Prospects for financial and Capital markets 1st quarter 2021 - Zurich, 04. January 2021

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Prospects for financial and

Capital markets

1st quarter 2021

Zurich, 04. January 2021

Foreword

The year 2020 was an eventful year that will the environment to remain challenging in the

be remembered by all. first quarter and to gradually improve from

the second quarter onwards, as vaccines are

At the beginning of 2020, the economic indi- not expected to have a sustained positive im-

cators still allowed for a cautiously optimistic pact until the second quarter of 2021. Until

economic assessment despite lower growth then, politicians will no doubt have to resort

expectations. At the time, we had identified a to familiar measures to control further flare-

number of risk factors for the economy, but ups in infection numbers. While most eco-

we had not anticipated a pandemic of this nomic forecasts do not expect significant in-

magnitude and the resulting consequences flation, we are currently assuming the rate will

for the global economy and society. The fis- be higher than expected. Furthermore, the

cal and monetary policy measures that fol- risk of a delayed wave of insolvencies does

lowed were extraordinary and far exceeded not seem to have been completely averted.

those of the financial crisis in terms of scope

and speed. Over the course of the year, fiscal We are rather optimistic for the equity mar-

policy continuously took over from monetary kets and expect returns above 5% for most re-

policy. Budget deficits reached unbelievably gions. We have taken into account the posi-

high levels in some countries and the total tive growth prospects for Asia by adding to

debt of households, companies and govern- this region and are currently slightly over-

ments has once again risen markedly. Central weight in the equity asset class. We remain

banks have increasingly had to place them- convinced of our overweight position in phys-

selves at the service of governments, which ical gold and think that our gold strategy is

raises questions about their independence. “spot-on”. Fixed-interest investments now of-

Interest rates are now firmly cemented at a fer virtually no return expectations. We prefer

record low, even in the US. inflation-linked bonds and focus on solid

credit quality. When selecting investments,

Financial markets have been characterised we stick to our guiding criteria of quality, li-

by exceptionally high volatility across all as- quidity and transparency.

set classes. Despite one of the most pro-

found economic downturns in recent history, Bank von Roll AG

equity markets quickly anticipated an eco- Bleicherweg 37

nomic recovery. The newly created money CH-8027 Zurich

further fuelled equity prices. The price of this

is a perceived disconnection from reality and

equity valuations last seen in the late 1990s.

Gold also performed very well during the year.

The economic estimates for the year 2021

are quite positive thanks to the record fast de-

velopment of vaccines. The Asian economies

in particular are likely to record the strongest

growth in the new year. Currently, we are as-

suming an economic development that is

slightly below consensus. We are expecting

Foreword 2

Strategic cornerstones - 2021

For the year 2021, our investment policy is guided by the following key points:

Overall, the economic outlook for the next 12 months has brightened considerably.

However, the pandemic remains a major factor of uncertainty and the vaccines will not

have a sustained positive effect until the second quarter of 2021. Due to this uncertain

Economy

forecast basis, we currently assume a positive economic development for 2021, how-

ever slightly below-consensus. We expect a persistently difficult environment in Q1 and

a gradual improvement from Q2 onwards. We expect the strongest growth in Asia. We

do not expect a return to the economic performance of 2019 for most regions in the

industrialised countries until 2022.

The focus in 2021 will continue to be on fiscal policy and thus debt is expected to con-

Monetary policy

tinue to rise. In our opinion, not too much should be expected from monetary policy in

2021. Monetary policy is likely to be supportive, reactive and asymmetric, but also in-

creasingly dirigiste. Interest rates are likely to remain at very low levels.

The inflation potential is enormous due to the ultra-expansive monetary policy and rec-

Inflation

ord high levels of debt. A pick-up in inflation will surprise the markets and the central

banks will accept an overshoot. Asset inflation is already in full swing. This could spill

over into the real economy.

We expect the following relative development of asset classes:

• Equities beat bonds

Markets

• Precious metals (gold and silver) and commodities beat bonds

• Equities, precious metals and commodities develop similarly

• Corporate bonds should perform slightly better than government bonds

Long-term drivers are intact and gold remains underrepresented in institutional investor

Gold

portfolios. Real interest rates should continue to fall and support the gold price. How-

ever, gold is one of the most volatile asset classes.

