Pharmaceutical Payment Methods, 2013 Update - amcp guide to - version 3.0

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

amcp guide to

Pharmaceutical Payment Methods,

2013 Update

version 3.0

amcp guide to

Pharmaceutical Payment Methods,

2013 Update

version 3.0

A M C P G u i d e t o P h a r mac e u t i ca l Pa y m e n t M e t h o d s , 2 0 1 3 U p d at e

about this publication

NOTE THIS MATERIAL EDITED FOR 2013. This is an update Author Disclosures: Howard Tag, JD, and Elan Rubinstein,

of the October 2009 AMCP Guide to Pharmaceutical Payment PharmD, MPH, provide consulting services to clients that include

Methods which was created by the Academy of Managed Care professional associations, health plans, purchasers, regulators,

Pharmacy Task Force on Pharmaceutical Payment Methods in providers, pharmaceutical, biological and medical device

conjunction with the consulting firm of Tag & Associates, Inc. The manufacturers, and other health care entities.

update incorporates revisions by Tag & Associates, Inc. (lead author:

Elan Rubinstein, PharmD, MPH. editor: Howard Tag, JD, production About AMCP: AMCP is a national professional association of

services: Debra Glover), Alexandria, VA. The Academy wishes to pharmacists and other health care practitioners who serve society

thank the following reviewers for their valuable input: by the application of sound medication management principles

and strategies to improve health care for all. The Academy’s nearly

Tom Bizzaro, RPh

7,000 members develop and provide a diversified range of clinical,

Vice President, Health Policy and industry Relations, educational, and business management services and strategies on

First Databank, Inc. behalf of the more than 200 million Americans covered by a managed

care pharmacy benefit. For more information about AMCP, visit

Loreen M. Brown, MSW www.amcp.org.

Senior Vice President, Commercial Consulting

XcendaAmerisourceBergen Consulting Services

Rob Coppola, PharmD, MBA

Senior Director, Business Development, Magellan Pharmacy

Solutions

Dan Hardin, RPh, MBA

Segment President, Public Sector and Pharmacy Technology

Solutions, Catamaran

Phil Lettrich

Director of Professional Relations,

Emdeon Business Services

Chuck Reed

Group Vice President, Pharmacy Technology and Solutions,

AmerisourceBergen Corp.

Academy of Managed Care Pharmacy | 2

A M C P G u i d e t o P h a r mac e u t i ca l Pa y m e n t M e t h o d s , 2 0 1 3 U p d at e

table of contents

Executive Summary............................................................ 5 Comparison of Benchmark Prices .....................................27

Highlights....................................................................6 Exhibit II-2. Estimated Prices Paid to Manufacturers,

Payment Benchmarks.........................................................6 Relative to List Price (AWP), for Brand-Name Drugs

Under Selected Federal Programs, 2003.....................27

Average Wholesale Price and Wholesale

Acquisition Cost ........................................................6 Benchmarks and the Goal of Appropriate Payment .........27

Average Sales Price ......................................................7

III. PAYERS AND PAYMENT METHODS.............................. 29

Average Manufacturer Price ...........................................7

Medicare........................................................................29

Federal Upper Limit ......................................................8

Background................................................................29

Best Price.....................................................................8

Medicare’s Influence on Prescription Drug Payment.........29

Maximum Allowable Cost or Maximum

Reimbursement Amount.............................................8 Hospital Outpatient Departments .................................29

National Average Retail Price and National Physician Offices.........................................................29

Average Drug Acquisition Cost.....................................8 Pharmacy-Dispensed Medicare Part B Drugs..................29

Public Health Service 340 B Price...................................9 Pharmacy-Dispensed Medicare Part D Drugs..................30

Payers and Payment Methods .............................................9 Exhibit III-1. Sources of Medicare Beneficiary Drug

Medicare .....................................................................9 Coverage, 2010.......................................................30

Medicaid ...................................................................10 Exhibit III-2. Standard Medicare Drug Benefit, 2012 ......30

Private Purchasers.......................................................10 Exhibit III-3. Brand-Name Prescription Drug Savings

Recent Pharmaceutical Payment Milestones...................12 in the Coverage Gap ................................................31

Table I. Pharmaceutical Payment Milestones: Exhibit III-4. Generic Drug Savings in the

2005–2013 ...........................................................12 Coverage Gap..........................................................31

Medicare Payment to PDPs .........................................31

I. INTRODUCTION............................................................ 17 Exhibit III-5. Aggregate Part D Reimbursement

Exhibit I-1. Milliman Medical Index Annual Rate of Amounts, CY 2013..................................................32

Increase in Costs by Component of Medical Care.........17 Exhibit III-6. Part D Risk Corridors for 2013...................32

Exhibit I-2. Monthly and Median Costs of Cancer Drugs PDP Report to CMS of “Lock-In-Price” Versus

at the Time of Approval by the FDA, 1965–2008 .......17 “Pass-Through Price”............................................33

Pharmaceutical Manufacturer Price Negotiations........33

II. PAYMENT BENCHMARKS ............................................ 19

Part B vs. Part D.....................................................33

Benchmarks....................................................................19

Protected Therapeutic Classes..................................33

Average Wholesale Price .............................................19 Least Costly Alternative (LCA).......................................33

Wholesale Acquisition Cost...........................................20 Home Health and Home Infusion..................................34

Average Sales Price.....................................................20 Exhibit III-7. Medicare Fee-For-Service Coverage for

Average Manufacturer Price..........................................21 Home Infusion.........................................................34

Exhibit II-1. Components of AMP Calculation..................22 Exhibit III-8. Medicare Payment Rates For Drug

Exhibit II-2. Example of Average Manufacturer Prices Infusion by Treatment Setting....................................35

For Oral Solid Generic Drugs, For August 2012...........23 Medicaid Background.......................................................36

Federal Upper Limit.....................................................24 Dual Eligibles (Medi/Medi)...........................................37

Best Price ..................................................................24 Retail Community Pharmacy Reimbursement.................37

Maximum Allowable Cost or Maximum Reimbursement Rebates.....................................................................37

Amount .................................................................25 Private purchasers...........................................................38

National Average Retail Price and National Average Structure of Privately Sponsored Health Coverage............38

Drug Acquisition Cost ..............................................25 Exhibit III-9. Coverage by Type of Health Insurance,

340B........................................................................26 2010 and 2011......................................................39

Academy of Managed Care Pharmacy | 3

A M C P G u i d e t o P h a r mac e u t i ca l Pa y m e n t M e t h o d s , 2 0 1 3 U p d at e

table of contents

Benefit Design ...........................................................40 IV. HOW PRODUCTS, SERVICES, AND PAYMENTS FLOW

Drugs Assigned to the Medical Benefit vs. Pharmacy THROUGH CHANNELS OF DISTRIBUTION .................... 52

Benefit....................................................................40 Exhibit IV-1. Pharmacy Benefit (Other Than Medicare

Exhibit III-10. Medical Benefit Cost Sharing for Specialty Prescription Drug Benefit) ........................................52

Drugs.....................................................................40 Exhibit IV-2. Medicare Prescription Drug Benefit .............53

Exhibit III-11. Pharmacy Cost Trends.............................40

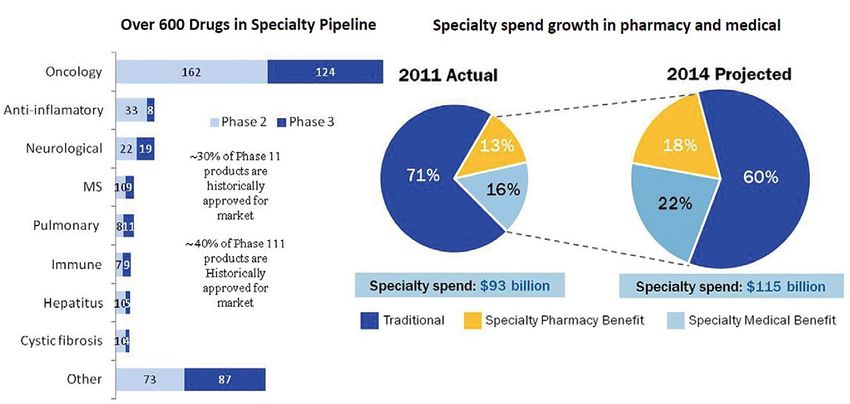

Exhibit III-12. Specialty Drugs in the Drug Development V. ISSUES AND IMPLICATIONS FOR STAKEHOLDERS ....... 56

