PLS: Athabasca's Shallow Depth, Highly Awarded Uranium Project - Toronto April 15 - 16, 2019 - Fission Uranium Corp.

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Exploration Project

of the Year

PLS: Athabasca’s Shallow Depth,

Highly Awarded Uranium Project

Toronto

April 15 - 16, 2019

FissionUranium.com

1

Disclaimer

The following information may contain forward-looking statements. Forward-looking

statements address future events and conditions and therefore involve inherent risks

and uncertainties. Actual results may differ materially from those currently anticipated

in such statements.

The technical information in this corporate presentation has been prepared in

accordance with the Canadian regulatory requirements set out in National Instrument

43- 101 and reviewed on behalf of the company by Ross McElroy, P.Geol. President and

COO for Fission Uranium Corp., a qualified person.

The updated Mineral Resources as reported April 15, 2019 are as reported from data up

to and including 2018 drill programs, and are reported within an open pit design at a

cut-off grade of 0.15% U3O8 and 0.25% U3O8 for resources outside the pit that are

potentially mined by underground methods. The R1620E, R840W and R1515W zones are

evaluated as underground at this time.

TSX: FCU OTCQX: FCUUF 2

Technical Information

Certain of the technical information contained herein is derived from the April 15, 2019 news release entitled “[TBD],” describing results of a PFS completed on the project – a

copy of which is filed on the Company’s profile on SEDAR at www.sedar.com. The PFS considers the PLS project as a stand-alone mine and mill operation, which includes

development and extraction of the R00E and R780E zones (Triple R deposit), based on a number of inputs, estimates, and results including the following (all values in C$ unless otherwise

noted):

Mineral Resources and Mineral Reserves are reported within the open pit design at a pit discard cut-off grade of 0.15% U3O8 and outside the design at an underground cut-off grade of

0.25% U3O8 based on a long-term price of US$50 per lb U3O8 and PFS cost estimates. Mineral Resources that are not Mineral Reserves do not have demonstrated economic viability.

Physicals:

• Four years of pre-production and 8 years of mine life, processing nominally 1,000 tonnes per day (350,000 tonnes per year)

• Total Tonnes Processed: 2.89 million tonnes at 1.42% U3O8 average grade; open pit mining of 2.30 million tonnes at 1.62% U3O8

• Underground mining of 0.59 million tonnes at 0.63% U3O8

• Process recovery of 96.7%, supported by metallurgical testwork

• Production of 90.5 million lbs U3O8; an average of almost 15 million lbs U3O8 per year for 5 years, followed by a lower-production tail

Revenue:

• Long term uranium price of US$50 / lb U3O8

• Exchange rate of 0.75 US$ / C$1.00

• Gross revenue of $5.84 billion, less Saskatchewan gross revenue royalties of $423 million

• Net revenue of $5.41 billion

Operating Costs

• Average OPEX of $9.03/lb (US$6.77/lb) U3O8 over the life of mine

• Unit Operating Costs of $274 per tonne processed.

• Combined Mining $89 per tonne processed

• Processing: $115 per tonne processed

• Surface and G&A: $71 per tonne processed

• Operating cash flow of $4.62 billion

Capital Costs

• Pre-Production capital costs of $1.498 billion

• Dyke and Slurry Wall $371 million

• Open pit mining $44 million

• Process plant $241 million

• Tailings Facility $101 million

• Infrastructure $114 million

• Indirects & Owner’s Costs $376 million

• Contingency $250 million

• Sustaining capital costs of $137 million (includes all underground mine capital costs, and tailings dam lifts)

• Reclamation and closure cost of $77 million

• Cash flow from operations of $2.91 billion

TSX: FCU OTCQX: FCUUF 3

Electricity Demand +150% by 2035

Reactor

Builds at

452 Current Reactors

Operation 55 Under

Construction 151 Planned 355 Proposed

25 year high

RUSSIA: +22

CHINA: +136

EUROPE: +35

USA: +28

SAUDI ARABIA: +16

E. ASIA: +10

UAE: +10

INDIA: +28

More reactors operating in 2018 More Japanese reactors coming online Middle East (home of Big Oil) aggressively

than in any other time in history due to strong regulator support securing nuclear energy supply

