Swedbank Investor presentation - February 2018

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Swedbank Investor

presentation

February 2018

© Swedbank Information class

Public

Disclaimer

Certain statements made in this presentation are forward looking statements. Such statements are based on current expectations

and are subject to a number of risks and uncertainties that could cause actual results and performance to differ materially from

any expected future results or performance, express or implied, by the forward looking statements. Factors that might cause

forward looking statements to differ materially from actual results include, among other things, regulatory and economic factors.

Swedbank AB assumes no responsibility to update any of the forward looking statements contained herein.

No representation or warranty, express or implied, is made or given by or on behalf of Swedbank AB or its directors, officers or

employees or any other person as to the accuracy, completeness or fairness of the information or opinions contained in this

presentation. None of Swedbank AB or any of its directors, officers or employees nor any other person accepts any liability

whatsoever for any loss howsoever arising from any use of this presentation or its contents or otherwise arising in connection

therewith.

This presentation does not constitute or form part of any offer or invitation to sell or issue, or any solicitation of any offer to

purchase or subscribe for, any securities of Swedbank AB, nor shall it or any part of it nor the fact of its distribution form the basis

of, or be relied on in connection with, any contract or investment decision.

© Swedbank Information class

Public

2

Table of contents

Executive summary 4

1. Swedbank overview 5

2. Quarterly financial update 15

3. Capital considerations 25

4. Liquidity and funding 30

5. Cover pool data 39

6. Swedish and Baltic economy 46

7. Swedish housing and mortgage market 55

8. Appendix 70

© Swedbank Information class

Public

3

Executive summary

Strong financial position Top 10 shareholders

■ Sweden’s largest retail bank with a leading position in our three Baltic home markets 1. Sparbanksgruppen, 10.3%

2. Folksam, 7.0%

■ ROE target of at least 15% 3. AMF, 5.5% Our four

4. Alecta, 4.5%

■ Strong asset quality! 5. Swedbank Robur, 4.1%

home

6. Sparbanksstiftelser, 3.3% markets

■ Solid liquidity and funding position – survival horizon more than 12 months 7. BlackRock, 2.5%

■ One of the best capitalised banks in Europe* with significant buffers to both MDA and Loss 8.

9.

Vanguard, 2.4%

Norges Bank, 2.0%

absorption trigger levels 10. SEB Fonder, 1.8%

■ Dividend policy of 75% - for six consecutive years Swedish owners, 59.5%

*According to EBA stress test 2016 Int’l owners, 40.5% Sweden

Swedbank Q4 2017 (Q3 2017) – Robust performance!

■ ROE: 14.4% (15.0%)

■ Cost/income ratio: 0.42 (0.37)

■ CET1 capital ratio: 24.6% (23.9%) – with requirements of 21.9% (fully loaded CRD IV) Estonia

■ Leverage ratio: 5.2% (4.7%) Latvia

■ Credit impairment ratio: 0.08% (0.06%) Lithuania

■ Share of impaired loans: 0.55% (0.55%)

■ Total provision ratio for impaired loans: 45% (45%)

■ Liquidity and funding: LCR: 173%, NSFR: 110%

■ Credit ratings: AA-(S)/AA-(S)/Aa3(S) from S&P/Fitch/Moody’s

© Swedbank Information class Dec 2017

Public

4

This is

Swedbank

1. Swedbank overview

© Swedbank Information class

Public

Swedbank This is

Swedbank

Low-risk, cost efficient and well capitalised

Large and diversified customer base Low risk

Leading retail bank in our 4 home markets Credit impairment ratio

7m PRIVATE CUSTOMERS 0.08%

Focus on Mid-corp and SME segments Market-leading cost efficiency

18% corporate lending market share in Sweden Cost income ratio

600k CORPORATE CLIENTS 39%

Stable profitability Solid capitalisation

Return on equity target of at least 15% 270bps buffer to regulatory requirement

15.1% 24.6%

© Swedbank Information class Note: Numbers for full year 2017

Public Source: Swedbank Fact book 4Q 2017

6Market leading position in our home markets This is

Swedbank

Loans (private)* Loans (corporate)* Deposits (private) Deposits (corporate) Payments** Funds

17% 21% 20% 20%

23%

36%

80% 64%

Sweden 77% 83% 79% 80%

37% 42%

46% 45% 44% 41%

54% 63% 55% 56% 58%

59%

Estonia

18% 16%

31% 32%

42%

50% 58%

69% 50%

68% 84%

Latvia 82%

18% 23%

34% 40% 37%

51% 49%

66% 60% 63%

Lithuania 82% 77%

* Excluding the Swedish National Debt Office and repurchase agreements Swedbank Other

** Bank Giro for Sweden, domestic payment transactions (Estonia, Latvia, Lithuania)

© Swedbank Information class Source: Swedbank Fact book 4Q 2017

Public

7Strong financial position This is

Swedbank

Low risk Stable earnings Market-leading cost

Liquidity and capital ratios (%) Profit before impairments (SEK bn)

efficiency

Total expenses (SEK bn)

10 20

NSFR LCR CET1 ratio, CRDIV (RHS)

One-offs from disposals Acquisition of Sparbanken…

200 30

8 18

25

150

20 6 16

100 15 4

14

10

50 2

5 12

2012 2013 2014 2015 2016 2017 Target

0 0 0

18

2012 2013 2014 2015 2016 2017 Q4 12 Q4 13 Q4 14 Q4 15 Q4 16 Q4 17

Credit impairment (bps) Return on equity (%) Cost / income ratio (%)

40 18 60

16 55

30 14

12 50

20 10

45

8

10

6 40

0 4

2 35

-10 0

30

Q4 12 Q4 13 Q4 14 Q4 15 Q4 16 Q4 17 2012 2013 2014 2015 2016 2017

2012 2013 2014 2015 2016 2017

© Swedbank Information class Source: Swedbank Fact book 4Q 2017

Public

8Stable and profitable business mix This is

Swedbank

- retail bank profile

Total income Net Interest Income Net Commission Income

NII NCI NGL Other

• 86% of total loans in Sweden • Sweden’s largest fund

100% • 51% Swedish mortgages manager (SEK1.2trn AuM)

90% • 5th largest card acquirer &

10th largest card issuer in

80% • Baltic banking very profitable Europe

70% • 10% of Group lending

60% • 20% of Group operating Other

13%

50% profit, FY2017

Asset

40%

Management

Lending and 11%

30% deposits

2017

63% Total

20% Payment,

income Cards

9%

10%

Treasury,

0% Trading and

2015 2016 2017 Capital

Markets

4%

© Swedbank Information class Source: Swedbank Fact book 4Q 2017

Public

9Swedbank strategy

Strategy

An available

full-service bank

Sustainability

and customer Offering based on

Low risk value through a customer need and

responsible expectations

core business

High cost

efficiency

© Swedbank Information class

Public

10Key priorities Strategy

Customer Interaction Savings Lending & Payment

Seamless omni-channel Regain market share through Fully-digital

customer journey high-quality digital savings offer mortgage process

Enhance corporate relationships

Proactive, tailor-made product Increase focus on

with our improved cash

offers and advice pension savings

management solution

One financial access point for Customer-centric Most convenient payments

customers Financial Planning Platform solutions for consumers

© Swedbank Information class

Public

11Digitalisation – cost and income opportunities Strategy

90% of our customers are happy or very happy with our digital services

Increase revenue via digital banking Improve cost and sales efficiency

• Customers increasingly connected via our • Further potential in manual to digital sales

digital channels transformation

• Higher transaction volumes

• More cross-selling opportunities 100%

80%

Customers 60%

w ithout Internet

bank agreement 40%

Digitally active 29%

customers 20%

47%

Connected 0%

customers (less Payments Savings & Lending Insurance

than monthly pensions

usage)

