Shopping our way into economic recovery - Colmar Brunton

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Shopping our way

into economic

recovery

A R E V I E W O F N Z R E TA I L D U R I N G C O V I D - 1 9

During COVID-19 lockdown in NZ we

set out to understand how Kiwis are

changing the way they engage with

retail, and what opportunities this could

hold for NZ brands, manufacturers and

retailers. This report showcases our

findings and insights.

RESULTS FROM

MAY / JUNE 2020

Did COVID-19 lockdown trigger an e-commerce revolution? Females of all ages were most likely to have shopped online during COVID-19 lockdown (82%), while 55+ year old males were less likely to have done so.

Did COVID-19 trigger Do you plan to shop online in the

coming months?

an e-commerce

NO YES – Same

revolution? 23% amount as now

65%

In June nearly 4 in 5 New Zealanders had

shopped online during the month, and the

same intended on doing so in the future. NETT YES

77%

Have You Shopped Or Ordered Anything

Online In The Last Month?

YES –

Increasingly so

12%

of kiwis

ordered

In June 77% of Kiwis planned to continue or

something increase the amount of online shopping they

online in the were doing.

past month

Kiwis aged 24-44 years, full-time employees were

most likely to engage with e-commerce

consistently, while males aged 25-34 years and

Asian ethnicities were most likely to lead the way in

increasing their e-commerce engagement.

Females of all ages were most likely to have

shopped online recently (82%), while 55+ year old

males were less likely to have done so.

Interestingly, consumers in the South Island,

specifically outside of Christchurch, saw the

highest rate of online shopping across any region.

$

COLMAR BRUNTON 2020

Some shoppers experienced issues

What are the purchasing online. Brands need to understand

who their target market is and for some there

potential barriers is a need to work harder to convince shoppers

to purchase online and provide an offline

to e-commerce? option. This is why brands need to optimize

their omnichannel strategy.

51% 18%

Preferred to look at, Worried about how 38% 6%

touch and try on things returns work

34% DELIVERY

FEE IS

NO CONVENIENT/

AFFORDABLE

Felt delivery TOO HIGH PAYMENT OPTIONS

fees are

too high

A new ‘retail frontier’ for 55+ year olds…

28% Prefer to look at, touch

59%

Felt delivery 25% and try on things

takes too long, Worried about Worried about

product quality

33%

they want things now product quality

Scared to use e-commerce

(security/privacy/ 10%

fraud concerns)

The ‘lack of tactility of the online shopping

For the 55+ age group, significantly bigger

experiences’ stood out as the biggest barrier,

barriers to this “new frontier” of e-commerce

by far.

included the lack of tactile experience, uncertainty

around product quality and concerns around safety.

Interestingly this was a significantly smaller barrier

to the 35-54 year age group. Perhaps the cohorts

Families often have to stretch budgets more than

existing experience with online shopping has

most people, and are often pressed for time in

helped to ‘normalize’ non-tactile retail

their purchases. It is no surprise that delivery fees

experiences. Instead, this group of consumers

and the wait time for purchases to arrive were

worried more about product quality and returns.

bigger barriers to e-commerce adoption for this

consumer group.

Delivery fees were one of the top concerns for

many Kiwis, with research indicating that higher Delivery fees are too high 42%

‘base prices’ (which include the delivery fee) and Delivery takes too long, we want things now 35%

an explicit offer of ‘free delivery’ was more

appealing to the consumer psyche, often resulting

in better sales conversion.

COLMAR BRUNTON 2020

How is e-commerce spending data stacking up

against this?

Online shopping saw an unprecedented year on year increase in April 2020, up almost

50% versus April of the previous year.

While shopping online, Kiwis are clearly still keen as to #supportlocal, with growth

clearly driven by ‘domestic online’ spending. This, despite overseas retailers reportedly

targeting Kiwis during lockdown.

