The 2019 Australian Grocer Retailer Preference Index (RPI) - The battle for the modern grocery shopper. Woolworths edges out Coles, but watch out ...

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

The 2019 Australian Grocer Retailer Preference Index (RPI) The battle for the modern grocery shopper. Woolworths edges out Coles, but watch out for Aldi.

CONTENTS

I. Executive summary......................................................................... 3

Ii. Introduction and context............................................................... 4

Iii. The RPI and its methodology....................................................... 5

Iv. Rankings and top findings............................................................ 6

V. A closer look at Aldi..................................................................... 18

Vi. Key takeaways............................................................................. 21

2 © 2019 dunnhumby Australia Retailer Preference Index

I. Executive summary

In a first-of-a-kind study -- The Australian Grocer Retailer Preference Index (RPI) -- dunnhumby conducted research on Customer

preference for grocery retailers. The report, modeled after a series of studies that dunnhumby has conducted in the US, takes a

snapshot of Customer preference for grocery retailers as well as the various levers retailers can pull to improve their rankings over

time. The key takeaways in this study, which looks at five prominent Australian retail grocers:

1 In this first RPI for Australia, Woolworths narrowly edges out Coles for the number-one position in

customer preference. But Aldi -- the global grocery retail discounter -- looms not far behind.

2 There are five primary Customers preference drivers (pillars) that the study correlates to emotional

connection (long-term brand equity) and financial performance.

3 Despite all the pressure retailers are facing around price, “value perception” – which is about both price and

quality – is what drives financial performance.

That said, price has become more important – it equals emotional connection, a critically outcome of

4 Customer preference. Price correlates closely with trust and other emotional attributes. These attributes

provide an emotional connection for Customers that ensures they are attracted and stay over the long term.

5 Store catalogues still play a key role in Customer pre-store influencers. This suggests that Customers are

creating their own consistent weekly shopping spend by cherry picking/budgeting across all retailers.

6 Everyone shops everywhere: There is very little loyalty between retailers, even those whose primary shop

was Coles and Woolworths still claimed one third of their shopping was also in Aldi.

The retail landscape is changing – both globally and in Australia. Aldi is shifting the price expectations

7 making Customers more price sensitive and aware than ever before. This is paving the way for more potential

entrants into the discount space.

1

See section III. The RPI correlates Customer preference with emotional connection and financial performance. Most studies have looked at these

variables separately. Note, however, that dunnhumby has conducted similar studies. For example, dunnhumby has been conducting Customer

Centricity Index (CCI) studies since 2015 based on an earlier version of a model for measuring customer preference. The RPI is an evolved version of

the CCI using a more advanced model.

2

The research guiding the RPIs takes note of global macroeconomic trends that have led to the reality today: shoppers are increasingly price sensitive.

3 © 2019 dunnhumby Australia Retailer Preference Index

II. Introduction and context A recent article in the Sydney Morning Herald commenced with this headline: “Coles and Woolies’ secret weapon in war with Aldi is Data.” As dunnhumby completed its first RPI for the Australian market, the article resonated with its researchers. Australian grocers -- as is true in other geographies throughout the world -- are facing intense pressure from sophisticated e-commerce leaders and discounters who are growing market share not just based on price but other factors that shape public perception, and ultimately preference. As the article in the Herald argues, there is a new normal in modern retail: the opportunity and obligation to leverage Customer Data -- beginning with “first-party Customer Data” -- to more effectively engage and retain Customers today. But that’s just part of the journey for retailers. The goal is to develop a unique strategy based on that Data in order to more effectively compete for mindshare and marketshare. Strategy based on Customer Data can help retailers combat: • Short-term and long-term trends that are disrupting the retail market • The competitive threat from retailers focused on perceived value (not just price) • The evolution of the modern shopper who increasingly is more value-aware • The threat from e-commerce giants that are moving about the globe with new strategies for integrating digital channels with brick and mortar • The continuing challenge of predicting future challenges to retailers that are emerging faster in other geographies but that might soon become real in Australia. As noted, this is the RPI in Australia. But it has been largely informed by both local and global trends that are likely to impact Australian grocery businesses. Understanding the levers that can be pulled in order to compete is critical, and more than ever Customer Data -- which is now becoming democratized -- can help retailers craft a unique strategy for winning and retaining the modern Customer. 3 Around the globe, the media has been chronicling the so-called retail apocalypse, noting volatility pressure on stock prices, store closures, and bankruptcies. See Section VII for resources on recent retail trends. 4 © 2019 dunnhumby Australia Retailer Preference Index

