Schroder Real Estate Investment Trust - Interim Results Presentation - Duncan Owen, Nick Montgomery and Rick Murphy - Schroders

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Schroder Real Estate Investment Trust

Interim Results Presentation

Duncan Owen, Nick Montgomery and Rick Murphy 17 November 2020

For professional clients only. This material is not suitable for retail clients

Agenda 01 SREIT overview 02 Portfolio 03 Outlook 04 Appendix Throughout this presentation the Schroder Real Estate Investment Trust will be referred to as SREIT. 1

SREIT overview

Overview of the half year to 30 September 2020

Active asset management, strong balance sheet and capital to invest

Property Performance Financial Performance Income Focus Portfolio

Sustained real estate

NAV total return of -2.2% 84% rent collection for the

outperformance vs. MSCI

over the interim period to quarter to September Focus on regional offices

Benchmark

30 September 2020 and multi-let industrial

86% current rent collection warehousing comprising

+1.0% over interim period;

NAV total return of +1.2% for the quarter to 70% of the portfolio’s value

+1.1% over 1 year;

over quarter to 30 December

+2.0% p.a. over 3 years; and

September 2020

+1.0% p.a. since IPO in 20041

Dividend reinstated in June

Share buy-back programme

at 0.38575 pps equivalent to 25.9% net loan to value at

46 lettings, rent reviews in September and October

50% of pre-Covid level 2.25% total cost p.a.

and renewals totalling achieved average discount

£6.0m, generating an uplift of 46% to NAV

Further 50% dividend £79 million of cash and

of £2.0m p.a.2

increase announced for the undrawn debt facilities for

Buy-back programme to be

quarter to September to reinvestment

recommenced

0.575 pps

Past performance is not a guide to future performance and may not be repeated. The value of investments and the income

from them may go down as well as up and investors may not get back the amount originally invested

Source: Schroders, November 2020. 1. Source: MSCI property level returns gross of fees on a like-for-like basis including direct and indirect. 2. This includes activity post-period end.

3

Unaudited interim NAV as at 30 September 2020

Total decrease of -2.8% and a NAV total return of -2.2%

£m PPS Comments

NAV as at 31 March 2020 309.8 59.7

Unrealised decrease in the valuations

of the direct real estate portfolio and (8.4) (1.6)

Joint Ventures Like-for-like valuation movements net of capex -3.4%; by sector was Industrial -0.1%,

Offices -0.9%, Other -6.0% and Retail -10.4%

Capital expenditure (direct portfolio

(5.4) (1.0)

and share of Joint Ventures)

Realised gains on disposals Nil Nil No disposals were made during the six month period

Net revenue 5.1 1.0 EPRA earnings for the six months ended 30 September

No dividend was paid for Q1 2020. The Q2 2020 dividend paid was 50% of the target

Dividend paid (2.0) (0.4)

rate

NAV as at 30 September 2020

299.1 57.7 Reflects prior shares outstanding of 518,513,409

(excluding the share buyback)

c.7.2m shares repurchased at average of 31.6 pps at 30 September 2020

Share buyback (2.3) 0.3

c.15.2m shares repurchased at average of 32.2 pps per share including post period

NAV as at 30 September 2020 296.8 58.0 Reflects shares outstanding of 511,364,955 as at 30 September 2020

4

Income and Dividend illustration

Dividend increased to 0.575 pps to reflect positive activity

EPRA Earnings Dividend

6 months to 6 months to 12 months to – Increased dividend of 0.575 pence per

30 September 30 September 31 March share will be paid in December 2020

2020 £m 2019 £m 2020 £m relating to the period 1 July 2020 to 30

September 2020

Rental income – direct portfolio 10.3 11.8 22.2

– The dividend payment will be made on 11

December 2020 to shareholders on the

Rental income – joint ventures 1.3 1.3 2.6 register as at 27 November 2020. The ex-

dividend date will be 26 November 2020.

Other income 0.1 1.0 1.3 – The dividend of 0.575 pps will be

designated 0.575 pps as an interim

Rental and related income 11.7 14.1 26.1 property income distribution (‘PID’)

– Future dividend increases will be

Property operating expenses (1.7) (1.2) (2.3) considered dependent on further progress

with rental collection rates, acquisitions

and other earnings accretive activity

Expenses (2.6) (2.9) (5.8)

– Note: Additional future income from

Finance costs – net interest reinvestment, asset management and

(2.3) (3.3) (5.3)

payments lower number of shares

EPRA Earnings 5.1 6.7 12.7

Source: Schroders, November 2020.