With the positive news on vaccines, we increased the equity allocation to slightly over-

weight during November. Equities remain more attractive than bonds. Should interest

Investment strategy

rates rise more than expected, the high equity valuations, especially in the US, could

turn-out to be a risk factor.

We remain convinced of our overweighting in gold. The price correction is likely to be

over.

Bonds offer hardly any earnings prospects. We remain underweighted, focusing on

solid credit quality and inflation-linked bonds.

We leave foreign currency risks at a relatively low level. Emerging market investments

in local currency are possible portfolio additions.

Strategic cornerstones - 2021 3

Strategic asset allocation

Balanced CHF

Asset Class

Liquidity 10%

Fixed Income 32%

Corporate Bonds BBB 17%

Inflation-Protected Government Bonds 15%

Highy Yield Bonds 0%

Equities 43%

Switzerland 11%

Europe 11%

USA 9%

Emerging Markets 5%

Gold Mines 7%

Precious Metals 15%

Currencies

CHF 80%

EUR 10%

USD 5%

Other Currencies 5%

in percent % 10 20 30 40 50 60 70 80 90 100

Our priorities for the year 2021

• We are rather optimistic for equity markets. The relative attractiveness to bonds is

given, which is why we are slightly overweight equities.

• The favoured regions are emerging markets and Asia, where demographics, rising con-

sumption, an expected weaker USD and technology/digitisation can provide increased

positive momentum.

• Depending on progress in the fight against the pandemic, the economies in the Euro-

pean periphery could also experience above-average development.

• The infrastructure sector, which is likely to be driven by fiscal p olicy measures, contin-

ues to look positive. These include: basic materials, industrial metals, mechanical engi-

neering and capital goods as well as energy and data infrastructure ("cybersecurity").

• We are maintaining our overweight in gold and gold mining stocks.

• In view of the low interest rates and the lack of tailwind from interest rate cuts, bonds

offer hardly any earnings prospects. Solid credit quality and inflation-linked bonds are

preferred.

Risk factors for the year 2021

• COVID-19 vaccines are not effective, vaccine uptake is very modest, or a new strain of

the virus emerges that reverses progress.

• Major social tensions in the USA, political assassination.

• Insolvency phase in the context of the pandemic crisis, intensification of the debt cri-

sis. Related to this, an accelerated loss of confidence in paper money.

• Food shortages, rising prices of agricultural goods, distribution struggles .

• Large-scale cyberattacks with negative consequences for the internet.

• Stronger than expected economic development leads to an unexpected and rapid rise

in interest rates, which brings down the highly valued asset classes.

Strategic asset allocation 4

Economic environment

Vaccines brighten the outlook

Covid-19 - Major challenges in the short term, vaccines sooner than expected

The pandemic continues to hold the world in its grip.

Sharp rise in case numbers pro-

While the summer months were rather quiet on the

vokes new measures. Develop-

Covid-19 front, new infections rose sharply again over

ment of effective vaccines is a

the course of autumn, particularly in Europe and the

success. Logistics and ac-

United States. Previous record numbers from the

ceptance as challenges. Sustaina-

spring, which were determined on a comparatively less

ble improvement only from 2nd

precise basis, have been exceeded by far. This develop-

quarter 2021 onwards.

ment – a second respectively in the US even a third

wave – was to be expected, but was surprising in its scope. In order to get back control of the

situation, various governments again took measures, including so-called “hard lock-downs".

These measures have had some effect, but have not yet materialized to be as successful as in

the spring. This brings with it the danger of even stronger political exertion of influence. Large

regions of Asia have so far been spared a significant second wave.

Source: European Centre for Disease Prevention and Control / own illustration

In November, substantial progress was finally made in the development of effective vaccines.

Scientists succeeded earlier than commonly anticipated. This is the final piece of the puzzle in

the COVID-19 measures and rounds off the massive assistance from fiscal and monetary policy

as well as the targeted lock-downs and testing of the general population. The number of coun-

tries that have licensed at least one vaccine and started vaccination is increasing daily.

The next milestone is to organise efficient logistics in order to produce the vaccines in the re-

quired quantities and distribute them as quickly as possible. Another issue that should not be

underestimated will be convincing the Corona-weary population of the benefits of vaccination.