24% Digital sales Manual sales

© Swedbank Information class Note: Data relates to Swedish Banking

Public

122017 Strategic achievements Strategy

Launched in Sweden Retail channels

Already operating in the Baltics

Fully digital consumer lending Positive AuM inflows

Strategic co-operation with Kepler Cheuvreux Personal finance app for customers

Mina Tjänster

Enhanced equity capabilities Fintech partnership

SmartID launched in the Baltics PayEx acquisition

Enables faster transaction process for customers Integration and new launches begun

Digital customer identification Enhanced merchant omni-

and authorisation channel payment solutions

© Swedbank Information class

Public

13Swedbank creates value Strategy

% SEK Return on Equity

30 14 >15% target

*

25 12

20

10 15.1% FY 2017

8

15 Common Equity Tier 1 ratio

6

10

One of the highest among European banks

4

5 2

24.6%

0 0

2012 2013 2014 2015 2016 2017

Dividend per share

Return on Equity (LHS) CET1 capital ratio (LHS) 75% payout ratio for 6th year in a row

Dividend per share (RHS)

SEK 13.00

* Dividend proposal (for the financial year of 2017) - to be decided by the Annual General Meeting in March 2018

© Swedbank Information class Source: Swedbank Fact book 4Q 2017

Public

14Quarterly

financial

update

2. Quarterly financial

update

© Swedbank Information class

PublicSwedish Banking Quarterly

financial

Solid mortgage volume growth update

SEKm Q4 17 Q3 17 ▲QoQ • Net interest income

Net interest income 3 861 3 812 49

– Continued mortgage loan volume growth and

Net commission income 1 952 1 859 93

stable back book margins

Other income 625 443 182

Total income 6 438 6 114 324

• Net commission income

Total expenses 2 309 2 204 105 – Benign stock market development supported

Profit before impairments 4 129 3 910 219 asset management and brokerage income

Credit impairments 264 66 198 – PayEx included for the full quarter

Ratios Q4 17 Q3 17 • Other income

ROE, % 21.2 21.6 – Higher contribution from Entercard and life

C/I ratio 0.36 0.36 insurance

Volumes, SEKbn Q4 17 Q3 17 ▲QoQ • Solid asset quality

Loans 1 150 1 138 12

Deposits 525 519 6

© Swedbank Information class Dec 2017

Public

16Baltic Banking Quarterly

financial

Record high profitability update

SEKm Q4 17 Q3 17 ▲QoQ • Net interest income

Net interest income 1 116 1 060 56

– Lending to households continues to grow

Net commission income 711 565 146

– Stable margins

Other income 226 218 8

Total income 2 053 1 843 210 – Firm deposit growth

Total expenses 737 647 90 • Net commission income

Profit before impairments 1 316 1 196 120

– Benefited from annual performance fees

Credit impairments -12 -26 14

• Positive FX effects

Ratios Q4 17 Q3 17

• Stable asset quality

ROE, % 20.8 18.2

C/I ratio 0.36 0.35

Volumes, SEKbn Q4 17 Q3 17 ▲QoQ

Loans 149 146 3

Deposits 185 172 13

© Swedbank Information class Dec 2017

Public

17Large Corporates & Institutions Quarterly

Result reflected mixed market dynamics financial

update

SEKm Q4 17 Q3 17 ▲QoQ • Stable net interest income

Net interest income 934 896 38

• Net commission income

Net commission income 656 525 131

Net gains and losses 332 554 -222

– PayEx contributed positively

Other income 42 32 10 – Positive stock market performance increased

Total income 1 964 2 007 -43 asset management and custody income

Total expenses 867 841 26 – Annual covered bond market maker fees

Profit before impairments 1 097 1 166 -69

• Net gains and losses

Credit impairments 59 195 -136

– Low FX and fixed income trading activity

Ratios Q4 17 Q3 17

ROE, % 14.2 13.0

– Negative valuation effects

C/I ratio 0.44 0.42 • Lower credit impairments

Volumes, SEKbn Q4 17 Q3 17 ▲QoQ

Loans 203 204 -1

Deposits 128 129 -1

© Swedbank Information class Dec 2017

Public

18Group results Quarterly

financial

Robust performance update

SEKm Q4 17 Q3 17 ▲QoQ

• Mortgage volume growth strengthened net

Net interest income 6 326 6 208 118

interest income

Net commission income 3 291 2 917 374

Net gains and losses 356 525 -169 • Stock market performance and full quarter

Other income 1 003 768 235 PayEx inclusion benefited net commission

Total income 10 976 10 418 558 income

Total expenses 4 563 3 883 680

Profit before impairments 6 413 6 535 -122

• FX effects and lower market activity

Credit impairments 311 235 76

impacted net gains and losses negatively

Other impairments 86 107 -21

• Expenses

Tax 1 277 1 444 -167

Net profit 4 737 4 743 -6 – Restructuring charge of SEK 300m

Ratios Q4 17 Q3 17 – PayEx included for the full quarter

ROE, % 14.4 15.0

• Solid asset quality

C/I ratio 0.42 0.37

CET1 capital ratio, % 24.6 23.9

© Swedbank Information class Dec 2017

Public

19Capital Quarterly

Strong capitalisation – no excess capital financial

update

24.2% 24.6% 23.9% 24.6%

• CET1 capital increased by SEK 0.4bn

21.9%

– Positive effect from net profit of SEK 1.1bn

excl. dividend

– Negative effect from IAS19 of SEK 0.6bn

• REA decreased by SEK 11.1bn

• Buffer above minimum requirements of

Q1 2017 Q2 2017 Q3 2017 Q4 2017 CET1 capital

ratio

around 270bps

requirement

© Swedbank Information class Dec 2017

Public

20Capital Quarterly

financial

Lower REA update

SEKbn

425 • REA decreased by SEK 11.1bn

419.5

– Received VISA-related proceeds

420

reduced REA

415 – Year-end effects reduced REA

-7.3

410 -1.1 -0.7 408.4

-2.0

405

400

Q3 2017 Credit risk Market risk CVA Other Q4 2017

© Swedbank Information class Dec 2017

Public

21Group results – FY 2017 FY

financial

Strong result • ROE of 15.1% - target achieved update

SEKm FY 2017 FY 2016 ▲YoY • Strong organic income generation

Net interest income 24 595 22 850 1 745 – One-off tax-free gains:

Net commission income 12 030 11 333 697 • SEK 2.1bn from VISA in 2016

Net gains and losses 1 934 2 231 -297 • SEK 0.7bn from Hemnet in 2017

Other income 3 879 4 407 -528

Total income 42 438 40 821 1 617

• Underlying expenses in line with FY 2017

Total expenses 16 415 15 627 788

guidance of SEK 16.1bn

Profit before impairments 26 023 25 194 829 • Strong asset quality

Credit impairments 1 285 1 367 -82

– Lower-than-anticipated credit impairments

Other impairments 196 66 130

Tax 5 178 4 209 969

• Higher tax expense - changed dividend

Net profit 19 350 19 539 -189 policy in Estonia and tax on subord. liabilities

Ratios FY 2017 FY 2016 • CET1 capital ratio of 24.6%

ROE, % 15.1 15.8 • Board proposal – dividend of SEK 13.00 per

C/I ratio 0.39 0.38 share

CET1 capital ratio, % 24.6 25.0

– 75% pay-out ratio: Six consecutive years

© Swedbank Information class Dec 2017

Public

22Group Quarterly

financial

Solid asset quality update

Credit impairments, SEKm Q4 17 Q3 17 ▲QoQ • Resilient asset quality in all business

Swedish Banking 264 66 198

segments

Baltic Banking -12 -26 14

Large Corporates & Institutions 59 195 -136

• Lower-than-anticipated credit

Swedbank Group 311 235 76 impairments for the full year (0.08%)

Ratios Q4 17 Q3 17

Credit impairment ratio, % 0.08 0.06

Share of impaired loans, gross % 0.55 0.55

Total provision ratio for impaired

45 45

loans, %

© Swedbank Information class Dec 2017

Public

23ROE target of 15% remains Outlook

2018

• Additional investments to further accelerate our digitisation and automation efforts

– Channel transformation

– Digital payment solutions and e-commerce

– Customer offerings

– Automation

• Investments will allow us to offset underlying cost inflation and over-time lead to net

cost reductions

– The re-organisation of our IT and business development processes – a key facilitator

• Total annual expenses for 2018 and 2019 will be below SEK 17bn

• ROE target of 15% remains

• No excess capital – dividend policy of 75% remains

© Swedbank Information class

Public

24Capital

– fully

loaded

CRD IV

3. Capital considerations

© Swedbank Information class

PublicComposition of Swedbank’s CET1 and total

Capital

– fully

loaded

capital ratio requirements CRD IV

270bp

30.7%

Systemic Risk

27.7% charge in Pillar 2

24.6% 2.0% 25% REA Mortgage

Floor

21.9% 15.9%

Individual Pillar 2

8.2%

2.0% charge

Capital Conservation

Pillar 2

13.3%

6.8% Buffer

2.3%

Countercyclical

2.5% Available Distributable Items

buffer (2.0%)

1.8% Swedbank AB (parent comp) FY 2016** FY 2017

Automatic MDA 1.3%

Restrictions Share premium reserve 13 206 13 206

2.5% Systemic Risk Buffer

Retained earnings 41 277 43 099

3.0% Available distributable items 54 483 56 305

1.3%

11.3% 14.8% Min. Additional T1 Dividend* -14 695

Pillar 1

3.0% 3.5% Comprehensive income 6 988

and T2 capital

other 195

ADI Q1 2017 46 971

Minimum CET1

4.5% 4.5% * paid out in April 2017

Requirement

** Based on fully audited numbers

** The calculation of the ADI is based on the Annual report,

Swedbank CET1 Requirements Swedbank CET1 Capital Ratio Swedbank Total Capital Swedbank Total Capital ratio why this exercise as per Q4 2017 should be seen as an

Requirements example based on changes during the year.

© Swedbank Information class Dec 2017

Public

26Capital

Regulatory uncertainty remains – fully

loaded

CRD IV

• Basel proposal – largely as expected

– Awaiting final details from EU and then Swedish regulator on new standardised approach

– Likely long phasing in period – potentially until 2027

– Comfortable buffers to current capital requirements

– Feel great comfort in our capital generation capacity

– No need to review current dividend policy on the back of the proposal

• IFRS 9

– Limited impact on CET1 capital ratio of – 6bps as per 1 Jan, 2018

© Swedbank Information class Sep 2017

Public

27Capital

MREL needs in line with expectations – fully

loaded

– no imminent issuance plan CRD IV

• Requirements for 2018 set and published by the Swedbank MREL requirements

Swedish National Debt office (NDO) on 20

Based on Risk Exposure Amount Based on total liabilities

December 2017 SEKbn

140 14%

+ own funds

– 7.3% based on Total liabilities + Own funds 31.8% 12.9%

30.7%

120 12%

– 34.8% based on Risk Exposure Amount (REA)

100 10%

• Transition period until 1 Jan, 2022 21.4%

80 8% 7.3%

– Already in compliance with current senior unsecured

debt outstanding 60 13.4% 6%

– Issuance need to the equivalent of around SEK 87bn 40 4%

in subordinated MREL eligible securities to meet

20 2%

requirement by 1 Jan 2022

• Sweden to adopt EU insolvency law 0

Loss absorption amount Swedbank total capital

0%

NDO Swedbank total

Recapitalisation amount Senior unsecured debt >1Y* requirement liabilities + own

– Expected by year end 2018 SREP 2017** funds***

*Nominal amount, ** Based on FY 2016 numbers, *** FY 2017, based on consolidated situation

© Swedbank Information class Dec 2017

Public

28Asset portfolios – low risk Asset

quality

Group loan book* Q4 2017, total SEK 1 502bn CET1 – EBA stress test, 2016, %

25%

Hotels and restaurants, Retail

Shipping and offshore, Transportation 8%

Manufacturing

20%

Other corporate lending 7%

15% 2015

Other property management

2016

15%

10% 2017

Residential properties

2018

Agriculture and forestry

5%

0%

SHB Nordea SEB Swedbank

Loan distribution

Household loans 70% Sweden Baltic banking

(90% mortgages)

30%

Private Private

45%

Corporate 55% Corporate

70%

Tenant ow ner associations

* Loans to the public excl. loans to credit institutions and SNDO

© Swedbank Information class Dec 2017

Public

29Liquidity

and

funding

4. Liquidity and funding

© Swedbank Information class

PublicCore balance sheet structure Liquidity

and

funding

SEKbn SEKbn

1 800

Assets 1 800

Liabilities

1 600 1 600 CET1

Suppl. capital

Simplified balance sheet

Lithuania Senior

Latvia unsecured debt

1 400 Estonia 1 400

1 200 Other corporate 1 200

lending, Sweden &

other Nordic countries

Deposits

1 000 1 000

Other private, Sweden

800 800

600 600

Swedish

400 400

mortgage loans

Covered

bonds

200 200

0 0

Q4 2017 Q4 2017

© Swedbank Information class Dec 2017

Public

31Covered bond strategy Liquidity

and

funding

Covered bond strategy Swedish households’ financial assets

Sweden SEKbn

100% 12 000

SEK 300-375bn

Thousands

90%

10 000

80%

70%

8 000

60%

50% 6 000

EUR/USD

40%

SEK 100-150bn 4 000

30%

20%

2 000

Other

10%

SEK 20-50bn

0% 0

1980 1990 2000 2005 2010 2015 2016

7Y Deposits, cash and retail bonds (LHS) Equities (LHS)

