 8%

Sources: Reuters (2014), Shell’s 2013 Financial Statements, Petron’s Annual Report (2013), 3Q and Petron’s

Quarterly Report (3Q 2014)

MRQ – Most Recent Quarter – End of 3Q 2014

3.2. Significant Accounts and Related Accounting Policies

3.2.1. Sale of Goods

Revenue from sale of goods in the course of ordinary activities is measured at the fair value of

the consideration received or receivable, net of returns, trade discounts, and volume rebates.

Revenue is recognized when the significant risks and rewards of ownership of the goods have

been passed to the buyer, which is normally upon delivery, and the amount of revenues can be

measured reliably.

Petron’s Sources of Revenue

The management of Petron identifies segments based on business and geographic locations.

The Group/s major sources or revenues come from sales of petroleum which include gasoline,

diesel, and kerosene. These are offered to motorists and public transport operators through the

station networks all over the Philippines.

Revenue also includes insurance premiums from the business and operation of all kinds of

reinsurance, both on sea and on land, of properties, goods and merchandise, of transportation

and conveyance, against fire, earthquake, marine perils, accidents, and all other forms and lines

of insurance authorized by law, except for life insurance.

Revenue also comes in the form of lease of acquired real estate properties which are used for

petroleum, refining, storage and distribution facilities, gasoline service structures, and other

related structures.

12Table 9. Petron’s Sources of Revenue

Source: Petron’s Annual Report (2013)

Breakdown of Petron’s Petroleum Business

The biggest contributor in revenue is the reselling of fuel, with a value of P245.8 billion or 53%

of total revenues. Almost 30% comes from industrial revenues, amounting to P132.46B. Other

sources of revenues account for 12%. Gasul has a contribution of 5% or P24.8B, while lube

comes in with a value of P3.086B or 1% of revenues. Revenue sources are presented in the pie

chart below.

Figure 6. Revenue Sources

Revenue Sources

12% Reseller

Lube

29% Gasul

53%

Industrial

Others

5% 1%

Source: Petron’s Annual Report (2013)

13For geographical segments, 80% comes from the local market which is equivalent to P284.5B.

Twenty percent or P72.5B comes from international sales. The pie chart below presents

Petron’s geographical segments.

Figure 7. Petron’s Geographical Segments

Geographical Segments

20%

Local

International

80%

Source: Petron’s Annual Report (2013)

Sales Trend

Gross profit margin has been decreasing since 2009, as shown in the table below.

Table 9. Petron’s Sales, Cost of Goods Sold, Gross Profit, and Gross Profit Margin

2013 2012 2011 2010 2009

Sales 463,638 424,795 273,956 229,094 176,531

Cost of Goods Sold 440,479 406,798 251,610 209,280 161,583

Gross Profit 23,159 17,997 22,346 19,814 14,948

Gross Profit Margin 5% 4% 8% 9% 8%

Source: Petron’s Annual Report (2011, 2012, 2013)

The Company showed an unusually high growth rate in 2012 due to the consolidation of newly

acquired Petron Malaysia operations.

Table 10. Growth Rate of Petron’s Sales, Cost of Goods Sold, and Gross Profit

2013 vs 2012 vs 2011 vs 2010 vs

2012 2011 2010 2009

Sales 9% 55% 20% 30%

Cost of Goods Sold 8% 62% 20% 30%

Gross Profit 29% -19% 13% 33%

Source: Petron’s Annual Report (2011, 2012, 2013)

14Effect of Supply Agreement with NPC and PSALM

The Parent Company entered into various supply contracts with National Power Corporation

(NPC) and Power Sector Assets Liabilities Management Corporation (PSALM). According to the

contract, Petron will supply the bunker fuel, diesel fuel oil, and engine lubricating oil of selected

NPC and PSALM plants, and NPC-supplied Independent Power Producers (IPP) plants.

It can be concluded that this agreement helped secure guaranteed sales for Petron. For NPC

alone, it has secured P1.43B sales since 2009, while PSALM has contributed P659M since

2012. While it may not be the huge chunk of their annual sales, these still have a significant

impact. For 2013 alone, their revenue from NPC stood at P1.3B and P42M from PSALM.

Combining these, they constitute 0.37% of the total revenue.

3.2.2. Accounts Receivable

Petron’s trade receivables are “noninterest-bearing and are generally on a 45-day term.”

Government receivables refer to duty and tax claims, such as duty drawback, VAT and specific

tax claims, as well as subsidies receivable from the Government of Malaysia. These include

receivables of more than 30 days but less than one year amounting to P6.3 billion and P14.8

billion in 2013 and 2012, respectively.