It is to be expected that the vaccines will not have a lasting positive effect on the broad popula-

tion until the second quarter of 2021 and that governments will therefore have to fall back on

the known instruments for the time being. Thus – even if the infection rates decline again over

Economic environment 5

the course of December and January due to the hard measures taken – an additional wave must

be expected in the coming spring.

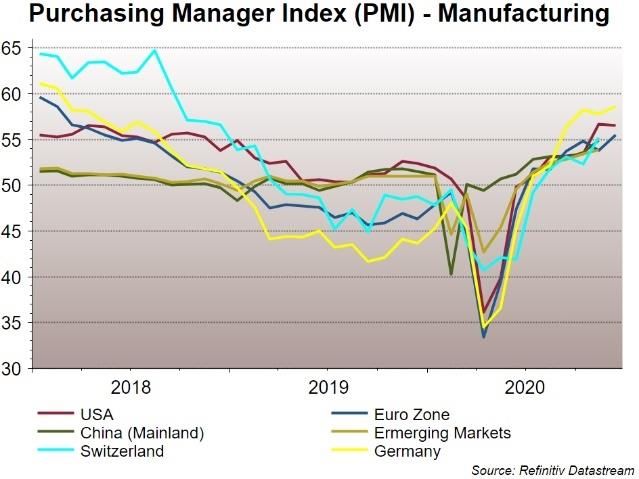

Economy - Impressive third quarter, challenging fourth quarter

In the third quarter, the various regions around the world

After strong growth in Q3, rising

recorded impressive growth. This has to be noted posi-

Covid-19 numbers weigh on the

tively after the deep fall in the first and second quarter.

services sector again. Impact on

The fourth quarter is again much more challenging. The

economy is limited. Availability of

economy as a whole seems to be able to come to terms

vaccines taken up positively. Nev-

with the changing situation and has become more flex-

ertheless, rather cautious outlook

ible. Nevertheless, the second (or third) COVID 19 wave

for 2021.

will again leave clear traces. Especially the regions and

countries heavily depending on tourism or the entertain-

ment and restaurant industry will have to cope with another quarter of negative growth. The

important purchasing managers indices (PMI) reflect the development described. The manu-

facturing sector continues to be quite positive in terms of both level and dynamics and is devel-

oping favourably in almost all regions of the world. There are clearer differences in the develop-

ment of the service sector, where the countries in the Eurozone in particular had to accept major

setbacks due to the pandemic situation mentioned above. In the course of the fourth quarter,

Brexit, which had been pushed into the background by the pandemic, be came a pressing issue

again. Finally, the parties were able to get their act together and reach a "deal" after more than

4 years since the Brexit decision, thus avoiding the worst-case scenario of a hard Brexit.

Source: Refinitiv / own illustration

Unemployment is still significantly above the pre-pandemic level, but differs regionally due to

varying labour market policies. With new measures against the pandemic and delayed effects,

for example due to short-time working, unemployment is likely to rise until the second quarter

of 2021.

Economic estimates for 2021 are generally quite positive. Growth is seen as above average,

especially in Asia, followed by Europe. Due to the vague forecast basis with many elements of

uncertainty and risk factors, we currently assume a slightly below-consensus positive economic

development for 2021. We expect a persistently difficult environment in Q1 and a gradual im-

provement from Q2 onwards. We also expect the strongest growth in Asia. The positive risk is

Economic environment 6

higher-than-expected growth driven by pent-up consumption, a boom in private investment fa-

cilitated by the availability of state-supported bank loans and non-negligible government invest-

ment programmes in the area of sustainability ("Green New Deal").

Monetary and Fiscal Policy - Ever Higher Debt, Ever Higher Money Supply

Governments have reacted to the negative economic ef-

Fiscal and monetary policy were

fects of the pandemic – like rising unemployment, loss

less active after the spectacular

of income, company shut-downs, etc. – with enormous

first semester. However, the econ-

rescue packages. Furthermore, far-reaching investment

omy can rely on continued sup-

programmes have been adopted in Europe and we ex-

port. Fiscal policy remains in fo-

pect similar steps for the USA under the new Biden ad-

cus.

ministration. The already sky-high national debts will

therefore continue to rise. The central banks are supporting the governments in their plans, so

that monetary and fiscal policy are increasingly merging and the independence of the central

banks must be seriously questioned. At the US-Fed, the focus has also clearly shifted from mon-

etary stability to achieving full employment. Relevant data suggest that the US-Fed has pur-

chased very large packages of new govern-

ment debt in the year 2020, while foreign

investors have made only small purchases

at this stage. Domestic investors even

made record sales in the first quarter, which

had to be absorbed by the US-Fed as well to

prevent the credit markets from freezing.

