Q1-2018 Review and Commentary - Convergence Long/Short Strategies

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Convergence Long/Short Strategies

Q1-2018 Review and Commentary

As we ended 2017, we foretold that the powerful bull market might slow as the countervailing

forces of global central bank tightening and U.S. Corporate Tax relief collide. We mentioned, and

still believe that despite this slowing, the global expansion should continue. What we did not

see was the inflation scare from a wage acceleration data point, and the massive uptick in tariff

and protectionist talk. These two events, along with a large dose of “tech wreck,” ratcheted up

market volatility and rattled complacent owners of tech companies that for many years could

“do no wrong.” We believe that as the trade talks mature with China, a reasonable compromise

will be worked out. Although interest rates are on an upward path, they remain low from a

long-term perspective and inflation appears contained. These higher rates may slow mortgage

refinancing, but with strong fiscal stimulus and a reduced regulatory environment, business

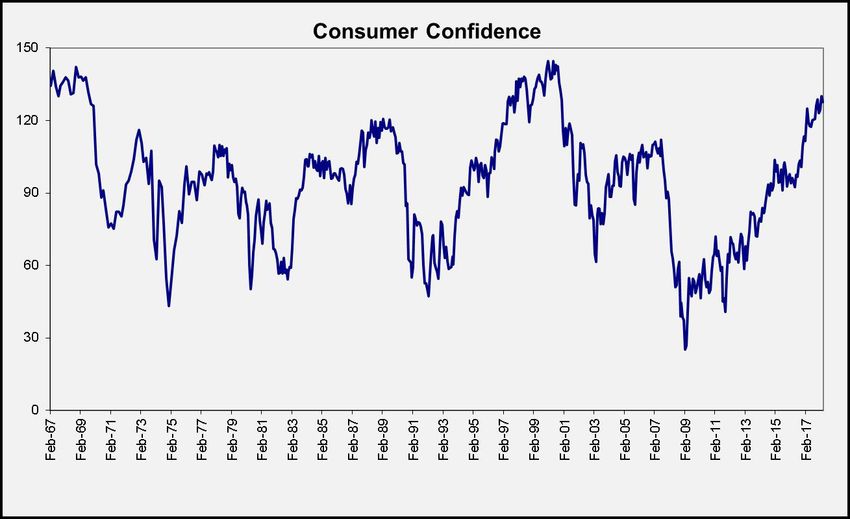

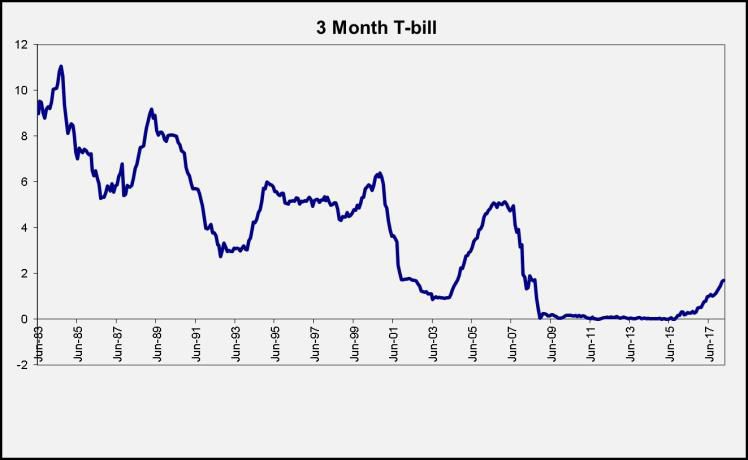

activity remains favorable. More importantly, small business optimism has remained elevated for

the last 5 quarters¹, and consumer confidence has been trending upward for nearly a decade

