PUBLIC EXPENDITURE REVIEW: GOVERNMENT PENSION OBLIGATIONS AND CONTINGENT LIABILITIES

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

PUBLIC EXPENDITURE REVIEW:

GOVERNMENT PENSION OBLIGATIONS

AND CONTINGENT LIABILITIES

Policy Note

November 2014

This note is a technical document of the World Bank produced as part of the PER and does

not represent an official position of the World Bank or of its Executive Board.Government pension obligations and contingent liabilities under base case, parametric reform and merger scenarios

(Net Present Value as % of 2013 GDP)*

All funds NSSF PPF PSPF** LAPF GEPF

Base case (no reform) 48.5% 5.7% 0.0% 41.8% 1.0% 0.0%

Harmonization rules 25.1% 0.6% 7.5% 17.1% 0.0% 0.0%

Harmonization rules-partial 19.7% 0.6% 7.5% 11.6% 0.0% 0.0%

Harmonization rules-all 18.6% 0.6% 7.5% 10.5% 0.0% 0.0%

Merger 15.9% 5.2% 10.7%

Merger + cost saving 12.4% 2.6% 9.8%

* Assuming interest rate equal to inflation and using 5% real discount

rate.

** Assuming PSPF does not finance pre99

pensions.

Harmonization Rules = parameters apply to all members NSS/ PPF/ GEPF but only to new members of PSPF/ LAPF

Harmonization Rules – partial = new reference salary applied to all members of PSPF/ LAPF

Harmonization Rules – all = all new parameters applied to all members of PSPF/ LAPF

Financial position of pension funds under base-case and reform scenarios

PSPF

NSSF PPF LAPF GEPF

excluding pre99 including pre99

Pensions at retirement, full/reduced*

Base case (no reform) 47%/40% 75%/37% 75%/37% 42%/31% (DB) 66%/33% 67%/50%

Harmonization rules 44%/33% 75%/37% 75%/37% 47%/35% (DB) 66%/33% 67%/50%

Harmonization rules-partial 62%/31% 62%/31% 55%/28%

Harmonization rules-all 58%/43% 58%/43% 52%/39%

Break-even point**

Base case (no reform) 2052 2024 2015 after 2080 2063 2072

Harmonization rules 2068 2022 2015 2036 2076 2072

Harmonization rules-partial 2028 2015 2077

Harmonization rules-all 2068 2065 2077

Assets depletion point***

Base case (no reform) 2061 2031 2019 after 2080 2072 after 2080

Harmonization rules 2077 2028 2019 2045 after 2080 after 2080

Harmonization rules-partial 2036 2021 after 2080

Harmonization rules-all 2075 2067 after 2080

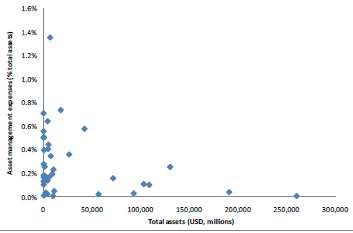

* Percentage of individual's last wage for an average male retiree in respective fund: retiring at average retirement age with average years of contributions, retiring in around 2035

** Year when the annual current balance turns negative assuming interest rate equal to inflation

*** Year when own assets are depleted and government needs to step in to cover deficits, assuming interest rate equal to inflation

2I. Current status

1. This report examines the current and future pension liabilities of the Government of

Tanzania. The report considers both the direct pension obligations which lie with the government

and the contingent liabilities for the pension system as a whole which the government holds

through its obligation to ensure pension benefits are paid, even if the pension funds themselves

do not have the resources to do so. Long term financial projections were produced using the

Pension Reform Options Simulation Toolkit (PROST) for five mainland pension funds: NSSF,

PSPF, PPF, LAPF and GEPF, based on data provided by each funds.1 Details of the model can

be found in Annex 3 and 4.

2. The study compares the financial sustainability of the pension funds and future

government obligations to finance the pension system using the parameters outlined in the

Harmonization Rules which were passed in July 2014. The modelling in this report contains

different scenarios demonstrating how the impact of the reforms on the contingent liabilities of

the government changes according to how the new parameters are applied.

Membership

Table 1. Base Year (FY2013) data on Pension System Members

All funds NSSF PSPF PPF-DB** PPF-DAS** LAPF GEPF

Contributors

Number*, thous. persons 997.3 421.8 315.3 110.9 21.5 95.0 32.7

Average age 38.3 38.2 39.9 36.5 35.3 37.6 34.6

Average annual wage, thous. TSH 7,096 6,427 7,047 11,097 9,330 6,006 4,336

Old age pensioners with regular pensions

Number*, thous. persons 69.0 5.9 33.2 25.2 - 4.7 -

Average age 62.6 65.2 61.6 63.2 - 62.5 -

Average annual pension, thous. TSH 1,970 1,929 2,343 1,593 - 1,401 -

Average annual pension, % of average wage in respective

fund 28% 30% 33% 14% - 23% -

System dependency rate (number of beneficiaries

devided by number of contribotors) 8.1% 1.9% 13.2% 23.3% n/a 5.6% n/a

*Average number during the year

**Number of active contributors for PPF was derived from data on contributions due in 2013, compliance rate and wages of contributors

contributors as % of working age population

Source: Data provided by respective pension funds

3. Table 1 outlines the current membership profile of the different pension funds. As of

2013, there were approximately 1 million active members contributing to five mainland funds, of

which about 75% are covered by the two biggest funds – NSSF and PSPF. This accounts for only

about 4.5 of the labour force or 2% of the population as a whole, meaning that the system is

fragmented and coverage rate is very low.

1

Despite some issues (which will be discussed directly with the funds), sufficient data was obtained to conduct the

modelling. Further improvements in the funds management information (MIS) systems to improve data quality are

recommended.

34. The number of pensioners is relatively low, mainly because most of the funds were set up

fairly recently (all funds, except PPF were converted to PAYG DB between 1999 and 2013).2

As a result, the system dependency ratios (the number of pensioners divided by the number of

contributors) are low – about 7% on average, though this does vary significantly from as little as

1% in NSSF to over 22% in PPF depending on the degree of scheme maturity. This means

currently the financial burden on each contributor is low. However, as the system matures, this

ratio will grow fast.

5. It is interesting to note how the introduction of competition for new members has affected

the funds in the last few years. Since the PROST modelling was last conducted in 2010 (using

2008 data), 3 overall membership of the funds has increased by 25%. However, the LAPF has

increased its membership by over 50% during this period. The average age of membership has

also changed across the funds – declining by around a year on average, but by more than 5 years

in the case of the LAPF and actually rising by 5 years at the PSPF. The biggest impact is

therefore on the LAPF where the financial position of the fund has been transformed by

acquiring a larger base of younger members (previous modelling showed the fund running into

financial difficulty around 2020s with the new membership base now keeping the fund in

balance for several more decades).

