The Irish economy and the 'New Normal' of 2018 and 2019 - Austin Hughes Chief Economist KBC Bank Ireland - Enterprise Ireland

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

The Irish economy and the

‘New Normal’ of 2018 and

2019

Austin Hughes

Corporate Treasury: Mark Hensey

Mark.hensey@kbc.ie 01 4321400 Chief Economist

Business Banking: Kevin McCarthy

Kevin.mccarthy@kbc.ie 0876684261 KBC Bank Ireland

Sweet or sour?

Global Growth IMF forecasts

5

4.5

4

3.5

3

2.5

2

forecast

Apr-11 Oct-11 Apr-12 Oct-12 Apr-13 Oct-13 Apr-14 Oct-14 Apr-15 Oct-15 Apr-16 Oct-16 Apr-17 Oct-17 Apr-18 Oct-18

date

forecasts for 2012 2013 2014 2015 2016 2017 2018 2019

An upturn for other people An increased global focus

on distributional (and reputational) issues

Demographic trends highlight key social and political

as well as economic changes

Trade tensions risk unravelling a globalised

world

Old and new both seen past the peak

Oceans apart of late

Shared currency, divided countries

Easier monetary policy is the answer. What

was the question?

Horses led to water may be drinking shock!

Central Banks Driving by the rear view mirror

Interest rates turning but market still

focussed on low for long‘Winter is coming’

Brexit; can it be ‘a gentle stroll along a smooth

path to a land of cake and consumption’?

YouGov 29 Nov‘Project fear’ strikes again

Divided they… stand?

I’m an empire , get me out of here

The UK border: preparedness for EU exit 24 OCTOBER 2018

• Key system developments are at risk. In September 2018, BDG reported that 11 of 12 major projects to replace or

change key border systems were at risk of not being delivered on time and to acceptable quality

• Infrastructure identified by government departments cannot be built before March 2019. …Without the necessary

infrastructure, HMRC, Border Force and others may not be able to fully enforce compliance regimes at the border on

day one. They are exploring alternative options

• Businesses do not have enough time to make the changes that will be needed if the UK leaves the EU without a ‘deal’.

Government departments can only implement some of the changes that are required at the border. They are also

heavily dependent on third parties, such as traders, being well-informed and making changes to their systems and

behaviour.. Government papers from July 2018 stated that it was already too late to ensure that all traders were

properly prepared for ‘no deal’.

• ….. Plans are progressing to cope with issues such as queues of traffic in Kent, and to enable the continued supplies of

essential goods and medicines

• In the event of ‘no deal’, departments accept that border operations will be less than optimal on day one….. The

government has not defined what ‘less than optimal’ might mean…Sterling already exposed but still vulnerable

For Ireland, Brexit is a known unknown

40

Ireland’s key trading partners 2015

(share of trade in goods and services)

35

30

25

UK

20 US

Non-UK EU

15

10

5

0

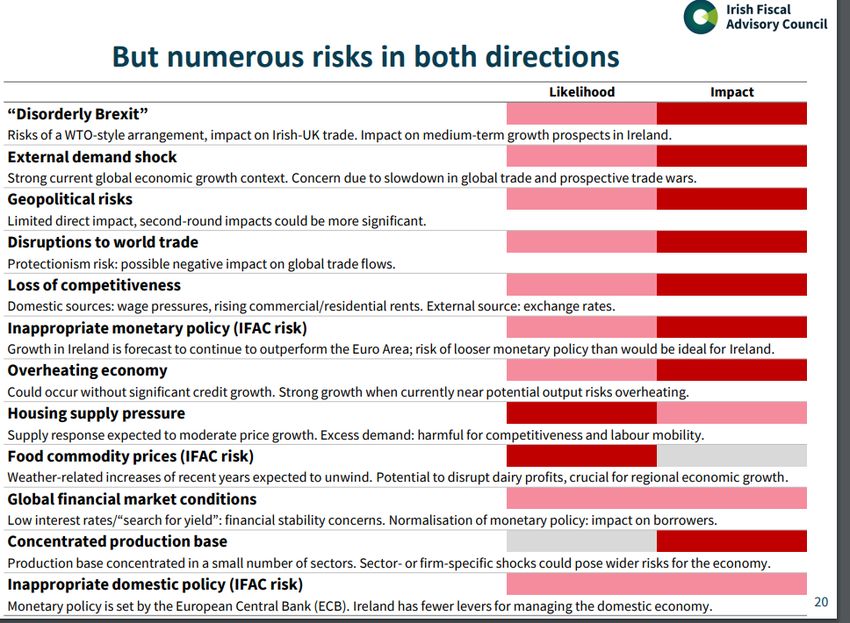

exports imports total tradePrecise scale of Brexit impacts still uncertain but aggregate estimates miss the point

Brexit hasn’t been a real shock… so far

But some areas are suffering

Irish Business beginning to focus on downside

But the end isn’t nigh

Precise scale of Brexit impacts still uncertain but where will hurt most seems clear

Non-Tariff Barriers a notable threat

It’s not all bad news.. (even if it mostly is) FDI could be boosted

Back to the boom?