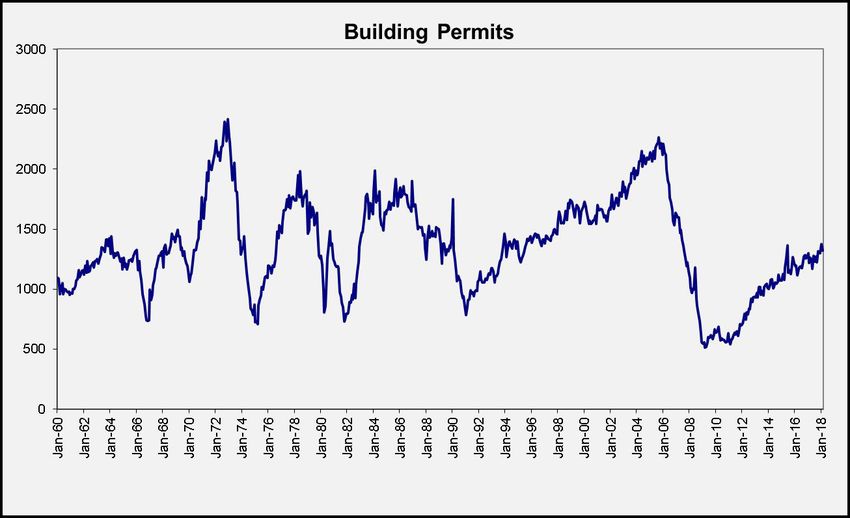

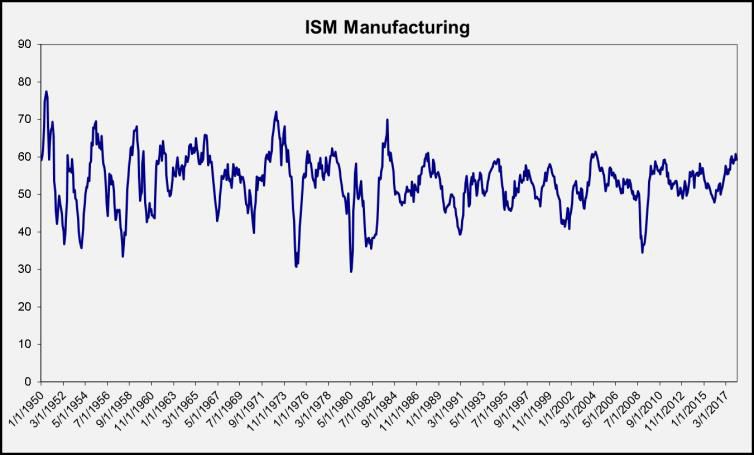

as shown in the chart below. Growth of the overall economy continues to trend upward as

GDP, housing, and manufacturing measures remain solid as shown in the following charts.

*

All Charts Sourced: Convergence Investment Partners, Bloomberg Finance L.P

Convergence Investment Partners, LLC | 1245 Cheyenne Ave. Suite 102, Grafton, WI 53024 www.investcip.com

Page 1

Convergence Investment Partners

We believe that increased volatility and intra-stock dispersion should allow shrewd and

discerning market participants who invest in fundamentally sound companies with strong growth

characteristics, to add notable alpha for their clients. Moreover, the market movement can create

opportunities for investors who take positions against (short) companies that exhibit poor and/

or deteriorating fundamentals. As always, the Convergence guiding mission is to stay focused on

long-term returns and identify companies that present opportunities based on their underlying

fundamentals. We believe that successful investing is based on consistently executing on a sound

and validated process. At Convergence our strategies are built on the premise that over the long

run, companies with strong and improving fundamentals tend to win, while companies with weak or

declining fundamentals tend to lose.

Again, as always, stay fundamental.

Overview of performance

In the first quarter of 2018, the equity markets took a pause from their upward charge. Inflation

worries, tariff threats and tech revaluations all served to temper U.S. stock returns with most major

indices ending the three months largely unchanged.

Much like the U.S. equity markets, the Convergence Long/Short strategies delivered “largely

unchanged” returns to start 2018. Our large cap focused Core Plus Strategy slightly outperformed

its Russell 3000 Index benchmark; our Market Neutral Strategy delivered a strong positive 1.87%

return while our Small Cap Strategy slightly trailed the Russell 2000 Index for the quarter. The

fundamentally favorable trends that began mid-year 2017 continued with the strong results we

witnessed in January, however, they took a pause in February and March, especially in the small cap

space.

