Super 101 Thank you for joining us. We will commence shortly - TelstraSuper

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

TODAY ’S TOPIC Super 101 Thank you for joining us. We will commence shortly Telstra Super Pty Ltd ABN 86 007 422 522, AFSL 236709 (Trustee) is the trustee of the Telstra Superannuation Scheme ABN 85 502 108 833 (TelstraSuper) Current as at 29 April 2021. This work is copyright and no part may be reproduced by any process without prior written permission from TelstraSuper.

IMPORTANT NOTICE

This presentation contains factual information and general advice only. It has been prepared without

taking into account your objectives, financial situation and needs. You should consider whether it is

appropriate having regard to your personal circumstances before making any financial decisions.

If you are considering acquiring a financial product you should obtain the relevant

product disclosure statement before making any decision.

The taxation information in the presentation is factual information only. If you require

taxation advice you should consult your accountant or tax adviser.

Current as at 29 April 2021. This work is copyright and no part may be reproduced by any process without prior written permission from TelstraSuper.

WHY IS SUPER CONSIDERATIONS FOR

IMPORTANT? YOUR SUPER

HOW TELSTRASUPER

QUESTIONS

CAN ASSIST

Current as at 29 April 2021. This work is copyright and no part may be reproduced by any process without prior written permission from TelstraSuper.

WHY IS SUPER

IMPORTANT?

Current as at 29 April 2021. This work is copyright and no part may be reproduced by any process without prior written permission from TelstraSuper.

W H Y I S S U P E R I M P O R T AN T ?

What are the facts?

9.5% $3 trillion

Employers are required to pay The pool of super money in

a minimum of 9.5% of your Australia is worth $3 trillion at the

salary into super end of the December 2020 quarter.

$13.8 billion

The total number of lost or unclaimed For most people super is likely to be

super across Australia totalled $13.8 their largest financial asset apart

billion as at 30 June 2020 from the family home

Source: www.superannuation.asn.au/resources/superannuation-statistics#:~:text=Superannuation%20Statistics,of%20the%20June%202020%20quarter.

www.ato.gov.au/About-ATO/Research-and-statistics/In-detail/Super-statistics/Super-accounts-data/Lost-and-unclaimed-super-by-postcode/?=banner_sup_sec_Find_Lost_super*

Current as at 29 April 2021. This work is copyright and no part may be reproduced by any process without prior written permission from TelstraSuper.

W H Y I S S U P E R I M P O R T AN T ?

Why is super a good place to invest your money?

▪ 9.5% compulsory superannuation guarantee contributions from your employer

▪ Pre-tax money you put into super is taxed at 15%

Employed ▪ Investment earnings are also taxed up to 15%

▪ After you’re 60 and you stop working, money that you withdraw is not taxed

▪ If you start a Retirement income stream, there is no tax on investment earnings

(up to the transfer balance cap limit *)

▪ You can also leave your super in your accumulation account

Retirement

You should be aware that there are limits and conditions on how much you can contribute each year.

* Subject to a $1.6 million Transfer Balance Cap that applies to retirement income streams.

Current as at 29 April 2021. This work is copyright and no part may be reproduced by any process without prior written permission from TelstraSuper.

CONSIDERATIONS

FOR YOUR SUPER

Current as at 29 April 2021. This work is copyright and no part may be reproduced by any process without prior written permission from TelstraSuper.

C O N S I D E R A TI O N S F O R Y O U R S U P E R

Insurance within super

Refer to the relevant Product Disclosure Statement and TelstraSuper insurance guide 1 March 2021 for full terms and conditions

Current as at 29 April 2021. This work is copyright and no part may be reproduced by any process without prior written permission from TelstraSuper.

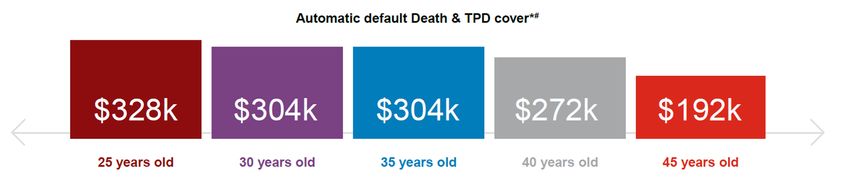

T E L S T R AS U P E R ’ S I N S U R AN C E O F F E R I N G

TelstraSuper Corporate Plus default insurance

^

Default Income Protection^

Your income protection benefit payment will be up to 75% of your salary plus 10% paid to your super

If you’re a TelstraSuper Corporate Plus Member, your default insurance cover is for Death & TPD insurance.

