RETAIL PROPERTY MARKET - FRANCE - Knight Frank

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Q2 2018

R E TA I L

RETAIL PROPERTY

MARKET

FRANCE

FRENCH RETAIL PROPERTY MARKET

OVERVIEW

• Household consumption will remain sluggish in 2018 due to increases in purchase power being worn away by the increase in inflation.

However, French spending should accelerate during the second half of the year and maintain a steady pace in 2019 and 2020 due to the

Economy

continued improvement in the job market, wage gains and more favourable tax measures.

• Following a record level in 2017, tourist numbers continue to increase in 2018 in the Greater Paris Region, with a 7% increase year-on-year

in the number of hotel arrivals during the 1st quarter, related to the dynamism of the international clientele (+ 16.5 %, compared to + 0.2 % for

the French).

• This is a time for multi-faceted approaches, merging and commercial innovation. Shop-in-shops, pop-up stores, showrooms and single-brand

stores, brand associations…. terms and formats are not lacking, revealing a deeply changed commercial landscape, notably as a result

Brands

of the joint development of physical and virtual worlds.

• This joint development, illustrated by the digitalisation of points of sale and the incursion of “pure-players” in the field of physical retail, also

continues to manifest itself as an increase in alliances between traditional retailers and internet players (Monoprix/Sarenza,

André/Spartoo, Carrefour/Google, etc.).

• Brand difficulties and their profitability requirements continue to punctuate the retail property market through an increase in disposals,

whatever the asset class. The lasting nature of the increase in vacancy rates is, however, a function of the intrinsic quality of each asset,

retail zone or retail pitch.

Rental

• Restaurants, food, sport, beauty and decoration account for a significant proportion of openings and thus partially offset the slow down in

fashion. This diversity of players, and new concepts that they are the source of, notably contribute to the dynamism of the very heart of Paris,

as well as the renewal of the retail offer in large regional cities.

• 1.6 billion billion euros were invested in the retail market in France during the 1st half of 2018, an increase of 23% year-on-year. The

Investment

increase, however, is misleading as it is due to the completion of one exceptional deal: the acquisition by Hines, for BVK, of the future Apple

Store on the Champs-Élysées for almost 600 million euros, which greatly inflated investment volumes on high streets (65%).

• Retail parks take second place, ahead of shopping centres. In this market sector, which only accounted for 14% of French retail investment

volumes, yields saw new upward pressure, indicative of investors’ wait-and-see attitude

2

Economic context

FRENCH RETAIL PROPERTY MARKET

ECONOMIC CONTEXT

Temporary slowdown On the right track

French economic indicators Change in unemployment rate

Annual growth as a %, unless otherwise indicated % of active population

12

Indicator 2016 2017 2018f 2019f

GDP 1,1 2,3 1,8 1,7

10

Inflation 0,3 1,2 2,0 1,5 8.9

8 8.0

Household consumption 2,0 1,1 1,1 1,6

Household income¹ 1,8 1,4 1,2 2,0

6

Metropolitan France

Unemployment (whole of France) 10,1 9,4 9,1 8,8 Ile-de-France

4

12341234123412341234123412341234123412341

¹Household real gross disposable income.

2008 2009 2010 2011 2012 2013 2014 2015 2016 20172018

Source: Banque de France, Macroeconomic projections Source: INSEE

• As with most other advanced economies, French GDP growth has clearly slowed down since the start of 2018, with growth limited to 0.3 % as at

Q2 following growth of 0.2 % in Q1. However, activity should strengthen in coming months as a result of expected increases in company

investment and household consumption.

• In spite of a lower level than in 2017, the upturn in employment remains on the right track. Following the creation of 333,000 private sector jobs

last year, more than 160,000 will be created in 2018, contributing to the progressive fall in unemployment. The unemployment rate should soon drop

below 9%, a level that in spite of everything remains clearly above that of the European average (7 % at the end of May 2018, within the EU28). 4

FRENCH RETAIL PROPERTY MARKET

ECONOMIC CONTEXT

Rebound expected…in 2019 Decreasing morale

Household consumption Household opinion

In France, % of annual change in volume Summary indicator – CVS-CJO data

130

120

2.00%

110

1.60%

1.60%

1.40%

100

1.10%

1.10%

0.80%

90

0.60%

80

mars-00

mars-07

mars-14

oct-00

juin-05

oct-07

juin-12

oct-14

mai-01

avr-04

janv-06

mai-08

avr-11

janv-13

mai-15

avr-18

déc-01

févr-03

nov-04

déc-08

févr-10

nov-11

déc-15

févr-17

juil-02

sept-03

juil-09

sept-10

juil-16

sept-17

août-06

août-13

2013 2014 2015 2016 2017 2018f 2019f 2020f

Source: Banque de France, Macroeconomic projections Source: INSEE

• Having slowed down in 2017, household consumption will remain sluggish in 2018 due to the increases in purchase power being worn away by

the increase in inflation (+ 2.0 % in 2018, following + 1.2 % in 2017).

• Nevertheless, French spending should increase during the second half of the year and will probably maintain a steady pace in 2019 and 2020 due

to the continued improvement in the job market, wage gains and more favourable tax measures (suppression of council tax, decrease in employee

contributions). 5

FRENCH RETAIL PROPERTY MARKET

ECONOMIC CONTEXT

THE WINNERS…

Organic products

+17% in value in 2017

+250 new shops in 2017

Sports goods

+4% in value in 2017

+9 - 10% for the “women’s” category

Garden centres

+4% in value in 2017

Beauty products

+3% in value in 2017

Bazaars Online perfume sales: +27% in 2017

+19.3% in value in 2017

335 shops (+115 in 2017)

…AND LOSERS

Hypermarkets Shoes

Market share / all products: 29.3% in 2017 (32.6% in 2012) -4.4% in value in 2017