On an absolute basis, our longest running Core Plus Strategy delivered 15.45% for the twelve months

ending 3/31/2018, and since inception (12/31/2009), this strategy, which maintains approximately

30-35% of capital in short positions, has delivered a 14.43% average annual return. Our next longest

running strategy, the Small Cap Strategy, returned 10.41% in the most recent 12 months. This small

cap focused portfolio, which has maintained a short position of 35-45% of invested capital, has

delivered a 13.50% average annual return since its May 2012 inception. And finally, our 35 month

old Market Neutral Strategy delivered a 8.14% return in the trailing twelve months and has returned

6.49% average annual since its May 2015 inception. This Market Neutral Strategy typically has

approximately 100/80 as its long/short exposure, and seeks to maintain a forward looking beta of

0.0-0.2. All of the aforementioned returns are stated net of fees as of 3/31/2018.

Long/Short Strategy Performance, ended 3/31/2018

Strategy % Short (of capital) Inception 1 year Since Inception Annualized

Large Cap Core Plus ~30-35% Dec 2009 15.45% 14.43%

Small Cap ~35-40% May 2012 10.41% 13.50%

Market Neutral ~80% May 2015 8.14% 6.49%

Annualized Total Return presented net of fees, including reinvested dividends

Convergence Investment Partners, LLC | 1245 Cheyenne Ave. Suite 102, Grafton, WI 53024 www.investcip.com

Page 2

Convergence Investment Partners

Beyond looking at the returns for each strategy in total, it is important to understand how the long

and short sides of each portfolio performed. The spread between long and short holdings provides

insight into how the market is rewarding/penalizing stocks based on fundamental rankings. We

often say that our Market Neutral Strategy is the purest expression of our fundamentally biased

investment philosophy, and the trend of months with positive long-short spread in this strategy

tends to be unsurprisingly long. This trend took a bit of a step back in February and March of 2018,

however, these months were not negative enough to counterbalance the powerful returns from

January. The Market Neutral Strategy’s return spread between the long and short holdings was

+2.3% for the quarter. Looking at the long and short sides individually, the long portfolio’s trend of

outperforming the U.S. market has been intact since May 2017 and the short’s since August 2016.

The Market Neutral Strategy (MN) delivered positive returns from its long positions, while the Russell

3000 Index was negative for the quarter. The MN’s portfolio of short positions also contributed

meaningfully to the quarter return by adding over 2%.

In our Core Plus Strategy, the long positions delivered modest outperformance in the first quarter

and the short positions provided a slight drag. The hedge ratio of the Core Plus Strategy (140/40)

was the true star as it exaggerated our long outperformance and reduced the negative contribution

of our shorts.

Our Small Cap Strategy faced a challenging short environment to start 2018. The long positions of

Small Cap underperformed by a few basis points while the short positions burdened performance

by being up just over 2%, which is undesirable in a quarter where the Russell 2000 Index benchmark

was down -0.10%. This negative long-short spread created a headwind that resulted in the Small

Cap Strategy finishing the quarter behind its benchmark.

The table below shows the industry groups from which each strategy had the most/least return

contribution in the first quarter of 2018.

Strategy Top Contributor(s) to Performance Top Detractor from Performance

Market Neutral Long Pharmaceuticals, Biotechnology & Life Sciences Capital Goods

Market Neutral Short Real Estate Software & Services

Core Plus Long Semiconductors & Semiconductor Equipment Food, Beverage & Tobacco

Core Plus Short Food, Beverage & Tobacco Software & Services

Capital Goods

Semiconductors & Semiconductor Equipment

Small Cap Long Semiconductors & Semiconductor Equipment Software & Services

Small Cap Short Real Estate Software & Services

The table above clearly shows that the Convergence Strategies had success selecting stocks in

the Semiconductor and Real Estate groups in the first quarter. Conversely, our strategies lagged

in the Software and Services group. During the second half of Q1, there was a meaningful “un-

fundamental”² rally that occurred in a few industry groups.

As active managers, we are hopeful that the recent months of rising stock dispersions and volatility

represent a shift of market dynamics. As we previously highlighted, the aging bull market combined with

rising interest rates, are resulting in higher volatility and stock dispersions. Those combined metrics tend

to provide more opportunities for active managers like Convergence that utilize long and short positions

to capitalize on stock dislocations.

