2016 Strategy Update New Platform to Deliver on Assets Modernization - London, May 2016 - Norilsk Nickel

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

2016 Strategy Update New Platform to Deliver on Assets Modernization London, May 2016

Disclaimer

The information contained herein has been prepared using information available to PJSC MMC Norilsk Nickel (“Norilsk

Nickel” or “NN”) at the time of preparation of the presentation. External or other factors may have impacted on the

business of Norilsk Nickel and the content of this presentation, since its preparation. In addition all relevant information

about Norilsk Nickel may not be included in this presentation. No representation or warranty, expressed or implied, is

made as to the accuracy, completeness or reliability of the information.

Any forward looking information herein has been prepared on the basis of a number of assumptions which may prove

to be incorrect. Forward looking statements, by the nature, involve risk and uncertainty and Norilsk Nickel cautions that

actual results may differ materially from those expressed or implied in such statements. Reference should be made to

the most recent Annual Report for a description of major risk factors. There may be other factors, both known and

unknown to Norilsk Nickel, which may have an impact on its performance. This presentation should not be relied upon

as a recommendation or forecast by Norilsk Nickel, which does not undertake an obligation to release any revision to

these statements.

Certain market share information and other statements in this presentation regarding the industry in which Norilsk

Nickel operates and the position of Norilsk Nickel relative to its competitors are based upon information made publicly

available by other metals and mining companies or obtained from trade and business organizations and associations.

Such information and statements have not been verified by any independent sources, and measures of the financial or

operating performance of Norilsk Nickel’s competitors used in evaluating comparative positions may have been

calculated in a different manner to the corresponding measures employed by Norilsk Nickel.

This presentation does not constitute or form part of any advertisement of securities, any offer or invitation to sell or

issue or any solicitation of any offer to purchase or subscribe for, any shares in Norilsk Nickel, nor shall it or any part of

it nor the fact of its presentation or distribution form the basis of, or be relied on in connection with, any contract or

investment decision.

1

Strategy Update 2016 – Agenda

Strategic vision | Andrey Bugrov

Operations Update | Sergey Dyachenko

Investment Governance and Portfolio Update | Sergey Dubovitskiy

Markets | Anton Berlin

Financial Strategy and Results | Sergey Malyshev

Corporate Governance | Andrey Bugrov

2

Strategic vision

Andrey BUGROV

Deputy Chairman of the Board,

Senior Vice-President

Strategic Goals for 2016–2018 –

“Three Years of Assets Modernization”

2016–2018

“Round 2”: Assets Modernization

2013–2015 Delivering on downstream reconfiguration /

Closure of 1942 Nickel Plant

“Round 1”: Building Efficiency Platform

Advancing on Environmental Protection /

ROIC/Tier I/capital discipline

strategy adopted

“One site” solution for the sulfur project

Redefining copper value chain

Refocusing on Tier I assets

Launch of the new asset – Bystrinskiy project

Successive “quick wins” – CapEx, working

capital, operating costs

Verification of the business case for

upstream growth optionality

Non-core and Non-Tier I disposals

4

Capital Discipline in Action –

Delivery on Norilsk Strategy “Round 1”

Despite Challenging Commodity Market … Norilsk Delivered Industry-leading Financial

Environment… Results While Maintaining Conservative Leverage

Bloomberg commodity index, bp Net Debt/EBITDA, 2015 EBITDA Margin, 2015

200

High: 174 1.0x 50%

180

160 1.1x 36%

Peer 1

140

Peer 2 1.8x 42%

120 -57%

100 Peer 3 2.7x 24%

80

Peer 4 3.0x 5%

Low: 74

60

2011 2012 2013 2014 2015 2016

Peer 5 3.6x 19%

Note: the peers group includes Rio Tinto, BHP Billiton, Vale, Glencore, Anglo American

5

Capital Discipline in Numbers –

Quick Wins of Norilsk Strategy “Round 1”

3

2 Release of Unproductive Capital

1 Capital Discipline Economic Impact of Initiatives

(US$ in bn)

Operational Efficiency Capital Expenditures

(US$ in bn) 2.0

Nickel Equivalent Unit Cash Cost 2.0 Guidance

(2012=100%)

1.7

1,1

1.3

1,0 0.8

-39%

0,9

0,8

NWC’13–15 Non-core Assets

0,7 Reduction (1) Sales

2013 2014 2015

0,6

0,5

2012 2013 2014 2015

Note: 1. Adjusted for external factors and one-off effects.

6

Industry-Leading Shareholder Returns

While the Global Metals & Mining Industry Lost Norilsk Nickel Delivered Positive and Industry

Almost US$1.0 trillion in Shareholder Value… Leading Total Shareholder Return, 2013–2016 YTD1

Market Capitalisation of MSCI World Metals & Mining Index

(US$ in trln)

Norilsk Nickel 11%

1,4

RTS M&M (18)%

1,2 High: 1.4

Peer 1 (27)%

1,0

Peer 2 (48)%

0,8

-71%

NN Commodity Basket (44)%

0,6

Peer 3 (50)%

0,4

Peer 4 (57)%

Low: 0.4

0,2

Peer 5 (62)%

0,0

2013 2014 2015 2016 (80)% (60)% (40)% (20)% 0% 20%

Sources: Bloomberg, Companies data; The peer group includes Rio Tinto, BHP Billiton, Vale, Glencore, Anglo American.

Note: 1. For Norilsk Nickel and peers total shareholder return calculated as the total percentage change in share price, inclusive of all dividends paid and announced (ex-div date)

in a period from April 2013 to April 2016. For indices and commodities – percentage change index from April 1, 2013 to April 1, 2016. 7

Strategic Focus for 2016–2018 – “Round 2”

Balanced, Modern and Environmentally Friendly Assets

Implemented (in execution) at the 1st stage of the reconfiguration program

Nickel Chain Copper Chain

Balanced Ni Comprehensive solution for New «copper configuration»–comprehensive solution

smelting capacity “SO2 problem” in Ni stream for “SO2 problem” in Cu stream (“One-site solution”)

Nadezhda Nadezhda Plant Copper Plant

smelting

capacity, Mtpa Smelting

Smelting

(Copper plant)

1.9

2.4 +

New facilities on

Nadezhda plant

Nickel plant shutdown in 2016 +

SO2 capturing project is under Converting

1 Upgrade of existing

2013 2016 way Sulphur production

facility at the

Modern and flexible Ni-refining capacity Copper plant

Anode

Ni refining capacities, Ktpa smelting

2 Shutdown of the

most polluting

facilities

Refining

145

Electrowinning

(Copper plant)

65

45

3

Sulphur production from low-sulphur gases to be

Tank- NNH Tank- concentrated on one site – Nadezhda Sulphur Project

house-2 house-1

8

Strategic Focus for 2016–2018: Verification of Upstream

Business Case and Strategic Options

Focus on Talnakh development

Verified mine plan - to maintain Norilsk Nickel metal

production level in the long-term

Talnakh ore production, Mt

+20–25%

17.5–18.5

Strategic options for future

15.5–16

14.8 partnerships

Chita project – building a new mining

center in Siberia / Far East region in

1 partnership with Chinese and other

potential investors

South Cluster:

potential development option –

investment case for ore production

2 growth up to 6Mtpa

partnerships to de-risk the project

2015 2020 2025 considered

9Responsible Corporate Citizen in Dialogue with Stakeholders

and Partnership with Government

Support of major Sustainable Employees Partnership with the

nation-wide sports development of partnership and Government

and cultural projects* territories motivation

Norilsk Airport Renewed 3-year Stable fiscal

(Alykel) collective environment

reconstruction bargaining

agreement Early cancellation of

Norilsk City export duties on nickel

infrastructure: ‘Our home’ and ‘My and copper

home’ housing

• Kindergartens programs Railroad to Bystrinsky

• Hospitals project

• Water park ‘Cumulative equity

Golden Mask • Shopping mall pension’ program Co-financing of Norilsk

Art Festival

• Churches Airport reconstruction

Relocation

Fiber-optic high- program for Norilsk Dialogue on support

speed internet citizens for environmental

to Norilsk program

Subsidies on the

Pasvik Natural basic food basket Strategic partnerships

Reserve in Norilsk with state-owned

banks

* Football Union of Russia, CSKA Basketball Club, Sochi 2014 Olympic Games, Krasnoyarsk 2019 Winter Universiade, Golden Mask

