Valuation Information: 21 - 25 Teed Street, Auckland - Sorted ...

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Valuation Information: 21 – 25 Teed Street, Auckland About this document CBRE Limited (CBRE) prepared and issued a valuation report in respect of the property at 21 – 25 Teed Street, Auckland as at 31 July 2021 (Valuation Report). This document comprises: Part A: a letter as at 31 August 2021 issued by CBRE in respect of the Valuation Report; and Part B: a summary of the Valuation Report prepared by CBRE. The information contained in this document has been prepared by CBRE and should be read in conjunction with Fabric Property Limited’s Product Disclosure Statement dated 13 September 2021 (PDS) and other information included on the Offer Register. References to "Stride Office Property Limited" are references to "Fabric Property Limited" (which changed its name from Stride Office Property Limited on 3 September 2021).

Part A: Letter as at 31 August 2021 issued by CBRE in respect of the

Valuation Report

Part B: Summary of the Valuation Report prepared by CBRE

CBRE VALUATION & ADVISORY SERVICES VALUATION REPORT 21-25 TEED STREET N E W M A R K E T, AU C K L A N D C L I E N T: STRIDE OFFICE PROPERTY LIMITED VA LUAT I O N DAT E : 3 1 J U LY 2 0 2 1 © CBRE LIMITED | VALUATION REPORT | PAGE 1 of 57

21-25 TEED STREET, NEWMARKET, AUCKLAND

31 JULY 2021

CONTENTS

1 INTRODUCTION .................................8 5.6 Car Park Rental Analysis .............................. 28

1.1 Instructions ................................................... 8 5.7 Naming & Signage Rights Rental Analysis ..... 29

1.2 Market Value Definition ................................. 8 5.8 Market Rent Assessment ............................... 29

1.3 Industry Practice ............................................ 8 5.9 Sales Evidence ............................................. 30

1.4 Fair Value Definition ..................................... 8 5.10 Key Sales Evidence Commentary .................. 30

1.5 Financial Reporting Standard ......................... 8 5.11 Sales Evidence Conclusion ........................... 35

1.6 Reliance ....................................................... 9 6 VALUATION ...................................... 36

1.7 Information Provided ................................... 10

6.1 Valuation Approaches .................................. 36

1.8 Special Assumptions .................................... 10

6.2 Capitalisation Approach .............................. 36

2 LAND ................................................11 6.3 Discounted Cashflow Approach .................... 37

2.1 Location ..................................................... 11 6.4 Valuation Reconciliation ............................... 40

2.2 Resource Management ................................ 12 6.5 Additional Requirements .............................. 40

2.3 Site Description ........................................... 13 7 DISCLAIMERS .................................... 41

2.4 Legal Description ........................................ 14

8 APPENDICES ..................................... 44

3 IMPROVEMENTS ................................16 Record of Title

3.1 Overview .................................................... 16 Valuation Definitions and Terminology

3.2 Accommodation.......................................... 16 Major Tenant Lease Summaries

3.3 Floor Areas ................................................. 19

3.4 Construction Details .................................... 19

3.5 Interior Finishes........................................... 19

3.6 Services ...................................................... 19

3.7 Capital Expenditure ..................................... 20

4 OCCUPANCY ....................................21

4.1 Tenancy Schedule ....................................... 21

4.2 Lease Commentary ..................................... 21

4.3 Lease Expiry Analysis ................................... 22

4.4 Outgoings .................................................. 22

4.5 Net Income Summary .................................. 23

5 MARKET.............................................24

5.1 Auckland Non-CBD Office Market Commentary

.................................................................. 24

5.2 Office Rental Evidence ................................. 26

5.3 Subject Office Rental Evidence ..................... 26

5.4 Office Rental Evidence Commentary ............ 26

5.5 Retail Rental Evidence .................................. 28

© CBRE LIMITED | VALUATION REPORT | PAGE 2 of 57

21-25 TEED STREET, NEWMARKET, AUCKLAND

31 JULY 2021

Teed Street Frontage

© CBRE LIMITED | VALUATION REPORT | PAGE 3 of 57

21-25 TEED STREET, NEWMARKET, AUCKLAND

31 JULY 2021

VALUATION SUMMARY

This report has been prepared for inclusion within a Product Disclosure Statement and will be uploaded to the

Companies Office Disclosure Register. Accordingly, in the interests of privacy and confidentiality, we have

abbreviated or redacted the following report sections:

• Rental Evidence (Sections 5.2 and 5.5): We have not included full details of the rental evidence considered

in order to protect the privacy requirements of the Lessors and Lessees involved. Notwithstanding, we have

summarised the key comparables and provided market rental ranges.

• Major Tenant Lease Summaries (Appendices): At the request of Stride Office Property Limited, this section

has been redacted to protect the privacy of lessees. Key lease details are summarised in the Tenancy

Schedule on page 21.

Market Value (plus GST if any)

$27,300,000

The above valuation is subject to the Special Assumptions and Disclaimers within this Report.

Key Valuation Metrics

Initial Yield: 6.39% Net Passing Income: $1,745,340 pa

Rate $psm (Excl. Cars): $5,786 psm Net Passing Income (Fully Leased): $1,766,660 pa

Adopted Cap Rate: 5.50% Net Market Income (Effective): $1,608,605 pa

Adopted Target IRR: 6.625% % Over Rented (On Occupied): 9.96%

Adopted Terminal Yield: 5.75% No. of Tenants: 13

Area (NLA): 4,027.2 sqm WALT (Income): 1.74 years

Car Bays: 82 Vacancy Rate: Nil

Key Valuation Assumptions

CPI: 1.92% (10 Yr Avg) Total Adopted Capex (10 yrs): $3,627,184

Office Mkt Rent Growth: 2.23% (10 Yr Avg) Office New Lease Term: 6 years

Retail Mkt Rent Growth: 2.08% (10 Yr Avg) Retail New Lease Term: 6 years

Outgoing Growth: 2.27% (10 Yr Avg) Renewal Probability: 50%

Tenancy Profile by Income Property Risk Profile

$3,000,000 Location Quality

$2,500,000

$2,000,000

$1,500,000

Liquidity Asset Quality

$1,000,000

$500,000

$0

Year 1 Year 2 Year 3 Year 4 Year 5 Year 6 Year 7 Year 8 Year 9 Year 10

Lettability Tenant Covenant

Renewal Rent Secured Rent Gross Market Rent (fully leased)

© CBRE LIMITED | VALUATION REPORT | PAGE 4 of 57

21-25 TEED STREET, NEWMARKET, AUCKLAND

31 JULY 2021

Income Breakdown Lease Expiry (by rent)

100%

Coffey Services (NZ) 90%

Limited 80%

30% 21%

Banzpay Technology 70%

Operations Limited 60%

50%

Kingston Property

Limited 40%

30%

Terabyte Interactive

20%

Limited

10%

17% City Rail Link Limited 0%

9%

Other

10% Vacancy Renewals Initial Expiries

13%

Property Description

A 6 level commercial building comprising ground level retail, ground and Level 1 parking and 5 upper office

levels. The building was constructed circa 1986 and has been progressively refurbished to provide good quality

retail and office accommodation. The property occupies a strong location within Newmarket and benefits from

a wide frontage to Teed Street.