6. The current modelling reflects faster increase in membership over the short-term for the

funds which are currently growing most, and then assumes that the membership across all funds

remains stable as a percentage of the labour force over the long-term. This conservative

assumption is used as achieving an extension of pension coverage is not easy, though coverage

will likely rise to some extent as GDP per capita levels increase.

Benefits and Financing

Table 2. Base Year (Y2013) data on Pension System Finances, millions TSH

All funds NSSF PSPF PPF LAPF* GEPF

Contributions 1,347,720 476,410 444,853 275,015 114,143 37,300

Benefit payments, total 957,645 228,049 543,712 131,971 44,751 9,162

- pension benefits** 943,501 220,454 543,344 127,094 43,447 9,162

- non-pension benefits 14,143 7,595 368 4,877 1,303

non-pension benefits as % of total benefits 1.5% 3.3% 0.1% 3.7% 2.9% 0.0%

Administrative expenses 180,897 86,253 26,097 39,994 21,687 6,866

Administrative expenses as % contributions 13% 18% 6% 15% 19% 18%

Assets, beginning of the year 4,709,170 1,970,636 953,021 1,091,500 539,601 154,411

*LAPF 2013 estimated by WB team as 2012/2013 annual report was not available

**GEPF excluding voluntary benefits

Source: Data provided by respective pension funds

7. The level of the current benefits varies, from moderate levels at the NSSF and PPF,4 to

relatively generous parameters for the PSPF and LAPF. However, commutation5 in all funds and

2

This means that these are partially funded schemes.

3

See World Bank Policy Note, ‘Options for the Reform of the Tanzania Pension System’, December 2010

4

This is partially due to the high levels of withdrawals in the funds, which leads to shorter periods of contributions.

4lack of indexation in some of them result in relatively low regular post-retirement pensions

(about 40% of final salary on average).

8. Mainly due to low system dependency rates, the contribution rate (20% in all funds,

including now GEPF) is currently sufficient to cover benefit payments, so all systems are

partially funded and presently run surpluses. PSPF is a special issue because of pre-1999 pension

rights.

5

Commutation in the pension context occurs where a retiree surrenders part of his or her rights to receive a pension

in the form of a future income stream in exchange for receiving an immediate lump sum payment.

5Table 3. Main parameters of the current pension system in Tanzania

Provision NSSF PSPF PPF LAPF GEPF Harmonization

(2013 Act) Rules 2014

Type of scheme PAYG DB; converted PAYG DB; PAYG DB (PPS) PAYG DB; PAYG DB Applies to DB funds

from a provident fund converted from a and funded DC converted from a (converted from a

in 1998 non-contributory (DAS) provident fund in funded DC starting

DB scheme in 2005 from July 2014)

1999

Membership - Private sector Central - Parastatals - Local - Government Will apply to:

(formal and self- government - Companies with government employees - New members

employed) (pensionable Government’s - Open to others - Open to others of all funds

- Government positions) shares - Existing

employees and - Private sector members of

other not covered (formal and self- NSSF, PPF,

by any pension fund employed) GEPF (not

LAPF, PSPF)

Contributions 10%/10% 5%/15% - 5%/15% - 5%/15% (local 10%/10% Not set in regulation

(employee/employer) (parastatals) government)

- 10%/10% - 10%/10%

(private sector) (private sector)

Types of benefits - Old age (retirement) - Old age Traditional Pension - Old age - Old age - Old age

- Invalidity (retirement) Scheme (PPS): (retirement) (retirement) - Others according

- Survivorship - Invalidity - Old age - Invalidity - Invalidity to their own

- Medical (insurance) - Survivorship (retirement) - Survivorship - Survivorship enabling

- Funeral grant - Withdrawal - Invalidity - Funeral grant legislation

- Maternity - Survivorship - Maternity,

- Withdrawal - Withdrawal marriage, other

Deposit unemployment

Administration - Withdrawal

Scheme (DAS):

- Defined

contribution

scheme (lump

sum)

Retirement age 60; min 55 (0.5p.p. 60; min 55 ( with 60; min 55 ( with 60; min 55 ( with 60 60; min 55 (with

repl. rate reduction no reduction) no reduction) no reduction) 0.3% reduction)

per year prior to age

60)

6Provision NSSF PSPF PPF LAPF GEPF Harmonization

(2013 Act) Rules 2014

Vesting period 15 15 10 15 15 15

Annual accrual rate 2% for first 15 years 2.22% 2.0% 2.22% 2.07% 2.07%

plus 1.5% for each

year above 15

Maximum 67.5% No maximum 66.7% No maximum No maximum No maximum

replacement rate

Minimum pension6 80,000 TSH 21,000 TSH 50,000 TSH No minimum No minimum 40% of sector

minimum wage

Income measure Best 5 year average of Final salary Best 5 year average Final salary Last 3 year average Best 3 year average

last 10 years (not (not valorized) (not valorized) of last 10 years (not

valorized) valorized)

Commutation/ 24 x Monthly income 50% of regular 25% of regular 50% of regular 25%; at 1:12.5 25% of annual full

Initial lump sum measure pension; at 1: pension; at 1: 12.5 pension; at 1: 15.5 amount of pension;

15.5 at 1: 12.5

Indexation Follow Ad hoc No indexation No indexation Assumed prices Ad hoc

recommendations indexation

from actuarial financed by

evaluation reports government

6

The current minimum pension paid by the NSSF constitutes approximately 15% of the average wage of members of the fund. For the PSPF the minimum pension

is less than 4% of the average wage,and less around 5% for PPF.

7II. Impact of Reform on Benefits

9. The reform scenarios for the pension funds are based on the new benefit formula outlined

in the Harmonization Rules which apply to all the existing social security funds from 1st July

2014. The main parameters include:

Annual accrual rate=2.07% (1/580 monthly) – this is the percentage of each year’s salary

an individual earns as a pension;

Income measure= last 3 year average wage, not valorized – this is salary which the

pension is based upon;

Commutation: maximum commuted portion =25%, commutation factor=12.57 - this is

the amount of pension which can be taken as a lump sum.

10. As can be seen in Table 3, the impact of the new parameters is different across the funds:

the new accrual rate is higher than the existing at the PPF, lower than the PSFP and

LAPF rate, and works out around the same for the NSSF (GEPF is already in line with

the Harmonization Rules);

the reference salary is higher for the PPF and NSSF and lower for the PSPF and LAPF;

the commutation rules are stricter for the PSPF and LAPF (PPF and GEPF are already in

line whereas in the current NSSF there is no commutation).

11. Given the impact of the new parameters, the Harmonization Rules state that they should

be applied to the different funds in the following ways:

GEFP/ PPF/ NSSF: parameters apply to all members of the funds;

PSPF/ LAPF: parameters apply only to new members of the funds.

12. The World Bank team understand that the application of these and other parameters

outlined in the Harmonization Rules is still under discussion. In addition, the Rules, as currently

stated, can be interpreted as applying at least some of the parametric changes to all members of

all funds. The World Bank pension team therefore modelled the following scenarios to show the

impact of applying the parameters in different ways.