TSX: FCU OTCQX: FCUUF 4

Moving Forward

Growing Electrical Demands and Nuclear Solutions

Electricity demand growing at rapid pace and increasingly

integrated into daily life

As demand for electricity increases, demand for clean energy is

paramount

EV’s entering the marketplace by major automobile

manufactures

Bitcoin POW mechanism annual electric consumption same as

Switzerland

Small Modular Reactors (SMR’s) – implementation is a game

changer Source: World Nuclear News

5

TSX: FCU OTCQX: FCUUF 5

Moving Forward

Small Modular Reactors (SMR’s)

Small Modular Reactors (SMR’s) – Game changing technology

Assembly line construction will standardize build and

reduce construction risk and decrease cost (analogous to

Ford’s Model T)

Shorter construction time (3 years as opposed to 10

years)

Transport modular components reduces major transport

requirements

Small footprint allows smaller safety zones around

reactors

Incremental power thus suitable for more countries,

more locations

Source: World Nuclear News

6

TSX: FCU OTCQX: FCUUF 6

Plans For New Reactors Worldwide

Source: https://pris.iaea.org/pris/

Reactors: Uranium Requirements & Future Nuclear Power

Source: WNA October 2018

452 Nuclear power reactors in 151 Nuclear power reactors

operation planned

55 Nuclear power reactors under 335 Nuclear power reactors

construction proposed

TSX: FCU OTCQX: FCUUF 7

China’s Strong Nuclear Buildout

China’s Reactor Construction Boom

2030 Estimate

150 reactors in operation* 240

33

50 under construction*

CGN, Fission’s Strategic Partner

19 operating reactors*

Important domestic and global builder

of reactors (23 new reactors under

construction world wide)*

Owns 19.9% of Fission

Offtake agreement - 20% of annual

uranium production from PLS; option to

purchase additional 15%

Beijing, China: Air Quality Red Alert *CGN Personal communication

TSX: FCU OTCQX: FCUUF 8

Japanese Recovery Continuing

2010 2016 2030

Nuclear 25% 2% 20-22%

“Our resource-poor country

cannot do without nuclear

power to secure the stability of

energy supply while considering

what makes economic sense and 9 reactors have currently 2 reactors under

the issue of climate change,” restarted construction

Shinzo Abe, re-elected Prime Minister of

Japan Oct. 2107 17 reactors currently in the 8 new reactors planned and

process of restart approval proposed

(Source: World Nuclear Association, February, 2019)

TSX: FCU OTCQX: FCUUF 9

Supply Side Vulnerable to Geopolitical Instabilities

Nearly 60% of primary supply comes from politically unstable countries

Saskatchewan, Canada:

Ranked #1 mining investment jurisdiction in 2017 by Fraser Institute

Increased share of global production from 17% to 22% in 2016

Other Countries

Australia 14.1%

Kazakhstan

10.2% (to reduce planned uranium

39%

production by 20%)

22%

Politically unstable

Permitting issues

Canada 13.8%

(indefinite suspensions at 7.9% Stable & supportive

McArthur River)

Africa Russia & E. Europe

All figures from Uranium Investing News (based on World Nuclear Association country reports)

TSX: FCU OTCQX: FCUUF 101B lbs U3O8 Uncovered in Next 8 Years and Supply Still Being Cut

Low U3O8 price impacts low cost producers

Kazakhstan production cut by 20% over three years starting in 2018

Production indefinitely suspended at McArthur River

Canadian operations shut down at Rabbit Lk and Eagle Pt

Production cuts at Cigar Lake

U3O8 M lb

250

Utilities are increasingly uncovered

200

150

100

50

0

2019 2020 2021 2022 2023 2024 2025

Uncovered US Utilities Uncovered Non-Us Utilities Covered

Source: UxC

TSX: FCU OTCQX: FCUUF 11Pressure is Growing for Return to Contracting

• Utilities buy high and

sell low

• Lack of long-term

contracting leaves

utilities exposed

• For contracting to

return, prices will

have to rise

• The longer the wait,

the stronger the

upwards pressure on

pricing

TSX: FCU OTCQX: FCUUF 12Stage Set for Higher Uranium Prices

Cameco CEO, Tim Gitzel, says today Cameco can buy uranium

on the market cheaper than they can produce it, which is what

they plan to do.

