Steel and Coal: A New Perspective - European Research and Innovation in Action - Philippe Samyn and ...

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Steel and Coal:

A New Perspective

European Research

European Research and

and Innovation

Innovation in

in Action

Action

EUR [number] EN

Research and EN

Innovation

EUROPEAN COMMISSION

Directorate-General for Research and Innovation

Directorate D — Industrial Technologies

Unit D.4 — Coal and Steel

Contact: Domenico Rossetti di Valdalbero, PhD

E-mail: Domenico.Rossetti-di-Valdalbero@ec.europa.eu

RTD-PUBLICATIONS@ec.europa.eu

European Commission

B-1049 Brussels

EUROPEAN COMMISSION

Steel and Coal:

A New perspective

European Research and Innovation in Action

Edited by Dr. Domenico Rossetti di Valdalbero

Directorate-General for Research and Innovation

2019 Research Fund for Coal and Steel EN

EUROPE DIRECT is a service to help you find answers

to your questions about the European Union

Freephone number (*):

00 800 6 7 8 9 10 11

(*) The information given is free, as are most calls (though some operators, phone boxes or hotels may charge you)

LEGAL NOTICE

This document has been prepared for the European Commission. However, it reflects the views only of the

authors. The Commission cannot be held responsible for any use that may be made of the information

contained therein.

More information on the European Union is available on the internet (http://europa.eu).

Luxembourg: Publications Office of the European Union, 2019.

PDF ISBN 978-92-76-02103-2 doi: 10.2777/842798 KI-04-19-372-EN-N

© European Union, 2019.

Reproduction is authorised provided the source is acknowledged.

Cover image: ©Philippe SAMYN and PARTNERS, architects & engineers, #Image d’Avilés E13_101/E11_2648

Contents

FOREWORD .................................................................................................................. 6

AN HISTORICAL, VITAL INDUSTRY IN TRANSITION ........................................................... 7

Steel and coal: from the roots of EU integration towards a Clean Union ........................ 7

Why, What and How to build now? ......................................................................... 10

Carbon capture and storage is needed and is becoming cheaper ................................ 10

Steel 4.0 and forward-looking applications .............................................................. 11

European Research and Innovation in Action ........................................................... 13

STEEL AND COAL R&I ASSESSMENT ............................................................................... 15

Steel technological achievements ........................................................................... 16

Coal technological achievements ............................................................................ 17

Steel and coal in the next decade .......................................................................... 18

Innovation leakages vs. Open Europe ..................................................................... 19

STEEL AND COAL IN THE NEW ECONOMY ........................................................................ 21

Decarbonisation: Mission possible even for harder-to-abate sectors ........................... 21

Land-use rehabilitation in coal regions in transition .................................................. 24

March for a Clean Europe ...................................................................................... 26

AGENDA ..................................................................................................................... 27

LIST OF PARTICIPANTS ................................................................................................ 28

ACKNOWLEDGEMENTS ................................................................................................. 30

4

List of figures

Figure 1. Steel industry production sites in the EU ........................................................................ 8

Figure 2. Coal and lignite production in the EU and imports ........................................................... 9

Figure 3. Circular economy: Coal power plant and Carbon Capture and Utilisation .......................... 11

Figure 4. Digital Twin of a steel rebar........................................................................................ 12

Figure 5. Autonomous drone .................................................................................................... 12

Figure 6. ECOSLAG process diagram ......................................................................................... 12

Figure 7. Global emissions pathways, Gt CO2 /year .................................................................... 21

Figure 8. CO2 emissions reductions potential in the steel industry ................................................ 22

Figure 9. Transition pathway in Poland - Silesia .......................................................................... 24

List of tables

Table 1. Steel technological achievements ................................................................................. 16

Table 2. Coal technological achievements .................................................................................. 17

Table 3. Steel challenges and recommendations ......................................................................... 18

Table 4. Coal challenges and recommendations .......................................................................... 19

5

FOREWORD

The EU's foundations originate from the Schuman Declaration

and the European Coal and Steel Community (ECSC). The 1951

Paris Treaty has been the bedrock of peace, welfare and

prosperity on our continent through industrial development.

A strong industrial base is of key importance for Europe’s

competitiveness. Associated with its environment and climate

leadership, Europe plays a forward-looking role on the global

stage. As Commission Vice-President Frans Timmermans

recently said: ‘The world is in a flux and we are in the midst of

the fourth industrial revolution. Everything is changing for

everyone. The question is whether we are a victim of change,

or whether we will embrace and guide it’.

For all sons and daughters of the European integration, coal and steel have a particular resonance. We

are especially concerned about the challenges that these industries are facing in particular

overcapacity, unfair competition and decarbonisation. But we must modernise our economies, secure

our natural environment and improve the health and wellbeing of all our citizens.

The European Commission endorsed the global commitment to limit climate changes by setting

ambitious CO2 emission reduction targets. Supported by Research and Innovation, several European

policies; such as the Energy Union and the Circular Economy Package, are materialising these

endeavours. The new EU Research and Innovation programme, Horizon Europe, with a proposed €100

billion budget will be the biggest ever research funding programme running from 2021 to 2027 and

supporting strong Public-Private Partnerships. Complemented by the Research Fund for Coal and Steel

and the Innovation Fund, we are convinced that coal and steel sectors will become more sustainable in

Europe.

We can deliver on the energy and environment targets. However, no European company, region or

citizen should be left behind. Our aim is to have a ‘just transition’. This is true for coal and steel as

well as for other energy intensive sectors like cement, chemical, ceramic, paper and glass. A carbon

neutral Europe by 2050 requires maximising the technical potential, pushing for breakthrough

technologies, deploying renewable sources of energy and ensuring the large-scale electrification of the

energy system. This transition has a certain cost. We need to be ready for such a structural shift that

is based more on quality than quantity and on high-added value rather than mass products and

applications.

This publication sheds light on the technological achievements in the steel and coal sectors. Much has

been done but more is needed to improve industrial energy efficiency, ensure affordable energy prices

and develop new clean technologies and processes like carbon direct avoidance and smart carbon

usage and storage. Recovering, recycling and reusing energy, heat and material streams across

industrial sectors are part of the new economy.

A clean Europe can go hand in hand with increased prosperity. To succeed, the EU and its Member

States and public and private sectors must join their forces and lead the way in science, technology

and modern infrastructure.