National Performance Arts Festival, Rosa Khutor Olympic Ski Resort 10Promotions in the Top Management Team

Sergey Dubovitskiy Vladimir Zhukov

Vice President Vice President

Head of Strategy Head of Investor Relations

▪ Joined Norilsk Nickel in 2013 as Head of Strategic ▪ Joined Norilsk Nickel as IR Director in 2013

Planning Department

▪ 15 years of experience in the metals and mining

▪ Spearheaded the development and updates of the industry

corporate strategy, supervised capital investment policy

▪ Prior experience: Metals and mining equity research

▪ Prior experience: 6 years in strategy function in the oil & analyst at HSBC, Lehman Brothers/Nomura, Alfa Bank

gas industry and McKinsey&Co

▪ Holds PhD from the University of Nottingham Business

▪ Holds MBA from INSEAD Business School School

11Operational Priorities

Next Round of Modernization &

Strategic Optionality

“On Time/On Budget” 3

Uncompromised Focus Project Delivery

on Health, Safety 2

and Environment

1

Second phase of modernization:

comprehensive solutions for

environmental issues:

First phase of modernization is

close to completion: ‒ cost-effective

Health & Safety culture ‒ Talnakh concentrator – upgraded ‒ based on new technologies/“no

change dogma” approach to solution

‒ Nadezhda smelter – upgraded

space definition

‒ Norilsk nickel smelter shutdown –

Strategic aspiration for Optionality for strategic

75% complete

“Clean Norilsk” – with partnerships – priority for

15 mining (brownfield extensions)

material progress achieved at scalable options with low risk and

projects commissioned relatively short lead time (South

both NN sites in 2016

Bystrinskiy project on track Cluster)

12Operations Update

Sergey DYACHENKO

First Vice-President

Chief Operating OfficerOperations Update

Focus on health, safety and environment –

world-class standards

Downstream reconfiguration is on track –

over 50% of projects commissioned

Major Upstream projects are on track

Potential development projects – value creation

options in case of market recovery

14Adherence to High Health & Safety Standards –

Progress Update

LTIFR Dynamics Health and Safety Culture Change

1*10-6 DuPont production safety culture index

-24%

0.80

2.30

0.61 2.10

0.46 1.40

2013 2014 2015 Mar 14 Mar 15 Mar 16

Ongoing implementation of Group safety standards in

key areas

Production safety training and assessment

program under way

Strategic Objectives:

1 Zero-fatality on production sites

2 Sustainable LTIFR improvement – two-year average went down by more than 20 %

15Progress in Implementation of

“Environmental Roadmap for New Norilsk”

Polar Division SO2

Project Impact Emissions Impact

(mtpa)

Talnakh Increased Sulphur content in

concentrator tailings -15%

upgrade & Enables moving smelting 1.8

expansion operations from Nickel to

Nadezhda plant 1.5-1.6

“Environmental

roadmap”

Nickel plant SO2 emissions in

(completed and agglomeration residential areas to

close to facility shutdown decrease by 170-190 ktpa

completion

projects)

Nickel plant SO2 emissions in

electric furnaces residential areas to

and anode decrease by 160-180 ktpa 2014 2017

smelters

shutdown Emissions in residential

areas cut by 30-35%

Emissions from facilities located outside of residential areas

Emissions from facilities located within the city of Norilsk area

16“One Site” Solution

New solution:

Previous solution:

Single project with a number of

“Two sites – two independent projects”

modernization initiatives

Nadezhda Copper Nadezhda Copper

plant plant plant plant

Furnaces Furnaces

Upgrade

! Existing ! Existing

Upgrade

Sulphur shop Sulphur shop

SO2 SO2

Converters Converters

New

Sulphur !

project #1 SO2 Sulphur SO2

project #1

Sulphur Sulphur

project #2 project #2

Electrowining Electrowining

Construction of new converters

based on new technology of

“weak” gases treatment

Cu cathodes Cu cathodes

Achievement of regulatory targets for emissions reduction

Maintenance of copper production capacity

Projected CAPEX saving (to be specified based on detailed

engineering)

17Nadezhda Sulphur Dioxide Capturing Project –

Progress to Date

May

2015

I

Tender process Stage 1 was completed with a decision to

November’15

separate detailed engineering and construction phases

Feasibility study completed and approved by the

December’15

government’s technical expertise («Glavgosexpertisa»)

II

January’16 Stage 2 tender initiation

February’16 Engineering survey on site is in progress

April’16 Construction site preparation is in progress

Detailed engineering contract awarded to one of the world

May’16

leaders in engineering and construction market – SNC Lavalin

May

2016

Dialogue with Russian Government on support measures for the Company’s environmental program launched

18Production Reconfiguration Program – Overview

Reconfiguration Program

Assets Location Mining Concentrating Smelting Refining

Cu cathodes

Copper Smelter Copper Refinery

Polar Division

Norilsk

Kola Division and Polar Division Concentrator

Upgrade

NN Harjavalta PGMs in

7 Mines

concentrate

Upgrade

Precious metals

Nadezhda Smelter refinery

Kola Division

Talnakh

Concentrator

Nickel Smelter Nickel Refinery

Finland

Ni cathodes

Kola Division & NNH

Upgrade

NN Harjavalta Chita Cu cathodes

Russia

PGMs in

Kola Nickel concentrate

Refinery

2 Mines Zapolyarny Nickel

Concentrator Smelter Ni cathodes

Ni salts

Harjavalta Refinery

Mining operations Cu conc.

Chita

Concentrators Au conc.

Bystrinsky Bystrinsky

Metallurgical plants O/P mine Concentrator Fe conc.

Overall cost saving and improved recovery

Reconfiguration SO2 emissions reduction by 15% resulting from concentrator upgrade and Nickel plant shutdown;

impact significant decrease of emissions in residential areas

Energy consumption reduction by Polar Division

19Reconfiguration Program – On-time Delivery in Progress

Reconfiguration Program

2014 2015 2016 >2017

1

Nickel plant shutdown 75% of smelting capacity is Complete plant

Rehabilitation

down shutdown

2

Talnakh concentrator

Phase 1

upgrade and capacity Phase 2 completed

completed

expansion

3

Smelter upgrade Nadezhda plant upgrade

Nadezhda smelter

(phase 1) completed; all Nickel smelting

upgrade

completed operations moved to Nadezhda

4

Re-launch of the Nickel Tankhouse-1

Kola downstream

upgrade Cobalt electrowinning facility launched

Concentrate briquetting facility launched

5

5

FS completed, regulatory approvals Construction works with gradual

Kola refining upgrade

received, contractor selected commissioning in 2017–2019

and expansion

201 Nickel Plant Decommissioning –

Two Main Facilities Shut Down in April

Reconfiguration Program

Current state Next steps

To date – 75% of smelting capacity is down All facilities to be shut down by

October 2016

Agglomeration Smelting

2016+ – closure and site rehabilitation

Agg. facilities Smelters Converters

212 Talnakh Concentrator Upgrade (Phase 2) –

Successfully Completed

Reconfiguration Program

Phase 2 – upgrade & Phase 3 (potential) –

Phase 1

capacity expansion to 10.2 mtpa capacity expansion to 16.0 mtpa

Optimized utilization Capacity increase up to 10.2 mtpa Next steps:

Increased of nickel recovery rate by 1 p.p. Concentrate volume decrease enables Nickel Update of project design as well as budget

plant shutdown & schedule

Recovery improvement: Confirmation of economic impact

‒ Impact of new technology (7.7 mtpa): Ni up to 1%

‒ Impact of re-directing volumes from Norilsk

concentrator to Talnakh (2.5 mtpa): Ni – 2 %, Cu –

2 %, PGM – up to 4 %

Completed in 2014 Commissioned in May, 2016

2223

3 “Single Stream” Smelting at Nadezhda Plant – “On

Track” Commissioning in March 2016

Reconfiguration Program

Smelting capacity, Mmtpa Moving of all Ni smelting operations to Nadezhda plant

2.4

1.9

2014 2016 Norilsk Nickel plant Nickel plant

concentrator

Ni conc.

Upgrade

Ni conc.

Talnakh

Nadezhda plant Kola refinery

concentrator

NNH

Concentrating Smelting Refining

Upgrade of smelting, concentrate drying and

filtering facilities

244 Kola Downstream Modernisation: Launch of New

Facilities and Added Synergy with Polar

Reconfiguration Program

Concentrate briquetting facility Launch of cobalt cathodes Re-launch of Ni

1 2 3

commissioned production Tankhouse-1

>30 ktpa +US$25m +45 ktpa

reduction EBITDA of nickel production

of SO2 emissions capacity

Reduction of emissions in the Additional profitability compared Additional capacity to balance

concentrate preparation stage to selling Co concentrate production during

(Zapolyarny production site) reconfiguration program

255 Chlorine Leaching Technology in Kola Downstream –

Targeting Further Efficiency Gains in 2018–2019

Reconfiguration Program

What has been done? Next steps Expected impact

Kola Ni refining capacity, ktpa

Tankhouse-1 Tankhouse-2

165 190

45 45

120 145

Before After

Project design completed Equipment delivery Increase of extraction rate by

Regulatory approvals received Construction works with staged >1.0 p.p.

EPC-contractor selected, commissioning of new chlorine Decrease in unit cost at refining

construction contract signed leaching technology stage by ~10%

Zinc-recovery circuit is Full capacity from 2019 Improvement of work-in-

under construction progress turnover

26Reconfiguration Program Impact

Capital Expenditures Expected Impact

(US$ in m) % Complete

(May 2016) Government Support through

the Cancellation of Ni and Cu

1,010–1,070 Export Duties

(Starting from August, 2014)

400–420

Cost Optimization

340–360 Average Yearly

EBITDA Impact

Starting from 2018

Improved Recovery Rates

US$250–300m

260–290

2013–2019

Talnakh conc. upgrade (Phase 2) Work-in-progress Metal Release

Nadezhda upgrade and Nickel Pl. shutdown

Kola Refinery Upgrade

27Priority Upstream Brownfield Projects

Project Highlight

Taimyrskiy Mine Oktyabrskiy Mine Komsomolskiy Mine2

Reserves covered

by projects 63 mt of ore 59 mt of ore

2.3% 1.0 % 1.5%

Ni1

3.5% 3.1% 24 mt of ore 1.8%

Total

Cu1

7.3 g/t 7.6 g/t 5.3 g/t

PGM1

Ore production ramp up to 3.9 mtpa by 2022 Maintain production at 5.0–5.2 mtpa until 2023 Maintain production at 3.8–4.1 mtpa until 2020

Next stage to be launched in 2016 Next stage to be launched in 2017 Next stage to be launched in 2016

Project description CapEx 2016–2018: US$201m CapEx 2016–2018: US$113m CapEx 2016–2018: US$140m

Completion: 52% Completion: 40% Completion: 47%

72.0 70.0

CapEx, US$m 45.0

(actual 2015)

7,600m of underground shafts and drifts 7,100m of underground shafts and drifts 4,700m of underground shafts and drifts

Completed

in 2015 Launch of 0.8 mtpa capacity Launch of 1.0 mtpa capacity Launch of 0.7 mtpa capacity

On time/

On budget / / /

Note: 1. Ore grade.

2. Komsomolskiy mine data doesn’t include Skalistiy mine (Skalistiy mine is illustrated on a separate slide).

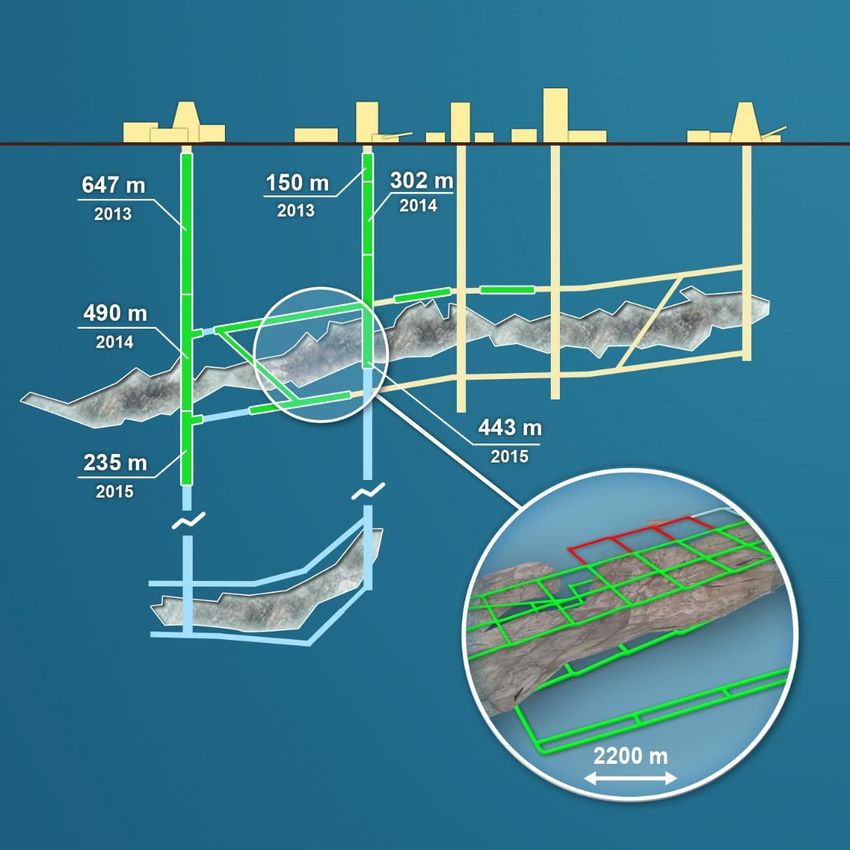

28Skalisty Mine: Project Development on Track

Project Highlight Project overview

Ventilation Shaft Main Shaft Auxiliary Shafts Ventilation Shaft Production capacity – 2.4 mtpa

Ore reserves – 58 mt

Estimated Project IRR > 30%

CapEx 2016–2018: ~ US$650m,

2015 CapEx ~ US$256m

Project timeline

Commissioned mining capacity – 500 ktpa in 2015

Next launch – 150 ktpa in 2016

Completion of ventilation shaft #10 in 2018

Completion of main shaft by 2019

Project update

Progress in 2015:

678m Shaft sinking Development

2,200m

Existing objects and shafts as at the beginning of 2015 Reconstruction works

Construction completed in 2013–2015 29

Total capital mine works planned in 2015–2025Bystrinsky Project – Pit Design Optimization Results

Indicators at 1Q16

Operational profile

macro conditions

Upstream (US$ in bn)

Pit optimization resulted in

significant reduction in

Reserves & Resources: 336 Mt

waste stripping CapEx’16–18

Cu – 0.64%

This in turn allowed to convert Fe – 20%

additional 40mt of ore resources Au – 0.8 g/t

into mineable reserves 0.9

Capacity: 10 Mtpa

Waste stripping Production profile

40,0 m m3

Ore production 10 9 10 EBITDA’20+

35,0 8

and processing, 8

30,0 Mt

6 0.4–0.5

25,0 4

2

20,0 2

0

15,0 2017 2018 2019 2020–2045

IRR

10,0

Annual production 2018–2020 (av.) 2021+

5,0

0,0

Cu (in concentrate) kt 45–50 70–75 >30%

2016 2017 2018 2019 2020 2021 2022

Au (in concentrate) koz 250–260 250–260

Previous design

Fe (magnetite kt 2000–2100 ~2900

Optimized design

concentrate)

Source: Norilsk Nickel.

30Bystrinsky Project: 45% Complete

Project Highlight

Railway link to the project site is near completion (227 km, 3.7 mtpa capacity). Project

financed in partnership with the Russian Government:

Trial operation launched in December 2015, full commissioning in 2016

An agreement reached with «FGC UES» regarding power line construction

and operation:

220kv power line construction is in progress. Commissioning is scheduled for 2Q17

Waste stripping at the open pits Ildikanskyi and Bystrinsky-2 is on schedule:

3m m3 of waste rock moved in 2015

Construction of main facilities/ordering of equipment on track:

Contractors have been hired for the construction works (concentrator, camp, etc.);

Ongoing construction of more than 20 facilities (ore supply, warehouses, etc.);

All concentrator equipment has been ordered (Outotec, FL Smidth)

31Bystrinsky Project: 45% Complete

Project Highlight

Primary Crusher Construction Crushed Ore Stockpile

Administration Building Mechanical Workshops

Source: Company data.

32Further Conversion of Norilsk Unique Resource Base into

Development Opportunities

Reserves and Resources – Polar Division (at 01/01/2016), mt

Comments

2,103 2,103

In addition to approved projects (15% of

15% 15% reserves) over 50% of reserves and

resources were subject to desktop studies

during 2015–2016

Long-term development scenarios were

identified – potential ore production increase

of 5–7 Mtpa by 2025–2030

56%

Potential development scenarios:

– Talnakh upstream projects

85%

– South Cluster development projects

– Talnakh concentrator upgrade (3rd stage)

Next stage – project design and schedule

29% development, commencing Investment

Committee procedures

2015 Strategy Current state

Reserves covered by approved projects Reserves for further review

Resources confirmed for development by desktop studies

33Long-term Mining Outlook for Polar Division

Upstream Development Scenarios, mtpa (ore)

South Cluster potential development Potential Talnakh concentrator

option: marginal returns – “zero”-NPV Expansion of concentrating

capacity after Talnakh-3: to upgrade (phase 3):

(@20%) at YTD spot

25 Mtpa Enables South Cluster

24 development

Polar Division concentrating capacity

after Talnakh-2: 19 Mtpa

20 Provides efficiency gains through

improved recoveries

16

Next steps:

12 Base production profile is stress

tested and demonstrates robust ‒ 2016–1H17:

profitability even in “gloomy” Update of project design and

8 market scenarios economic model

4 Detailed scheduling

‒ 2H17: Final investment decision

0

2015 2016 2017 2018 2019 2020 2021 2022 2023 2024 2025

South Cluster “development option”

Base case ore production profile: Talnakh + “sunset” South Cluster

34Screening for Potential Long-term Opportunities

East Siberia – “home” Far East – vast undeveloped

Screening approach I region for NN/still II resource potential and links to target

underexplored Asian market

Strategic criteria:

Regions where NN can build Potential

on it competitive edge – Copper

greenfields

Russian Federation

Preferred products

(metals) basket Brownfield

exploration

Potential to become Maslovskoe

Tier I asset New exploration

licenses

Risk mitigation options

(project financing,

partnerships, etc.)

Prospects around

Chita project

35Production Guidance

Production Guidance from Russian Feedstock

Ni/Cu – kt, PGM – t

(saleable metal)

PGM Cu Ni

95–100 The Company will maintain stable

99 95–100 production levels after 2016

88-93

Copper volumes growth due to

grade increase (and from 2018 –

420–440 due to launch of Bystrinskiy project)

353 342–352 370–380

224 206–212 215–220 215–220

2015 2016 2017 2018

One-off increase of work-in-progress due to Nickel plant

shutdown and moving refining operations to Kola division

36Investment Governance and

Portfolio Update

Sergey DUBOVITSKIY

Vice-President

Head of StrategyNorilsk’s Strategic Principles – Set Out in 2013

Progress

Most non-Tier 1 assets successfully

Focus on Tier I Assets

exited, Stage II Strategic review underway

Optimal Value Chain Unprecedented production reconfiguration

Footprint program on track

Quality of investment governance enhanced

Capital and Investment

Discipline Stay-in-business CapEx and working

capital optimized down to industry averages

Enhanced focus on Health & Safety

Social Responsibility Norilsk’s city area emissions cut

by 30–35%

38Strategic Context – Rise in Volatility Combined with

Weak Prices…

Lessons Learnt from Previous Downturns:

Number of Weeks When Ni Price Was Below

Ni Spot Prices -60%, Ni Price Volatility +80% Top Quartile of Cost Curve

100

25 000 35%

90 87

30%

20 000 80

25% 70

15 000 60

20%

50 47

15%

10 000 40 36

30

10% 30

22

5 000 20 16

5%

10

0 0% 0

Apr 2014 Oct 2014 Apr 2015 Oct 2015 Apr 2016 1982-1983 1985-1986 1993 1998 2013 2016YTD

Ni Price (US$/t) Ni Price Volatility Number of weeks with the price below upper cost quartile

(years with average annual price below upper cost quartile only)

Source: Bloomberg, Norilsk Nickel data;

Note: Rolling annual volatility.

39… Driven by Tectonic Shift in Chinese Economic Model

GDP and Investments Growth Rate in China is Structural Shift in Chinese Economy:

Slowing Down Growth in Services, Reduction in Industry

12% 60%

+8% +6%

10% 50%

+3% +3%

8% 40%

6% 30%

4% 20%

2% 10%

0%

2010

2011

2012

2013

2014

2015

2016E

2017E

2018E

2019E

2020E

1990 1995 2000 2005 2010 2015

China World Agriculture Industry&Processing Services

(Primary) (Secondary) (Tertiary)

Source: Bloomberg, Norilsk Nickel data, World Bank.

40… Impacting Negatively Metal Intensity of the

Chinese Growth

Fixed-Asset Investments Growth

The Lowest Level Since 2000 Ni Demand Growth Rate in China to Normalize

China Fixed Assets Investments (Exc. Rural Households) 25%

Cumulative YoY growth

60 20%

+13% +1%

50 15%

+2% +2%

40

10%

30

5%

20

10

(5)%

0

2010

2011

2012

2013

2014

2015

2016E

2017E

2018E

2019E

2020E

1999 2002 2005 2008 2011 2014

China ROW

+ХХ% Average growth rate in 2000–2015, 2016–2020E

Source: Bloomberg, Norilsk Nickel data, JP Morgan Research, NBS Research data, World Bank.