The US Fed's activities can certainly be de-

scribed as direct financing of additional

government debt. The US-Fed's balance

sheet has reached a staggering record vol-

Source: US Fed / own illustration

ume of USD 7,000 billion.

During the third and at the beginning of the fourth quarter, the central banks were staying at the

sideline, observing the development of the pandemic and economic situation. They then be-

came somewhat more active again in line with the rising infection figures. Thus, at the Decem-

ber meeting, the European Central Bank (ECB) was the first of the major central banks to adjust

the various monetary policy programmes to the significantly riskier economic environment. It is

striking that once again no changes were made to the negative key interest rates. The central

banks seem to be aware of the unfavourable effects of negative interest rates. The US-Fed com-

municated very similarly in its December meeting, but without making any significant adjust-

ments to its policy. The US-Fed is also in conflict with the US Treasury over the return of money

for unused rescue programmes. After some back and forth, the US government and parliament

seem to be able to agree on a new USD 900 billion package at the end of December.

Economic environment 7

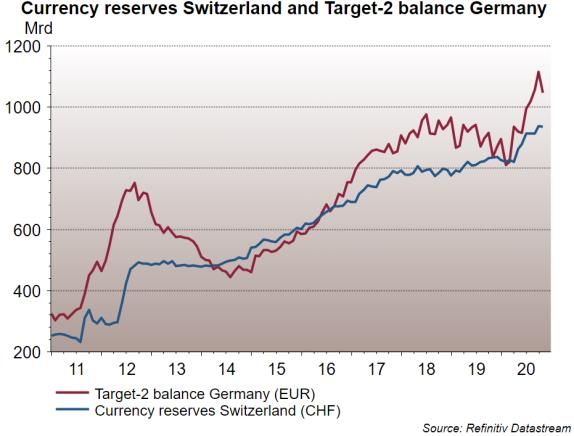

In Switzerland, the Swiss National Bank's for-

eign currency reserves attract a lot of attention.

They again rose strongly over the course of the

year. The development of the so-called Tar-

get2-balance of the German Bundesbank

shows an almost identical picture. Both statis-

tics are an expression of the same problem: if

one cannot (Germany) or does not want (Swit-

zerland) to let the exchange rate rise as a bal-

ancing instrument, the balance must be

achieved in some another form. In December,

Switzerland was added to the list of currency

manipulators defined by the US-Treasury. This decision did not come as a huge surprise. How-

ever, we do not expect any significant consequences from this decision.

The focus in 2021 will continue to be on fiscal policy and thus rising debt is to be expected. In

our view, not too much should be expected from monetary policy in 2021. Monetary policy is

likely to be supportive, reactive and asymmetric, but also increasingly dirigiste. Substantial ad-

ditional intervention and an even more expansionary monetary policy will only be implemented

in response to major market turbulence, especially in the credit markets. However, we do not

expect a shift to a restrictive monetary policy for a long time. The economy would have to send

clear signals that it is self-sustaining or inflation would have to rise well above the 2% target.

Consequently, interest rates should remain at very low levels for the time being. But, as the

example of Japan shows, central banks will not hesitate to use appropriate means to influence

the interest rate landscape in order to ensure the sustainability of government debt.

Financial and capital markets

Volatile fourth quarter

Financial and capital markets – elections in the USA and vaccines bring additional boost

The fourth quarter was a mirror for the development of

High volatility in the fourth quarter

the whole year. Hope and reality determine the opinions

with a price explosion in equities

of market participants while switching from one to the

in November. Lagging regions and

other. Liquidity spills into the markets and leaves them

sectors benefited. Safe havens

just as quickly. Performance is often made in a very

underperformed.

short time, only to remain in a sideways market after-

wards. One could also speak of "Covid-on" and "Covid-

off" markets. After a search for orientation from August to the end of October, November was a

pronounced "Covid-off" month with very significant price gains in risk assets. The outcome of

the US-elections and news on vaccines gave a boost to the markets. The previous winners,

which tend to have the character of safe havens, such as gold, the USD or technology stocks,

suffered from this development.