Jean-Eric Paquet, Director-General for Research and Innovation

6

AN HISTORICAL, VITAL INDUSTRY IN TRANSITION

This report reflects the presentations and deliberations during the European conference entitled 'Steel

and Coal: a New Perspective', which took place in Brussels on 28 March 20191. Hosted by the

European Commission's Directorate-General for Research and Innovation (DG RTD), the event

gathered 100 stakeholders from across the EU, including senior representatives from the major steel

and coal companies, associations, research and academic organisations. The aim of the conference

was to explore the prospects of technological breakthroughs for steel and coal in a world in transition

faced with globalisation, decarbonisation and digitisation. It was also an opportunity to discuss with

stakeholders the preliminary results of the seven-Years Monitoring and Assessment of the Research

Fund for Coal and Steel (RFCS) programme. Finally, this conference explored the challenges for steel

and coal sectors in a circular and carbon constrained EU economy and in the EU transition to a circular

economy.

Steel and coal: from the roots of EU integration towards a Clean Union

In the aftermath of World War II, steel and coal were the olive branch to secure peace among

European countries. Thanks to the management of coal and steel under a European High Authority, a

political long lasting political project based on collaboration has been forged. Jean Monnet used to say

‘Nous ne coalisons pas des Etats. Nous unissons des hommes’ – ‘We are not forming coalitions of

States, we are uniting people’. Building on coal and steel, step-by-step, the ECSC became the

European Community, and then the European Union. After almost 70 years of European integration,

the world has changed rapidly and significantly with new global players, new technologies and new

challenges.

The conference was organised in three sessions (see the agenda at the end of the publication). The

first keynote speeches dealt with Steel and Coal in a forward-looking perspective. The speakers

addressed the themes of architecture, steel 4.0, energy, electric mobility, innovation, technology and

socio-economic challenges. The conference offered the opportunity to discuss with stakeholders and

scientists the preliminary results of the Expert Group on Monitoring and Assessment of RFCS, the

Research Fund for Coal and Steel. The last session of the conference explored the issues of steel in a

climate constraint-world and of coal regions in transition. Finally, the opportunities offered by RFCS,

Horizon 2020 and the upcoming Horizon Europe and Innovation Fund have been presented in the

conclusions.

Ms Signe Ratso, Deputy Director-General of the European Commission’s DG RTD, opened the

conference emphasising that European industry provides 36 million direct jobs2 and contributes to

high standards of living for EU citizens. Industry plays a key role in supporting Europe´s global

leadership and international stature.

Europe´s competitors are investing heavily in the upgrade of their industry. The productivity gap with

some countries is increasing and major economic players like China are competing with those

industrial sectors where the EU was leading for several decades.

Europe has obtained excellent research results in many technological areas, which have helped it

develop a smart, innovative and sustainable industry. Nevertheless, more is needed to turn research

into breakthrough innovation, creating new markets that drive jobs and growth and that deliver a

cleaner, healthier and more prosperous planet for the next generations. The uptake of technologies

must be accelerated and improved particularly among SMEs and traditional industries while

investments in new skills must increase.

For this reason, the Commission adopted the ambitious proposal for Horizon Europe – the Framework

Programme for Research and Innovation under the next long-term EU budget 2021-2027. Building on

the achievements and success of Horizon 2020, the Commission has proposed €100 Billion to keep the

EU at the forefront of global research and innovation. EU institutions have reached a partial political

agreement on Horizon Europe at the end of March 2019.

Directly related to steel and coal, Ms. Ratso mentioned that the Commission is exploring the possibility

to exploit part of the assets of the European Coal and Steel Community in liquidation to build a critical

mass for investment in breakthrough technologies in the steel industry and for coal regions in

transition. This will also complement the Research Fund for Coal and Steel.

1

European Conference ‘Steel and Coal: A New Perspective’, 28/3/2019.

2

Investing in a smart, innovative and sustainable Industry - A renewed EU Industrial Policy Strategy, European

Commission COM(2017)479.

7

Figure 1. Steel industry production sites in the EU

The difficulties faced by the EU steel and coal industry is facing cannot be ignored. They include

overcapacity, unfair competition, decarbonisation, and relatively low demand. The steel industry is

present in most Member States taking the form of primary steelmaking plants, its Electric Arc

Furnaces plants and plants that process steel (See Figure 1)3. The EU steel sector provides more than

300,000 direct jobs. In some regions of Europe, coal plays a very important role: more than 230,000

people are employed in the mining and in the coal and lignite-fired power plants.

The EU industry has demonstrated that it is able to evolve and to become more sophisticated.

However, all ideas require research and development – in addition to a greater investment in

innovation - before they can be proven and implemented commercially. Breakthrough technologies will

be fundamental for leading international competition and for reducing the impacts on climate change.

Promising breakthrough technologies such as hydrogen-based steelmaking or primary steel production

using electricity are starting to be demonstrated by the EU steel industry. Mass industrial

implementation of these technologies will require a large amount of affordable renewable energy.

Smart carbon usage also has significant potential from the industrial symbiosis perspective. The EU

already has some successful examples of the steel and chemical industries working together.

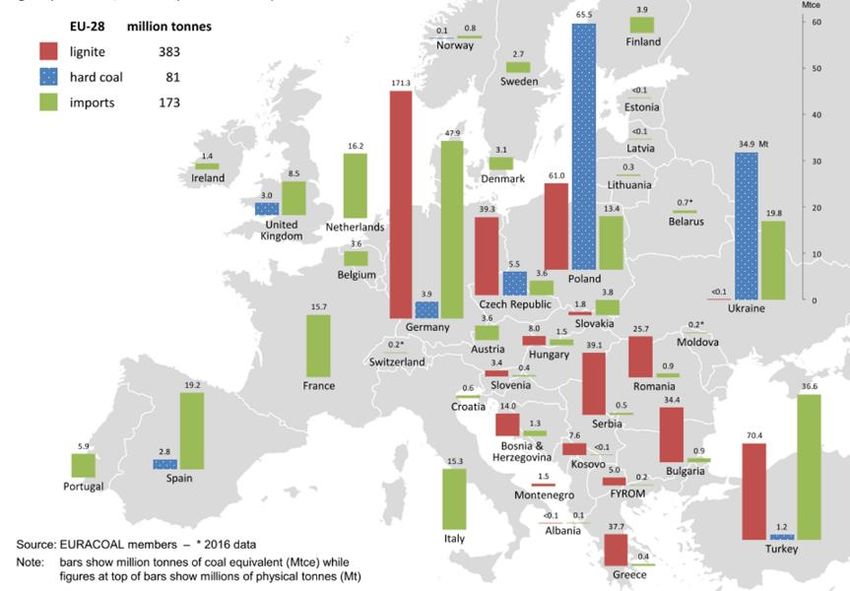

Ms. Ratso noted that coal supplies represent one third of worldwide energy. In Europe, the production

and consumption of coal has been steadily declining for years (See Figure 2)4. Today’s main challenge

is how to conciliate coal use with the climate targets agreed in Paris. To this end, the deployment of

3

Eurofer, European Steel in Figures, 2018.

