2020 Semi-Annual Comment - CV INVEST PARTNERS AG

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Dezember 29

Semi-Annual

Comment 2020

Tech Stocks and

Inflation –

A glimpse of the

future

CV Invest Partners AG 1

Semi-Annual Comment

Tech Stocks and Inflation –

A glimpse of the future

Michael Gunnarsson

Source: www.grrrgraphics.com

In the last 10 years, growth stocks have been among the The 10 largest companies by

biggest winners. In particular, the so-called FANMAG market capitalization 2020

companies (Facebook, Apple, Netflix, Microsoft, Amazon and

Google) and their shares have undergone a breathtaking

development. It is hard to imagine that Facebook, for example,

only went public in 2012 and is now one of the ten largest

companies in the world by market capitalization. No fewer than

5 of the tech giants mentioned are among the top 6.

Their impressive profit and revenue increases have made them

the darlings of investors. Hardly any fund manager could and

can afford to ignore the tech heavyweights. And if they dared

to do so, they paid for it with a clearly below-average

performance. The extent of the dominance of the FANMAG

Source: CV Invest Partners AG

companies is indeed remarkable:

The aggregated market capitalization of the six FANMAG companies (Facebook, Apple,

Netflix, Microsoft, Amazon, Google) corresponds to the market capitalization of all stocks

included in the German DAX, the French CAC 40, the Dutch AEX, the Italian MIB, the Spanish

IBEX, the Swiss SMI and the British FTSE 100!

Amazon alone is worth 30% more than all the stocks included in the German DAX, and this

includes heavyweights such as SAP, Linde, Siemens and Allianz.

The aggregate market capitalization of Apple, Amazon and Facebook is roughly equivalent

to the gross national product of Germany

The five largest stocks in the S&P 500 (Apple, Microsoft, Amazon, Facebook and Alphabet)

have a larger weighting in the index than ever before (25%).

Since 2013, Facebook, Amazon, Netflix and Google stocks have gained 928%, while the S&P

496 (without those four stocks) has "only" slightly more than doubled

From the beginning of the year to the end of October, the S&P 500 has gained 6%. However,

without Facebook, Amazon, Apple, Microsoft and Google, which have gained 39%, the index

would be down 1%.

CV Invest Partners AG 2

Semi-Annual Comment

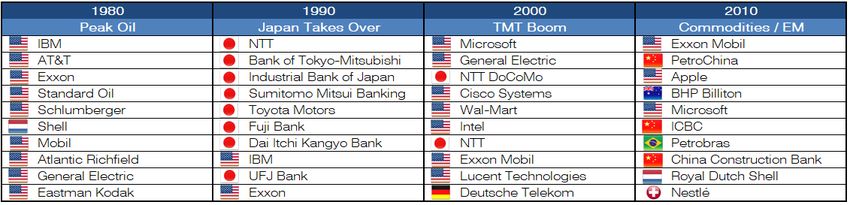

Even if it hardly seems conceivable from today's perspective, it is unlikely that today's big players in the

technology sector will retain their supremacy in the next decade. If we look at the ten largest

companies of the last decades we see that on average just two companies remained among the

largest in the following decade.

The 10 largest companies by market capitalization 1980-2010

Source: CV Invest Partners AG

The 1970s were dominated by oil multis, as the belief in "peak oil" prevailed at the time.

The 80s, in turn, were dominated by Japan's economic miracle. At the time, no one could have

imagined that Japan would fall into a decades-long depression and that Japanese stocks would

virtually disappear from the scene.

In the 1990s, Internet and telecom companies dominated the stock markets until the bubble burst in

2000. The hype surrounding the so-called "Volksaktie" of Deutsche Telekom or the crazy amounts that

telecom companies spent on UMTS licenses are well remembered.

The first decade of the new millennium was characterized by strong growth in emerging markets and

the associated commodity boom. At the time, everyone thought they knew that commodity prices

would only rise because of China's demand.

In other words, the dominant theme of one decade in the recent past was never also the dominant

Sir John Templeton

theme of the next decade. It would therefore not be surprising if, once again, the greatest risks lie in

Templeton Funds Founder

supposedly safe investments that have been characterized by high valuations, high popularity and high

and former Chairman

outperformance over the past few years.

„The four most expensive Although no one likes to hear it at the moment, we expect that in ten years' time completely different

words in the English companies will grace the rankings of the ten largest companies in the world. Whether that will be

language are “this time it’s Chinese companies, hydrogen stocks, clean energy companies, artificial intelligence companies, or

different“ something entirely different is anyone's guess. But it could also once again be commodity companies

that top the rankings in ten years' time. Which brings us to the next topic. Our expectation of rising

inflation rates over the next few years.