Market share / non-food products: 12.8% in 2017 (17.7% in 2012) -12% of shops > 400 m² between 2012 and 2017

Clothing / Textile Books

-0.8% in value in 2017

-13% in 10 years

E-books: +9% in 2017

- 2.8% in 2018 at end of May, following +0.6% in 2017

Toys

-3.8% in value in 2017

Sources: INSEE* / Union Sport & Cycle / IFM / NPD

*Large specialist retailer figures/Annual change Share of online sales: 24.9%

6

FRENCH RETAIL PROPERTY MARKET

ECONOMIC CONTEXT

Towards new peaks Foreigners driving growth

Change in number of hotel arrivals Change in number of hotel arrivals

In the Greater Paris Region, as at 1st quarter each year In the Greater Paris Region

400000

▲ 14%

350000

Foreign tourists

300000 ▲ 15%

+16.5%

250000 Q1 2018 / Q1 2017

200000 ▲ 31%

▲ 5%

150000

▲ 21%

100000

▲ 17%

French tourists

50000

+0.2%

0 Q1 2018 / Q1 2017

United States UK Germany China Japan Russia

2016 2017 2018

Source: Paris Tourist Office / Red box: annual growth between Q1 2017 and Q1 2018. Source: Paris Tourist Office

• Following a record level in 2017, tourist numbers continue to increase in 2018 in the Greater Paris Region, with a 7% increase year-on-year in

the number of hotel stays during the 1st quarter, related to the dynamism of the international clientele (+16.5%, compared to +0.2% for the French).

• Almost all nationalities show an increase, to varying degrees depending on the continent. For once, Europe saw the greatest increase year-on-

year (+19%), partly related to the rebound in arrivals of the Germans and Spaniards, and the return of the British. The increase in Asians is more

modest (+10.8%) due to the slowdown in growth of Chinese arrivals. 7

FRENCH RETAIL PROPERTY MARKET

ECONOMIC CONTEXT

Strong growth in Paris… …and the regions

Rate of Sunday openings in international tourist zones Rate of Sunday openings in international tourist zones

In Paris, according to activity sector as a % In regions, by town as a %

Food Luxury Other City End of January End of December

2017 2017

Antibes 12% 15%

Cagnes-sur-Mer 26% 45%

11% 27%

31% 16%

Cannes 10% 49%

43%

Deauville 70% 75%

63%

Dijon ˂10% 51%

La Baule 49% 56%

Nice 32% 36%

Saint-Laurent-du-Var 37% ˃80%

Before the measure End of Septembre 2017

Source: French Ministry of Economy and Finance Source: French Ministry of Economy and Finance

• Almost three years after the adoption of the Macron Law, a new assessment made by the Ministry of the Economy confirms the increase in Sunday

openings of shops in Paris, going from an average of 17.4% before the measure to 30.4% in September 2017.

• The analysis is the same outside of Paris, where 44% of shops located in international tourist zones opened on a Sunday at the end of 2017,

compared to 25% at the start of the year.

8

Brand strategies & retail formats

FRENCH RETAIL PROPERTY MARKET

BRAND STRATEGIES & RETAIL FORMATS

Increase of 14% expected in 2018 A general increase

E-commerce sales E-commerce market shares per sector

In France In France, estimations in 2017 as a %

100 50%

90

Cultural products High-tech Clothing

34%

80 40%

33%

70

28%

25%

24%

60 30%

22%

19%

13%

50 23%

15%

14%

14%

14%

14%

40 20% 45%

12%

30

20 10%

15.6

20.0

25.0

31.0

37.7

45.0

51.1

57.5

64.9

72.0

81.7

93.2

10

11.6

0 0%

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018f

Sales (€ billion) Annual growth (%)

Source: Fevad Sources: Fevad / GFK / IFM / Nielsen

• Internet sales increased by 14% in 2017 to reach almost 82 billion euros. Mobile devices accounted for 21% of this total (+50% year-on-year),

compared to barely 2% five years ago.

• In 2018, online sales should reach more than 93 billion euros, putting France in second place in Europe, behind the United Kingdom (178 billion)

and equal with Germany, but well ahead of other large European countries such as Italy and Spain (28 billion each).

10FRENCH RETAIL PROPERTY MARKET

BRAND STRATEGIES & RETAIL FORMATS

An ongoing revolution

Number of new concepts per year Highly sought-after formats The joint development

All sectors, in France of physical and virtual worlds

POP-UP

STORES

292

253

248

236

SHOP-IN-

SHOPS

2014 2015 2016 2017 SINGLE-

BRAND

STORES

Source: La Correspondance de l’Enseigne

• This is a time for multi-faceted approaches, merging and commercial innovation. Shop-in-shops, pop-up stores, showrooms and single-brand

stores, brand associations…. terms and formats are not lacking, revealing a deeply changed commercial.

• The joint development of physical and virtual worlds, illustrated by the digitalisation of points of sale and the incursion of “pure-players” in the field

of physical retail (AMPM, Birchbox, etc.), also continues to manifest itself as an increase in alliances between traditional retailers and internet

players (Monoprix/Sarenza, André/Spartoo, Carrefour/Google, etc.). 11FRENCH RETAIL PROPERTY MARKET

BRAND STRATEGIES & RETAIL FORMATS

Type of location

Expansion projects that combine formats Out-of-town

Examples of developing brands Shopping centres

In France, by activity

High street

Sources: Knight Frank, press and brands

FASHION / SPORTSWEAR RESTAURANT FOOD DISCOUNT / BAZAARS OTHERS

Calzedonia Au Bureau Ange Action Adopt’