4

Euracoal, Coal in Europe in 2017.

8

carbon capture and storage (CCS) is critical. Other advanced coal technologies could be implemented

such as underground coal gasification and coal to liquid or coal to chemical technology. These are

areas for innovation and demonstration.

But there are also other options for the future of coal such as ‘poly-generation’ or ‘multi-fuel plants’.

This would entail the simultaneous and flexible production of electricity, hydrogen, synthetic liquid

fuels, heat and/or chemicals. Also worth exploring is the alternative uses of coal, like coal-to-

fertilisers, coal-to-graphite, or coal-to-rare earths.

At EU-level, the ‘Platform on coal regions in transition’ has been providing opportunities for more than

a year for national, regional and local representatives to discuss how these regions can best

modernise their economies in line with the EU decarbonisation strategy. Key words in this context are

social fairness and ‘Just transition’, new skills and financing for the economy.

Figure 2. Coal and lignite production in the EU and imports

Whatever happens to the EU’s coal regions in the EU will be closely watched by China, India, the

United States and Canada, where coal communities are also challenged to re-think their future.

Europe aims to lead by example.

Highlighting the importance of creative minds, Ms Ratso introduced a famous architect of this century,

who was able to combine beauty, innovation and sustainability when designing the ‘Europa building’

that hosts the European Council. The reuse of windows frames from all Member States gives a

powerful message. It makes the window to the EU, represented by this building, a fitting symbol of

the EU’s diversity of cultures. The building’s beautiful lantern-shape also demonstrates the modern,

clean and efficient nature of steel.

9Why, What and How to build now?

Mr Philippe Samyn's keynote speech focused on the importance of recycling materials and reusing

what we have.

Before WW2, when something was destroyed (for example during the London bombings) people

looked at what could be done to reassemble and reuse what was left. Since WW2, when something is

destroyed, it has to be completely erased. In other words, a ‘tabula rasa culture’ has developed. Mr

Samyn argued that we must go back to salvaging what we have and producing less, despite the big

change in the types of building materials we use today.

Steel's advantages for many innovative designs and applications are clear. Steel is 100% demountable

and re-useable. On producing materials since WW2, Mr Samyn underlined that: ‘Before 1914, with a

few exceptions, constructions were made from earth, stone, baked earth bricks and tiles, wood,

vegetal and animal fibres. Since then, in industrialised countries, Portland cement, steel, plastic, glass

and aluminium gradually replaced these traditional materials. […]. The speeding up of the cement

production, which also occurred in the 1990s, correlates to the collapse of the USSR, the opening of

China, the emergence of globalisation and the establishment of a new global economic order. The

internet too became widely accessible in the 1990s, as the World Wide Web gradually developed.

Abundant energy suddenly doubled between 1990 and 1998 by an unbelievable financial abundance,

resulting straight from the value maximisation of future profits of listed companies around the globe

[…]. These funds are wasted in unbridled constructions. They are costly and fragile, wrapped in a

luxury that compares to the carelessness of that time. Urbanisation, cement production and general

material production is booming. In the meantime, issues related to energy resources and global

warming are arising. […]. The world production of primary energy follows the growth of the world

population and soars from 2000 on, maybe in order to address the needs of the data centres’ 5.

Mr Samyn questioned our way of life. Much of the energy produced goes to data centres, meaning

that this energy is used to communicate. Could we communicate less but better? Saving energy is

about changing the way we live.

Questioning the way we build, Mr Samyn made two key points:

For a global approach to architecture: The construction and the design of a building should

always be linked with the context in which it takes place. That is to say, the biological

diversity, lights, sounds, smells, etc.

For efficient and bright architecture: ‘Healthy architecture’ is useful for the future and

respectful of its environment. There is no need to use many luxurious materials (which require

more production) but to find efficient materials and bright techniques (e.g. punch steel).

Carbon capture and storage is needed and is becoming cheaper

Mr Tomasz Rogala, President of Polska Grupa Górnicza (PGG), Polish Mining Group and of Euracoal,

the European association for coal and lignite highlighted the importance of the coal industry’s value

chain and progress in clean coal technologies. He mentioned the triangle of values and challenges -

technology, society and economy - that PGG is confronted with in Poland.

In 2019, 200,000 jobs in Silesia are related to coal and these jobs pay 50% more than the average

salary in the region. €719 million of fiscal payments are transferred to the central government and

€181 million per year is spent on machines and equipment. Mr Rogala also underlined that climate and

energy has the potential to create more than 1 million additional jobs, mainly in construction,

agriculture and renewable energy, while the number of jobs in mining and extraction is expected to

fall.

Mr Rogala presented the new publication of the EU-supported CoalTech2051 project entitled ‘Changing

the face of coal: an outline strategic research agenda for future coal-related RTD in the European

Union’6.

He pointed out that carbon capture and storage (CCS) works, that it is necessary and that it will

become cheaper. Together with clean coal technologies, CCS will result in lower CO2 emissions. Based

on the experience gained from a full-scale project in Canada, he demonstrated that the specific costs

of second-generation CCS technologies should be 67% lower (per tonne of CO2). Mr Rogala pointed

5

E12-40 — WHAT TO BUILD WITH NOW? © Philippe Samyn and Partners.

6

CoalTech2051

10out that ‘the CCS installation at Boundary Dam coal power plant in Canada has been in operation since

2014 and captures circa one million tonnes of CO2 annually. CCS plants can capture up to 97% of the

CO2.'