13. Table 4 shows the impact of the reforms under the following different scenarios. There

are of course other possible applications of the Harmonization Rules (e.g. apply to certain

members over a certain age etc.). The scenarios chosen are presented by way of ‘extremes’.

7

Commutation rate (factor) defines the relationship between the lump sum payment received and the future income

stream foregone. A rate of 10:1 means that a person commuting would receive $10 now for every $1 of future

annual income foregone. An actuary normally calculates the commutation rate using life expectancy tables to reflect

the life expectancy of the person wishing to commute. The rate of 12.5 applied in the Harmonization Rules is

broadly actuarially fair – though this could change in future if longevity increases significantly.

8 Harmonization Rules = parameters apply to all members NSSF/ PPF/ GEPF but only to new

members of PSPF/ LAPF

Harmonization Rules – partial = new reference salary applied to all members of PSPF/ LAPF

Harmonization Rules – all = all new parameters applied to all members of PSPF/ LAPF

14. The table shows the level of benefits which would be received from the different funds,

measured as a percentage of final salary for an average male member of each fund. The first

figure is the replacement rate a member would receive if the full benefit is taken as a pension.

The second figure is the amount of pension income which would be received if the individual

opts to take a much as possible as a lump.

Table 4. Summary indicators under base case and reform scenarios

PSPF

NSSF PPF LAPF GEPF

excluding pre99 including pre99

Pensions at retirement, full/reduced*

Base case (no reform) 47%/40% 75%/37% 75%/37% 42%/31% (DB) 66%/33% 67%/50%

Harmonization rules 44%/33% 75%/37% 75%/37% 47%/35% (DB) 66%/33% 67%/50%

Harmonization rules-partial 62%/31% 62%/31% 55%/28%

Harmonization rules-all 58%/43% 58%/43% 52%/39%

Break-even point**

Base case (no reform) 2052 2024 2015 after 2080 2063 2072

Harmonization rules 2068 2022 2015 2036 2076 2072

Harmonization rules-partial 2028 2015 2077

Harmonization rules-all 2068 2065 2077

Assets depletion point***

Base case (no reform) 2061 2031 2019 after 2080 2072 after 2080

Harmonization rules 2077 2028 2019 2045 after 2080 after 2080

Harmonization rules-partial 2036 2021 after 2080

Harmonization rules-all 2075 2067 after 2080

* Percentage of individual's last wage for an average male retiree in respective fund: retiring at average retirement age with average years of contributions, retiring in around 2035

** Year when the annual current balance turns negative assuming interest rate equal to inflation

*** Year when own assets are depleted and government needs to step in to cover deficits, assuming interest rate equal to inflation

15. As noted above, the Harmonization Rules impact the funds in different ways. However, it

should be noted that even after the reforms the replacement rates (at least on a pre-lump sum

basis) which the funds can be expected to deliver are still reasonably high. This is even more the

case if the replacement rate is measured against the average wage of members of the fund (PSPF

and GEPF then delivering close to a 100% replacement rate, the PPF and LAPF around 70% and

the NSSF about 50%- as shown in Table 4a).

Table 4a. Pensions at retirement as percentage of average wage of contributors in respective fund

PSPF

NSSF PPF LAPF GEPF

excluding pre99 including pre99

Pensions at retirement, full/reduced

Base case (no reform) 52%/45% 108%/54% 108%/54% 65%/49% (DB) 86%/43% 95%/72%

Harmonization rules 48%/36% 108%/54% 108%/54% 73%/55% (DB) 86%/43% 95%/72%

Harmonization rules-partial 92%/46% 92%/46% 71%/35%

Harmonization rules-all 85%/64% 85%/64% 68%/51%

9PSPF

16. The table above shows the impact of reforms on existing members of the fund. If the

Harmonization Rules are strictly applied, existing members of the fund will have no reduction in

benefits are they are grandfathered and the old rules will continue to apply. New members, by

contrast, will receive over 20% less benefit under the new rules. This is on a pre-commutation

basis – the pension received after commutation actually rises as the lump allowed is significantly

smaller. However, if, for example, at least the revised reference salary were applied to all

members of the fund (which the Harmonized Rules could be interpreted to allow), existing

members would see a 17% decline in benefit levels.

LAPF

17. The impact of reform on benefits at retirement is very similar to PSPF. 20% lower

benefits at retirement before lump sum apply to new member (higher pension benefits because of

smaller lump sum portion), with existing members grandfathered. However, differently from

PSPF where post-retirement pensions are already indexed, LAPF pensioners will benefit from

the reform as indexation of their pensions will be introduced.

GEPF

18. The GEPF was previously a provident fund (paying only lump sum and not pensions),

and more of a savings account than a retirement vehicle (with membership limited to only a few

years on average, before individuals changed from their temporary employment contract and

transferred into one of the other social security funds).The GEPF Act was already altered in 2013

and largely reflects the parameters in the Harmonization Rules and therefore the impact of

reform is limited.

PPF

19. The Harmonization Rules are more generous than the existing parameters of the PPF.

Therefore, benefits of new pensioners after taking the lump sum will increase by 12% to around

47% of average wage after the reform. The replacement rates of existing pensioners will also

grow higher – assuming 100% inflation indexation of pensions in payment. The removal of the

maximum replacement rate will also raise the pension for around 5% of members (only this

number serve for a long enough period to see their replacement rate go beyond the current

ceiling).

NSSF

20. The impact of the new parameters is on balance neutral to the NSSF. Given the average

service period of 22 years, the previous average accrual rate for pension benefits was around

1.8%. However, members also received a lump sum pay-out (separate from any commutation of

benefits) of 2 years of service. This made the effective accrual rate around 2.12%, slightly above

the 2.07% in the Harmonization Guidelines. The reforms will therefore serve to reduce the

effective accrual rate, which improves the financial balance of the fund. However, this

improvement will be offset by an increase in the salary base (best 3 as opposed to best 5 years)

meaning that the pre commutation benefits in the reform scenario are little changed. Unlike the

10other funds, regular pensions (after lump sum) will be lower compared to the base case scenario

as new retirees will get more at retirement as a lump sum but less as regular post-retirement

income. In addition, post-retirement pensions will be affected by less generous indexation if this

is changed from wages to inflation (as assumed in the modelling).

III. Government Liabilities

21. The government’s actual pension payments, made out of the general budget, are limited

to PSPF and LAPF pensioners who retired before these pension funds were established and some

military pensioners. Total payments amount to TZS 213 billion in 2013/2014, consisting of

pension payments of TZS 74 billion made to around 59,000 civilian and military pensioners, plus

TZS 139 billion lump sum payments made to retiring military personnel. In addition the

government currently finances the indexation of all PSPF pensions. This amounted to TZS 21.7

billion in 2013.8

22. The government’s liabilities with respect to NSSF, PPF, LAPF and GEPF are limited to

deficit financing once funds’ own assets have been depleted. In other words, once the funds have

a negative cash flow (having to pay out more in benefits than they receive in contributions) and

have sold all their assets to cover the gap, the government would have to step in and pay

promised pension benefits to retiring members of the fund. As shown in Table 6, these funds are

largely financially sound over the few decades but would require some government support in

the longer run.