CV Invest Partners AG 3

Semi-Annual Comment

Inflation, the underestimated risk

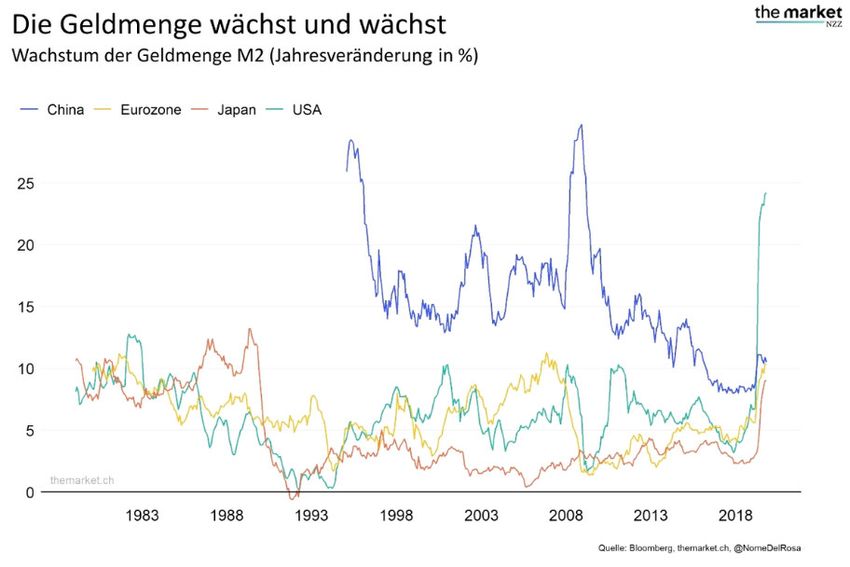

We already addressed the topic of inflation in this summer's issue. The reason for our concern was the

enormous expansion of the money supply since the financial crisis of 2008/2009, which has been

growing exponentially since this year due to the extremely loose monetary policy of various central

banks. Between March and October alone, the M2 money supply (cash, checking accounts, savings

accounts and money market funds) in the U.S. rose by almost 25%, the strongest increase in the post-

war period. In the euro area, the increase was close to 10 percent.

Source: www.themarket.ch

There is a great deal of skepticism about the theory of rising inflation rates, given that central banks

around the world began flooding the markets with liquidity as early as 2009 without inflation having

risen. But unlike today, the period between 2009 and 2019 was characterized by expansionary

monetary policy coupled with restrictive fiscal policy. Just remember Europe's austerity policies during

the euro crisis. The majority of the newly created money by the central banks seeped into the banking

system, which is why inflation showed up less in daily life and much more in financial markets and real

estate (asset inflation).

But why should things be different this time? It is the combination of loose monetary policy and

expansionary fiscal policy. Governments around the world are directly stimulating their economies by

issuing bank loans with a government guarantee and/or directly distributing checks to the population.

These measures are not going to disappear anytime soon, because the fear of sovereign over-

indebtedness doesn't really seem to interest anyone (ex: who still talks about the Maastricht criteria in

Europe?). Furthermore, additional stimulus packages such as infrastructure projects are a topic in

Russell Napier, ERIC various countries and probably only a question of time. So far, the measures taken by the states as well

„The control of money as the loose monetary policy have not yet been reflected in higher inflation rates, which is not

supply has moved from particularly surprising. In recent months, the battle has been over the threat of deflation. The sharp drop

central bankers to in the velocity of money in circulation is one indication of this. But that could soon change.

politicians. Politicians

have different goals and Governments around the world are not about to let go of their "new" powerful tool, namely direct

incentives than central stimulus, anytime soon. At the same time, the positive developments on the vaccine front are fueling

bankers. They need hopes of a foreseeable end of the COVID crisis. A cyclical recovery of the economy would be the

inflation to get rid of high consequence, as we are already seeing in China. A clear signal for central banks to reduce supportive

debt levels. They now measures. But we are firmly convinced that this is exactly what will not happen. Already in 2018, the US

have the mechanism to Fed tried to hit the brakes, with the result that financial markets plummeted in Q4. The dangerous mix: a

create it, so they will global economy recovering from the slump coupled with a monetary and fiscal policy that prefers to

create it” remain expansionary for too long rather than become restrictive too soon.

