2020 Covid-19 Payroll Webinar - Rob Cooper Presented by: AWS

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

2020 Covid-19

Payroll Webinar

Presented by:

Rob Cooper

Housekeeping

Housekeeping for Today …

• The slides used in today’s webinar are available on:

https://view.genial.ly/5ea801ad1241d90d8ac70bad

• This link is also shared in the Q&A section of the event. Q&A can be accessed by clicking on this icon at

the top right of your screen

• We will take a short 5-minute comfort break after each hour.

• Questions can be posted in the Q&A pane and will be dealt with after the breaks or at the end.

• The webinar recording will be available for 7 days after the event by clicking on the Teams Live event

link. You can listen to it as many times as you wish during this time frame.

4/29/2020 1The Plan for the Morning …

Welcome 09h00

Covid-19 Relief Measures

1. Compensation Fund Relief

2. PAYE Relief Measures

3. ETI Relief Measures

4. UIF Benefits

✓ Sessions (5 minute breaks every hour)

✓ Questions (answered during the breaks, and at the end)

✓ Informed by the PAGSA (Payroll Authors Group of South Africa)

Closing 11h30 …

© Rob Cooper 2Find me on facebook.com/robcooperza RobCooper@pagsa.org.za www.linkedin.com/in/robcooperza

Payroll Authors Group of SA

Your Company can become a Member

1. Payroll Authors Group of South Africa –

o Established in 1989 with SARS encouragement and support

o Represents the payroll industry with the statutory bodies

o Influences current and future legislation, as well as operational requirements

2. ‘Full’ members (Companies that supply computerised payroll systems)

o Indirectly represents all employers who use computerised payroll systems

3. Has opened Associate membership to Employers and Practitioners –

o R200 pm for up to 3 members per organisation to receive hot-off-the-press Newsflashes

o R300 pm extra for an email query service

o Newsflashes (65 issued in 2019)

o Channels of communication to statutory bodies

4. www.pagsa.org.za to register …

© Rob Cooper 4Introduction and Scope

► Today’s webinar focuses on Employment-related Covid-19 Relief measures

► Legislation that is important for today –

1. 15 March 2020: National State of Disaster [Gazette 43096]

2. 23 March 2020: Compensation Fund Notice [Gazette 43126]

3. 26 March 2020: C19 TERS Directive [Gazette 43161]

4. 8 April 2020: C19 TERS Directive Amendment [Gazette 43216]

5. 1 April 2020: Draft Disaster Management Tax Relief Bill

6. 1 April 2020: Draft Disaster Management Tax Relief Admin Bill

7. 23 April 2020: Draft Explanatory Notes on Further Covid-19 Tax Measures

► Scheduled for release –

1. 30 April 2020: Draft Amendment to the Disaster Management Tax Relief Bill

2. 30 April 2020: Draft Amendment to the Disaster Management Tax Relief Admin Bill

► We need: Further amendments to the (amended) Directive (clarity on TERS benefit post 30 April)

© Rob Cooper 5Covid-19 Compensation Fund Benefits

Compensation Fund Relief Measures

Conditions for approval of the Benefit

► Approval of a Covid-19 compensation claim by a previously “Covid-19 free” employee requires –

1. Occupationally-acquired i.e. arising out of the ‘course of employment’

2. Occupational exposure to a known source of Covid-19

3. In the workplace, or outside of the workplace i.e. business trips

4. Chronological sequence from work exposure to start of Covid-19 symptoms

5. Reliable diagnosis of Covid-19 as per the WHO guidelines

► “Home is simply not a workplace both in design and accreditation” (OHS requirements not met)