Chaussea Beef House Bio C Bon Centrakor Amazing Jewelry

Décathlon Bistro Régent Biocoop Easy Cash Basic Fit

Intersport Burger King Day by Day Gifi Cultura

JD Sport Five Guys Grand Frais Hema Darty

Kiabi La Pizza de Nico Kusmi Tea La Foir’Fouille Fnac

Primark O’Tacos La Vie Claire Maxi Bazar La Redoute

Superdry Pitaya Marie Blachère Noz Orchestra

Takko Steak n’ Shake Naturalia Stokomani Parfois

Uniqlo Vapiano NaturéO Tiger Rituals

Women’secret Yogurt Factory Nespresso Zeeman Sostrene Grene

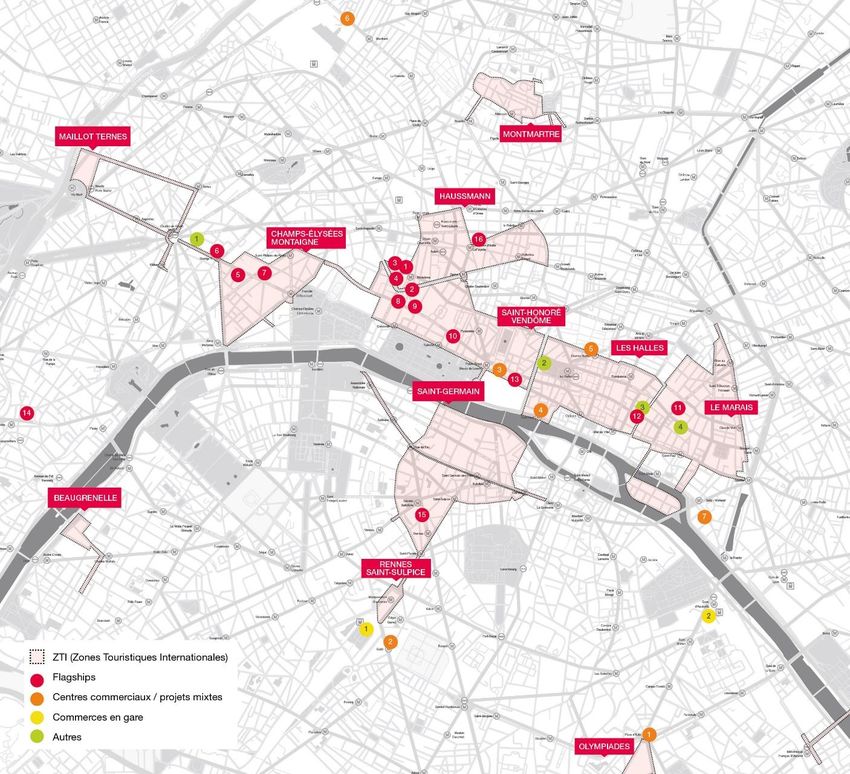

12The rental market High streets

FRENCH RETAIL PROPERTY MARKET

HIGH STREETS | PARIS

Continued dynamism

Trends in the Parisian high streets retail market

• Hotel arrivals increased by 7.4% year-on-year in the Paris region. The Rossignol has just taken over the Basler shop at 21 boulevard des

increase is 16.5% for foreign visitors. This dynamism benefits the Capucines.

retail market, particularly within international tourist zones (ITZ).

• The analysis of the different Parisian retail sectors does not really show

Moreover, the ITZs concentrate most new flagship projects, as well as

any new trends. Rue Saint-Honoré remains one of the most lively

most operations to create or renovate luxury hotels in the capital.

streets, with the advancing works to future large flagship stores

• The busiest streets are still the main targets of international brands (Chanel, Graff, Saint Laurent, etc.), new openings (Akillis, Isabel Marant,

looking to optimise their communications and offer their clients a Moschino, Herno, Hervé Chapelier, Marni, Serge Lutens, etc.) and

more qualitative and updated shopping experience, like H&M with recent deals (Balmain).

their flagship store at 1-3 rue La Fayette over almost 5,000 m². Whilst

• On the Champs-Élysées, certain or potential refurbishment projects

retailer movements are less numerous than a few years ago, the mass

remain numerous and continue to drive the avenue, which is more and

fashion giants continue to play an important role in this, especially given

more dedicated to flagship stores. These changes, in light of recent

that the disposals they undertake to streamline their network help to

and ongoing transactions, will likely intensify the avenue's

drive the market (Balmain instead of Zara at 374 rue Saint-Honoré).

upmarket move.

• Several other types of player are active: luxury brands and fashion

• Dormant for some time, the Left Bank seems to be making a

designers, the food and restaurant sectors, sport, cosmetics and

comeback. Brands (Tumi, Salomon), recent players (Five Guys) and

decoration account for a significant share of openings. Such a range of

new concepts (From Future, Décathlon City) are all active there; the start

players and concepts conveys the effervescence and upmarket move

of an increase in activity that has been seen in the mid and upmarket

of the capital’s very heart.

sectors, but which has not yet been seen in the luxury sector, in spite of

• This effervescence is also indicative of tests undertaken by brands to the reopening of Lutétia Hotel.

adapt their models to new consumer expectations and to take advantage

• The effervescence of the Parisian market is not expressing itself by a

of changes in buying patterns (Leroy-Merlin at Madeleine and in the

generalised increase in prices. Rental values remain generally stable

Batignolles area, the new AMPM flagship store on rue Étienne Marcel,

in the capital. Whilst these could still increase on a limited number of

etc.).

streets, they are suffering from downward pressure on some good

• Furthermore, the trend for brands to undertake their own distribution streets due to brand’s profitability requirements and high prices that

is increasing in the cosmetics, luggage and sport sectors. After have been reached in recent years.