CV Invest Partners AG 4

Semi-Annual Comment

While short-term interest rates are controlled by central banks and will remain very low for the

foreseeable future, a broad-based recovery of the economy would have the effect of increasing upward

pressure on long-term rates. We are already seeing the first signs of this. For example, the yield on 10-

Sven Henrich, year U.S. government bonds has risen from 0.50% at the beginning of August to 0.90% at present. At the

Northmantrader beginning of the year, the yield was still at 1.90%. The problem of rising long-term interest rates: due to

„The global financial the exorbitant debt levels worldwide, no one can afford higher interest rates. In the USA, for example,

system is so broken it the interest burden increases by USD 110 billion for every half percent. To put this figure in perspective:

can’t even handle 1% the US Navy and the US Air Force gobble up about USD 150 billion per year. We are therefore

rates. Let’s face it: it’s all convinced that the Fed will sooner or later resort to yield curve control. This will put a cap on long-term

mirage held up by cheap interest rates, preventing them from rising further. This tool is already being used in Japan and

money. The world is in Australia.

essence bankrupt,

couldn’t handle its But low interest rates are good as long as they are not in negative territory, aren't they? The problem is

obligations without zero to that in an economic recovery fueled by expansionary fiscal and monetary policies, the risk of rising

negative rates. And since inflation increases dramatically. And just last year, in a remarkable move, the Federal Reserve

nobody has any solutions announced that they are willing to let inflation overshoot 2%. Previously, the inflation target was 2%. (As

and nobody wants to face an aside, once let loose, inflation is difficult to control.) But what does this mean for investors? For

the music they’ll stay on example, if interest rates are fixed at 2% and inflation rises to 3% at the same time, the result is a

this path for as long as negative real interest rate of 1% (interest rate minus inflation). In other words, the saver suffers a

possible” gradual loss of value. For debtors, and thus also for countries like the USA, negative real interest rates

are a blessing, as they are among the winners of such a development.

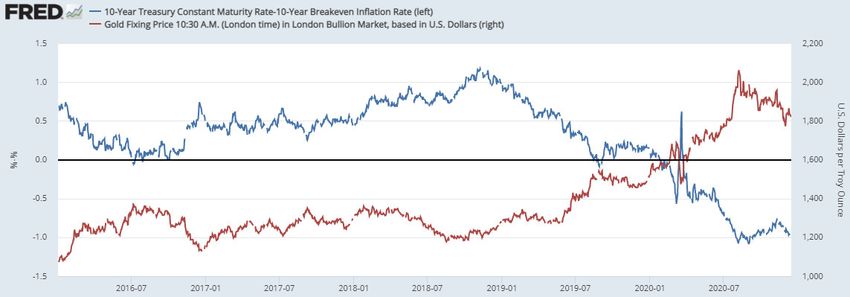

US Inflation Expectations (2016-current)

Source: St.Louis Fed

That our expectation of rising inflation rates is not so far-fetched is already evident. Since the

deflationary shock this spring, inflation expectations in the USA have been climbing relentlessly and are

currently quoted at 1.83%. According to the United Nations Food and Agriculture Organization (FAO),

food costs as much as it last did in 2014. Other signs also point to rising inflationary pressure, which

brings us to the outlook for the financial markets.

CV Invest Partners AG 5

Semi-Annual Comment

Financial Markets Outlook

Commodities are the asset class that reacts most strongly to signals on the inflation front. They have

Jeffrey Curie, made strong gains since the lows in March this year. Copper, for example, after testing the 2016 low in

Goldman Sachs Global March, has gained 80% and is now trading at its highest level in more than seven years. Wheat is

Head of Commodities trading at its highest level since 2015 and iron ore last traded this high in 2013. The economic recovery

Research in China specifically has certainly helped, as has the weak dollar (by the way: a weak dollar is also

„Every single commodity inflationary as it makes imported products more expensive for the U.S. consumer). Nevertheless,

market with the exception commodities should be watched closely.

of wheat is in a deficit

today” Agricultural Commodities and Industrial Metals 2000-2020

Source: www.stockcharts.com

In this context, the interesting chart constellation of various so-called commodity currencies should also

be pointed out. Among others, the Australian dollar and the Canadian dollar are breaking out of multi-

year downtrends to the upside.

Monthly AUDUSD and CADUSD (2000-2020)

Source: www.stockcharts.com

The chart below from Liechtenstein-based asset manager Incrementum impressively illustrates how

historically cheap commodities have become. The chart shows commodities in relation to the S&P 500.