Pipeline, and Projected Impact of Specialty Drugs No Clear Successor to the AWP Benchmark .......................56

on Drug Spend........................................................41 Issue ........................................................................56

Exhibit III-13. Medical and Pharmacy Benefit Implications ...............................................................56

Coverage by Drug Administration Type........................42 Bundling (Combining) Drugs with Services.........................57

Use of Formularies .....................................................41 Issue ........................................................................57

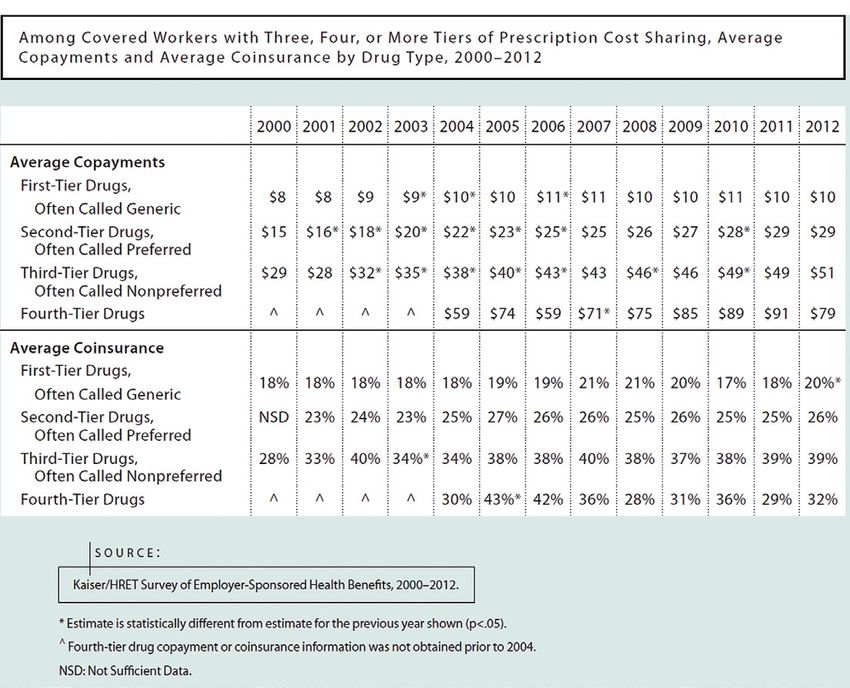

Exhibit III-14. Prescription Drug cost Sharing Among Implications ...............................................................58

Covered Workers .....................................................43 Pricing Transparency: Is It Meaningful?...............................58

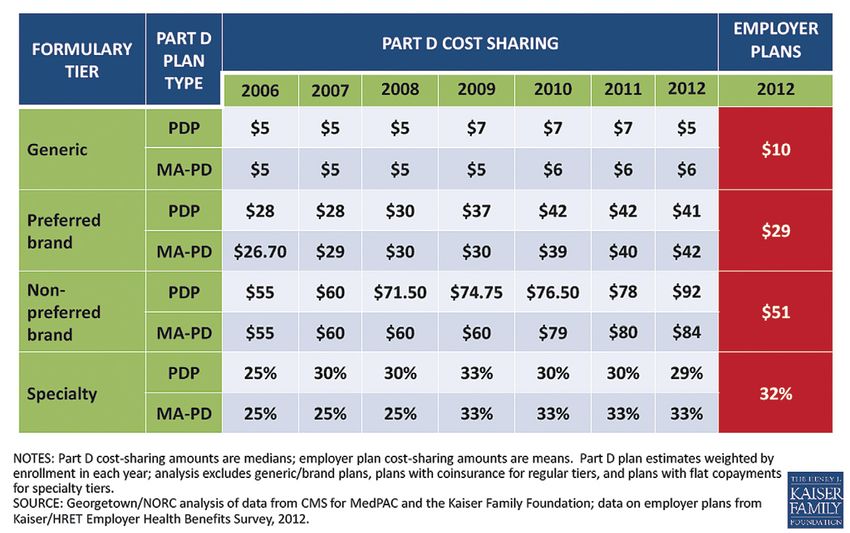

Exhibit III-15. Cost Sharing For Medicare Part D Plans Issue........................................................................ 58

2006–20012, and Employer-Sponsored Implications ...............................................................58

Plans, 2012 ...........................................................44 How Significant Will be Biosimilars’ Market Impact..............58

Traditional and Transparent Pricing................................43 Issue.........................................................................58

Class of Trade ............................................................44 Implications ...............................................................59

Exhibit III-16. Example of Pharmaceutical Classes PBM Dilemma: Challenges in the Face of Generic

of Trade..................................................................45 Prescription Clubs and Copay Coupons ..........................59

Prescription Drug Rebates ...........................................44 Issue ........................................................................59

Importation and Reimportation of Pharmaceuticals .........46 Implications ...............................................................59

Exhibit III-17. Shipper’s Customer Guidance for High Deductible Plan Cost Shift to the Beneficiary...............59

Pharmaceuticals Importation.....................................46 Issue ........................................................................59

Patient Expenditures for Pharmaceuticals.......................46 Implications ...............................................................59

Drug Copay Coupons and Copy Cards............................47 Role of Comparative-Effectiveness Research Findings to

Structure Drug Benefits and Manage Drug Access ............60

Relationship of Provider to Payment Method...................47

Issue ........................................................................60

Community Pharmacy.................................................47

Implications ...............................................................60

Exhibit III-18. Pharmacy Discounts and Dispensing

Will Pharmaceutical Manufacturers Accept Risk for Desired

Fees by Pharmacy Channel ......................................48

Therapeutic Outcomes From use of Their Products............61

Exhibit III-19. Drug Utilization per 1 Million Health Issue ........................................................................61

Plan Lives by Site of Service .....................................49

Implications................................................................61

Exhibit III-20. Private Sector ASP-based Physician Orphan and Ultra-Orphan Drugs........................................61

Reimbursement for Office-Administered Infusible and

Issue ........................................................................61

Injectable Drugs.......................................................49

Implications................................................................61

Exhibit III-21. Private Sector AWP-based Physician

How Will Greater Use of Pharmacogenomics Affect

Reimbursement for Office-Administered

Drug Pricing ................................................................62

Infusible and Injectable Drugs...................................50

Issue.........................................................................62

Exhibit III-22. Predominant Reimbursement

Methodology in the Physician-Office Setting................51 Implications................................................................62