5

Active strategy to deliver sustainable net income growth

Sales at 3%; refinancing; active management; reinvestment 6.5%+; buy backs

Active Asset Share Buyback

Asset Disposals Debt Refinancing Acquisitions

Management Programme

• £95m of disposals • Refinancing of • Immediate Covid-19 • Disciplined acquisition • Commenced on 8

completed in 2019 at £129.6m reduced the response focussed on strategy focused on September 2020

an average net initial cost of debt on the safety and wellbeing Winning Cities and

yield of 3.0% facility by £2.5m per of all stakeholders resilience of income

• The Company’s shares

at the prevailing price

annum, with one-off

• Disposals crystallised

break fee of £27.4m

• Continued activity • Focussed on income and discount to NAV

profits from asset with 46 new lettings, resilience and good offers attractive value

management and • Extended term to 13 renewals and reviews fundamentals for its shareholders

supported and 20 years since 31 March 2020

performance

• £60m of acquisitions • £5m of share

• Significant covenant • This activity increased at 6.5% equates to c. buybacks to date

• Further disposals of headroom contracted rental £4m of rental income added 1.4% of NAV

non-core assets will income by £2.0m p.a. accretion and

be considered

• Strong pipeline but no

improves dividend

urgency to invest due

cover

to market softening

Strong balance sheet

Reduced cost of debt Improved defensive Disciplined approach Accretive to NAV

with low LTV

qualities of the portfolio

Improved covenant Potential for c. £4m of Income saving on

Positioned to reinvest

flexibility Improved net income rental income dividend

post market correction

Past performance is not a guide to future performance and may not be repeated. The value of investments and the income from them may go down as

well as up and investors may not get back the amount originally invested.

Source: Schroders, November 2020.

6

Overview of share buyback programme

Daily average of 500,000 shares per day at average price of 32.2 pps

Price (pps)

Overview (as at 16 October 2020)

80

# shares repurchased

15.2

(m)

70

Shares outstanding

503.3

post repurchases (m) 60

Average price pps 32.2 50

40

Total investment £4.9m

30

Average discount to

-46% Lowest share price of 28.7 pps

NAV

20

NAV accretion 1.4% 10

Implied buyback yield 0

9.6% / 4.8%

(100% / 50% dividend)

Source: Schroders, November 2020.

7

UK real estate market overview

Polarisation accelerating across the sectors

MSCI all property index – capital value

% age change – month-on-month (average – bars; range1 – drop-down lines) and cumulative from end 2015 (line)

SDLT increase EU referendum

6% 6%

Industrial sector Industrial sector Industrial sector

5% 5%

4% 4%

3% 3%

2% 2%

1% 1%

0% 0%

-1% -1%

-2% -2%

-3% -3%

-4% -4%

-5% -5%

-6% Retail sector Retail sector -6%

-7% -7%

Dec

Dec

Sept

Dec

Dec

Feb

Sept

Oct

Oct

Sept

Oct

Sept

Oct

Sept

Jul

May

Jul

Jul

Jul

2016 Jan

Mar

May

Jun

Mar

May

Mar

Jun

Mar

May

Jun

May

Jun

Apr

2017 Jan

Nov

Feb

Apr

2018 Jan

Nov

Feb

Apr

2019 Jan

Nov

Feb

Apr

2020 Jan

Mar

Nov

Feb

Apr

Aug

July

June

Aug

Aug

Aug

Aug

Monthly change Range Cumulative

Source: MSCI as at 30 September 2020; 1Range shows highest and lowest change across 10 segments: Standard retail SE and rest UK; Shopping centres; Retail warehouses; Offices City, West

End/Midtown, rest SE and rest UK; Industrial SE and RUK; other.

8Portfolio

COVID-19: Rent collection and deferrals

86% of September quarter date rent currently collected

Rent collection overview (September quarter) Case-by-case approach to tenant deferment requests

Rent demanded by sector (%) Income impact Capital impact %1

Other Office

Negative short

term

Rent deferment Neutral 41

96% 94% Neutral medium

4% term

27%

40% Lease extension in Negative short

Positive 30

return for rent free term

86%

Remove break in Negative short

Positive 8

return for rent free term

Retail &

Industrial

Leisure

29%

60% 99%

Other structural Negative short

Positive 21

deal term

Rent collected as % of demanded rent

Source: Schroders, November 2020. 1 This analysis is illustrative of proposals both agreed and in negotiation.

10Portfolio overview

Structure vs. the MSCI Benchmark

SREIT MSCI Structure as a % of value post disposals

30/09/2020 30/09/2020

Office - City 0.0

Portfolio value (£m) 397.8 -

3.7

9.5

Number of properties 39 - Office - Mid and West End

7.6

7.3

Net initial yield (%) 5.9 4.8 Office - Rest South East

8.9

Reversionary yield (%)1 7.4 5.3 Office - Rest of UK 22.6

7.7

Rent (£m) 24.9 - 11.1

Industrial - South East

17.2

Estimated rental value (£m) 29.4 -

Industrial - Rest of UK 18.6

Unconditional contracted uplifts for the 9.8

2.7 -

next 24 months (£m) Retail - South East 0.6

8.5

Average unexpired lease term (years)2 5.6 9.7

10.0

Retail - Rest of UK

4.5

Void rate (%) 3 7.1 7.4

Retail - Shopping centre 0.0

Office weighting (%) 39.4 27.9 3.3

12.6

Retail - Warehouse

Industrial weighting (%) 29.7 26.9 9.1

Retail weighting (%) 23.2 25.4 7.7

Others

- Retail single use 17.5 - 19.7

- Retail ancillary to main use 5.7 -

0 5 10 15 20 25

Other weighting (leisure etc.) (%) 7.7 19.7

Portfolio MSCI Benchmark

1 On a like-for-like basis with MSCI i.e. ignoring acquisition costs. 2 Assuming earlier of lease break and expiry capped at 30 years. 3 % of ERV.