100% Alert Level 4 60%

27th March‘20

From 1 December 2019, most overseas businesses that sell goods to Kiwi 50%

80% consumers are required to charge GST on products valued at $1000 or less** 47% 50%

60% 40%

40% 30%

20% 20%

9% 7% 9% 9% 7% 8% 8% 6%

0% 6% 5% 4% 4% 10%

-1% 1%

-20% 0%

Mar-19 Apr-19 May-19 Jun-19 Jul-19 Aug-19 Sep-19 Oct-19 Nov-19 Dec-19 Jan-20 Feb-20 Mar-20 Apr-20 May-20

-40% -10%

Monthly spending vs / Same month prior year Domestic online International online

Consumers compensated for their lack of mobility by having bigger baskets in April.

In May we saw early evidence of recovery, in June the number of transactions bounced

back and basket sizes began to normalize. Long term trends remain to be seen.

Num. of transactions (mil) Average $

160 80

140 70

120 60

100 50

80 40

60 30

40 20

20 10

0 0

Number of electronic transactions Average Value per transaction

*Source: Market View , BNZ, Stats NZ ** Source: GST Consumer COLMAR BRUNTON 2020

We observed the rise of New Zealanders ‘shop local’ sentiment. For some brands and manufacturers this could be a growth driver, for others it could pose a risk.

xx/xx groups which scored significantly higher/ lower than total

Proximity is king for

shop local Located near me

(neighbourhood/ 72%

When hearing or saying ‘shop local’ a majority area/city)

of Kiwis agreed this meant ‘their neighbourhood’ MALE, ASIAN, AUCKLAND

FEMALE, NZ PAKEHA, SOUTH ISLAND (excl CHRISTCHURCH)

or ‘close to their home’.

Small businesses stand to benefit more from

these perceptions, this means bigger brands, Products

multinational corporations or franchises have manufactured 63%

to work harder to demonstrate how they are in NZ

‘local’ too.

25-34 YEARS

It’s time to think about local or community causes

your brand can support or partner with to establish

valuable ‘local cues’.

Made by kiwis

(for kiwis)

58%

55+ YEARS; 18-34 YEARS

Made with NZ

ingredients

49%

25-34 YEARS, AUCKLAND

Brands founded/

established in NZ

46%

25-34 YEARS

“ Do your shopping in your local town instead

of online shopping.”

“ It means support the smaller companies in

NZ and in your community. Where possible

purchase their products and services.”

“ Looking at locally family owned business

selling NZ manufactured items, then looking

at NZ owned and manufactured business.”

“ Shop local to me is the local businesses in

town and also includes New Zealand made

products around the country.”

“ Supporting New Zealand businesses and

products made in Aoteoroa.”

COLMAR BRUNTON 2020

What ‘local’ means to Older age consumers were most likely to define

local as ‘being located physically close’ to them,

Kiwis differed not only perhaps because that’s what retail and commerce

by age groups, but also has been traditionally.

by location. Meanwhile consumers aged 18-34 years

(especially those below 25 years) have taken the

Kiwis in the South Island were significantly more realities of the global economy they have grown

likely to interpret ‘shop local’ as meaning places up with to heart and think that products “made by

located near to them. kiwis (for kiwis)” still count as local.

Aucklanders were significantly more likely to Brands that were established in NZ were found to

define local as “made with New Zealand be more appealing to the younger cohort, while

ingredients”, and were also the most likely to the older consumer groups thought this was not

define ‘shop local’ as “products that are enough ‘localness’.

manufactured in NZ”.

72%

58%

Auckland Total 49%

46%

54% 73%

Made with NZ

18-24 years 73%

ingredients 47%

52%

67%

Products 63%

25-34 years 65%

manufactured in NZ 58%

56%

74%

59%

35-44 years 50%

South Island 47%

80% 72%

Located near me 51% 45-54 years 42%

41%

53%

Made with NZ

ingredients

Wellington 75%

55+ 52%

46%

40%

66%

54%

Located near me (neighbourhood/area/city)

Made for kiwis Made by kiwis (for kiwis)

Brands founded / by kiwis Made with NZ ingredients

established in NZ Christchurch Brands founded/established in NZ

COLMAR BRUNTON 2020

#Support(more)Local Traditionally more local businesses

such as cafés and grocery stores are

Just under a third of New Zealanders most likely to benefit from the ‘support

said they already try to support local local’ sentiment.

where possible.

