State of the Market 2021 - Aon South Africa

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Aon South Africa State of the Market 2021 Proprietary & Confidential

A robust approach to risk management and insurance solutions is essential for organisations to remain fit for purpose in a complex world.

Contents

Insurance Key Global Insurance Key South African Insurance Market

Industry Outlook Market Trends 2021 market Trends in 2021 Heat Map

4 5 6 7

How Aon is South Africa: How Insurance Why Aon

Supporting Clients COVID-19 Update in Buyers can Manage

respect of Business and Mitigate the

Interruption Impact

9 10 11 12

Insurance Industry Outlook

Business leaders have been confronted with a pre-existing conditions combined with a pandemic

number of decisions as they steer their workforces, event are being felt in terms of rate increases,

operating models, customers, portfolios and finances capacity constraints, tightening terms and conditions

through massive uncertainty. Some of the changes and growing insurer scrutiny on risk management

they’ve made are likely to last — and some are practices. At the same time, the impact of the United

poised to completely reshape parts of their business. Kingdom Business Interruption test case will have

In the case of risk, COVID-19 has forced companies widespread economic impacts on the industry that

to reprioritise risk and resilience. extend well beyond its geographies. The coming

months will be telling in this regard.

One of the greatest lessons of the past year is that

traditional Enterprise Risk Management processes Insurance and reinsurance pricing will remain

failed to identify the full scale of the pandemic as challenged, although there is general optimism

its impacts materialised into multiple key risks to that the roll-out of the COVID-19 vaccines and the

organisations, such as liquidity, credit risk, human introduction of additional capacity into the market

capital and accelerated rates of change. However, may temper in H2 2021. Coverage clarifications will

there is overwhelming evidence that taking an continue, especially for communicable disease and

enterprise-wide approach to the response was the Cyber. Innovative technologies for automation and

most valuable lesson, and one that organisations are digitisation will become investment priorities for the

likely to carry forward. With existing and emerging insurance industry, while alternative risk retention

risks converging, future shocks on an organisation’s and financing strategies will become more prevalent.

radar, together with heightened risks such as Cyber

associated with the pandemic’s remote and digitised Understanding how this could impact your

workforce response, organisations need to take steps organisation and the steps that you can take to

to reprioritise risk and resilience. proactively manage the expectations of your

business stakeholders and deliver an optimal

For commercial insurance buyers, the impact of

outcome is crucial.

Key global insurance market trends in 2021

Challenging conditions continue: Insurers, focused on balancing Operational & Underwriting Shifts: The insurance industry will

their books and improving their results are introducing focus on implementing controls and driving additional efficiencies

significant price and deductible increases and restricting throughout the entire distribution chain – from centralised

coverage terms. The environment is driven not only by underwriting to accelerating digitisation and virtual processing.

COVID-19 and resultant economic uncertainty, but also by Traditional data and analytics will be integrated with data

escalating loss costs and reduced investment income due to from alternative sources and artificial intelligence to enhance

low interest rates. underwriting and claims handling. As risk profiles have shifted,

underwriting strategies have changed. A risk that may have been

approved in Q1 may not have been approved in Q4, or significant

additional underwriting information may have been required.

Continued Price Escalation: Poor underwriting performance will

continue to be a focus, especially in certain lines of business,

and combined with uncertainty related to COVID-19, economic

conditions and social inflation will mean continued scrutiny Alternative Products & Solutions: Protected Cell Companies

around pricing. New capacity will enter the market through

ZAR insurer start-ups, reinsurance capacity and shifting insurer

(PCCs) and captives will continue to grow in popularity

as organisations look to access additional capacity via the

appetite, bringing some rate relief. COVID-19 has provided reinsurance market, but also utilise their balance sheet more

significant impetus to the Insurtech space as the traditional effectively to retain more risk and address new and emerging

insurance marketplace moves to implement more technologies risks. New products such a parametric policies, event-focused

and AI processes. policies and usage-based policies will increasingly gain traction as

data becomes more available and consumer trends evolve.