41…. Challenge the Validity of Many Investment Decisions in

the Industry

Global Miners’ CapEx + M&A: Volatile Capital Intensity Tends to Overact in Up and Down Turns

(US$ in bn)

3.0x Decline

104

74

71

53 52 54

Overreaction?

40 38

79

71

64

26

52 21

43 20

42

36 37

2008 2009 2010 2011 2012 2013 2014 2015 2016E 2017E 2018E

M&A Spending CapEx

Source: Bloomberg, Norilsk Nickel data; Total CapEx includes major diversified peers – BHP Billiton, Rio Tinto, Vale, Anglo American, Glencore and Norilsk Nickel.

42Norilsk Investment Strategy in the Industry Context

Global Miners Investments

(US$ in bn)

224

158

61

Robust (low-risk/high

profitability) projects portfolio

Norilsk Nickel CapEx +

(US$ in bn)

Enhanced focus on investment

6.6 discipline (improved investment

governance system

4.9

implemented in 2013–2015)

=

Consistent/solid investment

2010–2012 2013–2015 2016–2018

program through the cycle

Environmental program (1st Phase) & Chita

Source: Bloomberg, Norilsk Nickel data.

43Strategic Priorities – Focus on Investment Discipline

US$1.0bn of Capital Investment Savings in 2014–2015

Annual CapEx (Norilsk Nickel)

(US$ in bn)

2.7

Portfolio of highly profitable commercial

0.7

projects – stress tested under spot

2.0 Guidance / market expectation

macro parameters

2,7 0.3

0.7 1.7 Major commercial projects are delivered on

time/on budget (see details on the next slide)

1.0

1.3

1.1 1,3

2.0 0.7

1.0 Stay-in-business investments optimized to

0.6 0.6 industry benchmark levels

2012 2013 2014 2015

Stay-in-business Projects Commercial Projects

44Strategic Priorities – Focus on Investment Discipline

Delivery On Key Investment Projects

Schedule Deviation, % of Investments Budget Deviation, % of Investments

83% of Investments – On Schedule since 2013 >95% of investments – On Budget/with Savings

Accelerated 19%

4% 4%

13%

83%

96%

On Schedule Over 6m delay On Budget/with Savings Overspending More than 20%

Up to 6m Deviation Overspending Up to 20%

Rigorous investment governance procedures in action

Low-risk projects portfolio

FX impact tailwind

45Strategic Priorities – Focus on Investment Discipline

Stress-tested Profitability of 2013 Upstream Projects Portfolio

Portfolio of Upstream Projects – Approved by the Investment Committee in 2013

IRR as of 01.01.2013 Based on Original Macro IRR as of 01.01.2013 Based on Spot Macro

Parameters Parameters1

% %

Skalistaya 31% 27%

Mine Projects

Komsomolsky 40% 35%

Mine Projects

Taimyrsky 53%

61%

Mine Projects

Oktyabrsky 79%

Mine Projects 91%

20% 20%

Note: 1. Average 1Q16 macro parameters.

46Strategic Priorities – Focus on Investment Discipline

Robust Returns of Current Upstream Projects Portfolio

Returns (Point-forward) Sensitivity of Approved Upstream Projects Portfolio1 to Macro Scenarios

As of 01.01.2016

Ni price

18 000

IRR 59% At Average 1Q16 Macro Parameters

15 000 Other Actual (Short-term) Macro Data Points

IRR 60%

in 2Q15–1Q16

IRR 59%

12 000

IRR 60%

9 000

IRR 59%

IRR 53%

6 000

3 000

Area of Returns Below 20%

0

45 50 55 60 65 70 75 80 85 90

RUB/US$ FX Rate

Note: 1. Excluding projects with launch in 2016.

47Strategic Priorities – Focus on Investment Discipline

Stay-in-business CAPEX Optimisation

Production Assets Maintenance Energy Assets Maintenance

Implementation of risk assessment tools and Strategy review for Energy business – revised

long-term equipment replacement programs technological solutions

Approach

Implementation of Total Cost of Ownership approach

Enhanced tendering procedures/Review of payment terms

Example: capitalized maintenance dynamics Example: Energy business strategy review

Roubles –

Up to 20% of CapEx savings (excl. FX impact)

Examples zero inflation

while maintaining the same level of energy

supply security

US$ – (see next slide for more details)

>40%

2012-2013 2015-2016 optimization

average average

48Energy Business Strategy Review –

Optimization of CAPEX Program for 2016–2018 by 20 %

PV CAPEX in Energy Assets in 2016–2018

(US$ in m)

-19–20%

890 -220

+170 720

-120

550

Energy Business Revision of The Cost and Payment CapEx Program in Additional Projects “Nov 2015” Strategy

Strategy “2012” Projects Portfolio Schedule the Same Scope

Optimization

Review of Gas Midstream development strategy Additional projects identified due to

based on revised technological solution more rigorous planning process and

risk assessment

Investments synchronized with demand dynamics

492016 Investment Plan

US$0.5bn Optimization Vis-à-Vis the Guidance

Potential Tier-1 status confirmed

projects

Growth

Chita

500–550

Copper Project

De-risking strategy in implementation – partnership and

project financing

2.0 Guidance

Saving vis-à-vis

the Guidance

1.5 Downstream Nickel Plant shutdown, completion of Nadezhda Plant upgrade,

Base Investment Program

240–270 Reconfiguration Talnakh concentrator upgrade – Phase 2 launch

Brownfield extension projects to maintain current

Upstream Projects

330–370 production level

Other Efficiency improvement projects and initiatives (IT, automation,

140–160 Commercial Projects R&D, exploration, etc.)

250–290 Maintenance of Investments in Energy (gas, power) and Logistics (ports,

Infrastructure Assets fleet) assets

430–490 Maintenance of Investments in maintenance of production assets (equipment

Production Assets replacement, fulfilment of regulatory requirements, etc.)

2016 Plan

US$ in m

502016–2018 CAPEX Target – US$2bn p.a.

Cumulative CAPEX 2016–2018

(US$ in bn) Goals / Context Potential Co-funding

Growth Projects

~0.9 Chita Copper Project completion in 4Q2017

Partnership and project financing

Project and ramp-up

TBD Optional Projects

Investment decisions subject to market Partnership for South Cluster

Talnakh conc. (Ph.3) conditions and strategic review results considered

South Cluster

Environmental

Program

TBD Sulphur Dioxide First phase of “One-Site Sulphur

Government support discussed

Capturing Project Project”

+

4.4

Base Investment Program

0.5–0.6 Reconfiguration Full completion in 2019

1.2–1.4 Brownfield projects to maintain current

Upstream Projects

level of production

0.4–0.5 Other Commercial Process upgrades (IT infrastructure,

Projects automation), R&D, exploration, etc.