“…we’re going to reduce supply and we’re going to add to the

demand by going out to buy so that will bring better times

sooner rather than just continuing to produce into the market.”

Interview with Tim Gitzel and Country 600 CJWW / Saskatoon, SK, CA

UxC BAP TTM Chart

November 8, 2017 – Cameco

suspends production from

McArthur indefinitely. Will

purchase uranium to meet

delivery commitments.

Source: Data from the Ux Consulting Company, LLC http://www.uxc.com/, Haywood Securities

TSX: FCU OTCQX: FCUUF 13Building Shareholder Value Since 1996

Strathmore Minerals Corp (‘96) Energy Fuels

1996 – U3O8 spot at $7/lb Acquires Strathmore in 2013

$2M Mkt Cap to > $457M (‘07)

JV Sumitomo (Japan) ($50M)

Fission Energy Corp (‘07)

JV KEPCO (Korea) ($44M) Fission Uranium Corp (‘13)

J-Zone Discovery & Sale to Denison Takeover of Alpha Minerals

($85M) Triple R 43-101 Resource 87.76M

Indicated / 52.85M Inferred

PEA – OPEX $14.02/lb US

Fission 3.0 Corp (‘13)

CGN (Chinese Utility) buys 19.99%

Project Generator with several high- ($82M)