CV Invest Partners AG 6

Semi-Annual Comment

Source Incrementum

We view commodities as well as shares in commodity companies as an attractive investment to

protect against the real risk of rising inflation rates. Moreover, commodity stocks in particular have been

neglected compared to growth stocks in recent years.

What about gold? Regular readers of our Outlook know that we have been positive for gold since the

end of 2015. Although gold has nearly doubled in that time, we still see a lot of potential. But one of the

most important questions next year will be how high long-term interest rates will rise. This is especially

true for gold investors, because rising bond yields are problematic for the precious metal unless

inflation expectations also rise. This was impressively seen this fall. While ten-year Treasury note yields

rose, inflation expectations stagnated. The result was a declining gold price.

As mentioned, we expect the U.S. Federal Reserve to "cap" the rise in interest rates. At the same time,

we expect inflation expectations to rise further. As a result, real interest rates will fall further and further

into negative territory. The chart below illustrates how strongly real interest rates influence the gold

price. American real interest rates are shown in red, the gold price in blue. In phases of rising real

interest rates, gold struggles, while gold performs very well when real interest rates are falling.

US real interest rates versus gold (2016-current)

Source: St.Louis FedCV Invest Partners AG 7

Semi-Annual Comment

As already mentioned in the last issues, we also consider shares of gold mining companies as very

interesting, especially after the correction of the last months. Besides the fact that gold miners benefit

disproportionately from an increase in the gold price, the reasons for our optimism are manifold:

After years in which the majority of managers were busy lining their own pockets, making

overpriced acquisitions and inflating debt, the picture has changed completely. Today, the

industry has less debt than ever before, dividends are constantly being increased, and

acquisitions are being made very selectively. Companies have become much more

shareholder-friendly and are focused on increasing margins and cash flows.

Operating margins are rising sharply and significantly exceed the average margin of

companies in the S&P 500.

As one of the few sectors, gold mines generate and increase positive free cash flow

In recent years, companies have divested themselves of unprofitable mines. Quality before

quantity is the credo.

Lower energy costs provide tailwind.

Last but not least: Relative to the S&P 500, gold mines are still extremely cheap

Goldminers (Gold & Silver Index XAU) relative to the S&P 500 (1984-2020)

Source: www.stockcharts.com

In 2020, stock markets have gone through a real rollercoaster ride. The sharp sell-off in the spring was

followed by an impressive rally, which, however, has only a limited connection with the economic

development, as it will still take time for corporate profits to reach pre-crisis levels. The price explosion

is mainly due to a flood of liquidity from the central banks and the lack of alternatives. In addition, there

was an enormous discrepancy between technology stocks, which were responsible for the majority of

the price gains in the indices, and cyclical stocks, which have only shown signs of life in recent weeks

are still lagging behind significantly in some cases.

Sir John Templeton once said that "bull markets are born in pessimism, awake in skepticism, mature in

Sir John Templeton optimism and die in euphoria". A number of facts speak for the fact that we are already in the last

Templeton Funds Founder phase:

and former Chairman

The market capitalization of all U.S. stocks as measured by the Wilshire 500 Index is now 1.8

„Bull markets are born on

times U.S. GDP - a record. Even at the peak of the dot.com bubble, the ratio was "only" 1.6x.

pessimism, grow on

Newly listed companies are trading at absurd prices. For example, the valuation of Doordash,

skepticism, mature on

a U.S. meal delivery company, is 120% of the total meal delivery market in the United States.

optimism and die on

DoorDash would thus have to grow 20% to command 100% of the market. Or Airbnb. At the

euphoria“

time of the IPO, the company was worth more than all publicly traded U.S. hotel chains

combined.

The success story of the so-called Spacs (Special Purpose Acquisition Vehicle) is another

example of extreme carelessness. These are shell companies with no operating business ofCV Invest Partners AG 8

Semi-Annual Comment

their own. With the money from the Spac IPO, the founder goes in search of a suitable

takeover candidate, usually a start-up company. The merger should take place within two

years. The management of such a company practically receives a blank check

The enthusiasm of small investors who bet on higher prices with call options has grown

Scott McNealy enormously. Many retail investors believe that no money can be lost with shares.

Former CEO of Sun

Microsystems, 2002 Many things are very reminiscent of the dot.com bubble. Perhaps the big euphoria is yet to come. After

all, phases of exaggeration usually last longer than expected. But it is still amazing how short-term the

„At 10 times revenues, to memory of investors is. In March, they left the market in droves, believing that the end of the world was

give you a 10-year near. And just a few months later, it seems nothing can stop them and absurd prices are being paid for

payback, I have to pay you shares in companies that haven't made a profit in years and won't do so in the near future.