Currently support local…

A similar proportion said that they will try

to support more local in the future. Cafés 42%

Younger Kiwis were most likely to support

local more, while older Kiwis felt that they

Groceries,

were doing a lot already (less likely to Fresh Produce

40%

change future behavior).

Ready To

7% I have always tried Eat Food/ 37%

to shop local Restaurants

30% Will support local

25% NETT more

Clothing/Shoes

SUPPORT I will support a mix

/Fashion

17%

LOCAL of local, regional,

international

68% I don’t plan to Cosmetics

12% change how I shop

for or buy this

/Speciality 13%

27% Toiletries

Don’t know

However there is potential for local

clothing, shoes and fashion retailers to

be supported.

Where possible, I will try to

support more local:

Clothing/Shoes

/Fashion

29%

Groceries,

Fresh Produce

29%

Ready To

Eat Food/ 26%

Restaurants

Cafés 26%

Cosmetics/

Speciality 23%

Toiletries

COLMAR BRUNTON 2020

Does #supportlocal We observed the #supportlocal sentiment

correlating strongly to consumers’ income groups.

differ by consumer Consumers from a lower income background were

groups? significantly more likely to support local currently,

as well as showing interest in continuing doing so.

Yes it does. We found interesting behaviour

Conversely, higher income Kiwis were least likely

differences across ages and income groups.

to currently support local, although 1 in 4 said they

The 55+ age group, who defined ‘shop local’ as

would try to support more local in the future.

being located near them, were most likely to

currently support local businesses (32%), and This could give insights into the type of products

least likely to see the need to change to support and product ranges which could find a #shoplocal

more local businesses (21%). message resonate with their customer base.

Among others, job security of local employees

Meanwhile, younger consumers were most willing could be one message to embrace, to appeal to

to shift behaviour towards supporting more local these cohorts.

businesses, with almost a third (30%) of under 25

year old's saying they would support more local Nett Support local

goods and services where possible.

Below 50k

72%

CURRENT FUTURE income

I have always I will try to

tried to support support more

local/ domestic local/ domestic 50-99k

income 69%

where possible where possible

More than 100k

18-24

YEARS 32% 30% income / 66%

Prefer Not To Say

25-34

YEARS 23% 31%

35-44

YEARS 30% 27%

45-54

YEARS 27% 22%

55+

YEARS 37% 21%

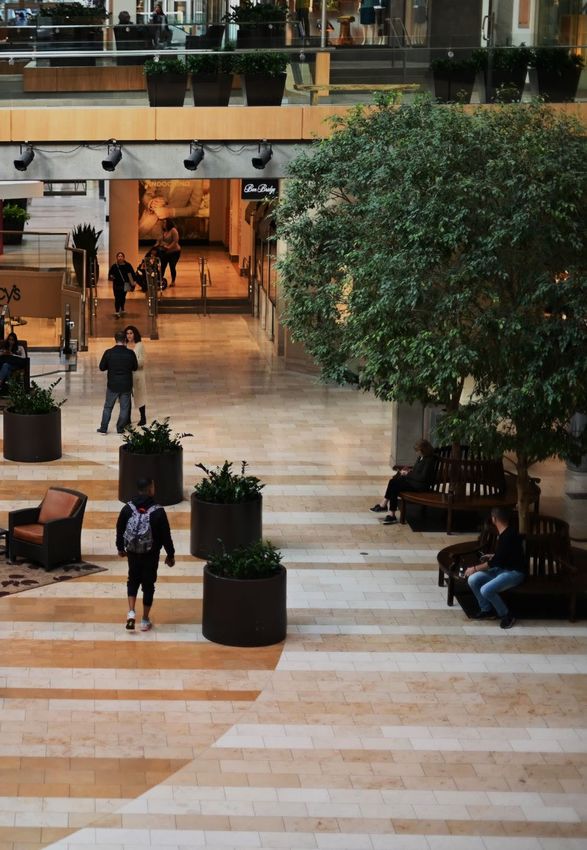

COLMAR BRUNTON 2020How has the ‘shop local’ sentiment impacted the shopping baskets of Kiwis?