► Occupations are classified according to ‘Exposure’ risks -

1. Very High: Doctors, nurses, paramedics, laboratories, mortuaries

2. High: Workers in healthcare, medical transport, mortuaries

3. Medium: Frequent or close contact (within 2 meters)

4. Low: Little or no close contact (within 2 meter)

© Rob Cooper 7Compensation Fund Relief Measures

Benefits and Claims Procedures

Type of Benefit If Approved by the Fund

1. Temporary disablement: Fund will pay (up to 30 days)

2. Permanent disablement: Fund will assess each case on merit

3. Death benefits: Fund will pay for burial and pensions

4. Confirmed illness cases: Fund will pay from diagnosis (up to 30 days)

5. Unconfirmed illness cases: Employer or UIF must pay (i.e. self isolation cases)

► Compensation claims:

o Online: CompEasy www.labour.gov.za

o Manual: Email to covid19claims@labour.gov.za

► Use code U07.1

© Rob Cooper 8Covid-19 PAYE Relief Measures saving jobs and

PAYE Relief Measures

Introduction

► PAYE relief measures –

1. Are only for tax compliant businesses

2. The relief assists employers, thereby saving jobs and assisting employees

► Published on 1 April 2020: Draft amendment Bills –

1. Disaster Management Tax Relief Bill

2. Disaster Management Tax Relief Administration Bill

► Legislation -

1. Published on 23 April 2020: Draft Explanatory Notes on Further Covid-19 Tax Measures

2. Scheduled for 30 April 2020: Two amended draft Disaster Management Tax Relief Bills

► PAYE relief measures that impact on employers and payrolls are –

1. Donations to the Solidarity Fund and to Covid-19 Trusts / Funds

2. Deferral of the employer’s monthly PAYE liability

3. Skills Development payment holiday

© Rob Cooper 10PAYE Relief Measures

Donations to the Solidarity Fund

► The Solidarity Fund is registered as a PBO and is a section 18A approved Fund

► Donations to all Funds (supported by a S18A receipt) qualify for a deduction in determining -

1. An individual’s taxable income for income tax calculation purposes

2. An employee’s ‘balance of remuneration’ for PAYE calculation purposes

► Current deduction thresholds for donations to all S18A approved Funds –

1. Income Tax:10 per cent of the taxpayer’s taxable income

2. PAYE: 5 per cent of the ‘balance of remuneration’

► Proposed deduction thresholds for donations to the Solidarity Fund (only) –

1. Income Tax: Additional 10% of taxable income i.e. maximum of 20% if total donation is to Solidarity

2. PAYE: From 1 April 2020: 33.33% (for 3 months) or 16.66% (for 6 months) of ‘balance of remuneration’

► Proposed (i.e. not yet final) Tax certificate code: 4055 (Covid-19 Donation)

© Rob Cooper 11PAYE Relief Measures

Donations to Covid-19 Relief Funds

► Covid-19 Disaster Relief Funds –

o Section 18A approval for four months from 1 April 2020 until 31 July 2020

o Donations to a Covid-19 Disaster Relief Fund will qualify for tax deduction in the hands of the donor

► My understanding of the proposed process -

1. The Covid-19 Fund approves a loan to an SMME at preferential interest rates and repayment terms

2. The loan is not paid to the SMME - weekly allowances are paid directly to the employees of that SMME

3. The allowance is ‘not remuneration’ therefore not subject to PAYE, SDL and UIF but is subject to income tax

4. The obligation to repay the loan remains with the SMME

► Payroll administration is likely to be -

1. The Covid-19 Fund must set up its own payroll and data capture the details of the SMME’s employees

2. Pay the weekly allowances “directly” to these employees (no PAYE, SDL or UIF)

3. Produce tax certificates with the appropriate tax certificate code (possibly code 3724), and

4. Notify the SMME of the total amount paid to the employees as being a preferential loan made to the SMME

© Rob Cooper 12PAYE Relief Measures

Deferral of Employers PAYE liability

► Deferral of the employers EMP201 PAYE payment to SARS –

1. Is limited to ‘Qualifying taxpayers’

2. A deferral of 35% (was 20%) of PAYE only (not of SDL or UIF)

3. Four months starting 1 April 2020 (for 7 May EMP201) and ending 31 July (7 Aug EMP201)

► ‘Qualifying taxpayer’ is a company, trust, partnership or individual that -

1. Is tax compliant (all tax returns have been submitted, and no outstanding tax debt)

2. Has gross income less than R100 million [Note: specified passive income types not included]

► Repayment of the deferred PAYE liability in -

o Six equal monthly instalments

o Starting Aug 2020 i.e. EMP201 of 7 Sep 2020

o Ending Jan 2021 i.e. EMP201 of 7 Feb 2021

► Penalties and interest -

o Not raised on deferred PAYE (if correctly calculated), but raised on repayment defaults