100% revenues for 10

straight years in dividends. In the short term, stock markets are extremely overbought, which can be clearly seen based on the

That assumes I can get chart below. We therefore assume that the stock markets are vulnerable for a correction, which could

that by my shareholders. well be swift and severe, but which would help to reduce the already almost euphoric mood and lay

That assumes I have zero the foundation for higher prices in 2021.

cost of goods sold, which

is very hard for a S&P 500 – Short term overbought and far too euphoric

computer company. That

assumes zero expenses,

which is really hard with

39’000 employees. That

assumes I pay no taxes,

which is very hard. And

that assumes you pay no

taxes on your dividends,

which is kind of illegal.

And that assumes with

zero R&D for the next 10

years, I can maintain the

current revenue rate. Now,

having done that, would

any of you like to buy my

stock at $64? Do you

realize how ridiculous

those basic assumptions

are? You don’t’ need any

transparency. You don’t

need any footnotes. What

were you thinking?“

Source: www.stockcharts.comCV Invest Partners AG 9

Semi-Annual Comment

This is because we basically assume that the final upward wave of the upward trend that began in

2009 started in March of this year. This final wave could well take on euphoric characteristics and

extend well into 2022.

S&P 500 – Long term still potential

Quelle: www.stockcharts.com

Conclusion

The technology sector, and a few tech companies in particular, have shaped the last decade and

achieved a level of market dominance that is unparalleled. However, history teaches us that each

decade is characterized by its own theme, which leads us to conclude that in the coming years, other

companies will move up and the list of the ten largest companies in the world will look different. It

would therefore not be surprising if once again the biggest risks are in supposedly safe investments

that have been characterized by high valuation, high popularity and high outperformance over the last

few years.

A key role in the change of favorites could be played by the topic of inflation, a danger underestimated

by investors, since the last decades have been characterized by disinflation. There is a great deal of

skepticism about the theory of rising inflation rates, given that central banks around the world began

flooding the markets with liquidity as early as 2009 by means of various QE programs, without inflation

having risen. But unlike back then, not only monetary policy is expansive, but also fiscal policy.

Together with the hope of effective vaccines, this should lead to a reflation of the economy. Since

central banks are unlikely to slam on the brakes, this makes for the perfect recipe for rising inflation.

There are already signs of a turnaround: inflation expectations are rising, albeit slowly, many

commodities are already trading at multi-year highs and commodity currencies are also breaking out

of long-term downtrends. We expect these developments to continue and rising inflation rates to lead

to a (forced) rethink by many investors in the coming years.

Disclaimer

This document has been prepared by CV Invest Partners AG. It is not considered as financial analysis regarding the SBA directives aimed at

guaranteeing independence in financial analysis. As such, these directives do not apply to it. The information contained herein is based on sources

believed to be reliable, but no assurance can be given that such information is current, accurate or complete. This document is for information

purposes only and shall not be construed as an offer, invitation or solicitation to enter into any particular transaction or trading strategy. This

document does not take into account the investment objectives, financial situation or particular needs of any particular investor. Investors should

obtain individual financial advice based on their own particular circumstances before making an investment decision on the basis of the

recommendations in this document. Opinions and references to prices and yields expressed are subject to change at any time without notice. CV

Invest Partners AG may from time to time, on their own behalf or on behalf of third parties, engage in transactions in the financial instruments

described herein, take positions with, perform or seek to perform investment banking or other services for any company mentioned herein or any of

its parents, subsidiaries and/or affiliates. This document is intended only for the recipient named. It may not be photocopied or otherwise reproduced,

or distributed without the prior permission of CV Invest Partners AG. The delivery of this document to any US person shall not be deemed a

recommendation of CV Invest Partners AG to effect any transactions in the securities discussed herein or an endorsement of any opinion expressed

herein. CV Invest Partners AG may furnish upon request all investment information available to it supporting any recommendations made in this

document. This document is not for distribution to Private Customers in the United Kingdom and investments mentioned in this report will not be

available to such persons. Email transmission cannot be guaranteed to be secured or error-free as information could be intercepted, corrupted, lost,

destroyed, arrive late or incomplete, or contain viruses. The sender does not therefore accept any liability as a result. If you are not the intended

recipient of this message, please immediately notify the sender and delete this message. Any disclosure, copy and/or distribution thereof is

prohibited.

© 2015, CV Invest Partners AGYou can also read