Stronger productivity growth would put Malaysia on a path to become a high-income economy

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Stronger productivity growth would put Malaysia on a path to become a high-income economy By Hidekatsu Asada and Patrick Lenain, South-East Asia Desk, OECD Economics Department Malaysia is enjoying remarkable economic growth. Real GDP grew at an average rate of 6.1% per year over 1970 to 2018 period, and short-term prospects are for growth to reach almost 5% in 2019-20, despite a difficult international environment. Thanks to pragmatic policies, Malaysia has transformed from an agricultural-based to an industrial- and services-based powerhouse deeply integrated in global supply chains. Living standards are now close to two-thirds of the average in OECD countries (Figure 1) and per capita GDP exceeds levels in Mexico, Turkey and Chile. The Mid-Term Review of the Eleventh Plan, announced in October 2018, postponed the target year of achieving a high- income nation status from 2020 to 2024 due to recent macroeconomic developments. To achieve the planned target would require implementing an ambitious agenda of reforms focused on productivity gains and skills development (OECD, 2019).

Since the mid-1990s, Malaysia has embarked on a programme to promote innovation and transform the economy from an input-driven to a knowledge-based one (EPU, 2015a). However, Malaysia’s productivity levels remain weak and the economy is still highly dependent on, and driven by factor inputs, especially non-ICT capital accumulation. As a result, Malaysia’s productivity level continues to lag behind most advanced countries. For instance, based on purchasing power parity terms, Malaysia’s productivity level in 2019 was about half that of the United States and Singapore (Figure 2). On the other hand, Malaysia’s productivity level is ahead of its regional peers like Thailand, China, Indonesia, India and Viet Nam. However, these countries experience higher productvity growth than Malaysia, implying a

rapid catching up of these countries. Human capital development is a key priority to boost Malaysia’s labour productivity. The importance of improving human capital has been highlighted in most development plans and industry-specific masterplans. Currently, Malaysia’s industries are excessively dependent on semi- and low-skilled workers and foreign low-skilled labour (MEA, 2018), as shown by the ratio of skilled workers to total employment, which is still low at 27.2% as compared to the target of 35% by 2020 set by the government (EPU, 2015b). As a result, the contribution of labour quality to economic growth remains low. On average, labour quality contributed only about 8% to real GDP growth over 2001-18, much lower than the OECD average. Skilled workers are crucial to facilitate innovation and technology adoption as well as to promote upgrading of activities to unlock potential economic growth. Therefore, efforts need to be intensified in producing high-quality talent pool to support the Malaysian government’s aspiration of becoming an advanced and inclusive country.

References EPU. (2015a). The Eleventh Malaysia Plan Strategy Paper 1 : Unlocking the Potential of Productivity. Economic Planning Unit, Prime Minister’s Department, Purtajaya. EPU. (2015b). The Eleventh Malaysia Plan, 2016-2020. Economic Planning Unit, Prime Minister’s Department, Putrajaya. MEA. (2018). Mid-Term Review of the Eleventh Malaysia Plan. Ministry of Economic Affairs, Putrajaya. OECD. (2019). 2019 OECD Economic Survey of Malaysia. Paris: OECD. http://www.oecd.org/economy/malaysia-economic-snapshot/ Offering better labour-market opportunities to all Malaysian women: a win-win strategy by Marieke Vandeweyer, OECD Directorate for Employment, Labour and Social Affairs The Malaysian labour market is facing substantial skills imbalances, including shortages in a range of occupations and

skills. To tackle these imbalances, the 2019 OECD Economic Survey of Malaysia features a special focus on skills development and on how better labour-market opportunities could be offered to all Malaysian women. Malaysian women participate much less in the labour market than men, in spite of similar levels of educational attainment. Only 55.2% of working age women are active in the labour market, compared with 80.4% of men. This gap is larger than in OECD countries, where the difference only equals 16 percentage points. In most OECD countries, the gap in participation rates between men and women reaches its peak in the age group of 30 to 39 year olds, after which it decreases for older age groups. In Malaysia, by contrast, the gap significantly increases at the age of 30 to 34, and continues to grow for older age groups. These numbers suggest that many women leave the labour market in their early thirties, probably because of childcare responsibilities, and do not return to work after that. The Malaysian government has set the goal to increase female labour market participation to 56.5% by 2020. Initially, this target was set at 59%, but because of slow progress the target has been revised downward.