potential projects: drilling-boulders-

Fission 3.0 Spin-Out

geochem-geophysics-showings

Rhyolite to spend C$22M to earn-in

80% of Macusani Assets

TSX: FCU OTCQX: FCUUF 15Award Winning Project and Team

Dev Randhawa • Ross McElroy

Mining Person/s of the Year, 2013

TSX: FCU OTCQX: FCUUF 15Major Exploration Success and Strong Prospects

New Discoveries: Still Early Days

Large, High Grade, Shallow,

Open Pit

Project Backed by PFS

Leading Jurisdiction

TSX: FCU OTCQX: FCUUF 16Athabasca: The Premier High-Grade Uranium District

% U3O8

ENVIRONMENT

• Political stability

• Pro-mining

• Permitting

INFRASTRUCTURE

• Mills nearby

• Power Grid

• Highways & Air

EXPERIENCE

• 60+ years of mining

• Supplies 22% of the world’s uranium

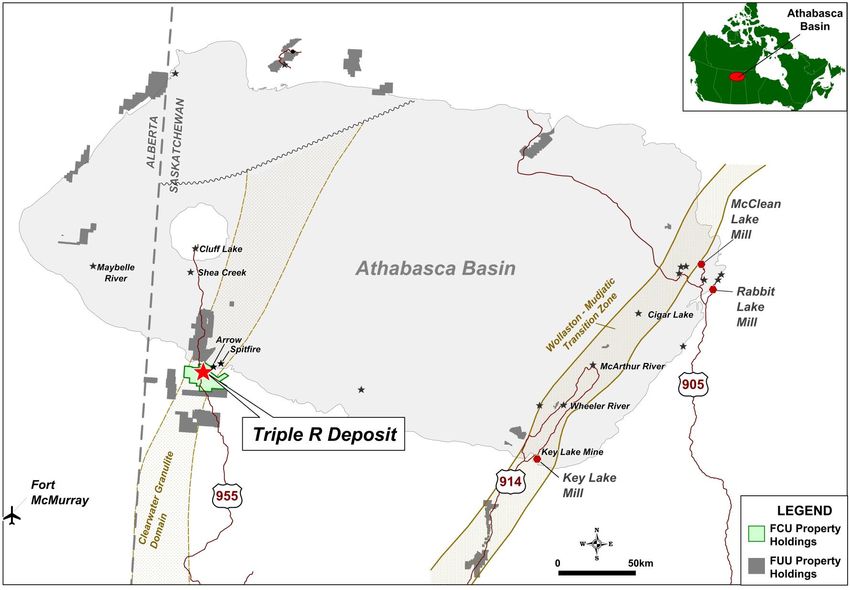

TSX: FCU OTCQX: FCUUF 18Canada’s Athabasca Basin District

TSX: FCU OTCQX: FCUUF 18Low Hanging Fruit Picked First

Triple R McArthur Arrow

Mined Out (FCU) Midwest River

Key Lake Phoenix

In production McClean Cigar Shea

Millennium

Cluff Lake Lake Roughrider Lake Creek

Undeveloped

Discoveries

100

Exploration 200

“Sweet-Spot”

300

400

500

600

700

800

900

McClean Lake Mine, Saskatchewan, Canada

TSX: FCU OTCQX: FCUUF 19PLS: Triple R Deposit & New Zones

“Total E-W strike length is now well beyond that of even Cigar Lake (1.95 km) or McArthur

River (1.70 km) – such a lateral extent to us underlines the magnitude of the strength of

the mineralizing system at PLS.”

Raymond James

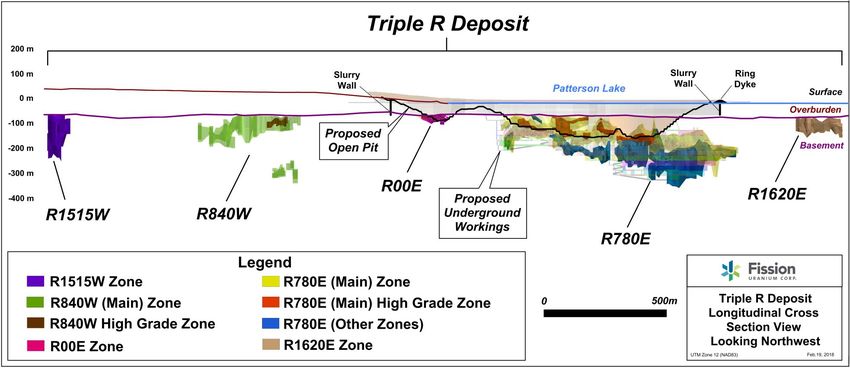

TSX: FCU OTCQX: FCUUF 20Triple R Deposit – 3.2km Mineralized Trend

W E

Triple R Deposit – Economic U3O8 Resources(1)