Pension savings and mutual funds (LHS) Other financial assets (LHS)

Maturity, years Total financial assets (RHS)

© Swedbank Information class Dec 2017

Public

32Senior unsecured debt strategy Liquidity

and

funding

SEKbn*

Senior unsecured debt maturity profile

60 Senior unsecured debt

40

20

0

2018 2019 2020 2021 2022 2023 2024-

*Nominal amount

© Swedbank Information class Dec 2017

Public

33Conservative funding position Liquidity

and

funding

• LCR 173% (Swedish FSA definition FFFS 2012:6)

• NSFR 110% (Basel committee)

• Issued SEK 181bn of term funding FY 2017

• Plan to issue around SEK 145bn in 2018

Term funding issuance – completed and planned SEKbn

Prefunded for more than 12 months

SEKbn

700

100 Covered bonds Senior unsecured debt

90 Planned, covered bonds Planned, senior unsecured debt 600

Survival horizon

80

500

70

60 400

50

300

40

30 200

20

100

10

0 0

0 20 40 60 80 100 120 140 160 180 200 220 240 260 280 300 320 340 365

Days forward

© Swedbank Information class Dec 2017

Public

34Long-term funding maturity profile Liquidity

and

funding

Long-term funding maturity profile, by funding source Long-term funding maturity profile, by currency

SEKbn SEKbn

Senior unsecured debt Covered bonds

200 200

150 150

Other

GBP

100 100 USD

EUR

SEK

50 50

0 0

2018 2019 2020 2021 2022 2023 2024- 2018 2019 2020 2021 2022 2023 2024-

© Swedbank Information class Dec 2017

Public

35Private placements – active in both covered Liquidity

and

funding

bonds and senior unsecured debt

• All major currencies • FRN’s (SEK and EUR) – issued with a

• Bullet format, FRN or Fixed “strike adjustment spread”*

• EUR 10m equivalent minimum size • Program formats available:

– Senior unsecured debt: MTN, NSV and potentially

• Sweet spots:

USD 144a format

– Senior: 2.5-5Y

– Covered bonds: MTN, RCB and Norwegian CB

– Covered: 3-8Y program

– Longer tenors also possible

• Open to larger placements with smaller investor

groups

• Open to tap existing bonds

• Listing is optional

*Spread added to the coupon to avoid negative coupon fixings. Bond issued above par to compensate for this. The above par value reflects the NPV of the adjusted

spread

© Swedbank Information class

Public

36Liquidity reserve Liquidity

and

According to the template defined by the Swedish Bankers' Association funding

SEKm

1

Cash and holdings in central banks 208 370

Deposits in other banks available overnight 3

Securities issued or guaranteed by sovereigns, central banks or multilateral development banks 88 006

Securities issued or guaranteed by municipalities or public sector entities 5 636

Covered bonds 46 621

- Issued by other institutions 44 349

- Own issued 2 272

Securities issued by non-financial corporates 292

Securities issued by financial corporates (excl. covered bonds) 409

Other

Total2 349 337

1) Including loans to the Sw edish Ntional Debt Office

2) 95% of the securities in the liquidity reserve per Q4 2017 are rated AAA. The rating requirement is AA-.

Assets included in the liquidity reserve should comply w ith the follow ing:

- assets shall be under the control of the Treasury function in the bank

- assets can not be encumbered

- market values are used for the assets

- only unencumbered securities receiving 0-20% risk w eight under the standardised approach to credit risk of the Basel II framew ork can be included

- securities received in reverse repo transactions shall be included in the liquidity reserve and securities used as collateral for repo transactions shall be excluded

© Swedbank Information class Dec 2017

Public

37Rating Liquidity

and

funding

• On 1 September 2017, Moody’s affirmed Swedbank's ratings at Aa3/P-1 with a stable outlook. The ratings reflect Swedbank’s

strong credit quality, solid regulatory capital and stable earnings, underpinned by its established franchise in Sweden. Swedbank is

also expected to be broadly resilient to the risks in the residential housing market and household sector in Sweden.

• May 26, 2016, Fitch upgraded the rating to AA- from A+, with a stable outlook. The main drivers behind the upgrade

are: Execution of the low risk strategy including conservative risk-returns and underwriting standards, strong retail

franchise and continued strong capitalisation.

• November 24, 2017, S&P affirmed the rating of Swedbank at AA-/A-1+, with a stable outlook. The rating reflect Swedbank’s

strong business position, given the market-leading retail position, strong revenue performance, and efficiency, as well as prudent

management and strategy. S&P also assess the capital and earnings as strong, reflecting the strong earnings capacity. The stable

outlook on Swedbank resilient earnings and capital as Sweden's economy benefits from improvements in Europe's economic

environment and the domestic housing market adjusts to higher volumes and stricter amortization requirements.

S&P (Stable) Moody's (Stable) Fitch (Stable)

Short Long SACP1 Short Long BCA1 Short Long VR1

Swedbank A-1+ AA- a+ P-1 Aa3 a3 F1+ AA- AA-

Swedbank Mortgage A-1+ AA- - P-1 Aa3 - - - -

Covered bonds - AAA - - Aaa - - - -

1

Standalone Rating

© Swedbank Information class Dec 2017

Public

38Swedbank is a labeled issuer of

the ECBC Covered Bond Label

Foundation

(www.coveredbondlabel.com )

5. Cover pool data

© Swedbank Information class

PublicCover pool data1 Swedbank is a labeled issuer of

the ECBC Covered Bond Label

Foundation

(www.coveredbondlabel.com )

Rating, S&P / Moody’s AAA / Aaa Repayment structure 7

Total pool size SEK 928.6bn – Amortising 68%

Geographic distribution Sweden 100% – Interest only 32%

Current OC-level 85.5%

Weighted average seasoning 2 66 months Average loan size SEK 577 975

Average LTV 3, 4 Number of loans outstanding 1 606 567

– WA LTV on property level (Max LTV) 49% Number of borrowers 1 119 065

Non-performing loans 5 None Number of properties 752 474

Dynamic pool Yes

Fixed /Floating interest loans 6

– Fixed 29.3% 1 As per 31 Dec, 2017

Public sector loans not included

– Floating

2

70.7% 3 Index valuation as per Sep, 2017

4 Maximum LTV: Residential 75%, Commercial 60%, Forest and Agriculture 70%

5 Past due loans > 60 days are not eligible for the cover pool

6 Floating interest loans < 365 days

7 Property level of cover pool

© Swedbank Information class Dec 2017

Public

40Cover pool data Swedbank is a labeled issuer of

the ECBC Covered Bond Label

Foundation

(www.coveredbondlabel.com )