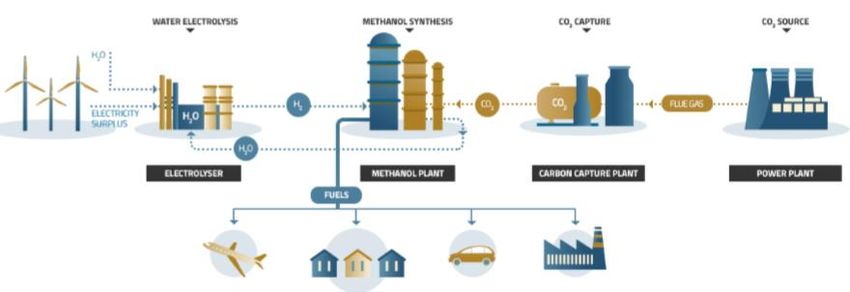

Mr Rogala stressed that PGG is making progress with coal gasification as an alternative to

conventional combustion processes and is therefore supporting the EU's circular economy (see Figure

3 on Carbon Capture and Utilisation — CCU). Coal and municipal waste gasification can also provide a

solution for the waste management problem. In Germany, with 46% (LHV) electrical efficiency, the

750 MW Lünen power plant is one the most efficient coal-fired power plants in the world.

A short video was shown covering the signing of the European Coal and Steel Community treaty in

1951 through to the present and future of clean coal technologies7.

Figure 3. Circular economy: Coal power plant and Carbon Capture and Utilisation

Steel 4.0 and forward-looking applications

Ms Delphine Snaet presented the European Steel Technology Platform (ESTEP) vision on the future of

the steel sector.

She noted that modern society is a dynamic system. Democratic shifts, urbanisation, climate change,

environmental pollution, economic crises, digital revolution are just few of today's global megatrends.

Driven by economic factors and social awareness, the European steel industry is trying to establish a

coherent model that encompasses low-carbon, digitalisation, sustainable and circular economies.

Many research and innovation projects demonstrate the potential of newly developed steel grades and

the benefits of new steelmaking approaches.

The researchers of Tenova, for example, succeeded in reducing the operational costs of a basic

oxygen furnace using machine learning. By predicting the steel temperature at the end of the blow,

they achieved lower energy consumption leading to higher process efficiency.

Concerning the digitisation of steel production, the I2MSteel, SOPROD and CyberPOS RFCS projects

have successfully adapted the ‘digital twin’ technology to the requirements of the steel industry. They

have developed digital models that predict the properties of the product, while interacting with

machines and optimising the production path (see Figure 4).

7

Video clip ‘From ECSC to advanced coal technologies’.

11Figure 4. Digital Twin of a steel rebar

The use of autonomous drones (See Figure 5 from DromoSPlan project), carrying additional sensors

for gas detection and detection of dangerous elements, allows to reduce the maintenance and

inspection costs. A European consortium is designing a drone that can operate in the harsh

environment of a steel production plant (the DromoSPlan project).

Figure 5. Autonomous drone

The transition to a circular economy is another key trend. It is an essential part of ESTEP Strategic

Research Agenda. Examples of projects to recover steel industry by-products include: (i) an RFCS

project entitled ‘ECOSLAG’ (See Figure 6) which aims to find technical solutions for heat recovery from

steelmaking slags while producing a high quality slag product for external or internal utilisation; and

(ii) another RFCS project entitled ‘REUSTEEL’ to widely disseminate and valorise research results on

the reuse and recycling of by-products.

Figure 6. ECOSLAG process diagram

A number of projects are developing steel solutions for electro-mobility where the researchers face

different challenges. Solutions include weight, crash performance and energy absorption of the new

12materials, fire protection and sustainability of the designed product. The projects put these solutions

into practice by designing products with inherent fire protection, customised steel grades and flexible

but stress resistant joining. For example, TkSE is exploring solutions while working on large steel

battery housing for e-vehicles, which will allow a saving of more than 50% CO2 over the entire

lifecycle of the battery housing.

Last but not least, a group of projects is focusing on products for energy production from renewables.

Salzgitter’s project entitled 'SALCOS' explores the Carbon Direct Avoidance pathway. The project uses

already established (direct reduction with natural gas) and novel (hydrogen production and use)

technologies that aim to save up to 95% of CO2. The project unites GrInHy and GrInHy2.0

(demonstration of the first steam megawatt electrolyser), WindH2 (onsite production of hydrogen and

electricity generation from wind power) and MACOR (feasibility study on the adopted route). The

project's results will be presented at the Hannover Fair in April 2019.

Dillinger's researchers work on different innovative steel slabs for durable constructions, applicable in

renewable and transport infrastructures. They are investigating the applicability of thermomechanical

rolling. This is the super positioning of thermal and mechanical rolling treatment at the same time with

a result that cannot be obtained by a thermal or mechanical treatment alone.

ArcelorMittal is also working on these issues. It is developing new materials for thermal solar units and

photovoltaic solar racks. The new products comprise high temperature resistant metals to be used for

hot molten salts storage tanks, pipes with better corrosion resistance than oils, innovative solutions

for metallic reflectors able to replace glass-based heliostats and coated high-strength steels for light,

and reflectors supporting structures with improved atmospheric corrosion resistance.

Finally, Ms Snaet concluded that:

‒ technological pathways for carbon neutral steelmaking exist8;

‒ considering that steel is a ‘permanent’ material, there are many promising sustainable

solutions that use it and its by-products;

‒ the digitisation of the steel sector is a key enabler for the future steel factories;

‒ electric mobility is not affordable without new steel products; and

‒ innovative steel solutions could improve the performance and increase the durability of

renewable energy infrastructures.

European Research and Innovation in Action

The European Council agreed at its 21 March 2019 meeting that ‘in view of the importance of a

globally integrated, sustainable and competitive industrial base, the Commission is invited to present,

by the end of 2019, a long-term vision for the EU’s industrial future, with concrete measures to

implement it. It should address the challenges European industry faces, touching upon all relevant

policy areas (…). To remain globally competitive in key technologies and strategic value chains, the EU

needs to encourage more risk-taking, and step up investment in research and innovation. Measures

should be taken to further support the European Innovation Council and to facilitate the

implementation of Important Projects of Common European Interest, while ensuring a level playing

field, as well as a regulatory environment and state-aid framework that are conducive to innovation’.

The European Commission has taken a number of policy actions in this area in recent years, including:

(i) the action plan for a competitive and sustainable steel industry in Europe [COM2013)407]; (ii) the

Communication on ‘Steel: Preserving sustainable jobs and growth in Europe [COM(2016]155]; (iii) the

renewed EU industrial policy strategy [COM(2017) 479]; and (iv) the Coal Regions in Transition

Platform9. In addition, the Commission has several instruments that can be used to support the

adaptation of the industry. These include the European Fund for Strategic Investments that will soon

become InvestEU, and the European Structural and Investment Funds.