Financial and capital markets 8

Fixed Income

The general phenomenon of very low interest rates did not change much in the fourth quarter.

If one digs a little deeper, however, he can see interesting developments. In the USA, the yield

curve has steepened, mainly due to higher interest rates in the medium and long maturities (over

3 years). Since expected inflation de-

rived from inflation-protected bond

prices increased during the same pe-

riod, the higher interest rates must be

an expression of concerns about ris-

ing inflation in the USD area. For the

EUR, the yield curve also steepened

slightly, but distinctively differently.

Interest rates fell across all maturi-

ties, but most strongly at the so-

called short-end. This must be inter-

preted as a rather negative signal Source: Refinitiv / Own representation

against the background of the pan-

demic development and the higher risk of another quarter of negative growth. Interest rates in

China increased across all maturities and the yield curve normalised, signalling an overall

healthy economy. Switzerland's yield curve followed that of the Euro-area in a weakened form.

Credit spreads continued to narrow and are now only slightly above the lows seen in the year

2018. This led to a slight increase in the price of corporate bonds in the fourth quarter, while

long-dated government bonds from the USA fell quite significantly in price as a result of the

above described change in the yield curve. Inflation-linked bonds also showed a slightly positive

performance.

For 2021, we expect only minor changes in interest rates. Interest rates will remain cemented

at a very low level. If there are any interest rate hikes, they will tend to be at the long end due to

better-than-expected growth and/or rising inflation expectations. In combination with slightly

rising inflation figures, further falling real interest rates should also result in 2021. In corporate

bonds, credit spreads play an important role. We see a slight widening, although the develop-

ment is likely to differ strongly among the

sectors. Particularly in pandemic-prone sec-

tors from tourism or strongly consumption-

dependent segments, there could be a

stronger widening of credit risk premiums,

especially in the course of the first quarter.

Overall, it should be difficult to generate rea-

sonable returns with bonds in the year 2021.

Corporate bonds are likely to outperform

government bonds and inflation-linked

bonds belong in well-diversified portfolios, in

our view.

Financial and capital markets 9Equities

The stock markets were trapped in a stubborn and, as expected, volatile sideways market from

August to the end of October. Rising infection figures and the outlook for a very tight race for

the US presidency kept many investors from making new commitments. In November, the pic-

ture turned clearly positive

within only a number of days.

Markets were relieved that the

US elections produced a fairly

clear result and that the so-

called "blue wave" did not ma-

terialise for the time being.

Shortly afterwards, news of

progress on vaccines provided

an additional boost. Even more

liquidity flooded into the equity

markets. The best performers Source: Refinitiv / Own representation

during this phase were the re-

gions and sectors that had previously lagged behind. Some stocks achieved even gains in the

mid-double-digit range during this short time-span. There was also a pronounced sector rotation

from growth to cyclical value stocks.

Recently, the heavy momentum in stock issues in the USA has also been striking. "SPAC" is the

acronym of the hour and stands for "Special Purpose Acquisition Company". SPACs are not a

fundamentally new invention. What is new, however, is the extent to which these vehicles are

being used. Some of the new issues made in this way achieved spectacular increases in value

on the first day of trading. The picture may therefore be strongly reminiscent of the "wild" years

of the dot-com market at the end of the 1990s. So far,

SPAC "Special Purpose Acquisi-

the phenomenon has been limited mainly to the US-

tion Vehicle" is a publicly traded

market and companies from the "hot" segments of elec-

shell company whose purpose is

tromobility and social media. Critics say that hedge

to acquire a private company

funds in particular are cashing in on their private equity

within a limited period of time.

investments this way.

Over the course of December, the rising Covid-19 infection numbers and the clearly overbought

market situation weighed on the markets again, but did not lead to a correction, only to a side-

ways movement. The hope for additional rescue packages and support measures from fiscal

and monetary policy, the relief of a Brexit-deal as well as the view of expected growth in the

course of 2021 supported the markets despite some warning signals from the area of market

sentiment indicators.

