Week ahead: Bananarama was right after all, but equities don't care

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

08 April 2020

Week ahead: Bananarama

was right after all, but

equities don’t care

Andreas Steno Larsen | Mikael Sarwe

- Some light at the end of the corona tunnel, but borders will be closed for

long

- US equities are almost on a par with June 2019. Does that make sense?

- Asian economies are re-closing – a clear risk in Europe/US over the summer

as well

If you want to receive a copy of Week ahead directly in your inbox, you can sign up via this

link.

Main Releases

Bananarama was right after all. We are facing a cruel summer and it’s getting increasingly visible (at least

to us) that we will have to live with substantial restrictions in the West at the very least until the middle of

Q3. Big festivals will be cancelled, historic sport events will be postponed; this is not a pleasant exercise. The

current clear-cut tendency to pre-cancel everything with substantial amounts of people gathered comes

despite a flattening of case curves across the Western world. Curfews work, the only thing we don’t know

now is how to get out of them again. So far, we haven’t seen a single feasible exit-plan being presented, and

who is able to tell how to prevent the case curve from re-accelerating once the economies are slowly re-

opened? The answer is currently no one.

Markets have taken the case-curve flattening as a conciliatory signal that the worst is now almost behind

us. March and April will be the worst months of this recession, while we will very slowly but surely rebound

e-markets.nordea.com/article/56816/week-ahead-bananarama-was-right-after-all-

but-equities-dont-care

from here. That is not an entirely unlikely scenario, the question is just how long it takes to return to just barely normal. Chart 1: Fatal cases are close to peaking in the United States – a fairly general phenomenon across the west In recent days authorities in eg Japan and Singapore have re-tightened the stance on Corona as a new case spike was seen. Singaporean authorities weren’t fully able to explain why, which means that case growth likely stems from people entering Singapore from the outside. This is a template of what other economies could be faced with, also in the West. Case growth may start accelerating swiftly again, if the economies are not opened very carefully only. And the Singaporean case also reveals that it is unlikely that freedom of movement will be normalised (to 2019 levels) across borders the next couple of quarters. Borders will be closed for long. 2020 is one to bury in the midden! Our best guess is that we won’t return to normal until during 2021. e-markets.nordea.com/article/56816/week-ahead-bananarama-was-right-after-all-but-equities-dont-care

Chart 2: Singaporean case growth re-spiked due to imported Corona cases We hence need to be on the watch around countries with a high sensitivity towards tourism. Tourism will not be allowed to return to normal anytime soon, if we are right on our corona assumptions. An Island-group like the Seychelles has 70% of GDP coming from tourism, but no one arrived last week. A true disaster for such a small society. In larger economies, Thailand, Greece and Portugal all have 20% of their respective GDP coming from tourism (Italy, Spain, Turkey, South Africa and Mexico are other highly tourism sensitive economies). None of this income will return anytime soon and these countries will in general be faced with ugly double deficits in the meanwhile. Is it possible to cope with both a fiscal deficit and worsening current account situations due to no tourism? This will test the Euro-area burden sharing again (since the Euro area in total holds a clear current account surplus), while countries like Thailand, Mexico and Turkey risks being faced with a material weakening outlook of their currencies due to the widening double deficits. A crisis in tourism-heavy EM countries needs to be avoided to turn the tide on the strong USD. We have highlighted the big downside risks to the USD, ONCE we are on the other side of the corona mess (FX weekly: USD needs to weaken or else a Plaza Accord 2.0 is in play). Getting closer to a firmer re-opening strategy is probably a prerequisite for starting the USD weakening trend. e-markets.nordea.com/article/56816/week-ahead-bananarama-was-right-after-all-but-equities-dont-care

Chart 3: Thailand’s current account to fall o a cli due to the sudden stop in tourism Tourism-heavy countries are of course not the only ones faced with renewed heavy upcoming debt burdens due to the corona crisis. The average bailout package (we dislike the word stimulus package, since you cannot stimulate a closed economy) is almost worth 20% of GDP in the five big economies. Japan joined the club with a 20% of GDP bailout program this week. No wonder the central banks will have to warm up the printers. From a risk/reward perspective such percentage of GDP numbers may even prove way to conservative, if we are right that it will take the most of 2020 to return to just barely normal. Can the market cope with such issuance? If our base case for the SOMA portfolio holds true (Global Macro: Policy responses if the corona recession deepens), the Fed will have bought more bonds than the US Treasury is about to issue during 2020 (the red line holds a conservative USD 2.5trn debt increase scenario). If you buy more than 100B’s a day (as the Fed has done in Treasuries + MBS), then USD 2.5trn is nothing. The only unknown is if inflation explodes on the other side of the crisis. NY Fed started writing about the 1940s yield- curve-control this week, which received widespread awareness. Does it matter a whole lot by now? Buying 100bn worth of bonds per day is close to YCC in practice, isn’t it? The case is not as clear cut in the Euro area, where the ECB will be tested. The politicians could be forced to discuss coronabonds unless the ECB pockets prove deep enough (Bond Watch: Overflow of bonds meets the ECB’s deep pockets) , but so far they are not even able to agree on a common communiqué in the Euro group. It’s either de facto burden sharing or else we are slowly looking at very adverse EUR scenarios. e-markets.nordea.com/article/56816/week-ahead-bananarama-was-right-after-all-but-equities-dont-care