Mandatory CapEx – to ensure

1.9–2.3 Stay-in-business

undisrupted production processes and

Projects

meeting of all obligations

2016–2018

51Norilsk Asset Portfolio – Status Update

Norilsk Asset Portfolio

Maslovskoe Honeymoon Well

Potential/Greenfields

Core Assets

Strategic Review Cash Proceeds &

Foregone Liabilities

Non-Core:

Exited/In Closing

Bystrinsky

Polar :

South Cluster Nkomati (50%)(1) Closed:

(PGM/Tail Co)

Kola Arkhangelsk Port US$0.8bn

Tati Nickel (85%)

Operating

Polar :

Talnakh Cluster Nordavia Inter Rao (13,2%)

NNH In Closing:

Australian assets

Gas UpstreamCo Minority stakes in

power grid companies US$0.6bn(2)

Other non-core assets

Tier I Non-Tier I/Supporting Business

– The size of the bubble represents indicative estimate of the assets’ value compared to each other

Note: 1. Closure pending due to regulatory approvals

2. Including proceeds from the sale of 0.79% treasury shares (US$158m).

52Norilsk’s Legacy Assets – Status Update

Pro-Forma

Overview Revenue Core/tier 1? Status

(FY’15, US$ in bn)

PGM-rich

Asset perimeter

mines (open pit

defined,

& underground)

business case

with own ~0.4 under review

concentrating

facility located Strategic

within Polar options

Division considered

Polar “South (incl. potential

partnerships)

Cluster” Norilsk

Upstream Ongoing legal

cluster of 4 restructuring of

developed gas ~0.1 gas business

fields in close into Upstream

Norilsk gas proximity to the and

upstream Polar Division Downstream

companies

53Bystrinsky Project De-Risking Plan – Implemented

Realized De-Risking Initiatives:

Leveraging Public-Private Partnerships:

Railway link construction on track; to be Best-in-class mining

Project Status

completed by the end of the year greenfield project

Project Launch: Agreement with Federal Grid and VTB bank on

On track, planned construction and financing of grid infrastructure Tier-1 status in

for 4Q17 Norilsk portfolio

Bringing high-quality strategic partners:

Residual CAPEX: Norilsk reiterates its

~US$0.9bn Sale of a minority stake (13.33 %) to a strategic interest in

consortium of Chinese investors. Binding operating the project

agreement signed in 2015 and increasing its

footprint in the region

Securing project financing:

US$800m facility from Sberbank for 8 years

approved; first installment received in May 2016

54Adaptive Dividend Targets Providing Superior Shareholder

Returns and Balanced Financial Model

Uses Sources

New Dividend Targets Dependent on Highest quality Tier I mining assets – strong

with Improved Flexibility Net debt/EBITDA margins and cash generation even at cycle lows

Dividend Ample liquidity – US$6bn in cash and

Floor committed credit lines as of 1Q16

3.65

Project financing for Bystrinskiy Project

Environmental

(up to US$0.8bn)

Projects & Chita

Highly Profitable, Proceeds from the sale of non-core assets

Disciplined CapEx (executed/signed transactions)

Base CapEx

Programme

4.4

Further strategic optionality – ongoing strategic

review and non-core asset disposal programs,

potential pre-payment/streaming options

2016–2018

55Superior Shareholder Returns

Leading Mining Companies - Projected Dividend Yield for 2016 FY

Corresponding

to the minimum

dividend of

$1.3bn*

6.2%

4.1%

1.7%

0.1% 0.0% 0.0%

Norilsk Nickel Peer 1 Peer 2 Peer 3 Peer 4 Peer 5

Sources: Bloomberg, Companies data; The peer group includes Rio Tinto, BHP Billiton, Vale, Glencore, Anglo American.

Note: 1. Projected dividend yield (ex-date) based on 2016 FY (including interim and final dividends for 2016 FY) - minimal definition of the “floor”, to be increased by Nkomati deal

proceeds 56Key Takeaways

Norilsk in the industry context – consistent and solid investment program through the cycle

1

“All-in” CAPEX Target for 2016-2018 – US$ 2bn p.a.

2 (incl. “Base Investment Program”, Chita, 1st Phase of Environmental Program and potential options)

“Base investment program”:

3 ‒ US$ 4.4bn cumulatively for 2016-2018

‒ Portfolio of verified investments: optimized stay-in-business CAPEX levels and stress-tested

commercial projects

Portfolio Review: non-core assets disposal program well advanced; ongoing strategic review of the

4 “legacy” assets; de-risking plan for Bystrinskiy project implemented

Strategic financial model enhanced through adaptive dividend targets – balanced and providing

5 superior shareholder returns

55Markets

Anton BERLIN

Head of Strategic MarketingMacro-Driven Commodity Prices, Increased Volatility

Commodity Prices are Inversely Correlated with

Trade-Weighted US Dollar Commodity Price Volatility Increased in 2015-2016

180 35

Corr (LTM) = -0.94 Bloomberg Commodity Index

30

150

25

20

120

15

10

90

5

60 0

Apr 2013 Apr 2014 Apr 2015 Apr 2016 янв фев мар апр май июн июл авг сен окт ноя дек

USTWBROA Bloomberg Commodity Index 2014 2015 2016YTD

Source: Company data, Bloomberg, WoodMackenzie; As of 25th April 2016.

Note: USTWBROA Index is a broad trade-weighted USD index relative to other world currencies, as reported by the US Federal Reserve.

59Lowering of the Cost Curve Driven by Currencies and Oil

Price Depreciation

C1 Nickel Total Projects Cash Costs (ex. Norilsk)

Mining Currencies and Oil Price Decline vs. USD Down 23% Driven Mainly by Currencies & Oil

End of March 2016/ End of December 2014, US$/t

(23)%

(6)%

(9)%

(11)%

(13)%

12,430

(22)% 9,592

(26)%

Other

C1 2014

C1 2016

FX Rates

By-product

Oil Prices

Ni Price

(36)%

credits

Oil (WTI) BRL ZAR RUB CAD CLP AUD

Source: Company data, Bloomberg, WoodMackenzie.

Note: C1 cash cost 2016 updated as of April, 2016 60Speculative Pressure Running High on Demand Concerns

Speculative Pressure on Metals Running High: Ni Speculations at Record High Levels:

Change in Exchange Trading Positions LME Turnover Over 200x of Physical Market

250

1Q 2016/4Q 2014¹ Mt

178% 245

200

74

150

82%

142

50%

100

101

88

66 116 124

58 64

50

46 84

32 36 33 68

45 50

(43)% 41

(46)% 26 24 32

22

0

(78)% 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Ni Cu Pd Annual Ni trade volumes (LME Ni quality)

LME SHFE xx

Change in speculative shorts Change in net positions Annual Ni output (LME Ni quality)

Source: Company data.

Note: 1. NYMEX,LME data used for metal trading positions.

61Sharp Downward Adjustment of Consensus Forecasts

Analyst Consensus Ni Price Forecast: Sharp

Nickel LME Forward Curve: No Sense of Direction Downward Adjustment, Bullish Outlook Retained

US$/t US$/t

18 000 25 000

21,200

15 000

20 000

12 000

15 000

US$11,900/t

9 000

12,300

10 000

10,600

6 000

9,300

3 000 5 000

Spot 3M 15M 27M Spot 2015 2016 2017 2018

Jan 2015 Jun 2015 Apr 2016 Jan 2015 Jul 2015 Apr 2016 Sep 2015

Source: Company data, Bloomberg.