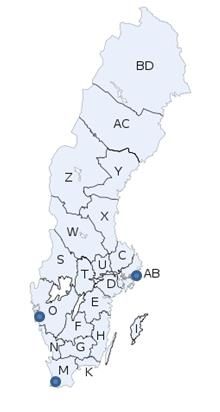

Type of loans Geographical distribution, Sw eden, per cent 31 Dec

(based on loan volum e) (based on loan volum e) 2017

Residentials 91.9% North 6.5

of w hich Single-family housing 56.9% Norrbotten county (BD) 1.4

of w hich Tenant ow ner rights 20.7% Västerbotten county (AC) 2.4

of w hich Tenant ow ner association 9.6% Västernorrland county (Y) 1.5

of w hich Multi-family housing 4.7% Jämtland county (Z) 1.2

Public 0.7% Middle (including Stockholm ) 43.9

Commercial 0.8% Dalarna county (W) 2.0

Forest & Agricultural 6.6% Gävleborg county (X) 2.1

100.0% Värmland county (S) 2.0

Örebro county (T) 2.5

Västmanland county (U) 2.4

Population, Sep 2017 Uppsala county ( C) 4.1

(thousands) Södermanland county (D) 2.1

Sw eden 10 094 Stockholm county (including Stockholm) (AB) 26.7

Stockholm, county 2 299 South (including Göteborg and Malm ö) 49.6

Västra Götaland, county (incl. Gothenburg) 1 686 Västra götaland county (Including Göteborg) (O) 17.9

Skåne, county (incl. Malmoe) 1 340 Östergötland county (E) 4.2

Jönköping county (F) 3.5

Halland county (N) 4.1

Kronoberg county (G) 2.1

Kalmar county (H) 2.9

Skåne county (including Malmö) (M) 12.9

Blekinge county (K) 1.4

Gotland county (I) 0.6

100.0

© Swedbank Information class Dec 2017

Public

41Cover pool loan-to-value distribution Swedbank is a labeled issuer of

the ECBC Covered Bond Label

• Weighted average LTV on property level 49% Foundation

(www.coveredbondlabel.com )

LTV distribution per property1 LTV distribution by volume1, 2

30% 30%

25% 25%

20% 20%

15% 15%

10% 10%

5% 5%

0% 0%

00-10 10-20 20-30 30-40 40-50 50-60 60-70 70-75 00-10 10-20 20-30 30-40 40-50 50-60 60-70 70-75

1Public loans of 0.7% of the cover pool are excluded as they are either guaranteed by a Swedish municipality or the government and have therefore no

LTV assigned to them. 2 LTV distribution as defined by the Association of Swedish Covered Bond Issuers (www.ascb.se)

© Swedbank Information class Sep 2017

Public

42Cover pool loan type and loan-to-value Swedbank is a labeled issuer of

distribution the ECBC Covered Bond Label

Foundation

(www.coveredbondlabel.com )

WA LTV per property type1

Percentage of the pool Average LTV per loan type

120% 120%

100% 100%

80% 80%

60% 60%

40% 40%

20% 20%

0% 0%

Single-family Tenant owner Tenant owner Multi-family Commercial Forestry & Total all

1

homes rights associations housing Agricultural types

(apartments)

1excluding public sector loans of 0.7%

© Swedbank Information class Dec 2017

Public

43Strong resilience to house price changes Swedbank is a labeled issuer of

the ECBC Covered Bond Label

Foundation

(www.coveredbondlabel.com )

House price sensitivity of the cover pool • Current OC-level of 85.5%

90%

OC, Q417

• 2% legal minimum requirement

80% Min req. 2%

• Can withstand a severe house price drop

70%

and still be able to issue AAA-rated

60% covered bonds

Over-collateralisation

50%

40%

30%

20%

10%

0%

0% -5% -10% -15% -20% -25% -30% -35% -40% -45% -50%

House price drop

© Swedbank Information class Dec 2017

Public

44Overview of the Swedish covered bond legislation

The Covered Bond Act entered into force on July 1, 2004 and is over-sighted by the Swedish FSA. Its main

characteristics are:

Dual recourse to the issuer and cover pool

The Covered Bond Act Dynamic, regulated pool of assets, frequently monitored by the Swedish FSA via appointment of an

independent inspector

Regulated valuation of cover pool assets which remain on the balance sheet

The cover pool may consist of certain mortgage credits, public credits and supplemental assets. There is no

requirement to segregate mortgage and public credits.

Maximum LTVs: Residential 75%, Agricultural 70%, Commercial 60%

Loan-to-value ratios and Maximum 10% commercial loans and 20% supplemental assets in cover pool

other limitations Regular monitoring of the property values, revaluation of property prices in case of significant drop (generally

interpreted as 15% drop)

The S.O. Act amended, effective as of 21 June 2016, requires that the nominal value of the cover pool shall, at all

times, be at least two per cent. higher than the aggregate nominal value of the liabilities relating to the covered

bonds..

Regional constraint on collateral assets (Mortgage - EEA, Public - OECD)

Matching requirements The cover pool value shall always exceed the aggregate value of claims (including derivatives)

A sound balance in terms of FX, interest rates and maturities must be achieved. It is deemed to exist when the

present value of the cover pool at all times exceed the present value of liabilities (including derivatives), even on a

stressed basis. Present value cover must hold even after 1% upward and downward shift in the yield curve and a

10% change in the currency

Non-performing assets in the cover pool which are more than 60 days overdue must be disregarded for the

purposes of the matching tests

Benefit of a priority right

over the cover pool Holders of covered bonds and relevant derivative counterparties benefit from a priority claim over the cover pool

should the institution be declared bankrupt and rank pari passu ahead of unsecured creditors and all other creditors

of the institution in respect of assets in the cover pool

The registered assets in the cover pool, the covered bonds and any relevant derivative contracts are required to be

Administration in event of maintained as a unit and kept segregated from other assets and liabilities of the bankruptcy estate of the institution.

bankruptcy The administrators-in-bankruptcy are then required to procure the continued timely service of payments due under

the covered bonds and any relevant derivative contracts

© Swedbank Information class Source: www.ascb.se

Public

45Swedish

and Baltic

macro

6. Swedish and Baltic

economies

© Swedbank Information class

PublicSweden - Strong growth gradually slowing Swedish

and Baltic

macro

Key economic indicators1, 2016-2019

Real GDP (calendar adjusted)

Most recent

2.9 (Q3)

2016

3.0

2017E

2.6

2018F

2.7

2019F

2.1

• Kingdom of Sweden rated

CPI growth, average 1.7 (Dec) 1.0 1.8 2.1 2.8 Aaa/AAA/AAA

CPIF growth, average 1.9 (Dec) 1.4 2.0 1.9 1.9

Unemployment rate (15-74), % of labor force 6.5 (Dec)2 6.9 6.7 6.4 6.3

Savings ratio (households),% of disp. income … 16.5 16.1 16.9 16.5

Real disposable income (households) … 3.3 2.1 3.3 1.5

Sources: Statistics Sweden & Swedbank Research

1 Annual percentage growth in percent unless indicated otherwise.

2 Seasonally adjusted and smoothed

Domestic demand drives growth Sentiments remain elevated

© Swedbank Information class Feb 2018

Public

47The Swedish economy Swedish

and Baltic

Households remain cautious Housing investments to be replaced by other investments macro

Percentage points

of GDP

Exports picking up

Overall investments are trending higher

© Swedbank Information class Feb 2018

Public

48The Swedish economy, con’t Swedish

and Baltic

Strong employment; wages and unemployment lag Solid public finances macro

4.0 % of GDP 49

3.0 47

45

2.0

43

1.0

41

0.0

39

-1.0 37

-2.0 35

Budget balance forecast Public debt (Maastrict), rhs forecast

Sources: Swedbank Research & Macrobond.