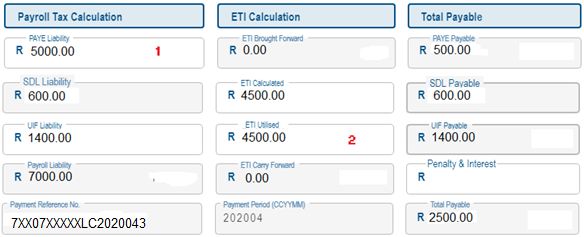

© Rob Cooper 13PAYE Relief Measures Deferral of Employers PAYE liability … continued Principle of Deferral of PAYE liability based on 20% (now 35%) Repayment of Deferred Total of R120 000 © Rob Cooper 14

PAYE Relief Measures

Deferral of Employers PAYE liability … continued

► Calculation

o PAYE liability (1 above) 5 000,00 [20% deferral = R1 000,00]

o Less: ETI utilised (2 above) -4 500,00

o PAYE due after ETI 500,00

o Less: 20% deferral -500,00 [to be repaid over 6 months]

o PAYE due after ETI and deferral 0,00

o Plus: SDL liability 600,00

o Plus: UIF liability 1 400,00

o Payment due to SARS 2 000,00

► Refer to PAGSA Newsflash 2020-39 for more details

© Rob Cooper 15SDL Relief Measure

Skills Development Levy Payment Holiday

► Every employer –

o Registered with SARS for PAYE

o With total annual remuneration for the next 12 months that exceeds R500 000

o Must register for Skills Development

o Make monthly SDL contributions of 1% of the ‘balance of remuneration’

► Proposed by the Draft Explanatory Notes on Further Covid-19 Tax Measures (23 April 2020) –

o A four-month ‘payment holiday’ for skills development levy contributions

o From 1 May 2020 and ending on 31 August 2020

► During the four-month SDL payment holiday period -

o Computerised payroll suppliers should change their systems to calculate the SDL contribution at 0%

o SARS will ‘freeze’ the EMP201 SDL field to prevent inadvertent errors by non-computerised employers

► The UIF contribution holiday is now off the table

© Rob Cooper 16Covid-19 ETI Relief Measures

Employment Tax Incentive

Principles of ETI

► Purpose of the Employment Tax Incentive Act -

o To share costs with Government by reducing the PAYE liability on the EMP201

o ‘Eligible employers’ are incentivised to hire youngsters that are ‘Qualifying employees’

► ‘Eligible employers’ –

o Are (broadly) private sector employers that are registered for PAYE

► ‘Qualifying employees’ are those that satisfy -

1. Six qualifying tests: Starting date; exclusions x 2; identity; minimum wage; remuneration less than R6,500

2. Seventh qualifying test: The ‘age test’ (employee must be 18 to 29 years of age)

► Up to 31 March 2020: ‘Eligible employers’ benefit from ETI for 24 ‘qualifying’ months to a –

1. Maximum of R1,000 pm for the 1st twelve ‘qualifying’ months

2. Maximum of R 500 pm for the 2nd twelve ‘qualifying’ months

► The above rules will continue after four months from 1 April 2020 i.e. from 1 August 2020

© Rob Cooper 18Employment Tax Incentive

Expansion of the ‘Age test’

► ‘Qualifying employees’ from 1 April 2020 to 31 July 2020 are those that satisfy –

1. The six qualifying tests

2. The seventh expanded ‘age test’

► The expanded age test now has two new components -

1. 18 to 29 years old (within the 24 qualifying’ months) [Unchanged]

