360 Analysis of Perspectives for Crypto-assets Through a systematic assessment of elements that may influence short, mid and long-term evolution ...

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Juncker Alexandre Blockchain Quarterly – August 2021 1/40

360° Analysis of Perspectives for Crypto-assets

Through a systematic assessment of elements that may

influence short, mid and long-term evolution of their

valuation

Quarterly Review

16th Edition, August 2021Juncker Alexandre Blockchain Quarterly – August 2021 2/40

Foreword

This is the 16th edition issue of our 360° report – a series of in-depth studies started in 2017 – that is

undertaken on a quarterly basis. It tries to systematically highlight key activities and trends of

distributed ledger technologies (DLTs) globally.

In order to ensure comprehensive coverage, each issue is supported by the material contained in

previous issues, and elaborates on already-debated considerations – thereby updating views,

introducing new solutions, and going deeper into the analyses.

In the present document, we discuss research, principles and fundamental appreciations about the

cryptosphere, as a whole. This includes the latest technical evolutions, updates on applications, new

regulations, etc., for the entire span of blockchain and other DLTs. The purpose is to ultimately reach a

reasonably exhaustive understanding of crypto developments worldwide. Hence, based on this

review, the reader should gain an educated view of the direction in which the industry is evolving. In

particular, we aim to identify the current underlying forces that are driving DLT-based currencies and

token markets, in order to identify possible scenarios.

Each time, the blockchain environment is evolving, densifying and getting more complex. All

information presented herein is considered to be accurate at the time of publication, but as a

disclaimer, no warranty of accuracy is given and no liability in respect of any error or omission is taken.

Any examples used are generic and for illustration purposes only. Any forecasts, figures, opinions or

strategies set out are for information purposes only; we explicitly do not provide any kind of

investment advice in any edition of Blockchain Quarterly.

Also as a disclaimer, note that some raw information titles are sometimes directly copy-pasted from

websites without notice, and that this document is a private personal work not for sale and merely to

be occasionally shared with friends and close relationships.

We hope that you have as much pleasure reading as we had in researching.

Alexandre Juncker,

Zürich, August 2021.Juncker Alexandre Blockchain Quarterly – August 2021 3/40

Table of Content

Foreword ..................................................................................................................... 2

1. Market aspects and general update on the last 3 months ............................................ 7

1.1 Editorial: global state of the DLT ecosystem ................................................................................. 7

1.2 Comments on crypto assets markets ............................................................................................ 7

1.2.1 Prices observation ......................................................................................................... 7

1.2.2 Correlations.................................................................................................................... 7

1.2.3 Exchange volumes and liquidity .................................................................................... 7

1.2.4 Volatility .......................................................................................................................... 7

1.3 Hype level ..................................................................................................................................... 7

1.4 Interaction with macroeconomics and the global economic situation ........................................... 8

1.4.1 Looming energy crisis .................................................................................................... 8

1.4.2 Impact of fiscal and monetary policies for and post Covid ............................................. 8

1.4.3 Concretely in the short term ........................................................................................... 9

2. Review by actors ................................................................................................. 10

2.1 Governments & regulators (legal aspects) .................................................................................. 10

2.1.1 Regulation on offerings of crypto assets ...................................................................... 10

2.1.2 KYC / AML / CFT ......................................................................................................... 10

2.1.3 Taxes enforcement ...................................................................................................... 10

2.1.4 Battle between permissionless pure cryptocurrencies vs official fiats ......................... 11

2.1.5 Smart-contracts legal recognition ................................................................................ 12

2.1.6 Conclusion on Global evolution of governmental positions and worldwide regulatory

coordination................................................................................................................................. 12

2.2 Validators: miners, stakers, etc ................................................................................................... 13

2.2.1 Proof of Work miners ................................................................................................... 13

2.2.1.1 Market growth and profitability .......................................................................... 13

2.2.1.2 Material ............................................................................................................. 13

2.2.1.3 Hash power concentration ................................................................................ 13

2.2.1.4 Environmental issue – electricity consumption ................................................. 13

2.2.2 Proof of Stake stakers ................................................................................................. 14

2.3 Exchange platforms and crypto gateways .................................................................................. 14