Prepared by CBRE Limited

Bradley Unthank, B.Prop, B.Com, MPINZ Cameron Barber, B.Prop

Registered Valuer Valuer

Director

Principal Valuer Valuation & Analysis Assistance

Property Inspected: Yes Property Inspected: Yes

Campbell Stewart, SPINZ, ANZIV, MRICS

Registered Valuer

National Director

Co-Signatory in capacity of Director

The Co-Signing Director confirms having reviewed the valuation methodology and calculations, however the opinion of value expressed has

been arrived at by the Principal Valuer alone.

© CBRE LIMITED | VALUATION REPORT | PAGE 5 of 5721-25 TEED STREET, NEWMARKET, AUCKLAND

31 JULY 2021

SWOT & RISK ANALYSIS

Strengths Weaknesses

◼ The property occupies a central location within ◼ Relatively short WALT of 1.74 years.

Newmarket experiencing strong levels of occupier

◼ Approximately 25% of passing income is from the

demand for both the retail and office areas.

retail component. Market conditions are

◼ Good level of surrounding amenity with the particularly challenging in the retail sector at

Newmarket strip retail precinct a short distance to present.

the east.

◼ The building has a current seismic rating of 50%

◼ The office and retail accommodation is fully leased. NBS, however works are planned to improve this to

at least 67% NBS.

◼ Strong linkages to the Auckland motorway system

and proximate to the Newmarket Railway Station. ◼ Somewhat limited outlook to lower levels.

◼ Good quality office accommodation having been ◼ Despite some recent refurbishment works, the

progressively refurbished. building will require continued capital expenditure

to remain competitive.

◼ Office floor plates of 820 sqm are considered to be

a good size and are easily sub-divided into smaller

tenancies.

◼ 82 car parking bays, reflecting 1 bay per 49 square

metres of lettable area. This is a strong car parking

ratio.

◼ Investment quantum appealing to a range of

purchasers.

Opportunities Threats

◼ Potential redevelopment options over the longer ◼ Office leasing competition from several superior

term. quality developments in Newmarket.

◼ Opportunity to negotiate longer lease terms with ◼ Retail leasing competition from the recently

the monthly retail tenants, improving the overall redeveloped Westfield 277 Newmarket shopping

income risk profile of the asset. centre.

◼ Office and retail vacancy rates have risen markedly

as a result of the economic impacts of COVID-19

combined with new supply. Net effective market

rents have also been affected in some areas.

◼ We refer you to the Market Risk comments below.

© CBRE LIMITED | VALUATION REPORT | PAGE 6 of 5721-25 TEED STREET, NEWMARKET, AUCKLAND 31 JULY 2021 Market Risk Comment Commercial property value growth has been strong in many sectors in recent years, even with the disruption caused by COVID-19 through 2020. This growth is largely due to historically low interest rates, alternative investment markets demonstrating more risk and volatility and low vacancy rates in some sectors (particularly industrial). Prime quality strongly leased property transactions continue to show some yields at historical lows. Notwithstanding currently buoyant conditions in many parts of the property market, the ongoing impact of COVID-19 upon the global economy means that values and incomes may change more rapidly and significantly than during standard market conditions. Should economic and property market conditions deteriorate in the future, then the market value of this asset may decline. This inherent risk factor should be considered in any lending or investment decisions. © CBRE LIMITED | VALUATION REPORT | PAGE 7 of 57

21-25 TEED STREET, NEWMARKET, AUCKLAND

31 JULY 2021

Introduction

1 INTRODUCTION

1.1 INSTRUCTIONS

Instructing Party: Jessica Rod on behalf of Stride Office Property Limited

Purpose of Valuation: Inclusion within a Product Disclosure Statement

Land

Basis of Valuation: Market Value ‘As Is’

Date of Inspection: 5 July 2021

Date of Valuation: 31 July 2021

1.2 MARKET VALUE DEFINITION

Improvements

In accordance with the International Valuation Standards (IVS), the definition of market value is: "The

estimated amount for which an asset or liability should exchange on the valuation date between a willing

buyer and a willing seller in an arm's length transaction, after proper marketing and where the parties had

each acted knowledgeably, prudently and without compulsion."

1.3 INDUSTRY PRACTICE

Occupancy

Subject to the assumptions and qualifications detailed within, this valuation report is issued in accordance

with the ‘Guidance Papers for Valuers & Property Professionals' effective 1 July 2021 and International

Valuation Standards (IVS) effective 31 January 2020. Where these are at variance, the assumptions and

qualifications included within this valuation report will prevail generally, and the International Valuations

Standards will prevail over the ‘Guidance Papers for Valuers & Property Professionals'.

We hereby certify that the Principal Valuer is suitably qualified and authorised to practise as a valuer; does

Market

not have a pecuniary interest, financial or otherwise, that could conflict with the proper valuation of the

property; and accepts instructions to value the property only from the Responsible Entity/Instructing Party.

1.4 FAIR VALUE DEFINITION

We have also had regard to the requirements of the New Zealand Equivalent to International Financial

Reporting Standard 13 (NZ IFRS 13). In particular, we have considered NZ IFRS 13 Fair Value Measurement,

Valuation

which adopts the following definition of Fair Value:

"Fair value is the price that would be received to sell an asset or paid to transfer a liability in an orderly

transaction between market participants at the measurement date."

Fair Value under NZ IFRS 13 is generally synonymous with the concept of Market Value under IVS 2017.

Under IVS, the date of valuation is the date at which our opinion of value applies, which in this case is 31

Disclaimers

July 2021. This is different to the date of inspection which is 5 July 2021. Our valuation is on the basis that

there are no material physical changes between the Inspection Date and Date of Valuation.

1.5 FINANCIAL REPORTING STANDARD

The valuation is undertaken in accordance with the requirements of PINZ Valuation and Property Standards

– NZVTIP 2 Valuations for Use in New Zealand Financial Reports. The property is an investment property

Appendices

© CBRE LIMITED | VALUATION REPORT | PAGE 8 of 5721-25 TEED STREET, NEWMARKET, AUCKLAND

31 JULY 2021

Introduction

and the valuer in conducting this report has also observed the requirements of New Zealand International

Accounting Standard 40 – Investment Property (NZ IAS 40).

1.6 RELIANCE

Reliance: This valuation is strictly and only for the use of the following Reliant Parties and

Purposes:

Land

◼ Stride Office Property Limited for inclusion within a Product Disclosure Statement

only.

◼ Due diligence committees established for the purpose of the proposed initial public

offer of shares in SOPL and listing of SOPL on the NZX Main Board (the offer).

For clarity, reliance is not extended to investors in Stride Office Property Limited.

Improvements

The Client acknowledges and agrees that all material or documents created by CBRE

in providing the Services are provided for its benefit and the purposes set out in the

Report and may not be relied on by anyone other than the Reliant Parties. We do not

assume any responsibility or accept any liability in circumstances where this valuation

is relied upon by any Reliant Party after the expiration of 90 days from the date of

valuation, or such earlier date if the Reliant Parties become aware of any factors that

have any effect on the valuation.

Occupancy

Confidentiality: Any valuation service is confidential as between CBRE and the Reliant Party as

specifically stated in the valuation advice/report. Neither the whole of the report, nor

any part of it, may be published in any document, statement, circular or otherwise by

any party other than CBRE, nor in any communication with any third parties, without

the prior written approval of CBRE of the form and context in which it is to appear,

which may be conditional on relevant third parties first executing (i) a reliance letter

Market

on terms approved by CBRE where the third party wishes to use and/or rely on the

relevant information; or (ii) a non-reliance letter where the third party wishes to use

the report for information purposes only.