23. The Harmonization Rules have a potential for a positive effect on the finances of all

funds (even when only applied to new members of the PSPF and LAPF), except PPF where the

new benefit formula will be more expensive. Overall the reforms reduce government direct

obligations and contingent liabilities from TZS 23.5 trillion (present value of government

obligations from 2013-2080) to TZS 12.3 trillion, or from 48% to between 25% of 2013 GDP.

Around 11% of these savings come from parametric changes imposed by the Harmonization

Rules (even if only applied to new members of the PSPF and LAPF). The rest comes from the

change in funding of indexation of PSPF pensions (which is assumed to move from the

government to the fund once the new Rules are applied).

24. By way of illustration, if the Harmonization Rules were also applied to existing members

of the PSPF and LAPF, the contingent liability would reduce to less than 20% of GDP.

8

Members of the PSPF receive two pension payments – the standard pension which covers nominal pension benefits

and an additional pension which covers indexation. The indexed, additional pension is paid by the government from

the Consolidated Account. The PSPF acts as the payment agent for the government. Unlike the pre-1999 liabilities,

the government has been paying the PSPF for making these transfers on its behalf under an agreement signed in

2006, and the fund does not suffer any arrears relating to these payments. Since the Harmonization Rules have been

applied, the PSPF will now take on the payment on of these additional, indexed pensions themselves.

11Table 5. Government obligations and contingent liabilities under base case and reform scenario

(net present value as % of 2013 GDP)*

All funds NSSF PPF PSPF** LAPF GEPF

Base case (no reform) 48.5% 5.7% 0.0% 41.8% 1.0% 0.0%

Harmonization rules 25.1% 0.6% 7.5% 17.1% 0.0% 0.0%

Harmonization rules-partial 19.7% 0.6% 7.5% 11.6% 0.0% 0.0%

Harmonization rules-all 18.6% 0.6% 7.5% 10.5% 0.0% 0.0%

* Assuming interest rate equal to inflation and using 5% real discount rate.

** Assuming PSPF does not finance pre99 pensions.

***Pre-99 pensions and indexation

Figure 1+2. Annual Government Obligations, % of GDP

Base case Harmonization Rules

1.0% 1.0%

0.9% 0.9%

0.8% 0.8%

0.7% 0.7%

0.6% 0.6%

0.5% 0.5%

0.4% 0.4%

0.3% 0.3%

0.2% 0.2%

0.1% 0.1%

0.0% 0.0%

PSPFtotal NSSF LAPF PPF GEPF PSPF NSSF LAPF PPF GEPF

PPF: the change to the Harmonization Rules has the biggest effect on the PPF. The impact of

the higher benefits on the system finances will be negative, shifting the break-even point,

when benefits are larger than contributions, from the end of the projection period to 2036,

and the asset depletion point (by when all assets will have been sold to cover the cash flow

gap) forward to 2045 . In addition to benefits being 12% more generous, the PPF is assumed

to move to full price indexing, which has a major impact on the financing of the fund. A

combination of further parametric change and / or a merger between funds will be necessary

to ensure the financial position of the fund over the long-run. The deterioration in the fund’

financial position means that the PPF goes from not representing any contingent liability to

the government, to being around one-third of the total contingent liabilities under the new

Harmonization Rules.

NSSF: in the short term expenditures increase because of larger lump sum payments at

retirement, in the longer run this effect is outweighed by lower post-retirement benefits.

Overall, financial position of NSSF improves with the break-even point and the depletion

point moving back by about 16 years, keeping the fund financially sustainable over the

longer term. The NSSF moves in the opposite direction to the PPF, going from representing

5.7% contingent liability to the government to effectively zero.

12 LAFP: the impact of the Harmonization Rules is to improve the financial position of the

fund over the long-run as benefits are reduced. However, much of this reduction will be

offset by the introduction of indexation. Given the fund is in a healthy financial position to

start with (due to the improved demographics), applying the rules to new or existing

members has limited impact. The LAPF barely registers as a contingent liability for the

government over the projection period.

GEPF: the combination of growing dependency ratio and decreasing benefits of existing

pensioners will result in a small deficit of current balance in the long run. The deficit will not

deplete fund’s assets until after 2070, so there will effectively be no government obligations

for the whole duration of simulation period.

PSPF

25. The biggest impact on government liabilities remains the PSPF. Whilst the government’s

liabilities to the other funds is limited to deficit financing once their own assets have been

depleted, with respect to PSPF the government’s liability covers the following:

1) Pre99 portion of pensions of government employees retired after July 2004 (arrears and

future payments);

2) Indexation of the pre and post99 portion of pensions of government employees retired

in/after July 2004 (assumed price indexation);

3) Financing PSPF deficits (assuming PSPF finances only post-1999 portion of pensions

received by government employees retired after July 2004).

Table 6. Government obligations to PSPF and contingent liabilities under base case and reform

scenario (net present value as % of 2013 GDP)*

Base case (no reform) Harmonization rules Harmonization rules- Harmonization rules-

partial all

Pre99 pensions, excluding indexation 9.9% 9.9% 8.9% 7.5%

Indexation of pre- and post-99 pensions 15.1% 1.9% 1.7% 2.0%

PSPF deficits 16.8% 5.3% 1.1% 1.0%

Total 41.8% 17.1% 11.6% 10.5%

26. Similar to LAPF, the overall long term impact of reform on PSPF finances is positive,

though in the short run it will be negative if the new parameters are only applied to new members

This is due to the shift of pension indexation financing from the government to PSPF itself. In

terms of indexation, in the current system PSPF is the only pension fund where indexation of

post-retirement pensions is financed from the state budget. In all other funds indexation policy

and its financing is the responsibility of the respective fund. In the reform scenario it is assumed

that indexation policy is harmonized as well and all funds, including PSPF, are responsible for

financing their own indexation.

27. An improvement in the fund’s position in the short-run can only occur if at least some of

the new parameters are applied to all members, especially if that includes the new commutation

rules which mean the fund would have to pay out smaller amounts in the short-term, when they

are facing financial difficulties.

1328. In addition to reducing benefits, the stabilization of the PSPF has to come from the

government increasing its recompense to the fund for payments made on its behalf for liabilities

accrued by members before 1999 when the fund was established.

29. In terms of the pre-1999 liabilities, the base case estimates the net present value of the

liabilities from 2013 to 2080 to be TZS 4.8 trillion. This includes TZS1.5 trillion of pre-1999

liabilities already paid on behalf of the government by the PSPF between 2004-2014, (the net

amount of these arrears standing at TZS 1.4 trillion as the government has paid TZS 160 billion

to the fund).9 The PV of the future pre-1999 liabilities coming due is estimated at TZS 3.3

trillion. Annual payments of pre-1999 deficits currently amount to TZS 300 billion, and are

rising as more members with these benefits retire. The peak will come in 2027 and the last

cohorts with pre99 pension rights are projected to retire by around the end of 2030s. As older

cohorts of pensioners are replaced with pensioners retiring with fewer and fewer pre-1999 years,

pre-1999 pension payments decrease and will essentially phase out by around 2055.