Convergence Investment Partners, LLC | 1245 Cheyenne Ave. Suite 102, Grafton, WI 53024 www.investcip.com

Page 3

Convergence Investment Partners

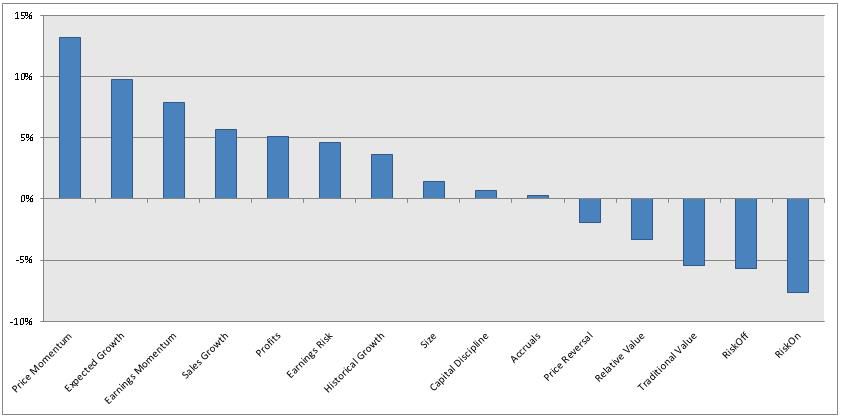

What Factors Worked?

The following table shows our top and bottom three performing factors over different time periods.

We ranked all 15 factor composites by quintile spread return³ in order to show that what works over

the long term is not always true in the short term (see disclosures for a definition of quintile spread

return).

3 mo 6 mo 12 mo 5 yr 10 yr 20 yr

Expected Price Price Traditional Traditional

Earnings Risk

Growth Momentum Momentum Value Value

Price Earnings Expected Price Price

Sales Growth

Top 3

Momentum Risk Growth Reversal Reversal

Sales Earnings Earnings Relative

Accruals Low Risk

Growth Momentum Momentum Value

Relative Relative Traditional

Accruals Profits Size

Value Value Value

Bottom 3

Traditional Relative Expected Price

RiskOn Low Risk

Value Value Growth Momentum

Traditional Price Expected

RiskOn RiskOn RiskOn

Value Momentum Growth

The table below shows how the factors that we monitor and employ at Convergence Investment

Partners performed over the 12 months ending 3/31/2018 based on long-short quintile spread

return.

One of our best long term factors, Traditional Value, had a rough trailing 12 months. We found

that overvalued names outperformed undervalued names by 5.44% over this period. This is

counterintuitive to Convergence logic, but we (like Warren Buffett) will always play the long game

and bet on reasonably valued companies for our longs. Also, we found that lower risk companies

(in terms of beta and historical volatility) trailed their higher risk counterparts by 5.72% in the

trailing 12 months… again, the same principle applies.

Convergence Investment Partners, LLC | 1245 Cheyenne Ave. Suite 102, Grafton, WI 53024 www.investcip.com

Page 4

Convergence Investment Partners

How is Convergence positioned?

The following table illustrates a few of the many fundamental factors that we utilize to rank the

relative attractiveness within our investment process. The values shown for each factor represent the

weighted average value of that specific factor and the broader market overall.

LONG MARKET SHORT

Category Factor Market Russell 3000 Russell 2000 Market

Neutral Core Plus Small Cap Index Index Neutral Core Plus Small Cap

Value Price to Earnings 13.4 15.2 18.9 24.8 73.7 82.6 143.4 -60.1

Value Price to Free Cash Flow 11.2 13.4 11.5 23.3 41.1 -12.5 -22.1 -7.5

Free Cash Flow to

Value 7.1% 6.5% 11.7% 3.9% 3.4% -2.1% -1.3% -5.2%

Enterprise Value

Profitability Net Income Improvement 24.5% 17.9% 24.8% 3.1% 4.2% 0.9% -1.4% -10.7%

Profitability Cash Flow to Sales 20.3% 19.8% 21.6% 10.9% -126% -45.8% -58.8% -208.5%

Profitability Internal Growth 37.2% 36.6% 27.5% 15.8% -0.6% -20.5% -22.2% -26.3%

Change in Shares

Capital Discipline -0.9 -1.3 0.0 0.6 8.6 12.8 13.3 39.8

Outstanding

Capital Discipline Dividend Growth 124% 150% 56% 101% 40% 52% 34% 26%

Quality Accruals/Assets 2.4% 2.4% 1.2% 4.5% 4.7% 13.1% 14.2% 10.5%

Quality Return on Assets (ROA) 7.0% 7.6% 7.2% 6.2% -0.2% -1.1% -3.7% -8.9%

Consecutive Qtrs

Earnings Growth 2.1 1.8 2.2 1.3 0.6 0.0 -0.3 -0.7

Earnings Growth

Earnings Growth Slope of Earnings 0.18 0.14 -0.03 1.70 10.15 -0.09 -0.19 -0.29

Cash Flow Consecutive Qtrs Cash

1.2 1.1 1.4 1.1 0.4 0.0 -0.2 -0.6

Growth Flow Growth

As of 03/31/2018; Source: Wilshire Analytics & Convergence Investment Partners.