11Reversionary income yield of 7.4% (MSCI 5.3%)

Supporting income growth during a period of negative growth

£m

35

c.4

2.1

30 29.4

2.7 1.0

-1.3

24.9

25

Uplift

Top five fixed uplifts Timing

£k p.a.

20 University of Law (London) +416 Jan-21

Lidl (Bedford) +335 Jun-21

BBC Scotland (Edinburgh) +191 Dec-20

Home Bargains (Bedford) +190 Jun-21

Quentor (Norwich) +181 Dec-20

15

Contracted Fixed uplifts next ERV growth Vacant space Overrent ERV New acquisitions

income as at 30 24 months income of

Sep 2020 c.£60m at 6.5%

Source: Schroders, Knight Frank, September 2020. New acquisition income shown for illustrative purposes

12Asset management overview

High quality assets let at sustainable rents with income growth potential

Milton Keynes, Stacey Bushes Leeds, Millshaw London, Bloomsbury, Store Street

(Industrial) (Industrial) (Office; 50% Share)

– 345,000 sq ft multi-let industrial estate – 460,000 sq ft multi-let industrial estate – 85,814 sq ft freehold office and

comprising of 42 units comprising of 27 units educational campus across 0.8 acres

– 10 lettings, renewals and reviews – 6 lettings, renewals and reviews – Rent review with the University of Law

completed generating additional completed generating additional completed post period end

net rent of £225,000 p.a. vs. Mar-20 net rent of £130,000 p.a. vs. Mar-20 – New rent of £1.85m p.a. or £42 per

– Sustainable average rent of £6.25 per – Sustainable average rent of £5.75 per sq ft delivering a £415,500 increase

sq ft vs. average ERV of £7.00 per sq ft sq ft vs. average ERV of £6.50 per sq ft – The Company will receive £326,708 of

– Heathfield Gateway development – Progressing change of use strategy back rent and the tenant has received

completed comprising six units of with completion of the JD Sport Gyms a three month rent free period

circa 15,000 sq ft. Terms out on five unit that adds amenity to the estate – Improving location due to mix of uses,

units at £14.00 per sq ft. – Working with the adjoining land ‘Camden Project’ and infrastructure

– Potential to acquire further adjoining owner to promote a new station to – The new rent reflects a yield of 4.9%

ownerships service the location based on the valuation

Multi-let industrial Multi-let industrial Redevelopment opportunity

Source: Schroders, November 2020.

13Asset management overview (2)

Mixed use and retail assets with sustainable rents in urban locations

Manchester, City Tower Leeds, Headingley Central Bedford, St. John’s Retail Park

(Office / Mixed-use; 25% share) (Retail / Mixed-use) (Retail Warehouse)

– 610,000 sq ft of office, retail, leisure – 90,000 sq ft convenience retail, 98- – 130,000 sq ft retail warehouse scheme

and hotel accommodation on a three room hotel and gym scheme let to 11 tenants with two vacant units

acre island site in the heart of – Top tenants by income are Premier – Lidl and Home Bargains letting

Manchester Inn, Sainsbury’s, The Gym (AFL) and completed generating £525,000 p.a.

– 6 lettings, renewals and reviews Boots. Average rent on retail units rent with higher footfall forecast

completed generating additional reflects c. £50 per sq ft Zone A rents across the scheme

net rent of £130,000 p.a. vs. Mar-20 – Recent asset management includes – 10 year letting to Easy Bathrooms at

– Offering short term ‘plug-and-play’ converting office space into new gym, £22 per sq ft and re-gear with Curry's

leases to achieve premium to ERV lease renewals with William H Brown PC World for 10 years

– Sustainability and public realm and BHF, re-gear with Market Town – Average rent of £17.25 per sq ft with

improvements are a focus. Achieved a Taverns and Heavenly Desserts letting average ERV of £16.20 per sq ft.

BREEAM In Use certification of ‘Good’ – Potential to increase food retail use – Valuation reflects c.7% yield on expiry

for Part 2 Building Management of Lidl and Home Bargains rent free

Winning City Mixed-use convenience-led Value retail warehousing

Source: Schroders, November 2020.