Overall, we are rather optimistic about equity markets for the year 2021 and see returns of more

than 5%, with Switzerland and Europe expected to slightly underperform. In terms of corporate

earnings expectations, analysts assume the strongest growth in the cyclical consumer, basic

materials, industrials and information technology sectors, while earnings in the defensive utili-

ties, healthcare, real estate and non-cyclical consumer sectors could underperform. Energy is

Financial and capital markets 10in the middle of the pack. The favoured regions are emerging markets and Asia, where de-

mographics, rising consumption, an expected weaker USD and technology/digitisation may pro-

vide increased positive momentum. One can also find some lagging equity markets in this re-

gion (for example India or Indonesia). Depending on progress in the fight against the pandemic,

the tourism-heavy economies in the European periphery could also experience an above -aver-

age development. The entire infrastructure sector, which is likely to be driven by fiscal policy

measures, continues to be viewed positively by us. Sectors benefiting from this include basic

materials, industrial metals, mechanical engineering and capital goods, as well as the entire

theme around energy and data ("cybersecurity") infrastructure. There is no doubt, that valua-

tions must be viewed as challenging. This will be a drag and could even manifest itself as a

significant risk factor if interest rates do rise more significantly.

Precious metals and raw materials

Commodity prices recovered strongly during

the fourth quarter. The energy complex per-

formed best, followed by industrial metals and

food. As was the case throughout the year, the

cyclically sensitive copper performed very

strongly, benefiting from additional demand

from the battery sector and the switch to elec-

tromobility. But even platinum, which under-

performed for a long time, was given new life.

Overall, a rather optimistic economic scenario

and higher inflation expectations can be de-

rived from the development of commodities.

This development has carried over to the stock performance of commodity companies.

The precious metals – gold and silver – entered a sideways market in the course of August.

Gold experienced a correction of around 15% after exceeding the USD 2,000 per ounce mark.

We had expected a so-called retest of the previous highs from the year 2012 in the area of USD

1820 after the break-out. The somewhat

more difficult market phase was caused by a

significant decline in investment demand, so

the same factor that had previously helped

driving prices higher. Precious metals – and

the related gold mining stocks – are still

among the best performing asset classes for

the year 2020, despite this recent healthy cor-

rection. In our view, the above described re-

test was successfully confirmed by the latest

positive price movement in gold, which

should provide a basis for further advances.

The fundamental price drivers such as the exorbitant increase in debt and money supply, the

outlook for further declines in real interest rates and a potential loss of confidence in paper

money remain.

Financial and capital markets 11Gold should be able to profit from rising inflation and thus further falling real interest rates in

the year 2021. But even in the environment of a possible debt crisis, gold should be sought after

as a credit-free financial asset. We remain invested in gold with a healthy overweight. Silver

appears even more attractive due to its stronger industrial use. Commodities should perform

with an appreciation of over 5% over the next year. For the oil price (Brent), we see a trading

range of USD 45-55.

Currencies

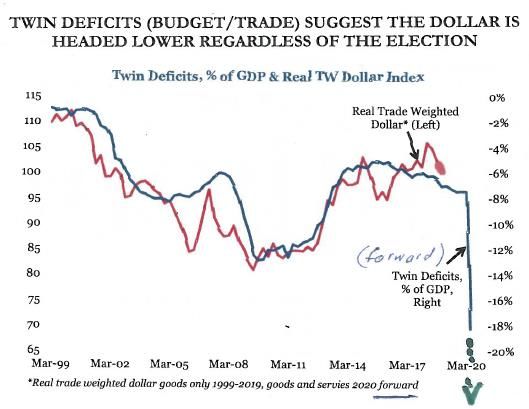

The weak USD continues to be the topic of intense discussions on the currency markets. The

USD-index, which measures the USD against a basket of various foreign currencies, seems to

have broken the upward trend that has lasted since the end of the financial crisis. We had ex-

pected this development, as the US twin deficit

in particular argues against a strengthening

USD. The outcome of the US-elections has led

to further weakness, as larger programmes

can be expected under a Biden administration.

