2020 Freight Rate Survey - Owner-Operator Independent Drivers Association Foundation - Owner-Operator Independent ...

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

2017 Freight Rate Survey 0

2020 Freight

Rate Survey

Owner-Operator Independent Drivers Association Foundation

02/19/21

2020 Freight Rate Survey

February 2021

OOIDA Foundation, Inc.

One OOIDA Dr.

Grain Valley, MO 64029

FoundationDept@ooida.com

Table of Contents Introduction .................................................................................................................................................. 6 Looking Back at 2020 .................................................................................................................................... 7 Analysis of the Freight Rate Survey ............................................................................................................ 15 Conclusions and Economic Outlook ........................................................................................................ 23

List of Figures Figure 1: JOC Truckload Capacity Index ........................................................................................................ 8 Figure 2: Weekly Initial Jobless Claims, 2020 ................................................................................................ 9 Figure 3: ISM Purchasing Managers Index, 2020.......................................................................................... 9 Figure 4: Industrial Production Index .......................................................................................................... 10 Figure 5: Retail Sales YoY Change, (Electronic Shopping and Mail-Order Houses), 2020 ........................... 11 Figure 6:Total Business Inventory/Sales Ratio, 2020 .................................................................................. 11 Figure 7: Outbound Tender Volume Index, 2018-2020 ............................................................................... 11 Figure 8: Van and Reefer Outbound Tender Reject Index, 2020 ................................................................. 12 Figure 9: Truckstop.com Van, Reefer, and Flatbed Freight Rates, 2020 ..................................................... 12 Figure 10: New For-Hire Trucking Companies............................................................................................. 13 Figure 11: Operation by Region .................................................................................................................. 16 Figure 12: Non-seasonally Adjusted Truck Transportation Employment (000s) ......................................... 24 Figure 13:ACT Research Class 8 Equipment Orders .................................................................................... 24 List of Graphs Graph 1: Type of Operation ........................................................................................................................ 15 Graph 2: Compensation per mile, 2015-2020 ............................................................................................. 17 Graph 3: When were freight rates at their peak? ....................................................................................... 18 Graph 4: Comparison of Pay Per Mile between those who do and do not know their Cost of Operations 19 Graph 5: Comparison of Pay Per Mile by those who attempt to Negotiate their Rates ............................. 20 Graph 6: Loads turned down due to cheap freight, 2018-2019 .................................................................. 21 Graph 7: Freight Market Outlook................................................................................................................ 21 Graph 8: Negotiating Rates and Fuel Surcharge......................................................................................... 22 Graph 9: Rates are, 2013-2020 ................................................................................................................... 26 Graph 10: Prospects for Next Year, 2016-2020........................................................................................... 26 List of Tables Table 1: Year-over-Year (YOY) Performance of Key Trucking Metrics......................................................... 13 Table 2: Accuracy of DAT Trendlines ........................................................................................................... 23

2020 Freight Rate Survey 6

Introduction

The Owner-Operator Independent Drivers Association Foundation, Inc. (OOFI) was established in 1991 as

a 501(c)(3) non-profit with a mission to conduct research to fight for the rights of all truck drivers through

education. This research includes both economic and safety issues that especially affect small business

owners and professional truck drivers. According to the Federal Motor Carrier Safety Administration

(FMCSA), 85 percent of all fleets operate six trucks or less and approximately 95 percent have fewer than

twenty trucks.1 Single-truck motor carriers represent nearly half of all active motor carriers operating in

the United States today.

Since 1998, OOFI has performed yearly surveys of its membership not only to understand the profile and

demographics of its members, but also to document the holistic changes that are occurring within the

trucking industry, including freight rates. Information concerning the current state of the freight market

is vital in order to help professional truck drivers and small business owners-operators run a successful

business. The freight rate data not only provides important information for the Owner-Operator

Independent Drivers Association (OOIDA or Association), but it also helps give a clearer and more time

sensitive image of the present-day freight market in order to equip OOIDA members with the right

information to make good business decisions.

In 2010, OOFI conducted the first freight rate survey of the Association’s membership. The purpose of

the survey was to gather valuable information and knowledge of OOIDA’s members, who are the

professional truckers who truly represent the long haul truckload industry and move our nation’s

economy, and to examine the data in order to better understand today’s freight market. This is the ninth

edition of the Freight Rate Survey, or “Survey,” which is conducted annually.

1

Source: Motor Carrier Management Information System Database December 2020

Owner-Operator Independent Drivers Association Foundation

7 2020 Freight Rate Survey

Looking Back at 2020

In many ways, the trucking industry is the lifeblood of the nation as it not only employs approximately 3.9

million commercial driver’s license holders, but it is also responsible for delivering 70 percent of all freight

worth $11.5 trillion2 while collecting $791.7 billion in gross revenue.3 For obvious reasons, trucking is

vital to the overall economic health of the United States, and thus serves as a barometer for the current

state of the economy. When the freight market experiences higher freight volumes and strong rates, this

typically indicates a healthy economy, along with sturdy consumer confidence levels, housing and

construction starts, oil prices, industrial production, and manufacturing output.