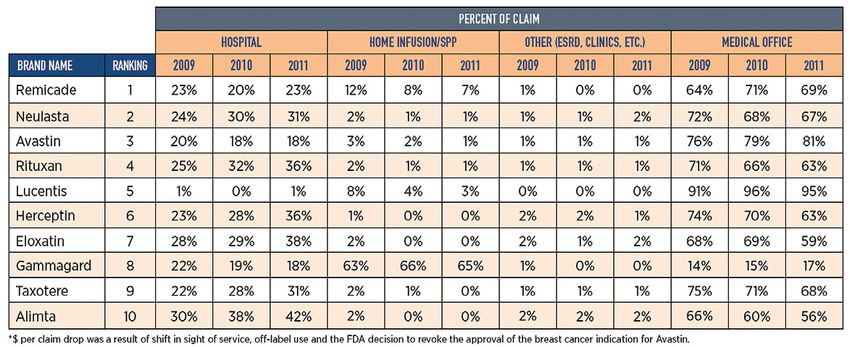

Exhibit III-23. Specialty Pharmacy Distribution to

VI. ACRONYM LIST.......................................................... 78

Physician Office.......................................................51

Hospital Inpatient and Outpatient .................................48

VII. GLOSSARY................................................................ 83

Physician Office Drugs.................................................49

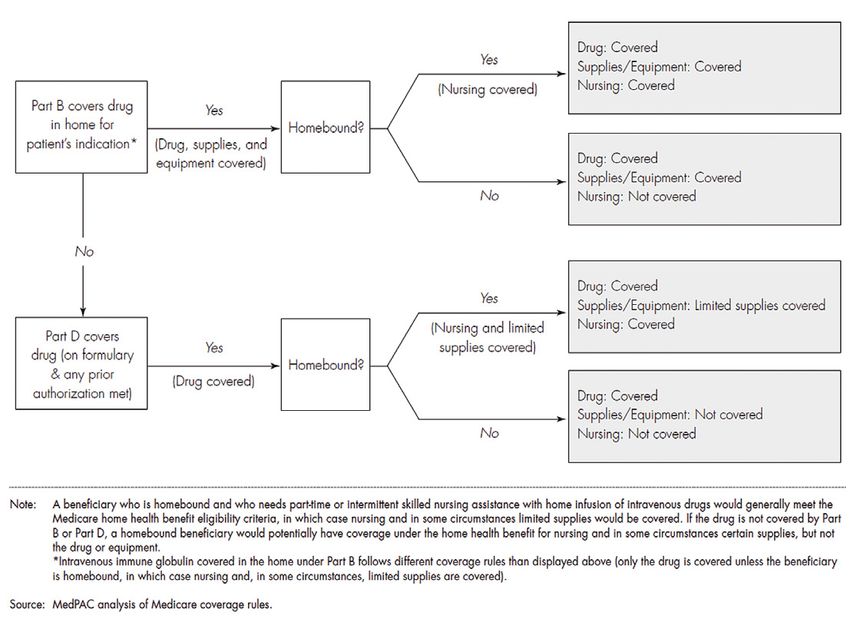

Home Health..............................................................50 viii. REFERENCES........................................................... 96

Academy of Managed Care Pharmacy | 4

A M C P G u i d e t o P h a r mac e u t i ca l Pa y m e n t M e t h o d s , 2 0 1 3 U p d at e

Executive Summary

Executive Summary 17.1% of AMP for blood clotting factors, all per unit or the

difference between the AMP and the best price per unit and

The methods by which the U.S. health care system pays for adjusted by the Consumer Price Index-Urban (CPI-U) based

prescription drugs are changing because of on launch date and current quarter AMP.

• Growth of healthcare as a percentage of GDP. • Cap on total rebate amount for innovator drugs to 100%

• Healthcare reform (The Patient Protection and Affordable Care of the AMP

Act, known as PPACA). • Additional Medicaid Line Extension rebates for oral solid

• Payer demands for price transparency. dosage forms of single source or innovator multiple source

drugs (e.g., new formulations such as extended release).

• Increasing cost sharing by patients.

• Extended Medicaid rebates to cover Medicaid patients in

• The belief by many stakeholders that prescription drug prices managed care organizations.

and price increases should be moderated.

• A new formula for calculating the Federal Upper

• Increasing Generic Dispensing Rates. Reimbursement Limit (FUL)

• Increase in specialty pharmaceuticals on the market, their • New definitions of AMP and multiple source drug.

increasingly high cost per course, and increasing specialty

pharmacy penetration and utilization (in both the pharmacy • Expanded eligibility for Public Health Service 340B

and medical benefit). discounts.

• Undisclosed prescription drug rebates and discounts which • An FDA approval pathway for biosimilar biological

may differ by type of purchaser. products and Medicare Part B payment that would

incentivize their use.

The current debate about prescription drug payment methods

centers on determining the most appropriate basis for calculating Private payers have followed the government’s lead but

how payers, including patients, government agencies, employers, have not aggressively ventured out on their own to change their

and health plans, should pay pharmacies and other providers payment methods and benchmarks. As of the publication date

for dispensing prescription drugs and providing pharmaceutical of this Guide, AWP and manufacturer-determined Wholesale

services. Historically, payment for prescription drugs has been Acquisition Cost (WAC) remain widely used payment benchmarks

based on published prices that do not necessarily reflect the for private insurance reimbursement to pharmacies, physicians,

actual acquisition costs paid by providers, primarily pharmacies, and other providers. It is unclear how replacement of the AWP

physicians, and hospitals. This has led policymakers to believe benchmark might affect provider payment for two reasons: (a) no

that Medicare and Medicaid programs have paid more than widely available alternative benchmark has been selected, and

is necessary for prescription drugs. The reality is much more (b) pharmacy benefit manager contracts with network pharmacies

complex, confounded by the two necessary components of a often include language to adjust payment under any new

reimbursement formula: estimated ingredient cost and dispensing benchmark to maintain comparable pricing to the AWP standard.

fee. Currently, reimbursement of the ingredient cost often Despite the pushback on using AWP, this much-maligned

subsidizes the dispensing fee, which can be confusing and which benchmark continues to be available from a variety of sources.

may generate calls for more transparency. Bundling of outpatient prescription drugs into payment for

selected diagnoses and procedures is being tried on an expanded

Thus, in an effort to reform the payment system and reduce

basis by Medicare for renal dialysis, hospice and on a limited,

drug expenditures, policymakers have made significant and

voluntary basis with Integrated Delivery Networks and some

proposed changes to the benchmarks used by public programs to

private payers. However, the tradition for outpatient treatment

pay for drugs, and, in some cases, have created new benchmarks

continues to be that drugs are a pass-through cost to be charged

altogether.

at the providers’ actual or estimated acquisition price plus a

Federal government activity to reduce drug expenditures via pre-determined markup.

payment system changes was a component of healthcare reform.

The U.S. drug purchasing and distribution system is

PPACA included these changes that impact drug payment and complex and involves multiple transactions among myriad of

payment methodologies: stakeholders, including drug manufacturers, distributors, Group

• Increased minimum Medicaid drug rebates to 23.1% of the Purchasing Organizations, government entities, third-party

Average Manufacturer Price (AMP) for single source drugs, payers, pharmacies (retail, mail order, specialty), pharmacy

13% of AMP for non-innovator multiple source drugs, and benefit managers, physicians, and patients. Changes in

Academy of Managed Care Pharmacy | 5

A M C P G u i d e t o P h a r mac e u t i ca l Pa y m e n t M e t h o d s , 2 0 1 3 U p d at e

Executive Summary

payment methods or benchmarks, and laws impacting pricing by private payers, and the relationship of these factors to the

to government entities and government-specified entities, availability of rebates from drug manufacturers.

have significant implications for all stakeholders, affecting

the payments and prices to and from each of these groups. How Products, Services, and Payments Flow Through Channels

Knowledge of the intricate distribution and payment systems for of Distribution. Section IV provides a detailed analysis of

prescription drugs is essential to ensure that payment reform how drugs are purchased, distributed, and paid for by various

results in desired outcomes including fair and equitable payment entities within the pharmaceutical supply chain in the U.S. The

to providers while avoiding unintended consequences such as purpose of this section is to examine the complexity of the drug

reduced access to medically necessary drugs. distribution system as well as the multiple direct and indirect

transactions that occur.