Transmission: Only an original valuation report (hard and/or soft copy) received by the Reliant Parties

directly from CBRE without any third party intervention can be relied upon.

Restricted: No responsibility is accepted or assumed to any third party who may use or rely on Valuation

the whole or any part of the content of this valuation.

Copyright: As between CBRE, the Instructing Party and the Reliant Parties, all intellectual property

rights in this Valuation Report are owned by CBRE. Neither the whole nor any part of

the content of this valuation may be published in any document, statement, circular or

otherwise by any party other than CBRE, nor in any communication with any third

party, without the prior written approval from CBRE, and subject to any conditions

Disclaimers

determined by CBRE, including the form and context in which it is to appear.

Appendices

© CBRE LIMITED | VALUATION REPORT | PAGE 9 of 5721-25 TEED STREET, NEWMARKET, AUCKLAND

31 JULY 2021

Introduction

1.7 INFORMATION PROVIDED

We have been provided with the following key information which has been relied upon within our report:

◼ Tenancy Schedule and Lease Documentation provided by Stride.

◼ Outgoings budget for the year ending 31 March 2022 provided by Stride.

◼ Detailed Seismic Assessment Report prepared by Envelope Structural Limited dated 31 May 2021.

Land

◼ Preliminary Budget Estimate for Seismic Work to 25 & 35 Teed Street prepared by WT Partnership dated

24 June 2021.

◼ Technical Due Diligence Report prepared by Cedar Tree Building Consultants dated 28 May 2021.

◼ Asbestos Management Survey Report prepared by Accurate Consulting Limited.

Improvements

Our valuation is undertaken on the basis that provided information is accurate. Should this not be the case,

we reserve the right to amend our valuation.

1.8 SPECIAL ASSUMPTIONS

Assumptions are a necessary part of undertaking valuations. CBRE adopts assumptions for the purpose of

providing valuation advice because some matters are not capable of accurate calculation or fall outside the

scope of our expertise, or our instructions. Assumptions adopted by CBRE will be formulated on the basis

Occupancy

that they could reasonably be expected from a professional and experienced valuer. The Reliant Parties

accept that the valuation contains certain specific assumptions, and acknowledges and accepts the risk that

if any of the assumptions adopted in the valuation are incorrect, then this may have an effect on the

valuation. Refer to the Disclaimers, Limitations and Qualifications Section, which is pertinent to this valuation

report.

Particularly critical to our valuation are the following assumptions:

Market

Seismic A Detailed Seismic Assessment Report provided identifies a Critical Structural

Strength: Weakness, being the roof level cantilever steel columns. Accordingly, the seismic rating

is ~50% NBS(IL2).

We have been advised that the owner intends to seismically strengthen the building to

>67% NBS and the budgeted costs for remediation works are $138,000. Our

Valuation

valuation is prepared on the basis that the remediation costs provided are accurate

and that the subject achieves a seismic rating of no less than 67% NBS on completion.

Disclaimers

Appendices

© CBRE LIMITED | VALUATION REPORT | PAGE 10 of 5721-25 TEED STREET, NEWMARKET, AUCKLAND

31 JULY 2021

Introduction

2 LAND

2.1 LOCATION

Location Map:

Land

Improvements

Occupancy

View the subject property in Google Maps.

Nearest Main Newmarket is a well-established fringe CBD commercial and retail location,

Centre: approximately 4 kilometres south east of the Auckland CBD.

Location & A central position within Newmarket, proximate to the prime retail and pedestrian

Surrounds: areas that are orientated around the Broadway/Remuera Road intersection.

Market

Newmarket is acknowledged as a premier retail strip destination in the Auckland

market, with the majority of major retailers present. The strength of the location has

provided the impetus for ongoing development.

Newmarket is also a well-established fringe CBD office location. This is considered a

strong fringe location, experiencing good occupier demand.

Valuation

Given the central Newmarket location, the subject property is surrounded by low rise

commercial properties with an emphasis on ground level retail or showroom

activities. Located within proximity to the subject is Westfield's 277 Broadway

shopping centre, which has recently been extensively expanded and redeveloped.

Transport Links: Newmarket Railway Station is situated approximately 350 metres to the east of the

subject. The property has good motorway linkages via Gillies Avenue which provides

Disclaimers

access to the northern and north western motorways, whilst access to the southern

motorway is obtained via Khyber Pass Road.

Appendices

© CBRE LIMITED | VALUATION REPORT | PAGE 11 of 5721-25 TEED STREET, NEWMARKET, AUCKLAND

31 JULY 2021

Introduction

2.2 RESOURCE MANAGEMENT

Local Authority Auckland Council, Auckland Unitary Plan Operative in part (15 November 2016).

and Plan:

Zone: Business – Metropolitan Centre Zone

This zone applies to centres located in different sub regional catchments of Auckland.

These centres are second only to the city centre in overall scale and intensity and act

Land

as focal points for community interaction and commercial growth and development

and contain hubs serving high frequency transport.

The zone provides for a wide range of activities including commercial, leisure, high

density residential, tourist, cultural, community and civic services. Zone provisions, in

conjunction with rules in the other business zones, reinforce metropolitan centres as

Improvements

locations for all scales of commercial activity. These centres are identified for growth

and intensification. Expansion of these centres may be appropriate depending on

strategic and local environmental considerations.

Precincts and overlays that modify the underlying zone or have additional provisions

apply to some of the metropolitan centres. Generally, however, to support an intense

level of development, the zone allows for high-rise buildings.

Occupancy

View full details of the relevant zone planning controls.

Indicative The Zone provides for a wide range of permitted activities including office, retail,

Permitted Uses: leisure, high density residential, tourist, cultural, community and civic services.

Key The maximum height of the building must not exceed 72.5 metres unless otherwise

Development specified in the Height Variation Control on the planning maps (see below).

Controls:

If the new building exceeds 32.5 metres in height a minimum setback of 6 metres is

Market

required.

Additional wind requirements apply to any new building exceeding 25 metres in

height.

Additional maximum tower dimension and tower separation controls apply to any

new high rise building. Valuation

Present Use: The present use appears to comply with the underlying zoning.

Site Controls, Natural Heritage: Regionally Significant Volcanic Viewshafts and Height Sensitive

Overlays & Areas Overlay [rcp/dp] – E11 & E12, Mount Eden, Viewshafts

Designations:

◼ The purpose of this is to protect regionally significant views to the Auckland

Disclaimers

maunga. Buildings that intrude into a regionally significant volcanic viewshaft

require restricted discretionary activity consent up to 9 metres in height, beyond

which they are a non-complying activity. According to the planning maps, the

volcanic viewshaft starts at approximately 35.5 metres above the subject site.

Controls: Building Frontage Control – General Commercial Frontage

Controls: Macroinvertebrate Community Index – Urban

Appendices

© CBRE LIMITED | VALUATION REPORT | PAGE 12 of 5721-25 TEED STREET, NEWMARKET, AUCKLAND

31 JULY 2021

Introduction

Development We are not aware of any development approvals currently relating to the site.

Approvals:

Highest and Best The current use is considered to be the highest and best use of the property.

Use:

Heritage Listing: Our online search of Council records did not identify any Heritage issues.

