Robinhood and Gamestop: a cautionary tale - Initio

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Robinhood and Gamestop:

a cautionary tale

Laurens Verelst – Renaud Joseph

INITIO Groupe Square

Contents

Introduction ......................................................................................................... 2

The players........................................................................................................ 2

The bet ............................................................................................................. 2

The consequences .............................................................................................. 3

Last update ....................................................................................................... 3

The future ......................................................................................................... 3

Appendix 1: List of potential targets for short-sellers (Feb 12, 2021) ........................ 5

Appendix 2: GME - short volume (Jan 26 – March 03, 2021) .................................... 8

About the author ................................................................................................... 8

About Initio .......................................................................................................... 9

Contact ............................................................................................................. 9

Initio Belgium ................................................................................................. 9

1

Introduction

In our previous article (“Robinhood, a force to be reckoned with”, December 2020) we

briefly talked about a growing group of amateur traders disrupting long-standing norms in

capital markets. We concluded that these traders could have a significant impact on the

behavior of small cap stocks and warned short sellers of what we called the “Robinhood

effect”. This phenomenon was again at play last month with the short-squeeze of

GameStop, and the ensuing trading halt unilaterally decided by the discount online broker.

The players

All the elements required to provoke the explosive situation that made the headlines in

the news. First of all, a company with a failing business model. GameStop (GME), a listed

company renting video games through a network of physical stores was a perfect

candidate at a time where pandemic restrictions and online gaming are the norm. At the

time of the bet, GME’s decreasing expected earnings were correctly reflected in its falling

stock price. Second, Melvin Capital, a powerful hedge fund, one of whose strategies is to

bet against such distressed companies by massively short-selling its stocks. Third, Citadel

Securities, a market-maker which Robinhood uses to route and execute trades on their

behalf on the market. Lastly, a group of Redditors 1, passionate about financial bets and

determined to counter the plans of the biggest market players, by instigating a coordinated

purchase of a company such as GME. Finally, Robinhood, a low-cost US brokerage app

targeted at millennials which makes the connection between the 3 aforementioned players.

The bet

The story begins when a group of wannabe traders led in this case by a Reddit well-known

member and deep value investor decided to poke fun at short-sellers in the market and

collectively invest their “game” money into a failing company. If there was some rationality

behind this particular bet, it would be the onboarding of Ryan Cohen on the board of

directors of GameStop. Cohen was the former CEO of Chewy - a very successful online

company selling pet toys and accessories - who gave credibility to the promise of turning

GME into an e-commerce giant. However, in this case most of the frenzy probably arose

from enthusiastic posts on subreddit r/ WallStreetBets stirring the forum members into

pumping a cheap stock for the pure fun of it. The group of Redditors directed their purchase

at GameStop, so as to counter short-sellers in the market, in this case Melvin Capital, a

hedge fund who took the opposite side of the bet.

How does this work? Short sellers look at a company’s fundamentals, try to correctly

identify companies on the verge of bankruptcy and then bet against those companies on

the market. They do this by borrowing shares, which they immediately sell on the open

market hoping to buy these shares back later at a lower price before returning them to

the borrower. In the GameStop story, this bet went fantastically south for the hedge fund

when GME’s stock price was multiplied by a factor of five in just a few days. At this time,

the short-seller starts to feel “squeezed” because his cost of borrowing is going up

drastically. Indeed, shorting a stock is not free, the short-seller needs to borrow the shares

from a broker at a cost. As the company’s stock price increases, the seller’s exposure

increases and the borrower pressures to get his stocks back. The borrowing cost increases

further and further as the stock price goes up and the short-seller has to post even more

collateral. This could ultimately force him to close his short position by buying back the

stock at an inflated price with the direct consequence of pushing the stock price even

higher.

However, in this specific case, most Redditors did not buy GME stock directly but call-

options on the stock, which tremendously magnified the effect of the short squeeze (this

is called a “gamma trap” in the financial jargon).

1

Reddit is a social news aggregation, web content rating, and discussion website. Users

of this social network are called Redditors.

2At the end of the day, Melvin Capital and other big short-sellers lost around $20 billion

with this particular trade.

The consequences

To understand the consequences of this story we first need to understand the rules of the

game. The business model of Robinhood is quite simple: they make money by routing

transactions originated in its platform to large brokerage companies who then compensate

Robinhood for the additional trading volume. The larger the number of trades, the better

for Robinhood. Moreover, the discount trading firm also allows its customers to use

leverage by offering them to leverage up to two times the amount of equity on their trading

account. This lending operation is also a source of money for Robinhood, but forces the

company to comply with additional margin requirements.