III. The RPI and its methodology

As a template for measuring Customer preference, the RPI originated in the U.S. in early 2018. It is widely regarded as an original

approach to understanding what drives Customer preference in the grocery sector, and the Data-based tools that can be leveraged

to improve Customer preference. The Australian Grocery RPI applies a focused lens by looking at the five national Australian grocery

retailers -- Woolworths, Coles, Aldi, IGA, and 7-Eleven -- based on how well they are meeting their Customer needs today. The study

included 1,500 individual respondents -- resulting in 3,900 unique retailer evaluations -- factoring age, state, and family composition.

There are a number of ways the RPI can be used to develop effective grocery retail strategy. But our chief goal was to answer four

core questions:

+What drives retailer preference among Australian shoppers?

+Which retailers are winning or losing?

+Why are they winning or losing?

+What can retailers do to improve emotional connection and financial performance?

The methodology we applied in the RPI is to correlate a retailer’s preference driver scores (convenience and quality; easy shopping

experience; price; operations; drive time) with their emotional connection with Customers (satisfaction; likelihood to recommend;

trust; intensity of attachment) and financial performance (share of visits).

This correlation is what makes the RPI unique, and what could help retailers more effectively compete for Customers today. In

addition, a stretch goal for the RPI is to deliver a dependable, standardized reference point for emotional connection (long-term brand

equity) and financial performance to see how they fare among their peers globally. It would enable retailers everywhere to learn from

one another, and develop strategies that are driven by both current challenges and value in the future for their Customers.

RPI

PREFERENCE EMOTIONAL FINANCIAL

DRIVERS CONNECTION PERFORMANCE

Convenience & Quality Satisfaction Share of Visits

Easy Shopping Likelihood to

Experience recommend

Price Trust

Operations Intensity of attachment

Drive time

5

See, e.g., “New ‘Retailer Preference Index’ Puts Trader Joe’s, Costco and Amazon at the Top.” https://progressivegrocer.com/new-retailer-preference-

index-puts-trader-joes-costco-and-amazon-top.

6

While 7-Eleven is a different shopping mission front the other retailers – i.e., convenience – we kept in for comparison and to qualify the report’s

accuracy (it scores highly where you expect it to and low where you’d expect.).

5 © 2019 dunnhumby Australia Retailer Preference Index

IV. Rankings and top findings

A. Rankings

There are five primary Customer preference drivers -- or “pillars” -- in Australia that we correlated to emotional connection and

financial performance. In order of importance among Australian shoppers they are:

Convenience and quality

Easy shopping experience

Price

Operations

Drive time

In the rankings, Woolworths comes in just ahead of Coles. But the “race,” so to speak, may be too close to call. Aldi comes in third (the

“dark horse” in the race”)7, but its growth in recent years suggests they might be closing the gap. IGA and 7-Eleven are currently trailing

(on weak perceived value propositions).

Woolworths Coles Aldi IGA 7Eleven

7

See section V for a closer look at Aldi.

6 © 2019 dunnhumby Australia Retailer Preference Index

B. Customers want convenience & quality and easy shopping experience. They also want to shop in as little

time as possible.

The following graph illustrates the relative weights for the five Customer preference drivers in Australia. While price matters greatly

(third on the list, but close behind), convenience & quality and easy-shopping experience are on the top of the list. As we note later, this

might matter to retailers who can check off the boxes on the bottom three drivers and have the resources to focus on the top two.

Convenience & Quality

Convenience & Quality

• Get in-and-out quickly

• Convenient locations

• Store experience

• Quality products and RTE items

Easy Shopping Experience

Easy Shopping Experience

• Information, rewards, and discounts

• Variety and one-stop-shop

Price Price

• Lower prices on conventional, organic, and

natural items

• Private brand strength

Operations Operations

• Out-of-stocks

• Price fluctuations

Drive Time

Drive Time • Drive time minutes

C. While convenience & quality is the top overall preference driver, for Woolworths and Coles Customers, it is

less important. Still, Woolworths and Coles Customers are more “satisfied” in this category.

For the other three retailers, convenience & quality perceptions are larger drivers of preference. This suggests an opportunity for them,

because each of their scores on satisfaction are lower than the top two. Again, the Data suggests opportunities for growth based on

what levers might be pulled to attract and retain Customers.