Notable research and innovation programmes include:

the EU R&I Framework Programme Horizon 2020 with the Public-Private Partnership ‘SPIRE’

(Sustainable Process Industry through Resource and Energy Efficiency) and the Societal

Challenge 3 on Energy and the Societal Challenge 5 on Resource efficiency; and

the Research Fund for Coal and Steel (RFCS).

8

European Commission, European Steel — The Wind of Change, Publications Office of the EU, 2018.

9

https://ec.europa.eu/energy/en/topics/oil-gas-and-coal/coal-regions-in-transition

13In 2021-2027, Horizon Europe will offer R&I opportunities for energy-intensive industries,

especially in its ‘Digital, Industry and Space’ and ‘Climate, Energy and Mobility’ clusters. The

Innovation Fund will also be important for scaling up innovative low-carbon technologies and

processes in energy-intensive industries, including products substituting carbon intensive ones,

carbon capture and utilisation (CCU), construction and operation of carbon capture and storage

(CCS), innovative renewable energy generation and energy storage.

Finally, in addition to RFCS, the Commission is exploring how the assets of the European Coal and

Steel Community in liquidation could support breakthrough technologies for low-carbon

steelmaking and accompany the restructuring of the coal regions in transition.

14STEEL AND COAL R&I ASSESSMENT

The second half of the conference took stock of the preliminary results of RFCS' seven-year monitoring

and assessment exercise. It highlighted a number of achievements in both the steel and coal sectors

thanks to RFCS research, innovation and demonstration projects.

Domenico Rossetti di Valdalbero, Deputy Head of DG RTD’s ‘Coal and Steel’ unit opened the session

stressing the importance of monitoring and assessing the impact of research and innovation. Such

monitoring and assessment is crucial to formulate solid recommendations for improvements in the

steel and coal sectors.

Council Decision 2008/376, the legal basis of the RFCS programme, requires that the research

programme undergo a monitoring and assessment exercise every seven years. The last monitoring

and assessment report covered the period 2003-2010. In 2018, a new monitoring and assessment

exercise was launched to produce a review of RFCS for 2011-2017 and a possible revision of the

multiannual technical guidelines in line with the Commission's better regulation guidelines

(effectiveness, efficiency, relevance, coherence and EU added value). The report also gives

recommendations and investigates ways to improve collaboration and the sequencing of funding,

notably between the RFCS and the Research and Innovation Framework Programmes (Horizon 2020

and Horizon Europe) and the Innovation Fund.

After explaining the RFCS monitoring and assessment process, Mr Rossetti introduced a panel of

experts chaired by Jean-Marc Steiler, one of the Steel Rapporteurs, Ms Valérie Prudor, the Coal

Rapporteur, Mr Nikolaos Koukouzas and Ms Elisabeth Clausen.

Mr Rossetti pointed out that this session was to present the preliminary results of the RFCS monitoring

and assessment report and to actively involve stakeholders by gathering their written comments, via a

form distributed earlier, on:

the preliminary results of the RFCS monitoring and assessment exercise (2011-2017) and

what is missing; and

future challenges for RFCS by 2030, emerging trends and how to get a greater impact

from R&I?

Mr Jean-Marc Steiler described the RFCS monitoring and assessment report's methodology stating that

out of 293 projects funded and 178 projects completed between 2011 and 2017, the report

qualitatively evaluated 60 projects based on the inputs received from the technical groups. It also

quantitatively assessed another 38 projects via questionnaires sent to the project coordinators.

Overall, around 33% of the projects funded in 2011-2017 have been monitored and assessed.

15Steel technological achievements

Mr Steiler and Ms. Prudor drew the attention of the public towards the most emblematic steel

achievements stemming not only from projects’ results achieved during 2011-2017, but also from

some projects launched prior to this period. He focused on the following fields:

New and improved steelmaking and finishing techniques

RFCS supported projects on highly efficient roll cooling and advanced process control, which allowed

for an optimal use of the assets. Moreover, advanced detection and on-line control systems

improved the management of quality.

Breakthrough CO2 reduction technologies in ironmaking

RFCS pioneered the development of Ultra Low CO2 Steelmaking (ULCOS) and of other promising

technologies as smelting reduction (HIsarna).

Contribution to Circular Economy and improvement of working conditions

RFCS pursued an enhanced use of recycled scrap and waste recycling, as re-use of process water and

waste energy. Moreover, the Programme contributed to the development of sensors, automation

and monitoring systems enhancing health and safety in the workplace. It also improved the air

quality inside the steelworks and safety in construction.

Environmental footprint

RFCS contributed to greening both the steelmaking processes and steel as a product by promoting

the use of alternative carbon sources in electric arc furnace and blast furnace, developing new eco-

friendly coatings and lightweight steel solutions.

Simulation, modelling and quality

RFCS contributed to the development of digital monitoring systems to improve process and product

quality, models of the risk of quality defects, along with predictive simulation on microstructures and

in continuous casting.

Steel product performance

New generations of steel combining strength and ductility, Advanced High Strength Steels (AHSS)

and quenching and partitioning (Q&P) steels have been created also thanks to RFCS support, which

improved steel grades and processing technologies.

New steel applications

High Performance Steel applications, new rules and technologies have been implemented. Practical

tools for testing have been designed with RFCS support.

Table 1. Steel technological achievements

16Coal technological achievements

Ms Elisabeth Clausen, Member of the Expert Group and Mr Nikolaos Koukouzas, Coal Rapporteur,

presented the audience with the most emblematic achievements in the coal sector during 2011-2017.

In particular, they presented achievements in:

Automation and digitalisation in coal mines

RFCS played a role in integrating ICT technologies in coal mines, e.g. new sensors technologies, mine

power engineering and real-time process reconciliation.

Health and safety

Working conditions in mines have improved thanks to the deployment of devices for dust control

and ventilation-on-demand, gas control and novel rescue devices developed with RFCS funding.

Protection of the environment

In accordance and collaboration with the Coal Regions in Transition initiative, mine water usage,

environmental monitoring and land reclamation and restoration highly improved.

Sustainable coal technologies

RFCS underpinned the development of technologies to produce sustainable coal by capturing CO2,

implementing emission reduction systems (smart control and sensors) and co-firing coal with solid

waste or biomass.