Barriers to labour market participation can be reduced by

promoting family-friendly policies, including:

employment-protected paid leave around

childbirth and when children are young

subsidised childcare

and a statutory right to request flexible work.

The current right to maternity leave in the private sector

in Malaysia is below the 14 weeks minimum that is stipulated

in the ILO

Maternity Protection Convention. Moreover, the full cost of

the maternity

allowance in Malaysia is covered by employers, which could

create a strong

disincentive for employers to hire women of childbearing age.

Access to

reliable and affordable childcare facilities in Malaysia is

limited, although

several financial incentives exist for parents and foremployers to provide on-site childcare facilities. Finally, access to flexible work arrangements is limited, making it difficult for parents in Malaysia to combine work and family responsibilities. To help women return to work after a career break, they would benefit from targeted career guidance and training opportunities. The Malaysian Career Comeback Programme provides tax incentives and training to women returning to work, but also offers grants to employers for implementing or enhancing programmes or campaigns to recruit women returnees and for hiring and retaining women returnees. More efforts like these are needed to help women (re-) enter the labour market and ensure that their skills are put to good use. http://www.oecd.org/economy/malaysia-economic-snapshot/ Are there ways to protect economies against potential future housing busts? by Boris Cournède, Maria Chiara Cavalleri, Volker Ziemann, OECD Housing, a large and volatile sector, is often at the centre

of economic crises, as a trigger or amplifier. The current

situation, which is characterised by house prices approaching

or exceeding pre-crisis levels in many countries, raises

questions as to whether these price levels may be indicative

of a possible impending correction and what can be done to

reduce housing-related macroeconomic risks.

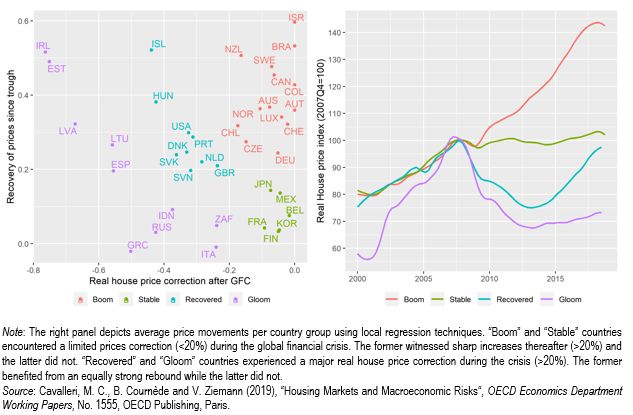

Figure 1. House price developments since the global financial

crisis

The OECD has been developing models that allow assessing to

which extent economic trends associated with housing booms,

such as steep house price increases or strong debt expansion,

can fuel the risk of a severe economic downturn (Turner,

Chalaux and Morgavi, 2018). About half of the countries

covered by the models are estimated to face real yet limited

risks (above 20% but below 30%) of experiencing a severedownturn over the medium term, with housing trends playing a

significant role.” Model results suggest that housing booms

can fuel crisis risk domestically but also across borders as a

consequence of international financial links (Cavalleri,

Cournède and Ziemann, 2019).

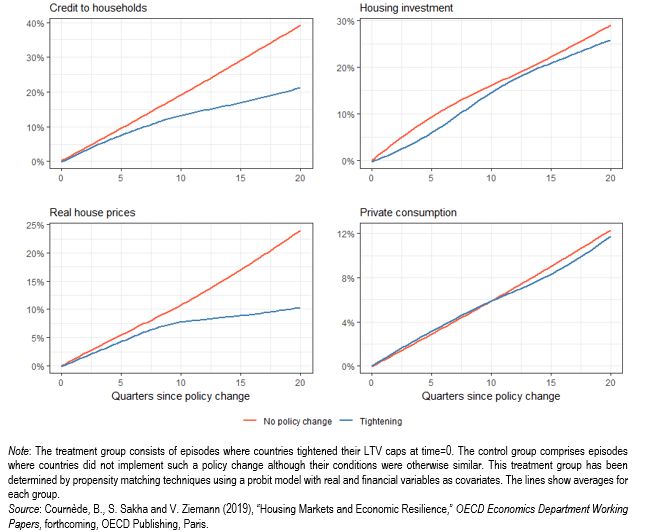

Countries can reduce housing-related risks in particular by:

Capping the size of loans relative to house prices. New

evidence suggests that such caps are capable of

containing house prices and mortgage lending incurring

limited economic cost (Figure 2): housing investment is

only marginally reduced and there is very little effect

on consumption. Tighter loan-to-value ratios are also

linked with a lower risk of severe downturns.