Position Map – Convenience & Quality

Importance

Satisfaction

7 © 2019 dunnhumby Australia Retailer Preference Index

D. Drilling into “satisfaction,” the strengths of Woolworths and Coles are quality products, meat & produce, cleanliness, and convenient locations Notes about each of the retailers: +Woolworths is the strongest on quality & convenience and has an advantage on IGA, Aldi, and 7-Eleven. But it does not have this advantage on Coles. +Coles is consistently above average. But the gaps are not significant against IGA or Aldi for quality. Convenience gaps, however, are significant versus Aldi. +IGA is near average across most attributes and is not far from Coles on others. IGA’s strongest attributes are customer service and clean, well-maintained stores. +Aldi is similar to Coles and IGA on quality, but trails Woolworths and Coles on convenience. +7-Eleven’s biggest issues are cleanliness and perishables, while their ready-to-eat items are above average. 8 © 2019 dunnhumby Australia Retailer Preference Index

E. The biggest advantage that Woolworths and Coles have is on easy shopping experience.

While easy shopping experience is only the second most important preference driver for Australian shoppers, Woolworths and

Coles are far dominant and it’s what separates them from the pack. It is an opportunity that other retailers might look at to improve

financial performance.

Easy Shopping Experience Value Map

Importance

Satisfaction

9 © 2019 dunnhumby Australia Retailer Preference Index

F. Within the easy shopping experience pillar, Woolworths and Coles have a strong advantage on product variety, one-stop shop, online shopping, discounts and promotions, and rewards. +Woolworths is ahead of Coles on the one-stop shop attributes. But thes gaps are not significant. +Coles has an advantage over Woolworths on discounts and rewards, and these gaps are close to being statistically significant. +IGA and Aldi are significantly below Woolworths and Coles on all attributes except natural/organic variety and sending its Customers useful information. +As a convenience store, it is not surprising that 7-Eleven scores low of most of these attributes. 10 © 2019 dunnhumby Australia Retailer Preference Index

G. Across all retailers (especially IGA and Aldi), catalogue has the largest pre-store influence

Retailer catalogue has the highest influence in Aldi and IGA, as does friends and family. But note: both require an emotional

connection, in real time or in discussion and sharing of information with friends. Across the newer reward and tech-based

experiences, the traction among Customers is not as strong yet. This is a trend that’s become apparent in other geographies.8 But

industry opinion suggests that this soon might change.

Agreement (%T2B) Avge Coles WW Aldi IGA

Retailer Catalogue 44.5% 43.4% 43.9% 46.3% 46.5%

Store Website 27.0% 28.7% 28.0% 28.5% 27.3%

EXPERIENCE

Email 24.5% 25.5% 26.4% 26.6% 24.2%

Coupon 21.4% 23.6% 22.2% 21.3% 21.9%

Friends and Family 34.2% 32.1% 33.0% 35.0% 35.2%

Recipe 19.8% 18.1% 19.2% 20.9% 20.2%

REWARDS

Social Media 14.4% 14.8% 15.5% 15.3% 15.3%

Store App 14.3% 14.0% 13.5% 15.1% 13.3%

8

For comparison, Trader Joe’s in the US – which has earned the top spot in the US Grocery RPI for two consecutive years – has a relatively small

digital footprint. https://www.Customerscontactweekdigital.com/Customers-experience/articles/paradox-of-choice-trader-joes

11 © 2019 dunnhumby Australia Retailer Preference IndexH. Price is Aldi’s main domain today, and they deliver it better than anyone else.

As a global disruptor in retail – leveraging economies of scale9 -- Aldi has commanded an increasing amount of attention among

Customers and media influencers.10 Its growing strength in Australia is impacting competitors. Aldi, Woolworths, and Coles

shoppers are similar on price importance; however it is the satisfaction on delivering to this importance that pushes Aldi forward.

As Aldi and other discounters increase their presence and impact, we expect the price pillar in Australia to become more important

to all retailers. Note: price is most important to 7-Eleven shoppers, while it is the least important to IGA shoppers.

Position Map - Price

Importance

Satisfaction

9

See https://www.youtube.com/watch?v=RD8bai4hNBw. They have configured the store to be ultra-efficient. In the U.S. it only takes about four people

to run a store. Suppliers have to provide product in special boxes to quickly get things to the shelf. Every decision they make is made to reduce costs

and prices.

10

Another Germany-based grocery discounter – Lidl – has also penetrated global markets.