Table 11. Petron’s Receivables

Source: Petron’Annual Report (2013)

Accounting Policies

Subsequent to initial measurement, receivables are carried at amortized cost using the effective

interest rate method less any impairment in value. The company recognizes any interest earned

on receivables and periodic amortization as part of “interest income” account in the consolidated

statements of income on an accrual basis. Calculating amortized cost includes any discount or

15premium on acquisition and fees that are part of the effective interest rate. When receivables

are derecognized or impaired, gains or losses are recognized in profit or loss.

The company maintains allowance for impairment losses on trade and other receivables at a

level considered enough to provide for potentially uncollectible receivables. The level of

allowance is based on past collection experience and other factors that affect collectability.

When the company identifies accounts receivable to be worthless after exhausting all collection

efforts, impaired accounts receivable are written off. An increase in allowance for impairment of

trade and other receivable adds to the Group’s recorded selling and administrative expenses

and decrease current assets.

Accounts Receivable Aging

In 2013, 41% of unimpaired trade account receivables were not collected during the 31- to 60-

day period. This is a little improvement compared to the previous year when the company failed

to collect about 46% of the unimpaired receivables during the 61- to 90-day period. Presented in

the table below is the age of past due but not impaired trade accounts receivable, as of

December 31, 2013 and 2012:

Table 12. Petron’s Past Due But Unimpaired Trade Receivables

Source: Petron’s Annual Report (2013)

Based on the company’s past collection experience, there is no need for allowance for

impairment for these past due but unimpaired trade receivables. There are no significant

changes in credit quality. Thus, these amounts may still be recovered.

Petron collects its receivables 7.39x, which is above the industry’s 4.72 receivable turnover.

However, Petron’s main rival, Shell, is more efficient in collecting its receivables, with a turnover

of 13.55x.

16Table 13. Petron’s, Shell’s, and Industry’s Receivable Turnover

Petron Shell Industry

Receivable turnover 7.39 13.55 4.72

Source: Reuters, Shell’s 2013 Financial Statements and Petron’s 2013 Annual Report

Collection Period and Credit Risk

In general, “the maximum credit risk exposure of trade and other receivables is its carrying

amount without considering collaterals or credit enhancements, if any.” However, Petron has no

significant credit risk concentration because its trade customers are largely homogenous. Below

is the credit risk exposure of the company based on receivables, as of December 31, 2013 and

2012.

Table 14. Petron’s Credit Risk Exposure

Source: Petron’s Annual Report (2013)

To monitor trade receivables and credit lines, Petron records real-time daily sales and collection

transactions of all customers. The company also requires collateral to minimize credit risks in

trade receivables. Moreover, Petron adopts a comprehensive credit rating system based on

financial (i.e., customer’s financial standing) and non-financial (e.g., customer’s nature of

business, industry background, and payment habit) assessments of its customers.

3.2.3. Trade Payables

Petron’s accounts payable are liabilities to haulers, contractors and suppliers that are

noninterest-bearing and are generally settled on a 30-day term. These also include provisions,

retention payable, accruals of selling and administrative expenses, and deferred liability on

customer loyalty program that are normally settled within a year.

Trade payables to crude suppliers and contractors of ongoing capital projects contributed mainly

to the 21-percent increase in total liabilities from 203.43 billion to 245.57 billion in 2013.

173.2.4. Inventories

Accounting Policies

Inventories are carried at the lower of cost and net realizable value (NRV). For petroleum

products, crude oil and tires, batteries and accessories (TBA), the net realizable value is the

estimated selling price in the ordinary course of business, less the estimated costs to complete

and/or market and distribute. For materials and supplies, net realizable value is the current

replacement cost.

Petron uses the first-in, first-out method in costing petroleum products, crude oil, and other

products. Cost is determined using the moving-average method in costing lubes and greases,

waxes and solvents, materials, and supplies inventories.

Table 15. Petron’s Inventories

2013 2012 2011

Crude oil and others (2013 – at NRV; 2012 – at

cost) 25,509 22,182 19,322

Petroleum (2013 – at NRV; 2012 – at cost) 24596 25955 17,378

TBA products, materials and supplies:

Materials and supplies – at NRV 1584 1418 1,033

Tires, Batteries, Accessories – at cost 32 27 30

51,721 49,582 37,763

Source: Petron’s 2013 Annual Report.

The cost of these inventories amounted to Php53 million and Php50 million as of December 31,

2013 and 2012, respectively.

Inventories charged to cost of goods sold amounted to P433 million, P398 million, and P245

million in 2013, 2012 and 2011, respectively. Inventory write-down included in cost of goods

sold amounted to Php737 million in 2013.