Limiting the size of loans relative to income. This

measure holds promising potential but has been seldom

used so far, which means there is little scope yet to

evaluate it ex post.

Tightening bank capital requirements for riskier housing

loans. Measures of this nature are linked to more

moderate output fluctuations and stronger recoveries

after downturns.

Reducing the tax advantages given to housing assets.

Higher effective taxation of housing assets (which can

come from higher property taxes or lower income tax

breaks for housing) favours smoother housing cycles.

Figure 2. Effect of tightening LTV capsReferences: Cavalleri, M. C., B. Cournède and V. Ziemann (2019), “Housing Markets and Macroeconomic Risks“, OECD Economics Department Working Papers, No. 1555, OECD Publishing, Paris. Turner, D., T. Chalaux and H. Morgavi (2018), “Fan Charts around GDP Projections Based on Probit Models of Downturn Risk”, OECD Economics Department Working Papers, No. 1521, OECD Publishing, Paris.

Des réformes doivent être engagées maintenant pour s’adapter aux évolutions du monde par Laurence Boone, Cheffe économiste de l’OCDE Des réformes doivent être engagées maintenant pour s’adapter aux évolutions du monde La mondialisation, la transition numérique, le vieillissement démographique et la dégradation de l’environnement sont autant de mégatendances qui déterminent ce que seront, demain, les niveaux de vie et le bien-être. Or, en l’absence d’une reprise de la dynamique des réformes, les perspectives s’annoncent moroses. L’économie mondiale risque de voir à nouveau souffler des vents contraires, avec une croissance qui va fléchir sur fond d’incertitudes commerciales fortes. Parallèlement, les gains de niveaux de vie tels que mesurés par le PIB par habitant n’ont pas encore retrouvé leur niveau d’avant la Grande crise financière. Tous ces facteurs devraient inciter les responsables de l’action publique à engager les réformes nécessaires pour instaurer une croissance plus vigoureuse, plus inclusive et écologiquement durable, et permettre à tous les citoyens de tirer le meilleur parti des perspectives offertes par ce nouvel environnement. L’édition 2019 d’Objectif croissance présente, à l’intention des décideurs publics de chaque pays, un ensemble de priorités de réformes nationales spécifiques qui doit permettre de se préparer aux évolutions futures et de transformer les défis liés aux mégatendances en chances pour tous.

Les gouvernements s’emploient de plus en plus à relever les défis sociétaux et cela commence à porter ses fruits Si l’on examine les résultats des réformes obtenus au cours des deux dernières années, on aboutit à un bilan mitigé. Le rythme global des réformes est retombé à son modeste niveau d’avant la crise, mais plusieurs pays ont tout de même réussi à mettre en oeuvre des réformes majeures, répondant directement à des priorités énoncées dans des éditions passées d’Objectif croissance. On peut citer comme exemples des réformes visant à stimuler l’emploi et à rendre le marché du travail plus inclusif. La France a ainsi amélioré les négociations collectives et la sécurité juridique des licenciements, réformé les règles de l’assurance-chômage et renforcé les prestations liées à l’exercice d’un emploi. Le Japon de son côté a pris des mesures pour améliorer l’offre de services d’accueil de jeunes enfants et adopté de nouvelles lois sur les heures supplémentaires afin d’améliorer l’équilibre vie professionnelle-vie privée. Des actions de simplification de la réglementation et des mesures relevant de la politique fiscale ont été également mobilisées pour soutenir l’investissement et la croissance des entreprises, mais aussi pour donner aux pouvoirs publics les ressources nécessaires à la redistribution. Ainsi, les États- Unis ont abaissé le taux de l’impôt sur les bénéfices des sociétés et réformé la fiscalité des entreprises, mesures qui font partie depuis longtemps des priorités formulées dans Objectif croissance. L’Inde a procédé à une réforme fiscale qui fera date avec l’introduction d’une taxe sur les biens et services. D’autres pays, comme l’Espagne, la Grèce et la Pologne, ont pris d’importantes mesures pour améliorer le