12 © 2019 dunnhumby Australia Retailer Preference IndexI: Customers also perceive Aldi to be the cheapest basket.

In the RPI research, we asked Customers two questions:

+How much do you spend on groceries during a typical month at your primary retailer?

+Imagine a basket of groceries you typically buy costs $100. How much would you expect to spend on this basket of items at the

following retailers?

A startling fact: Customers who primarily shop at Aldi spend $61 less than at Woolworths or Coles. With the reality that Australian

shoppers – like most shoppers around the globe – shop at multiple retailers each week and month, the price of a basket might matter

more and more.

Q. How much do you spend on groceries during a typical Q. Imagine a basket of groceries you typically buy costs

month in your primary retailer $100. How much would you expect to spend on this

basket of items at the following retailers?

$445 $69.18

$465 $87.58

$509 $85.32

$509 $84.39

400 420 440 460 480 500 520 0 10 20 30 40 50 60 70 80 90 100

13 © 2019 dunnhumby Australia Retailer Preference IndexJ: Aldi’s success is not just about price but private brand. The value of private brands -- both as a mechanism for lowering prices and instilling Customer trust11 -- is a global trend, and we are witnessing its impact with Aldi in Australia. Woolworths and Coles significantly trail Aldi on both overall prices and private brand, but beat IGA on these attributes. IGA has the lowest scores in the market on prices, significantly trailing everyone except 7-Eleven. Aldi clearly leads on these attributes, but natural/organic prices are perceived to be more similar across all brands. In the meantime, 7-Eleven performs significantly below average on both overall prices and private brand. The latter could be an opportunity for 7-Eleven. See “Four Reasons CPG Brands Are Losing Out To Retailers’ Private Labels.” https://www.forbes.com/sites/ 11 pamdanziger/2019/04/25/four-reasons-why-cpg-brands-are-losing-out-to-retailers-private-labels/#233c19c41a2b 14 © 2019 dunnhumby Australia Retailer Preference Index

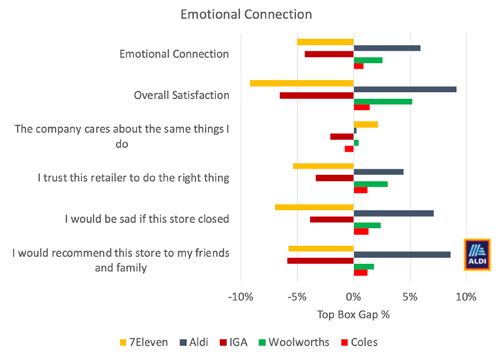

K: Price satisfaction aligns closely with emotional connection Another win for Aldi: it has the strongest emotional connection with its shoppers. Its biggest advantages are on recommendations and satisfaction. This is one of the most worrisome statistics for Woolworths and Coles. A strong emotional connection with its customers suggests it has stronger brand equity, and positions it well for continued success. Specifically, Aldi is significantly higher on the emotional connection attributes of “recommend,” “satisfaction,” and “sad of if store closed.” Woolworths and Coles come second and third in this category. But Woolworths scores higher than Coles on all measures (but only overall satisfaction is statistically significant). For “being the neighborhood store,” one might expect IGA to perform stronger emotionally. But it appears that their poor price perceptions impact that connection. Like IGA, 7-Eleven performs particularly poorly. 15 © 2019 dunnhumby Australia Retailer Preference Index

L: No retailer excels at operations (out-of-stock and inconsistent prices)

This too is part of a global trend. The operational challenges facing retailers today -- getting the basics right, making sure items are on

the shelf with consistent pricing -- are daunting. Operations appear to be less important for Woolworths and Coles. This could be an

opportunity for 7-Eleven, Aldi, and IGA.

Position Map - Operations

Importance

Satisfaction

16 © 2019 dunnhumby Australia Retailer Preference IndexN: “Customer loyalty” is low in Australia: 50 percent, well below global benchmarks.

79.5% of Shoppers have shopped at Woolworths in the last four weeks, compared to 83.3% at Coles. Woolworths and Coles capture

two thirds of all supermarket visits. However more than 53.3% had also shopped at Aldi and 27.8% at IGA.

79.5% of Shoppers have shopped at WW in the last 4 weeks, compared to 83.3% at Coles.

However over 53.3% had also shopped at Aldi and 27.8% at IGA.

Woolworths and Coles capture a 2/3rds of all supermarket visits.