Figure 3. PSPF: projected pre-1999 liabilities (TZS million)

Annual payments of pre-99 pensions by PSPF on behalf of

Government, TZS mln (nominal values)

600,000

500,000

400,000

300,000

200,000

100,000

0

Base, Harmonization Harmonization-partial Harmonization-all

9

The MOF wrote to the PSPF in March 2013 committing to cover the TSZ 716.6 billion arrears (as estimated by

the independent actuarial review commissioned by the BOT in 2010) in installments of TZS 71.6 billion over 10

years starting from FY2012. To date only TSZ 160 billion out of the promised TZS 395 scheduled payments

between FY11-FY15 has been received by the PSPF, making net arrears of TZS 1.4 trillion.

14Table 7. PSPF: projected annual payments of pre99 pensions in 2013-2022, mln TZS

2013 2014 2015 2016 2017 2018 2019 2020 2021 2022 2023 2024 2025 2026 2027 2028 2029 2030

Base case (no reform) 215 272 300 328 356 383 408 431 453 474 494 511 525 534 538 535 525 504

Harmonization rules 215 272 300 328 356 383 408 431 453 474 494 511 525 534 538 535 525 504

Harmonization rules-partial 215 272 252 278 303 326 348 368 387 404 420 434 445 453 456 453 444 427

Harmonization rules-all 215 272 138 161 183 205 227 249 270 290 310 329 346 361 373 382 387 387

30. The reforms only reduce the pre1999 liabilities if at least some new parameters are

applied to all members of the fund. If all new parameters were applied to existing members of

the fund (scenario 3 – Harmonization all), the pre1999 liabilities could be reduced by TZS 1.2

billion, or 25%. If only the new reference salary were applied to existing members (scenario 2 –

Harmonization partial) the reduction is TZS 500 million or 10%. In the case of applying all new

rules only to new members, the pre-1999 obligations remain the same.

Table 8. PSPF: projected pre99 pensions in 2013-2080, net present value

% of 2013 GDP TSH bln

Base case (no reform) 9.9% 4,773

Harmonization rules 9.9% 4,773

Harmonization rules-partial 8.9% 4,283

Harmonization rules-all 7.5% 3,627

31. Whatever scenario is applied, the PSPF remains the issue for the government well into

the future (the contingent liabilities for the other funds only kick in from 2060 onwards). Some

combination of increased government cash injections and parametric reform will be needed to

stabilize the PSPF. If this does not happen the fund will shortly be unable to pay promised

benefits. The fund has been paying out more in benefits than it receives in contributions since

2013, with investment income no longer able to cover the gap from this FY2015. Unless the

government is to step in with further payments, the PSPF will have to conduct a fire sale of its

assets, and /or risks only being able to pay reduced benefits. Similar situations in other countries

have led to public protests, which can undermine confidence in the pension system as a whole,

and potentially have an impact on overall savings rates.

Other Issues

Discount Factor

32. As with any present value modelling, the results in this analysis are highly sensitive to the

discount factor used. The rate of 5% real is in line with other assumptions and modelling used by

World Bank economists. However, if the discount factor were reduced by 1% to 4% the overall

government liabilities would be over 40% higher. Such sensitivity needs to be taken into account

when interpreting the findings from this report.

Indexation

33. The Harmonization Rules state that indexation of benefits should be done on an ad hoc

basis following an actuarial valuation. As it is not possible to estimate what this will mean in

practice, for simplicity the scenarios assume this will be close to price indexation, which is

15therefore applied to all funds. Price indexation is the minimum recommended by the World Bank

as in the long-run it maintains the real value of pensions, whilst at the same containing costs.

Compared to the base case, where current practice regarding indexation is applied, indexation of

benefits at the NSSF will be slightly less generous (moving from wage to price indexation),

LAPF and PPF benefits are more generous (as no or very minimum indexation is currently

applied to benefits) and PSPF and GEPF remain the same. The breakeven scenarios of the funds

are of course sensitive to the indexation assumption.

Minimum Pension

34. The Harmonization Rules apply a minimum pension to all funds, based on 40% of the

minimum sector wage. As the Rules have only been in place since the 1st July this year, the funds

are as yet uncertain as to how this will impact their benefit levels and financial position. For

example, the NSSF believes that the 40% minimum sector wage could in some case actually be

below the TZS 80,000 a month they currently guarantee, though they do not envisage reducing

their minimum pension level. On the other hand, the 40% minimum sector wage could actually

be higher than the TZS 21,000 applied at the PSPF. The funds therefore intend to continue with

their current minimum pension policy for the time being until further guidance is provided. The

reform scenarios modelled assume no change in minimum pension. It is recognized that, if

changed, this could mean an increase in benefits in future, and therefore a deterioration of some

of the funds’ financial position.

Withdrawals

35. Early withdraws are legally only allowed to be taken from the funds after 6 months of

unemployment. In 2012, the SSRA attempted to enforce this legislation. However, following a

strong negative reaction from members’ of the funds, this rule has not been applied in practice,

with members effectively withdrawing their balance when they change employment. This

remains a major problem for the PPF and the NSSF (covering more mobile, private sector

workers), where withdrawals constitute around 75% of benefit payments. The reform scenarios

modelled assume that current withdrawals patterns continue. However, it is acknowledged that

SSRA are currently examining the issue again and a stricter policy is likely to be applied in

future. Previous World Bank analysis showed, this would improve the financial position of the

funds in the shorter-term. For example, the NSSF, which could see its breakeven point improve

by around 5 years.

Segregation of schemes

36. In addition to stating that the new benefit parameters apply only to new members of the

PSPF and LAPF, the Harmonization Rules also require that separate accounts are established for

new members joining the LAPF and PSPF. This would effectively mean that these funds would

run two different schemes, and closed DB fund for existing members based on the old

parameters, and an open scheme for new members based on the parameters outlined in the

Harmonization Rules. The contributions paid by new members would be directed to the new

fund (which would build up a surplus as benefit payments would not commence for 30 years or

so), and would not be used to cover the benefit payment of existing members.

1637. The closed funds – particularly the PSPF which would be responsible for paying the pre-

1999 liabilities on behalf of the government - would therefore run into financial difficulties

sooner than the integrated fund, as the table below shows. The PSPF and LAFP confirm that they

are currently still running their scheme on an integrated basis, and are awaiting further guidance

from the SSRA. The reform scenarios modelled assume that the PSPF and LAPF continue to

operate on an integrated basis. It is acknowledged that if the segregation is applied the PSPF will

need larger cash injections from the government in order to pay benefits in the current and

coming years. Though this is a useful exercise to illustrate the financial position of the funds, it is

recommended that they continue to operate on an integrated basis.