recouvrement de l’impôt. Plusieurs pays ont fait en sorte de faciliter l’entrée sur les marchés et d’offrir des règles du jeu équitables aux entreprises en réduisant les lourdeurs administratives, en déréglementant les services professionnels et les secteurs de réseaux ainsi qu’en renforçant les pouvoirs des autorités de la concurrence. Les gouvernements ont également intensifié leurs efforts de réforme pour relever les défis sociaux. La Grèce et l’Italie ont adopté des plans nationaux de lutte contre la pauvreté. En Inde, le raccordement de tous les villages à l’électricité a été achevé et le pays a mis en place un régime national de protection santé ciblant 100 millions de familles pauvres. La Chine a obtenu des avancées dans la réduction de la fracture entre les zones rurales et les zones urbaines qui caractérisait son système de santé en améliorant la portabilité de l’assurance maladie. Toutes ces réformes ont déjà pour effet d’améliorer la vie de millions de personnes. Pourtant, il reste encore à faire, et Objectif croissance se fait l’écho de l’expertise des spécialistes de l’OCDE quant aux domaines sur lesquels les responsables de l’action publique devraient concentrer leur action de réforme afin d’offrir aux générations futures une croissance durable et inclusive. Il faut faire davantage, notamment en matière de réformes susceptibles de déboucher sur des résultats plus forts et plus justes Les priorités de réforme destinées à promouvoir une croissance inclusive diffèrent d’un pays à l’autre. De fait, l’éducation est la priorité de réforme la plus largement partagée, et elle

est indispensable pour garantir un emploi aux générations actuelles et futures, de façon à stimuler la productivité et à donner à chacun les meilleures chances de mener une vie épanouissante. Un grand nombre de recommandations relevant du domaine de l’éducation mettent l’accent sur un meilleur ciblage des ressources en direction des élèves et des établissements défavorisés ; c’est le cas dans de nombreux pays d’Europe et d’Amérique latine, mais aussi aux États-Unis. Pour des économies de marché émergentes comme l’Inde ou l’Afrique du Sud, il est recommandé de moderniser les infrastructures scolaires. La croissance et l’égalité des chances pourront aussi bénéficier de mesures visant à remédier au cloisonnement du marché du travail ainsi qu’à améliorer l’intégration des femmes, des migrants, des minorités et des travailleurs seniors sur le marché du travail, autant de mesures qui constituent un autre ensemble de priorités d’Objectif croissance, en particulier en Europe, mais aussi aux États- Unis, au Japon et dans plusieurs économies de marché émergentes. Des réformes fiscales visant à donner plus de poids à la fiscalité du patrimoine constituent une priorité à l’appui de la croissance dans de nombreux pays, notamment des économies avancées. Faire en sorte d’améliorer l’efficience du secteur public, de renforcer l’état de droit et d’offrir des infrastructures appropriées et accessibles sont des mesures qui comptent pour économiser les ressources, ouvrir l’accès aux marchés et créer des conditions favorables aux entreprises et à l’innovation, en particulier dans les économies de marché émergentes, mais pas seulement. Les réformes des marchés de produits constituent un domaine où

les pays ont tendance à prendre du retard. De fait, ces réformes sont souvent délicates et leur mise en oeuvre parcellaire, mais l’ouverture des marchés à l’entrée, à la concurrence ainsi qu’aux échanges et investissements étrangers est essentielle pour favoriser l’innovation, la diffusion des technologies numériques et, au final, les gains de productivité et l’inclusion sociale. Des réformes de ce type restent parmi les fréquemment préconisées dans Objectif croissance. Objectif croissance contient des orientations à l’intention des responsables de l’action publique sur les domaines où ils peuvent concentrer leurs efforts de réforme pour assurer le bien-être de leurs concitoyens et pour asseoir une croissance forte, durable, équilibrée et inclusive. Cela étant, certaines des priorités énoncées relèvent d’un effort coordonné de l’ensemble des pays, notamment en ce qui concerne l’ouverture aux échanges, les droits de propriété intellectuelle, la fiscalité des entreprises multinationales, le changement climatique, la sauvegarde des océans ou encore le traitement des déchets. En tant que telles, elles viennent utilement nous rappeler les avantages de la coopération multilatérale. La croissance doit être écologiquement durable Répondant à l’urgence climatique et en écho à l’Accord de Paris, la présente édition d’Objectif croissance aborde pour la première fois les problématiques sous l’angle de la viabilité environnementale. Partout dans le monde, les tensions sur l’environnement s’intensifient, et constituent une menace pour la soutenabilité des gains de croissance et de bien-être. Aucune stratégie de croissance durable ne saurait se concevoir sans des mesures de lutte contre la pollution de l’air, le changement climatique et d’autres grands problèmes

