The IRS and Treasury Speak - NASPP

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

The IRS and Treasury Speak

1

Speakers

Amber Salotto*

U.S. Treasury Department

amber.salotto@treasury.gov

Stephen Tackney*

Internal Revenue Service

Stephen.B.Tackney@irscounsel.treas.gov

Stephen LaGarde

Ernst & Young LLP

stephen.lagarde@ey.com

Deborah Walker

Cherry Bekaert LLP

DWalker@cbh.com

*Government speakers did not participate in the preparation of these slides

2

Agenda

• Deferral of employee social security tax

• GLAM 2020-004 and IRM procedural update

• Section 162(m)

• Section 409A

• Section 83(i)

• Form 1099-NEC

3

Deferral of employee social

security tax

4

Presidential Memorandum (August 8, 2020)

• Directs Treasury to use section 7508A authority “to defer the withholding,

deposit, and payment of” the employee portion of social security tax on wages

paid September 1, 2020, through December 31, 2020, subject to two

conditions:

− Limited to employees whose bi-weekly wages are less than $4,000 (adjusted for other

payroll periods)

− No penalties, interest, etc. on deferred taxes

• Directs Treasury to “explore avenues, including legislation, to eliminate the

obligation to pay the taxes deferred”

5Notice 2020-65 and IR-2020-195 (August 28, 2020)

• Employer is “allowed” to defer withholding and payment of the employee

share of social security tax from September 1, 2020, through December 31,

2020

• Deferred tax must be withheld and paid ratably from wages paid between

January 1, 2021, and April 30, 2021, or interest, penalties, and additions to tax

will begin to accrue on May 1, 2021

• If necessary, employer “may make arrangements to otherwise collect” the

deferred taxes

• Clarifies that $4,000 threshold is applied each pay period irrespective of

amounts paid in other pay periods

− No distinction between regular wages and supplemental wages (such as equity-based

compensation or bonuses)

6Considerations

• Employee relations

• Employer’s tax/financial exposure

− Responsible party liability

• Administrative challenges

• Likelihood of forgiveness

− For employees with deferred taxes

− For all employees

• Politics

• Additional guidance?

7GLAM 2020-004 and

IRM procedural update

8Live Polling Question

How familiar are you with GLAM 2020-004 and the IRM procedural

update?

A. Not at all familiar

B. Have heard of them, but don’t know what they say

C. Somewhat familiar with the contents

D. Very familiar

9Background

• 2003 Field Directive

− Payroll deposit timing rule based on T+3 SEC rule

− Applied only to NSOs (nonqualified stock options)

• 2012 IRM 20.1.4.26.2 update

− Incorporated 2003 Field Directive rule based on T+3 SEC rule

− Applied only to NSOs

• 2017 SEC settlement cycle regulations

− Changed T+3 to T+2

• 2020

− GLAM 2020-004 (May 18, 2020)

− IRM 20.1.4.26.2 update (May 26, 2020)

10GLAM 2020-004 (May 18, 2020)

• Stock-settled SARs (stock appreciation rights) and NSOs

− Subject to FITW and FICA upon exercise

− Deposit due by close of the next day (if at least $100k of employment taxes accumulated)

• Stock-settled RSUs (restricted stock units)

− Subject to FITW and FICA “when Employer initiates the payment of shares of stock”

− Deposit due by close of the next day (if at least $100k of employment taxes accumulated)

11Observations

• RSU facts are unusual

− “The terms of the RSU provide that the payment of shares will occur on the date the

vesting condition is satisfied” so “Employer initiates payment” on the vesting date

− More typically, vesting and payment would not occur on the same date

− GLAM treats the date the employer “initiates payment” (not vesting) as the relevant date

• Income tax treatment of RSUs

− The GLAM treats stock-settled RSUs as section 83 property

− Compare, for example, Treas. Reg. § 1.451-2 (constructive receipt rules apply to a “stock

bonus”) and Treas. Reg. § 1.83-3(e) (section 83 property does not include “an unfunded

and unsecured promise to pay money or property in the future”)

− Whether section 83 applies may affect the timing of the employer’s tax deduction as well

as the employee’s income and withholding

12Observations (continued)

• FICA treatment of RSUs

− “An RSU award is not a stock right and therefore provides for the deferral of compensation

for purposes of I.R.C. § 3121(v).”

− No mention of Treas. Reg. § 31.3121(v)(2)-1(b)(3)(iii) short-term deferral rule

13IRM 20.1.4.26.2 update (May 26, 2020)

• Narrowed to reflect T+2 SEC rule

• Expanded to include stock-settled SARs and stock-settled RSUs as well as NSOs

• Effective date?

• What if an employer uses share withholding rather than sell-to-cover?

14Section 162(m)

15Live Polling Question

Is your company relying on section 162(m) grandfathering?