If the re-election of two senators in the state of

Georgia on 5.1.2021 goes in favour of the Dem-

ocrats, the Senate majority would finally tip and

the "blue wave" would become reality. Further-

more, US investors seem to be increasingly

looking again at foreign stock markets, as they

are often cheaper than the US home market,

have catch-up potential and currency gains are possible. These investments are likely to be

made without hedging foreign currencies, putting additional pressure on the USD. The EUR re-

cently benefited from lower risk aversion and tended to strengthen against the USD. The CHF

moved sideways against the EUR and thus also tended to strengthen against the USD. The AUD

should also be mentioned positively, as it was able to resist even the strength of the EUR. Un-

doubtedly among the winners was Bitcoin,

which more than doubled in the fourth quar-

ter. The acceptance of this most important

of the cryptocurrencies among investors is

growing. The lively interest meets a still

comparatively low supply. However, the

price movements must still be character-

ised as strongly herd-driven and oriented to-

wards simple marks (for example USD

20,000). However, the success of Bitcoin is

probably based on the same reasons as is

applicable for gold. Bitcoin is a child of the

financial crisis, when people started to think more deeply about trust in paper currencies.

Currency forecasts in the market (source: Refinitiv) point to higher prices of the more cyclical

currencies (EUR, SEK) and lower quotes of the "safe-haven" currencies (USD, CHF) in the year

2021. We assume most currencies will trade around current levels. We see a range of 0.87-0.92

Financial and capital markets 12for the USD to CHF, 1.07-1.09 for the EUR to CHF and 1.19-1.25 for the USD to EUR. We are

positive on emerging market currencies.

Graphics and tables

Key economic expectations for the year 2021

Source: IMF, ECB, US Fed, KOF, own estimates

Graphics and tables 13Global debt as % of GDP Inflation

Spending and tax reliefs Loans and guarantees

Source: Blackrock

US Dollar

Record new issuance of US-government

debt (purchased by central bank)

Outstanding US-treasureies: change vs previous year in bn USD

Gold

Graphics and tables 14Equities

Market capitalization of global equities. As high 25 largest US-growth stock/US-GDP, largest

as in January 2018 (in million USD) extreme of all times.