AMCP recognizes the need to help stakeholders and

policymakers better understand, evaluate and navigate the Select Issues and Implications for Stakeholders. Section V

profound changes occurring in payment for prescription drugs in explores the issues and implications of the most significant

the United States. This 2013 update to the 2009 AMCP Guide changes to drug payment methods or benchmark prices that

to Pharmaceutical Payment Methods1 offers a comprehensive have been proposed or implemented in recent years. The topics

examination of the methods and price benchmarks that have been evaluated in this section include actual acquisition cost (AAC)

used in the public and private sector to pay for pharmaceuticals in and the surveys used to determine NADAC and NARP; the use

the United States, the changes that have occurred or are likely to of weighted average AMP for calculation of federal upper limit

occur in the future, and the forces that are behind these changes. (FUL); the implications of ASP+6% payment under Medicare

AMCP has made every effort to make the Guide an unbiased Part B; pricing transparency; the role of comparative-effectiveness

presentation of information, issues, and implications. research; orphan drugs; and bundling of provider payment for

Following the introduction (Section I), the Guide is presented prescription drugs with payment for other related services.

in four main sections covering the following subject areas:

Highlights

Payment Benchmarks. Section II explains the drug payment

The following are discussed in this Guide. Please refer to the

benchmarks that have come into use over the past four decades,

corresponding section in the Guide for a more detailed discussion

how and when they are used, and how they compare to one

of trends in drug pricing and payment.

another. The benchmarks discussed in detail are those that

have the greatest overall impact on pharmaceutical payment

or are currently receiving the most scrutiny and discussion, nn Payment Benchmarks

including average wholesale price (AWP), average sales price Health plans cover pharmaceuticals under the “medical benefit”

(ASP), average manufacturer price (AMP), wholesale acquisition (typically drugs administered in a medical office or clinic setting,

cost (WAC), maximum allowable cost (MAC) also referred to as or administered through home health), and the “pharmacy

maximum reimbursement amount (MRA), federal upper limit benefit” (typically drugs dispensed by a retail, mail order or

(FUL), national average retail price (NARP), and national average specialty pharmacy). Pharmaceuticals covered under the medical

drug acquisition cost (NADAC). benefit and/or the pharmacy benefit component of a health plan

typically have differing payment methods and use different pricing

Payers and Payment Methods. Section III describes payment benchmarks.

methods used by payers as well as manufacturers’ price

concessions related to product preference and acquisition Average Wholesale Price and Wholesale

across various settings of care such as community pharmacy,

Acquisition Cost

mail service pharmacy, physician offices, clinics and

hospitals. Discussed in this Guide are: Public payers such as Historically, AWP has been the generally accepted drug payment

Medicare, Medicaid, the Department of Defense, the Veterans benchmark for most payers, primarily because it is current

Administration, and the Public Health Service’s 340B program; and readily available. However, in recent years AWP became

private payers such as commercial insurers, self-funded recognized as a “sticker price” that does not reflect the average

employers and individual patients; intermediaries including wholesale price ultimately paid after subtraction of undisclosed

managed care organizations and pharmacy benefit managers; price concessions.

and providers such as hospitals, physicians, pharmacies and AWP is related to WAC, although not by a standard multiplier.

home health providers. Also covered are topics relevant to private Historically, the relationship of AWP to WAC has been most

health insurance, including benefit design, the use of formularies commonly, though not always, characterized by one of the

Academy of Managed Care Pharmacy | 6

A M C P G u i d e t o P h a r mac e u t i ca l Pa y m e n t M e t h o d s , 2 0 1 3 U p d at e

Executive Summary

following equations, as determined by the publisher: AWP = 1.20 Average Sales Price

x WAC, or AWP = 1.25 x WAC for branded pharmaceuticals.

As a result of the 2003 Medicare Prescription Drug, Improvement,

While multiple source generic drugs may have WACs from which

and Modernization Act (MMA) (Public Law 108-173), ASP

AWPs can be calculated, their reimbursement is typically based

replaced AWP as the basis for payment for most drugs covered

instead on maximum allowable cost.

under Medicare’s medical benefit—Medicare Part B—as of

However, WAC is not reflective of an actual acquisition cost for January 1, 2005. Unlike AWP, ASP is based on manufacturer-

a wholesaler, because the WAC does not include discounts and reported actual selling price data and includes the majority of

price concessions that are offered by manufacturers. For sole- rebates, volume discounts, and other price concessions offered

source branded pharmaceuticals, WAC more closely approximates to all classes of trade (excluded from the calculation of ASP are

the price that pharmacies pay to manufacturers or wholesalers all sales that are exempt from “best price” and sales at “nominal

than does AWP and, for this reason, often serves as the basis for price” [see Glossary]).

discounts and rebates negotiated between manufacturers and

Because ASP is a volume-weighted average, some providers

private payers (i.e., discounts and rebates are typically based on

are able to obtain pharmaceuticals below this average selling

WAC) for both medical and pharmacy benefit drugs. Manipulation

price, while others are able only to purchase the drugs at a price

of the so-called “spread” or differential between WAC and

that is above the average. ASP prices are based on manufacturer-

AWP has been the subject of lawsuits against pharmaceutical

submitted data that is two quarters in arrears, and do not include

manufacturers and publishers alleging “gross inflation” of AWP

subsequent pricing changes. In general, small physician offices

for certain drugs and has led to the discontinuation of publishing

and regional specialty pharmacies buy small quantities at the

or to a dramatic overhaul of its ‘definition’ by the remaining

least favorable prices and are unable to purchase some drugs at

publishers of this widely used benchmark.

prices at or below the ASP prices or ASP-based payment amounts.

Recognition of the unreliability of AWP (or of its continued Generally, large physician groups and hospitals are able to

availability) as a benchmark of real-world prices actually paid negotiate the best discounts and price concessions and are better

by pharmacies and other purchasers, including physicians, has positioned under the ASP payment system.

precipitated the search for other reference prices for payment

From a payer perspective, ASP can also create misaligned

purposes. The uncertainty of AWP as a basis for payment for

incentives to dispense higher cost drugs due to a flat 6% mark-

pharmaceuticals in the United States became an issue for

up in Medicare Part B (larger mark-ups are applied by some

all stakeholders on March 17, 2009, with the decision by

commercial health plans), when less expensive alternatives exist.

U.S. District Court Judge Saris on the proposed settlement in

Some commercial health plans have implemented a tiered mark-

the two national class action lawsuits against First Databank

up on ASP, varying with compliance to health plan prescribing

and McKesson. This decision resulted in the roll-back of the

policies (for example, Blue Shield of California Professional fee

multiplier used to calculate AWP. The WAC multiplier of 1.25 (or

Schedule. See: https://www.blueshieldca.com/provider/claims/fee-

greater than 1.20) was reduced to 1.20 for the 1,442 National

schedules/home.sp).

Drug Code (NDC) numbers referenced in the lawsuit, effective

September 26, 2009, under order of the court in acceptance Average Manufacturer Price

of the proposed settlement. First Databank, an independent

Congress created Average Manufacturer Price (AMP) as part of the

commercial publisher of drug pricing information, announced

Omnibus Budget Reconciliation Act (OBRA 1990) for the purpose

that it would discontinue publication of AWP no later than 2

of calculating rebates to be paid by manufacturers to states for

years following implementation of the recalculated AWPs—and

drugs dispensed to their Medicaid beneficiaries. AMP was defined

has done so. Medi-Span made a similar announcement at the

as the price available to the retail class of trade and reflected

time, but ultimately reversed that decision, announcing that it

discounts and other price concessions afforded those entities. The

will continue to publish AWP until there is a generally accepted

Deficit Reduction Act of 2005 (DRA) mandated that AMP instead

alternative.2 Truven Healthcare, publisher of Redbook, and

of AWP be used for the calculation of the FUL.