2.3.1 Decentralized exchanges (DEX – DeFi) ...................................................................... 14

2.3.2 Off-chain crypto exchange platforms ........................................................................... 14

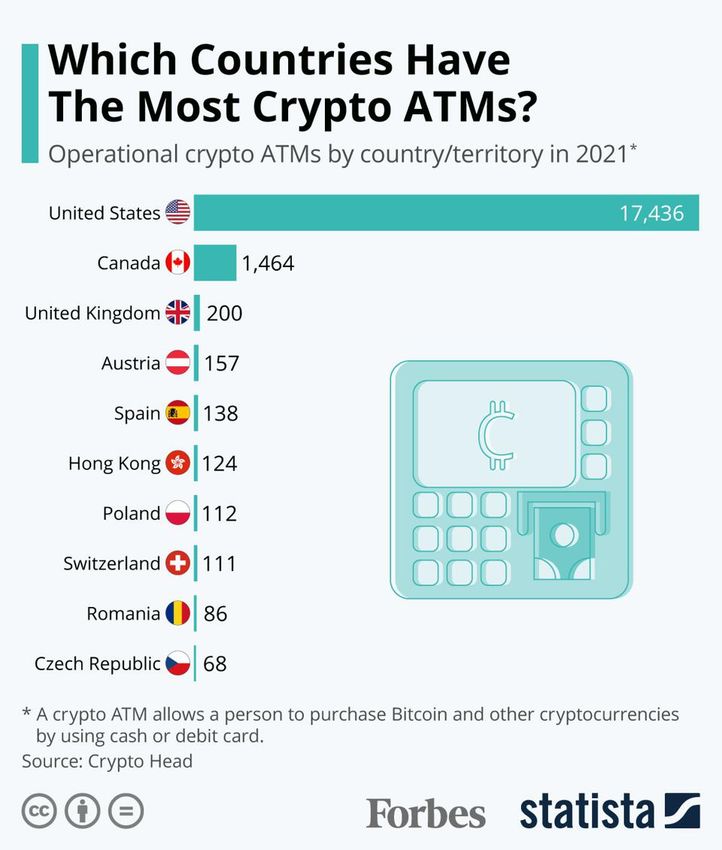

2.3.3 Crypto ATMs ................................................................................................................ 14

2.3.4 Legacy exchanges ....................................................................................................... 15

2.4 Monetary erosion ........................................................................................................................ 15

2.5 Investors/speculators .................................................................................................................. 15

2.5.1 Whales ......................................................................................................................... 15

2.5.2 Casual holders – Retail investors ................................................................................ 15

2.5.3 Liquidity providers and on-chain yield farmers ............................................................ 16

2.5.4 PE/VCs ........................................................................................................................ 16

2.5.5 Private bankers and investment / hedge funds ............................................................ 16

2.5.6 Crypto ETF................................................................................................................... 16

2.5.7 Industrial corporations ................................................................................................. 17

2.6 Service providers ........................................................................................................................ 17

2.6.1 Data and intelligence providers ................................................................................... 17

2.6.2 Auditors & business consultants .................................................................................. 17

2.6.3 Custodians and retail bankers ..................................................................................... 17

2.7 Blockchain creators, entrepreneurs ............................................................................................ 17

2.8 Universities and research centers ............................................................................................... 17

2.9 Employees – talent ..................................................................................................................... 17

2.10 Malicious actors ................................................................................................................ 17

2.10.1 Double spending – the 51% attack .............................................................................. 17

2.10.2 Market manipulations ................................................................................................... 18

2.10.3 Thefts, hacks, frauds and scams ................................................................................. 18

2.10.4 Mining malware ............................................................................................................ 18

Conclusion on the cash entering and leaving the crypto eco-system ................................................... 18

3. Sectorial and use cases review .............................................................................. 19

3.1 Banking and finance ................................................................................................................... 19Juncker Alexandre Blockchain Quarterly – August 2021 4/40

3.1.1 Investment banking ...................................................................................................... 19

3.1.2 Payment ....................................................................................................................... 19

3.2 Insurance .................................................................................................................................... 19

3.3 Supply chain ............................................................................................................................... 19

3.4 Telecommunication, Media, including social networks ................................................................ 20

3.5 Energy ......................................................................................................................................... 20

3.6 Transports ................................................................................................................................... 20

3.6.1 Aeronautics .................................................................................................................. 20