The trucking industry in general however is always in flux and often difficult to predict as it faces numerous

government regulations and mixed economic growth. The 2020 freight market was no different as the

excess capacity which plagued the industry during the later portion of 2018 and most of 2019 continued

to keep truckload rates low at the start of 2020 as indicated in Figure 1. While there was some optimism

for a gradual increase in rates by the second quarter due to the United States-Mexico-Canada Agreement

(USMCA), the phase one trade agreement between the U.S. and China, and a potential recovery for the

U.S. manufacturing sector after a months-long slump, 2020 began with much uncertainty.

Susquehanna Financial Group released a report in early January 2020 predicting that dry van spot rates

would decline through the first quarter before increasing later in the spring. The report concluded, “Most

carriers expect a slow bleed of this extra capacity as we move through 1H20 [the first half of 2020] aided

by depressed rates, increasing insurance costs and new regulations that are expected to limit supply.4”

Paul Bingham, the director of transportation consulting in the Economics and Country Risk unit of IHS

Markit, expected that 2020 “may not be a boom year, but it could still be a better one [than 2019].5” Few

could have anticipated the global pandemic which would shape most, if not all, of 2020.

On December 31, 2019, the world received first news of the virus that would eventually be called COVID-

19 after Chinese health officials informed the World Health Organization (WHO) of 41 patients who had

been diagnosed with a “mysterious pneumonia.” Chinese media reported its first death two weeks later,

while the CDC confirmed the first case of the Coronavirus in the U.S. on January 20, 2020. On March 11,

the WHO declared the virus a pandemic.6 Nevertheless, COVID-19 was already starting to impact trucking

even before it became a global pandemic as China quickly shuttered its manufacturing in an attempt to

curb the virus, which began to negatively impact imports and thereby outbound tender volumes and

trucking rates in the first two months.

2

Bureau of Transportation Statistics, Transportation Statistics Annual Report 2020, Department of Transportation

(2020) pg. 4-3

3

“Trucking Moved 11.84 Billion Tons of Freight in 2019,” American Trucking Association (July 13, 2020),

https://www.trucking.org/news-insights/trucking-moved-1184-billion-tons-freight-2019

4

John Kingston, “Trucking rates may be moving toward a ‘melt-up’: Majors,” FreightWaves (January 15, 2020).

5

William B. Cassidy, “US manufacturing upturn may boost spring freight volumes, truck rates,” Journal of Commerce

(Jan 22, 2020).

6

Bryson, Derrick. (March 27, 2020). A Timeline of the Coronavirus Pandemic. Retrieved from

https://www.nytimes.com/article/coronavirus-timeline.html

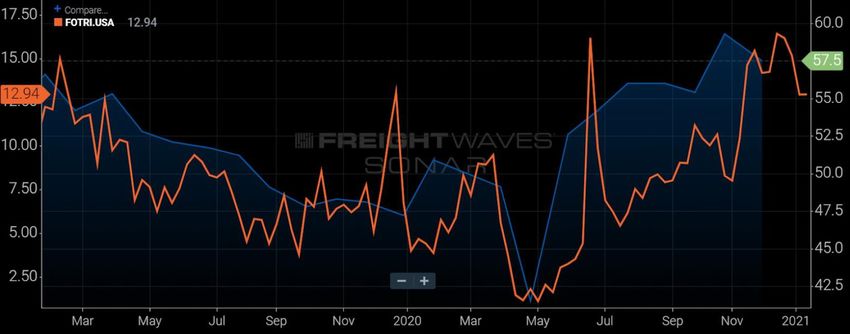

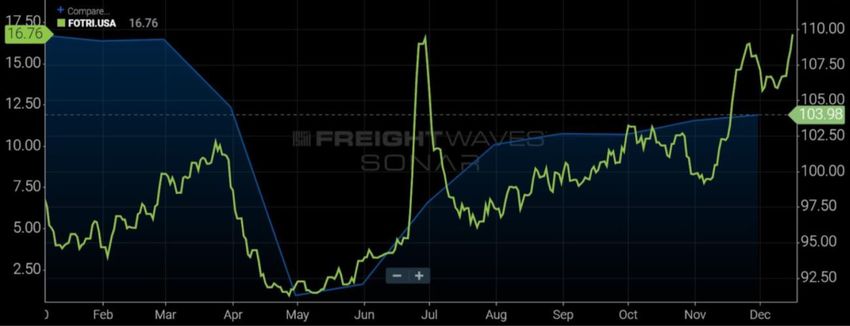

Figure 1: JOC Truckload Capacity Index7 Shippers however were warned in early March to begin preparing for a potential trucking rate shock, but few could have expected the tremor that would occur. Jeff Tucker, CEO of freight brokerage Tucker Company Worldwide, predicted in an interview with The Journal of Commerce, “A shock wave is going to be felt across the country in trucking…shippers better brace for the worst.” He forewarned that once China reestablished its supply chains and began moving freight through U.S. ports it would “be like the 2018 market all over again when the freight starts flooding back in, folks are going to charge an arm and a leg, and that will have a ripple effect that doesn’t go away in a quarter. It’s going from one extreme to another.8” President Donald Trump declared a national emergency on March 13, 2020 with most states following suit. In the wake of these declarations, many non-essential businesses, and thereby the overall economy in many respects, were forced to close their doors and all public gatherings of more than ten people were banned, greatly impacting the various service and good industries, especially restaurants and industrial 7 The TCI represents change in tractor count at a group of companies fielding more than 23,000 tractor-trailers, and is meant to capture and measure changes in capacity at large contract carriers, and may not reflect trends at mid- sized companies and smaller truckload fleets, which in many respects are a different operational segment of the overall trucking market. 8 William B. Cassidy, “Coronavirus blurs trucking’s 2020 vision,” Journal of Commerce (March 5, 2020).