As we explained before, this frantic buy of a thinly traded stock like GME indeed caused

intense volatility on the market and increased activity on the Robinhood app. At some

point, Robinhood was thus required by the NSCC (National Securities Clearing Corporation)

to post an additional $3 billion collateral in its margin account to hedge against potential

default. At that time Robinhood took the decision to halt all trading on GME stock, with

the goal of removing these volatile stocks off its balance sheet thereby reducing the

company’s overall risk exposure. In addition, the company drew on a line a credit from six

different banks to meet higher margin or lending requirements.

This halt on trading prevented a lot of willing investors to buy or sell certain securities via

the Robinhood app, among which GME stocks. This led to a loud revolt against Robinhood

in the news and online forums, accusing the platform to protect hedge funds by restricting

trading. Some investors even filed class-action lawsuits against the discount-broker for

violating its fiduciary obligations towards its clients.

Last update

Last week, the share price of GameStop surged again. Opening at just under $45 last

Wednesday, GME rose by 50% during the day, and even reached $170 on Thursday. It is

still not clear why such a rally happened. One possible explanation is the recent company

announcement that Ryan Cohen, who is a major shareholder in GameStop, an activist

investor and a well-known Redditor, joined the company’s board to speed up the retailer’s

transition towards a digital model of video games distribution. This news along with a

mysterious tweet from Cohen could have signaled the new bullish sentiment for GME’s

share price. Then the buying frenzy resumed as followers of the stock and r/WallStreetBets

Redditors encouraged others to buy and hold GME, in the hope that they could secure

again a hefty return, given how famously well the share did last time around (at least

before the crash). The extra volatility in GME and other stocks led to outages on Reddit

platform and periodic trading halts by the New York Stock Exchange. Robinhood

commented that this would impact all brokerages, but that it had not paused trading.

The future

This raises some important questions for the current business model of the asset

management industry and the way banks and asset managers will conduct business and

approach customers in the future.

The first set of questions will be directed towards the necessity to enlarge the scope of

companies targeted by stricter transparency requirements to all market players, including

online brokers. In the present case, Robinhood was indeed already charged by the SEC in

the past for misleading customers about its revenue sources and failing to satisfy their

duty of best execution. The payment for order flow model was not advertised to clients

either. Furthermore, if the possibility of a unilateral trading halt was indeed disclosed in

3Robinhood’s terms and conditions 2, it left quite a bitter aftertaste in many investors’

mouths at the time of the decision. This calls for greater clarity around the wording used

in the contract, and the way one could formally “agree” on the terms and conditions.

Second, we need to balance the advantage for the end-client to enjoy a cheap and

convenient way to access markets from the comfort of their home with the necessity to

protect the retail investors sometimes against themselves. By allowing its users to

leverage their trades and by failing to test their knowledge and experience in complex

financial products such as options, Robinhood was encouraging unknowing customers to

engage in risky trades. By contrast in the EU, MiFID regulation imposes those clients to fill

out appropriateness tests before being granted access to these complex products. On one

dramatic occasion this led to the suicide of one young Robinhood user who incorrectly

believed he was losing a large amount of money on one trade involving a call option. The

company’s aggressive marketing of options will probably fall under the regulator’s spotlight

in the coming months, and probably be one additional element in the legal investigation

of this case.

Third, the conflict of interest. As mentioned earlier Robinhood’s business model relies on

payment for order flow. This creates a conflict of interest between the broker and its clients

because it incentivizes the broker to execute its clients’ orders with counterparties based

solely on their willingness to pay commissions. In this respect, trading options is even

more lucrative for these companies than trading classical equities: as options are traded

less frequently, there is a larger bid-ask spread for these kinds of securities, and thus a

larger potential profit for the broker. By directing trades orders exclusively to Citadel,

Robinhood allowed a situation where Citadel could front-run trades i.e., know which trades

will be executed and act accordingly. In essence, Citadel was thus buying information from

Robinhood to inform on their own trades. Meanwhile in Europe this payment for order flow

model and its inherent conflict of interest is clearly limited under MiFID II regulation:

“MiFID II also limits the possibility for brokers to receive any remuneration, discount or

non-monetary benefit for routing client orders to execution venues, there is a clear onus

on firms to ensure that the execution quality achievable at a venue is the driver for sending

client orders to such a venue – and not any payment for order flow.”3

Lastly, this cautionary tale also illustrates the unprecedented and intricate connections

between social networks and market finance. If the cross-incentives between Citadel and

Robinhood pose questions, should we also consider such “pump and dump” game played

by bored Redditors as market manipulation?

Whether big incumbent players like it or not, the trend to diversify savings into discount-

online brokers is here to stay, and it challenges the way future relationships between

clients, brokers and companies will be established in a world where the classical trusted

intermediary is disappearing.