Fusalp in the Marais and Salomon on boulevard Saint-Germain,

14FRENCH RETAIL PROPERTY MARKET

HIGH STREETS | PARIS

Examples of recent transactions in Paris

Source: Knight Frank

Retailer Address District Total area ZA rent

(m²) (€/m²)

IKEA 23 boulevard de la Madeleine Paris 1 6,000 Confidential

AMPM 49 rue Etienne Marcel Paris 1 564 1,700

HEMA 3 rue du Havre Paris 9 316 2,400

Future IKEA store, 23 bd de la Madeleine, Paris 1

ROSSIGNOL 21 boulevard des Capucines Paris 2 300 2,940

TUMI 17 rue du Vieux Colombier Paris 6 240 2,670

BAP 16 boulevard des Capucines Paris 9 220 3,250

DYPTIQUE 56 rue de Passy Paris 16 220 3,370

SALOMON 129 boulevard Saint-Germain Paris 6 211 2,770

HUGO BOSS 118 rue Vieille du Temple Paris 3 168 2,350 Salomon, 129 bd Saint-Germain, Paris 6

TUMI 63 Avenue des Champs-Élysées Paris 8 165 15,970

FOOTPATROL (JD SPORT) 45 rue du Temple Paris 4 110 1,160

SERGE LUTENS 324 rue Saint-Honoré Paris 1 87 10,000

L’OCCITANE 144 rue de Rennes Paris 6 86 3,060

DUPONT ST 10 rue de la Paix Paris 2 50 6,200 Foot Patrol, 45 rue du Temple, Paris 4

15

Note: rounded valuesFRENCH RETAIL PROPERTY MARKET

HIGH STREETS | PARIS

Record in sight Alignment of the planets

Worldwide sale of luxury items An array of favourable factors

300 50%

Boom in

250

40% online

sales

30% Rise in

200 tourism

Increase in spending

13%

10%

12%

from Chinese consumers

6 - 8%

11%

20%

150

7%

4%

3%

3%

10%

0% Success of

-2%

-2%

100 beauty and

-8%

0% accessories

50 276 - 281 -10% Local

consumption

159

170

167

153

173

192

212

218

224

251

250

260

0 -20% Millenials

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018f

Sales (€ billion) Annual growth (%)

Source: Bain & Company Sources: Bain & Company / Knight Frank

• After a slowdown in 2016 and then an increase last year, luxury sales should once more gain strength in 2018. The increase for this year will

thus be comprised between 6 and 8%, driven by the dynamism of sales in Asia (between 9 and 11%).

• The luxury industry is benefitting from an array of structural and temporary favourable factors, ensuring durable growth in the long-term. Among

these factors are the continued rise in international tourism (worldwide increase in arrivals of 3.3% per year between 2010 and 2030), as well as

the growing adjustment of luxury brands to new consumption methods (digitalisation, expectations of millenials, etc).

16FRENCH RETAIL PROPERTY MARKET

HIGH STREETS | PARIS

Recovery still to be confirmed

Focus on the luxury Paris market

Breakdown of openings per street

Change in number of luxury shop openings

Share as a %, out of total openings in Paris

In Paris

2018 Rue Saint-Honoré

52

50

Avenue Montaigne

39 23% 24%

37

24% 22% Vendôme / Paix

28

Faubourg Saint-Honoré

4% 2012-2017

8% 12%

7% Sèvres / Saint-Germain

13%

10% 12% George V / François 1er

11% 11%

5% 11% Champs-Elysées

Annual average 2015 2016 2017 2018* 5%

2012-2017

Autres

¹Survey undertaken at the end of June 2018.

Source: Knight Frank Source: Knight Frank

• More than thirty definite and potential openings are expected over 2018, equating to an increase of more than 30% already compared to

openings that took place in 2017.

• Three streets have confirmed their dynamism: rue Saint-Honoré, avenue Montaigne and the Place Vendôme / Rue de la Paix area concentrate

nearly 50% of openings in 2018, a share equivalent to that of the last five years. Whilst the Champs-Élysées has seen their share increase,

thereby confirming its upmarket move, others are less dynamic, for example rue du Faubourg Saint-Honoré and the Left Bank. 17FRENCH RETAIL PROPERTY MARKET

HIGH STREETS | PARIS

A larger supply of high-end accomodations

Luxury hotels in Paris: recent and future openings

Source: Knight Frank

18FRENCH RETAIL PROPERTY MARKET

HIGH STREETS | PARIS

Few changes…

Prime rental values, in Paris, in €/sq m/year Zone A*

Changes in prime rental values

Street or retail area District Rent Rent Trend Between 2006 and 2018, on some Parisian

as at Q2 2017 as at Q2 2018 streets, in €/sq m/year Zone A*

25,000

Avenue des Champs-Élysées Paris 8 20,000 20,000

20,000

Avenue Montaigne Paris 8 15,000 15,000

15,000

Rue du Faubourg Saint-Honoré Paris 8 15,000 15,000

10,000

Rue Saint-Honoré Paris 1 12,000 12,000 5,000

-

Boulevard Haussmann Paris 8 / 9 6,000 6,000

Q2 2018

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

Sèvres / Saint-Germain Paris 6 / 7 6,000 6,000

Champs-Elysees

Marais Paris 3 / 4 5,000 5,000 Avenue Montaigne

Rue Saint-Honoré

Rue des Francs-Bourgeois

Capucines / Madeleine Paris 1 / 2 / 8 / 9 4,000 4,000

Source: Knight Frank

Rue de Rivoli Paris 1 / 4 3,500 4,000

Rue de Passy Paris 16 2,500 3,000

*Rental value: decapitalised rent + assignment (leasehold/business) 19FRENCH RETAIL PROPERTY MARKET

HIGH STREETS | PARIS

Change is in the air

Examples of recent and upcoming projects

In Paris, between 2017 and 2021

Source: Knight Frank

20FRENCH RETAIL PROPERTY MARKET

HIGH STREETS | REGIONS

Supply undergoing strong renewal

Trends in the high streets retail market in the regions

• A record number of new companies in Lyon, an unemployment rate at thus continue to spread, following the inspiring examples of some large

its lowest level since 2008 in Nantes, the number of overnight stays at European cities, such as “Time Out Market” in Lisbon and “Foodhallen”

its highest level for 15 years on the Côte d’Azur, a strong increase in in Amsterdam.

the number of foreign visitors in Bordeaux… For several months,

• Large refurbishment projects remain numerous. They constitute

macro-economic indicators have been green in the largest regional

both new establishment solutions for brands, as well as an important

cities, supporting the dynamism of their retail property markets.

opportunity for large cities to regenerate and strengthen their retail offer.