environnementaux. En conséquence, la plupart des pays, y compris les plus grands pollueurs de la planète, se sont vu attribuer des priorités et recommandations de réforme qui visent à la fois les freins mis à la croissance et les goulets d’étranglement environnementaux. Ces réformes doivent être engagées maintenant, pour assurer une vie meilleure aux citoyens d’aujourd’hui et aux générations futures. The time for reform is now to respond to global challenges by Laurence Boone, OECD Chief Economist Globalisation, digitalisation, ageing and environmental degradation are the megatrends shaping tomorrow’s living standards and well-being. The prospects look weak in the absence of renewed reform dynamism. The global economy is facing further headwinds, with growth weakening in the wake of high trade uncertainty. At the same time, gains in living standards, as measured by GDP per capita, have been much slower since the Great Financial Crisis. All this should prompt policy makers to implement necessary reforms to deliver

on stronger, more inclusive and environmentally-sustainable growth and help people make the most out of opportunities created in this new world. This 2019 Going for Growth edition offers policy makers a set of country-specific reform priorities to prepare for the future and turn mega-trend challenges into opportunities, for all. Governments are increasingly addressing social challenges and reforms are paying off Looking back at reform achievements over the past two years gives a contrasted picture. Although the overall pace of reforms has returned to the modest pre-crisis pace, a number of countries have managed to implement major reforms – reforms that respond directly to past Going for Growth priorities. Significant examples include reforms to lift employment and make the labour market more inclusive. France improved collective wage bargaining and legal certainty for dismissals, reformed the rules for unemployment insurance and increased in-work benefits. Japan took steps to improve childcare provision and new laws on overtime work to improve work-life balance. Regulatory simplification and tax policy have also been used to support firms’ investment and growth, but also provide governments with necessary resources for redistribution. The

United States has cut corporate income tax rates and reformed business taxation – a long-standing Going for Growth priority. India implemented a landmark tax reform with the introduction of its Goods and Services Tax. Other countries, such as Greece, Poland and Spain took significant measures to improve tax collection. Several countries took measures to facilitate firm entry and level the playing field for businesses by reducing red tape, deregulating professional services and network sectors as well as by reinforcing competition authorities. Governments have also intensified reform efforts to tackle social challenges. Greece and Italy rolled-out nationwide anti-poverty schemes. India finalised the connection of all its villages to electricity and launched a national health protection scheme targeting 100 million poor families. China made progress on bridging the rural-urban divide in its health care system by increasing the portability of health insurance. These reforms are already improving the lives of millions. Yet, there is more to do, and Going for Growth reflects OECD’s expert judgement on where policy makers need to focus reform actions to deliver sustainable and inclusive growth for future generations. More needs to be done, especially on reforms that ensure stronger and fairer outcomes The reform priorities to boost inclusive growth differ across countries. Education is the most common reform priority and is crucial to make sure current and future generations find

employment, which would both boost productivity and give everyone the best chance for a fulfilling life. A significant number of recommendations in the area of education focus on improving the targeting of resources to disadvantaged students and schools, for example in many European and Latin American countries, as well as the United States. Upgrading school infrastructure is a recommendation in emerging-market economies such as India and South Africa. Both growth and equal opportunities will also benefit from addressing labour market segmentation and improving the labour market inclusion of women, migrants, minorities and older workers – another set of top Going for Growth priorities, in particular in Europe, but also in the United States, Japan and several emerging-market economies.. Tax reform, with increasing reliance on property taxation, is a pro-growth priority in many, particularly advanced economies. Better public sector efficiency, rule of law and adequate, accessible infrastructure provision are equally important to save resources, access markets and create conditions for businesses to invest in innovation, in particular, but not only in emerging-market economies. Where countries have tended to lag behind is product market reforms. Reforms are often difficult and granular in implementation, but opening up markets to entry, competition and foreign trade and investment are essential for innovation, the diffusion of digital technologies and