9 2020 Freight Rate Survey

production.9 Freight volumes plummeted, pushing rates to all-time lows as carriers competed over limited

loads. Although most of the country shuttered its doors, causing unemployment to rise exponentially,

truck drivers continued to haul essential goods to homes, grocery stores, and hospitals across the nation.

The following figures were generated using SONAR, an analytics platform which collects data from

hundreds of different indices, such as CASS, Freightos Baltic Index, Institute of Supply Management

Metrics, Logistics Managers’ Index, etc., to provide a comprehensive view of the freight market and how

it was impacted by COVID-19. Figure 2 demonstrates that weekly initial jobless claims spiked in late March

and in early April due to the shutdowns, which effectively limited manufacturing (Figure 3) and industrial

production (Figure 4), as well as consumer spending, driving down volumes, rejection rates, and trucking

rates.

Figure 3 depicts the Institute for Supply Management’s (ISM) Purchasing Managers Index (PMI) which is

a diffusion index that summarizes economic activity in the manufacturing sector. A PMI over 50

characterizes overall expansion of the manufacturing economy where as a PMI under 50 represents a

contraction. Figure 4 shows the Federal Reserves’ Industrial Production Index (IPI) which measures real

output in the manufacturing, mining, electric, and gas industries. Industrial production is perhaps the

largest single contributor to domestic surface freight movements in the economy and thereby trucking,

of which manufacturing makes up approximately 75 percent. Hence industrial output, as measured by

the IPI, serves as a starting point for most of the goods that end up flowing through various supply chains

to the end consumer.10

Figure 2: Weekly Initial Jobless Claims, 2020

SONAR: Weekly Initial Jobless Claims (blue line)

Figure 3: ISM Purchasing Managers Index, 2020

9

Mark Schremmer, “A coronavirus timeline: How we got here,” Land Line Magazine (April 1, 2020),

https://landline.media/a-coronavirus-timeline-how-we-got-here/

10

https://knowledge.freightwaves.com/industrial-production-ipro-iprog/SONAR: ISM Purchasing Managers Index (blue line), Flatbed Outbound Tender Rejection Index (orange line)

Figure 4: Industrial Production Index

SONAR: Industrial Production Index (blue line), Flatbed Outbound Tender Rejection Index (green line)

Each of these individual factors impacted one another with unemployment reaching a pandemic high of

14.7% in April, the worst since the Great Depression. Some owner-operators experienced freight rates

below a dollar during the onset of the pandemic. However, the figures presented above also display a

sharp V-shaped recovery following the first round of stimulus checks, increased jobless claims benefits,

and federal loans administered through the Paycheck Protection Program and the Economic Injury

Disaster Loan program, which combined to inspire consumer confidence and spending. Demand for goods

rose steeply and so did trucking rates throughout the second half of 2020.

Consumer spending traditionally comprises 70 percent of the overall economy. Of that, two thirds

typically derive from services while the remaining one third results from goods. In 2020 however, the

traditional split moved closer toward 60/40, with goods (the items which truckers transport) accounting11 2020 Freight Rate Survey

for 40 cents of every dollar of consumer spending.11 This was particularly manifested in ecommerce,

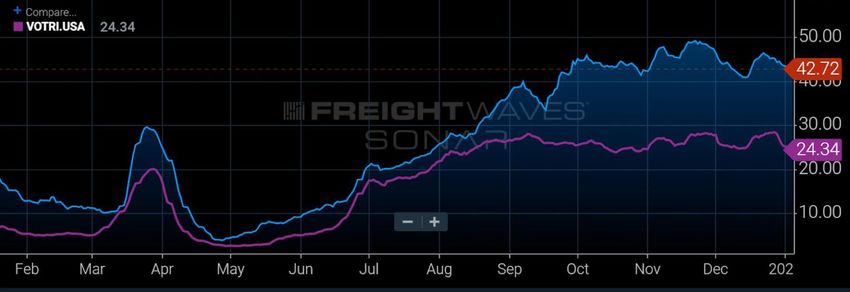

shown in Figure 5, which exploded as Americans were unable to travel or shop in brick-and-mortar stores.

In response, shippers sought to pull their freight forward in order to both meet demand and mitigate their

depleting inventories (Figure 6), which pushed freight volumes to all-time highs (Figure 7) and challenged

trucking capacity. Large motor carriers were forced to reject more than a fourth of their tendered loads

(Figure 8), which shifted freight toward the spot market and increased rates after the trough earlier in the

year (Figure 9).