A. Yes

B. No

C. Don’t know

D. Not applicable

16Update on proposed section 162(m) regulations

• Grandfathering rule issues

− Modifying performance targets

− Repricing (does it matter if 1:1 or value-for-value)

− Cashing out underwater options

− Acceleration of vesting

− Extension of post-termination exercise period

• Comments Treasury/IRS received

• Timing of final regulations

− Publication

− Applicability date

17Section 409A

18Update on section 409A guidance

• No Code Y reporting for 2020

• Current issues

− Delaying 2020 payments until December 31, 2020

− Possible substitutions arising from agreeing to “forgo” compensation

− Initial deferral elections

− Unforeseeable emergencies

o Cancellation of deferral election

o Acceleration of payment

o Coronavirus-related distributions from 401(k) plans (Notice 2020-50)

• Status of rulemaking

− 2008 proposed section 1.409A-4 “income inclusion” regulations

− 2016 proposed “grab bag” regulations

− 2016 proposed section 457(f) regulations

19Section 83(i)

20Update on section 83(i) guidance

• Notice 2018-97 provided limited guidance

− Rule requiring grant to 80% of employees applies annually, not cumulatively

− Escrow arrangement required for income tax withholding

− Employer may opt out

• Any further guidance?

21Live Polling Question

Additional guidance on section 83(i) would be:

A. Very helpful

B. Helpful, but this is not a top priority

C. Not helpful at all

D. Not applicable

22Form 1099-NEC

23Background

• PATH Act

− Accelerated the due date for filing any Form 1099 that includes nonemployee

compensation (NEC) from February 28 to January 31

− Eliminated the automatic 30-day extension for forms that include NEC

• IRS response

− Rather than having different Form 1099-MISC due dates depending on whether NEC is

reported, the IRS created a “new” Form 1099-NEC beginning with tax year 2020

o “Experienced” practitioners may recall the original Form 1099-NEC from circa 1980

− Form 1099-MISC has been revised/rearranged in light of Form 1099-NEC

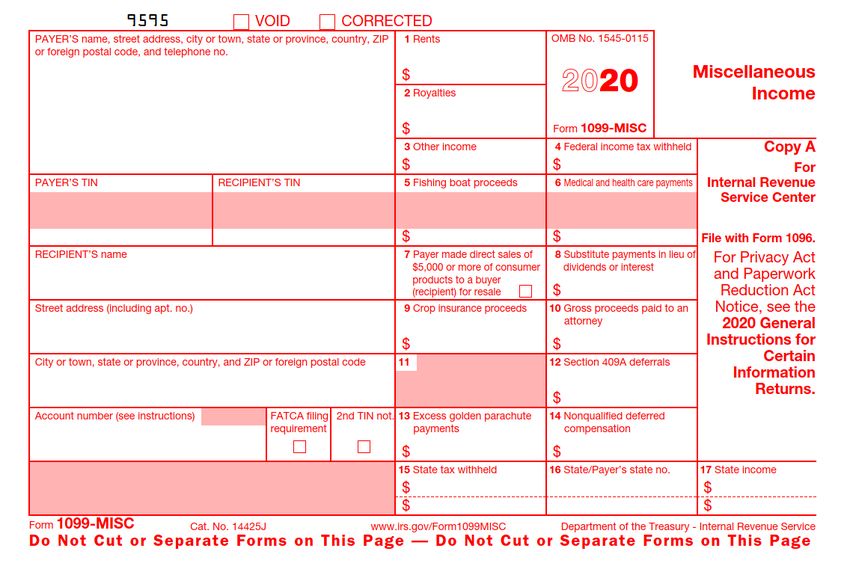

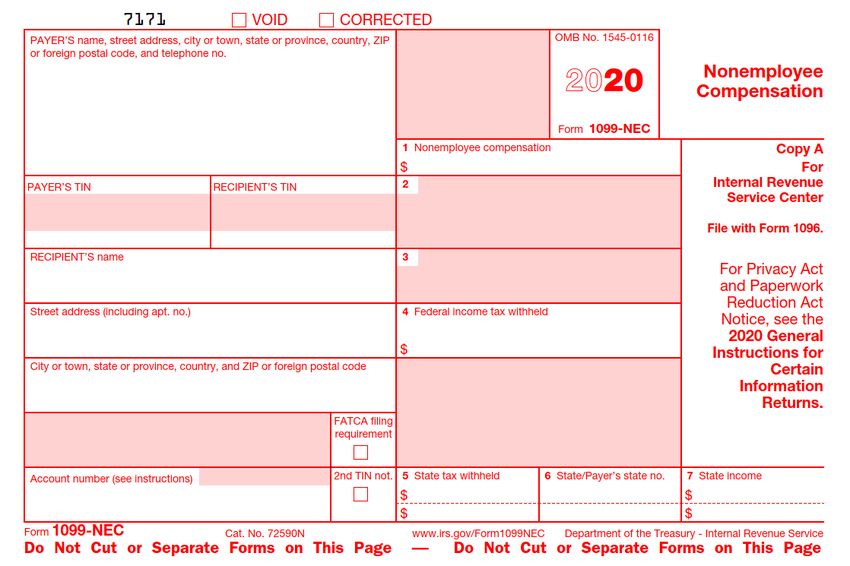

242020 Form 1099-MISC vs. 2020 Form 1099-NEC

25Live Polling Question

Do you have experience with the original Form 1099-NEC?

A. Yes

B. No

C. Maybe

D. Not applicable

26Questions?

27Thank You!

28You can also read