Elsevier, publisher of Gold Standard (ProspectoRx) continue to

publish AWP as of the publication date of this Guide. Like ASP, AMP represents an effort by the federal government

to step away from AWP to an alternate benchmark price. In

While several independent publishers have proposed

2003, the AMP approximated 79% of AWP for brand name drugs

alternative pricing benchmarks, at the time of this publication, no

with no generic equivalents. The Congressional Budget Office

comprehensive, transparent, and widely acceptable alternative to

(CBO) estimated that the acquisition cost to retail pharmacies

AWP has been identified.

averages approximately 4% above the AMP for brand name drugs

without generic equivalents.3

Academy of Managed Care Pharmacy | 7

A M C P G u i d e t o P h a r mac e u t i ca l Pa y m e n t M e t h o d s , 2 0 1 3 U p d at e

Executive Summary

In March 2010, the Patient Protection and Affordable Care Act the draft methodology used to calculate the FULs.7, 8 Because

(PPACA, PL 111-148) changed the definition of AMP, to represent posted monthly AMP-based FULs fluctuated significantly month-

the average price paid to the manufacturer by wholesalers for to-month, CMS created an alternative methodology based on

drugs distributed to retail community pharmacies and by retail a rolling 3-month average of the monthly AMP-based FULs.9

community pharmacies that purchase drugs directly from the However, the monthly and three month rolling average FUL files

manufacturer. PPACA excluded certain payments and rebates do not exactly match, because CMS does not have three months

or discounts provided to certain providers and payers from of data for all drugs, and because the older data may be less

calculation of AMP, including wholesaler customary prompt reflective of pharmacies’ current purchase price. As of publication

pay discounts, certain bona fide services fees, manufacturer of this Guide, these results are posted on the CMS website for

reimbursement for unsalable returned goods, and payments, review and comment.10 Until the draft is finalized, CMS is using

rebates or discounts related to entities that do not conduct the prior formula of 150% of the lowest published price as an

business as a wholesaler or retail community pharmacy. “interim methodology” to calculate FULs.4

Federal Upper Limit Best Price

The Deficit Reduction Act of 2005 (DRA) mandated that AMP Medicaid best price was created by OBRA 90 and took effect

instead of AWP be used for the calculation of the federal upper January 1, 1991 in the calculation of rebates that manufacturers

limit (FUL), the maximum amount of pharmacy reimbursement are required to pay to the states and the federal government for

for product costs for certain generic and multiple-source drugs sales of single-source and multiple-source branded products to

that the federal government will recognize in calculating federal Medicaid beneficiaries. According to a Congressional Budget

matching funds for payment to state Medicaid programs. That Office (CBO) report published in June 2005, best price for brand-

is, Federal Medicaid matching funds to states are limited to name drugs approximates 63% of AWP.

payments that do not exceed the FUL in the aggregate for

multiple-source drugs, plus a dispensing fee set by each state. Maximum Allowable Cost or Maximum

The FUL list is created and maintained by CMS for use by states Reimbursement Amount

in their Medicaid Pharmacy programs, but it is also in the public

Maximum allowable cost (MAC), also referred to as maximum

domain for use by any entity.

reimbursement amount (MRA) is typically a reimbursement limit

Effective October 1, 2010, PPACA revised the Social per individual multiple-source pharmaceutical, strength and

Security Act to require HHS to calculate the FUL as no less dosage form. MAC price lists are established by health plans and

than 175 percent of the weighted average (determined on PBMs for private sector clients and by many states for multiple-

the basis of utilization) of the most recently reported monthly source pharmaceuticals paid for by their Medicaid and other state-

average manufacturer price (AMP) for pharmaceutically and funded programs. Private sector MACs usually are considered

therapeutically equivalent multiple source drug products that confidential. While clearly defined in FUL for Medicaid, there is no

are available for purchase by retail community pharmacies on standardized private sector definition, methodology, update timing

a nationwide basis. In a study published October 2012, the or market application for MAC.

Office of Inspector General reported that FUL amounts based Medicaid generic drug cost containment in some states is built

on published prices were more than four times total pharmacy around MAC programs. Those state Medicaid programs create

acquisition costs; and that AMP-based FULs were 61% lower their own lists of maximum reimbursement prices for generic

than published price-based FULs at the median.4 drugs. As a general rule, state MAC lists include more drugs and

CMS has proposed that FUL be a unit price calculated for establish lower reimbursements than the FUL list because they

each multiple source drug for which the FDA has rated three or are not bound by the FUL three-drug/three-supplier rule, nor by

more products therapeutically and pharmaceutically equivalent, the FUL payment methodology. For a drug on the FUL list, the

meaning A-rated in the FDA Orange Book.5 “Initially a FUL will state MAC can be lower but not higher than the FUL.

not be published for any FUL group that does not contain at least

three innovator and/or non-innovator drug products at the NDC-9 National Average Retail Price and National

level, that are “A rated” with three monthly AMP prices with AMP Average Drug Acquisition Cost

units greater than zero reported and certified by manufacturers to State Medicaid programs currently reimburse pharmacies for

calculate the weighted average of monthly AMPs.”6 covered outpatient drugs based, in part, on the estimated

CMS has issued draft AMP-based FUL reimbursement files acquisition cost (EAC), the agency’s best estimate of the price

for review and comment, for multiple source drugs, including generally and currently paid by providers for a drug marketed or

Academy of Managed Care Pharmacy | 8

A M C P G u i d e t o P h a r mac e u t i ca l Pa y m e n t M e t h o d s , 2 0 1 3 U p d at e

Executive Summary

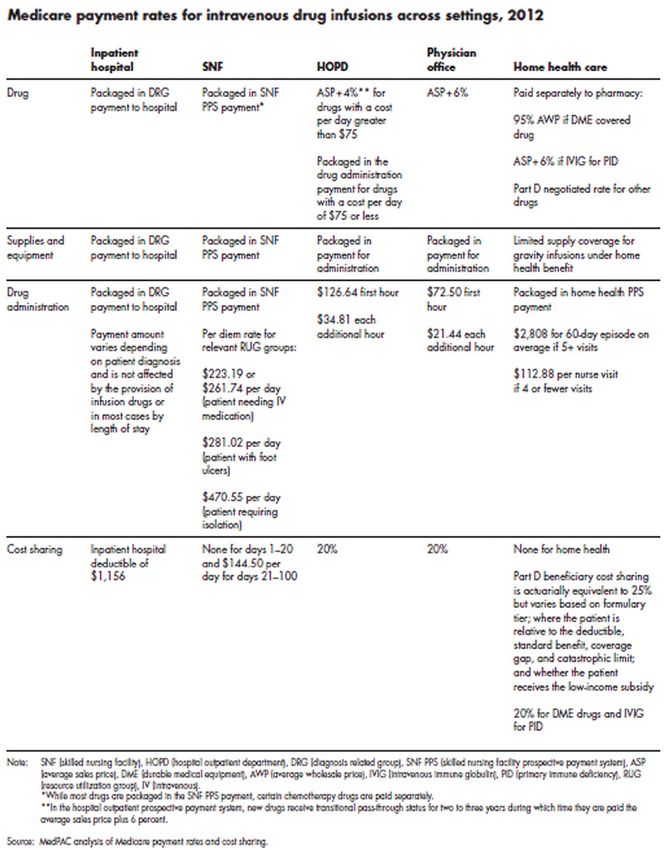

sold by a particular manufacturer or labeler in the package size of nn Payers and Payment Methods

drug most frequently purchased by providers. On February

Payment to providers for the drugs they administer or dispense

2, 2012, in CMS-2345-P, CMS proposed replacement of EAC

varies depending on the payer and the site of care.

with estimated actual acquisition cost (AAC), and engaged

(through competitive procurement) Myers & Stauffer (a private

Medicare

accounting firm) to provide state Medicaid agencies with

acquisition costs and consumer purchase prices of covered Medicare’s payment for drugs depends on the treatment setting.

outpatient drugs dispensed by pharmacies (not including Drugs provided in the hospital inpatient setting typically do not

specialty pharmacies), through a recurring pharmacy survey receive separate payment, but instead their costs are accounted

described in “Survey of Retail Prices: Payment and Utilization for in the diagnosis related group (DRG)-based prospective

Rates and Performance Rankings”. payment made to the hospital. Similarly, drugs used in the

hospital outpatient department for which the cost per day is

The survey objectives are to collect data for calculation of

$80 or less (for CY 2013) are bundled into ambulatory payment

National Average Retail Price (NARP), a monthly pricing database

classification (APC) reimbursement for the procedures with which

of actual drug prices provided voluntarily by independent and

they are used; there is no separate payment made for those drugs.