Land

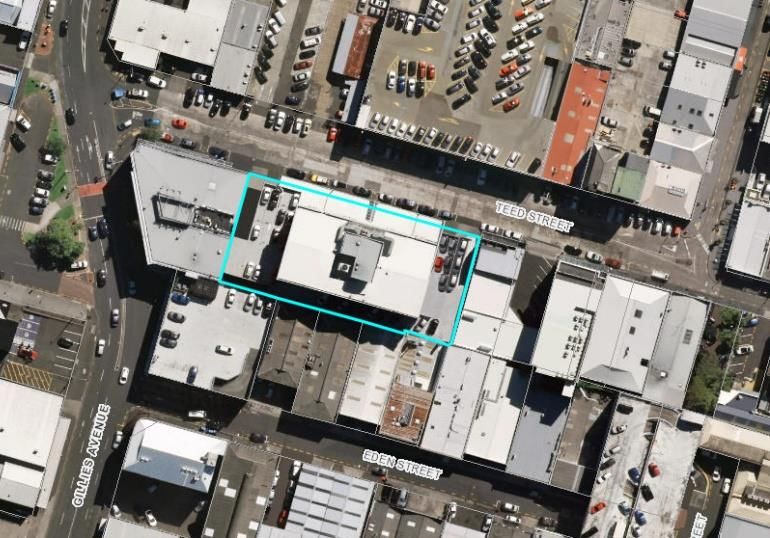

2.3 SITE DESCRIPTION

Improvements

Occupancy

Aerial View Indicative Title Boundaries

Land Area: 2,028 sqm (more or less).

Contour: Relatively level throughout.

Market

Services: All typical municipal services appear to be connected to the site.

Accessibility: Access available via Teed Street.

Valuation

Disclaimers

Appendices

© CBRE LIMITED | VALUATION REPORT | PAGE 13 of 5721-25 TEED STREET, NEWMARKET, AUCKLAND

31 JULY 2021

Introduction

Potential Flooding: The site is bisected by an Overland Flow Path and is identified within a Flood Plain

( ) and a Flood Prone Area ( ).This is depicted on the plan below:

Land

Improvements

Occupancy

Contamination: We have requested site contamination information held within the Environmental

Health Unit of the Licensing and Compliance Services Department, Auckland

Council. The Contaminated Site Enquiry team have advised us that there is no

contamination information held within their records for this site. Of necessity our

valuation assumes that there are no contamination issues that would have a

material effect on the market value, use or marketability of the property which

Market

would prevent the property from continuation of its current use.

We are not environmental experts and we do not know the extent of contamination

(if any). Should subsequent investigations reveal the presence of contaminated

material, we reserve the right to revisit our valuation.

2.4 LEGAL DESCRIPTION Valuation

Identifier Lot Plan Area Registered Owner Tenure

(sqm)

NA65C/273 Lot 1 DP 115150 2,028 Stride Property Limited Fee Simple

Disclaimers

Relevant Interests: Registrations of note include:

◼ Subject to an electricity right (in gross) over part in favour of The Auckland Electric

Power Board created by Transfer C0178813.1

◼ Subject to a light and air, and service rights over part marked F on DP 115150

created by Transfer B796313.2.

Appendices

© CBRE LIMITED | VALUATION REPORT | PAGE 14 of 5721-25 TEED STREET, NEWMARKET, AUCKLAND

31 JULY 2021

Introduction

◼ Subject to a light and air, and service rights over part marked E on Plan 115149

created by Transfer B752977.8.

◼ Subject to a light and air right over part marked D on Plan 115149 created by

Transfer B752977.7.

◼ Subject to a light and air right over part marked C on Plan 115149 created by

Transfer B752977.6.

Land

◼ Some of the easements created by Transfer B752977.3 are subject to Section

309 (1) (a) Local Government Act 1974.

◼ Subject to a right of way and to light and air, and stormwater drainage rights

over part marked A and to light and air right over part marked B on Plan 115149

created by Transfer B752977.3.

Improvements

The above easements regarding the rights of way, light and air easements relates to

a small area situated at the rear of the site, on the boundary with the adjoining

building to the south as depicted in the plan below:

Occupancy

Market

Valuation

We do not consider these easements impact the value of the property in its current

configuration.

Title Search: We refer you to the Appendix for copies of the relevant title documentation.

Disclaimers

Appendices

© CBRE LIMITED | VALUATION REPORT | PAGE 15 of 5721-25 TEED STREET, NEWMARKET, AUCKLAND

31 JULY 2021

Introduction

3 IMPROVEMENTS

3.1 OVERVIEW

Brief Description: A 6 level commercial building comprising ground level retail, ground and Level 1

parking and 5 upper office levels.

Age: Circa 1986.

Land

Condition and Generally good having regard to its age and use.

Repair:

Capital We have been provided with a detailed 10 year capital expenditure schedule, which

Expenditure: we have adopted within our valuation (refer Section 3.7).

Improvements

BWOF: The BWOF sighted during our inspection expired on 17 June 2021. Of necessity,

our valuation is on the basis that the buildings comply with the relevant provisions

of the Building Act 2004. Should this prove to be incorrect, we reserve the right to

review and if necessary amend our valuation findings.

Asbestos: We have received an Asbestos Management Survey Report undertaken by Accurate

Consulting Limited dated 24 November 2017. This report indicates that asbestos

is potentially contained within the following areas with the following risk levels:

Occupancy

◼ Gaskets to pipework flanges – Low to moderate Risk.

Control measures advised are: “Control and monitor”.

The presence of asbestos is still very much prevalent on older buildings throughout

Auckland. This generally does not pose a problem as long as the building is well

maintained. The subject is listed within the report as being maintained in a “Fair”

condition. Extra demolition costs will be incurred if the improvements are removed.

Market

Seismic Comment: A Detailed Seismic Assessment Report provided identifies a Critical Structural

Weakness, being the roof level cantilever steel columns. Accordingly, the seismic

rating is ~50% NBS(IL2).

We have been advised that the owner intends to seismically strengthen the building

to >67% NBS and the budgeted costs for remediation works are $138,000. Our

Valuation

valuation is prepared on the basis that the remediation costs provided are accurate

and that the subject achieves a seismic rating of no less than 67% NBS on

completion. Refer Special Assumptions.

3.2 ACCOMMODATION

Retail Tenancies: The ground level incorporates 5 retail tenancies with frontage to Teed Street that

Disclaimers

range between 92 and 136 sqm in size. The shops have full height retail glazing

to the frontages with a generous stud height towards the frontage and a double

height stud at the rear. Shops 2 & 3 benefit from secondary frontage to the entrance

lobby of the building. The tenancies comprise a mix of plasterboard lined, exposed

or suspended tile ceilings and are provided with air conditioning and lighting. A

canopy extends the length of the Teed Street frontage. Amenities are provided at

Appendices

the ground floor including bathroom facilities.

© CBRE LIMITED | VALUATION REPORT | PAGE 16 of 5721-25 TEED STREET, NEWMARKET, AUCKLAND

31 JULY 2021

Introduction

Land

Upper Levels: Access to the upper office levels is provided via the ground level lift lobby that is

accessed directly from Teed Street. The lobby also provides access to the ground

level parking spaces situated at the rear of the building. It is recessed from the street

frontage and presents to a reasonable standard with ceramic tiling, plasterboard

Improvements

linings, feature lighting and a double height atrium.