Aldi still has a relatively lower loyalty rate than Coles and Woolworths. This shows that Aldi is still not the primary shop, however provides

ample headroom for the retailer to grow.

Loyalty Conversion Rate Share of visits

60

52% 51% 4%

50 8%

40

15% 38%

30

23%

20

14%

10

2%

0 35%

Coles Woolworths Aldi IGA 7Eleven

17 © 2019 dunnhumby Australia Retailer Preference IndexV. A closer look at Aldi

By now, any reader of the RPI may have concluded that Aldi poses a bigger threat to its competitors12 than previously thought. The

fact remains that there are strategies for each of the retailers to compete on its own terms. That said, there is some benefit to taking

a closer look at Aldi across several dimensions.

+Growth

While Woolworths and Coles dominate market share, Aldi has grown three times as fast over the last three, five, and ten-year

intervals. The compound annual growth rate for Aldi in Australia dwarves its competitors. If Aldi continues to grow at this pace, they

could double their marketshare in ten years.

Compound Annual Growth Rate

Grocery Sales

15

12

9

6

3

0

-3

Aldi 7 Eleven Woolworths Coles IGA

CAGR_3yr CAGR_5yr CAGR_10yr

This is what many of the UK retailers thought and by the time they realized what was happening, Aldi and Lidl captured

12

more than 10% of the market.

18 © 2019 dunnhumby Australia Retailer Preference Index+The evolution of the Aldi store

Aldi also poses a threat by moving toward a more “complete shop,” even with its small range of products. Based on Customer

satisfaction scores, there is still a lot of head room for this retailer. Looking at “shopping trip” highlights -- one of its opportunities

-- Aldi is now catering to all shopping missions and scores higher than IGA in many of the convenience trips. It is 20% below

Woolworths and Coles, but we can see this gap shrinking.

Aldi Shopping Trip / Reason

31.5% 17% 15.5% 31.2%

A quick emergency Snacks Ready meal / dinner Bigger Shop

food trip

+The Aldi shopper: more like everyone

A few statistics about Aldi shoppers:

• It has a higher number of households with 2+ kids vs Coles, WW and IGA.

• It has a similar age spilt to the other retailers. 21% of shoppers are +65 versus (25%) and Woolworths and Coles (19 and 20%)

• It has the same average income splits as Woolworths and Coles.

• It is slightly higher among lower-income shoppers.13

• Highest income earners represent the same percentage of Customerss as Coles (4.6%).

The battle for lower-income shoppers is apparent in other geographies. See “Three Retail Stocks That Have Proven

13

Resilient During Rough Market Climate.” https://finance.yahoo.com/news/3-retail-stocks-proven-resilient-200208397.html

19 © 2019 dunnhumby Australia Retailer Preference Index+Aldi has proven its dominance in price: it might now look at other pillars.

This might also pose a threat to other Australian retailers. There’s a lot of headroom for Aldi to improve convenience & quality perception

-- where it has scored low -- and easy shopping experience. Experience from the U.S. has shown that they have used remodels to clean

up stores, built more modern and updated-looking new stores in higher income areas, and improved perishable quality.

Convenience and Quality Aldi vs Average

Offers appetizing prepared and ready to eat foods

Has the freshest meat, fruits, and vegetables

Offers the highest quality products

Look and feel of the store is up-scale

Staff make me feel valued

My store is clean and well maintained

Has convenient locations

Check out is fast and easy

Its easy to get in and out quickly

0% 10% 20% 30% 40%

Top Box Average Aldi

Convenience and Quality is where Aldi will likely focus their efforts. Aldi are currently winning on price so it is likely that they will focus on

Convenience and Quality improvements to drive future growth

Aldi Value Map

Convenience &

Quality

Price

Easy Shopping

Experience

Importance

Operations

Drive Time

Satisfaction

20 © 2019 dunnhumby Australia Retailer Preference IndexVI. Key takeaways

As noted earlier, there are at least seven key learnings in this first edition of dunnhumby’s Australian Grocery RPI:

In this first RPI in Australia, Woolworths narrowly edges out Coles for the number-one position in customer

1 preference. But Aldi -- the global grocery retail discounter -- looms not far behind.

There are five primary Customers preference drivers (pillars) that the study correlates to emotional connection

2 (long-term brand equity) and financial performance. Here are the drivers, in order of importance to Australian

shoppers: convenience & quality; easy shopping experience; price; operations; drive time.