chain pharmacies in the United States, including for cash

For CY 2013, CMS will pay acquisition and pharmacy overhead

paying customers, customers with commercial third party

cost for hospital outpatient separately payable drugs and biological

insurance, and Medicaid customers. Another survey objective,

without pass-through status at ASP plus 6%. Part B prescription

established by CMS but not mandated in PPACA, is to collect

drugs administered in the physician office or clinic are also paid at

data on the purchase prices of all Medicaid covered outpatient

ASP plus 6%.

drugs dispensed by independent community pharmacies and

chain pharmacies, for calculation of the National Average Drug The Federal Government’s financial and budget issues have

Acquisition Cost (NADAC). As with AMP-based FUL, CMS has the potential to cause changes in reimbursement. For example,

posted draft NARP and NADAC reimbursement files for review the Sequester of 2013 will result in reduction of Medicare Part

and comment by the public.11 B payment from ASP+6% to ASP+4% for claims on or after

April 1st. However, as of the time of publication of this Guide,

Separately, some state Medicaid programs have implemented

it is not possible to know if this change in reimbursement

or are in the process of implementing an AAC-based

will be sustained or if there may be other changes in federal

reimbursement methodology. These states include Alabama,

health services reimbursement. It is also impossible to know if

Oregon, Idaho, Iowa, Louisiana, California and New York.12

these changes in federal reimbursement will influence or affect

reimbursement by commercial entities that sometimes emulate

Public Health Service 340B Price government reimbursement methods.

Public Health Service (PHS or 340B) price (referred to as a

For end stage renal dialysis, injectable and oral drugs with

‘340B ceiling price’) is the highest price that a ‘340B-covered

injectable equivalents administered in relationship to dialysis

entity’ could be charged, and is equal to the price that the state

treatment are included in the Medicare per-dialysis prospective

Medicaid agency would pay absent any supplemental discount

payment.14 The American Taxpayer Relief Act (H.R. 8), signed

or rebate. However, 340B pricing can be better than Medicaid

into law on January 1, 2013, included delay in addition to

pricing because sales do not include retail pharmacy markups and

the prospective payment of orals-only drugs related to dialysis

because 340B providers usually negotiate sub-ceiling prices.

treatment until January 1, 2016 (previously these drugs had been

340B ceiling prices for brand-name drugs were reported scheduled for addition to the prospective payment on January 1,

to average 51% of AWP. PPACA expanded the 340B program 2014).15

to include certain children’s hospitals, freestanding cancer

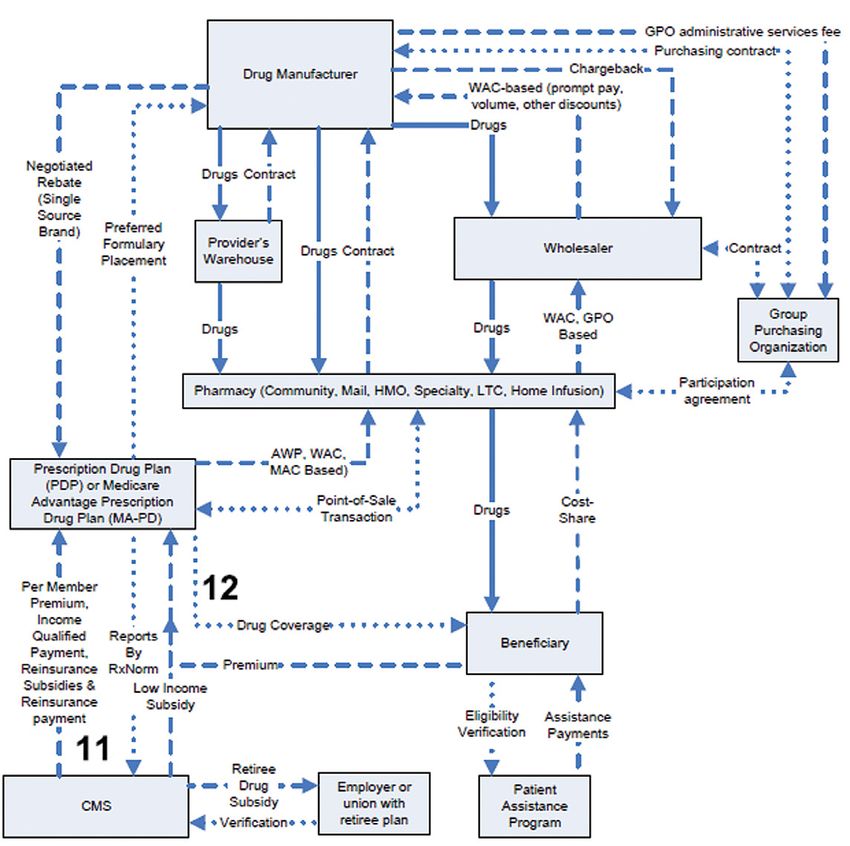

On January 1, 2006, as a result of passage of the MMA,

hospitals, critical access hospitals, rural referral centers, and

Medicare began to pay for outpatient pharmaceuticals dispensed

sole community hospitals. PPACA exempted pharmaceutical

at the pharmacy under Part D. Part D benefits are provided

manufacturers from having to provide discounts on orphan drugs

through stand-alone prescription drug plans (PDPs) or Medicare

to these newly eligible entities, as proposed, if the drugs are used

Advantage prescription drug plans that are integrated with a

to treat diseases for which they received orphan-drug designation.

medical plan (MA-PDs). These drug plans typically are offered

by PBMs and commercial health plans. Subject to legislated

mandates and to CMS guidelines and approval, each PDP

and MA-PD sets its own premiums, benefit structures, drug

Academy of Managed Care Pharmacy | 9A M C P G u i d e t o P h a r mac e u t i ca l Pa y m e n t M e t h o d s , 2 0 1 3 U p d at e

Executive Summary

formularies, pharmacy networks, and terms of payment. Thus, OIG found that 10 of 22 states using the carve-in approach did

unlike the other components of Medicare where a standard not collect rebates.19

payment formula typically exists, drug payment to pharmacies Every state Medicaid program, either directly or through

and member cost-share vary by individual plan under Part D. managed Medicaid organizations, also pays for drugs that are

Part D plans and MA-PDs may negotiate discounts and/ utilized under the medical benefit (e.g., in the physician’s office

or rebates with drug manufacturers. In late 2012, it was and clinic). Drugs covered under the medical benefit are typically

proposed that Part D drug sales for dual eligible and low income paid for differently than are drugs covered under the pharmacy

beneficiaries, together representing approximately 56% of Part benefit, using formulas that vary by state, that are based on AWP,

D enrolled patients, be made subject to Medicaid statutory drug WAC, or ASP. States are required to collect rebates for drugs

rebates. However no such change has been implemented as of administered in these settings also, but as of 2009, not all states

the publication date of this Guide.16 were in compliance.20

Medicaid Private Purchasers

Currently, every state Medicaid program includes an outpatient Compared with public payers, there is less transparency in the

prescription drug benefit (also called a “pharmacy benefit”). payment methods used by private payers to pay for prescription

As of July 1, 2011, 74.2% of Medicaid enrollees nationwide drugs. For example, private payers use MAC price lists for

were enrolled in managed care plans, including health insuring multiple-source drugs; however, prices contained in these MAC

organizations, commercial managed care organizations, lists, the methodology by which these lists are constructed, the

Medicaid-only managed care organizations, Primary Care Case frequency with which they are updated, and network pharmacies

Management, prepaid inpatient health plans, prepaid ambulatory at which they apply are not publicly disclosed. Similar to public

health plans, programs for all-inclusive care for the elderly and payers, private payers use drug formularies to manage beneficiary

others. However health insuring organizations, commercial prescription drug use and the cost of drugs paid for by the plan.

managed care organizations and Medicaid-only managed care Most formularies have copayment “tiers” that correspond to

organizations represented only 47% of this enrollee pool.17 different levels of beneficiary cost sharing. The placement of drugs