This is generally paid for by your employer as an employee benefit°

# If you are aged under 25 or have an account balance that is less than $6,000 you must opt in within 120 days of commencing employment to receive member paid insurance cover subject to 'At Work’ requirements. If

cover is required 120 days after joining the fund, you will need to will need to apply and be assessed by our insurer.

*Death & TPD default cover is calculated based on a salary of $80,000 p.a.

^ To be eligible for default cover in TelstraSuper Corporate Plus, you must join TelstraSuper within 120 days of commencing employment otherwise all cover is subject to application and acceptance. Income protection is not

available to casual employees.

° For many permanent full-time and part-time TelstraSuper Corporate Plus members, your Default Death & TPD Cover is currently paid by your Employer, as an employee benefit. Except for employees of Sensis (new

employees from 1 July 2014), 1300 Australia, Chief Entertainment and Telstra SNP Monitoring, Telstra Health and Telstra Purple (new employees from 1 June 2019) where premiums will be deducted from your account

quarterly in arrears or on withdrawal if you leave TelstraSuper Corporate Plus. It also excludes members who don’t have their Superannuation Guarantee (SG) contributions paid to TelstraSuper. As a casual Employee, if

you satisfy the Default Cover Conditions, you will receive an age-based level of Default Death & TPD Cover, however the premiums are not paid for by your employer.

Refer to the relevant Product Disclosure Statement and TelstraSuper insurance guide 1 March 2021 for full terms and conditions.

Current as at 29 April 2021. This work is copyright and no part may be reproduced by any process without prior written permission from TelstraSuper.

C O N S I D E R A TI O N S F O R Y O U R S U P E R

Beneficiaries

Who would you like to get your death benefit?

You can nominate one or more of your dependants or Legal personal representative to receive your death benefit. Your eligible

dependants are:

✓ Spouse Inflation

Market risk

✓ Child risk

✓ Financial dependant

✓ Interdependency relationship

✓ Legal personal representative - is the person:

• nominated by you to be the executor of your Will

• appointed to distribute your assets according to the laws of the relevant State or Territory.

Binding nomination

Non-Binding nomination

A valid binding death benefit nomination gives

you certainty about who will receive your benefit in A non-binding nomination is not binding on

the event of your death and means TelstraSuper

must pay your death benefit to the beneficiaries the Trustee of TelstraSuper. The Trustee will

nominated in the proportion set out in the nomination. take your nomination into consideration when

To be valid and in effect, the binding nomination determining to whom to pay your death benefit.

must meet all the superannuation law requirements.

Current as at 29 April 2021. This work is copyright and no part may be reproduced by any process without prior written permission from TelstraSuper.C O N S I D E R A TI O N S F O R Y O U R S U P E R

Maximising contributions

*Based on no initial balance, weekly regular deposit of $20 until age 65, an investment return of 7% p.a. net of fees, taxes and other costs, retirement age of 65. Not discounted to today’s dollars. Past

performance is not a reliable indicator of future performance. This presentation contains factual information and general advice only. It has been prepared without taking into account your objectives,

financial situation and needs. You should consider whether it is appropriate having regard to your personal circumstances before making any financial decisions.

If you are considering acquiring a financial product you should obtain the relevant product disclosure statement before making any decision.

Source: www.moneysmart.gov.au/budgeting/compound-interest-calculator

Current as at 29 April 2021. This work is copyright and no part may be reproduced by any process without prior written permission from TelstraSuper.C O N S I D E R A TI O N S F O R Y O U R S U P E R

Summary of contribution caps

Pre-tax Post-tax

(concessional contributions) (non-concessional contributions)

Employer contributions, salary sacrifice, personal deductible Contribution made from after-tax income, and

contributions, insurance premiums paid by your employer spouse contributions

15% tax rate 0% tax on the way in

Annual contribution cap $25,000† Annual contribution cap $100,000†*^

Rolling 5-year catch up Bring forward rule^#

If your total super balance is less than $500,000 as at end of the previous If your total super balance is less than $1.6 million individuals aged

financial year, any unused concessional contributions cap amounts can be under 65 may be able to make up to three years’ worth of post-tax

carried forward for up to five years before they expire. contributions (up to $300,000) to their super in a single year.