Improvement of the use of coal

Innovative and advanced uses of coal as optimised systems to prepare coking fuel blends, co-

processing and improvement on existing catalysts in coal liquefaction, development of novel porous

carbon materials have been supported by RFCS.

Alternative use of coal ensuring energy security of supply

RFCS co-funded projects on underground coal gasification and on production of syngas, simplified

gas cleaning and methanol or Fischer-Tropsch-fuels with the aim of securing the EU energy supply.

Table 2. Coal technological achievements

17Steel and coal in the next decade

The expert group members then turned to the future of the RFCS programme, focusing on the main

challenges that the coal and steel sectors need to tackle in the next decade. The experts also

presented the main recommendations to be raised in the monitoring and assessment report. Overall,

the challenges identified are common to both the steel and the coal industry (climate, digitalisation,

circular economy, health & safety), although certain challenges and all recommendations are intrinsic

to one of the two sectors.

Steel challenges and recommendations

Table 3. Steel challenges and recommendations

Mr Steiler presented the challenges and recommendations for the steel sector (as outlined in Table 3

above). He started by stressing the urgency of taking action on climate change and reducing the steel

industry’s carbon footprint. He said that the EU should lead the global effort in achieving net-zero

10

greenhouse gas emissions by 2050 in a cost-efficient manner and pointed out that energy efficiency

and cost-effectiveness should improve in the next decade thanks to sustainable and high performing

processes.

Although positive steps have been taken to achieve a circular economy, more needs to be done. To

fully close the loop, we need to make improvements in the use of secondary raw materials, waste and

scrap recycling.

After focusing on the environment in which the steel sector operates, Mr Steiler turned the spotlight

on the industry itself. In his view, for the EU steel industry to remain competitive on the global

market, it needs to devise new and improved solutions, such as advanced high-strength steels,

lightweight design and structural safety. Moreover, while new processing technologies and Industry

4.0 may challenge the steel sector, they also represent major opportunities for the sector to develop

further based on new emerging processing technologies, digitalisation, artificial intelligence,

instrumentation and modelling.

In his conclusion, the Chair of the high-level expert group focused on steel workers, highlighting the

need to fully involve them in the changes mentioned above, to continuously enable them to develop

new skills through lifelong learning and to improve their working conditions.

10

A Clean Planet for All — A European strategic long-term vision for a prosperous, modern, competitive and

climate neutral economy, European Commission, COM (2018) 733.

18This final challenge also applies to the coal sector, explained Ms Clausen (see Table 4 below).

Together with Mr Koukouzas, she added that the coal sector should also concentrate on redirecting

skills and that further efforts should be made to increase social acceptance and awareness of the

sector.

Coal challenges and recommendations

Table 4. Coal challenges and recommendations

In addition to the challenges identified for the next decade, all energy-intensive industries agree on

the need to further develop clean technologies to reduce their carbon footprint.

Specific to the coal sector is the push towards technology-intensive mining practice to increase mining

sustainability. Post-mining and land restoration continue to challenge the coal industry, which is

studying new methods to ensure the long-term stability and safety of closed mines. The sector is also

keen to explore alternative use of coal areas for renewables, while increasing the value of coal

products (e.g. gasification and integrated hydrogen production).

Finally, digitalisation and digital transformation challenge the coal industry and provide an opportunity

to improve the sector.

Innovation leakages vs. Open Europe

During the debate with the audience, stakeholders raised concerns that technologies developed with

EU funds may be used in non-EU countries. The Commission representative replied that the EU is

aware of potential ‘innovation leakages’ and is taking measures to limit it. Nevertheless, international

cooperation in research and innovation is important. The EU has been an open area, allowing

exchanges within its borders and beyond them.

On the future of the RFCS programme and its management in the coming years, another stakeholder

questioned the restructuring of the technical groups (TGs) which, according to the legal basis11, advise

the Commission on project monitoring and on defining the programme's priority objectives where

necessary. The TGs will start to be restructured as of 2020 for greater efficiency and effectiveness.

The steel TGs will be merged and reduced from nine to five TGs, whereas the coal TGs will be reduced

from three to two. This reorganisation was endorsed by Steel Advisory Group (SAG), Coal Advisory

Group (CAG) and Committee of Steel and Coal (COSCO) in 2018 and will be presented in the RFCS

Information Package 2019.

11

Council Decision 2008/376/EC, Article 24.

19In his concluding remarks, the Chair recalled that the RCFS programme has brought significant

benefits to the steel and coal sectors and to society. These benefits are maximised through links with

other programmes, notably the Framework Programme for research and innovation that addresses

climate change, energy efficiency, circular economy, digitalisation and health & safety issues.

The RFCS programme is unique in its ability to unite and gather a community that shares knowledge

and disseminates research results. As such, it accomplishes what the architect, Mr Samyn, expressed

in his opening speech: the need to create and share knowledge, not only to produce communication.

This was also one of the objectives of the European integration: uniting Persons, not forming coalitions

of States.

The RFCS programme will continue to achieve this goal, while guiding the coal community towards a

more sustainable future and keeping the steel industry at the forefront of research and innovation of

breakthrough technologies for ultra-low CO2 emissions.

Mr Rossetti thanked those stakeholders and scientists who commented on the preliminary results of

the seven-year RFCS monitoring and assessment and said that their input would be included in the

report to be made available in autumn 2019.

20STEEL AND COAL IN THE NEW ECONOMY

Decarbonisation: Mission possible even for harder-to-abate sectors

Mr Hervé Martin, Head of DG RTD’s Coal and Steel Unit moderated the conference's final session:

‘What’s next? Steel and coal in the new economy’.

Ms Faustine Delasalle spoke on behalf of the Energy Transitions Commission (ETC)12. She invited the

audience to take a step back from the very interesting granular research innovation projects covered

earlier and to look at the future of the steel industry from a broader, global perspective, focusing on

carbon emissions.

The latest IPCC report (2018) ‘Global warming of 1.5 °C’ informed the world of the major negative

impacts on people and the planet of a rise in global temperatures of 1.5 °C and the even more

dramatic consequences of a 2 °C rise which would lead to increased sea levels, more frequent extreme

weather events and forced migrations. IPCC recommends achieving net-zero CO2 emissions globally

by 2050 (Figure 7)13.