Coverage Clarifications: Continued uncertainty around coverage

for COVID-19 and pending regulatory guidance through

the January reinsurance renewals will give rise to continued

clarification and exclusion of coverage for communicable Business Interruption (BI) risks intensify: BI has been on the

disease. As insurers continue to exclude Silent Cyber from Top 10 list of risks facing businesses since Aon’s Global Risk

existing policies, the need for stand-alone Cyber coverage will Management survey started 2007. The UK FCA business

heighten. interruption test case represents a watershed moment for

the industry. While the impacts have yet to play out, they are

expected to reach well beyond the specific geography and line

of coverage (Business Interruption) that were the subject of the

Heightened Risk Complexity: Supply chain dislocation will case.

heighten underwriter focus on supplier transparency and

supply chain resilience, particularly for Business Interruption

coverage, and especially for the technology, manufacturing and

automotive industries. Long-term and continued work-from-

home arrangements will heighten focus on employee safety,

employee wellbeing and Cyber.

Page 5 – State of the Market Report 2021Key South African market trends in 2021

1. 5. 8.

Risk readiness is falling: Climate Change: Cyber Risks are amplifying:

While risk readiness is falling, volatility Weather catastrophes and resultant losses Cyber security and privacy risks are

is growing due to the financial are intensifying with climate change. It is amplifying, with COVID-19, remote

implications of uninsured losses. already taking on increased prominence as working and digitised workforces seeing

consumer attitudes change and investors an increase in cyber-attacks and large-scale

seek assurance that companies have identified and put disruption. A robust technical infrastructure and end-

2.

Reinsurance markets are hardening : in place plans to mitigate climate change risks. to-end digital processes are key elements to safeguard

The reinsurance market continues to harden productivity.

into 2021 which ultimately has a knock-

6. 9.

on effect on the overall market. COVID-19

Growing geopolitical and socio-economic Market volatility drives need for

claims, high natural catastrophe losses and

risks: payment protection:

poor returns on investment have led to widespread

rate increases. Prices hardened in all major lines of GDP growth prospects for 2021 are South Africa is currently experiencing

reinsurance business and geographies for excess-of-loss expected to be negative, with investor difficult political and economic

treaties. and consumer confidence at the lowest conditions, which is driving the need

ebb since just before South Africa’s transition to for trade credit insurance.

democracy in 1994. Further credit rating downgrades

3.

Capacity is reducing: will lead to increased financial market volatility.

Insurers continue to withdraw from poor Record high unemployment rates and failing

performing classes and refocus their appetite service delivery and infrastructure are likely to fuel

especially on challenged occupancies heightened destructive social unrest. Deteriorating

such as the mining sector, heavy industry, public infrastructure, poor local administrative

textiles, food industry and any cold storage-related delivery and energy shortages and load shedding

exposure (Expanded Polystyrene), as well as from are significant risks to business continuity and

poor performing classes such as D&O, Professional profitability.

Indemnity, Casualty, Cyber, natural catastrophe exposed

and large limit Property.

7.

Regulatory Changes:

4.

Property rates will continue to increase: Compliance with both local and

Property rates have been increasing for international laws and regulations will

the past three years and are expected to increase risks and costs of compliance and

continue increasing in 2021. Increases in working.

2021 could be as much as 30% up, based

on acceptable claims performance. COVID-19 will

continue to have a major impact on the sector in 2021

and there is increased competition for tenants, capital

and property assets.

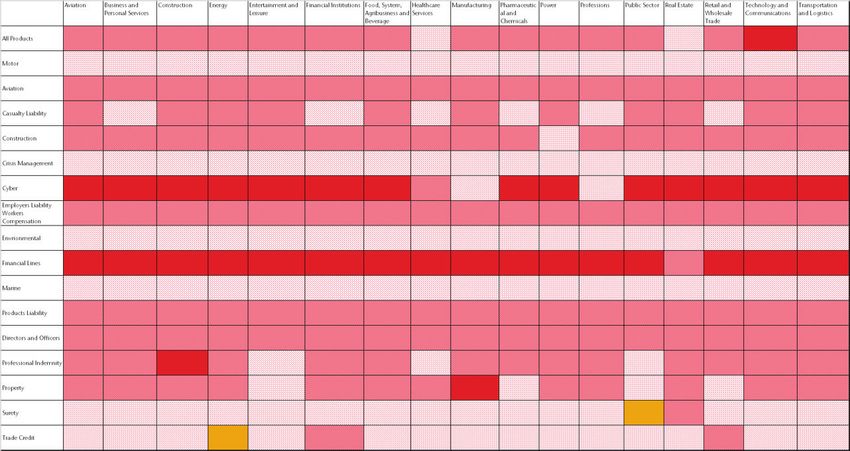

Page 6 – State of the Market Report 2021Insurance market heat map Q1 2021 Market Dynamics: EMEA and South Africa Page 7 – State of the Market Report 2021