Indicated 103.7M lbs at 1.85% U3O8

Inferred 32.8M lbs at 1.20% U3O8

(1) Please see legal disclaimer on slides 2 and 3 of this presentation

TSX: FCU OTCQX: FCUUF 212019 Winter Drill Program – areas of work

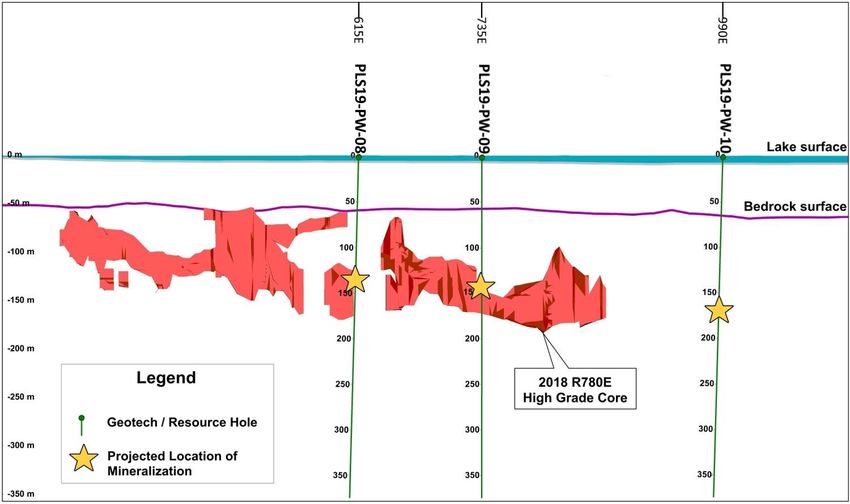

TSX: FCU OTCQX: FCUUF 22R780E Resource Expansion Drill Holes

TSX: FCU OTCQX: FCUUF 23Progressing Triple R Towards Production

Q1, 2018 Q3, 2018 Q2 2019 2020

Resource Update Summer PFS Work PFS Completed FS Complete

Zone Expansion Submit EA

R00E

R780E

Triple R Deposit – Resource Estimate (1)

Indicated 103.7M lbs at 1.85% U3O8

Inferred 32.8M lbs at 1.20% U3O8

(1) Please see legal disclaimer on slides 2 and 3 of this presentation

TSX: FCU OTCQX: FCUUF 24How the Triple R Measures Up: Base Case Economics

Average OPEX of US$6.77/lb U3O8 Rapid pay back (2 yr pre-tax) / 2.3 yr (post-tax)

Pre-tax NPV $1.32B (8% discount rate) Pre-tax Net Cash Flow over LOM of $2.9B, post-tax

$1.8B

IRR: Pre-tax 29%, post-tax 21%

Estimated CAPEX of $1.49B

18% Increase in Indicated Resource

from Feb 2018

Project OPEX (US$/lb U3O8) Owner/Operator

Triple R $6.77 Average OPEX(1) Fission Uranium

Kazakhstan Avg (ISL mining) $15.41 (2) Uranium One

Cigar Lake, Canada $15.70 (3) Cameco

McArthur River, Canada $16.34 (4) Cameco

Willow Creek, US (ISL mining) $33.85 (5) Uranium One

(1) Base case using US$50/lb U3O8 and an exchange rate of US$0.75:C$1.00

(2) Uranium One Inc., Audited Annual Consolidated Financial Statements For the years ended December 31, 2014 and 2013

(3) Cigar Lake Project NI 43-101 Technical Report, February 24, 2012

(4) McArthur River Operation NI 43-101 Technical Report, November 2, 2012

(5) Uranium One Inc., Audited Annual Consolidated Financial Statements For the years ended December 31, 2014 and 2013

TSX: FCU OTCQX: FCUUF 25PFS – Key Take Aways

Optionality

Potential to develop mine as combination open pit / underground or underground only

Low OPEX:

Base Case of US$6.77/lb U3O8

UG Only PEA Case of US$7.17/lb U3O8

CAPEX:

Base Case of C$1.49B (reflecting the Company’s conservative approach)

UG Only PEA Case of C$1.19B (lower CAPEX, less construction time, higher IRR)

Resource Growth

Increase in Indicated resource by 18% from February 2018

Resource Expansion:

Growth Opportunities to convert inferred to indicated resources

▪ R780E still open at depth and along plunge to east

▪ R1515W, R840W, R1620E zones mostly inferred and not included in the mine reserve

plan

TSX: FCU OTCQX: FCUUF 26PFS Base Case vs UG Only

OP/UG PFS Base

Item Units Case UG Only PEA Case

Construction Period Years 4 3

Mining Mt 2.89 2.55

% U3O8 1.42 1.64

Mine Life Years 8.2 7.3

Production M lbs U3O8 90.5 81.4

Operating Costs C$/t 274 335

C$/lb U3O8 9.03 9.57

Initial Capital Cost C$ M 1,498 1,194

Sustaining Capital Cost C$ M 137 258

Pre-Tax Cash Flow C$ M 2,910 2,587

After-Tax Cash Flow C$ M 1,759 1,533

After-Tax NPV @8% C$ M 693 696

After-Tax IRR % 21 26

TSX: FCU OTCQX: FCUUF 27How the Triple R Measures Up: Annual Production

2016

Mining Percent of

Position Project Location Production

Method Total

(M lbs U3O8)