† The concessional and non-concessional contributions cap will be indexed from 1 July 2021

* For the 2020-21 financial year, you must meet the work test if aged 67 to 74 or satisfy the work test exemption criteria. To satisfy the work test you must complete at least 40 hours of paid work in a period of not

more than 30 consecutive days in the financial year in which you plan to make non-concessional contributions. The work test exemption means you can also make personal contributions during the first financial year

you don’t meet the work test if your total superannuation balance at the end of the previous financial year is less than $300,000.

^ Subject to $1.6 million total superannuation balance cap. Individuals with a total superannuation balance of $1.4 million or more are not able to utilise the full bring forward rule.

# Must be under 65 at the start of the financial year and meet other eligibility criteria.

Source: www.ato.gov.au/Rates/Key-superannuation-rates-and-thresholds/?page=3 | www.ato.gov.au/Individuals/Super/In-detail/Growing-your-super/Super-contributions---too-much-can-mean-extra-tax/?page=3

Current as at 29 April 2021. This work is copyright and no part may be reproduced by any process without prior written permission from TelstraSuper.C O N S I D E R A TI O N S F O R Y O U R S U P E R

Summary of contribution caps

Total super balance Transfer balance cap

Includes all superannuation funds Maximum amount that can be transferred from superannuation

and retirement income streams accumulation funds into the tax-free retirement phase

$1.6 million^ $1.6 million^

No further post-tax Example

(non-concessional) contributions John retires at age 62 with a total super balance of $2 million.

He is able to commence a retirement income stream with

If the total superannuation balance across all your

up to $1.6 million. John can leave the remaining $400,000

superannuation and retirement income streams (not just your in his superannuation accumulation account and access this

TelstraSuper account) is equal to or greater than $1.6 million money when needed tax-free as he has retired and reached

at the end of the previous financial year. his superannuation preservation age.

TelstraSuper Financial Planning has a team of phone-based Advisers who can provide you with simple advice in relation to your contributions. There's no additional cost

for our phone-based advice as this is included in your TelstraSuper membership. You can contact us on 1300 033 166 or request an appointment with our online contact form.

Telstra Super Financial Planning Pty Ltd (TSFP) AFSL 218705– which is wholly owned by Telstra Super Pty Ltd (TSPL).

^ The total super balance and transfer balance cap will be indexed from 1 July 2021

Source: www.ato.gov.au/Individuals/Super/In-detail/Growing-your-super/Super-contributions---too-much-can-mean-extra-tax/?page=5 | www.ato.gov.au/individuals/super/withdrawing-and-using-your-super/transfer-balance-cap/

Current as at 29 April 2021. This work is copyright and no part may be reproduced by any process without prior written permission from TelstraSuper.C O N S I D E R A TI O N S F O R Y O U R S U P E R

Consolidating accounts

There are literally billions of dollars of lost money out there and some

of it could be yours.

Every dollar counts in superannuation and holding multiple accounts

means you’re paying multiple sets of fees. Multiple super accounts

aren’t just messier with more paperwork to manage – they can eat into

your savings too.

Before consolidating your super you should:

✓ Consider the implications of consolidating your super funds (eg insurance, tax and

fees) and in particular, review any insurance cover you have within those funds in

which you are still a member, which could be impacted. If you choose to consolidate

your accounts into TelstraSuper you’ll lose any insurance cover held with your current

funds;

✓ Before consolidating your super, you should consider whether this is right for

you. Think about seeking financial advice before you make a decision to

consolidate your super.

Current as at 29 April 2021. This work is copyright and no part may be reproduced by any process without prior written permission from TelstraSuper.Y O U R TE L S T R A S U P E R F U N D

Investment choice

If we look at a high growth

fund, our objective is to earn a

high return. However, we must

also be prepared for a higher

level of volatility.