The Level 1 office accommodation is essentially a mezzanine area being set behind

the double height retail space. Outlook and natural light are limited with glazing

to the southern elevation only, overlooking the Level 1 parking area. This space has

a lower stud height than the levels above. The western tenancy on Level 1 is utilised

as storage by Coffey Services (NZ) Limited.

Occupancy

Levels 2-5 comprise good quality office accommodation that has been

progressively refurbished in recent years. The levels have a stud height of 2.6 metres

with external glazing extending from approximately 80 centimetres above the floor

level to 30 centimetres below the ceiling where a bulkhead protrudes outwards due

to the bay window configuration.

The tenancies are typically provided with carpet floor coverings, plasterboard lined

Market

walls and suspended ceiling tiles incorporating fluorescent lighting, air conditioning

diffusers and smoke detection systems. Views obtained from the upper levels are

considered to be reasonable with good levels of natural light due to the elongated

floor plates and extensive glazing. Male and female amenities are provided on

each level and present to a good standard.

Valuation

Disclaimers

Appendices

© CBRE LIMITED | VALUATION REPORT | PAGE 17 of 5721-25 TEED STREET, NEWMARKET, AUCKLAND

31 JULY 2021

Introduction

Land

Car Parking: The car parks within the subject building are located on the ground and Level 1.

The ground level parks are situated behind the retail tenancies and are accessed

directly from the Teed Street frontage. They are secured by automated roller doors

at either end of the retail tenancies. The ground level provides approximately 29

Improvements

single parking spaces. The upper level parking spaces are accessed via an ingress

ramp from the eastern side of the frontage and an egress ramp from the western

side of the frontage. Parking to level 1 comprises 32 single parks and 21 triple

stacked parks.

The building provides a total of 82 car parking bays, reflecting 1 bay per 49 sqm

of lettable area.

Occupancy

Market

Floor Plan: The layout of a typical upper level tenancy (Level 4) is illustrated in the following

floor plan:

Valuation

Disclaimers

Appendices

© CBRE LIMITED | VALUATION REPORT | PAGE 18 of 5721-25 TEED STREET, NEWMARKET, AUCKLAND

31 JULY 2021

Introduction

3.3 FLOOR AREAS

LETTABLE AREA ANALYSIS Tenant Lettable % of

Type Area (sqm) Total

Major Tenants

Other Tenants

Coffey Services (NZ) Limited Office 903.5 22.44% 23%

Banzpay Technology Operations Limited Office 818.9 20.33%

Kingston Property Limited Office 541.6 13.45%

Terabyte Interactive Limited Office 373.4 9.27%

City Rail Link Limited Office 445.0 11.05%

Land

Major Tenants 3,082.4 76.54%

Other Tenants

Other Office Tenants 374.7 9.30%

Other Retail Tenants 570.1 14.16%

Other Tenants 944.8 23.46% Major Tenants

77%

Total 4,027.2 100.00%

Improvements

Source: Certified plans.

3.4 CONSTRUCTION DETAILS

Foundations & Concrete slab to ground level and suspended concrete slab to upper levels.

Floors:

Structure: Reinforced concrete column and beam.

Occupancy

External Walls: Aluminium framed glazed curtain wall.

Roof: Unable to inspect.

3.5 INTERIOR FINISHES

Entry Foyer: Ceramic tiling, plasterboard linings, feature lighting and a double height ceiling.

Market

Floors: Typically carpet, tile or polished concrete.

Walls: Mixture of glazed and plasterboard lined internal perimeter walls.

Ceilings: Suspended tile ceilings.

Amenities: Ceramic floor and wall tiles and plasterboard lined ceilings.

Valuation

3.6 SERVICES

Air Conditioning: Central air conditioning system providing air conditioning to the retail and office

tenancies.

Fire Prevention: The building is fitted with smoke detectors, fire hydrants, hose reels and handheld

extinguishers.

Disclaimers

Security/Access Proximity security system for controlled and after-hours access and a CCTV camera

Control: system.

Lifts: Two Kone 900kg 13 person lifts.

Appendices

© CBRE LIMITED | VALUATION REPORT | PAGE 19 of 5721-25 TEED STREET, NEWMARKET, AUCKLAND

31 JULY 2021

Introduction

3.7 CAPITAL EXPENDITURE

Capital Major assets require continual expenditure to maintain the aesthetic appeal,

Expenditure structural integrity, and hence their capital value. We have incorporated a specific

Adopted: capital expenditure allowance throughout the term of our cash flow analysis in

recognition of the requirement for an ongoing refurbishment program.

We have been provided with a Technical Due Diligence Report prepared by Cedar

Land

Tree Building Consultants dated 28 May 2021. This report includes a detailed 10

year capital expenditure schedule which has been adopted within our valuation.

In addition to the budgeted capital expenditure items provided, we have allowed:

◼ Capex escalation based on CPI.

◼ A minimum capital expenditure allowance equivalent to 0.50% of gross income

Improvements

per annum.

◼ An allowance of $200 psm on each office lease expiry and $100 psm on each

retail lease expiry as a general lessor make good allowance, weighted by the

adopted probability of renewal in that year.

Our adopted Capital Expenditure is summarised as follows:

Occupancy

Capital Expenditure Summary Years 1 to 3 Years 4 to 6 Years 7 to 11* Total

Client Advised Programmed General Capital Expenditure

Seismic Remedial Works $138,000 - - $138,000

Structure & Fabric $180,035 $137,146 $264,415 $581,596

Mechanical Services $385,372 $558,134 $479,920 $1,423,425

Electrical Services $244,752 $80,976 - $325,728

Fire Services $13,382 $21,049 $13,824 $48,254

Hydraulic Services $7,000 - - $7,000

Vertical Transport Services $214,919 - - $214,919

Market

Environmental - - - -

NZ Building Code $12,500 $21,335 - $33,835

Total Client Advised Capital Expenditure $1,195,959 $818,640 $758,159 $2,772,758

Refurbishment (on expiring leases) $332,130 $52,011 $435,020 $819,160

General Capital Expenditure Allowance - - $35,266 $35,266

Budgeted CAPEX (incl. Refurb Allowance) $1,195,959 $818,640 $758,159 $2,772,758

Total CAPEX (Adopted Overall) $1,528,089 $870,651 $1,228,445 $3,627,184

Total CAPEX $psm $379.44 $216.19 $305.04 $900.68

% of Adopted Value 5.60% 3.19% 4.50% 13.29%

Valuation

Note: Year 11 represents values included in terminal valuation

Disclaimers

Appendices

© CBRE LIMITED | VALUATION REPORT | PAGE 20 of 5721-25 TEED STREET, NEWMARKET, AUCKLAND

31 JULY 2021

Introduction

4 OCCUPANCY

4.1 TENANCY SCHEDULE

Area Car Base Rent Outgoings Lease Term Start Expiry Review Review

Level/Suite Tenant (sqm) Bays $pa $psm $pa $psm Term (yrs) Date Date Options Date Structure

Office Tenants

Level 5, CO05002 Kingston Property Limited 527.6 - 183,218 347 54,595 103 5.0 31-May-18 31-May-23 6 31-May-23 Expiry

Level 5, CO05001 SNB Finance Holdings Limited 290.9 - 103,393 355 30,106 103 5.2 1-Oct-18 30-Nov-23 4 1-Oct-21 Fixed Ann. 3%