Figure 5: Retail Sales YoY Change, (Electronic Shopping and Mail-Order Houses), 2020

SONAR: Retail Sales Electronic and Mail-Orders (blue line), Van Outbound Tender Rejection Index (orange line)

Figure 6:Total Business Inventory/Sales Ratio, 2020

SONAR: Total Business Inventory/Sales Raito (white line)

Figure 7: Outbound Tender Volume Index, 2018-2020

11

2021 Freight Forecast, FreightWaves FreightIntel Research (January 2021).SONAR: Outbound Tender Volumes 2020 (blue line), 2019 (purple line), 2018 (green line)

Figure 8: Van and Reefer Outbound Tender Reject Index, 2020

SONAR: Van Outbound Tender Reject Index (purple line), Reefer Outbound Tender Reject Index (blue line)

Figure 9: Truckstop.com Van, Reefer, and Flatbed Freight Rates, 2020

SONAR: Truckstop.com 7 Day Van Rate Per Mile (blue line), Truckstop.com 7 Reefer Rate Per Mile (purple line),

Truckstop.com 7 Day Flatbed Rate Per Mile (green line)13 2020 Freight Rate Survey

The above figures illustrate that the year 2020 experienced both extreme lows and highs due to the COVID-19

pandemic, which greatly impacted owner-operators and professional drivers who witnessed acute fluctuations in

rates over the course of the year. According to DAT Trendlines, spot rates for dry vans, refrigerated trailers, and

flatbeds hit bottom around April and May. The lowest average monthly spot rate was $1.60 for dry vans, $1.93 for

reefers, and $1.91 for flatbeds. Conversely, the spot rates shifted gears starting in June, reaching year highs in

November and December. The highest average monthly spot rate was $2.46 for vans, $2.70 for reefers, and $2.48

for flatbeds. Table 1 also depicts the volatility of the freight market through three key trucking metrics, tendered

load volumes, tender rejection rates, and Truckstop.com spot rates.

Table 1: Year-over-Year (YOY) Performance of Key Trucking Metrics

Metric Q1 Q2 Q3 Q4

Tendered Load Volumes YoY 6.42% 2.91% 39.31% 55.02%

Tender Rejection Rate YoY 13.5% 26.0% 371% 278%

Truckstop.com Spot Rates YoY -1.4% -12.9% 28.8% 29.4%

Source: SONAR

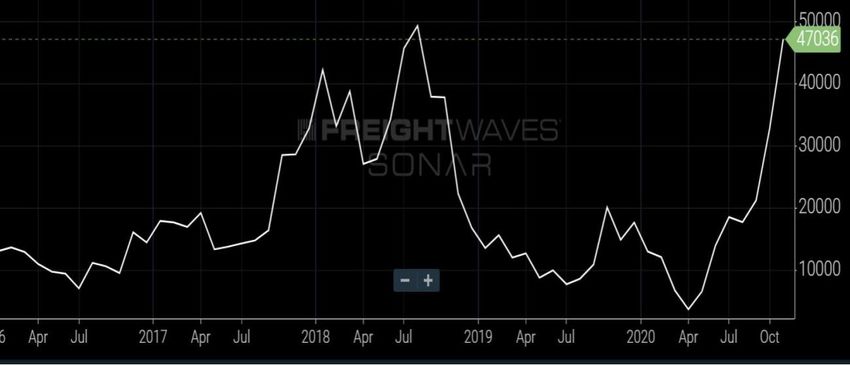

These dynamics combined to help make 2020 a boon year for trucking, especially for owner-operators. In

fact, OOIDA filed a record number of new authorities on behalf of its’ membership. Interestingly, this

trend began at the start of the pandemic in March 2020. When OOFI asked those members who were

seeking to become owner-operators under their own authority why they were doing so at this time, 74

percent stated that they wanted to because they desired to be their own boss. However, this trend gained

even more momentum in the second half of the year with FMCSA granting nearly 58,000 common

authorities in 2020 overall, a 36 percent increase from 2019.12 The movement to become an owner-

operator was not just sparked by those seeking to become their own boss, but by those company drivers

hoping for a more successful and profitable career as an owner-operator in a time when spot rates were

rising too meet increasing demand.

Figure 10: New For-Hire Trucking Companies

Source: FTR analysis of FMCSA data

12

Avery Vise, “New Entries in Trucking Surged in 2020,” Heavy Duty Trucking (Feb 9, 2021).15 2020 Freight Rate Survey

Analysis of the Freight Rate Survey

While most economic and trucking industry analysts focus primarily on large carriers and shippers, as well

as various macro-economic factors as highlighted above, few remember the small owner-operators and

professional drivers. Thus, in order to gauge the current freight market for this unique segment of

trucking, OOFI emailed a thirty-two question survey to 21,000 members who allow for email

communication on November 4, 2020. The Survey generated 425 responses for a started/viewed rate of

51 percent and a 99 percent confidence level with a 6.2 percent margin of error, thus the Survey provides

an essential snapshot of what is occurring within the small carrier population today.

In particular, the survey respondents were comprised almost entirely of owner-operators (88%), with a

small segment of company drivers (8%) and fleet owners (6%). Owner-operators consisted of two distinct

segments, owner-operators under their own authority (44%), which experienced a five-percentage point

increase from 2018, and owner-operators leased-on to a motor carrier (40%), which, for the first time

since OOFI began conducting this survey in 2010, did not represent the largest section of respondents. A

majority of members indicated that they are truckload carriers (77%) regardless of the type of equipment

or freight they haul. It is interesting to note that those pulling hazmat (63%) and oversize loads (64%)

were more likely to be a leased on owner-operator than most other types of operation, perhaps due to

higher insurance and equipment costs related to these freight types.