Figures 4+5. PSPF and LAPF: Existing member scheme on open and closed basis

PSPF LAPF

500

2014 2017 2020 2023 2026 2029

(500) 400

(1,000) 300

Operating 200 Operating

(1,500) deficit/surplus if the deficit/surplus if the

fund remains open 100 fund remains open

(2,000)

Operating Operating

(2,500) deficit/surplus in the 2014 2017 2020 2023 2026 2029 deficit/surplus in the

(100)

closed fund closed fund

(3,000) (200)

(3,500) (300)

(4,000) (400)

38. The PPF currently consists of two funds, a DB scheme and the Deposit Administration

Scheme (DAS) which is a DC fund (members are generally those who join the PPF after age 45

and therefore would not be able to build a sufficient number of years of contribution history to

qualify for a DB benefit). These schemes are current managed in an integrated fashion and there

is no segregation of assets between the two (the DAS members being allocated the investment

return on assets after the DB benefits have been paid). Due to the young demographics and

surplus of the fund, this has not been a problem to date. However, it is not good practice to

manage these different types of fund on an integrated basis. This issue should be addressed as a

different type of membership from the informal sector is recruited to the join the DAS scheme. If

the DB and DAS were to operate on a separated basis, the financing of the DB scheme would be

worse. The breakeven point under the new Harmonization Rules of the separated DB fund would

be closer to 2030 than the estimated 2036 for the combined DB and DC fund.

17Figure 6. PPF DB + DC schemes

0.5%

0.4%

0.3%

0.2%

0.1%

0.0%

-0.1%

-0.2%

-0.3%

DB and DC integrated DB and DC segregated

Asset values

39. The financial viability of the funds, depletion schedules, and estimates of government

liabilities do depend on investment income. However, as these are these are only partial funded,

effective PAYG schemes, the modelling results are not very sensitive to asset valuations and

returns.10 That said, these are important considerations for the short-term cash flows, and long-

term investment decisions have an important impact on the economy as a whole.

40. This modelling exercise uses a conservative asset return assumption, based on zero real

return. The exercise also uses current valuations of the fund assets, as stated in the latest annual

reports. All assets are assumed to be liquid and sellable at marked values. In practice, some

assets will be worth more than their book value, whilst others would not be fully liquid. A full

asset liability management (ALM) study of the portfolios would be required to derive a more

accurate picture.

41. The Social Security Schemes Investment Guidelines issued by the BOT in 2012 under the

SSRA Act No 8 2008 are a welcome development given the lack of diversification of the funds’

portfolios. Almost half of the portfolios on average are in government bonds and bank deposits.

Ensuring that the portfolios of the funds meet the spirit as well as the letter of these guidelines

will be the next challenge.

42. The most urgent is to ensure that the high level of direct government loans in the funds’

portfolios (currently 24% on average) are reduced in line with the 10% maximum prescribed in

the investment guidelines. This has further increased the government’s exposure to the funds -

particularly to PSPF, where almost half of their portfolio consists of these loans, and NSSF, with

10

For example a 1% increase in returns improves the breakeven position of the funds in the long-run by around 2

years.

18over one-third of their assets in these instruments, and the exposure highly concentrated in the

UDOM loan. The government also needs to address the non-performance of a number of these

loans (estimated as of 2013 at TZS 400 billion of total TZS 1.8 billion outstanding, or around

10% of the funds’ combined assets).11 The BOT has instructed the funds not to undertake any

new loans until the 10% limit in the investment guideline has been achieved.

43. To allow further diversification of the portfolios’, investment across the East Africa

Community is under consideration, which would bring the Tanzanian funds in line with the other

social security funds in the region, and the EAC investment guidelines which are being drafted.

Table 9. Portfolio Allocation of Social Security Funds

Investment Funds'

Pension Fund Allocations (% portfolio) Guidelines Average NSSF PSPF PPF LAPF GEPF

Government Securities 20-70 29 22 13 27 38 47

Fixed Deposits 16 18 13 5 26 16 30

20

Loans + other special (10 gov/ 10 corp) 24 37 46 14 18 6

Corporate bonds 40 2 1 1 3 3 4

45

(15 listed/

Equity (+collective investments) 30 collective inv) 12 6 16 20 11 5

Real estate 30 14 21 19 10 14 8

Infrastructure 25

Source: pension fund annual reports

Figure 7. Comparison Pension Funds’ Portfolios

60

50

40

30

20

Tanzania Pension Funds

10

0 CPPIB Canada

GEPF SA

Source: Pension Funds’ Annual Reports

11

The topic is covered in more detail in the full Contingent Liabilities Study.

19IV. Impact of Merger

44. The Harmonization Rules serve to improve the financial position of the funds. However,

contingent liabilities to the government still remain over the long-term. Merging some of the

funds (and thereby combining funds which have surpluses and deficits at different times), would

serve to reduce the contingent liabilities further – from 25% to 16% of GDP.

Table 10. Government contingent liabilities under base case and reform scenarios (net present

value as % of 2013 GDP)*

All funds NSSF PPF PSPF** LAPF GEPF

Base case (no reform) 48.5% 5.7% 0.0% 41.8% 1.0% 0.0%

Harmonization rules 25.1% 0.6% 7.5% 17.1% 0.0% 0.0%

Merger 15.9% 5.2% 10.7%

Merger+cost saving 12.4% 2.6% 9.8%

* Assuming interest rate equal to inflation and using 5% real discount rate.

** Assuming PSPF does not finance pre99 pensions.

45. Merging also has the advantage of addressing some of the structural inefficiencies which

arise from the having a large number of small funds. Harmonization alone, without merging

funds, does not solve issues related to fragmentation, especially the issue of high administrative

costs – which, taking the basic measure of administration costs as percentage of contributions,

range from 6% at the PSPF to almost 18-19% at LAPF, NSSF and GEPF.

46. Administrative costs in the Tanzanian funds are high by international standards, possible

due to the relative high numbers of staff employed vs. the size of the funds and the due to the

small level of assets under management at each.12 This is clearly a snap shot in time and costs

may improve for small funds such as the GEPF as they grow. However, the planned expansion

into the informal sector could actually raise costs in the short-term. .

Table 11: Operating costs of public pension funds as share of gross income, mid- to late 2000s

Country grouping Operating cost as Selected countries in category

share of gross

income

Most efficient public pension Less than 1% Denmark, Ecuador, Singapore, Korea, Finland,

programs Sri Lanka, Malaysia

Intermediate efficiency public 1% to 3.3% New Zealand, Ghana, Egypt, France, USA,

pension programs Japan, Ireland

Most inefficient public 5% to 24% Tanzania, Philippines, Fiji, South Africa, Costa

pension programs Rica

Source: Sluchynskyy, 201413

12

The ILO is currently conducting a review for the SSRA of the cost structure of the pension funds. Further details

and recommendations should be available in this forthcoming report.