Chart 4: Record issuance? No problem, we buy it all. Best regards from the Fed The cascade of central bank printed liquidity in USDs, EURs and JPYs etc is probably also the best reason to buy equities and likely also a big part of the reason why equities have been bought in recent weeks. S&P 500 is very close to the levels seen in June 2019. It’s not like it has been a smooth ride since, so do equities really belong up here despite a worse-than-2008 recession underway? Essentially you can’t print demand or profit during a politically decided recession and if everyone believed we were in a late cycle to start with, isn't it a high risk that companies don't re-hire people on the other side of the Corona-lockdown? When a lot of money is printed versus the overall size of the equity and debt market, it is usually a bull signal, but not until a while after. Maybe 2021 will be the most ketchupped market ever, but we likely need to go lower before. e-markets.nordea.com/article/56816/week-ahead-bananarama-was-right-after-all-but-equities-dont-care

Chart 5: If money printing accelerates versus bond/debt markets it usually means happy days after a while SPX forward P/Es remain elevated around 16.8, which are clearly above equity market bottoms in 2015, 2016 and 2018, when we had no recession and also far from the bottoms seen during the GFC and Eurodebt crisis periods. Isn’t that a little odd given that the current recession will most likely prove (much) deeper than the 2008-one? If P/Es eventually drop, it may be a decent sign for gold vs equities – in particular if our 6-12-month call of a weaker USD also materialises (Global: Once we are out of this mess, the USD could be hammered). e-markets.nordea.com/article/56816/week-ahead-bananarama-was-right-after-all-but-equities-dont-care

Chart 6: Forward P/Es are above 2015,2016 and 2018 bottoms, which seems odd given the current recession In Scandinavia, lay-os sadly, but naturally, continues as a result of the virus containment eorts and the global recession. 12,700 workers were given notice in Sweden last week (indicating that unemployment will rise swiftly in coming months. The spike in redundancy notices gives some sort of translation to personal consumption expenditures. It currently looks worse than both the 08/09 financial crisis and the 90s crisis in Sweden. SEK looks oddly strong given this. The big question is whether the Riksbank could be tempted to go back to negative in this scenario – at least there is a risk still, if the SEK stays relatively strong. e-markets.nordea.com/article/56816/week-ahead-bananarama-was-right-after-all-but-equities-dont-care

Chart 7: Redundancy notices hint of historically weak spending figures in Sweden What is most important in the week ahead? Writing this editorial in the morning before Maundy Thursday, we remain focused on the oil market ahead of the discussions between Saudi Arabia and Russia in the OPEC+ meetings. We consider it a decently conciliatory signal that Aramco postponed publishing the monthly price list until Thursday. It means that the two parties are at least talking to each other currently. This also leaves us with a slightly more constructive taste in our mouth surrounding NOK compared to a few weeks back. We doubt whether the US will be involved in a production cut. The US rig count will likely drop markedly over the coming 2-3 months, why it “may happen automatically” to use the words of Donald Trump. Levels around USD 40-45 per barrel is needed for the US shale production to be just barely profitable, meaning that the OPEC+ group can cut production (a lot) and still annoy the US shale producers another while. e-markets.nordea.com/article/56816/week-ahead-bananarama-was-right-after-all-but-equities-dont-care