Level 4, CO04001 Coffey Services (NZ) Limited 817.2 - 290,214 355 84,566 103 6.0 1-Jul-18 30-Jun-24 6 1-Jul-22 Fixed Ann. 3%

Level 3, CO03001 Banzpay Technology Operations Limited 168.9 - 54,879 325 17,474 103 10.5 1-Aug-11 31-Jan-22 - 31-Jan-22 Expiry

Level 3, CO03002 Banzpay Technology Operations Limited 650.0 - 211,250 325 67,265 103 10.5 1-Aug-11 31-Jan-22 - 31-Jan-22 Expiry

Level 2, CO02002 City Rail Link Limited 138.6 - 45,745 330 14,816 107 5.0 16-Dec-19 15-Dec-24 2 16-Dec-22 3 Yrly Mkt (Hard Ratchet)

Level 2, CO02003 City Rail Link Limited 306.4 - 101,201 330 32,746 107 5.0 16-Dec-19 15-Dec-24 2 16-Dec-22 3 Yrly Mkt (Hard Ratchet)

Land

Level 2, CO02001 Terabyte Interactive Limited 373.4 - 121,355 325 39,910 107 2.0 1-Oct-20 30-Sep-22 - 1-Oct-21 Expiry

Level 1, CO01001A Wisdom Management Limited 83.8 - 20,112 240 8,672 103 12.5 1-Aug-10 31-Jan-23 - 1-Aug-21 Expiry

Level 1, CO01001B Coffey Services (NZ) Limited 86.4 - 13,736 159 8,936 103 6.0 1-Jul-18 30-Jun-24 6 1-Jul-22 Fixed Ann. 3%

3,443.1 - 1,145,103 333 359,086 104

Retail Tenants

Ground, SS00001 Danny & Alma Chan 107.5 - 73,100 680 10,735 100 12.5 1-Jul-09 31-Dec-21 - 31-Dec-21 Expiry

Ground, SS00002 Darran Mangelsdorf & Erin O'Malley 128.7 - 77,220 600 12,852 100 19.3 1-Sep-02 31-Dec-21 - 31-Dec-21 Expiry

Ground, SS00003 Foresta D'Oro Limited 106.3 - 77,656 731 10,610 100 20.5 1-Nov-02 30-Apr-23 - 1-Nov-21 Ann. CPI

Ground, SS00004 Belloro Fine Jewellery Limited 135.8 - 84,713 624 13,561 100 8.6 1-Jun-13 31-Dec-21 - 31-Dec-21 Expiry

Ground, SS00005 Eyemax Limited 91.8 - 55,104 600 9,171 100 12.0 11-Sep-12 10-Sep-24 - 11-Sep-21 Expiry

570.1 - 367,793 645 56,929 100

Signage Tenants

Naming Rights, NR00001 Coffey Services (NZ) Limited - - 19,669 - - - 6.0 1-Jul-18 30-Jun-24 6 1-Jul-22 Fixed Ann. 3%

Media, MEDIA01 Val Morgan Cinema Advertising (NZ) Limited (VMO) - - - - - - 5.0 1-Sep-18 31-Aug-23 - 1-Sep-21 Expiry

Signage, SIGN001 Vacant - - - - - - - - - Vacant

- - 19,669 - - -

Improvements

Storage Tenants

Level 6, ST06001A Kingston Property Limited 14.0 - 2,756 197 - - 5.0 31-May-18 31-May-23 6 31-May-23 Expiry

Storage, ST06001 Vacant - - - - - - - - - Vacant

14.0 - 2,756 197 - -

Car Parking Tenants

Covered Kingston Property Limited - 7 20,925 57 - - 5.0 31-May-18 31-May-23 6 31-May-23 Expiry

Covered Coffey Services (NZ) Limited - 7 21,239 58 - - 6.0 1-Jul-18 30-Jun-24 6 1-Jul-22 Fixed Ann. 3%

Covered Banzpay Technology Operations Limited - 5 16,900 65 - - 10.5 1-Aug-11 31-Jan-22 - 31-Jan-22 Expiry

Covered Terabyte Interactive Limited - 3 10,140 65 - - 2.0 1-Oct-20 30-Sep-22 - 1-Oct-21 Expiry

Covered Danny & Alma Chan - 2 5,928 57 - - 12.5 1-Jul-09 31-Dec-21 - 31-Dec-21 Expiry

Covered Darran Mangelsdorf & Erin O'Malley - 1 3,120 60 - - 19.3 1-Sep-02 31-Dec-21 - 31-Dec-21 Expiry

Covered Belloro Fine Jewellery Limited - 2 5,741 55 - - 8.6 1-Jun-13 31-Dec-21 - 31-Dec-21 Expiry

Covered Vacant - 2 - - - - - - - Vacant

Uncovered Kingston Property Limited - 5 12,899 50 - - 5.0 31-May-18 31-May-23 6 31-May-23 Expiry

Uncovered Kingston Property Limited - 2 5,160 50 - - 5.0 31-May-18 31-May-23 6 31-May-23 Expiry

Uncovered Coffey Services (NZ) Limited - 8 24,273 58 - - 6.0 1-Jul-18 30-Jun-24 6 1-Jul-22 Fixed Ann. 3%

Uncovered Banzpay Technology Operations Limited - 6 18,720 60 - - 10.5 1-Aug-11 31-Jan-22 - 31-Jan-22 Expiry

Uncovered Terabyte Interactive Limited - 8 24,960 60 - - 2.0 1-Oct-20 30-Sep-22 - 1-Oct-21 Expiry

Uncovered Wisdom Management Limited - 3 7,020 45 - - 12.5 1-Aug-10 31-Jan-23 - 1-Aug-21 Expiry

Uncovered Vacant - - - - - - - - - Vacant

Occupancy

Stacked Kingston Property Limited - 3 6,020 39 - - 5.0 31-May-18 31-May-23 6 31-May-23 2 Yrly Fixed 5%

Stacked Terabyte Interactive Limited - 9 21,060 45 - - 2.0 1-Oct-20 30-Sep-22 - 1-Oct-21 Expiry

Stacked Foresta D'Oro Limited - 3 5,912 38 - - 20.5 1-Nov-02 30-Apr-23 - 1-Nov-21 Ann. CPI

Stacked Vacant - 6 - - - - - - - Vacant

- 82 210,018 49 - -

Total 4,027.2 82 1,745,340 433 416,015 103

4.2 LEASE COMMENTARY

Monthly The leases to Belloro Fine Jewellery Limited, Danny & Alma Chan (t/a Broadway

Tenancies: Blooms) and Darran Mangelsdorf & Erin O'Malley have expired albeit the tenants

remain in occupation. We have been advised that the tenants are currently holding

Market

over on a monthly basis. Our valuation adopts a 6 month lease term for these

monthly tenants.

Outstanding As part of its lease over Level 5, Kingston Property Limited had an option to

Incentives: surrender its lease on the fourth anniversary of the commencement date. The tenant

has not acted on this option and accordingly is entitled to a three month net office

Valuation

rent free period from 1 June 2021 to 30 August 2021. The present value of this

outstanding incentive is $29,964.

Outgoings The leases are structured on a net rental basis, whereby each lessee pays their

Recoveries: proportion of all outgoings expenses, with such proportion calculated by reference

to each tenancy’s lettable area as a percentage of the overall building’s lettable

area.