13

See Sluchynsky, O., (2014), ‘Defining, Measuring and Benchmarking Administrative Expenditures of Public

Pension Programs.’ The numbers for the Tanzania funds quoted in the report are based on 2007 data.

20Table 12: Administration costs and indicators for public pension funds in selected African

and Asian countries

Country/Fund Insured Admin Admin expenses /

beneficiaries per expenses/contribution AUM %

staff USD revenue %

Malaysia Provident 1,251 1.83 0.27

Fund

Philippines Social 1,579 9.58

Security

Singapore Central 2,089 0.66

Provident Fund

Thailand Social 1,662 2.23

Security

Thailand Government 4,324 3.05

Pension Fund

NSSF Uganda 2,250 13 1.6

NSSF Kenya 528 4.9 3.3

RSSB Rwanda 1081 27 3.8

PSPF 1,704 6 2.6

NSSF 363 18 4.5

LAPF 497 19 4.0

PPF 486 15 4.0

GEPF 402 18 4.5

Source: Sluchynskyy, 2014 14

47. Merging funds would allow for economies of scale, which can be significant for pension

funds. For example Sluchynsky (2014) estimates that plans with 100,000 pay a premium of 50%

in terms of costs due to their size vs. the same plan with 500,000 beneficiaries, and that larger

plan sizes can be 25% less expensive per beneficiary to manage. At almost 1 million members,

merging all social security funds in Tanzania into one National Fund would easily achieve these

beneficial economies of scale sizes, whilst even two separate funds for the private sector (which

would have over 500,000 members) and public sector (at almost 500,000) would also be

beneficial.

14

See Sluchynsky, O., (2014), ‘Defining, Measuring and Benchmarking Administrative Expenditures of Public

Pension Programs.’ The numbers for the Tanzania funds quoted in the report are based on 2007 data.

21Figure 8. Economies of scale in administrative expenditures (per beneficiary costs relative to

per beneficiary costs of plan with 500,000 beneficiaries)

Source: (Sluchynsky 2014)

Figure 9. Costs of Managing Pension Assets

Source: (Sluchynsky 2014)

48. Merging funds will reduce government liabilities even if administrative costs remain at

their current level. Contingent liabilities would be reduced from 25% to around 16% were two

funds – one for the public and one for the private sector –established. If administration costs at

the more inefficient funds could be reduced to the industry average, contingent liabilities reduce

further to around 12% of GDP. However, such reductions may be difficult to achieve in practice

(particularly if staff cuts are involved). It should also be noted that costs at most funds are

22currently increasing as the funds expand their coverage to informal sector workers. Though a

worthy aim over the long-run, this trend needs to be watched.

V. Experience of Other Countries

49. How does the reform of the social security funds compare with reforms conducted in

other countries in the region and elsewhere?

Level of Parametric Reform

50. The Harmonization Rules do not increase the contribution rate of the social security

funds, which is practical given these are already high compared with funds in the region and

given levels of economic development in the country.

Figure 11. Social Security Fund Contribution Rates Selected Sub-Saharan African Countries

35.0

30.0

Contribution Rate (% of Covered Wage)

25.0

20.0

15.0

10.0

5.0

0.0

Liberia

Seychelles

Kenya

Burundi

Benin

Guinea

Chad

Mali

South Africa

Gabon

Eritrea

Sudan

Mauritius

Niger

Equatorial Guinea

Ethiopia

Senegal

Nigeria

Cameroon

Congo, Dem. Rep.

Congo, Rep.

Sierra Leone

Ghana

Mauritania

Rwanda

Burkina Faso

Gambia, The

Togo

Uganda

Central African Republic

Zambia

Sao Tome and Principe

Tanzania

Zimbabwe

Swaziland

Cape Verde

Cote d'Ivoire

Madagascar

Additional Contribution Rate for Non-Old Age Social Security Employer Old Age/Disability/Survivorship

Employee Old Age/Disability/Survivorship

Source: World Bank pension database

51. In terms of reforms to benefit parameters, many countries have had to adjust their annual

accrual rates on pension downwards in recent decades to make their systems sustainable. Table

13 shows the regional average annual accrual rates in DB pension systems by region and in

selected African countries.

23Table 13: Average Accrual Rate by Region

Civil Service Scheme National Scheme

Asia 1.8

LAC 2.3

CEE 0.9

MENA 2.4

OECD 1.5

Africa 2.05

Benin 2 2

Burkina Faso 2 2

Burundi 1.67 2

Central African Republic 2.7

DRC 2

Congo 1.7

Cote d’Ivoire 2 1.7

Ethiopia 3

Gabon 2 1.8

Ghana 2.5

Guinea 2

Liberia 1

Madagascar 2 1

Mali 2 2.6

Mauritania 1.5

Namibia 1.5

Niger 1.3

Nigeria 2 1.875

Rwanda 2

Senegal 2 1

Sierra Leone 2

Togo 2.5 1.33

Uganda 2.4

Zimbabwe 1.3

Source: World Bank pension database

52. The Harmonization accrual rate of 2.07% brings Tanzanian social security funds in line

with their regional peers. Though now less generous than the average fund in Latin America or

the MENA region, the Tanzania reforms lag behind those in Asia, Central and Eastern Europe

and the OECD countries (with the more pressing demographic challenges potentially being

behind the impetus for greater parametric reforms). The replacement rates (pre commutation)

remain generous (particularly in relation to the average wage of fund members), and the funds

will require further reform in future as their membership ages

53. No change in the retirement age under the Harmonization Rules means that the members

of the Tanzanian funds will on average spend over 17 years in retirement, which is at the longer

24end of regional comparisons. 15 years in retirement is considered the actuarially fair standard,

with international good practice then linking the retirement age to life expectancy.

Figure 12. Retirement Age and Life Expectancy (at retirement age) in Selected African

Countries

90

80

17.9 18.1 18.8 18.9 16.4 12.2 14.0

22.0 16.2 16.6 16.7 16.7 17.2 17.2

19.4 19.5 20.0 20.0 20.2 14.9 15.3 15.5 15.5 15.6 15.7 15.8 16.1

70 16.9 15.0 13.1 13.9 14.2

10.3

60

50

Age

40

30

20

10

0

Life Expectancy at ret. age Retirement Age - Men

Source: World Bank pensions database

Merging National and Civil Service Funds

54. Other countries have successfully merged various social security funds – including

introducing an integrated national fund for the private and public sector. There is a global trend

to consolidate systems, but progress varies by region. Central European countries have

historically always run consolidated schemes with both civil service and private sector workers.

In OECD countries, around half have consolidated schemes, and in Asia around 45 percent of

countries have.