Graph 1: Type of Operation

Fleet owner Retired

6% 1%

Other

Company driver 0%

8%

Owner-operator (own

authority)

45%

Owner-operator

(leased to motor

carrier)

40%

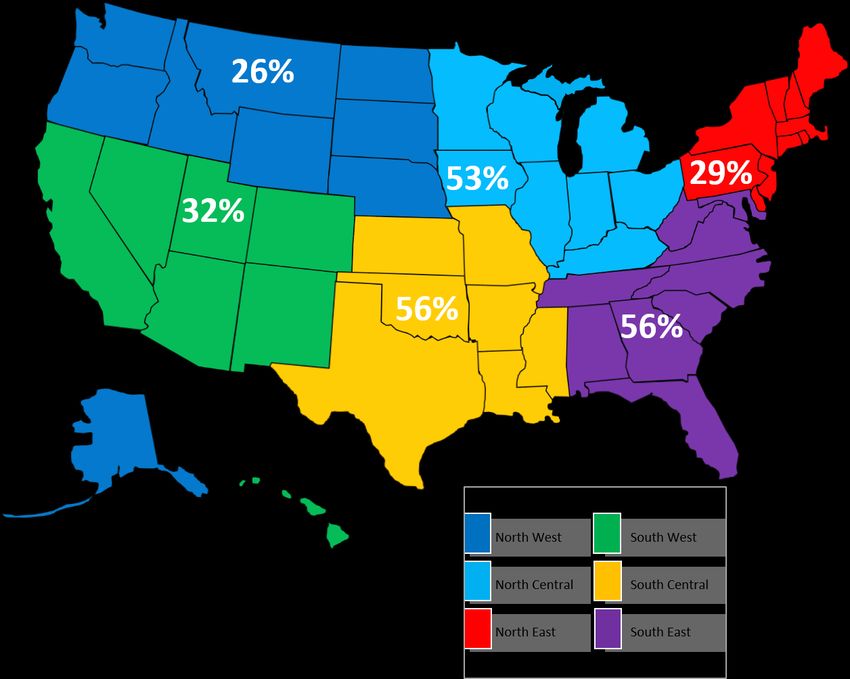

Consistent with other surveys of OOIDA members, OOFI found that dry vans, flatbeds, and refrigerated

trailers, or reefers, were the three most common types of trailers members pull. General food products

were the most common type of freight regardless of operational type followed by refrigerated freight.

Although most members indicated that they were long haul operators, meaning that their average

distance hauled was over 500 miles, fleet owners (57%) and those pulling hazmat (48%) or buildingmaterials (52%) were principally regional, i.e. operating between 151 and 500 miles. Most members

continue to drive in the north central, south central, and south east regions of the United States. However,

those under their own authority tend to operate primarily in the south east, while those leased-on operate

mainly in the south central region.

In terms of compensation, “per trip” and “per mile” pay continue to be the primary methods of payment

for all operational types except for those members who are leased-on. They primarily receive

compensation by the “percentage of the load,” which was also true for those hauling hazmat loads.

Although the methods of compensation were fairly similar across the various operational and equipment

types, the rates were not as leased-on owner-operators received the highest average compensation rate

per trip at $1,937.45, a nearly 22 percent increase from 2019, and fleet owners experienced the highest

average per mile at $2.65, which was a 24 percent increase over last year. Company drivers on the other

hand received the lowest compensation overall at $0.52 per mile, which actually represented a 17 percent

decrease from 2019.

Figure 11: Operation by Region17 2020 Freight Rate Survey

Most of the industry segments that OOFI surveyed experienced an increase in pay per mile year-over year

except for company drivers and those pulling flatbeds, in particular those hauling building materials and

oversize and overweight (OSOW) loads. While general and refrigerated freight saw steep rebounds after

the initial effects of the pandemic in the spring, flatbed freight experienced a much slower recovery as

nonresidential construction spending gradually improved throughout the year. Thus, those pulling

flatbeds witnessed a 12 percent decrease in per mile pay, from $2.33 per mile in 2019 to $2.05 in 2020,

and those hauling building materials and OSOW loads observed a 6 percent and a 55 percent decrease in

pay per mile, respectively. Members overall lost a penny in average per mile pay this year from $1.85 per

mile in 2019 to $1.84 in 2020. However, most of this was due to a decrease in pay per mile for company

drivers. If this segment is filtered from the data, members actually received a 12 percent increase in

compensation per mile, which is in harmony with the rest of the freight market.

Graph 2: Compensation per mile, 2015-2020

$2.00

$1.92

$1.90

$1.85 $1.84

$1.80

$1.71

$1.70

$1.64

$1.60

$1.54

$1.50

2015 2016 2017 2018 2019 2020

Though pay per mile decreased slightly, compensation per trip continued its positive trend, increasing 9

percent from $1,609 in 2019 to $1,756 in 2020, and nearly 16 percent from 2018. The most noteworthy

increases were experienced by fleet owners (32%) and those leased-on (22%), and those pulling dry van

trailers (41%) and OSOW loads (86%).