ultimately productivity growth and social inclusion. Such reforms remain among the most frequent Going for Growth priorities. Going for Growth guides policy makers where to focus their reform efforts for the well-being of their citizens and to achieve strong, sustainable, balanced and inclusive growth. However, some priorities require a co-ordinated effort by all countries. Examples include trade openness, intellectual property rights, taxation of multinational enterprises, migration, climate change, oceans and waste. As such, they are a useful reminder of the benefits of multilateral co- operation. Growth has to be environmentally sustainable Responding to the urgency of climate change and to the Paris agreement, this edition of Going for Growth includes an environment sustainability angle for the first time. Around the world, environmental pressures are mounting, posing a threat to the sustainability of gains in growth and well- being. Tackling air pollution, climate change and other key environmental problems have to be part of a sustainable growth strategy. As a result, most countries, including key global polluters, have reform priorities and recommendations that address both growth and environmental bottlenecks. The time for reform is now, for better lives today and for future generations!

> Making access to housing more affordable to all in Luxembourg by Jan Strasky, Luxembourg Desk, OECD Economics Department Luxembourg’s economy has been buoyant – robust growth has strongly outpaced the euro area average over most of the past decade. However, this success creates new problems, in particular in the housing market, which the 2019 Economic Survey of Luxembourg [link] analyses in detail. Strong population growth, mainly reflecting the number of foreign workers attracted by a buoyant economy, has kept housing demand growing for many years. When coupled with supply-side restrictions, such as limited use of land available for construction and cumbersome zoning restrictions, the imbalance between demand and supply stokes rising house prices (Figure 1). Increasing mortgage debt also raises the debt service burden for a larger share of households than in other countries and a tight rental market impedes housing affordability for poorer parts of the population.

As the housing stock has not expanded in line with growing demand for many years, the essential part of the solution is an increase in construction of new housing. Although the land available for housing construction seems sufficient, it is mainly in private ownership and many landowners do not have a strong incentive to sell or develop their land. In order to reduce the practice of land hoarding, where constructible land is kept undeveloped to capitalise on continuing land price increases, the opportunity cost of holding land for construction should be increased. Possible ways of doing so include introducing land value taxes on land zoned for housing construction or imposing sanctions on landowners and developers for non-use of building permits. Higher recurrent taxes on immovable property, based on up-to-date valuations reflecting the market price of the

property, could also help to incentivise the owners to sell vacant dwellings (Figure 2). Both municipalities and the central government could improve the situation in this area. Municipal autonomy in spatial planning decisions is high and the current framework has not delivered sufficient supply of housing. Some instruments exist in the law, but are simply not used. This is the case of an annual tax on constructible land not developed for more than three years, and also of a tax on unoccupied housing. Other instruments, such as a special property tax on building land for residential purposes, were introduced more broadly, but they are based on obsolete cadastral valuations and provide negligible revenues.

Given the high level of urban sprawl, which has important environmental costs, new housing construction should aim at increasing residential density, namely by constructing higher buildings, in particular around transport hubs. To soften municipal resistance to densification, the targets on new housing construction agreed between the municipalities and the central government in the Housing Pact could be extended to include numerical targets for densification measures or social housing construction. It is clear that a lot remains to be done by the central government, too. For example, a reduction of mortgage interest deductibility could help reduce demand for owner-occupied housing, while financing for new land acquisition by public providers of social housing would help expand the stock of social rental housing. Measures reducing demand for owner-occupied housing would also help reduce the build-up of already high household indebtedness, which creates risks for poorer households (Figure 3).

The stock of social rental housing is small in international comparison, despite recent efforts by social rental management companies, and often allocated to tenants who are not those most in need. The low stock reflects many factors, including the historical policy of building affordable housing for sale, which could later be re-sold on the private market. This practice has now been phased out and the public housing providers focus on building social housing for rental, rather than for sale. The allocation of social housing also needs to be improved. The admission criteria for social housing are often flexible and with low transparency. Recurrent means- testing should be combined with tailored plans for re-entering the private rental sector, similar to those used by social rental agencies. Housing allowances and rents in the social housing sector could also become more geographically differentiated, reflecting the differences in market rents across municipalities: for example, Luxembourg City has clearly higher market rents than the north of the country. Reference:

OECD (2019), OECD Economic Surveys: Luxembourg 2019, OECD Publishing, Paris.

You can also read