2

Robinhood’s terms and conditions document reads (p.11) : “Robinhood may, in its

discretion, prohibit or restrict the trading of securities, or the substitution of securities”,

https://cdn.robinhood.com/assets/robinhood/legal/Customer%20Agreement.pdf

3

ESMA, 2016 Global Capital Markets Conference. Perspective from the Buyside,

December 2016.

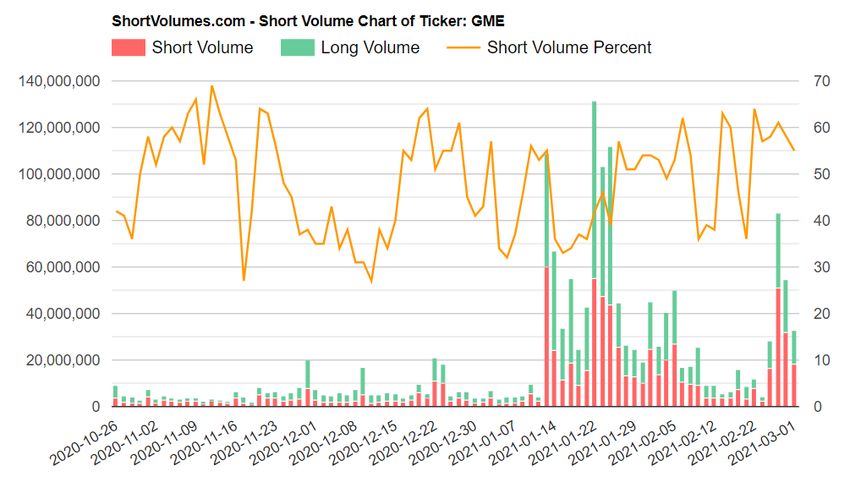

4Appendix 1: List of potential targets for short-sellers (Feb 12,

2021)

As we mentioned, being a company with an obsolete business model, a thinly traded low-

price stock, and a high short-interest, GME was only one of the potential targets for a

short-seller. As a means of illustration, we display below a list of the top 50 companies

with short interest higher than 20%, an indicator of companies which could suffer the

same fate as GameStop.

Ticker Company Exchange Short Float Outstanding Industry

Interest shares

GME GameStop Corp. NYSE 41.95% 51.03M 69.75M Retail (Technology)

SKT Tanger Factory NYSE 40.86% 90.14M 93.47M Real Estate

Outlet Centers Operations

ISUN iSun Inc Nasdaq 39.72% 1.70M 5.31M Renewable Energy

Equipment &

Services

LGND Ligand Nasdaq 38.91% 15.34M 16.08M Biotechnology &

Pharmaceuticals Drugs

Inc.

KOSS Koss Nasdaq 38.16% 1.98M 7.62M Household

Corporation Electronics

TRIT Triterras Inc Nasdaq 37.73% 23.25M 83.20M Fintech

GSX GSX Techedu Inc NYSE 36.31% 128.58M 128.69M Personal Services

CLVS Clovis Oncology Nasdaq 35.78% 80.68M 103.20M Biotechnology &

Inc Drugs

FIZZ National Nasdaq 34.91% 11.65M 46.65M Non-Alcoholic

Beverage Corp. Beverages

AXDX Accelerate Nasdaq 34.73% 30.82M 57.03M Scientific & Technical

Diagnostics Inc Instruments

GOGO Gogo Inc Nasdaq 33.49% 33.26M 85.25M Communications

Services

SPWR SunPower Nasdaq 31.93% 80.92M 170.16M Semiconductors

Corporation

OTRK Ontrak, Inc. Nasdaq 31.91% 7.41M 17.42M Healthcare Facilities

LAZR Luminar Nasdaq 31.35% 34.38M 218.82M Electronic Equipment

Technologies Inc & Parts

5RKT Rocket NYSE 31.33% 112.90M 100.37M Consumer Lending

Companies Inc

TR Tootsie Roll NYSE 31.10% 16.11M 39.34M Food Processing

Industries, Inc.

PGEN Precigen, Inc Nasdaq 30.28% 78.76M 178.60M Biotechnology &

Medical Research

SRG Seritage Growth NYSE 28.26% 34.27M 38.64M Real Estate

Properties Operations

VXRT Vaxart Inc Nasdaq 28.20% 108.76M 109.47M Biotechnology &

Medical Research

BBBY Bed Bath & Nasdaq 27.78% 114.36M 126.01M Retail (Specialty

Beyond Inc. Non-Apparel)

REV Revlon Inc NYSE 27.64% 6.81M 53.33M Personal & Household

Products

RVP Retractable AMEX 26.89% 14.48M 33.82M Medical Equipment,

Technologies, Supplies &

Inc. Distribution

PETS Petmed Express Nasdaq 26.63% 19.59M 20.27M Retail (Drugs)