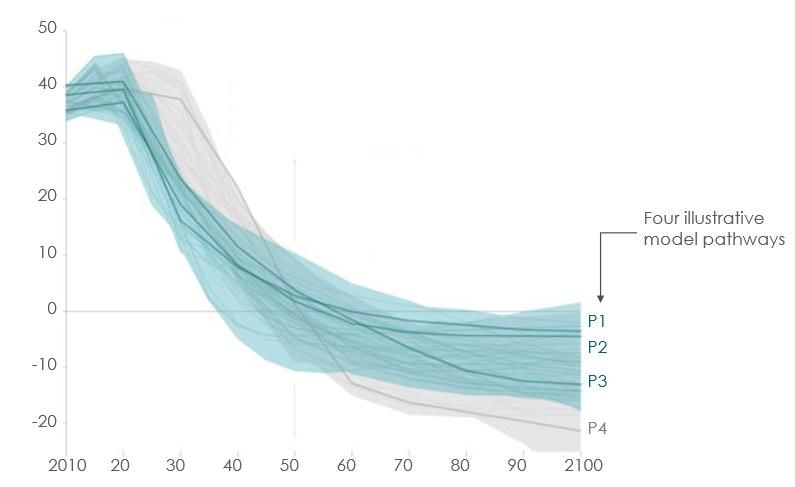

Figure 7. Global emissions pathways, Gt CO2 /year

Both the 2˚C and 1.5 °C scenarios present tremendous challenges for industries, be they the fossil

fuels industry or energy-intensive industries. This is an imperative, but also a major opportunity. The

new economic model will drive rapid technological innovation, increase resource productivity, create

jobs in new industries and deliver local environmental benefits, which increase quality of life.

To that end, the use of fossil fuels - coal in particular - needs to decrease globally. Any coal use that is

not combined with carbon capture should disappear from the system by mid-century.

Figure 7 presents a model trajectory for carbon emission to avoid drastic climate changes. There is a

very similar trajectory for fossil fuel use.

If no action is taken, between 2014 and 2050: (i) transport sector emissions could grow from 7.4 Gt

CO2/year 10.1 Gt CO2/year; (ii) power sector emissions could grow from 13.6 Gt CO2/year to 14.3 Gt

CO2/year; and (iii) iron and steel industry emissions could grow from 2.3Gt CO2/year (7% of a total

emission of 34.3 Gt CO2/year from the energy and industrial system) to 3.3Gt CO2/year (8% of a 39

Gt of CO2/year)14.

In a 2˚C scenario: (i) the power sector should eradicate all CO2 emissions; (ii) the transport sector

should reduce emissions to 4.3 Gt CO2/year; and (iii) iron and steel emissions should fall to 1.3 Gt

CO2/year, increasing their share to 20% of remaining energy and industrial emissions in 2050.

12

ETC is a coalition of global leaders in energy: energy producers, energy consumers, equipment suppliers,

investors, environmental NGOs and academics from the developed and the developing world. ETC explores

ways to comply with the Paris climate agreement to limit the rise in global temperature while enabling robust

economic development.

13

IPCC, Global Warming of 1.5˚C, 2018.

14

IEA, Energy Technology perspective, 2017.

21The ETC examined whether it would be possible to reach net-zero carbon emissions from heavy

industry (in particular steel, cement and chemicals) and heavy-duty transport (heavy-duty road

transport, shipping and aviation) labelled the ‘harder to-abate’ sectors, i.e. the hardest sectors to

decarbonise. The good news is that, after surveying technologies that are currently under

development or already exist, the ETC concluded that reaching net-zero CO2 emissions by mid-

century is technically and economically feasible. Technically, because as seen during the presentations

on RFCS achievements, there are innovative technologies in the pipeline. Economically, as ETC has

calculated that decarbonising all the harder-to-abate sectors by mid-century would cost considerably

less than 0.5% of global GDP.

The ETC expects annual global demand for steel to grow, but that rate of growth will vary significantly

from region to region. For example, it does not expect steel demand to grow substantially in Europe.

The ETC looked at all combinations of solutions to reach a steel net-zero carbon emission pathway and

identified three main routes:

reducing the demand for primary steel;

improving the energy efficiency;

deploying decarbonisation technologies.

For the analysis of the first route, global demand for steel is predicted to grow significantly assuming

that developing countries will seek to achieve the same level of prosperity as developed ones and will

therefore move towards a similar amount of steel per person (measured in tonnes). However,

according to data from various steel applications, most of the growth in global demand could be met

by scrap recycling (if recycling technologies improve), by reducing melting losses and by solving

contamination problems. According to the ETC, Europe's entire steel demand could be met through

scrap-based production.

Car sharing could also have a large impact, as the number of cars on the roads would go down and so

would the amount of steel used in the automotive sector.

Taken together, materials circulation (maximising recycling) and product circulation could lead to a

37% cut in the steel industry's global emissions by 2050 (see Figure 8)15.

Figure 8. CO2 emissions reductions potential in the steel industry

In terms of decarbonising the primary production process, four main pathways that apply to other

industrial sectors and transport have been identified. These are:

direct electrification of industrial processes, in particular the generation of high temperature

heat;

15

Material Economics analysis for the Energy Transitions Commission, 2018.

22 the use of biomass as an energy source for heat production, as a reduction agent in steel

production or as a feedstock in particular for plastics production;

carbon capture, combined with either use or underground storage;

using hydrogen as a heat source, or as a reduction agent in the case of steel and chemicals

production, with zero-carbon hydrogen derived from electrolysis or near-zero-carbon hydrogen

derived from steam methane reforming with carbon capture.

In each industrial sector, the most cost effective route to decarbonisation will likely vary by location,

depending on the local resources.

The ETC examined the determining factors leading one solution to dominate the market rather than

the others and concluded the key factor to be the price of zero-carbon electricity. In the ETC’s

assumption, Europe is likely to produce zero-carbon electricity for around $55/MWh by the 2030.

Therefore, its most competitive option would be carbon capture rather than hydrogen-based

production. China, with its large potential for exploiting renewable resources in its North-western

provinces, will probably be able to produce zero-carbon electricity for around $30/MWh. It therefore

might engage in hydrogen-based production and be able to produce zero-carbon steel at a lower price

than the European steel industry.