Gradually increasing inflation Stable krona

© Swedbank Information class Feb 2018

Public

49The Swedish credit market Swedish

and Baltic

Lending to households dampens Interest rates remain low; while margins are stable macro

A gradual tightening of monetary policy Quantitative easing formally ended in 2017

© Swedbank Information class Feb 2018

Public

50Baltics – continued growth albeit at slower rates Swedish

and Baltic

macro

Key economic indicators1, 2015-2019

Most recent 2016 2017E 2018F 2019F

Real GDP Estonia 4.2 (Q3) 2.1 4.4 3.9 3,0 Ratings

Latvia 4.2 (Q4) 2.1 4.7 4.2 3.2 • Republic of Estonia: A1/AA-/A+

CPI growth, average

Lithuania

Estonia

3.6 (Q4)

3.4 (Dec)

2.3

0.1

3.8

3.4

3.2

3,0

2.5

2.5

• Republic of Latvia: A3/ A-/A-

Latvia 2.2 (Dec) 0.1 2.9 3.7 2.5 • Republic of Lithuania: A3/ A-/A-

Lithuania 3.9 (Dec) 0.9 3.7 3.3 2.5

Unemployment rate (15-74), % of labor force Estonia 5.2 (Q3) 6.8 6,0 7,0 7.2

Latvia 8.5 (Q3) 9.6 8.8 8.1 7.5

Lithuania 6.6 (Q3) 7.9 7.2 6.9 6.9

1 % growth rate unless indicated otherwise, Y/Y growth for the most recent data

Real economic growth peaked in 2017 Unemployment is declining

© Swedbank Information class

Public

51Estonia: Growth to slow after peak Swedish

and Baltic

Economic growth expanded in the fastest pace in five years in 2017 macro

Domestic demand and export the main drivers Export and manufacturing output accelerate

© Swedbank Information class

Public

52Latvia: Solid growth to continue Swedish

and Baltic

Supported by strong confidence, pro-cyclical fiscal policy, rapid wage growth, global tailwinds macro

Sharp cyclical pick up in growth to moderate in 2019 Sentiments are strengthening

© Swedbank Information class

Public

53Lithuania: GDP growth will revert to potential Swedish

and Baltic

Weaker household consumption and export growth, but investments to pick up macro

Growth has peaked and start to ease Capacity constrains will limit export growth

© Swedbank Information class

Public

54Swedish

housing

and

mortgage

market

7. Swedish housing and

mortgage market

© Swedbank Information class

PublicSwedish

The decline in prices is not unexpected housing

and

mortgage

• Strong price increases in recent years due to high demand and limited supply market

• Supply has increased on the back of a surge in housing investments

• Stricter borrowing criteria both by lenders and authorities

Home prices and macroprudential measures

2010 2011 2012 2013 2014 2015 2016 2017 2018

20%

Valueguard HOX Sweden house price index y/y

15%

10%

5%

0%

-5%

1 2 3 4 7 8 9 10 11 12

-10% 5 6

© Swedbank Information class

Public

56Swedish

Price developments have varied across the housing

and

mortgage

country and type of housing market

• Price increases, and recent falls, have been most pronounced in the Stockholm area

• Prices of apartments most volatile, again in the Stockholm area

• Single-family houses are holding up better

Flats +177%, houses +104% since 2005 1) Trends and average house prices, December 20172)

Tenant owner rights

1 month 3 months 12 months SEK/sqm

Sweden total -3% -7% -2% 34 944

Stockholm greater area -3% -7% -6% 53 998

Gothenburg greater area -2% -6% +4% 42 650

Malmoe greater area -2% -8% +8% 26 399

Single-family homes

1 month 3 months 12 months SEK

Sweden total -2% -3% +5% 2 814 000

Stockholm greater area -3% -6% -1% 5 271 000

Gothenburg greater area -1% -3% +4% 4 335 000

Malmoe greater area -1% -3% +7% 3 573 000

1) Source: Valueguard (HOX index)

2) Source: Mäklarstatistik

© Swedbank Information class

Public

57Swedish

Supply increase puts pressure on prices, but housing

and

mortgage

supports transaction volumes market

• Following recent years’ investment increase, supply will continue to grow

• Demand and number of transactions is still high, especially in large city areas

• Housing shortages still persist, in particular in the larger cities

Housing investments support continued supply Transactions increase, as well as supply

80 000

19 000

70 000

17 000

60 000

15 000

50 000

13 000

40 000

30 000 11 000

20 000 9 000

10 000 7 000

0 5 000

Jan-10 Jan-11 Jan-12 Jan-13 Jan-14 Jan-15 Jan-16 Jan-17 Jan-18

Number of transactions

Newly added for sale on Hemnet

Housing starts (lagged 2 yr) Finished housing

Newly added for sale incl new production

Source: Statistics Sweden Source: Mäklarstatistik and Hemnet

© Swedbank Information class

PublicSwedish

Household borrowing dampens while financing housing

and

mortgage

costs remain low market

• Mortgage volume growth benefitting from new housing supply, housing turnover and higher

mortgage amounts by existing borrowers

• Housing financing costs at historically low level

• Reasonable to expect some slowdown from last year’s 7.4% market growth

Mortgage growth and housing prices Low mortgage costs

© Swedbank Information class

Public

59Swedish

Structural foundation for the housing and housing

and

mortgage

mortgage market market

• Full recourse (very limited debt forgiveness possibilities)

• No securitisation (on balance sheet), no sub-prime market, no 3rd party origination

• Restricted buy-to-let market – limited speculation

• 64% home ownership

• Rental market is regulated

• Transparent credit information (credit information agency, www.uc.se)

– Publicly available information regarding income, debt, payment track record etc.

• Consumer credit legislation requires affordability calculations including stress test of higher interest rate and

conservative cost of living

• Strong social security and generous unemployment benefit system

© Swedbank Information class

Public

60Swedish

Household fundamentals support the housing housing

and

mortgage

market market

• Population growth and urbanisation trends continue

• Solid labour market developments

• Solid balance sheets among households

High population growth and urbanisation Solid labour market Strong household balance sheets

The overcrowding rate is defined as the

percentage of the population living in an

overcrowded household.