According to the results of last year’s survey, the majority of members indicated that rates had gone down

over the course of 2019, though this trend actually originated in the second half of 2018. Thus, for almost

a year and half the freight market experienced a contraction in rates. The 2020 survey however saw a

stark reversal as percentage of members who believed rates were going down decreased from 70 percent

in 2019 to 33 percent in 2020. Moreover, the percentage of members who stated rates were increasing

jumped from 4 percent to 28 percent, which was seven times greater than the previous survey. When

asked when freight rates were at their peak, 41percent indicated it was best within the past six months.Graph 3: When were freight rates at their peak?

35%

30%

25%

20%

15%

10%

5%

0%

1 YEAR AGO 6 MONTHS AGO 3 MONTHS AGO RIGHT NOW HAVEN'T SEEN A

CHANGE

The acquisition of loads is vital for both fleet owners and those under their own authority and yet these

two operational types tend to obtain freight through different means. Fleet owners typically build direct

relationships with shippers and receivers, while those under their own authority primarily utilize load

boards. Although OOIDA encourages its members to work directly with shippers, it is interesting to note

that the compensation per mile was similar between these two methods. For those utilizing load boards,

the top three are DAT (58%), Truckstop.com (34%), and C.H. Robinson (24%). While load boards have

become highly popular over the past few years, a fairly new option has entered into the market place.

Namely, digital load matching.

Digital load matching primarily consists of a technology company, acting as a broker, who develops a

platform which automates the load acquiring process by allowing a driver to match their truck with a

pending load. The platform then utilizes machine learning and artificial intelligence in an attempt to

match that driver to future loads of similar kind. Thereby bypassing the various brokers who typically post

loads on load boards. According to the 2020 Freight Rate Survey, four percent of members utilize such

applications. For those who do, the most popular load matching apps are Convoy, Uber, and JB Hunt 360.

When asked how they set their rates, several fleet owners and owner-operators under their own authority

stated that they do so by utilizing region, state, and seasonal information, as well as various economic

data such as DAT’s 15-day rate view. Members also calculate their rates by determining the minimum

price per mile they need in order cover their operating costs, including fuel, insurance, tolls, truck

payments, etc. In fact, 77 percent of respondents indicated that they know their cost of operations. This

was especially true for fleet owners (92%). The average cost per mile was $1.85 for those under their own

authority, $1.61 for those leased-on, and $1.96 for fleet owners.19 2020 Freight Rate Survey

It is critical for an owner-operator to know how much they need to earn in order to both cover their

operating expenses and pay themselves. Without this knowledge, the possibility for failure rises

exponentially every year within the first five years of operation. An owner-operator who knows their

costs is better equipped to choose which freight, region, and type of operation is best for their business,

as well as being better able to negotiate their rates. Those who knew their cost of operations earned

$1.00 more per mile and over $700 more per trip than those who did not know.

Although most company drivers did not know how their carrier sets their rates (79%), those who did said

their carrier utilized various market information, including volume, demand, distance, season, freight lane,

spot rate, and what specialized equipment is needed to complete the shipment.

Graph 4: Comparison of Pay Per Mile between those who do and do not know their Cost of Operations

$2.50

$2.09

$2.00 $1.84

$1.50

$1.09

$1.00

$0.50

$-

DO KNOW DO NOT KNOW OVERALL

When it comes to negotiating, fleet owners (65%) and those with their own authority (56%) felt that they

were in a better position in 2020 to negotiate rates than in 2019, which was also true for those pulling dry

van trailers (56%) and reefers (56%). However, leased-on owner-operators (65%), those pulling flatbeds

(55%), and those hauling hazmat (88%) and OSOW (85%) loads felt that they were in a worse position this

year. Again, this probably due to the sluggish recovery for these segments of the industry.

While 45 percent of respondents always attempt to negotiate their rates, several members were unable

to negotiate and instead were pressed to obtain a certain level of compensation. For example, several

members stated that they always strive to earn a certain benchmark, or more, on all miles, while others

felt forced to settle for less than their operating costs or just enough to pay their bills. Some members

chose not to negotiate their rates because they were afraid of losing business, did not feel they would

receive it anyway, or were not comfortable with negotiating. Additional members stated that they did

not negotiate simply because the rates were in the range of what they were asking for. Others stated the

rates were pre-set or that the rates have always been this way. One member wrote, “I only negotiate if Ifeel the rate is substandard.” It is important to note however that those who at least attempt to negotiate

their rate earned more per mile and per trip than those who never made the attempt.

Graph 5: Comparison of Pay Per Mile by those who attempt to Negotiate their Rates

$2.40

$2.21 $2.23

$2.20

$2.05

$2.00

$1.80 $1.75

$1.60

$1.40

$1.20

$1.00

ALWAYS USUALLY OCCASIONAL NEVER

For company driver members, 41 percent stated that their carrier was better equipped to negotiate rates

in 2020 rather than in 2019, which was a 40 percent increase from the previous survey. This positive trend

also transitioned into the number of loads hauled overall, as both those who receive freight through

brokers or a third party and those who utilize carriers or shippers, indicated that loads were increasing,

particularly fleet owners and those pulling van or reefers. Moreover, members also demonstrated that

they are turning down less loads than before due to cheap freight, with 51 percent stating that they turned

down less than 25 percent of their loads in comparison to 35 percent in the previous survey as shown in

Graph 6.