Refer to TelstraSuper’s Investment Guide dated 1 March 2021 for further information

Current as at 29 April 2021. This work is copyright and no part may be reproduced by any process without prior written permission from TelstraSuper.Y O U R TE L S T R A S U P E R F U N D

Understanding MySuper

87.5% 71.5% 35%

Growth Growth Growth

MySuper MySuper MySuper

Growth Balanced Conservative

(under 45) (45 to < 65) (65 and over)

12.5% 28.5% 65%

Defensive Defensive Defensive

Refer to TelstraSuper’s Investment Guide dated 1 March 2021 for further information

Current as at 29 April 2021. This work is copyright and no part may be reproduced by any process without prior written permission from TelstraSuper.Y O U R TE L S T R A S U P E R F U N D

TelstraSuper’s investment options

Suggested

Growth / Defensive Investment objective

Investment Option Risk of negative return investment

assets CPI

timeframe

Growth 87.5 / 12.5% + 3.5% pa 4 - 6 years in 20 7 – 10 years

Balanced 71.5 / 28.5% + 3% pa 4 - 6 years in 20 5 – 10 years

Diversified Income 54.5% / 45.5% + 2%pa 3 - 4 years in 20 4 – 6 years

Defensive Growth 54.5% / 45.5% + 2% pa 3 - 4 years in 20 4 – 6 years

Conservative 35 / 65% + 1.5% pa 1 - 2 years in 20 3 - 10 years

International Shares 100 / 0% + 3.5% pa 4 - 6 years in 20 8 - 10 years

Australian Shares 100 / 0% + 3.5% pa 6 or more years in 20 8 - 10 years

Property 57.5 / 42.5% + 3% pa 3 - 4 years in 20 5 - 7 years

Fixed interest 0 / 100% Outperform CPI 2 - 3 years in 20 4 - 6 years

Cash 0 / 100% Refer footnote* Less than 0.5 years in 20 0 - 2 years

*The Cash option investment objective is to outperform the Bloomberg AusBond Bank Bill Index, on a pre-tax basis. The Bloomberg AusBond Bank Bill Index is a commonly used benchmark for

cash-like investments. It measures the return earned on a diversified portfolio of different types of short-term cash investments. Cash investments are generally taxed at 15% in the superannuation

accumulation phase. Refer to TelstraSuper’s Investment Guide dated 1 March 2021 for further information

Current as at 29 April 2021. This work is copyright and no part may be reproduced by any process without prior written permission from TelstraSuper.Y O U R TE L S T R A S U P E R F U N D

Fees and costs

Fee type TelstraSuper Corporate Plus*

Administration fees $1.50 per week + 0.20% per annum

Range 0% p.a. – 1.05% p.a. depending on investment option

Indirect Cost Ratio

(deducted in the calculation of unit prices daily)

Range 0.12% p.a. – 0.54% p.a. depending on your chosen investment

Investment fees

option deducted in the calculation of unit prices daily

Contribution fees

Ranges from $550 to $2,500 plus GST (where applicable) depending

Comprehensive personal advice fees

on the nature and complexity of advice required.

Insurance premiums Default cover generally paid for by your Telstra Group Employer

Exit fees

* Refer to TelstraSuper Corporate Plus Product Disclosure Statement 1 March 2021 and TelstraSuper Financial Planning Financial Services Guide 1 December 2020 for full fee details.

Current as at 29 April 2021. This work is copyright and no part may be reproduced by any process without prior written permission from TelstraSuper.HOW

TELSTRASUPER

CAN ASSIST

Current as at 29 April 2021. This work is copyright and no part may be reproduced by any process without prior written permission from TelstraSuper.H O W TE L S T R A S U P E R C AN AS S I S T