Source: cnn.com

Graphics and tables 15Market Overview 2020

So urce: Reuters per 31.12.2020 / Equity M arkets in lo cal currency

Economic Indicators per Close Close prev. Year YTD

University o f M ichigan Co nsumer Sentiment Index 30.09.2020 79.0 99.3 -20.3

ISM M anufacturing P M I SA 30.11.2020 57.5 47.8 9.7

ISM No n-M anufacturing NM I 30.11.2020 55.9 54.9 1.0

US Leading Indicato r Index 30.11.2020 109.1 111.4 -2.3

ZEW Euro zo ne Expectatio n o f Eco no mic Gro wth 31.12.2020 54.4 11.2 43.2

Ifo P an Germany B usiness Climate 31.12.2020 92.8 92.4 0.4

S&P Co reLo gic Case-Shiller 20-City Co mp. Ho me P rice NSA Index

31.10.2020 235.8 218.7 17.1

Currency vs. CHF per Close Close prev. Year YTD

EUR 31.12.2020 1.0807 1.0852 -0.4%

USD 31.12.2020 0.8851 0.9678 -8.5%

GB P 31.12.2020 1.2102 1.2828 -5.7%

SEK 31.12.2020 10.7400 10.3300 +4.0%

JP Y 31.12.2020 0.8571 0.8908 -3.8%

A UD 31.12.2020 0.6806 0.6789 +0.3%

Currency vs. EUR YTD

USD 31.12.2020 1.2217 1.1215 +8.9%

CHF 31.12.2020 0.9251 0.9217 +0.4%

GB P 31.12.2020 1.1189 1.1829 -5.4%

SEK 31.12.2020 0.0995 0.0953 +4.4%

JP Y 31.12.2020 0.7926 0.8208 -3.4%

A UD 31.12.2020 0.6298 0.6261 +0.6%

Equity Markets in local currency per Close Close prev. Year YTD

M SCI Wo rld Index (USD) 31.12.2020 2’ 690.0 2’ 358.5 +14.1%

M SCI Emerging M arkets Index (USD) 31.12.2020 1’ 291.3 1’ 114.7 +15.8%

Do w Jo nes (USD) 31.12.2020 30’ 606.5 28’ 538.4 +7.2%

S&P 500 (USD) 31.12.2020 3’ 756.1 3’ 230.8 +16.3%

Nasdaq Co mpo site (USD) 31.12.2020 12’ 888.3 8’ 972.6 +43.6%

Russell 3000 (USD) 31.12.2020 2’ 248.4 1’ 892.2 +18.8%

B razil B OVESP A (B RL) 30.12.2020 119’ 017.2 118’ 573.1 +0.4%

DA X (EUR) 30.12.2020 13’ 718.8 13’ 385.9 +2.5%

Euro Sto xx50 (EUR) 31.12.2020 3’ 552.6 3’ 745.2 -5.1%

IB EX 35 (EUR) 31.12.2020 8’ 073.7 9’ 549.2 -15.5%

SP I (CHF) 30.12.2020 13’ 327.9 12’ 938.7 +3.0%

SM I (CHF) 30.12.2020 10’ 703.5 10’ 699.8 +0.0%

FTSE (GB P ) 31.12.2020 6’ 460.5 7’ 542.4 -14.3%

RTS (USD) 31.12.2020 1’ 427.1 1’ 564.2 -8.8%

Nikkei 225 (JP Y) 31.12.2020 27’ 258.4 23’ 204.9 +17.5%

China Shanghai Co mp. (CYN) 31.12.2020 3’ 473.1 3’ 050.1 +13.9%

India B SE 30 (INR) 31.12.2020 47’ 751.3 41’ 253.7 +15.8%

A ustralia S&P /A SX200 (A UD) 31.12.2020 6’ 587.1 6’ 684.1 -1.5%

Interest Rates and Bond Markets per Close Close prev. Year YTD

3-M o nth Euribo r 31.12.2020 -0.55% -0.38% -0.16%

10-Years Germany Generic Go vernment 31.12.2020 -0.58% -0.19% -0.39%

10-Years EUR Swap 31.12.2020 -0.27% 0.21% -0.48%

3-M o nth ICE USD-Libo r 31.12.2020 0.24% 1.91% -1.67%

10-Years US Generic Go vernment 31.12.2020 0.91% 1.91% -1.00%

10-Years USD Swap 31.12.2020 0.92% 1.87% -0.95%

3-M o nth ICE CHF-Libo r 31.12.2020 -0.76% -0.69% -0.08%

10-Years Switzerland Generic Go vernment 31.12.2020 -0.49% -0.56% 0.08%

10-Years CHF Swap 31.12.2020 -0.29% -0.12% -0.17%

IB OXX Euro Go vernment 3-5 Jahre 31.12.2020 212.5 209.7 +1.3%

REX P erfo rmance Index (German Go vernment B o nds) 30.12.2020 499.2 492.6 +1.4%

IB OXX Euro Co rpo rates 3-5 Jahre 31.12.2020 244.2 237.7 +2.7%

Swiss B o nd Index A A A -B B B 31.12.2020 144.5 144.2 +0.2%

Emerging M arkets Hard Currency in USD (ETF) 31.12.2020 115.9 114.6 +1.2%

Emerging M arkets Lo cal Currency in USD (ETF) 31.12.2020 45.3 43.9 +3.1%

CS High Yield Index II 31.12.2020 1’ 498.4 1’ 411.4 +6.2%

Alternative Investments per Close Close prev. Year YTD

VIX-Index (Vo latility S&P 500) 31.12.2020 22.8 13.8 +65.1%

RICI Co mmo dity Index (To tal Return, USD) 31.12.2020 178.3 196.6 -9.3%

Go ld in USD/Oz 31.12.2020 1’ 896.5 1’ 517.0 +25.0%

Go ld in CHF/kg 31.12.2020 1’ 680.0 1’ 468.2 +14.4%

Go ld in EUR/Oz 31.12.2020 1’ 553.7 1’ 352.8 +14.8%

Silver in USD/Oz 31.12.2020 26.4 17.8 +47.8%

Crude Oil B rent USD (Future) 31.12.2020 51.8 66.0 -21.5%

Co pper (Future) 31.12.2020 351.4 279.4 +25.8%

B altic Dry Index 24.12.2020 1’ 366.0 976.0 +40.0%

HFRX Glo bal Hedge Fund Index (USD) 30.12.2020 1’ 377.9 1’ 292.5 +6.6%

LP X50 (P rivate Equity) 31.12.2020 2’ 913.0 2’ 870.7 +1.5%

Market 16You can also read