1 McArthur River Canada UG 18.0 11%

2 Cigar Lake Canada UG 17.3 11%

Triple R

3 Katco Kazakhstan ISR 10.4 7%

4 Olympic Dam Australia UG 9.6 6%

5 Central Mining Uzbekistan ISR 6.2 4%

District

6 Inkai Kazakhstan ISR 5.7 4%

7 Somair Niger OP 5.6 4%

8 Karatau Kazakhstan ISR 5.4 3%

9 Ranger Australia OP 5.2 3%

10 South Inkai Kazakhstan ISR 5.1 3%

- Remaining - - 69.2 44%

Total 157.7 100%

Source: SNL Metals and Mining

>50% of global uranium supplied by 10 mines

Averaging +15M lbs per year in first 5 years, Triple R positioned to be one of the top

global producers and the largest open pit production

TSX: FCU OTCQX: FCUUF 28Moving Forward

Competitive Advantage

• Shallow, Large, High-Grade

• Optionality of Combination Open Pit / Underground or

Underground only

2019-2020 Goals

• Pre Feasibility Study completed April, 2019

• Advance UG to PFS (by July 2019)

• Continue towards Feasibility Study

Feasibility Study Work

• Grow by conversion to indicated from R780E, R00E (20

holes) and zones outside of PFS resource (40 holes)

• Permitting

• Feasibility level mine design, scheduling and cost

estimation

TSX: FCU OTCQX: FCUUF 29Corporate Information

Financial Summary Analyst Coverage

Market Cap: C$ 282 million Alex Pierce – BMO Capital Markets, London

(as at April 12, 2019)

David Talbot — Eight Capital, Toronto

Cash: C$ 15.0 million

(as at March 31, 2019) Colin Healey — Haywood Securities, Vancouver

Heiko Ihle — H. C. Wainwright & Co., New York

Shares outstanding: 486.0 million Tyron Breytenbach — Cormark Securities, Toronto

Options: 30.4 million

Fully diluted: 516.4 million

(as at Jan 31, 2019)

Board of Directors:

Executive Management Team: Advisory Board:

Dev Randhawa - Chairman

Dev Randhawa, MBA — CEO Ron Netolitzky

Ross McElroy

Ross McElroy, P.Geol. — President & Michael Halvorson

Frank Estergaard

COO Mark Wittrup

William Marsh

Chief Teddy Clark

Rob Chang

Darian Yip

Paul Ma

Deshao Chen

TSX: FCU OTCQX: FCUUF 30Fission’s Management Team

Dev Randhawa, Chairman & CEO Paul Charlish, CFO, Corporate Secretary

▪ Fission Energy founding CEO and chairman from 2007 to 2013 ▪ 30 years specialization in the mining sector

leading company to Tier One status ▪ Experience in mergers, acquisitions, spin outs and divestments

▪ Finance Monthly ‘Dealmaker of the Year 2013’, Northern for mining companies, including Fission Energy and Fission

Miner ‘Person of the Year 2013’ Uranium

▪ Founder of Pacific Asia China Energy, sold for $34M

Ray Ashley, VP Exploration

Ross McElroy, President and COO ▪ Professional geophysicist with 30+ years

▪ Formerly with Cameco, Areva, BHP Billiton ▪ Responsible for PLS field operations

▪ PDAC 2014 ‘Bill Dennis Award for Exploration Success’, ▪ Involved in several important discoveries including a key role

Northern Miner ‘Person of the Year 2013’ in the Ekati diamond mine discovery

▪ Significant role in 4 major uranium discoveries in Athabasca

Basin, incl. Fission’s Waterbury Lake & PLS

▪ Professional geologist of 30+ yrs exp

TSX: FCU OTCQX: FCUUF 31Fission Uranium Corp. Phone: +1 250 868 8140 Toll Free: +1 877 868 8140 (North America) Web: www.fissionuranium.com Investor Relations: Email: ir@fissionuranium.com

You can also read