Table 14. Arrangement of National and Public Service Social Security Funds by Region

Central

Latin

Africa MENA Asia Eastern OECD

America

Europe

Integrated Schemes 24 (63%) 8 (42%) 8 (30%) 21 (73%) 30 (97%) 11 (48%)

Partially Integrated 2 (5%) 4 (21%) 4 (15%) 5 (17%) 2 (9%)

Separate Civil Service Schemes 12 (32%) 7 (37%) 15 (55%) 3 (10%) 1 (3%) 10 (43%)

Source: World Bank pension database

2555. Some countries which integrated their national and civil service funds did so as part of a

systemic reform, with the public sector scheme being brought into a completely new system that

covered the entire formal sector. This was the case in Latin America, Central Europe and Hong

Kong. Other countries which managed such mergers without systemic reform include Ghana,

Jordan and the United States, though parametric reform of the national scheme usually took

place at the time of the merger.

Table 15. Integration of Civil Service Pension Schemes

Country Year Systemic Reform Transition

Cabo Verde 2006 No New entrants

Chile 1981 Yes New entrants; choice for others

Dom Republic 2003 Yes New entrants; choice for others

El Salvador 1998 Yes New entrants; choice for others

Ghana 1972 No New entrants

Hong Kong 2001 Yes New entrants

Jordan 1995 No New entrants

Peru 1994 Yes New entrants; choice for others

Turkey 2006 No All (pro-rate benefits)

USA 1984 No New entrants

Zambia 2000 No New entrants

Source: (Palacios and Whitehouse 200)15

56. Reforms of the public sector scheme, largely to ensure the financial stability of the

scheme and to reduce the burden on government resources, have been undertaken in various

African countries, including Botswana, Senegal, Sierra Leone, Zambia and Capo Verde.

15

Palacios, R., Whitehouse, E., (2006), ‘Civil Service Pension Schemes around the World’

2657. The recent reforms do not address the coverage of the pension system, though important

developments are taking place. All social security funds have registered supplementary schemes

and are reaching out to informal sector workers, with around 100,000 new members having been

recruited in total. In terms of covering the most vulnerable elderly, the Tanzania Social Action

Fund (TASAF) is extending its coverage to the most vulnerable households, many of which

include elderly members.

Figure 13. Pension Coverage Rates in Selected Sub-Saharan African Countries

60%

50%

40%

68.6%

Axis Title

30%

51.6%

20%

25.5%

10% 18.8%17.6%

12.8%

11.4%

8.8% 9.4%

10.4% 10.0%10.4%

6.8% 7.9% 7.6%

5.8%

4.8%4.9% 4.5% 5.0%5.0% 4.9%5.2%

2.0%

3.7%

2.1% 1.7% 2.5% 3.1% 4.2%

1.5% 0.9%

0% 0.8%0.8%

Sao Tome and…

Central African…

Niger

Malawi

Togo

Liberia

Benin

Burundi

Cote d'Ivoire

Nigeria

Burkina Faso

Madagascar

Mauritania

Swaziland

South Africa

Seychelles

Congo, Dem. Rep.

Tanzania

Lesotho

Sudan

Mali

Ghana

Namibia

Botswana

Zimbabwe

Mauritius

Angola

Chad

Mozambique

Uganda

Kenya

Cape Verde

Senegal

Sierra Leone

Ethiopia 1/

Rwanda 1/

Congo, Rep.

Zambia

Cameroon

Gambia, The

Occupational Schemes Civil Service National Scheme

Source: World Bank pension database

27VI. Regulation

58. This aspect of the PER review was also asked to consider the regulation of the funds. An

extensive review was undertaken on behalf of the IMF earlier in 2014, as part of technical

assistance to the SSRA. As this report is still being finalized, it is not possible for the World

Bank team to comment extensively on the topic at this time.

59. However, as noted previously, ensuring the compliance of the pension funds with

existing regulation – notably the investment guidelines – will be an important factor for

contributing to their on-going stability, and thereby the potential liability they pose to the

government.

60. Given the introduction of competition between the mandatory funds, and the

development of voluntary pensions, regulations guiding market conduct including the advertising

and selling of pension products are required and should be developed by the SSRA. This was one

recommendation made in the 2013 World Bank ‘Tanzania Diagnostic Review of Consumer

Protection and Financial Literacy’.

61. As discussed, the regulator may also need to address the issue of costs within the system

– particularly given the ultimate government guarantee of the funds.

28IV. Conclusion

62. The obligations and contingent liabilities of the government to the pension system in

Tanzania, under the previous rules of the pension funds, are estimated to amount to TZS 23.5

trillion, or 48% of 2013 GDP.16 This may be reduced to around TZS 12 trillion by the reforms

instituted by the new Harmonization Rules as of 1st July 2014. At current levels, this still

represents a large contingent liability to the government – including TZS 4.8 trillion or 10% of

GDP in actual arrears which the government owes to the PSPF. If paid in full, this would have a

substantial impact on either government finances and /or debt levels.17

63. The results of the DSA analysis conducted through the Contingent liability TA study in

December 2014, which includes PSPF arrears (pre-1999) of TZS 1.5 trillion and the actuarial

deficit of TZS 3.3 trillion, indicate that Tanzania’s debt is still sustainable both in the short and

medium term. The inclusion of these additional pension and contingent liabilities raises all the

ratios, including the PV of debt to GDP, the PV of debt service to revenue and the PV of debt

service to export, to a level that is above those obtained by the recent IMF and national DSAs.

Furthermore, the full inclusion of the actuarial deficit of the pension system in the DSA will push

the ratios even higher which may threaten the sustainability of Tanzania’s debt position. 18 In

addition, a new DSA, which incorporates more recent data including revised projections on

pension liabilities and the rebased GDP numbers, will be conducted in the first half of 2015

jointly with the Fund and the Bank.

64. The financial position of the PSPF remains vulnerable in the short term. If the parametric

reforms are applied only to new entrants government contingent pension liabilities will be

reduced over the long term, but the financial position of the system will remain vulnerable. In

order to ensure an immediate improvement in the financial position of the pension system, some

parametric reform will have to be applied to the pre-1999 liabilities, impacting all members of

the fund. This would also share the burden of reforms better between older and. The political

challenges of making such changes are recognized.

65. A reduction in the government obligations to the PSPF could come through applying

some of the Harmonization Rules to all members, at least to the pre-1999 portion of the benefits.

The government could also make cost savings which could be used to cover increased payments

to the PSPF by stopping indexing the pre-1999 portion of the liabilities.

66. In addition to applying some parametric changes to the PSPS, the government will have

to increase its payments to the fund in order to secure its financial position. This will have to be

done via a combination of cash transfers from the Consolidated Account and debt issuance. If

not, the fund will shortly be unable to fully pay promised benefits. Similar situations in other

countries have led to public protests, which can undermine confidence in the pension system as a

whole, and potentially have an impact on overall savings rates.

16

Present value of government obligations from 2013-2080 using 5% real discount rate.

17

A fuller assessment of the pension liabilities on government finances is included in the full Contingent Liability

report.

18

For a detailed discussion of the DSA which includes PSPF arrears and the actuarial deficit of the pension system,

see the Contingent Liability TA study.

29You can also read