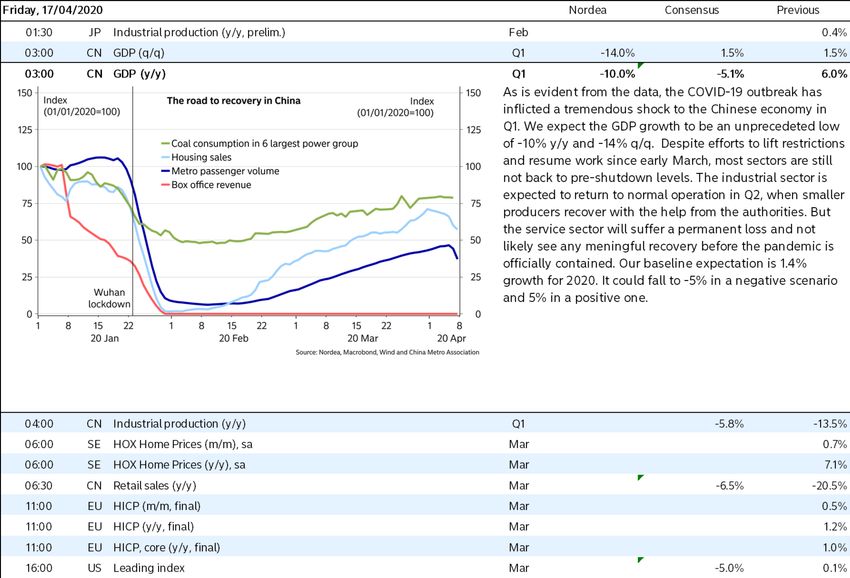

Chart 8: The number of rigs in operation will likely drop markedly in the coming months in the US Otherwise, the US retail sales figure will likely be the most important one to watch in an otherwise relatively quiet data week next week. Spend-trend data suggest that we might be in for the weakest ever retail sales growth. Key figures play a secondary role currently and communication from politicians on whether economies will be gradually re-opened after Easter as was communicated in both Austria, Norway and Denmark (Corona daily update) this week may prove more important than any key figures. China will already publish Q1 GDP figures next week (yes, you heard it right). We expect the GDP growth to be an unprecedented low of -10% y/y and -14% q/q – an early warning of what we will see across the western world (if not the globe). e-markets.nordea.com/article/56816/week-ahead-bananarama-was-right-after-all-but-equities-dont-care

Chart 9: The weakest ever retail sales report to be delivered in the US? Recent Research EM Trac Light March 2020 (7 Apr) Norway Macro: Three scenarios for the Norwegian economy (6 Apr) FX weekly: USD needs to weaken or else it is time for a new Plaza accord (5 Apr) Monday No major events as most markets are closed due to Easter Monday. Tuesday The first business day after Easter brings inflation numbers for Denmark and Finland. Later in the evening, Fed’s Evans (non-voter, dove) speaks in Pittsburgh. e-markets.nordea.com/article/56816/week-ahead-bananarama-was-right-after-all-but-equities-dont-care

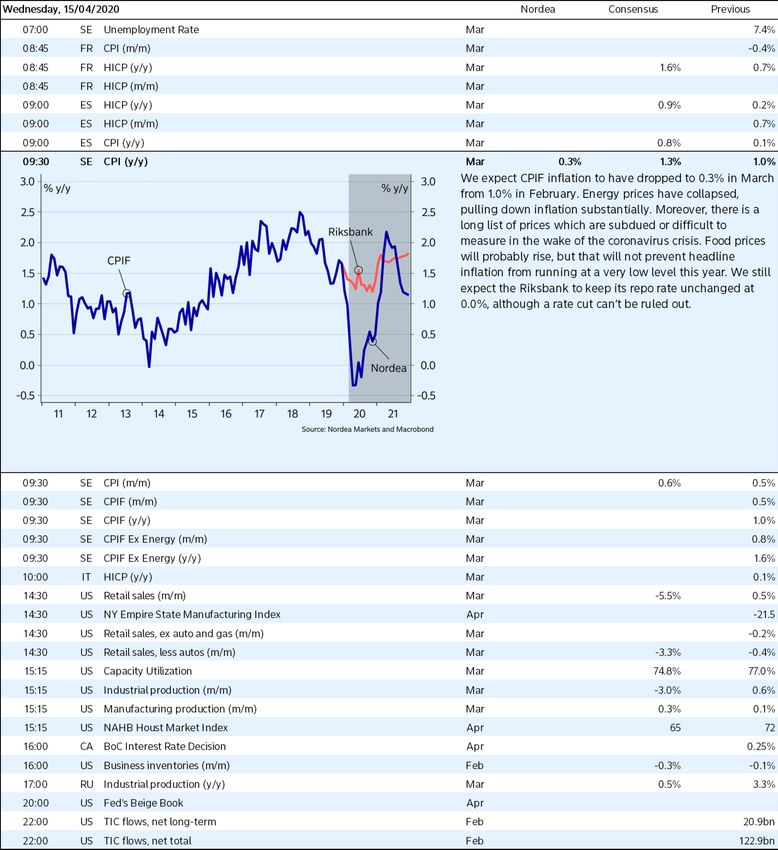

Wednesday On Wednesday, both inflation and SPES unemployment figures are released for Sweden. In the evening, we can look forward to a cocktail of data from the US, with the NY Fed manufacturing index, retail sales and industrial production as the most important events. After that, the Bank of Canada announces its rate decision. e-markets.nordea.com/article/56816/week-ahead-bananarama-was-right-after-all-but-equities-dont-care

Thursday The, for the moment, most anticipated weekly statistic, US initial jobless claims, is released on Thursday. At the same time, the Philly fed business index is released. In Europe, Swedish inflation expectations and euro zone industrial production figures are out in the morning. e-markets.nordea.com/article/56816/week-ahead-bananarama-was-right-after-all-but-equities-dont-care

Friday Friday is all about China. After the huge slump in industrial production last month, will Chinese figures rebound? China, which was first out in the corona crisis, also reveals its GDP figures for the first quarter. Retail sales figures for March will also provide a hunch whether domestic consumption is picking up or not. Andreas Steno Larsen Mikael Sarwe Global FX/FI Strategist Director, Head of Strategy Sweden andreas.steno.larsen@nordea.com mikael.sarwe@nordea.com +45 55 46 72 29 +46 8 614 99 09 e-markets.nordea.com/article/56816/week-ahead-bananarama-was-right-after-all-but-equities-dont-care

You can also read