Under fee-for-service Medicaid, most states pay pharmacies within copayment tiers is related to their relative safety, efficacy,

directly for the drugs dispensed to Medicaid beneficiaries, using and effectiveness as determined by health plan or PBM pharmacy

a rate based on AWP or WAC for brand drugs and maximum and therapeutics (P & T) committees as well as their direct cost,

allowable cost (MAC, based on federal and state upper limits) including the price concessions that private payers can obtain

for multiple-source brand and generic drugs. Several states from drug manufacturers.21 It has been suggested that P & T

have implemented average Actual Acquisition Cost (AAC)-based committees refocus to address value-based reimbursement and

reimbursement as well.18 If the beneficiary is enrolled in a accountable care.22 Generic drugs are most commonly placed in

Medicaid managed care plan, the state may pay the Medicaid the lowest formulary copayment tier, although some formularies

managed care plan to cover pharmacy benefits for beneficiaries, list preferred generics on the lowest tier, and non-preferred

or the state may choose to “carve out” the pharmacy benefit generics on the second tier together with preferred brands. Private

and pay for it directly under fee-for-service administered by the payers negotiate drug payment rates with pharmacy providers;

state. Under managed Medicaid without carve-out, each MCO historically, these rates have been based on AWP or WAC, and

negotiates with drug manufacturers for rebates and discounts and include MAC pricing for most generic drugs.

manages its own drug formulary and network. Under carve-out, As in Medicare DRGs, private payers prefer to bundle payment

the state pays pharmacies for prescription drugs directly and for prescription drugs in DRG-based payments or in per-diem

manages a statewide formulary that may include a preferred drug rates for inpatient hospital, while hospital outpatient drugs are

list (PDL) and supplemental rebates as well as rebates mandated more commonly paid for separately if they exceed a specified cost

by federal statute. Beneficiaries who are eligible for both threshold. Drugs administered in physician offices and clinics are

Medicaid and Medicare (“Medi/Medi” or “dual eligibles”) receive usually paid separately based on AWP, WAC, or ASP.

prescription drug benefits through the Medicare Part D outpatient Pilot programs are underway in several commercial settings to

drug benefit. evaluate bundled payment mechanisms. A RAND Evidence-based

When pharmacy benefits are carved into Medicaid managed Practice Center study published in August 2012 by the Agency

care contracts, CMS requires states to collect drug utilization for Healthcare Research and Quality concluded in part: “There

data, for collection of statutory rebates from pharmaceutical is weak but consistent evidence that bundled payment programs

manufacturers. However, in a study conducted in Q2 2011, the have been effective in cost containment without major effects on

Academy of Managed Care Pharmacy | 10A M C P G u i d e t o P h a r mac e u t i ca l Pa y m e n t M e t h o d s , 2 0 1 3 U p d at e

Executive Summary

quality.”23 Private sector initiatives include, for example, United 3. Pharmacies receive payment from the health plan or PBM

Healthcare’s bundled payment pilot study in oncology.24 for the drugs dispensed to the plan members based on a

reimbursement formula agreed to by the payer (or agent)

nn How Products, Services, and and pharmacy. Physicians and other providers also negotiate

Payments Flow Through Channels of with health plans for payments for the drugs they administer

directly to beneficiaries. Drug payment may be bundled

Distribution (See Exhibit 1) in some channels (e.g., DRGs for hospital inpatient and,

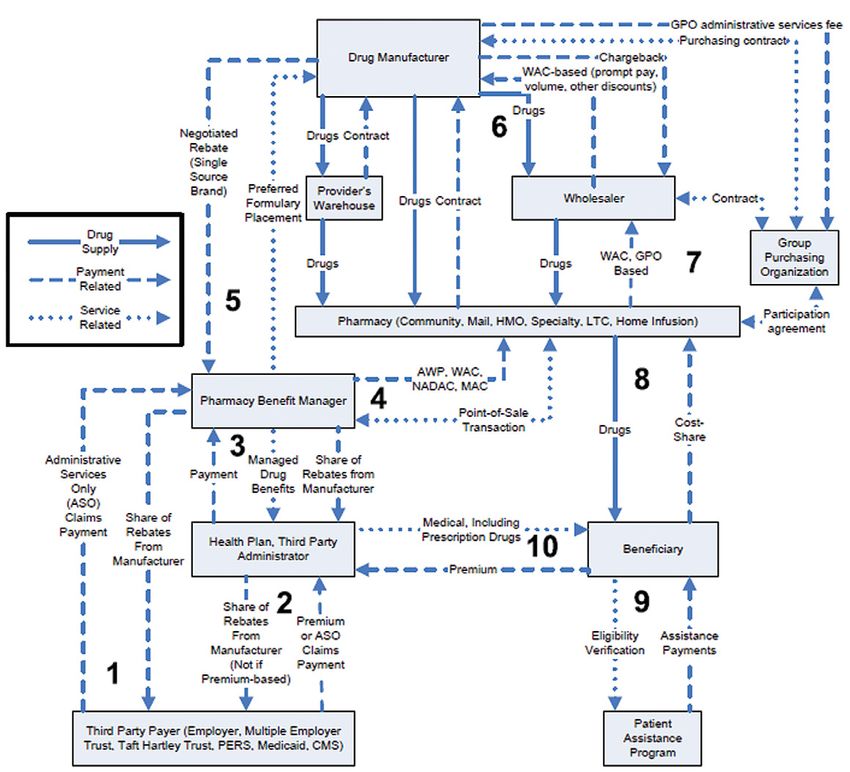

Any discussion of drug payment should consider the impact of depending on circumstances, APCs for hospital outpatient),

channel of pharmaceutical distribution (e.g., hospital, physician, or in other channels (e.g., pharmacy and physician office)

pharmacy) on both payment method and level. drugs may be paid on the basis of individual prescriptions

1. The majority of drug manufacturers ship drugs directly dispensed or administered.

to drug wholesalers or distributors, who then distribute 4. At the pharmacy counter or other point of sale, beneficiaries

the drugs to their end customers. Manufacturers enter with health insurance that includes prescription benefit

into various forms of contracting arrangements, including coverage will typically pay a cost-share to the pharmacy for

discounts and rebates, with all of the entities within the the prescription drug. The cost-sharing type (e.g., copayment

pharmaceutical supply chain. Manufacturers typically offer or coinsurance) and amount are set by the terms of that

different contracting arrangements, depending on customers’ health plan member’s benefit design. If the pharmacy plan

channel of distribution or class of trade, which may be is administered by a PBM, the PBM then bills the member’s

administered by wholesalers or distributors or directly with health plan or other payer an amount based on the payment

the manufacturers. formula stipulated in its provider service agreement, minus

2. Health plans and PBMs also negotiate with manufacturers the beneficiary cost-share amount collected by the pharmacy.

for discounts and rebates, primarily for single-source branded Individuals without health insurance or other coverage for the

pharmaceuticals in competitive therapeutic categories purchase of their prescription drugs or without the assistance

purchased for the individuals enrolled in their plans or under of negotiated pricing through a “discount card” program must

their management, based on volume, market share, and pay the pharmacy’s or other provider’s “usual and customary”

formulary placement. (U&C) price to obtain their drugs.

EXHIBIT 1. Drug Distribution Model

Academy of Managed Care Pharmacy | 11A M C P G u i d e t o P h a r mac e u t i ca l Pa y m e n t M e t h o d s , 2 0 1 3 U p d at e

Executive Summary

Recent Pharmaceutical Payment Milestones Disclosures

The timeline (Table 1) summarizes recent events affecting There was no external funding for this research. The contributors,

payment for prescription drugs and provides hyperlinks to obtain Howard Tag, JD, and Elan Rubinstein, PharmD, MPH,

further information. provide consulting services to clients that include professional

associations, health plans, purchasers, providers, pharmaceutical,

biological, and medical device manufacturers, and other health

care entities.