14Sustainable investing

Sustainable and Impact Investing central to approach

– Focussed on ESG and ‘positive impact’ investing to generate

ISAP Case Study:

improved returns, contribute to tenants’ business

performance and create tangible benefits to communities City Tower, Manchester

– ESG and Impact integrated in asset management processes: Community & Social Impact

– Acting responsibly during Covid-19 pandemic – Residencies for local start-ups and charities in the City

Tower pop-up shop

– Signatory to BBP Climate Change Commitment

– Dedicated occupier engagement portal to promote City

– Energy audits undertaken to identify asset opportunities Tower specific events and provide discounts and reduced

fees to local shops, restaurants and gyms

– LED lighting and Automatic Metering programmes

– EV charging installation programme Energy & Waste Management

– 99.5% landlord procured electricity on renewable tariff; – Energy management strategy being implemented

5% fall in like-for-like landlord procured energy in 2019 following building-wide metering audit

– Impact and sustainability action plans (‘ISAP’) for major – Re-negotiated waste management contract to improve

refurbishments initiated with the aim of industry recycling, occupier engagement to reduce plastics and

building awareness of waste reduction at work and home

sustainability accreditations

– Key recent achievements include: Green & Active Transport

– Three star rating in 2019 GRESB survey with 16% scoring – Two onsite dedicated cycle storage areas

improvement. 2020 results expected shortly

– New ‘VeloZone’ with increased cycle storage with drying

– EPRA Best Practice Sustainability Reporting Gold Award room, showers and changing facilities

for the year end accounts

Health & Wellbeing

– BREEAM In Use Certification: ‘Good’ Rating at The Arc,

Nottingham and City Tower, Manchester; ‘Very Good’ at – Health and well-being programme which includes

Cheltenham exercise classes three times per week and on-line yoga

15 Source: Schroders, November 2020.Summary

Summary

Strong balance sheet provides investment capacity to grow net income

– Sales of £95 million of assets at an Investment Capacity

average net initial yield of 3.0% in

2019 £ (million)

£52.5m £79m Acquisitions

80

– Refinancing to lower debt cost and at 6.5% NIY

extend term

70 c.£4m

– 25.9% net loan to value and £79 (Non- rental

million of cash and undrawn debt 60 utilisation income

facilities fee of 0.64%

50 with margin

– Reinvestment to generate of 1.6%)

additional c. £4 million of rental Share buy

40 backs

income, with strong pipeline of c.£65

opportunities million

30 £27m NAV and

to invest

– Share buy backs to increase NAV income

and increase dividend cover accretive

20

– Active management to capture

10

£4.5 million of reversion, of which

£2.7 million is fixed contractual Asset

uplifts 0 management

Cash 30-Sep-20 RCF facility Cash for activity to

– Review dividend each quarter as investment capture

reinvestment occurs and asset reversion

management delivers

Source: Schroders, November 2020. Note activity and additional income are shown for illustrative purposes only.

17Management update from July 2020

No change day to day

RNS ANNOUNCEMENT UPDATE ON THE INVESTMENT MANAGER

The Board of Schroder Real Estate Investment Trust (‘’SREIT’’), the actively managed UK-focused REIT, has

been notified that Duncan Owen, SREIT’s Fund Manager since IPO in 2004, has decided to step down from

his role as Global Head of Real Estate at Schroders REIM (‘’SREIM’’). Duncan Owen will remain at SREIM as

Global Head of Real Estate until 31st December 2020.

From 1st January 2021 Duncan will become a special advisor to SREIM with a focus on SREIT. This will mean

he will continue to work closely with the Board and the existing team including Nick Montgomery, assisting

Schroders in fulfilling its role as the appointed investment manager. SREIT’s investment strategy and

objectives remain unchanged. The board of Schroder Real Estate Investment Trust will continue to monitor

the position closely.

Source: Schroders, July 2020.

18Appendices

SREIT portfolio performance to 30 September 2020

Higher income return and asset management generating relative outperformance

Six Month Total Return Three Year Total Return Since IPO Total Return *

1.0% relative outperformance 2.0% relative outperformance p.a. 1.0% relative outperformance p.a.

(%) 4.0 (%) 7.0 (%) 10.0

Total Return Income Return

6.0

8.0

5.0

2.0

4.0 6.0

3.0 4.0

0.0

2.0

2.0

1.0

-2.0 0.0 0.0

SREIT MSCI Benchmark SREIT MSCI Benchmark SREIT MSCI Benchmark

MSCI sector/total return SREIT total return MSCI Index total return Relative

Six Three Six Three Six Three

Since IPO* Since IPO* Since IPO*

To 30 September 2020 months years months years months years

(% p.a.) (% p.a.) (% p.a.)

(%) (% p.a.) (%) (% p.a.) (%) (% p.a.)

Offices 1.7 5.9 7.9 -0.5 4.3 7.3 2.2 1.5 0.6

Industrial 2.8 14.2 9.4 2.2 10.6 8.6 0.6 3.2 0.8

Retail -6.0 -4.6 3.8 -5.1 -4.5 3.4 -0.9 -0.1 0.4

Other commercial -8.7 -1.6 2.2 -1.8 4.5 7.5 -7.0 -5.9 -4.9

All -0.3 5.0 7.1 -1.3 2.9 6.0 1.0 2.0 1.0

Past performance is not a guide to future performance and may not be repeated. The value of investments and the income from them may go down as

well as up and investors may not get back the amount originally invested.