Inc

MDGL Madrigal Nasdaq 26.06% 10.10M 15.44M Biotechnology &

Pharmaceuticals Medical Research

Inc

APT Alpha Pro Tech, AMEX 25.72% 11.53M 13.58M Medical Equipment,

Ltd. Supplies &

Distribution

BLNK Blink Charging Nasdaq 25.54% 34.06M 35.95M Utilities - Electric

Co

VTVT vTv Nasdaq 25.39% 12.96M 44.68M Biotechnology &

Therapeutics Inc Medical Research

OPK Opko Health Inc. Nasdaq 25.34% 404.66M 670.00M Biotechnology &

Drugs

ICPT Intercept Nasdaq 25.32% 27.50M 32.99M Biotechnology &

Pharmaceuticals Medical Research

Inc

LCI Lannett NYSE 25.11% 31.18M 41.40M Biotechnology &

Company, Inc. Drugs

SRNE Sorrento Nasdaq 24.96% 240.43M 262.94M Biotechnology &

Therapeutics Inc Medical Research

OXBR Oxbridge Re Nasdaq 24.57% 3.96M 0K Insurance -

Holdings Ltd Reinsurance

CVNA Carvana Co NYSE 24.16% 68.55M 69.43M Retail (Specialty

Non-Apparel)

6TMBR Timber AMEX 23.96% 6.41M 12.03M Biotechnology &

Pharmaceuticals Medical Research

Inc

IRBT iRobot Nasdaq 23.74% 27.47M 28.13M Electronic Equipment

Corporation & Parts

WKHS Workhorse Nasdaq 23.52% 109.72M 120.53M Auto & Truck

Group Inc Manufacturers

RUBY Rubius Nasdaq 23.40% 32.55M 80.92M Biotechnology &

Therapeutics Inc Medical Research

KNDI Kandi Nasdaq 23.29% 57.89M 72.38M Auto & Truck

Technologies Manufacturers

Group Inc

FUBO Fubotv Inc NYSE 23.20% 87.76M 67.56M Online Services

SDC SmileDirectClub Nasdaq 23.03% 91.37M 113.55M Medical Equipment,

Inc Supplies &

Distribution

RVLV Revolve Group NYSE 22.89% 25.54M 25.75M Retailers -

Inc Department Stores

SCVL Shoe Carnival, Nasdaq 22.78% 8.61M 14.10M Retailers - Apparel &

Inc. Accessories

DVAX Dynavax Nasdaq 22.76% 98.44M 110.17M Biotechnology &

Technologies Medical Research

Corporation

EBIX Ebix, Inc. Nasdaq 22.55% 25.35M 30.96M Computer Networks

TLRY Tilray Inc Nasdaq 22.48% 136.83M 158.26M Pharmaceuticals

KPTI Karyopharm Nasdaq 22.10% 64.23M 73.60M Biotechnology &

Therapeutics Inc Medical Research

INO Inovio Nasdaq 21.31% 203.25M 204.55M Biotechnology &

Pharmaceuticals Medical Research

Inc

OMER Omeros Nasdaq 21.04% 58.94M 61.65M Biotechnology &

Corporation Drugs

CEMI Chembio Nasdaq 20.89% 17.37M 20.18M Pharmaceuticals

Diagnostics Inc

BKE Buckle Inc NYSE 20.89% 29.06M 49.41M Retail (Apparel)

Source: https://www.highshortinterest.com/all/2, Feb 12, 2021.

7Appendix 2: GME - short volume (Jan 26 – March 03, 2021)

(Source: http://shortvolumes.com/?t=GME, March 2nd, 2021)

About the author

Laurens Verelst joined Initio in 2018 after having worked as a

financial management consultant for two years. He is a CFA level III

candidate who is passionate about everything related to the

investment management industry ranging from new trading &

investment strategies to technological advancements like robo-

advisors. He has a soft spot for fund and portfolio management and

the academical and technological advancements that could propel the

industry forward.

Maxime Liénart has over 5 years of experience in Asset Servicing

and Global Custody with roles combining both operational

coordination (orders processing and monitoring) and client knowledge

as their dedicated representative. He serviced and built a solid

relationship with a broad range of institutional investors, and

specialized more recently in the Luxembourg offshore funds industry.

8About Initio

Initio is an international business consultancy firm specialized in management and

strategy. Every day, our consultants contribute to the successful delivery of your

business projects.

Initio operates in Brussels and Luxembourg and his part of the SQUARE GROUP, an

international strategy and management consulting firm.

Contact

Initio Belgium

Boulevard General Wahislaan, 17

Brussels, 1030

Belgium

+32 (0)2 669 77 44

brussels@initio.eu

9You can also read