62Nickel Market: Little Guidance from Inventory Movements

Total Exchange Inventories Up 19% in 2015, LME Inventories: Relocation Between Asian

Relocation from LME to SHFE Warehouses Since 2H 2015

Kt Mt

600 25 000

456

441

431

413

500

20 000

192 166

165

400

177

15 000

1

300 53

2 59

10 000

200

5 000 203 209

100 178 166

0 0

Apr 2012 Apr 2013 Apr 2014 Apr 2015 Apr 2016 Dec 2014 Jun 2015 Dec 2015 Apr 2016

LME SHFE Ni price ($/t) Johor Singapore Taiwan Other

Source: Bloomberg, Company data;

63Ni-Intensive Stainless Steel in China – Healthy Demand

Variety of Chinese Sources: Ni-intensive Stainless … with Modest Growth Rates Continuing into 1Q

Steel Production Up 5–11% in 2015 2016

Mt YoY Kt

1 200

+5% +2% 1Q16: +3%

+1%

3,4 1 000

4,0 3,6

4,1

3,9 4,0

11% 800

14%

6% 9,8 10,9

9,3 10,6

9,2 9,7 600

400

6,9 7,8 7,2

6,6

5,4 5,0

200

2014 2015 2014 2015 2014 2015 Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

Source 1 Source 2 Source 3

2013 2014 2015 2016

200 series 300 series 400 series

ХХ% YoY

Source: Company data, Umetal, BGRIMM, TSSINFO

64China – Nickel Destocking in 2015 and Surge of Ni Imports

Implied Ni Units Destocking in China Excluding Strong Increase of Fe-Ni and Refined Ni Imports to

Build Up of SHFE Inventory (48 kt) in 2015 China in 2015 Extended into 1Q 2016

Ni Units, Kt Ni Units, Kt

500 Refined Ni +125% +342%

Fe-Ni +90% +15%

400

123

118 300

198

200

35

65

292

48 31

100

130

(10) 106

Incremental China Incremental Ni Change in Implied

net-import production usage in SHFE inventory destocking 0

(2015) losses stainless steel (2015) 2014 2015 мар.16

production

Refined Ni Fe-Ni

YoY%

Source: Company data, China customs statistics, Bloomberg, TSSINFO, UMETAL.

65Supply Rigidity – Investment Cycle

Major Ni Projects Ramp-up When Ni Market is High Reported Ni Stocks: After 3Y of Potential

Trending Downward Drawdowns Inventory Would Still Run High

US$ in bn Kt Kt

7,0 450

400 83 days 70

6,0

350 70 –100

5,0

300

70 –100

4,0 250

48 days

3,0 200 485

40 days

150

2,0 31 days

100 255

1,0 8 days

50

0,0 0

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016E

2017E

2018E

Ni 2016E 2017E 2018E Ni Al Zn Cu

exchange exchangeExchangeExchangeExchange

inventory inventory inventory inventory inventory

(2015) (2015) (2015) (2015)

Production ramp-up Project capex

Industry inertia (cycles) Constant inventory re-allocation

Barriers to exit/re-entry Unknown off-exchange stocks

Political considerations

Source: Bloomberg, Norilsk Nickel data

66Slow Response From Supply Side Helped by Lowering Cost

Curve

1Q 2016 Average Ni Cash Cost (C1) Down 23% vs. 4Q 2014

US$/t

30 000

25 000

20 000

15 000

10 000

5 000

0

(5 000)

(10 000)

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

1Q 2016 4Q 2014

Flattening of the Cost Curve

Decreasing marginal cost – reduced support for Ni price

Source: Bloomberg, Norilsk Nickel data, WoodMackenzie.

67Only a Quarter of Loss Making Capacity Runs a

Shut-Down Risk

At Spot Price, Over 70% of Global Nickel Production

is Making a Cash Loss … … but Only 17% Run a Shut-down Risk

US$/t

35 000

30 000 44%

30% 70%

25 000 5%

4%

20 000 17%

15 000 2016 consensus forecast of US$9,889/t Diversified miners

Average 1Q 2016 of US$8,526/t Government support

10 000 Ramp-up

Price sensitive production (under risk)

5 000

Ni Industry Has Entered a Major Restructuring Phase

0

Norilsk

Production cuts and shut-downs, kt

(5 000)

(10 000) 218

48

(15 000) 90

00 10%

10020% 20030% 30040%

40050%

50060%

60070% 70080%80090%900100% 1000 42

Diversified miner Government support

Ramp up Price sensitive production 139

Spot price

2015 2016 Assets for sale

China ex.China Assets for sale

Source: WoodMackenzie, Bloomberg.

68Pressure on Loss Making Ni Producers Rising Rapidly

Most of the Ni Industry Became EBITDA Negative

Only in 2H 2015 … … Pressure on CFs is Mounting in 1H 2016

EBITDA Ni Segments Ni price, US$/t Re-based to Nickel Price, US$/t Performance H-o-H

800 20 000 18 000

EBITDA

Expansion

600 16 000

15 000

EBITDA

400 14 000 contraction

200 10 000 12 000

0 10 000

5 000

(200) 8 000

(400) 0 6 000

1H 14 2H 14 1H 15 2H15 1H 2014 2H 2014 1H 2015 2H 2015 1Q 2016

EBITDA Ni segments Average Ni price Crude Oil (WTI) Mining Currencies Nickel price

Source: Bloomberg, Norilsk Nickel data

Note: Combined EBITDA includes results of Anglo American, Glencore, Sherritt, BHP Billiton and ERAMET nickel business units 69Nickel Feed for China: Philippines

Nickel Ore Imports from Philippines to China Were Mine Life of Nickel Ore Reserves with Ni Grade >1.5%

Down 26% in 2015 and Continue to Fall in 2016 in Philippines is Less than 3 Years

Mt Ni Units, Kt

10,0 1 400 3,0

2015 YoY: (26)% 2.6

1 200

2,5

8,0 1Q 2016 YoY: (25)%

1 000

2,0

6,0

800

1,5

600

4,0

1,0

400

2,0

0,5

200

0,0 0 0,0

Mar 2013 Sep 2013 Mar 2014 Sep 2014 Mar 2015 Sep 2015 Mar 2016 Ni Ore Ni Reserves Number

Number

Production in (>1.5%) by the of Years

of Years

Indonesia Philippines Other 2015 End of 2015

Source: Company data, China customs statistics, Bloomberg

70Nickel Feed for China: Indonesia

Only 3 Projects in Indonesia Have High Probability

of Completion Indonesia NPI Output Forecast for 2015-2017

Ni Units, Kt

Capacity, 250

Project Name Process Status Start Year Kt pa Ni

Indoferro BF Started 2013 18

200

PT Cahaya

BF Started

Modern Metal 2014 4

Industry 150

Tsingshan RKEF Started 2015 30

100

Tsingshan

RKEF High 2015 60-120

2–3 stages

50

9 projects RKEF, BF Medium 2016-2018 70

RKEF, BF, 0

8 projects Low 2016-2017 150 2014 2015E 2016E 2017E

Leach

Commissioned in 2014-2015 High probability

Medium probability Low probability

Source: Company data, China customs statistics, Bloomberg.

71Nickel Market Moving into Deficit in 2016

Moderate Supply Cuts Have Been Triggered … … while Global Consumption Holds …

Kt Incremental change in global supply Kt Incremental change in global demand

100 150 +2.0%

+1.3% +2.1%

100

50

40

50

40

0

20

0

2015 2016E 2017E

(50)

… and Growth Reliant on China

Kt

(100) +3.0%

+3.6%

?

?

(150)

2 000

1 960

1 920

(200)

2015 2016E 2017E

New projects growth Indonesian NPI ramp-up

2015

Americas

Americas

China

Europe

China

Europe

2016E

2017E

Other Asia

Other Asia

China NPI production losses Change at existing operations

Source: Company data.

72Palladium Market in Structural Deficit

Palladium ETFs Holdings Change:

Driven by the Macro Concerns Global Palladium Market: Structural Deficit

Koz YoY Kt Surplus/(Deficit), Koz

1 104

904

507 1 015

381 430

24

(24) (225) ETF

(435)

(655) outflow

(520)

(703)

(1,622)

2008

2009

2010

2011

2012

2013

2014

2015

2016YTD

2010

2011

2012

2013

2014

2015

2016E

2017E

Source: Norilsk Nickel data.

73Platinum Market – Deficit Holds

Platinum ETFs Holdings Change:

2015 Outflow Reversed in 2016 Global Platinum Market: Deficit Holds

Koz YoY Kt Surplus/(Deficit), Koz

902

583

384

276

228

183

102 247 233

72

(261)

(574) ETF

outflow

(975)

(278)

2008

2009

2010

2011

2012

2013

2014

2015

2016YTD

2010

2011

2012

2013

2014

2015

2016E

2017E

Source: Norilsk Nickel data.