As the table above demonstrates, the Convergence fundamental stock selection methodology leads

us toward holdings in the long portfolios with strong cash flow, earnings, revenues and other desirable

financial characteristics, at reasonable valuations. Over time, companies with these qualities have

typically rewarded investors as these are signs of healthy and growing companies with competitively

strong business models. Separately, the Convergence process also identifies companies with weak or

declining fundamentals demonstrated in the statistics, and our research has shown this to be effective

in sourcing alpha from shorting.

Convergence Investment Partners, LLC | 1245 Cheyenne Ave. Suite 102, Grafton, WI 53024 www.investcip.com

Page 5Convergence Investment Partners

Disclosures

Past performance is no guarantee of future results.

Source of all factor data: Convergence Investment Partners.

No graph, chart, or formula should in and of itself be used to determine which securities to buy or sell.

This communication is limited to the dissemination of general information pertaining to Convergence Investment

Partners, LLC’s (Convergence) services and general economic market conditions. The information contained herein

is not intended to be personal legal or investment advice or a solicitation to buy or sell any security or engage in a

particular investment strategy. There is no guarantee that the views and opinions expressed in this letter will come to

pass. The views expressed do not take into account any individual personal, financial, or tax considerations. The opinions

and forecasts herein are based on information and sources of information deemed to be reliable, but Convergence

Investment Partners does not warrant the accuracy of the information that this opinion and forecast is based upon.

Opinions expressed are subject to change without notice.

Strategy returns are presented net of fees. Net of fee performance returns are presented after actual standard

management fees, actual performance-based management fees and all trading expenses. No other fees are deducted

aside from trading and management fees for the calculation of net of fee performance. Returns include the reinvestment

of income.

Convergence Investment Partners is an investment adviser registered with the Securities and Exchange Commission

and is a majority owned subsidiary of Mariner Holdings, LLC. Registration of an investment adviser does not imply any

level of skill or training. For additional information about Convergence please refer to the Investment Adviser Public

Disclosure website at www.adviserinfo.sec.gov.

The Russell 1000 Index, Russell 2000 Index and the Russell 3000 Index are measures of the performance of the largest

1000, 2000, and 3000 US companies respectively. They are constructed to provide a comprehensive, unbiased, and

stable barometer of the broad market and it is reconstituted annually to ensure new and growing equities are reflected.

Comparison to any index is for illustrative purposes only and the volatility of the benchmark may be materially different

from the volatility of the strategies due to varying degrees of diversification and/or other factors. Index performance

returns do not reflect any management fees, transaction costs, or expenses. Indices are unmanaged. You cannot invest

directly in an index.

1.The president of the National Federation of Independent Business (NFIB) was recently quoted saying, “This is the

first time in 35 years where the fewest number of small business owners have told us that taxes are their number

one business problem. They’ve been so optimistic that they feel confident enough to raise wages and invest in their

business, which grows the economy.”

2.Un-fundamental: An “un-fundamental” rally is a temporary environment where companies with strong, positive

corporate fundamentals underperform companies with weak or declining fundamentals. These periods tend to be

short in duration (days or weeks). Over the long-run, sound economic and financial principles such as profitability,

growth, valuation, capital discipline, etc. tend to work positively over time. A normal fundamental market environment

is one where positive fundamentals are rewarded, and conversely, negative fundamentals are punished.

3.Quintile spread return: The return difference between the top 20% of stocks and the bottom 20% of stocks as ranked

by a specific factor or statistic, such as Price-to-Earnings ratio or 5-year earnings growth rate.

Convergence Investment Partners, LLC | 1245 Cheyenne Ave. Suite 102, Grafton, WI 53024 www.investcip.com

Page 6You can also read