The number of overall loaded miles decreased slightly in 2020 compared to the previous year, primarily

due to a sharp decrease in miles for those pulling flatbed trailers and hauling building materials and OSOW

loads. In fact, all other operational and equipment types experienced increases in loaded miles, with only

33 percent of members in general stating their loaded miles shrank in comparison to 48 percent who

indicated so in 2019. Deadhead or unloaded miles also decreased overall, but much more drastically as

only 28 percent stated their deadhead miles grew in 2020 compared to 50 percent in 2019.

The average member drove approximately 93,500 loaded miles and 13,000 unloaded miles, representing

a 1 percent decrease in loaded miles and a nearly 45 percent decrease in unloaded miles. Those hauling

reefers continued to incur the most loaded miles at 121,500, a 20 percent increase, while leased-on

owner-operators drove the fewest. Fleet owners and those pulling dry vans experienced the most

unloaded miles behind leased-on owner-operators. In general, a majority (54%) of members were able

to negotiate a fuel surcharge into their freight rates.21 2020 Freight Rate Survey

Graph 6: Loads turned down due to cheap freight, 2018-2019

50%

45%

40%

35%

30%

25%

20%

15%

10%

5%

0%

I do not turn down 0 to 25% 26 to 50% 51 to 75% More than 75%

cheap freight

2019 2020

Graph 7: Freight Market Outlook

70%

60%

50%

40%

30%

20%

10%

0%

Overall, freight rates are: If you use a freight broker or third If you get your loads from a motor

party, the number of loads are: carrier or shipper, are the number of

loads:

Increasing Decreasing Staying the same

OOFI also inquired to know how many members utilize factoring services, which are designed to help

motor carriers to obtain finances for their immediate cash needs in return for a percentage of their

accounts receivable or invoices. A vast majority do not use a factoring service in their trucking business

(77%). The average fee overall for those who do use such a service was 3.2 percent, which was the same

fee as in 2019.When asked concerning their professional opinion of factoring in the 2018 Freight Rate Survey, most

members responded that they were not supportive of such a service, stating, “It’s better to manage your

own money, than to pay someone to pay you.” Many wrote that the fees were too high and that factoring

simply enables those that cannot manage their cash flow properly. However, others view factoring as a

necessary evil and even a useful tool for small carriers and independents who do not have the funds to

run their business for 30, 90, or 180 days while they wait to be compensated. One member said, “Honestly

I think they provide a very important service to those of us looking to get a foothold in the industry.”

However, many noted that individuals should use factoring sparingly.

Graph 8: Negotiating Rates and Fuel Surcharge

Have you been able to include a fuel surcharge in freight

rates?

Have you been able to negotiate rates more this year than

last?

42% 44% 46% 48% 50% 52% 54% 56%

No Yes

In order to obtain a better understanding of the current freight market, as well as to ascertain the accuracy

of other freight indicators, OOFI posed three different questions concerning the average spot and contract

rates as indicated by DAT Trendlines for the dry van, flatbed, and reefer segments of the industry. OOFI

also asked if any of the respondents were currently utilizing additional economic information published

by groups such as DAT, FreightWaves, the Cass Index, IHS Markit, etc. Although a majority of respondents

stated the figures published by DAT were correct, the members’ average compensation rate per mile for

each equipment type was below DAT’s numbers.

Of those members earning less than the average pay per mile, 40 percent did not know their cost of

operations and 30 percent stated that they never try to negotiate their rate. These figures suggest that

members who are receiving less than average compensation are those same individuals who do not know

what they need to make to be profitable and do not ask for more pay. Conversely, of those members who

receive more than the average per mile pay, 87 percent know their cost of operations and 52 percent said

they always attempt to negotiate their rates. Regardless, the table below demonstrates that DAT’s23 2020 Freight Rate Survey

Trendlines is an accurate barometer of the current freight rates across the trucking industry according to

OOIDA’s members.

Table 2: Accuracy of DAT Trendlines

These figures The average spot and The average spot and The average spot and

are: contract rates for vans has contract rates for flatbeds contract rates for reefers

been $1.96 and $2.10 has been $2.18 and $2.47 has been $2.26 and $2.36

respectively respectively respectively

Far too high 19% 16% 12%

Slightly high 26% 19% 19%

Correct 33% 45% 46%

Slightly low 14% 12% 15%

Fart too low 9% 9% 9%

Conclusions and Economic Outlook

From 2018 to 2020, OOIDA members have seen dramatic shifts in the overall freight rates as the freight

market reached record highs in June 2018, but began to slowly contract through the later part of the year

and into 2019. Following a disappointing 2019, freight rates once again roared back to record heights

during the second half of 2020. In particular, the number of respondents who indicated that freight rates

were dropping in comparison to the previous year, decreased 53 percent, coupled with a 600 percent

increase in those who stated rates were improving.

Despite the volatility in the freight market throughout 2020 due to the pandemic, the trucking industry

overall finished off the year strong and is expected to continue into the first half of 2021. However, the

health of the freight market will depend largely on a few factors. Perhaps the most important factor is

unemployment as jobless claims continue to hover around high levels. This could potentially stunt

consumer confidence and thereby consumer spending which will ultimately impact freight demand

moved by trucks. Moreover, analysts believe that the market will return to normal in regards to

traditionally consumer spending. In 2020, consumer spending shifted more toward goods than services

as the country began shuttering its doors. The consensus however is that this trend will shift back to the

more traditional 67/33 split instead of the current 60/40 split, which could possibly lesson freight demand.