74PGM Demand Drivers In Automotive Industry –

Tightening Environmental Regulations

Increasing Complexity of Emission Systems and

Powertrains Requires Higher PGM Loadings Tightening Emission Legislation

2015 2016 2017 2018 2019 2020 2021 2022 2023 2024 2025

Requires soot (particulate matter) filter

Gasoline

(Euro 6c) = more PGMs RDE Phase 2/95

Europe Eu 6b Eu 6c/RDE Phase 1 EU 7?

g/km CO2

North America Tier 2 Tier 3 Phase In: NMOG + Nox, PM Tightening

EPA

Requires advanced NOx control

Diesel North America LEV III Phase In: NMOG + Nox, PM

(SCR, LNT, SCR-LNT) LEV III Further Tightening

CARB Tightening

Japan JP09 JP18?

Smaller engines but frequent “cold start” requires more

Hybrid South Korea K-

PGMs loadings K-ULEV 70 K-SULEV?

(Gasoline) ULEV

South Korea

Eu 6b Eu 6c

(Diesel)

Direct Cooler exhaust gas, higher HC and soot requires more

injection PGMs in catalyst China (Beijing) BJ5 (EU 5) BJ6 BJ6 Phase 2

China

China 4 (EU 4) China 5 (EU 5) China 6

(Nationwide)

Gasoline

Lean Requires LNT = more PGMs

burn India BS4 (EU 4) BS6 (EU 6)

Indonesia EU 2 EU 4

Current ~30 g Pt per vehicle

Fuel Cell

Pd for hydrogen production and storage Thailand EU 4 EU 5 EU 6

Source: Norilsk Nickel analysis ,Johnson Matthey

75PGM Demand Drivers In Automotive Industry – Rising

Vehicle Production

Total Number of Vehicles Forecasted to Increase:

Gasoline Remains the Main Driver Global Light Vehicle Sales Expected to Grow in 2016

Mln Units Mln Units

120

+3%

100

80

60

91

40

89

20

0 2015

Japan/Korea /

China

Europe

North America

South America

2016E

ME+Africa

2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 2022 2023

South Asia

Total Diesel Total Gasoline Electric cars

Source: Norilsk Nickel analysis, IHS estimates

76Copper Market: China Driven Demand and Low Global

Inventories

China Remains the Main Driver for LME Copper Price Near Multi Year Lows while

Cu Consumption Growth Inventories Run Tight

Mt Mt US$/t

1 000 8 000

+4%

+3% 900

23,3 7 000

800

22,9

6 000

+2% 700

5 000

600

22,3

+1%

500 4 000

21,8 400

3 000

21,6

300

2 000

200

1 000

100

0 0

2014 2015 China Other 2016E China Other 2017E 2018E Apr-13 Oct-13 Apr-14 Oct-14 Apr-15 Oct-15 Apr-16

ХХ% YoY LME COMEX SHFE Cu price

Source: Company data, Macquaire Research, Wood Mackenzie.

77Copper Market Remains Balanced, Supply Disruptions -

Limited

Copper Supply Disruptions: Unfold in 2015 at 5% in

Line with Historical Average Copper Supply/Demand Balance

Kt Kt

1 400 10%

560

1 200 8%

8%

1 000

5% 6% 6% 190

800 170

6% 6% 6%

5% 5% 5% 10

600

4%

400 4%

2%

200

(330)

0 0%

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016E 2010 2011 2012 2013 2014 2015 2016E 2017E 2018E

Disruption Relative to original production target

Source: Company data, Macquaire Research, Wood Mackenzie

78Metal Markets Outlook

Loss making

Inventory Forecasted market Medium-term

Metal production

(days of consumption) balance fundamentals

(% of cost curve)

Kt

Deficit

? 30%

Nickel 80 70% (70)

(70-100)

Exchange Off-exchange 2016E 2017E

Profitable Loss-making

Koz Deficit

Palladium 87

(550)

(700)

46%

ETF 2016E 2017E

54%

Koz

Deficit

1

120 Profitable Loss-making

Platinum (150)

(130)

ETF

2016E 2017E

Kt Balanced

160

9 10% 50

Copper 90%

Exchange inventory 2016E 2017E

Profitable Loss-making

Source: Company data; Note: 1. South Africa and Zimbabwe

79Financial Strategy and Results

Sergey MALYSHEV

Senior Vice-President

Chief Financial OfficerFinancial Policy Framework…

Financial Policy Goals Recent Achievements

1

▪ Industry leading US$ unit cost

▪ Maintain industry leading profitability by containing operating

improvement in 2012–2015

Profitability costs while benefiting from rouble devaluation

▪ Industry leading EBITDA margin

2

▪ Debt maturity extended

▪ Maintaining investment grade credit ratings ▪ Funding sources diversified (Chinese

Prudent Balance ▪ Balanced debt structure in terms of currencies, maturities, credit line, Sberbank project

Sheet Management and financing sources financing etc.)

▪ Defensive liquidity management ▪ Above-average liquidity and

comfortable leverage ratios

3

Working Capital ▪ Following significant improvement in previous years,

▪ Working capital stable despite one-

off increases; some release

Management maintain achieved levels of net working capital

expected in 2016

4

Financial ▪ 2015 audited results published in

▪ Gradually speed up publication of IFRS financials mid-March (vs late March in

Disclosure previous years)

81… Resulting in Global Leadership on Margins and Balance

Sheet Strength

EBITDA margin, 2011–2015 Net debt/EBITDA, 2011–2015

50% Peer group range

Norilsk

Peer group range 1,0x

Norilsk

2011 2012 2013 2014 2015 2011 2012 2013 2014 2015

Company’s leading cost position and conservative financial policy allow Norilsk to maintain strong

standing through the commodity cycle

Source: Bloomberg, Company data.

Peer group includes BHP Billiton, Rio Tinto, Glencore, Vale, and Anglo American.

82Unit Costs Under Control Despite Some Headwinds

Profitability

Unit costs in US$, 2012 = 100%

Norilsk Peer 1 Peer 2 Peer 3 Peer 4

-39% -39% -33% -20% -17%

2012 2013 2014 2015 2012 2013 2014 2015 2012 2013 2014 2015 2012 2013 2014 2015 2012 2013 2014 2015

Despite some of the negative underlying trends (ore degradation, depletion of low-cost secondary

feedstock, catch-up inflation of consumables and salaries etc.) the company managed to

outperform peers

Tight cost controls were greatly helped by the US$ appreciation starting from 2H14

Peer group includes Rio Tinto, Glencore (industrial assets only), Vale, and Anglo American.

83EBITDA and FCF Strongly Supported by FX

Profitability

At the year-end US$/RUB rate of 72.9, 1% change in exchange rate translates into EBITDA change of US$ 22.0m, FCF change of

US$ 36.3m

US$m

60 exchange

rate as at

31.12.15

50 44.1

40.7

40 36.3

33.1

29.4

30 26.7

24.7 Free cash

22.0

20.0

17.8 flow

20

EBITDA

10

60.0 65.0 72.9 80.0 90.0

Share of Foreign Currency in Company CapEx Share of Foreign Currency in Company OPEX

Non- Non- Non-

Non-

RUB RUB

RUB 7% RUB

11% 22% 24%

24% 13%

5%

2014 2015 2014 7% 2015

76% 78% 31% 76%

89%

RUB RUB RUB RUB

Source: Company data.

84You can also read