Source: MSCI property level returns gross of fees on a like-for-like basis including direct and indirect property investments. *IPO in July 2004.

20Compliance Disclosure Requirement

Schroder Real Estate Investment Trust – discrete yearly performance

12 months to 12 months to 12 months to 12 months to 12 months to

Discrete Yearly Performance (%)

Sep-2020 Sep-2019 Sep-2018 Sep-2017 Sep-2016

Share Price -39.5 -3.2 1.4 11.9 2.7

SREIT NAV Total Returns -12.6 2.8 8.9 11.8 4.4

SREIT Real Estate Total Returns -1.1 5.4 11.0 12.2 6.6

MSCI UK Balanced Monthly and Quarterly

-2.3 2.7 8.6 9.8 4.4

Funds Quarterly Property Index

Past performance is not a guide to future performance and may not be repeated. The value of investments and the income from them may go down as

well as up and investors may not get back the amounts originally invested.

Schroder Real Estate Investment Trust – Risk Considerations:

Investments in real estate are relatively illiquid and more difficult to realise than equities or bonds. Yields may vary and are not guaranteed. The use of

gearing is likely to lead to volatility in the Net Asset Value (‘NAV’) meaning that a relatively small movement either down or up in the value of the

Company’s total assets will result in a magnified movement in the same direction of that NAV. There is no guarantee that the market price of shares in

Investment Companies such as SREIT will fully reflect their underlying NAV. The value of real estate is a matter of a valuer’s opinion rather than fact.

The trust may be concentrated in a limited number of geographic regions, industry sectors, markets and/or individual positions. This may result in large

changes in the value of the fund, both up or down, which may adversely impact the performance of the funds.

The Company may borrow money to invest in further investments, this is known as gearing. Gearing will increase returns if the value of the assets

purchased increase in value by more than the cost of borrowing, or reduce returns if they fail to do so.

Source: Property portfolio level returns. MSCI September 2020.

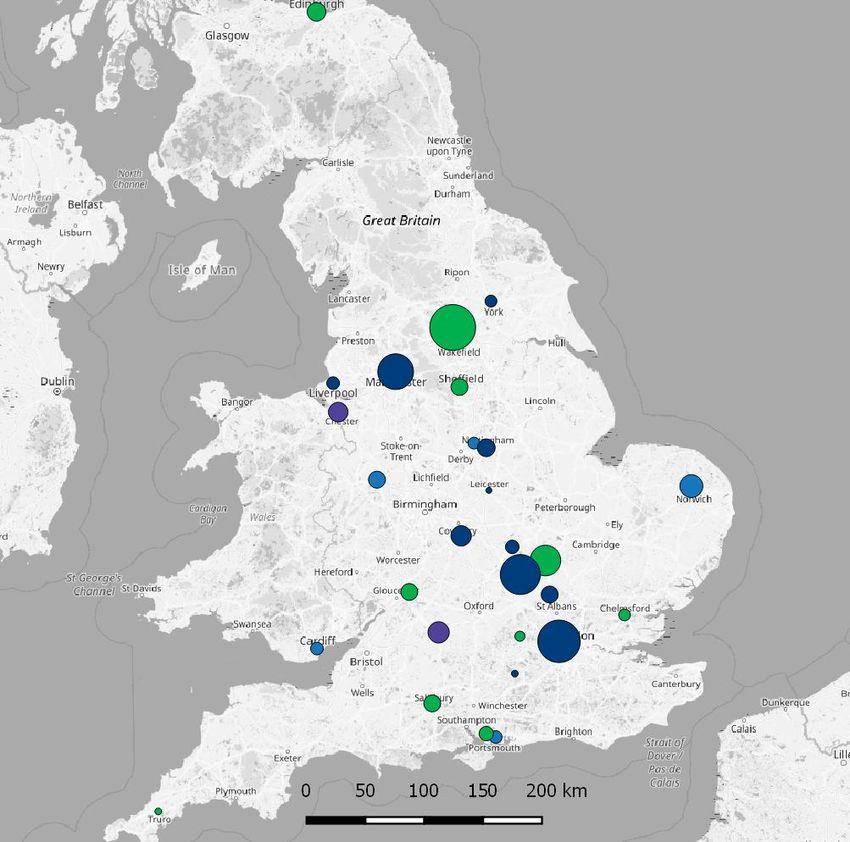

2186% of the portfolio located in higher growth locations

% of SREIT Capital Value

3%

11%

11%

15%

% of UK

51% 49%

GDP

37% 23%

Fastest growing centres Second quartile

Third quartile Slowest growing centres

Source: Oxford Economics, Schroders November 2020. Note: Size of the bubbles represents capital values as at 30 September 2020. The colours are where the cities and towns are within

the four quartiles of GDP growth between 2020 and 2025. For illustrative purposes only and should not be viewed as a recommendation to buy or sell. Forecast risk warning: Please refer to

the important information slide at the end of this presentation.