Table 16. Inventory Level

Petron Shell MIR*

Inventory Turnover 8.52 6.57 -

Ave. Age of Inventory 42.70 54.8 30.00

*MIR – Minimum Inventory Requirement

Source: Reuters, Shell’s 2013 Financial Statements and Petron’s 2013 Annual Report

18Inventory Management

For petroleum products, Petron has two major projects aimed at improving the delivery to

customers–the Inventory-Driven Delivery System (IDDS) and the Global Position System

(GPS). Eighty percent of its accounts and service stations have been enrolled in the IDDS from

only 18% in 2012. IDDS is a program that ensures the stable supply of petroleum products at

Petron’s service stations. This resulted in an optimum utilization of its tank trucks. Meanwhile,

88% of the company’s contracted tank truck fleet is already equipped with GPS tracking system

which allows real-time monitoring of deliveries. These initiatives and the continuous Tank Truck

Modernization Program enabled the company to improve the safety, product integrity, and

delivery reliability of its operations. These also ensured that dealers have sufficient supply at all

times, ultimately benefiting customers.

Minimum Inventory Requirement

Effect of Crude Oil Prices

Since inventory is measured at NRV, with the current trend of decreasing crude oil price, there

is a risk that the crude oil value may be written down.

Figure 8. Effect of Crude Oil Prices

Source: NYSE (2014)

3.2.5. Property, plant and equipment

Accounting Policy

Property, plant and equipment (PPE), except land, are stated at cost less accumulated

depreciation and amortization and any accumulated impairment in value. Such cost includes the

cost of replacing part of the PPE at the time that cost is incurred.

19Construction in progress (CIP) represents structures under construction and is stated at cost.

This includes the cost of construction and other direct costs. Borrowing costs that are directly

attributable to the construction of PPE are capitalized during construction period. CIP is not

depreciated until such time that relevant assets are ready for use.

Depreciation and amortization, which commence when the assets are available for their

intended use, are computed using the straight-line method.

Table 17. Property, Plant and Equipment

Buildings Service Computers,

Refinery, Land and

and Stations and Motor and Construction

Plant and Leasehold TOTAL

Related other Office in Progress

Equipment Equipment Improvement

Facilities Equipment

COST

December 31, 2012 22,457 48,743 14,276 4,142 11,754 57,591 158,963

Additions 869 60 831 88 243 49,494 51,585

Disposals/reclassifi

cations/Acquisition 4,081 771 510 (124) 265 (14,741) (9,238)

of subsidiaries

Currency

translation 455 73 52 51 40 (76) 595

adjustment

December 31, 2013 27,862 49,647 15,669 4,157 12,302 92,268 201,905

DEPRECIATION

AND

AMORTIZATION

December 31, 2012 13,343 28,095 9,152 2,747 1,515 - 54,852

Additions 1,310 2,389 1,175 313 66 - 5,253

Disposals/reclassifi

cations/Acquisition 1,021 (251) (687) (172) 18 - (71)

of subsidiaries

Currency

translation 129 51 33 9 1 - 224

adjustment

December 31, 2013 15,803 30,284 9,673 2,897 1,600 - 60,258

NET BOOK VALUE

December 31, 2012 9,114 20,648 5,124 1,395 10,239 57,591 104,111

December 31, 2013 12,059 19,363 5,996 1,260 10,702 92,268 141,647

Source: Petron’s Annual Report (2013)

The most significant item is the “Construction in Progress” which refers to the P92.3B – RMP2

Project.

20The RMP Project

RMP-2 is Petron’s $2-billion project that allows the full utilization of the PBR’s 180,000 barrels-

per-day capacity, therefore enhancing the country’s supply security. Petron will convert low-

value fuel oil to high-value white products, such as LPG, gasoline, jet fuel, and diesel. The

construction of this project is set to be fully commissioned by early 2015.

The parent company has signed and executed a US$480 million (2011: $1=P43.31, Php20.79B)

term loan facility which is amortized over 5 years and is subject to a floating interest rate plus a

fixed spread. Interest capitalized in 2013 and 2012 amounted to Php3,529 million and Php886

million, respectively. Capitalization rate used for borrowings was at 6.22% and 5.71% in 2013

and 2012.

Tax Incentive

On June 3, 2011, the Board of Investments approved Petron’s application under RA 8479 as an

existing industry participant with a new investment in modernization/conversion of Bataan

Refinery’s RMP-2. The BOI is extending the following major incentives: income tax holiday for

five years, minimum duty of 3% and VAT on imported capital equipment, tax credit on domestic

capital equipment, and exemption from real property tax and contractor’s tax.