The next factor that will have a significant impact on the outlook for 2021 is imports and global trade. The

ports of Los Angeles and Long Beach have experienced tremendous congestion through the first two

months of 2021 due to extremely high inbound volumes and logistical complications both inside and

outside the ports. On February 1, 2021, there were twenty-five container ships at berth at the ports and

40 container ships at anchor, an all-time record.13 The congestion issues are rippling across other major

U.S. ports as well, which virtually guarantees high truck demand for the foreseeable future in certain

markets.

The final factor is capacity, which has slowly been coming back online as carriers have been filling their

empty seats and ordering new trucks. Figure 12 demonstrates that there was a steep drop in truck

13

Greg Miller, “New video shows massive scope of California box-ship traffic jam,” FreightWaves (February 11, 2021)transportation employment in early 2020 after the industry had experienced few years of steady increase.

The figure also illustrates how truck employment has rebounded since then, eventually reaching 2018

employment levels by the end of the year. Moreover, according to ACT Research, while the trucking

industry experienced a large influx in new Class 8 truck orders in 2018 and 2019, equipment orders

dropped off significantly in 2020. However, as with the other economic indicators discussed in this report,

new orders have rapidly recovered since then. This additional capacity could potentially put downward

pressure on freight rates as it did in 2018 and 2019.

Although macroeconomic indicators which help to gauge the overall health of the economy such as the

PMI, Gross Domestic Product, the Cass Freight Shipments Index, the Freightos Baltic Daily Index, U.S.

Customs and Maritime Import Shipment Volumes, Total Construction Spending, and others have showed

momentum over the last few months of 2020 and into 2021, capacity is a crucial element concerning the

condition of the freight market. Thus the trucking industry faces a possible overhang if capacity rises

freight demand normalizes or falls. For example, when economic growth began to slow in 2019, the

truckload market found itself in the midst of an overcapacity problem due to the record number of Class

8 truck orders in 2018, causing rates to fall. It is imperative for the owner-operator to be examining the

current condition of the freight market and to prepare accordingly.

Figure 12: Non-seasonally Adjusted Truck Transportation Employment (000s)

Source: SONAR

Figure 13:ACT Research Class 8 Equipment Orders25 2020 Freight Rate Survey

Source: SONAR

While large motor carriers and the broader market tend to focus on these economic indicators, it is

important for the small business owner to do the same. The purpose of the Freight Rate Survey is to

gather information from the owner-operator and professional truck driver. Thus when members were

asked for their perception concerning the prospects for the coming year based on their experience and

professional opinion, 70 percent forecasted either similar or improving prospects for 2021, compared with

62 percent in the previous survey.

Though many members have positive outlooks for next year, there is some disconnect between market

analysts and those truckers on the ground level. While many reports indicate that the first quarter in 2021

will be a strong one, some members felt rates were dropping and that political uncertainty would

negatively impact the market for the foreseeable future, as well as increased capacity. It is important to

note however that OOFI sent the survey Wednesday, November 4, 2020. Since that time, much of the

uncertainty surrounding the presidential election has been resolved, yet there is still more uncertainty to

come, which is normal when a new administration enters the White House. Members are not only

concerned with market conditions, but also how the regulatory agenda of a new incoming administration

will affect their livelihoods.

In response to the members’ prospects for 2021, 46 percent indicated that they are planning to make

changes in their business plan for next year, which is the same percentage as last year. Several fleet

owners and owner-operators under their own authority expressed their desire to expand their operations

by either purchasing a new truck, new or newer equipment, or even both. Others mentioned downsizing

their operation or leaving the business altogether due to volatile rates and excessive rules and regulations.

For leased-on owner operators, many are looking to obtain their own authority, while a few are looking

to get out of the business. However, regardless of operational type, many members pledged to increase

the efficiency of their business, whether through more research into freight markets, changing lanes orregions, being more selective of their routes and securing backhauls, becoming more specialized, or

simply focusing to reduce expenses and deadhead miles.

Graph 9: Rates are, 2013-2020

80%

70%

60%

50%

40%

30%

20%

10%

0%

2013 2014 2015 2016 2017 2018 2019 2020

Going up Going down Not Changing

Graph 10: Prospects for Next Year, 2016-2020

50%

45%

40%

35%

30%

25%

20%

15%

10%

5%

0%

2016 2017 2018 2019 2020

Better Worse About the same

In short, the data from the survey creates a picture of a freight market ready to continue strong into the

first half of 2021. There are still some big questions that remain however, will unemployment rise and

consumer spending decrease, will industrial production and manufacturing cool off, will freight demand27 2020 Freight Rate Survey

finally level out, and most importantly, will carriers continue to add truck capacity in order to gain more

business as they did in 2018 and 2019. Much of the freight market will hinge on these important factors.

It is crucial for any small business owner or professional truck driver to keep these questions in mind

moving into 2021. Depending on capacity and freight volume, members might consider consolidating

their business, changing operations, or perhaps even obtaining their authority or purchasing another truck

in order to expand their scope of operation. Either way, it is vital for members to follow the state of the

market in order to make the best decision for their business and their livelihood.You can also read