22Overview of SREIT income at 30 September 2020

Diversified income base with 294 tenants across a range of sectors

Top 20 Tenants % by industry2

Rent p.a.

# Tenant

(£m)

% Portfolio

3% 1%

3% 19%

1 University of Law Limited 1.58 6.1 4%

2 Buckinghamshire New University 1.15 4.4

4%

3 The Secretary of State 0.73 2.8

4 Cineworld Cinema Properties Limited 0.58 2.2

5%

5 Matalan Retail 0.57 2.2

6 Express Bi Folding Doors 0.53 2.0 14%

7 TJX UK Limited T/A Homesense 0.51 1.9 5%

8 Jupiter Hotels Limited T/A Mercure 0.46 1.8

9 SportsDirect.com Retail Limited 0.46 1.7 7%

10 Premier Inn Hotels Limited 0.42 1.6

11 Lidl Great Britain Limited

1

0.42 1.6 11%

9%

12 Geldards LLP 0.41 1.6

13 Wickes Building Supplies Limited 0.40 1.5

11%

14 Morgan Sindall Construction 0.38 1.4 Retail Non-Food Manufacturing Education

15 Lloyds Banking Group 0.35 1.3

Business Services Leisure Other Industries

16 Tulip Limited 0.34 1.3

17 Jaguar Land Rover Limited 0.33 1.3 Retail Food Public Sector Wholesale

18 Higher Education Statistics Agency Limited 0.32 1.2 Construction Financial IT

19 Sennheiser UK Limited 0.30 1.2

Transport Other Services Healthcare

20 Smyths Toys UK Limited 0.30 1.1

Sub-total top 20 tenants 10.55 40.3

Utilities Charity

Source: Schroders, MSCI, October 2020. 1 This includes agreement for lease at St John’s Retail Park, Bedford. For illustrative purposes only and should not be viewed as

a recommendation to buy or sell. 2 This data is as at 30 September 2020. Post period end rent review settled that increased University of Law rent to £2m p.a. or 7.5%

23Reinvestment overview

No urgency to reinvest. Focus on resilience of income

Winning Cities Active Management Potential

+

Differentiated economy Secondary Prime

Grade A

Building quality

Infrastructure

Employment

Secondary

Tertiary

Grade B

Environment -

- Income quality +

Sector Focus Target Metrics

• Multi-let industrial acquired below

replacement cost Asset value Net Initial Yield Timing

Industrial

• Regional offices • Potential as part of

Strong fundamental mixed-use building or

£10-30m 6%+ 2020/21

•

Office

Retail

occupational demand where valuation

• Active management

Mixed-use supported by

to capture alternative use

reversionary potential • Mispriced assets

Other Sep-20: £10.2 million Sep-20: portfolio net

average initial yield of 5.9%

Past performance is not a guide to future performance and may not be repeated. The value of investments and the

• Creating rather than buying income from them may go down as well as up and investors may not get back the amounts originally invested.

Source: Schroders, November 2020.

24Results for the six month period to 30 September 2020 Key metrics Period to 30 September 2020 30 September 2019 % change (Loss)/Profit for the period (£8.8m) £4.6m -291% EPRA1 earnings £5.1m £6.7m -23% EPRA1 earnings per share £1.0p £1.3p -23% Dividend per share paid £0.39p £1.3p -70% As at 30 September 2020 30 September 2019 % change Net Asset Value £296.8m £354.3m -16% Net Asset Value per share (pence) 58.0 68.3 -15% Property valuation2 £397.8m £456.2m -13% Loan to Value, net of cash 25.9% 23.1% -12% Past performance is not a guide to future performance and may not be repeated. The value of investments and the income from them may go down as well as up and investors may not get back the amounts originally invested. Source: Schroders. 1European Public Real Estate Association (“EPRA”) earnings calculated as total comprehensive net income (i.e. after fund expenses and finance costs) excluding realised and unrealised gains/losses on investment property and share of profit on joint venture investments. 2Independent valuers’ valuation of property and joint ventures.. 25

Balance sheet

Summary Balance Sheet (£m)

30 September 2020 31 March 2020 30 September 2019

As at

£million £million £million

Investment properties 1 388.3 397.0 409.1

Cash 78.7 33.1 23.3

Net current assets 11.2 8.4 49.3

Debt (181.4) (128.7) (127.4)

Net Asset Value 296.8 309.8 354.3

NAV (pence per share) 58.0p 59.7p 68.3p

Loan to Value (%) 25.9% 23.7% 23.1%

Past performance is not a guide to future performance and may not be repeated. The value of investments and the income from them may go down as

well as up and investors may not get back the amounts originally invested.

Source: Schroders as at November 2020. 1 Excludes leasehold interests grossed up under IFRS 16.