Disclaimers

Sundry Income: Storage and sundry income are summarised in the tenancy schedule.

Review Rent reviews are a mixture of annual fixed or CPI increases or 3 yearly to market.

Mechanisms:

Appendices

© CBRE LIMITED | VALUATION REPORT | PAGE 21 of 5721-25 TEED STREET, NEWMARKET, AUCKLAND

31 JULY 2021

Introduction

4.3 LEASE EXPIRY ANALYSIS

Year No. of Net Lettable Area Gross Passing Rent

1,400

Tenants sqm % $ pa %

1,200

Vacant - - - - -

1,000

Year 1 1 819 22.4% 386,489 20.6%

Year 2 4 1,105 30.2% 632,981 33.8% 800

Area (sqm)

Year 3 3 1,194 32.7% 596,132 31.8%

600

Year 4 2 537 14.7% 258,783 13.8%

Year 5 - - - - - 400

Land

Year 6 + - - - - -

200

Total 10 3,655 100.0% 1,874,385 100.0% -

WALT By Area 1.84 years By Income 1.74 years

WALT Comment: A relatively short WALT of 1.74 years.

Improvements

4.4 OUTGOINGS

Item Adopted

$pa $psm

Recoverable Outgoings

Occupancy

Municipal/Council Rates 128,520 32.02

Water and Sewerage Rates 14,940 3.72

Other Statutory Charges 3,860 0.96

Insurance Premiums 25,032 6.24

Air Conditioning/Ventilation 26,572 6.62

Common Area Cleaning 59,176 14.75

Electricity 52,044 12.97

Market

Fire Protection/Public Address 4,892 1.22

Lifts & Escalators 11,200 2.79

Pest Control 315 0.08

Repairs & Maintenance 36,550 9.11

Security/Access Control 11,124 2.77

Gardening/Landscaping 312 0.08

Administration/Management Fee 37,416 9.32 Valuation

Auto Doors (contract) 1,280 0.32

Cleaning (Level 2) 2,782 0.69

Total Statutory Charges 147,320 36.71

Total Operating Expenses 268,695 66.95

Total Outgoings 416,015 103.66

Source: Client outgoings schedule

Disclaimers

Outgoings The outgoings detailed above are within typical market parameters for a property

Comment: of this type, albeit towards the upper end of the range.

Appendices

© CBRE LIMITED | VALUATION REPORT | PAGE 22 of 5721-25 TEED STREET, NEWMARKET, AUCKLAND

31 JULY 2021

Introduction

4.5 NET INCOME SUMMARY

We summarise the property’s net income as follows:

INCOME SUMMARY Area Gross Passing Rent

(sqm) $pa $psm

Rental Income

Coffey Services (NZ) Limited 903.5 462,633 512.02

Land

Banzpay Technology Operations Limited 818.9 386,489 471.98

Kingston Property Limited 541.6 285,574 527.31

Terabyte Interactive Limited 373.4 217,425 582.29

City Rail Link Limited 445.0 194,508 437.11

Total Major Tenants 3,082 1,546,629 501.77

Improvements

Other Income

Other Office Income 375 162,283 433.08

Other Retail Income 570 424,722 745.01

Other Car Parking Income - 27,721 -

Total Other Income 945 614,726 650.63

GROSS INCOME 4,027 2,161,355 536.69

Less Expenses

Occupancy

Statutory Expenses (147,320)

Operating Expenses (268,695)

Total Outgoings Expenses (416,015)

NET INCOME 4,027 1,745,340 433.39

Market

Valuation

Disclaimers

Appendices

© CBRE LIMITED | VALUATION REPORT | PAGE 23 of 5721-25 TEED STREET, NEWMARKET, AUCKLAND

31 JULY 2021

Introduction

5 MARKET

5.1 AUCKLAND NON-CBD OFFICE MARKET COMMENTARY

ABSORPTION, SUPPLY & VACANCY

Land

Improvements

Occupancy

The impacts of COVID-19 on the office occupier market are now becoming apparent. Net absorption for

the Auckland non-CBD was negative 23,900 sqm, in the six months to December 2020 and vacancy

increased to 7.8%. Overall Auckland non-CBD vacancy increased 1.3% in 2020 and is now above the 5

Market

year of 7.4%. Grade A vacancy now sits at 6.3% (up from 5.5% in June 2020), Grade B vacancy is at 9.4%

(up from 6.7% in June 2020) and Grade C vacancy is at 7.7% (up from 6.6% in June 2020).

One of the major characteristics of the Auckland office market since the start of the pandemic has been the

rapid emergence of sublease space options. We have recorded approximately 37,000 sqm of potential

sublease options in the non-CBD market since April 2020 and most notably, approximately 48% of this

space is attributable to Grade A stock. It is important to note that these opportunities are not all immediately Valuation

available spaces. Rather, they often represent occupiers engaging with leasing agents about releasing some

of their spaces onto the sublease market without actively vacating the premises. For this reason, it is

challenging to assess the impact of sublease options on office vacancy.

We have seen approximately 9,250 sqm of new and refurbished office space come to market during the

second half of 2020 with the completion of 55 Corinthian Drive in Albany, a new build in Parnell by Mansons

TCLM and a fully refurbished 13 Blake Street in Ponsonby. We are expecting similar volumes of new supply

Disclaimers

through 2021 with approximately 14,300 sqm of office stock forecast to come to market including a 6,300

sqm refurbishment of 656 Great South Road in Ellerslie by Mansons TCLM.

New Zealand’s success at containing COVID-19 and facilitating a return towards normal levels of activity

across most industry sectors, coupled with significant fiscal and monetary stimulus has led to a more material

bounce back in the economy than previously forecast. Whilst we predict we are nearing a vacancy peak,

Appendices

© CBRE LIMITED | VALUATION REPORT | PAGE 24 of 5721-25 TEED STREET, NEWMARKET, AUCKLAND

31 JULY 2021

Introduction

our forecast is that the economic recovery is unlikely to drive a significant vacancy improvement during

2021-2024 as the expected supply pipeline will likely offset net demand.

RENTS

Auckland Non CBD Office Rents & Yields

310 10.0%

Land

290 9.5%

9.0%

270

8.5%

Rent ($/sqm/annum)

250

8.0%

Improvements

Yield

230

7.5%

210

7.0%

190

6.5%

170 6.0%

150 5.5%

Occupancy

Rent Yield

CBRE Research expanded the suburban basket of properties in Q4 2020 to allow for more detailed reporting

of the performance of non-CBD submarkets. Within the above chart, the overall rent figures for December

2020 reflect the average rents based on the extended basket of evidence while the figures discussed below

Market

reflect the performance of the true “market” change on the basis of the old basket of properties.

The second half of 2020 saw a continued trend of higher incentives being offered, contributing to a decline

in net effective rents in the 12 months to December 2020. Grade A rents have seen a significant contraction

of 4.4% and are currently at $331 psm. Secondary rents have experienced a lesser decline of 1.4% and are

at $249 psm.

Valuation

We expect that rental weakness will extend into 2021 based on weak demand for new completions and

some high quality sublease options undermining recovery. Scaled back supply and healthy economic growth

is forecast to result in reasonably strong rental growth for Grade A and B from 2022 onwards.