3.3. Technical Analysis

3.3.1. Stock price trend

Towards the end of the first quarter of 2014, Petron stocks (PCOR) dropped by 15% from

Php13.40 on March 26 to Php11.7 the following day. This movement was repeated on August

18 when Petron’s stock price fell from Php12.70 to Php11.78

Figure 9. Petron Stock Price Trend January 1 to November 28, 2014

Source: Philippine Stock Exchange (2014) PCOR OHLC Stock Data

213.3.2. Sale of PCOR shares by PCERP

Petron’s two separate disclosures on March 27 and August 18, 2014 stated that one of the

company’s major stockholders, Petron Corporation Employees’ Retirement Plan (PCERP), sold

470 million and 380 million Petron common shares, respectively, at a price of Php11.50 per

share through the facilities of the Philippine Stock Exchange pursuant to a placement

agreement.

4. Investment Recommendation and Justifications

Based on quantitative and qualitative analyses, it can be concluded that Petron is a “Buy”

investment. Moreover, the company’s strong operating revenue growth and cash flows,

improved operational efficiency, acquisition of Petron Malaysia, and high potential upside justify

this recommendation.

4.1. Strong Operating Revenue Growth and Cash Flows

Petron’s cash flows significantly improved in 2013. This trend is expected to continue provided

that oil prices stabilize. Moreover, the high demand forecast in the coming years, as driven by

an expected car buying boom, will solidify the company’s growth targets.

4.2 Improved operational efficiency

RMP-2 will allow PBR to maximize its production capacity, process a wider range of crude oil,

and eliminate the production of low margin fuels. One of the units will also have a by-product

called petcoke, which, because of its high-heating value, makes it a good fuel for the newly

operational Refinery Solid Fuel-Fired Boiler. This, in turn, will generate steam and power for the

refinery, lowering refining costs due to self-reliance on power generation.

The risks of the capacity of the domestic market to absorb the additional volume are mitigated

as the Philippines remains to be a net importer of finished products. Petron can also offer to

service the requirements of other petroleum retailers through competitive pricing agreements,

as buyers will have no freight cost.

4.3 Petron Malaysia, a good investment

The acquisition of Petron Malaysia is a good strategic decision because of Malaysia’s robust

economy. Moreover, Malaysia’s per capita consumption of fuel is two times larger than that of

the Philippines (World Bank, 2014).

4.4 High potential upside

Less than four months away from the full completion of RMP-2, it is a good time to buy the

stock. Since the sale of PCOR shares held by PCERP, the stock has traded at a range of

Php11.10-Php11.98 from January’s high of Php14.40. This could mean a 20-40% potential

upside.

22REFERENCES

Asian Development Bank. (2014.) Asian Development Outlook 2014. Retrieved from

http://www.adb.org/countries/philippines/economy

Department of Energy. (June 2014). Supply and Demand Report H1 2014.

Department of Energy (2003). Department Circular 2003-01-001

Munoz, Michael. (Sep. 25, 2014). ADB Latest GDP, Inflation Forecasts to 2015. Retrieved from

http://www.bloomberg.com/news/2014-09-25/adb-latest-gdp-inflation-forecasts-to-2015-table-

.html.

National Economic Development Authority. (2014). Statement of Sec. Balisacan on the 2014 Q3

Performance of the Philippine Economy. Retrieved from http://www.neda.gov.ph/?p=4460

New York Stock Exchange. (2014). WTI NYMEX Crude Oil Price Trend.

Nielsen. (April 16, 2014). “Rising Middle Class Will Drive Global Automotive Demand in the

Coming Years.” Retrieved from http://www.nielsen.com/my/en/press-room/2014/rising-middle-

class-will-drive-global-automotive-demand.html

Organisation of Petroleum Exporting Countries. (2014). World Oil Outlook 2014.

Petron Corporation. (2011, 2012 and 2013). Annual Report.

Petron Corporation. (Oct. 28, 2014). 2012 Annual Corporate Governance Report (updated on

Oct. 28, 2014).

Philippine Stock Exchange. (January 13, 2014). Public Ownership Report (PSE Form No POR -

1).

Philippine Stock Exchange. (April 2, 2012). Acquisition of down-stream oil business of Exxon

Mobil Malaysia.

Philippine Stock Exchange. (March 19, 2012). Mandatory Take-Over Offer.

Philippine Stock Exchange. (May 20, 2014). Petron's US$2 Billion Project Nears Completion.

Philippine Stock Exchange EDGE. (2014). PCOR OHLC Stock Data.

Pilipinas Shell. (2013). Pilipinas Shell 2013 Annual Report

Reuters Markets. (2014). Financials: Petron Corp (PCOR.PS). Retrieved from

http://www.reuters.com/finance/stocks/financialHighlights?symbol=PCOR.PS

World Bank. (2014). Global Economic Monitor.

23You can also read