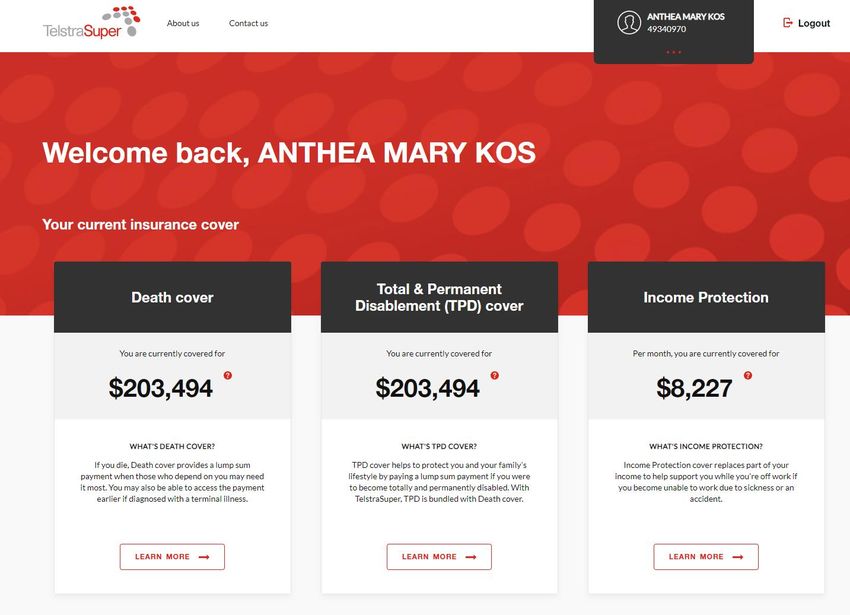

SuperOnline

Update your email address and

personal details

Check your account balance

Review your insurance cover

View your nominated beneficiaries

Make a non-binding nomination

Review your investment options

Pre-tax contributions against the

concessional contributions cap

Benefit statements Login to SuperOnline

at

Latest contributions telstrasuper.com.au

Current as at 29 April 2021. This work is copyright and no part may be reproduced by any process without prior written permission from TelstraSuper.H O W TE L S T R A S U P E R C AN AS S I S T

TelstraSuper app

Estimated account balance

Available on

Investment options, allocation of units Android

and investment returns and Apple

iOS.

Latest contributions

Pre-tax contributions against the

concessional contributions cap

Benefit statements

Insurance cover

Transactions

Digital Member Card

Contact TelstraSuper

Current as at 29 April 2021. This work is copyright and no part may be reproduced by any process without prior written permission from TelstraSuper.H O W TE L S T R A S U P E R C AN AS S I S T TelstraSuper insurance portal Current as at 29 April 2021. This work is copyright and no part may be reproduced by any process without prior written permission from TelstraSuper.

H O W TE L S T R A S U P E R C AN AS S I S T Retirement projector Current as at 29 April 2021. This work is copyright and no part may be reproduced by any process without prior written permission from TelstraSuper.

H O W TE L S T R A S U P E R C AN AS S I S T

Financial advice

General and simple advice

General and simple personal advice over the

phone about your TelstraSuper account including

contributions, investment options and insurance

cover through TelstraSuper

Provided at no additional cost as part of your

membership

Comprehensive financial advice

Comprehensive personal advice available on a

one-off or on-going basis. An advice fee applies.

Ongoing advice service is available at a

competitive price.

General,Top 6 and

simple things to do with

comprehensive adviceyour superbythis

are provided year

Telstra Super Financial Planning Pty Ltd (TSFP) AFSL 218705– which is wholly owned by

Telstra Super Pty Ltd (TSPL). Refer to TSFP Financial Services Guide (FSG), dated 1 December 2020 for important information about the services.

Current as at 29 April 2021. This work is copyright and no part may be reproduced by any process without prior written permission from TelstraSuper.The fund you trust

with your super, is now

there for your friends.

Invite a friend.

We’ll do the rest.

telstrasuper.com.au/refer Competitive Profits back Strong long-term Simple advice When we win, Responsible

fees to you performance on you super you win! investors

Current as at 29 April 2021. This work is copyright and no part may be reproduced by any process without prior written permission from TelstraSuper.Happy to answer

your questions.

1300 033 166

8:30am - 5:30pm (Melbourne time) Monday to Friday

talkingsense@telstrasuper.com.au

telstrasuper.com.au

As a leading profit-to-member fund, TelstraSuper is committed helping our members build a financially secure future.

As a current TelstraSuper member, you are able to refer friends and family members to join TelstraSuper.

Current as at 29 April 2021. This work is copyright and no part may be reproduced by any process without prior written permission from TelstraSuper.You can also read