3.6.2 Automotive ................................................................................................................... 20

3.6.3 Shipping ....................................................................................................................... 20

3.7 Healthcare ................................................................................................................................... 20

3.8 Gaming & entertainment ............................................................................................................. 21

3.9 Consulting ................................................................................................................................... 21

3.10 Administration and politics ................................................................................................ 21

Conclusion on industrial applications throughout sectors ..................................................................... 21

4. Latest advancements in technology........................................................................ 22

4.1 Investment in the technology ...................................................................................................... 22

4.2 Governance and consensus modes ........................................................................................... 22

4.2.1 Centralization vs decentralization ................................................................................ 22

4.2.2 Platform governance .................................................................................................... 23

4.2.3 Consensus modes ....................................................................................................... 23

4.2.4 Consensus participation incentivization modes / tokenomics ...................................... 23

4.2.5 Hard forks .................................................................................................................... 24

4.3 Scalability (in terms of throughput rate – transactions per unit of time) ...................................... 24

4.3.1 First layer ..................................................................................................................... 24

4.3.2 Second layer - side-chains, child-chains and lightning networks ................................. 24

4.3.3 Off-chain ...................................................................................................................... 24

4.4 Confirmation time – finalization mechanisms .............................................................................. 24

4.5 Interoperability ............................................................................................................................ 24

4.6 Data management ...................................................................................................................... 24

4.6.1 Anonymity, privacy, confidentiality ............................................................................... 24

4.6.1.1 Mixers ............................................................................................................... 24

4.6.1.2 Mimble-Wimble ................................................................................................. 25

4.6.1.3 Zero-Knowledge Proof (ZKP) ........................................................................... 25

4.6.1.4 Trusted Execution Environments (TEEs).......................................................... 25

4.6.1.5 Multi Party Computation (MPC) ........................................................................ 25

4.6.2 Distributed identity management ................................................................................. 25

4.6.3 Private key management ............................................................................................. 25

4.6.4 Oracles......................................................................................................................... 25

4.7 Relationships and Synergies with other technologies ................................................................. 25

4.7.1 IoT synergy .................................................................................................................. 25

4.7.2 Artificial intelligence, machine learning ........................................................................ 25

4.7.3 Quantum computing .................................................................................................... 25

Conclusion on technical developments ................................................................................................. 26

5. Analysis by nature of DLT tokens ........................................................................... 27

5.1 A – Anonymity characteristic ....................................................................................................... 27

5.2 I – Infrastructure – native crypto assets ...................................................................................... 27

5.2.1 I(Ē) – Pure accounting infrastructure functionality ....................................................... 27

5.2.1.1 Bitcoin ............................................................................................................... 27

5.2.1.2 Litecoin ............................................................................................................. 27

5.2.1.3 XRP .................................................................................................................. 27

5.2.1.4 Doge ................................................................................................................. 27

5.2.2 (I)E – Execution environment platforms ....................................................................... 27

5.2.2.1 Ethereum .......................................................................................................... 27

5.2.2.2 Cardano ............................................................................................................ 27

5.2.2.3 Polkadot ............................................................................................................ 28

5.2.2.4 Cosmos ............................................................................................................ 28

5.2.2.5 Tezos ................................................................................................................ 28

5.2.2.6 Stellar ............................................................................................................... 28

5.2.2.7 NEO .................................................................................................................. 28

5.2.2.8 Zilliqa ................................................................................................................ 28Juncker Alexandre Blockchain Quarterly – August 2021 5/40

5.2.2.9 Avalanche ......................................................................................................... 29

5.2.2.10 Concordium ...................................................................................................... 29

5.2.2.11 Hyperledger ...................................................................................................... 29

5.2.2.12 Corda ............................................................................................................... 29

5.2.2.13 IOTA ................................................................................................................. 29

5.2.2.14 EOS.................................................................................................................. 29

5.2.2.15 TRON ............................................................................................................... 29

5.3 F – Financing, fundraising (public token sales) ........................................................................... 29

5.4 O – Ownership representation .................................................................................................... 29

5.4.1 “Securities” (in an official sense) .................................................................................. 29

5.4.2 Commodities, including precious metals ..................................................................... 30

5.4.3 Real estate ................................................................................................................... 30

5.4.4 Arts & collectibles – “NFT’s”......................................................................................... 30