2. 18 to 29 years old (outside of the 24 qualifying’ months) [New]

3. 30 to 65 years old [New]

► The expanded age test applies only –

1. From 1 April 2020 to 31 July 2020, and

2. To those eligible employers who were registered for PAYE on or before 1 March 2020

► Legislation –

1. Draft ‘Explanatory Notes on Further Covid-19 Tax Measures’ (published on 23 April 2020)

2. Scheduled for 30 April 2020: Two amended draft Disaster Management Tax Relief Bills for the detail

© Rob Cooper 19Employment Tax Incentive

Increase to the value of the ETI

INCREASE TO THE BASE VALUE AND ADJUSTMENTS TO THE FORMULAE

1. Draft Disaster Management Tax Relief Bill (published on and effective from, 1 April 2020)

2. Draft Explanatory Notes on Further Covid-19 Tax Measures (published on 23 April 2020)

► Note:

1. The increased ETI values in red apply from 1 April 2020 to 30 April 2020

2. Add R250 to the ETI values in red from 1 May 2020 until 31 July 2020 (but this is under discussion)

3. Refer to PAGSA Newsflash 2020-41 (Further Tax Relief Measures - Draft EN) for more details

© Rob Cooper 20Employment Tax Incentive

ETI Reimbursements paid Monthly

► ETI Reimbursements -

o Reimburses tax compliant employers bi-annually when the ETI exceeds monthly PAYE

o Amendment proposed to assist the employer’s cash flow for four months from 1 April 2020 to 31 July 2020

► Proposed amendment to the ETI reimbursement principle –

1. Up to 31 March 2020: Bi-annual reimbursements based on the 6-monthly tax certificate cycle

2. From 1 April 2020: Monthly reimbursements

3. From 1 August 2020: Bi-annual reimbursements are reinstated …

► Reimbursement value is the ‘ETI Carry Forward’ value on the EMP201

► Tax non-compliant employers will not be reimbursed

© Rob Cooper 21Covid-19 UIF Benefits

UIF Benefit Relief Measures

BCEA Principles

Leave and UIF Benefits

► Employees can be absent from work –

1. Without permission [Dodgy employees, Deserters, AWOL, etc.]

2. With permission [BCEA leave provisions]

3. Layoff’s [Temporary or Permanent for various reasons]

► The BCEA has been ‘locked down’ … No changes at all to leave requirements

Leave Paid Covid-19

BCEA LEAVE TYPE

By Impact?

1 Annual Employer

2 Sick UIF Yes

3 Maternity UIF

4 Family Responsibility Leave Employer

5 Parental UIF

6 Adoption UIF

7 Commissioning UIF

► Employer can ‘force’ Annual leave to be taken in the absence of agreement [BCEA Section 20(10)]

© Rob Cooper 23UIF Benefit Relief Measures

Temporary Employer/Employee Relief System (TERS)

Legislation Foundation

Directive Amendment to Directive of 26 March 2020

[Gazette No. 43161 published 26 March 2020] [Gazette No. 43216 published 8 April 2020]

1.1.7 "temporary lay -off" means a reduction in work

1.1.6 "temporary lay -off" means a temporary closure of

following a temporary closure of business operations,

business operations due to Covid-19 pandemic for the

whether total or partial, due to Covid-19 pandemic for the

period of the National Disaster.

period of the National Disaster.

3.1 Should an employer as a direct result of Covid-19 3.1 Should an employer as a result of the Covid-19 pandemic

pandemic close its operations for a 3 (three) months or close its operations, or a part of its operations, for a 3 (three)

lesser period and suffer financial distress, the company shall months or lesser period affected employees shall qualify for a

qualify for a Covid-19 Temporary Relief Benefit. Covid-19 benefit.

3.2 The benefit shall be de-linked from the UIF's normal

benefits and therefore the normal rule that for every 4

(four) days worked, the employee accumulates a one day

credit and the maximum credit days payable is 365 for every

4 (four) years will not apply.