Despite all the pressure retailers are facing around price, “value perception” – which is about both price and

quality – is what drives Customer preference and financial performance. Woolworths and Coles rise above

3 the others in the quality & convenience pillar (as well as easy shopping experience), whereas Aldi outperforms

on all price attributes.

That said, price has become more important – it equals emotional connection, a critically important outcome of

customer preference. Price correlates closely with trust and other emotional attributes These attributes provide an

4 emotional connection for Customers that ensures they are attracted and stay over the long term. Aldi’s satisfaction

scores reflect these findings as the stand-out price beacon. IGA’s future success depends on getting this right.

Store catalogues still play a key role in Customers pre-store influencers. This suggests that Customers are

creating their own consistent weekly shopping spend, by cherry picking/budgeting across all retailers. There is an

5 opportunity for a retailer to help Customers with total basket spend consistency within a more personalised and

tailored shop.

Everyone shops everywhere: There is very little loyalty between retailers, even those whose primary shop was

6 Coles and Woolworths still claimed one third of their shopping was also in Aldi.

The retail landscape is changing – both globally and in Australia. Aldi is shifting price expectations, making

7 Customers more price sensitive and aware than ever before. This is paving the way for more potential entrants

into the discount space.

Which leads us to an additional, conclusory, takeaway: strategy that’s driven by Data about Customers might empower all grocery

retailers to compete more effectively in Australia. As the Sydney Morning Herald noted, Woolworths and Coles are not standing idly and

waiting for the so-called retail apocalypse. They are “investing heavily in Data analytics and artificial intelligence capabilities to crunch

Data they collect through loyalty schemes, apps and online shopping.” And that’s just the tip of the iceberg in the world of modern retail.

Data-driven strategy can help any competitor to better understand which Customers preferences to pull. Whether it be convenience

and quality, easy shopping experience, price, operations, or drive time. But there are three realities that retailers must confront:

+Low prices alone will not enable them to compete. What modern Customers want is value, which Aldi and others have demonstrated

is about both quality and price.

+The second reality: while many retailers in fact fear the apocalypse, many others see the new era as a retail renaissance. The entire

industry is undergoing profound change, and it will pay for retailers to position themselves on the right side of history.

+Finally -- and it bears repeating -- the reinvention and renaissance in retail is being driven by the democratization of Data Science.

The biggest players in retail are already aware of that, but we are just at the very beginning of this new era. And we believe that we will

see motion across all the indices we presented in this year’s RPI, as early as next year. Data Science might not only democratize –

level the playing field – for retailers. It also might also help retailers look beyond the immediate horizon and plan for their future.

The dunnhumby team

21 © 2019 dunnhumby Australia Retailer Preference IndexReferences https://www.smh.com.au/business/companies/coles-and-woolies-secret-weapon-in-war-with-aldi-is-data-20190529-p51sej.html http://www.roymorgan.com/findings/7936-australian-grocery-market-december-2018-201904050426 https://www.youtube.com/watch?v=Ry31bD5xNgQ https://www.planetretailrng.com/ https://www.youtube.com/watch?v=vzSLiM7hPIo https://www.youtube.com/watch?v=l1wA0n3cklY https://insidefmcg.com.au/2019/05/31/woolworths-turns-focus-to-building-price-trust/ https://finance.nine.com.au/2018/07/09/10/14/aldi-is-now-the-most-trusted-brand-in-the-country For more information about dunnhumby, please visit : https://www.dunnhumby.com/australia 22 © 2019 dunnhumby Australia Retailer Preference Index

THE WORLD’S FIRST CUSTOMER DATA SCIENCE PLATFORM

dunnhumby is the global leader in Customer Data Science, empowering businesses everywhere to compete and thrive in the

modern data-driven economy. We always put the Customer First. Our mission: to enable businesses to grow and reimagine

themselves by becoming advocates and champions for their Customers.

With deep heritage and expertise in retail — one of the world’s most competitive markets, with a deluge of multi-dimensional

data — dunnhumby today enables businesses all over the world, across industries, to be Customer First.

The dunnhumby Customer Science Platform is our unique mix of technology, software and consulting enabling businesses to

increase revenue and profits by delivering exceptional experiences for their Customers – in-store, offline and online. dunnhumby

employs over 2,000 experts in offices throughout Europe, Asia, Africa, and the Americas working for transformative, iconic

brands such as Tesco, Coca-Cola, Meijer, Procter & Gamble, Raley’s, L’Oreal and Monoprix.

Connect with us to start the conversation

dunnhumby.comYou can also read