• This vigour first and foremost benefits the best retail pitches, where Following the Grand Hôtel Dieu, inaugurated at the end of April in Lyon,

several flagship stores have recently opened or are expected, for recent news was dominated by the progress of the mixed-use

example Primark in Toulouse and Strasbourg, Uniqlo in Rennes, “Iconic” project in Nice and the call for proposals undertaken within

Toulouse and Nantes, and Zara in Vieux Lille. Certain large mass- the scope of the transformation of the Palais du Commerce in

market brands are also continuing to move their pawns into smaller Rennes.

towns, for example the recent opening of H&M in Vannes and the

• Finally, certain projects related to the vacating of large areas seen in

future opening of a Swedish brand by 2019 in Agen.

recent years in town centres are being implemented, for example, the

• Like in Paris, mass-market fashion brands are also helping to animate upcoming launch of the marketing of the former Galeries Lafayette

the market through their transfers. JD Sports has thus just taken two building in Marseille, and the CDAC authorisation that has been

former H&M shops on rue de la République in Lyon and avenue Jean obtained for the creation of 5,000 m² of retail in Bordeaux’s former

Médecin in Nice. Other sectors, other than sport, are also Virgin Megastore.

supporting activity in regional retail streets, such as beauty (L’Oréal

• The stabilising of prime rental values seen in 2017 has been

in Lyon, Rituals in Rouen, etc.), decoration (AMPM in Lille, Sarah

confirmed since the start of 2018. Lyon and Bordeaux show the highest

Lavoine in Bordeaux, etc.), and the urban format of brands who are

rental values (€ 2,500 /sq m/year, sometimes more, for the best

more typically found in out-of-town locations (Truffaut in Toulouse,

locations). Nice completes the podium. Other regional capitals, such as

Boulanger “Le Comptoir” in Rouen, H&H in Lyon, etc.).

Strasbourg and Toulouse, follow with rental values of between €2,000

• The restaurant sector also remains very active, like the new and 2,200 /sq m/year, levels that have been seen for several years

openings of successful brands (Big Mamma in Lille, after Five Guys and now.

Big Fernand) and the growth in “food hall” projects (“Halle Bocca” in

Bordeaux, the former “Halles Alstom” in Nantes, etc.). These formats

21FRENCH RETAIL PROPERTY MARKET

HIGH STREETS | REGIONS

Significant arrivals

Examples of openings and recent projects in the regions

Source: Knight Frank LILLE

Zara / Zara Home

ROUEN AMPM

Rituals Boggi

Tiger Big Mamma

Boulanger

RENNES

Uniqlo

Nespresso AMIENS

Mauboussin STRASBOURG

Courir Primark

Hugo Boss

VANNES

Starbucks

H&M

Samsonite

NANTES LYON

Uniqlo JD Sports

COS L’Oréal

Superdry Ba&sh GRENOBLE

Bensimon / Home Kujten Hema

BORDEAUX

Former Virgin Megastore

Lalique NICE

Sarah Lavoine JD Sports

Balibaris Sœur

Cities in the Top 10 French AGEN

urban areas H&M

CANNES

Sneakers Specialist

TOULOUSE AIX / MARSEILLE Akris

Other cities Primark Five Guys Dolce & Gabbana

Uniqlo Philipp Plein Oysho

Truffaut Scotch & Soda Seafolly

22FRENCH RETAIL PROPERTY MARKET

HIGH STREETS | REGIONS

Stabilising of rental values

In the regions, end Q2 2018, in €/sq m/year Zone A*

Source: Knight Frank

Lyon 2,200 / 2,500

Bordeaux 2,200 / 2,400

Nice 2,200 / 2,400

Lille 1,800 / 2,000

Toulouse 1,800 / 2,000

Strasbourg 1,800 / 2,000

Marseille 1,500 / 1,700

Nantes 1,400 / 1,600

€0 € 500 € 1,000 € 1,500 € 2,000 € 2,500 € 3,000

*Rental value: decapitalised rent + assignment (leasehold/business)

23The rental market Retail complexes

FRENCH RETAIL PROPERTY MARKET

SHOPPING CENTRES

Opening up

Market trends in the French shopping centre market

• Several new centres opened during the 1st half of diversity also enables the loss of impetus of TOP 10 of the largest French

2018 (“Le Prado” in Marseille, “B’Est” in Lorraine, certain traditional players in the shopping centre shopping centres

“Grand Hôtel Dieu” in Lyon). However, the market to be compensated. As such, fashion Area in thousands of m²

dominant trend remains that of a slowdown of continues with arbitrations, assigning certain shops

new creations to the benefit of improvements to whilst at the same time opening large flagship

existing centres, as recently demonstrated by the stores. Vélizy 2 106

launch of some significant extension and/or

• This trend first and foremost benefits the most Mondeville 2 108

renovation projects (“Les Trois Fontaines” in Cergy,

visited regional shopping centres, which remain the

“Créteil Soleil”, “Italik” in Paris, etc.).

main target of international brands and the Rosny 2 112

• Whilst the different types of centres (retail galleries, most upmarket players. Among the most

regional centres, city-centre shopping centres) are significant movements, Galeries Lafayette has Grand Littoral 119

not all impacted in the same way, all operators are just made the opening of a new shop in

Parly 2 123

making an effort to renew the supply. Beaugrenelle official, following the recent opening

of shops in Prado in Marseille and in the Carré Créteil Soleil

• Shopping centres have thus entered a new era, 125

Sénart extension.