EMEA and South Africa Q1 2021 Rate Trends

Down Flat +1-10% +11-30% +30% N/A

Page 8 – State of the Market Report 2021How Aon is supporting clients

Aon’s United Broking approach facilitates Aon’s Data Scientists, Actuaries, and AI Experts in the

engagement across retail, wholesale, reinsurance, Aon Centers of Excellence in Dublin, Singapore and

Aon’s legal, technical, and policy wording experts

and risk engineering to identify traditional and non- Krakow use cutting-edge methodologies to interrogate

challenge insurer behaviour and ensure any changes

traditional approaches to approaching the market, Aon data together with data from external sources

made are fully understood by insureds.

structuring the placement and managing cost of and develop new client solutions – like the Aon Client

risk. Treaty.

Aon’s Protected Cell Companies (PCC) and captive

teams work with clients to optimise the balance

of risk transfer and retention financing through Partner with Aon and Insurers on Business Interruption

comprehensive valuation, comparative analysis, loss valuation methodology.

feasibility studies and utilisation/strategic reviews for

existing captives.

Page 9 – State of the Market Report 2021South Africa – COVID-19 Update in respect

of Business Interruption

The recent appeal court judgments in South Africa and insurers and reinsurers, most insurers have not wanted to although the court cases have provided greater certainty

internationally has led to greater legal certainty regarding relinquish their previously stated positions until the appeal regarding certain key principles, one would still need to take

certain key questions that the insurance industry has courts had provided legal certainty. account of the actual cover provided by the relevant policy

been grappling with since March last year. The courts under consideration. Each policy would be governed by its

The leading judgment in South Africa has been that of own specific terms and conditions.

have supported the principle that the insured peril for

Guardrisk Insurance Company Limited v Café Chameleon

the purposes of the infectious and contagious disease

CC. This appeal was heard on the 23rd November 2020 in Our claims advocacy team has already begun the process

extensions on business interruption policies includes both

the Supreme Court of Appeal and judgment was handed of engaging with the respective insurers in relation to

the occurrence of the disease within the specified radius and

down on the 17th December 2020. Before that, a full the business interruption claims that have been notified.

the government’s response to it.

bench of the Western Cape High Court had ruled in favour In some cases, previously closed claims have been

of the insured policyholders in the case of Ma-Afrika Hotels reopened. In other cases, information is being sought from

In the case of Guardrisk Insurance Company Limited Café

(Pty) Ltd. and Stellenbosch Kitchen (Pty) Ltd. v Santam policyholders to enable loss adjusters to be appointed or to

Chameleon CC the Supreme Court of Appeal stated

Limited. enable loss adjusters to begin their work of adjusting the

that “Viewed slightly differently, because the lockdown

claims.

was a response to a national outbreak, which included, In the UK, judgement was handed down on the 15th

predominantly, the Cape Town outbreak, Café Chameleon’s January 2021 in the test case of the Financial Conduct No doubt we expect there to be a backlog as the insurers

losses were due at the very least to concurrent causes. As a Authority v Arch and Others. In this case the Supreme and adjusters will be dealing with claims that have been

matter of ‘reality, predominance and efficiency’, therefore, Court dismissed the insurers’ appeals in favour of the FCA’s lodged from all parts of South Africa and via other brokers

the local outbreak and government response, was the real appeals. as well. We also recognise that there is much work to be

or proximate cause of the business interruption.” done and individual circumstances and other ancillary policy

Whilst some insurers have communicated their respective issues may give rise to additional challenges.

Considering the significant financial impact of the COVID-19 positions following the latest court developments, others

pandemic on businesses and the potential impact for have yet to do so. It should also be borne in mind that

Page 10 – State of the Market Report 2021How insurance buyers can manage

and mitigate the impact

Expand risk management decision-making to address long-tail and emerging risks

Boards and executive management teams need to broaden their perspective when considering risk and increase their focus on identifying and evaluating

future major shocks that could disrupt strategic objectives and present threats to the organisation. This will help organisations increase their preparedness and

explore opportunities to enable them to thrive. It is becoming clear that resilience plans associated with prior business models will not be sufficient to protect

organisations from these emerging risks.

Build a resilient workforce

In Aon’s COVID-19 Risk Management and Insurance Survey conducted in Q4 of 2020, it was notable that survey responses point to an overwhelming

consensus that people are at the heart of business resilience and strategy success. Workforce stability and engagement is a key driver for businesses to be

sustainable and adaptable across all countries and regions in a volatile and changing risk landscape.