© Rob Cooper 24UIF Benefit Relief Measures

Temporary Employer/Employee Relief System (TERS)

Legislation Foundation … continued

Directive Amendment to Directive of 26 March 2020

[Gazette No. 43161 published 26 March 2020] [Gazette No. 43216 published 8 April 2020]

3.3 The benefits will only pay for the cost of salary for the

employees during the temporary closure of the business

operations.

3.4 The salary to be taken into account in calculating the

3.4 The salary benefits will be capped to a maximum

benefits will be capped at a maximum amount of R17,712.00

amount of R17 712, 00 per month, per employee and an

per month, per employee and an employee will be paid in

employee will be paid in terms of the income replacement

terms of the income replacement rate sliding scale (38%-

rate sliding scale (38 % -60 %) as provided in the UI Act.

60%) as provided in the UI Act.

3.5 Should an employee's income determined in terms of

3.5 Should an employee's income determine in terms of the

the income replacement sliding scale fall below the

income replacement sliding scale fall below R3500, the

minimum wage of the sector concerned, the employee will

employee will be paid a replacement income equal to that

be paid a replacement income equal to minimum wage of

amount.

the sector concerned.

© Rob Cooper 25UIF Benefit Relief Measures

Temporary Employer/Employee Relief System (TERS)

Legislation Foundation … continued

Directive Amendment to Directive of 26 March 2020

[Gazette No. 43161 published 26 March 2020] [Gazette No. 43216 published 8 April 2020]

3.6 Qualifying employees will receive a benefit calculated in 3.6 Qualifying employees will receive a benefit calculated in

terms of sections 12 and 13 of the UI Act, provided that an terms of Sections 12 and 13 (1) and (2) of the UI Act,

employee shall receive a benefit of no less than sector provided that an employee shall receive a benefit of no less

specific minimum wage. than R3 500.

5.3 Subject to the amount of the benefit contemplated in

clause 3.6, an employee may only receive covid-19 benefits in

5.3 An employee who is being paid by the employer during terms of the Directive if the total of the benefit together with

this period is not entitled to this benefit. any additional payment by the employer in any period is not

more than the remuneration that the employee would

ordinarily have received for working during that period.

5.4 All amounts paid by or for the UIF to employers or

Bargaining Council(s) under the terms of the Scheme shall be

utilized solely for the purposes of the Scheme and for no

other purpose. [continues]

Effective Date: 26 March 2020 Effective Date: No date [assumed to be 26 March 2020]

© Rob Cooper 26UIF Benefit Relief Measures

Comparison of UIF Benefit Calculations

Covid-19 Benefits IRR % Uses Limited To Minimum

1. Unemployment 38% to 60% Credit days Remuneration

2. Illness 38% to 60% Credit days Remuneration

3. Dependant 38% to 60% Credit days Remuneration

4. Reduced Work Time (RWT) 38% to 60% Credit days UIA S12(1B)

5. C19 TERS 38% to 60% ‘Days’ Claimed UIA S12(1B) R3,500 pm (?)

Type of Layoff Reason Benefit Available Reason

1. Permanent Retrenchment Unemployment benefit Operational Requirement

2. Temporary ‘Short time’ RWT benefit Alternative to Retrenchment

3. ‘Forced’ Layoff ‘Lockdown’ RWT or C19 TERS benefit Enforced by National law

Best Practice: Use the C19 TERS benefit for Covid-19 because it does not use or reduce Credit Days

© Rob Cooper 27UIF Benefit Relief Measures

Illness Benefit

► Employee has not contracted Covid-19, but decides to ‘self-isolate’ -

1. Employer and employee must confirm this arrangement in writing

2. Medical certificate is not required if there is a letter from the employer that confirms this arrangement

3. If approved, an illness benefit will be paid for a maximum of 14 days

► Employee has contracted Covid-19 –

o Diagnosis and medical certificate required

o Apply for illness leave benefit as normal

► The illness benefit calculation –

o Uses the Income Replacement Rate formula (38% to 60%)

o Uses, and then reduces, credit days

© Rob Cooper 28UIF Benefit Relief Measures

Reduced Working Time Benefit (RWT)