Jobs growth highlights current momentum

The turn in the Irish economy is forcefully seen in strong and sustained growth in employment

Dublin and Border the standouts but regional

job gains remain choppyPay picking up, not powering ahead

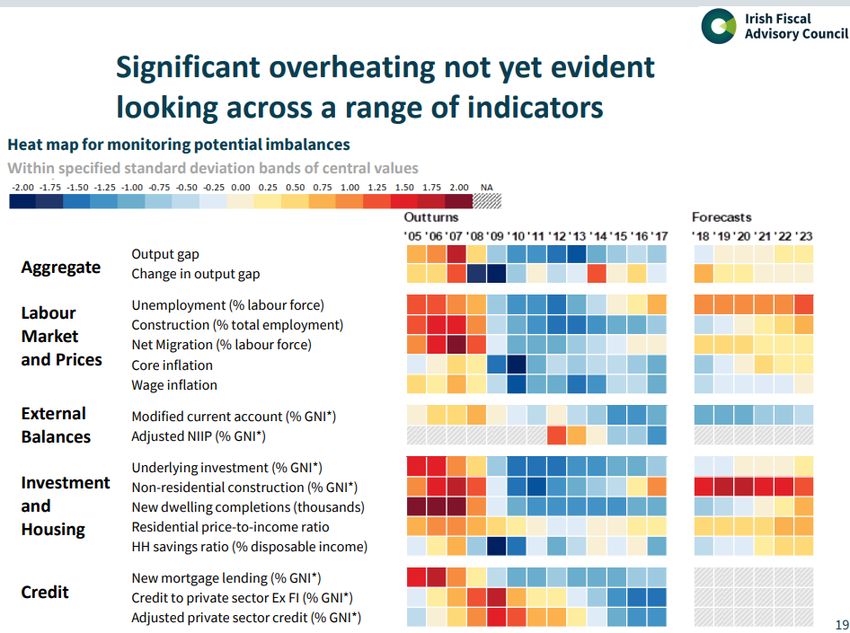

Overheating worries overdone but that doesn’t mean there aren’t problems

Once bitten….

Housing market still a major problem

Jobs Growth and Property Market Telling

Broadly Similar StoriesHousing market slowly moving towards balance but path likely to remain bumpy

Fundamentals still fair?

The housing market remains central to wealth and

woeFiscal constraints less binding than

they appearCan we avoid another own goal?

500

400

Stock of FDI as % of GDP,2015 (source OECD)

300

200

100

0

LUX IRL NLD BEL EST HUN CZE SWE LVA PRT EU SVK GBR AUT ESP POL OECD FIN ISR DNK USA SVN FRA DEU ITA GRC KOR JPNA gradually ageing population creates

opportunities as well as problems

6000000

5000000

679100

493500 560100

4000000

529300

440000 439500 471100

421500

362000 553800 589400 650500

311500

3000000

486100

449400

669200 704000 769500

571600

526600

2000000 724200

776300 623700

548900 628400

656800 565000 608100

642600 639600

1000000

928100 992300 1008600

831800 832400

0

1998 2002 2008 2012 2018

0-14 years 15-24 years 25-34 years 35-44 years 45-54 years 55-64 years 65+ years Employment, TotalIn case I forgot something….

Summary

➢ The ‘New Normal’ is a world of rapid change but slower growth, lower

rates and continuing surprises

➢ Uncertainty and ‘localised’ shocks key features of new global backdrop

➢ Central Banks starting to ‘normalise’. What sort of rate rises are coming

and where?

➢ Some further Brexit twists to come

➢ Irish recovery strong and sustainable but

challenged by ‘Brexit’ and tax wars

uneven sectorally and geographically

still scarred by the crisis

Not notably improved by Budget 2019Business Banking

Presentation to RBK

14.08.2018Welcome to the Bank of You + Your Business

You focus on your business.

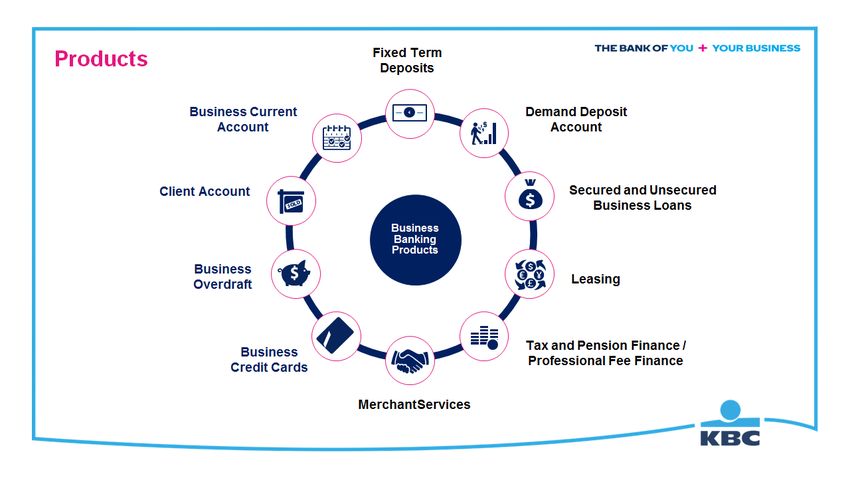

We'll focus on you.What’s special about KBC Business

Banking is that every one of our

customers has a KBC Business

Partner assigned to work with them.

A business partner that knows your

business area and is dedicated to

making sure you get the support

you need.

Someone on your side, at the other

end of the phone or email. If you

can’t come to us, your Business

Partner can come to you.Corporate Treasury KBCI, a provider of Treasury services to Irish corporates for over 40 years. Corporate Deposits Call, Notice and Term – All interest bearing. • Min deposit €500,000 • Turnover > €3mil per annum. • Terms ranging from overnight out to 1 year. • Deposits offered in all major currencies. Foreign Exchange Innovative • Bonus FX – Deposit account rate will be further enhanced by transacting FX with us Vanilla • Spot • Forward . KBCI Treasury do not charge payment or transaction fees. Dedicated Treasury Specialist will manage your trade for its life cycle.

You can also read