Decarbonisation technologies are more expensive than current technologies. Therefore, a combination

of market forces and policy-drivers will be needed to enable the switch. The cost of decarbonisation

may seem very high to the industry today, but the additional cost for the end-consumer will be

relatively low, given that steel accounts for only a small proportion of the overall cost of a car. This

opens up great opportunities, because one could imagine a ‘niche market’ starting to develop where

end-consumers and consumer-facing producers, knowing that the impact on the prices will be low,

decide to respectively buy and produce products with green steel, and are able to cover the additional

cost.

23Land-use rehabilitation in coal regions in transition

Mr Jan Bondaruk, Deputy Director for Environment at Glówny Instytut Górnictwa (GIG), painted a

more optimistic picture of the decarbonisation process, giving concrete examples from one of the coal

regions involved in the transformation.

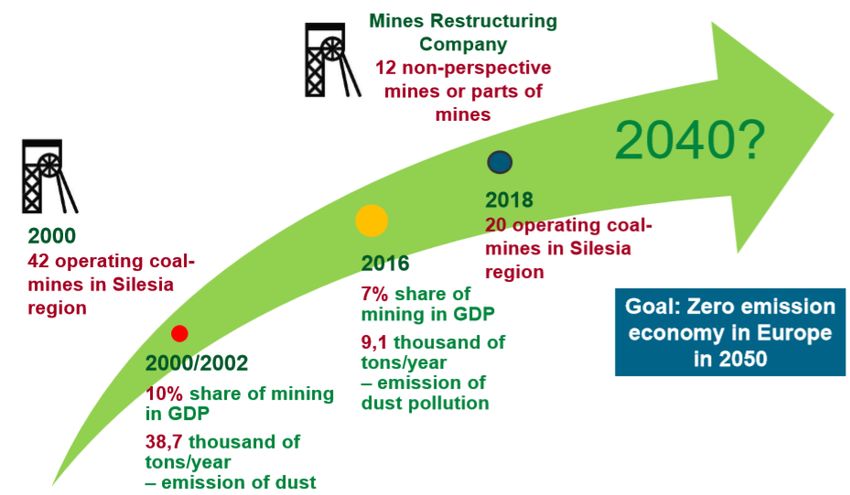

He reported that in 2000 there were 42 operating coal mines in Silesia (Poland), which accounted for

10% of the GDP. In 2018, 20 coal mines were still operating (see Figure 9)16. As the ultimate goal for

all European regions is to achieve a zero emission economy by 2050, Mr Bondaruk considered that a

significant number of areas will be abandoned or degraded unless appropriate action is taken.

‘We are looking at this process not as a disaster but as a chance’, he said. According to him, post-

mining could be a key economic asset for the circular economy, for geothermal energy from mine

water, post-mining infrastructure and cultural and leisure services.

A particularly successful reconversion strategy is the transformation of Eminenzgrube (former coal

mine compounds) into the Silesia city centre in Katowice. This initiative demonstrates the importance

of land rehabilitation for the revitalisation of post-industrial areas. Mr Bondaruk believes that the

Silesia region is one of the best examples of the benefits of environmental economic transformation.

Researchers are already exploring the potential benefits of further developing this reconversion

strategy.

Figure 9. Transition pathway in Poland - Silesia

Mr Bondaruk also stressed that the European Research Fund for Coal and Steel has provided an

opportunity to accumulate knowledge and create new ideas and solutions for the post-mining sector.

Researchers in Silesia have started promoting the smart closure of mines to reuse these newly

abandoned areas in the most sustainable way, looking at different possible scenarios. One valuable

approach is ecosystem restoration. This has enormous potential for creating a new value chain, but as

it is not yet a mainstream practice there is no information available on the cost-effectiveness of land

rehabilitation. Despite this, there are many examples of efficient and cost-effective restoration

projects that respect the ecosystem and biodiversity and directly or indirectly benefit local authorities

and society.

16 GIG, Transition Pathway in Poland, 2019.

24A key aspect of ecosystem restoration is how to determine which land rehabilitation and ecological

restoration options will deliver the greatest return on investment considering maintenance costs.

The restoration planning and prioritisation framework developed by the researchers sets out five

steps:

mapping and assessing ecosystem services;

formulating alternative actions with stakeholder involvement;

assessing land rehabilitation techniques;

cost-benefit assessment;

conducting restoration strategies.

The researchers noted that as financing is still a critical consideration, the cost-benefit assessment is

the most crucial step and needs to be constantly reassessed. To assist this process, an information

platform called ‘Post-industrial and degraded areas’ (OPI-TPP) was launched in 2013 and is available

to public access for acquiring, processing and sharing data on all industrial areas that face a similar

challenge.

Mr Bondaruk concluded by affirming that post mining provides a number of positive outcomes. For

example: creating new jobs; generating measurable economic value; reducing the ‘consumption’ of

green spaces; new energy and heating schemes in urban areas near post-mining areas (e.g. closed

mines can either generate or accumulate energy); and greater collaboration between industry,

researchers and local authorities.

25March for a Clean Europe

Mr Peter Dröll, Director for Industrial Technologies in DG RTD, thanked the speakers and summarised

the main points, giving his personal views on the outcome of the conference.

The fact that every Friday students are marching in the streets calling for stronger action to protect

our planet should make us reflect and possibly join them, he said. Striving for a greater level of

ambition should be the way forward. He invited the coal sector to replicate in Europe the second-

generation carbon capture and storage installation at the Boundary Dam coal power plant in Canada,

which — referring to Mr Rogala’s (Euracoal) presentation — will be significantly cheaper than the

current carbon capture and storage plant.

Mr Dröll was pleased that the conference participants consider the ambitious 'decarbonisation by 2050'

target to be achievable. In this regard, he noted that the RFCS' significant portfolio of projects is

largely thanks to the effort and involvement of a wide range of stakeholders that are part of this

community.

Mr Dröll stressed that the EU should remain an industrial leader — a point also made by the European

Council in the conclusions of its 22 March 2019 meeting. A declining industry could push citizens to

more easily embrace the promises of populist politicians, putting the EU at risk of reversing its hard-

won integration. The time has therefore come to develop an assertive EU industrial policy underpinned

by green targets to save our planet: ‘If coal and steel sectors can take the leadership, it will be good

for us, for the planet and for the economy’.

The conference was also a good opportunity to take stock of the work carried by the high-level group

of experts for RFCS monitoring and assessment (2011-2017). Mr Dröll expressed his appreciation of

the group's work and the preliminary results that will be enriched by stakeholders' views.

26You can also read