that of an opening up of centres that was

Carré Sénart 130

needed by a model weakened by the rise in e- • The latest changes in the shopping centre market

commerce, new consumer expectations and the also show the desire to open shopping centres La Part-Dieu 132

requirements of brands looking to reduce their up to their surroundings: through the

costs and increase their arbitrations. development of hybrid concepts (“Open Sky”) but Les 4 Temps 139

also by developing activities without a direct

• This opening up is expressed through a wider Belle Epine 141

connection to the retail function (coworking areas,

variety of supply, with the welcoming of new

medical centres, etc.).

brands from the high street or out-of-town

locations, the more frequent resorting to kiosks and • Finally, emphasis is placed on the digital,

temporary boutiques, and a growing share of sport, notably with the aim of providing a seamless Centres located in the Paris region

leisure and restaurant brands. In reply to the shopping experience.

changes in buying behaviour, this wider range of Source: LSA

25FRENCH RETAIL PROPERTY MARKET

SHOPPING CENTRES

A busy 1st half of 2018

Examples of significant shopping centre openings and projects

Source: Knight Frank

2018

Share of shopping centre creations

Centre Town Type Area (m²)

in France

B’Est Farebersviller (57) Creation 55,000 As a % of the total volume of openings

Le Prado Marseille (13) Creation 23,000 2018

Leclerc Baleone Sarrola-Carcopino (2A) Creation 18,000

Grand Hôtel Dieu Lyon (69) Creation 17,000

La Lézarde Montivilliers (76) Extension 15,000

38% 40%

Shop’In Houssen Colmar (68) Extension 5,200

2017

Note: pink box= projects already opened

2019

Centre Town Type Area (m²)

Lillenium Lille (59) Creation 56,000

Open Sky Plaisir (78) Redevelopment 37,000

Creations

Cap 3000 Saint-Laurent-du-Var (06) Extension 32,500

Vélizy 2 Vélizy-Villacoublay (78) Extension 19,970

Italik Paris (75013) Extension 7,000 Sources: Knight Frank, CNCC

Les Berges de l’Ourcq Les Pavillons-sous-Bois (93) Creation 6,800 26FRENCH RETAIL PROPERTY MARKET

RETAIL PARKS

Practicality, proximity, profitability…and quality

Trends in the French retail park market

• Following 480,000 m² in 2017, almost 200,000 m² discount stores continue to expand and take Year-on-year change in T/O of

specialist retail

has already been opened since the start of 2018, advantage of, notably, transfers undertaken by

Accumulation January-May 2018

including some large, regional projects (“Les other brands. Stokomani and Centrakor recently

Océanides” near Bordeaux, “Cap Saran” near took over several Fly shops. Furthermore, Gifi is

Orléans, “Frunshopping” in south Nancy etc.). about to take over Besson Chaussures, having

Several complexes ˃ 10,000 m² will open in the 2nd bought Tati a few months ago. Town centre Out-of-town

0

half of the year, including “PAC de Chalezeule”

• That being said, out-of-town locations are not

-3.5

-3.2

-2.2

-2.6

-1.9

-4

close to Besançon and “L’Aren’Park” in Cergy. -0.5

retail’s poor sibling. Fashion, for example, is more

-1

• In 2019, some large scale projects are expected, present than previously, with a wider range of

such as “Steel” in Saint-Étienne and the “Puisoz” formats and levels. This is also the case with sport -1.5

site in Vénissieux, near Lyon. which, at the same time as the expansion of the -2

usual suspects (Intersport) or tests undertaken by

• Contrasting with the slowdown in developments of -2.5

new brands (JD Sports), is seeing the number of

new shopping centres, the pace of creation of retail -3

gym implantations multiplying (Basic Fit, Fitness

parks remains sustained. Size and flexibility of the -3.5

Park, etc.); a success that is indicative of the

premises, ease of access and parking, occupancy

growing position more generally given to -4

costs noticeably lower than those of other retail

leisure, whose new concepts continue to -4.5

formats: the model meets the practicality and

expand, for example, the “B’Fun” space that

proximity requirements of the ever increasing

recently opened in Farébersviller to complete the City centre including:

number of suburban consumers, as well as the

offer in the “B’Est” shopping cetre. Shops in shopping centres

profitability logic of brands.

High street shops

• Finally, food and restaurant brands are also more

• The good value for money of out-of-town formats,

present, driven by the boom in franchising and the Out of town including :

and their success with consumers, explains the

desire of brands to create dedicated hubs which Shops in shopping centres

broadening demand of a growing number of brands.

have a wider and more qualitative offer. Large & medium size units

Low cost brands admittedly continue to make up the

DNA of the retail park market. Bazaars and

Source: Procos

27FRENCH RETAIL PROPERTY MARKET

RETAIL PARKS

A sustained pace of development

Examples of significant retail park openings and projects

Source: Knight Frank

2018

Centre Town Type Area (m²) Share of retail park creations in France

As a %, out of the total volume of

Les Promenades de Brétigny Brétigny-sur-Orge (91) Creation 49,000 openings

La Sucrerie Abbeville (80) Creation 30,000

2018

Cap Saran Saran (45) Creation 29,200

Frunshopping Nancy Sud Saint-Nicolas-de-Port (54) Creation 23,000

Les Océanides La Teste-de-Buch (33) Creation 22,000

Aren’Park Cergy-Pontoise (95) Creation 20,000

2017

Note: pink box= projects already opened

2019

81%

73%

Centre Town Type Area (m²)

Steel Saint-Étienne (42) Creation 70,000

Puisoz Vénissieux (69) Creation 50,000

Creations

Wood Shop Cesson (77) Redevelopment 42,000

Eden 2 Servon (77) Creation 35,000

Shopping Promenade Arles (13) Creation 19,000 Sources: Knight Frank, CNCC

Frunshopping Fourmies Fourmies (59) Creation 13,000 28FRENCH RETAIL PROPERTY MARKET

DESIGNER OUTLETS

More and more sought after

Trends in the French designer outlet market

• With a stock totalling more than 500,000 m² that is • In spite of the specific features of this distribution Gross lettable area worldwide

mainly located in the north of the country, designer format, France still has a relatively significant For 1,000 inhabitants, in m²

outlets only account for a limited share of the development potential, in certain regions with

retail market in France. little current stock in particular, and owing to the

success of the format with consumers.