26Underlying EPRA profitability

24% reduction in underlying profit

£ (million)

10

6.7

1.3 5.1

5

(1.5)

(0.9)

(0.5)

0

HY 2019 Rental income Other income Property expenses Expenses HY 2020

Past performance is not a guide to future performance and may not be repeated. The value of investments and the income from them may go down as

well as up and investors may not get back the amounts originally invested.

Source: Schroders, November 2020.

27Profit bridge

HY 2020 vs. HY 2019

£m Sep-20 Sep-19 £m Sep-20 Sep-19

£ £ (million)

Profit on sale Valuation

15 - £1.5 (£13.9m) (£3.6m)

of properties (Loss)/Gain*

10

4.6m (1.6m)

5

(1.5m)

(10.3m)

(8.8m)

0

-5

-10

HY 2019 Net rental income Profit on disposal of Valuation loss* HY 2020

investments

Past performance is not a guide to future performance and may not be repeated. The value of investments and the

income from them may go down as well as up and investors may not get back the amounts originally invested.

Source: Schroders, November 2020. *Properties and Joint Ventures.

28Statement of comprehensive income

30 September 30 September 31 March

2020 £m 2019 £m 2020 £m

Rental income – direct portfolio 10.3 11.8 22.2

Rental income – joint ventures 1.3 1.3 2.6

Other income 0.1 1.0 1.3

Property operating expenses (1.7) (1.2) (2.2)

Net rental and related income 10.0 12.9 23.9

Profit on disposal of investment property - 1.5 1.9

Net valuation (loss)/gain on investment property (13.5) (3.5) (17.4)

Expenses (2.6) (2.9) (5.8)

Refinancing costs - - (27.4)

Finance costs – net interest payments (2.3) (3.3) (5.3)

Joint venture (loss)/gains (0.4) (0.1) (2.4)

(Loss)/Profit before tax (8.8) 4.6 (32.5)

Ongoing charges – fund only expenses 1.3% 1.4% 1.4%

Ongoing charges – fund and property expenses 2.5% 2.3% 2.3%

Past performance is not a guide to future performance and may not be repeated. The value of investments and the income from them may go down as

well as up and investors may not get back the amounts originally invested.

Source: Schroders as at November 2020.

29EPRA earnings

Earnings excluding property revaluations, gains on disposals and non-recurring expenditure

30 September 30 September 31 March 2020

2020 2019 £m

Year to

£m £m

(Loss)/Profit after tax (8.8) 4.6 (32.5)

Excluding:

Profit on disposal of investment property - (1.5) (1.9)

Net valuation (loss)/gain on investment property 13.5 3.5 17.3

Joint venture (gains)/loss 0.4 0.1 2.4

Refinancing costs - - 27.4

EPRA earnings 5.1 6.7 12.7

Weighted average number of shares 518,056,505 518,513,409 518,513,409

EPRA earnings per share (pence) 1.0 1.3 2.5

Past performance is not a guide to future performance and may not be repeated. The value of investments and the income from them may go down as

well as up and investors may not get back the amounts originally invested.

Source: Schroders, November 2020.

30Balance sheet overview

Net LTV of 25.9%

– The Company has two debt facilities – a £129.6 million long term fixed loan and a £52.5 million revolving credit facility –

providing operational flexibility. The table below is as at 30 September 2020:

Lender Loan Maturity Total interest Assets Value Loan to Value LTV ratio Interest cover ICR ratio

(£m) 1 rate (%) (£m) ratio (%)2 covenant (%)2 ratio (%)3 covenant (%)3

Canada Life 129.6 50%: 15/10/2032 2.5 4 254.1 51.0 65 359 185

(43.8 net of

50%: 15/10/2039

cash in facility)

RBS 52.55 03/07/2023 1.7 6 104.8 50.1 65 7 871 185

– The Company’s consolidated net loan to value is 25.9% as at 30 September 2020

– Total debt £182.1 million, portfolio value of £397.8 million and cash of £78.9 million

– The Company’s target leverage range is 25-35%

– The debt facilities are secured against the Company’s assets. The Company retains uncharged properties valued at £38.9

million as at 30 September 2020

Source: Schroders as at September 2020. 1 Balance as at 30 September 2020.

2 Loan to Value (‘LTV’) is the loan balance divided by the property value as at 30 June 2020.

3 For the quarter preceding the Interest Payment Date (‘IPD’), ((rental income received – void rates, void service charge and void insurance)/interest paid). In addition,

there is a forward ICR covenant of for the four quarters following the IPD (rental income to be received void rates, void service charge and void insurance)/interest

paid).

4 Fixed total interest rate for the loan term.

5 Facility drawn at 30 June 2020 from a total facility of £52.5 million.

6 Total interest rate as at 30 June 2020 comprising 3 months LIBOR of 0.14% and the margin of 1.6% at an LTV below 60% and a margin of 1.90% above 60% LTV.