© Swedbank Information class

Public

61Swedish

Overall indebtedness among Swedish housing

and

mortgage

households remains low market

• Of appr. 4 million households less than 50% carry a mortgage

• Median debt-to-income ratio of mortgage holders less than 300%

• Less than 15% of mortgage holders have a debt to income ratio of more than

600%

Debt ratios of Swedish households Distribution of debt ratios in 2016

Total debt as % of gross income No. of households w/ mortgages

450000

100%

>600 400000

350000

80%

400-600 300000

60% 250000

200-400 200000

40% 150000

0-200

100000

20% No 50000

mortgages 0

0% 0-100 100-200 200-300 300-400 400-500 500-600 600-700 >700

2011 2012 2013 2014 2015 2016 Source: Riksbank Total debt as % of post tax income

Source: Riksbank

© Swedbank Information class

Public

62Swedish

The Swedish economy underpins the housing

and

mortgage

housing market market

• Fiscal policy will be supportive and public debt is at a historic low level

• Monetary policy to remain expansionary

• Economic growth expected to continue at solid rates despite weakening housing

investments

Expansionary fiscal policy Gradually tightened monetary policy Slowdown in growth from high rates

4.0 % of GDP 49

0.25 %points

3.0 47

45

2.0 0.05

43

1.0

41

0.0 -0.15

39

-1.0 37

-0.35

-2.0 35

-0.55

2015 2016 2017 2018 2019

Budget balance forecast

Public debt (Maastrict), rhs forecast Market pricing Swedbank forecast

Outcome Riksbank forecast December 2017

Sources: Swedbank Research & Macrobond. Sources: Swedbank Research & Macrobond

© Swedbank Information class

Public

63Swedish

Swedbank and the real estate market housing

and

mortgage

market

• Swedbank has a low risk residential property portfolio

• Origination discipline and profitability have been

prioritised over volume

• Engagement in low risk projects with well-known

residential property developers will continue

© Swedbank Information class

Public

64Swedish

Swedbank has a low risk residential property housing

and

mortgage

portfolio market

Real estate lending, net loans in Sweden, SEKbn

1 200

• Swedbank has pursued a low risk

• Private mortgages: SEK 759bn, average

strategy by tightening origination

1 000 LTV 54% standards, and prioritised price and

• Tenant Owner Associations (“TOA”): SEK risk over volume growth

109bn

800

759

SEK 95bn existing TOA, average LTV 40% • Bulk of assets in low risk segments

SEK 14 bn TOA under construction

600

• Property Management: SEK 187bn, average • Average LTVs in lower ranges

LTV 58%

400 SEK 64bn in residential property management • Exposures towards residential

(rental apartment properties)

109 SEK 123bn in other property management

property developers of SEK 21bn

200

64 • Construction SEK 16bn

123 21 SEK 7bn residential property development

0 16

SEK 9bn infrastructure, groundwork, craftsmen

Total real estate Of which:

portfolio Residential

property

development

© Swedbank Information class

Public

65Swedish

Private mortgages – a low risk portfolio housing

and

mortgage

market

• Low average LTVs (54%)

• Low historic losses (0.04% on average during the last 25 years)

• About 73% of total loans to single family homes

• Swedbank has grown, but at a slower rate than the market

Growth but lower than the market High diversification Only 1% above 75% LTV

9 Loan growth in % Loans net1) by geography Loans1) to Private Mortgage by LTV-bucket

8 20

18 SEKbn 87% with 99% with

7 LTVSwedish

Tenant Owner Associations – low leverage housing

and

mortgage

market

• Total loan portfolio SEK 109bn, of which SEK 14bn is construction loan for new

development:

– 50-80% needs to be pre-sold and before final financing 100% needs to be sold

– When the construction is finalised about 60% of construction loans will be repaid through equity from the TOA

members

• Low historic losses (average 0.17% over the last 25 years)

Growth but lower than the market Portfolio reflects market Average LTV of only 40%

12 Loan growth in % Loans net1) by geography Loans1) to Tenant Owner Associations by LTV-bucket

4

10

SEKbn 95% with 100% with

8 12% LTV 50 000 inhabitantsSwedish

Residential property developers - low exposure housing

and

mortgage

market

• Total exposures of SEK 21bn, more than half of it to the larger listed construction firms, with

which Swedbank has long-term relations

– SEK 14bn of the exposures are related to tenant-owner rights projects through loans to Tenant Owner

Associations backed by residential property developers

• 99% of these projects will be finalised in 2018 and 2019

– SEK 7bn of the exposures are related to residential rental housing and other non-residential projects

• Pre-sale level of tenant owner rights close to 90%

Mainly exposures to the larger construction firms Tenant owner rights related construction loans1) – the risk is highly mitigated

Loans1), SEKbn By geography Finalisation year Average % pre-sold by

finalisation year2)

100

Large building firms 7% 1% 90

10

29% 80

25% 70

New developers 4 SEK 60

14bn 55% 50

4% 70% 40

Smaller building firms 7 9% 30

20

10

0 10 Stockholm region 2018 2019 0

Gothenburg region 2020- 2018 2019 2020-

Malmö region

© Swedbank Information class 1) As of 31 December 2017

Public

68Swedish

Residential property management – stable housing

and

mortgage

cash-flow generation market

• Total exposures of SEK 64bn towards residential property management companies

– Financing of rental apartment properties

• Well-known companies with solid finances and high collateralization

• Strong and stable cash-flow generation, no speculation and low vintage risk

Slower growth in 2017 Regional cities dominate Average LTV of 58%

8 Loans net1) by geography Loans1) to Residential Prop Mgmt by LTV-bucket

Loan growth, %

1.4

SEKbn 86% with 99.7% with

6 1.2 LTVAppendix

© Swedbank Information class

PublicSwedbank – largest retail bank in our four This is

Swedbank

home markets

Sweden

Latvia

Population 10.0m

Population 2.0m

Private customers 4.1m

Private customers 0.9m

Corporate customers 270 000

Corporate customers 83 000

Organisations 68 000

Branches 36

Branches 218

Cards 1.0m

Cards 4.2m

Number of card purchases 38.5m

Number of card purchases 323m

Digitally active customers* 0.7m

Digitally active customers* 3.1m

Estonia Lithuania

Population 1.3m Population 2.9m

~86%*

Private customers 0.9m Private customers 1.5m

Corporate customers 135 000 Corporate customers 69 000

Branches 34 Branches 63

Cards 1.1m Cards 1.7m

Number of card purchases 50.9m ~10%* Number of card purchases 36.3m

Digitally active customers* 0.6m Digitally active customers* 0.7m

* Share of loan book

© Swedbank Information class Source: Swedbank Factbook 4Q 2017

Public * Number of customers that have made a payment, transfer, application, investments or lending activity in the last month

71Swedbank – low-risk bank with strong capital This is

Swedbank

base

• Low risk – a Board of Directors’ strategic priority – ensures access to funding

markets and low funding cost

• Retail profile and four home markets a key feature Liquidity & capital, %

NSFR LCR CET1 ratio, CRDIV (RHS)

– 86% of total loans originated in Sweden - Swedish mortgages account for 50% of 200 30

total loans

150

– 91% of total loans are collateralised (78.5% real estate and 12.5% other collateral) 20

100

• Strong capital position – Board of Directors’ decision to maintain a buffer above 10

50

prevailing SFSA capital requirements to have operational flexibility – current buffer

around 270bp 0 0

2012 2013 2014 2015 2016 2017

• Conservative funding and liquidity position – survival horizon longer than 12 months Credit impairment ratio, bps