► Use the RWT benefit if ‘Short time’ has been agreed to

► The RWT benefit calculation –

o Applies the Income Replacement Rate sliding scale (38% to 60%)

o Takes the wage that the employer continues to pay into account to reduce the benefit (same as TERS)

o Uses, and then reduces, credit days

► Caution: It may not be beneficial for employees to use the RWT benefit -

o Employees will have different credit days, therefore different benefit amounts

o Uses, and then reduces, credit days

► RWT can be used for Lockdown claims, but the TERS benefit is a far better option

© Rob Cooper 29UIF Benefit Relief Measures

Benefit Calculation Principles

► SCENARIO: Remuneration fluctuates significantly but is more than the R17 712 limit every month

1. Mthly Average Remuneration: MAR = R17 712

2. Daily Remuneration Rate: DRR = MAR x 12 / 365 = R17 712 x 12 ÷ 365 = R582.31 per day

3. Income Replacement Rate: IRR = 29.2 + (7173.92 ÷ (232.92 + DRR)) = 38

4. Daily Benefit Rate: DBR = DRR x IRR / 100 = R582.31x 38 / 100 = R221.28

5. Reduce DBR: If ‘continued’ (or ‘top up’) remuneration is paid during the benefit period

6. Increase DBR (TERS only): If DBR is less than the daily equivalent of R3 500, then DBR = minimum rate

7. Days (Credit days = 100): CD = 100 (the Fund calculates the credit days at 1 day for every 4 days)

8. Benefit Amount: BA = DBR x CD = R221.28 x 100 = R22 128

► My ‘guess’ on how, and the sequence in which, steps 5 and 6 must be applied for the TERS calculation

1. Step 5: If DBR is greater than the ‘top up’ remuneration’s DBR, then the difference x CD = Benefit Amount

2. Step 6: Adjust the reduced DBR NMW up to the daily equivalent of the R3 500 minimum

► TERS: ‘Top up’ remuneration must less than the benefit amount if unemployed and unpaid

© Rob Cooper 30UIF Benefit Relief Measures

TERS Benefit Examples

► Manually calculated examples of TERS calculations, based on –

1. Credit Days = 30 calendar days

2. Minimum wage calculation not included

Monthly ‘Top-up’ Benefit

Remuneration Remuneration Amount

R20 000 R 0 R6,638.31

R20 000 R 5 000 R1 706,80

R20 000 R10 000 R 0,00

R10 000 R 4 000 R 194,51

R10 000 R 5 000 R 0,00

► Disclaimer:

1. Unfortunately, there is no guarantee of these examples being correct

2. Until the Fund publishes their Benefit calculator, treat these numbers with extreme caution!

© Rob Cooper 31UIF Benefit Relief Measures

C19 TERS: Spreadsheet fields

► Hierarchy of ‘Periods’ for the TERS benefit application –

1. National Disaster period As announced by the President (no end date as yet …)

2. Lockdown period Falls within the National Disaster period (a moving target …)

3. Shutdown period Falls partially or fully within the Lockdown period (employer decision)

4. Employment period Falls partially or fully within the Shutdown period (appointments / terminations)

► Contentious fields specified on the application spreadsheet –

1. Shutdown Date ‘From’: These dates must be aligned with the remuneration paid in point 4

2. Shutdown Date ‘Until’: These dates must be aligned with the remuneration paid in point 4

3. Remuneration Monthly: Last full month’s remuneration can be used

4. Remuneration … during Shutdown: Remuneration paid by employer during the shutdown period

5. Sector minimum wage: It appears that the NMW daily rate will be used in all cases

6. Bank account: Employer’s bank account is probably the best option (if no B.C.)

► You cannot claim more than once for the same shutdown period for the same employees

© Rob Cooper 32UIF Benefit Relief Measures Questions Asked but no Answers … © Rob Cooper 33

As you can see, there is still some water to flow under the bridge … Thank You for joining us today

You can also read