REFORM IN IRELAND IMPLEMENTING EUROPEAN MARKET - PAUL MCGOWAN COMMISSIONER, CER

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Implementing European Market

Reform in Ireland

(and other Regulatory Matters)

Paul McGowan

Commissioner, CER

Energy Ireland

June, 2013

• CER is Ireland’s independent energy regulator • CER has broad economic, safety and customer protection functions in energy – water to follow • Details of the CER’s role at www.cer.ie • CER is currently led by: – Dermot Nolan, Chairperson – Garrett Blaney, Commissioner – Paul McGowan, Commissioner

In a world where energy supply and prices are highly volatile, the mission of the CER, acting in the interests of consumers is to ensure that: • The lights stay on • The gas continues to flow • The prices charged are fair and reasonable • The environment is protected • Energy is supplied safely

Agenda • SEM/Market Integration • Networks • Retail • Safety

SEM Integration Project

• Target Model - Implementation by 2016

• Final Decision on Next Steps published Feb 2013:

o Key decisions/working assumptions on:

Central Dispatch,

Capacity mechanisms and

RES-E – promotion/priority dispatch

• DCENR and DETI formally accepted the SEM Committee

recommendations in the Next Steps Paper and have

published governance arrangements for project

SEM Integration Project

• SEM Committee Next Steps Decision states that:

o It is important that the total remuneration from energy payments,

capacity payments and ancillary services is sufficient to ensure

security of supply

• Prices

• European Commission is expected to publish a communication

on state intervention in the internal market in July. Key guidance

is expected on:

o How Capacity Remuneration Mechanisms and RES support

schemes should be designed

• Will be important for SEM and GB market coupling to consider

these guidelinesSEM Integration Project

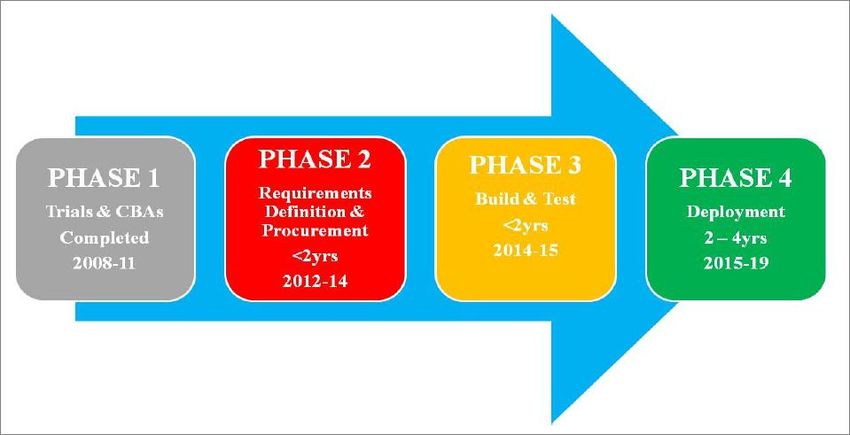

- Timelines/Next Steps

June 2013: Consultants on board, Project office

Q2/Q3 2013: PID/Project Governance

Q4 2013: High Level Design Consultation

Q1 2014: High Level Design Proposed Decision

Q2 2014: High Level Design Decision

2014 - 2016: ImplementationSEM Current Market

Gas Transportation Capacity

• Previously, the costs related to GTC have not been included in

SEM bids

• Trading of GTC has since developed

• SEM consultation on the issue was published late 2012 with

approx. 35 responses from a variety of stakeholder groups

• Responses presented a wide variety of views on this complex

and challenging issue - RAs have engaged both legal and

economic advice

• SEM Committee is to publish Provisional Conclusions and Next

Steps on the issue by 20th JuneSEM Current Market

DS3

• DS3: Delivering a secure, sustainable power

system

• All-island project led by TSOs aiming to ensure

policies and procedures to support the safe

operation of the system with instantaneous

penetration of wind of up to 75%SEM Current Market

DS3 – System Non-Synchronous

Penetration (SNSP)

50% SNSP 75% SNSPSEM Current Market

DS3: Wind Curtailment 2020

8%

75%SEM Current Market

DS3 – Key Elements

• System Services

o TSOs recommendations to SEMC published on 24th May

o SEMC Decision in Q4

– New services required to support the system as levels of wind increase

– TSOs have proposed a total value of €355 million

o SEM Committee will consider appropriate value to ensure service

delivery at lowest cost to consumer

• Rate of Change of Frequency (ROCOF) Grid

Code Modification:

o CER consultation paper in coming weeks following series of

meetings with generators

– Increase in Grid Code Standard from 0.5 Hz/sec to 1 Hz/sec:

o Impact on SNSP level and ability to deliver 2020

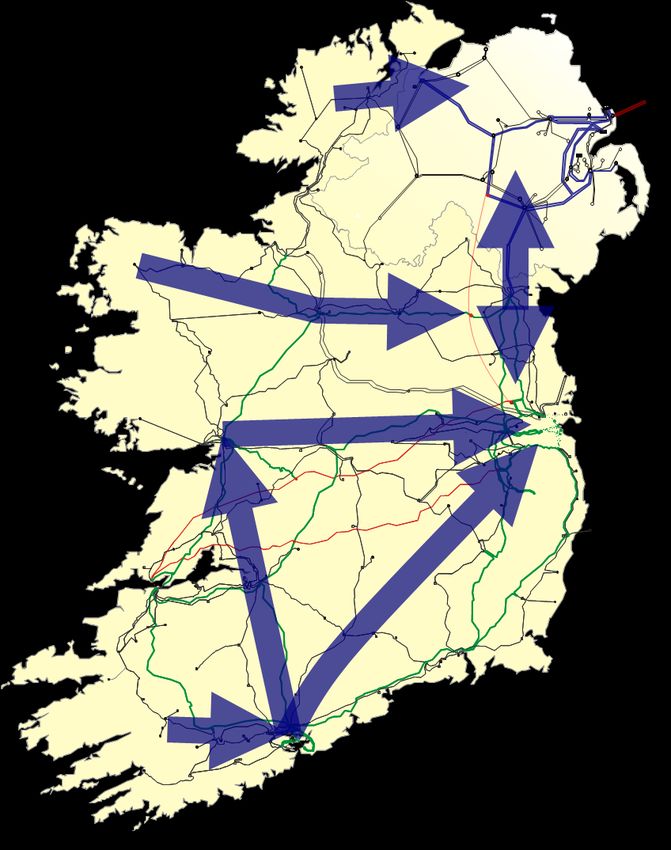

RES–E targets if both elements not deliveredElectricity Networks • Much wind in west, demand in east • Rolling out the grid is critical to meeting 2020 renewable target • New N-S line important for SEM • Over €1 billion planned grid investment 2011 to ‘15 • Planning and land access are a major challenge

Electricity Networks

• Incentivisation

– NSIC: Project Specific & Co-ordinated with UR

– Transmission Generally: Outcome Focused

• Gate 3 update:

o Constraints Reports currently issuing by Gate 3 area

o Offers must be accepted (or rejected) within 50 business days of

receipt of constraint report

• EWIC:

o Fully operational/Positive impact on SEM SMP

o SO – SO countertrading at times of high wind to reduce curtailmentGas Networks

Capacity Bookings

• Unprecedented decline in capacity bookings

• Interim tariff rise

• CER13/122 Consultation considers removal of flexibility in

order to increase bookings

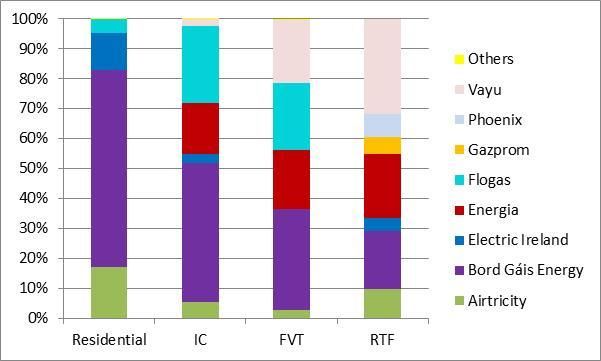

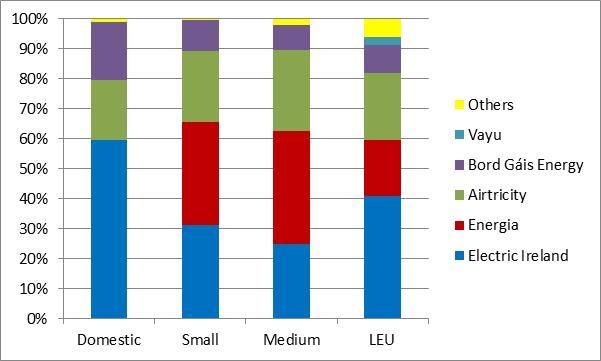

• Consultation closes 15th July 2013Retail Electricity Market, MWh, Q4 2012 Gas Market, Customer Numbers, Q4 2012

Retail

Deregulation & Competition

• Electricity Switching rate: 11.3% - considered active

• Gas Switching rate: 17% - considered very active

• Gas Domestic Market Deregulation

– Conditions outlined in NDM Review Decision paper CER/13/096

• With strong competition and deregulation, market

monitoring and customer protection an increasing focus

for CERRetail

Developments

• Revised Supplier Handbook published; formally adopting

changes to Codes of Practice.

• Accreditation framework for price comparison website

services launched

o Two websites now accredited: www.bonkers.ie and www.uswitch.ie.

• Market Innovation

o Suppliers launched their own Prepayment market models, providing

greater customer choice

• Disconnections

o Ongoing concern

o Monitoring closely

o Working closely with industry to address issueNSMP

• Decision on Smart Meter Decision 4th July 2012

– National rollout of Electricity and Gas smart meters

– CBA €229m NPV positive over 20 years (1 billion investment)

What do we hope to achieve by

implementing the NSMP?

1. Encourage Energy Efficiency

2. Facilitate Peak Load

Management

3. Support Renewables & Micro-

Gen

4. Enhance Competition &

Improve Customer Experience

5. Improve Network ServicesDownstream Safety

• Gas Safety Framework - legislation enacted in 2012 to

incorporate new safety functions including:

o LPG safety licences for Distribution Network operators

o LPG incident reporting

o Enhanced enforcement powers

• Safety Supervision:

o Will become law that only Registered Electrical Contractors

can complete domestic electrical works

o Three successful prosecutions of unregistered gas installers

o Consultation due on registration for Commercial Gas InstallersUpstream Safety

Petroleum Safety Framework

• A Risk-Based Petroleum Safety Framework (PSF) for

Designated Petroleum Activities

• Covers petroleum exploration and extraction (i.e. onshore and

offshore oil and gas including onshore shale gas extraction)

• Designed to meet best international practice

o Engender confidence & assurance amongst the public & industry

o Bring greater clarity & transparency to safety regulation of industry

• Will become fully operational on 30th November this year

• New Directive on Offshore Safety – Greater EU HarmonisationQuestions and Answers

You can also read