What is a Credit Score and, how does it affect me?

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

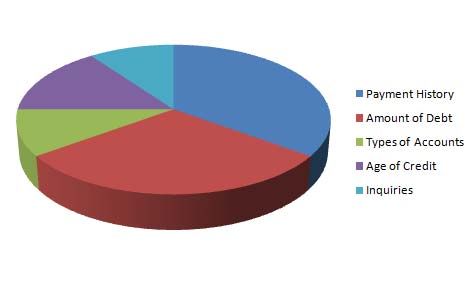

What is a Credit Score and, how does it affect me? Although they are closely related, credit reports and credit scores are two completely different things. Credit scores are typically three-digit numbers that represent the quality of your overall credit-worthiness. Many different types of credit scores exist, but the two most often used is the FICO score and the VantageScore. Five main factors affect your credit score. Those factors and the percentage weights they carry in determining your score are as follows: •Payment history (35%) •Amount of debt (30%) •Types of accounts (10%) •How long you’ve had credit (15%) •Your history of looking for credit (inquiries) (10%) You should try to learn about each of these factors and how you can change your financial behaviors to improve your credit score. Having a Good Credit Score has never been more Important than now Financial Education and Loan Services works with two nationally respected and well established credit repair and credit restoration companies to deliver our clients with a diverse array of services of which to choose to take the necessary steps to correct their credit reports, increase their credit scores, and put them back on the road leading to financial stability. Both companies are bonded and registered to provide credit repair and restoration services. Both are members of the Better Business Bureau with A ratings. The diverse services are completely legal with satisfaction guaranteed or your money back. Financial Education Services has more than 15 years of experience and their corporate headquarters is in Michigan. United Credit Education Services is a non-profit, has been in operation for 10 years, and their corporate office is also located in Michigan. Both companies were founded with the mission of assisting individuals and businesses to restore damaged credit so that they can recover and purchase their dream home, launch that successful business enterprise, or secure that job so that they can become productive members of our society and plan for their family’s future.

Both company’s have a mandate to provide quality services that will have productive,

long lasting, and quality results that will allow Financial Education and Loan Service

clients to overcome their current credit and financial challenges through financial and

budgeting classes or credit restoration or repair and thus leading to a more secure

financial future.

While one company uses time tested and confirmed “credit bureau dispute letter”

techniques, the other agency prefers a more innovative credit repair method with the

hands on assistance of credit professional who use legal technicalities to challenge

credit bureau reports -- also with proven results.

While you may be under extraordinary stress and pressure with bill collectors and

collection agencies hounding you, taking the necessary steps to repair your credit is the

first and most important step to take to help plan and move forward in taking control of

your financial crisis. And, with our financial planning and budgeting assistance that you

will qualify for with the credit repair membership, you will actually be several steps

ahead of conquering your problems and meeting your financial and credit challenges

head-on.

Indeed, today, credit is the one issue that you almost come into contact with on a

regular basis:

Have you recently applied for a credit card?

Tried to purchase a new home or to lease an apartment?

Been turned down for that small business loan because of your poor credit

score?

Are you getting calls from major credit cards daily?

All of this can be corrected and, without a large deposit upfront and little progress after

months of waiting for calls to be returned. This is our partners 15th year of operation

and they are members of the Better Business Bureau with an “A+” rating. Their

nationally respected company has assisted thousands with their credit challenges and

has never had a compliant filed against their company.They are so confident of the service, if you are not completely satisfied, we’ll refund all of your money. Moreover, Financial Education Services and United Credit Education Service have been recognized in the industry for their reasonable rates in terms of the excellent work product customers receive. Our Services is just what you need Based upon your situation and how you choose to work with us, the two companies can and have assisted our clients with the following issues on their credit reports: Slow Pays Liens Collections Student Loans Inquiries Charge-offs Bankruptcy Repossessions Foreclosures Judgments But the service far exceeds just credit repair and credit restoration. Indeed, it is important to us that you are not a repeat customer and that you continue on the road to credit and financial stability. The other services include: Improving your Credit Score Improving your chances for credit card approval in the future Clearing up misinformation with all three (3) major credit bureaus Removing any wrong charges on your report Removing wrong charge amounts on your report Removing outdated or incorrect personal information on your report All of the above items may seem minor; however, each can have a great affect on an individual’s overall credit report/score. Good Credit Allows for Great Things... Financial Education and Loan Services believe it is our responsibility to help our clients obtain the most coverage from existing consumer credit laws. Indeed, through these two companies that we contract with, we focus our attention and activity on keeping abreast of innovative techniques to help clients to compete and beat the odds against creditors and credit bureaus and then work with our clients to match them with the company that best matches their financial situation and credit repair needs. Our clients usually see results within the first 60 days and the companies must complete the work within 120 business days from the time they are paid.

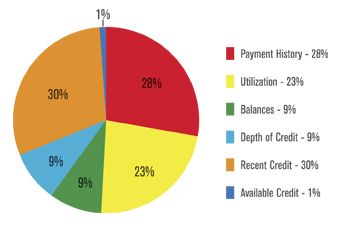

FICO: The Company The FICO score was developed by a company called Fair Isaac (known as FICO), which was started by engineer Bill Fair and mathematician Earl Isaac in 1959. One year after the company’s inception, it was hired to program and install a complete billing system for one of the first credit cards, the Carte Blanche. Since its inception by mathematician Earl Isaac in 1959, FICO has grown in influence and scope. Today, it boasts a client list that includes nine of the top-ten companies in the Fortune 500 and two-thirds of the top one hundred banks in the world. FICO™ (NYSE:FICO) is the leader in Decision Management, transforming business by making every decision count. We use predictive analytics to help businesses automate, improve and connect decisions across organizational silos and customer lifecycles. VantageScore Initially launched in 2006, VantageScore was developed to improve scoring consistency among the three major credit reporting organizations — Equifax, Experian and TransUnion. According to the VantageScore website, VantageScore 2.0, released in January of 2011, pulls from recent lending environments to be as accurate and predictive as possible for the credit lenders while providing clarity to consumers. VantageScore Model Unlike the FICO score, the VantageScore has six criteria that affect your credit score. The criteria percentages which determine your score are as follows: •Recent Credit (30%) – Measures the number of recently opened lines of credit and credit inquiries a consumer has on file. •Payment History (28%) – Scored as satisfactory, delinquent or derogatory, a history of late payments can negatively impact your credit scores. Creditors typically report those payments that are late by one day in with payments received after 59 days of a payment’s due date. •Utilization (23%) – Determines how much of a consumer’s available total credit is currently being used. Consumers who have “maxed out” their lines of credits may find it difficult to receive additional credit or have access to the best terms. •Balances (9%) – Assessing consumers’ current and past balances provide insight into their borrowing history and liquidity. •Depth of Credit (9%) – Evaluates the length of a consumer’s credit history. Having long-term credit relationships is important under this criterion; however, a diverse mix of credit such as loans and credit cards is advantageous. •Available Credit (1%) – Analyzes the balances of your current lines of credit. Keeping low balances at 30% of their total available credit can assist consumers.

VantageScore Grading Scale VantageScore model also provides consumers with a letter grade classification associated to the numeric score which ranges from 501 to 990. •“A” is the numeric equivalent to 900-990 •“B” is the numeric equivalent to 800-899 •“C” is the numeric equivalent to 700-799 •“D” is the numeric equivalent to 600-699 •“F” is the numeric equivalent to 599 and below According to Experian, research has revealed that the average credit score for consumers was 748 as of August of 2010.

You can also read