TABLE 1. Pharmaceutical Payment Milestones: 2005–2013

Date Description of Milestone Key References

January 1, 2005 Initiation of Average Sales Price CMS’s effort to establish a new http://www.gpo.gov/fdsys/pkg/

for Medicare Part B medications, payment benchmark for prescriptions PLAW-108publ173/pdf/PLAW-

as a result of the 2003 Medicare administered in physician office, 108publ173.pdf

Prescription Drug, Improvement, clinic and hospital outpatient

and Modernization Act (Public settings.

Law 108- 173).

January 1, 2006 Initiation of Medicare Part D, Competitive delivery model without Medicare Part D Benefit Designs and

administered by stand-alone centralized drug pricing, mandatory Formularies 2006-2009. J Hoadley,

PDPs and by MA-PDs with manufacturer rebates or community for MedPAC. 12/5/08 http://www.

prescription drugs and services pharmacy reimbursement guidelines. medpac.gov/transcripts/MedPAC%20

delivered primarily by community Formulary%20Presentation%20

pharmacies. -%20Hoadley%2012-05-08%20

revised.pdf

February 8, 2006 Deficit Reduction Act of 2005 CMS’s effort to establish a new Deficit Reduction Act of 2005:

establishes AMP as basis of payment benchmark for prescriptions Implications for Medicaid. 2/06.

Medicaid FUL calculation, and dispensed through pharmacy Kaiser Commission on Medicaid and

requires AMP to be publicly channels. the Uninsured. http://www.kff.org/

disclosed. medicaid/upload/7465.pdf

October 6, 2006 Wall Street Journal article First Databank increased the markup Martinez B. How quiet moves by

reporting on litigation revealed for of WAC to determine AWP for a large a publisher sway billions in drug

the first time that First Databank number of drugs in 2002 from 1.20 spending. Wall Street J. October 6,

took action in 2002 to increase to 1.25. 2006:A1. Available at: http://www.

the markup of AWP from WAC for AWP was not based on actual dc37.net/news/newsreleases/2006/

certain brand-name drugs. surveys of drug wholesaler prices. drugpricing_WallStJ.pdf

November 14, 2006 U.S. District Court for the District Public disclosure of disconnect Proposed Settlement by Judge Saris

of Massachusetts, Judge P. Saris, between AWP and actual market in CIVIL ACTION NO. 05-11148-

granted preliminary approval to a prices. PBS; New England Carpenters

settlement in class action re AWP Benefit Fund et al. vs. First

with First Databank Databank-McKesson. Available at:

http://www.prescriptionaccess.org/

docs/FDB-prelim-approval-order2.pdf

Continues.

Academy of Managed Care Pharmacy | 12A M C P G u i d e t o P h a r mac e u t i ca l Pa y m e n t M e t h o d s , 2 0 1 3 U p d at e

Executive Summary

TABLE 1. Pharmaceutical Payment Milestones: 2005–2013 (Continued)

Date Description of Milestone Key References

July 6, 2007 Deficit Reduction Act of 2005 Retail pharmacy class of Medicaid Drug Pricing Regulation.

definition of “retail pharmacy trade means any independent CMS Fact Sheet. 7/6/07. http://www.

class of trade” for AMP pharmacy, chain pharmacy, mail amcp.org/WorkArea/DownloadAsset.

calculation purposes, and of class order pharmacy, or other outlet aspx?id=11424 and Section

of trade to be included in the that purchases drugs from a 447.504, Determination of AMP.

AMP calculation. manufacturer, wholesaler, distributor, http://www.gpo.gov/fdsys/pkg/

or other licensed entity and CFR-2008-title42-vol4/pdf/CFR-

subsequently sells or provides the 2008-title42-vol4-sec447-504.

drugs to the general public. pdf and Retail Pharmacy class of

Sales, rebates, discounts, or other trade, Federal Register v72 #136,

price concessions included in AMP. 7/17/07.

Includes several non-retail pharmacy http://www.gpo.gov/fdsys/pkg/FR-

channels (see references). 2007-07-17/html/07-3356.htm

November 1, 2007 Judgments against two major Public disclosure of disconnect Memorandum and order by Judge

brand-name drug manufacturers between AWP and actual market Saris in: Re MDL 1456 and

for “grossly inflating” the AWPs prices with respect to particular Civil Action No. 01-12257-PBS.

of certain expensive physician- products; preceded by about 7 Available at: http://wexlerwallace.us/

administered drugs (PADs). years of allegations and settlements files/00079404.pdf

between several pharmaceutical

manufacturers and state and federal

prosecutors over inflating the

“spread” between AWP and actual

acquisition cost for physicians.

July 2008 Medicare Improvements for With a federal court injunction, http://www.gpo.gov/fdsys/pkg/

Patients and Providers Act of results in delay of (a) expansion PLAW-110publ275/pdf/PLAW-

2008 (MIPPA). of the number of drugs subject 110publ275.pdf

to the FUL amounts, (b) change

in the basis for the calculation

of FUL amounts to AMP, and (c)

requirement that CMS share AMP

data with states.

December 31, 2008 CMS’s Medicare Part B drug Postponed because of contractual http://www.cms.gov/Medicare/

Competitive Acquisition Program issues with successful bidder. Medicare-Fee-for-Service-Part-B-

(CAP) postponed as of December No official notice regarding if or Drugs/CompetitiveAcquisforBios/

31, 2008. when program may be restarted. index.html

Continues.

Academy of Managed Care Pharmacy | 13A M C P G u i d e t o P h a r mac e u t i ca l Pa y m e n t M e t h o d s , 2 0 1 3 U p d at e

Executive Summary

TABLE 1. Pharmaceutical Payment Milestones: 2005–2013 (Continued)

Date Description of Milestone Key References

January 2009 Hospital outpatient settings: For CY 2009, separate drug payment http://www.cms.gov/Regulations-and-

Payment for non-pass-through in hospital outpatient settings Guidance/Guidance/Transmittals/

drugs and biologicals in CY reduced to ASP + 4% for non-pass- downloads/R1702CP.pdf

2009 is made at a single rate through drugs and biologicals.

of ASP + 4%, which includes For CY 2009, pass-through drug

payment for both the acquisition payment continues at ASP + 6%.

cost and pharmacy overhead

costs associated with the drug or

biological. For pass-through drugs

and biologicals in CY 2009, a

single payment of ASP + 6%

is made to provide payment for

both the acquisition cost and

pharmacy overhead costs of these

pass-through items.

January 2009 The American Recovery and Objective is to increase research that Comparative Effectiveness. J Holzer,

Reinvestment Act of 2009 compares treatment modalities. G Anderson. Health Policy Monitor.

provides $1.1 billion funding The hope is that availability of CE 2009. Available at: http://hpm.

for comparative effectiveness research results will help care givers org/en/Surveys/Johns_Hopkins_

(CE) research through the make best possible therapeutic Bloomberg_School_of__Publ._H_-_

Agency for Healthcare Research choices. USA/13/Comparative_Effectiveness_

and Quality (AHRQ) and the Research.html

Council is precluded from making

National Institutes of Health

coverage or reimbursement

(NIH), and establishes the

decisions.

Federal Coordinating Council for

Comparative Effectiveness.

February 2009 OIG release of comparison Analysis of “average unit DHHS Office of Inspector

of community pharmacy reimbursement amount” including General. Comparing pharmacy

reimbursement amounts for dispensing fee with ingredient cost. reimbursement: Medicare Part D to

Medicare Part D plans versus Median 0.6% lower Part D Medicaid. Report no. OEI-03-07-

Medicaid in the second half of reimbursement for single-source 00350. February 2009. Available at:

2009 for 40 single-source drugs brand drugs. https://oig.hhs.gov/oei/reports/oei-03-

and 39 multiple-source drugs 07-00350.pdf

Medicaid reimbursement exceeded

with high expenditures.

Medicare Part D reimbursement by

10% or more for 28 of 39 multiple-

source drugs and was 17% higher

at the median for the 39 multiple-

source drugs.

Continues.

Academy of Managed Care Pharmacy | 14You can also read