7 This covenant drops to 60% after year three of the five-year term.

31£129.6 million Canada Life Loan

Two main covenant tests which are closely monitored by the Manager

– The Canada Life security pool comprises of 32 assets valued at £254.1 million, with the metrics below as at 30 September 2020

Loan to Value (‘LTV’) Interest Cover Ratio (‘ICR’)

As at 30 September 2020 Actual from quarter to September 2020

Loan (£m) 129.6 Rent (£m) £3.3m

Portfolio Value (£m) 254.1 Non-recoverable Costs (£m) (£0.4m)

Gross Loan to Value (%) 51.0% Net Rent (£m) £2.9m

Cash held in Facility (£m) 18.3 Interest (£m) £0.8m

Net Loan to Value (%) 43.8% Interest Cover Ratio (%) 359%

Covenant (%) 65% Covenant (%) 185%

– Net Loan to Value on the secured assets against this loan is 43.8%. On this basis, a decline of 33% in the property value could be sustained

prior to the 65% covenant being breached

– The ICR is 359% based on actual net rents. A 48% fall in net income could be sustained prior to 185% covenant being breached. Assuming

25% non-recoverable costs in addition to rental declines, this equates to 34% rent decline

– The Company has additional flexibility to add cash and assets to the facility to further improve cover against loan covenants

Source: Schroders as at November 2020.

32Important Information Marketing material for professional clients only. Past performance is not a guide to future performance and may not be repeated. The value of investments and the income from them may go down as well as up and investors may not get back the amount originally invested. Exchange rate changes may cause the value of any overseas investments to rise or fall. Schroders has expressed its own views and opinions in this document and these may change. This information is not an offer, solicitation or recommendation to buy or sell any financial instrument or to adopt any investment strategy. Nothing in this material should be construed as advice or a recommendation to buy or sell. Information herein is believed to be reliable but we do not warrant its completeness or accuracy. Any data has been sourced by us and is provided without any warranties of any kind. It should be independently verified before further publication or use. Third party data is owned or licenced by the data provider and may not be reproduced, extracted or used for any other purpose without the data provider’s consent. Neither we, nor the data provider, will have any liability in connection with the third party data. The material is not intended to provide, and should not be relied on for accounting, legal or tax advice. Reliance should not be placed on any views or information in the material when taking individual investment and/or strategic decisions. No responsibility can be accepted for error of fact or opinion. Any references to securities, sectors, regions and/or countries are for illustrative purposes only. Schroders will be a data controller in respect of your personal data. For information on how Schroders might process your personal data, please view our Privacy Policy available at www.schroders.com/en/privacy-policy or on request should you not have access to this webpage. The forecasts stated in the presentation are the result of statistical modelling, based on a number of assumptions. Forecasts are subject to a high level of uncertainty regarding future economic, and market factors that may affect actual future performance. The forecasts are provided to you for information purposes as at today's date. Our assumptions may change materially with changes in underlying assumptions that may occur, among other things, as economic and market conditions change. We assume no obligation to provide you with updates or changes to this data as assumptions, economic and market conditions, models or other matters change Schroder Real Estate Investment Trust (‘SREIT’) is a real estate investment company with a premium listing on the Official List of the UK Listing Authority and whose shares are traded on the Main Market of the London Stock Exchange. On 1 May 2015 SREIT converted to UK-REIT status. SREIT continues to be an authorised closed ended investment scheme registered in Guernsey with number 41959. Registered office: Royal Bank Place, Glategny Esplanade, St Peter Port, Guernsey GY1 2HS 33

Important Information (continued) Risk considerations of The Real Estate Investment Trust Investments in real estate are relatively illiquid and more difficult to realise than equities or bonds. Yields may vary and are not guaranteed. The use of gearing is likely to lead to volatility in the Net Asset Value (‘NAV’) meaning that a relatively small movement either down or up in the value of the Company’s total assets will result in a magnified movement in the same direction of that NAV. There is no guarantee that the market price of shares in Investment Companies such as SREIT will fully reflect their underlying NAV. The value of real estate is a matter of a valuer’s opinion rather than fact. The trust may be concentrated in a limited number of geographic regions, industry sectors, markets and/or individual positions. This may result in large changes in the value of the fund, both up or down, which may adversely impact the performance of the funds. The Company may borrow money to invest in further investments, this is known as gearing. Gearing will increase returns if the value of the assets purchased increase in value by more than the cost of borrowing, or reduce returns if they fail to do so. Use of MSCI data and indices: © and database right MSCI and its Licensors 2013. All rights reserved. IPD has no liability to any person for any losses, damages, costs or expenses suffered as a result of any use of or reliance on any of the information which may be attributed to it For your security, communications may be recorded or monitored. Issued in November 2020 by Schroder Real Estate Investment Management Limited, 1 London Wall Place, London EC2Y 5AU. Schroder Real Estate Investment Management Limited is authorised and regulated by the Financial Conduct Authority. Registration number 1188240 England. UP000206 34

Contact Duncan Owen, Nick Montgomery, Rick Murphy Schroder Real Estate Investment Management Limited, 1 London Wall Place, London EC2Y 5AU. schroders.com

You can also read