• In recent years, projects have continued to multiply. Germany 1

As such, almost 150,000 m² have opened since • Furthermore, a growing number of brands are

the start of the 2010s, including approximately expanding their presence within designer outlet Poland 2.5

35,000 m² in 2017 with the extension of Romans- centres, such as department stores (Galeries

sur-Isère and the opening of two new centres: Lafayette), and several brands of accessible luxury

France 4.1

“Honfleur Normandy Outlet” and “McArthurGlen (The Kooples, the SMCP group, Zadig & Voltaire,

Provence” in Miramas close to Marseille. etc.). Others are opening their first shop, for

example, Rituals in ”Villefontaine”. Spain 4.4

• The 1st half of 2018 saw the opening of “The

Village” in Villefontaine, near Lyon. With an area • Indeed, designer outlets have reinvented Italy 7.6

of 25,000 m², this new designer outlet, developed themselves and now better fit the needs of

by Compagnie de Phalsbourg, has some 80 consumers and brands. They thus offer a more

Portugal 7.8

brands including Galeries Lafayette who have thought out buying environment and architecture,

almost 1,500 m². as well as more diversified and more upmarket

concepts, very different to the first factory outlet UK 13.9

• The pace of development of new designer outlet

centres of the 1980s.

centres shouldn’t weaken. As such, almost

USA 20.8

180,000 m² could potentially be completed by

2021. Some will supplement stock in regions that

already have some (the Greater Paris Region with

“City Outlets Paris” in Romainville). Others will be Source: Neinver/ICSC

the 1st opening, for example “Viaduc Village” in La

Cavalerie, in Aveyron.

29FRENCH RETAIL PROPERTY MARKET

DESIGNER OUTLETS

Some projects…and a lot of uncertainty

Examples of significant designer outlet openings and projects

Source: Knight Frank

Opening Centre Town Type Area (m²)

2011 Nailloux Outlet Village Nailloux (31) Creation 24,800

Change in openings in France

In m², total volume per year*

2012 The Style Outlets Roppenheim (67) Creation 27,300

2013 One Nation Paris Les-Clayes-sous-Bois (78) Creation 24,000

70000

2015 Marques Avenue A13 Aubergenville (78) Redevelopment 13,700

60000

2017 Honfleur Normandy Outlet Honfleur Creation 12,700

50000

2017 McArthurGlen Provence Miramas Creation 25,000

40000

Opening Centre Town Type Area (m²)

30000

2018 The Village Villefontaine (38) Creation 25,000

20000

2019 Viaduc Village (Phase 1) La Cavalerie (12) Creation 7,500

2019 L’Escale Hautmont (59) Creation 19,900 10000

2019 City Outlets Paris Romainville (93) Creation 20,000 0

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

2021

2020 Village des Alpes Châtillon-en-Michaille (01) Creation 16,000

2021 Village de marques Coutras (33) Creation 13,000

Source: Knight Frank

2021 Village de marques Sorigny (37) Creation 20,000 *Definite and potential projects

Note: pink box= projects already opened 30The investment market

FRENCH RETAIL PROPERTY MARKET

INVESTMENT MARKET

H1 2018 H1 2017 TREND

Retail investment volume in France €1.6 billion €1.3 billion

Share of retail* 14% 16%

Number of transactions > €100 million 4 3

Share of Ile-de-France** 53% 52%

Share of foreign investors** 55% 30%

Prime yield | High streets 2.75% 2.75%

Prime yield | Shopping centres 4.25% 3.75%

Prime yield | Retail parks 5.00% 4.75%

Source: Knight Frank

* On total investment in France,all asset types – excluding non divisible portfolios.

** On total retail investment in France.

32FRENCH RETAIL PROPERTY MARKET

INVESTMENT MARKET

A deceptive increase

Change in retail investment volumes

In France

Source: Knight Frank

€ 30,000 35%

30%

€ 25,000

25%

€ 20,000

20%

€ 15,000

+23%

14%

15%

€ 10,000 In one year

10%

€ 5,000

5%

€ 1,560

€0 0%

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 1S

2018

Investment volume in France Retail investment volume in France Retail share (%)

• Almost 1.6 billion euros were invested in the French retail market during the 1st half of 2018, equating to 14% of total corporate real estate

volume, and an increase of 23% year-on-year. This increase is deceptive because it is due to one exceptional deal undertaken by Hines, for

BVK, of the future Apple Store on the Champs-Elysées for almost 600 million euros.

• Retail activity remains limited by the imbalance between available supply and investor demand, whose selective nature has increased and is

now widespread across all asset classes.

33FRENCH RETAIL PROPERTY MARKET

INVESTMENT MARKET

Paris accounts for almost half of volume

Geographic breakdown of retail investment volumes

In France

Source: Knight Frank TOP 3 | Deals in H1 2018*

Regions Paris / IDF

H1 2018

114 Champs-El.

Grand Vitrolles

3%

9%

24%

277 Saint-Honoré

Paris

Ste-Catherine

Promenade

47% Ile-de-France (excl. Inner Paris)

44% 2017

Regions

13%

Non-divisible portfolios

54%

St-Priest Retail Park

Lutèce portfolio

6%

Source: Knight Frank

*Excl. Non-divisible portfolios

• The sale to Hines, for BVK, of the future Apple Store on the Champs-Élysées inflated the share of investment volume in the capital since the start

of 2018. Furthermore, Paris concentrates almost a third of the total number of deals recorded in France.