40

assuming closed funding markets, NSFR 110% and LCR 173%

30

• Baltic operations self-funded – loan-to-deposit ratio < 100%

20

10

0

-10

Q4 12 Q4 13 Q4 14 Q4 15 Q4 16 Q4 17

© Swedbank Information class Dec 2017

Public

72Swedbank – strong and stable earnings This is

Swedbank

capacity

• Four home markets – Sweden, Estonia, Latvia and Lithuania

– Strong and stable economies

– Market-leading position in all home markets

– Largest customer base in all home markets

• Retail profile ensures stable earnings with low volatility

• High cost efficiency – a strategic priority – ensures good profitability

• Stable earnings support a low risk profile and a strong capital position Profit before impairments, SEKbn

10

One-offs from disposals

8

6

4

2

0

Q4 12 Q4 13 Q4 14 Q4 15 Q4 16 Q4 17

© Swedbank Information class Dec 2017

Public

73Swedbank – market leader in cost efficiency This is

Swedbank

• Best-in-class cost efficiency – an executive management strategic priority

• Executive management strongly focused on cost and change management

Total expenses, SEKm

− Integrated in corporate culture 20

Acquisition of Sparbanken…

− Focus on straight-through-processing 18

− Evolving household banking model – digitisation trend 16

• Retail profile a key feature 14

− Four home markets – Sweden, Estonia, Latvia and Lithuania – reduce 12

complexity 2012 2013 2014 2015 2016 2017 Target

− Largest private and SME customer base 60

18

C/I ratio, %

− High degree of digitisation in home markets 55

50

45

40

35

30

2012 2013 2014 2015 2016 2017

© Swedbank Information class Dec 2017

Public

74Focus on sustainable business

Improved sustainability scores First green bond issued in October (5yr EUR 500m)

Swedbank issued its first Green Bond Approximately 72% of the amount was

Dow Jones Proceeds will allocated to investors with dedicated green

• Finance sustainable real-estate funds.

Sustainability • Renewable energy

Index • Reduction of carbon emissions With our established Green Bond

• Contribute to several of the UN framework Swedbank intends to be a

2011 2012 2013 2014 2015 2016 2017

Sustainable Development Goals. regular issuer in the green bond market.

Swedbank Robur’s sustainability funds Eligible green assets Sustainable Development Goal

Nordic Swan Since October 2017, five of Swedbank Robur's active Renewable energy SDG7 and SDG13

managed sustainability funds have the Nordic Swan Ecolabel.

Ecolabel Sustainability work is also further progressing in the

Energy efficiency SDG7, SDG11 and SDG13

management of the Access Index-based funds. Sustainable management of living natural resources SDG15

Pollution prevention and control SDG6 and SDG11

Stronger Environmental Management System (EMS) Clean transportation SDG9 and SDG11, SDG13

Swedbank’s upgraded Environmental Management System

ISO was certified with the new and more rigorous standard Sustainability Indicators: towards the 2030 Agenda

ISO14001:2015.

Swedbank has developed a new methodology, Sustainability Indicators, to review the

progress towards the UN 2030 Agenda for Sustainable Development. The aim is to support

Swedbank is included in The Sustainability Yearbook 2018 the business looking at ESG (environmental, social, governance) criteria and help to

identify weaknesses and strengths in Sweden and the Baltic countries operations.

The The Sustainability Yearbook lists the world’s most sustainable Progress towards UN SDGs, % of benchmark*

companies in each industry as determined by their score in Estonia Latvia Lithuania Sw eden

Sustainability RobecoSAM’s annual Corporate Sustainability Assessment. Sustainable medium-term grow th (SDGs #4, 8, 9) 71 61 64 90

Social inclusion (SDGs # 1, 3, 5, 10) 56 55 55 89

Yearbook Environmental protection (SDGs # 6, 7, 11, 12, 13) 58 72 70 82

Governance and institutions (SDGs # 16, 17) 70 51 62 97

Dow nw ard/stable trend during last 5 years (4 years for governance) – ↓

* Benchmark is 90 or 10th percentile of the EU 28 in 2015. In total 40 indicators covering 14 from 17 SDGs, aggregated to four pillars.

Traffic lights - Sw eden: >90% for green, 70-90% for yellow 0-70% for red; Baltics: >80% for green, 60-80% for yellow , 0-60% for red.

© Swedbank Information class

Public

75Our objective Strategy

• Daily banking is fully digital – 100% self service

• Meet our customers with relevant offerings, in our own or external channels

• Data and knowledge automation – to foresee needs, provide proactive offering and advice.

This will generate loyalty as well as increased sales

• Have an attractive financial platform for customers and 3rd party suppliers, providing value-

added and competitive edge

• Branches attract new customers - build the brand and increasingly focus on corporate

customers

© Swedbank Information class

Public

76Sweden – the dominating home market This is

Swedbank

• Total lending to the public amounts to SEK 1 502bn (as per Q4 2017), out of

which around 86% is originated in Sweden

• Estonia makes up 48% of total lending in the Baltics

Lending distributed by countries

Sweden 85.8% SEK 1 288bn

Estonia 4.7%

Swedish Mortgage loans (private+corp)

Latvia 2.1% Other corporate (incl. LC&I, Sweden)

Lithuania 3.1%

Other* 4.3%

0 200 400 600 800 1000 1200 1400 * Mostly Norway and Finland

© Swedbank Information class Dec 2017

Public

77Oil sector still under pressure Asset

quality

• Loan portfolio negatively impacted by lower oil price, SEK 13.4bn

– Less than 1% of total loans gross

– Derivatives exposures of SEK 1.0bn (incl. collateral)

• Net, unchanged provisions* in Q4

10 LC&I Shipping & Offshore, loans gross, SEK 24bn 14 Oil-related, exposure by risk grade, SEKbn

2016-12-312 2017-12-31 12

8 56% of the portfolio is

negatively impacted by 10

lower oil price

6

8

4 6

4

2

2

0 0

Def 0 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21

2014-12-31 2015-12-31 2016-12-31 2017-12-31

© Swedbank Information class * Total provisions of SEK 1 358m for the whole Shipping and Offshore sector with a provision ratio (for impaired

Public loans) of 30%.

78Capital

No automatic sanctions for breaching the – fully

loaded

Pillar 2 capital requirements CRD IV

21.9%

● “It is particularly important that FI has the possibility of giving due

consideration to the specific situation…in which a firm in financial stress

finds itself… For example, certain risks included in the assessment

of the Pillar 2 basic requirement might have materialized, which 10.6%

might mean there are no longer grounds for requiring the firm to

hold capital for them”.

● “It ought to be positive for financial stability that a firm has the Pillar 2 CET1

possibility… to restore its capital without the firm necessarily becoming requirements

subject to priory specified and automatic legal restrictions. In other Automatic MDA

words, firms are hence given the possibility of re-establishing their Restrictions

capital in a strained situation without automatic restrictions on Pillar 1 CET1

requirements

distributions or, depending on the size of the capital shortage, a

formal resolution phase being activated." 11.3%

● “Hence…a firm may freely choose…the most suitable way of restoring

the capital in that specific situation. For example, the firm is not

obliged to halt or limit dividends or interest payments on Tier 1

capital contributions, if the firm can identify other and more

appropriate ways of restoring the capital sufficiently quickly.”

Swedbank CET1 requirements

© Swedbank Information class Dec 2017

Public

79You can also read