YIELDS

The investment market has shown remarkable resilience since the COVID-19 lockdowns. The non-CBD

Disclaimers

office market continues to be characterised by a weight of capital in search of good quality and well leased

properties. CBRE Research indicates that prime CBD office yields firmed by 25 basis points since June 2020

and are currently at 5.75%. Secondary yields have firmed 23 basis points since June 2020 (to 6.36%). On

an annual basis, given some COVID induced yield increases, non CBD office yields are on a par with

December 2019.

We forecast yields will continue to firm through to 2022.

Appendices

© CBRE LIMITED | VALUATION REPORT | PAGE 25 of 5721-25 TEED STREET, NEWMARKET, AUCKLAND

31 JULY 2021

Introduction

5.2 OFFICE RENTAL EVIDENCE

In this version of the Valuation Report, we only provide a summary of the rental evidence considered in order

to protect the privacy requirements of the Lessors and Lessees involved.

In establishing our opinion of market rental for the subject property, we have had regard to recent rental

transactions within the wider market. Net effective office rentals recently achieved within Newmarket and

Grafton show a relatively wide net effective range from $280 psm to $404 psm. Those rentals at the lower

Land

end of the range typically relate to inferior quality accommodation and those towards the upper end are

generally fitted out tenancies.

The most relevant benchmarks indicate a range of approximately $295 - $320 psm.

5.3 SUBJECT OFFICE RENTAL EVIDENCE

Improvements

Recent transactions within the subject property provide the most useful benchmarks for determining the

market rentals applicable as less subjective adjustment is required:

Terabyte Interactive Limited

Level 2: Most recently, Terabyte Interactive Limited agreed to a new 2 year lease over part-

Level 2. The net face rental was agreed at $325 psm over the 373 sqm premises.

Occupancy

After accounting for a lessor provided incentive of 2 months net rent free and a

$10,000 fit out contribution, the net effective rental analyses at $295 psm.

City Rail Link Limited

Level 2: In October 2019, City Rail Link Limited agreed to a new 5 year lease over 445 sqm

of office space on Level 2. The net face rental was agreed at $330 psm, reducing

to a net effective rental of $296 psm after allowing for a 5 month net rental

abatement.

Market

5.4 OFFICE RENTAL EVIDENCE COMMENTARY

109 Carlton Gore Road, Newmarket

Description: 109 Carlton Gore Road comprises a 4,528 sqm, 4 level office building plus

basement car parking situated in a high profile location on Carlton Gore Road. We Valuation

understand that the building was originally constructed in the early 2000’s by

Mansons TCLM, however has been progressively refurbished.

A new lease over Level 3 (1,122 sqm) commenced in April 2021. A new lease was

also agreed in September 2020 over 541 sqm of ground floor office

accommodation. The net rentals are in the vicinity of $300 psm.

Disclaimers

Comparability: Overall comparable.

Appendices

© CBRE LIMITED | VALUATION REPORT | PAGE 26 of 5721-25 TEED STREET, NEWMARKET, AUCKLAND

31 JULY 2021

Introduction

12 Kent Street, Newmarket

Description: 12 Kent Street comprises a 4 level office building featuring 2 ground floor tenancies,

level 1 car parking and 2 levels of office accommodation above. The building was

originally constructed during the 1980’s and presents to a reasonable standard.

In September 2019 a new 3 year lease was agreed over 269 sqm of Level 2. The

net effective rental is in the early $300’s psm. As part of the new lease, we are

Land

aware the premises were refurbished by the lessor, including new carpet tiles to

office areas, new ceiling tiles including LED lighting, and upgrades to the air

conditioning. Lobby and kitchenette areas feature polished concrete finishes and

exposed ceilings.

Comparability: Highly comparable Newmarket location.

Improvements

103 Carlton Gore Road, Newmarket

Description: 103 Carlton Gore Road comprises a 7 level commercial building constructed in

2000 and providing good quality A-Grade office accommodation. The building

features 2 levels of basement parking, ground level office, car parking and entry

Occupancy

foyer and 4 upper office levels.

A recent new lease and lease extension indicate net rentals in the vicinity of $300

psm.

Comparability: Overall comparable quality office accommodation.

Market

107 Carlton Gore Road, Newmarket

Description: 107 Carlton Gore Road is a modern commercial office building which has recently

undergone significant refurbishment works including new lighting, air conditioning

systems, seismic restraints, foyer refurbishments, end of trip facilities, new

bathrooms and lift replacements. The building provides A-Grade office

accommodation with a Green Star rating. Valuation

Housing New Zealand agreed a new lease over the entirety of the building

commencing in March 2020. The lease includes 2% annual increases and a 15

month rent free period.

Comparability: Superior in terms of quality. We are aware that the lease negotiations were

protracted, and we consider that the agreed rental was below market by

Disclaimers

commencement.

60 Khyber Pass Road, Grafton

Description: This is a seven level office building constructed in 1975 which was refurbished in

2010. The top two levels are subject to a new lease with the uppermost level being

Appendices

© CBRE LIMITED | VALUATION REPORT | PAGE 27 of 5721-25 TEED STREET, NEWMARKET, AUCKLAND

31 JULY 2021

Introduction

full refurbished, including new carpet tiles, exposed ceiling and services, LED

lighting, and upgraded HVAC system.

The property is positioned to the northern side of Khyber Pass Road, 150 metres

east of the intersection with Symonds Street and 150 metres west of Grafton Road.

The lease was agreed in April 2020 with a commencement date in April 2021.

Comparability: Superior in terms of quality, however inferior location.

Land

111 Carlton Gore Road, Newmarket

Description: At 111 Carlton Gore Road, we are aware of a sublease over part-Level 2 agreed

in June 2021. The net rental was agreed at the current passing rental. We have

Improvements

been advised that no incentives were provided, however existing fitout is in place.

Comparability: Comparable quality office accommodation.

5.5 RETAIL RENTAL EVIDENCE

Occupancy

In this version of the Valuation Report, we only provide a summary of the rental evidence considered in order

to protect the privacy requirements of the Lessors and Lessees involved.

In establishing our opinion of market rental for the retail tenancies within the subject property, we have had

regard to recent rental transactions within the wider market.

The evidence demonstrates a wide net effective rental range of $376 to $1,220 psm, depending on the

size, location, profile and quality of the premises. The most relevant benchmarks indicate a range of

Market

approximately $550 - $600 psm.

Over the past 10 years, Teed Street has emerged as a sought after retail location in Newmarket.

Notwithstanding, the expansion of the Westfield 277 shopping centre, along with the COVID-19 outbreak

have increased retail vacancy rates in parts of Newmarket and this has also affected market rents.

In August 2018, Eyemax Limited agreed to renew its lease over Shop 5. The rental remained unchanged at

Valuation

$600 psm over the 92 sqm tenancy.

5.6 CAR PARK RENTAL ANALYSIS

The most recent car park leasing transactions within the subject property indicate a rental range of between

$45 and $65 per week.

Covered car parks within comparable buildings have leased for between $45 and $70 per week, however

Disclaimers

the majority of the recent evidence is in the range of $50 - $65 per week.

Considering the most recent leasing transactions in the building, together with our knowledge of comparable

rentals achieved in the surrounding locality, we have adopted a market rental of $60 per week for the single

covered secure car parks, $50 per week for the open car parks and $40 per week for the triple stacked car

parks.

Appendices

© CBRE LIMITED | VALUATION REPORT | PAGE 28 of 57You can also read