In June, more than 1 in 2 Others were less likely to have recently

visited a mall, including:

New Zealanders had visited

a mall in the past month. Income under

Below 50k49.9 k

income 41%

Around 1 in 5 said they

couldn’t wait to go back Rural

Rural 33%

after lockdown levels

South Island

changed (or businesses Other SI

(excl Christchurch) 31%

re-opened). North Island

Other(excl

North island

Auckland) 42%

Visited a mall in the last month

YES NZ Pakeha ethnicity

NZ Pakeha 48%

52%

55+ Years

55+ 41%

NO

48%

Some consumers were more likely than

others to have recently visited a mall,

they included:

18-24 Years

18-24 76%

Asian Ethnicity

Asian 66%

Auckland

Auckland 64%

Christchurch

Christchurch 72%

Urban

Urban 61%

Full-timeFull

employed

time 55%

White collar

White-collar job

application 58%

Family Households

HH with family 59%

Households withkids

HH with Kids 60%

More than 100k100K+

income 56%

COLMAR BRUNTON 2020In June, there were mixed Some consumers were significantly more

likely to visit a mall soon:

intentions from consumers

about visiting malls

Don’t usually go

Can’t wait to go back Christchurch RANK 1

as soon as lockdown

there anyway

levels allow

24% 24%

18-24 Years RANK 2

Asian ethnicity RANK 3

North Island RANK 4

(excl Auckland)

Others indicated being significantly less

Won’t be going in the Not sure if I will likely to visit a mall in the coming months,

next few months go there for now they were:

18% 27%

Unemployed RANK 1

Home-makers RANK 2

Females RANK 3

55+ Years RANK 4

Wellington RANK 5

COLMAR BRUNTON 2020‘Malls’ the word Within Auckland, Sylvia Park had the most

people raring to go, followed by the three

biggest Westfields.

The locations set to benefit most from the

post-lockdown excitement of re-engaging Sylvia

Park

24%

with retail are local town shopping

centres. In June, around half of New Westfield

19%

Zealanders said they were excited to Newmarket

pop in for a visit. Westfield 17%

Albany

My Local Westfield

16%

Shopping Centre/ 48% St Lukes

Town Centre

Dressmart 16%

Onehunga

29%

27%

26%

23%

This was more pronounced in the

South Island.

52%

NORTH ISLAND

55%

SOUTH ISLAND

COLMAR BRUNTON 2020Some categories were worse-affected than

others, but there remains recovery potential for

each of them.

3,000

Spending ($Mil)

2,500

2,000

1,500

1,000

500

0

Oct 2018

Oct 2019

Feb 2019

Mar 2019

Apr 2019

Mar 2020

Apr 2020

Feb 2020

May 2018

May 2019

May 2020

Jun-20

Jul 2018

Jul 2019

Jun 2018

Jun 2019

Aug 2018

Sep 2018

Nov 2018

Dec 2018

Jan 2019

Aug 2019

Sep 2019

Nov 2019

Dec 2019

Jan 2020

Consumables Durables Apparel Hospitality

Panic buying in March 2020 resulted in a 23%

In the News

increase in consumable spending (measured via

electronic transactions) compared to the same

time last year. To put this into perspective, that

exceeds the annual spike observed for Christmas

over the last 2 years.

Due to the lockdown, durables and other products

took a nose dive over the same period. NZ was

under lockdown measures for all of April, and this

resulted in a 72% decrease in spending on

durables, a 89% decrease in spending on

apparel, and a 9% increase for consumables

versus same time last year.

NZ moved to alert level 3 on April 27th, which

saw the opening of non-essential retail stores and

shopping malls. This had a significant impact on

durables and apparel transactions. Within a

matter of weeks durables recovered to higher

than pre-Covid-19 levels (March 2020).

At the start of June apparel transactions remained

below last year’s spend, we see the resulting

closure of outlets making headlines recently.

Thus far hospitality had shown the weakest

recovery, but positive momentum had already

been made by kiwis taking it upon themselves to

drive domestic recovery in this area.

*Source: Stats NZ** Note that the YoY increase in consumable spending may also be due to more electronic

transactions in place of cash as stores encouraged the use of contactless payment like payWave as a

measure to decrease COVID spread Source: Newshub COLMAR BRUNTON 2020For more information contact Yasmin.Handrich@colmarbrunton.co.nz

You can also read