• Following an already slow start to the year, investment volumes in the regions were relatively low during the 2nd quarter and, with the

exception of part of the Promenade Saint-Catherine, were mainly for the sale of retail parks and brand portfolios.

34FRENCH RETAIL PROPERTY MARKET

INVESTMENT MARKET

High streets increase their domination

Breakdown of retail investment volumes by asset type

In France

Source: Knight Frank

100%

15%

90%

80% 37%

20%

70%

60%

50% 27%

40%

65%

30%

65%

20% 36% Share of high street retail in H1

2018 investment volume in

10% France

0%

2010 2011 2012 2013 2014 2015 2016 2017 1S 2018

High streets Retail warehousing Shopping centres

• Inflated by the sale of 114 Champs-Elysées, high street investment volumes accounted for 65% of retail investment volumes. Other

significant deals were mainly for Parisian assets. In the regions, the 1st half of 2018 saw the transfer of part of “Promenade Sainte-Catherine” in

Bordeaux by Redevco within the scope of the start of the Urban Retail Ventures fund formed with PGGM. Other large sales are expected, such as

that of “65 Croisette” in Cannes, for which a sale commitment has just been signed.

• Retail parks take second place due to some sales of individual assets of more than 20 million euros, but also due to the sale of brand portfolios.

The shopping centre market, on the other hand, remains subdued. 35FRENCH RETAIL PROPERTY MARKET

INVESTMENT MARKET

Examples of significant retail investment deals in H1 2018

Source: Knight Frank

Address Type City Seller Purchaser Price

Apple Store | 114 Champs-Élysées HS Paris 8 EPI Hines (BVK)

Grand Vitrolles SC Vitrolles Klépierre / CNP Carmila

Promenade Sainte-Catherine* HS Bordeaux Redevco PGGM

& Other Stories | 277 rue St-Honoré HS Paris 8 Private Private

Lutèce portfolio | 46 assets HS Paris Generali Groupe Madar Apple Store, Paris Champs-Élysées

Retail Park RW Saint-Priest - ImocomPartners

Ermenegildo Zegna | 50 rue du Fbg St-Honoré HS Paris 8 - BMO Rep

H&M, Desigual | 45-55 rue St-Jean HS Nancy Vastned UBS

Hypermarché Géant SC Pessac Groupe Casino Tristan Capital Partners

Jardiland portfolio RW France Covivio Inter Gestion

Les Grands Philambins RW Chasseneuil-du-Poitou - ImocomPartners

Léon de Bruxelles portfolio RW France AEW Ciloger Sofidy Retail Park, Saint-Priest

ZAC Benoît Hure HS Bagnolet Vinci immo Heracles

Portfolio | 8 assets HS France Family Office F&A Asset Management

Les Portes de Gayant RW Flers-en-Escrebieux Marne & Finance Midi 2i / Duval

ZAC de la Haie Passart RW Brie-Comte-Robert - Perial

Place des Fêtes HS Paris 19 Duval Private

26 rue de Rivoli / 19 rue du Roi de Sicile HS Paris 4 - Fiducial

JD Sports | 29 rue Saint Ferréol HS Marseille Vastned Voisin

45-55 rue Saint-Jean, Nancy

*Transfer of part of “Promenade Sainte-Catherine” in Bordeaux by Redevco within the scope of the start of the Urban Retail Ventures fund formed with PGGM.

< €20M €20-50M €50-100M > €100M Note: HS high street, RW retail warehousing, SC shopping centre

36FRENCH RETAIL PROPERTY MARKET

INVESTMENT MARKET

French investors declining Insurers / Mutual funds in the lead

Retail investment volumes by nationality Retail investment volumes by investor type

In France, as at 1st half 2018 In France, as at 1st half 2018

Source: Knight Frank Source: Knight Frank

4% 1%

3% 12%

4% Insurers / Mutual funds

France

SCPI / OPCI

12% 39%

Eurozone

Property investment

45% companies

Europe (outside Eurozone) Funds

North America Private investors / Family

12% Office

44%

Others Others

24%

• French investors only accounted for 45% of retail investment volume, a share that is clearly down compared to the 1st quarter (71 %) due to a

limited number of deals and the acquisition of 114 avenue des Champs-Elysées on behalf of the German BVK fund.

• This same deal explains the increase in volumes invested by insurers/mutual funds, which accounted for the largest share of activity (39%),

ahead of SCPI / OPCIs (24%) and property companies (12%).

37FRENCH RETAIL PROPERTY MARKET

INVESTMENT MARKET

New upward pressure

Prime retail yields

In France, as a %

Source: Knight Frank

10.00

9.00

8.00

7.00

6.00

5.00 5.00

4.25 High street

4.00

Regional shopping centres

3.00 Retail parks

2.75

2.00

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

Q2

• With the exception of the best ground floor retail locations (2.75%), yields in the retail market saw new upward pressure, bearing witness to the

increased prudence of investors with regard to off-prime and secondary locations, and even prime locations that do not offer all guarantees with

regard to return.

38Antoine Grignon

Partner | Head of Retail Capital Markets & Leasing

+33 (0)1 43 16 88 70

+33 (0)6 73 86 11 02

antoine.grignon@fr.knightfrank.com

Antoine Salmon

Partner | Head of Retail Leasing

+33 (0)1 43 16 88 64 Contacts

+33 (0)6 09 17 81 76

antoine.salmon@fr.knightfrank.com

Vianney d’Ersu David Bourla

Partner | Retail Leasing Partner | Chief Economist & Head of Research

+33 (0)1 43 16 56 04 +33 (0)1 43 16 55 75

+33 (0)6 75 26 03 96 +33 (0)7 84 07 94 96

vianney.dersu@fr.knightfrank.com david.bourla@fr.knightfrank.com

39You can also read