Rethink access to capital

Few respondents in Aon’s COVID-19 Risk Management and Insurance Survey said they submitted COVID-19-related insurance claims,

suggesting that insurance was not viewed as a solution or was unable to meet the needs of organisations in financing their risk

exposure. This is likely to be because either the risks are uninsurable or the scale of the event exceeds conventional program limits or

capacity. The insurance industry needs to adapt and develop solutions capable of anticipating, responding to and mitigating financial

volatility for organisations. The trend towards increased retentions will almost certainly lead to more extensive utilisation of captives,

even from organisations that may have previously discounted this approach due to a lack of scale. Leverage Aon’s risk financing

decision platform to optimise your insurance program and manage volatility.

Start early

With more submissions in the market, and greater underwriting scrutiny, the process is taking longer. Work with Aon

to establish a proactive strategy and begin the process early. The whole process must start much earlier and with more

preparation and detail. Companies will have to increasingly reconsider and justify their approach to risk and the degree

of insurance cover that they have in place.

Page 11 – State of the Market Report 2021How insurance buyers can manage Why Aon

and mitigate the impact

Proactively prepare for change Aon is not about insurance products

As-is renewals are rare. Establish budgets and manage internal expectations related to price increases, and policies – we’re about risk

deductible increases and other program changes. Buyers are potentially being asked to pay more for leadership and risk understanding

risk transfer, as well as taking higher retentions and refocusing on the quality of their risk. Coverage and being your navigator and trusted

restrictions are being applied and fewer coverage extensions are available as insurers seek to return to advisor. Our clients have the power

core coverages. The risk management function may need to help the C-suite in their organisations to of Aon United by your side - a group

understand how this shift might affect the business from a cost and volatility perspective. of colleagues, some of the greatest

minds and experts in the industry,

banded together around the world,

with unique skills and capabilities to

Provide detailed information help your businesses succeed, thrive,

Bring the insurance buying function and enterprise risk management (ERM) team more closely recover from adversity and grow.

together to better inform perspectives on risk profile and the control environment. Use all financial

levers at your disposal to manage risk and follow through with risk control and recommendations.

That’s Aon, by your side.

Engage constructively on claims

Provide solid, fully calculated claims submissions. Avoid engaging external coverage counsel unless

absolutely necessary. Be ready to consider negotiated settlements at less than the full claim value.

Manage internal expectations with regard to decision and payment timeliness.

Challenge your broker

Buyers must work with their broker to proactively assist their risk financing strategy and navigation of

the market so that they are ‘positively differentiated’.

A robust approach to risk management and insurance solutions is essential for

organisations to remain fit for purpose in a complex world.

Page 12 – State of the Market Report 2021About Aon plc

Aon plc (NYSE:AON) is a leading global professional

services firm providing a broad range of risk, retirement

and health solutions. Our 50,000 colleagues in 120

countries empower results for clients by using proprietary

data and analytics to deliver insights that reduce volatility

and improve performance. Visit Aon.com for more

information.

About Aon South Africa

Aon South Africa is a leading provider of Risk

Management Services, Insurance and Reinsurance

Broking, Employee Benefits Solutions and Specialty

Insurance Underwriting. The company employs more

than 700 professionals in its 12 offices in South Africa

with its head office in Sandton, Johannesburg.

The information contained in this marketing material is of a

general nature only and not intended to constitute advice or to

make recommendations. Although we endeavour to provide you

with accurate, relevant and current information by using sources

we consider reliable, we cannot guarantee that the information

is accurate, relevant, current or fit for your purposes. Reliance

should not be made on the information in this document

without verifying it and receiving the appropriate professional

advice. A licensed Aon broker or consultant will assist you with

any insurance related advice or query you may have.

Aon South Africa (Pty) Ltd

The Place, 1 Sandton Drive,

Sandhurst, 2196

P O Box 78367, Sandton, 2146

Tel: 0860 100 404

www.aon.co.za

Facebook | Twitter | LinkedIn

Aon South Africa Pty Ltd, an Authorised Financial Service Provider, FSP 20555

Aon Re Africa Pty Ltd, an Authorised Financial Service Provider, FSP 20658

Aon Limpopo Pty Ltd, an Authorised Financial Service Provider, FSP 12339You can also read