5.4.5 Various commercial utilities (open combinations of profit sharing, presale, loyalty program,

membership level, exotic…) ........................................................................................................ 30

5.5 P – Payment functionality............................................................................................................ 30

5.5.1 Acceptance of cryptocurrencies (mostly BTC) in retail ................................................ 30

5.5.2 “Wrapped” cryptocurrencies......................................................................................... 30

5.5.3 Fiat pegged stablecoins ............................................................................................... 31

5.5.3.1 Tokens based on decentralized mechanisms ................................................... 31

5.5.3.2 Tokenized fiat .................................................................................................... 31

5.5.3.2.1 Central Bank Digital Currencies (CBDCs)....................................................... 31

5.5.3.2.2 Tether’s Domoclès sword ................................................................................ 31

5.5.3.2.3 Diem (ex-Libra) ............................................................................................... 31

6. Press review per country ...................................................................................... 32

6.1 Asia ............................................................................................................................................. 32

6.1.1 Japan ........................................................................................................................... 32

6.1.2 South Korea ................................................................................................................. 32

6.1.3 China (PRC Mainland) ................................................................................................. 32

6.1.4 Hong Kong ................................................................................................................... 32

6.1.5 Philippines.................................................................................................................... 32

6.1.6 Vietnam ........................................................................................................................ 32

6.1.7 Thailand ....................................................................................................................... 32

6.1.8 Singapore .................................................................................................................... 32

6.1.9 Indonesia ..................................................................................................................... 32

6.1.10 India ............................................................................................................................. 32

6.1.11 Pakistan ....................................................................................................................... 32

6.1.12 Iran ............................................................................................................................... 32

6.1.13 United Arabian Emirates .............................................................................................. 33

6.1.14 Israel ............................................................................................................................ 33

6.1.15 Turkey .......................................................................................................................... 33

6.1.16 Russia .......................................................................................................................... 33

6.1.17 Ukraine......................................................................................................................... 33

6.1.18 So-called “united” kingdom of great britain and northern Ireland ................................. 33

6.1.19 Switzerland .................................................................................................................. 33

6.1.20 Island ........................................................................................................................... 33

6.1.21 European Union ........................................................................................................... 33

6.1.21.1 Germany .......................................................................................................... 33

6.1.21.2 France .............................................................................................................. 33

6.1.21.3 Luxembourg ..................................................................................................... 33

6.1.21.4 Spain ................................................................................................................ 33

6.1.21.5 Malta ................................................................................................................ 33

6.2 North America ............................................................................................................................. 33

6.2.1 Canada ........................................................................................................................ 33

6.2.2 United States of America ............................................................................................. 34

6.2.3 Mexico.......................................................................................................................... 34

6.2.4 Bahamas ...................................................................................................................... 34

6.3 South America ............................................................................................................................. 34

6.3.1 Venezuela .................................................................................................................... 34

6.3.2 Argentina...................................................................................................................... 34

6.3.3 Brazil ............................................................................................................................ 34Juncker Alexandre Blockchain Quarterly – August 2021 6/40

6.4 Africa ........................................................................................................................................... 34

6.4.1 Marocco ....................................................................................................................... 34

6.4.2 Kenya ........................................................................................................................... 34

6.4.3 Ethiopia ........................................................................................................................ 34

6.4.4 Nigeria.......................................................................................................................... 34

6.4.5 Congos......................................................................................................................... 34

6.4.6 South Africa.................................................................................................................. 34

6.5 Oceania ....................................................................................................................................... 34

6.5.1 Australia ....................................................................................................................... 34

6.5.2 New Zealand ................................................................................................................ 34

Conclusions – mid-term considerations .......................................................................... 35

Bibliography ............................................................................................................... 39Juncker Alexandre Blockchain Quarterly – August 2021 7/40 1. Market aspects and general update on the last 3 months 1.1 EDITORIAL: GLOBAL STATE OF THE DLT ECOSYSTEM The period from May to July has been extremely delusional; after way too much and too fast growth, this has been too much of a correction. As of end of June / beginning of July, the global state of crypto has been simply disgusting, with haters and critics in power and wide spread uncertainty at virtually all levels. This all felt like very unfair, at a moment when planets were aligned and the cycle was supposed to be clear. This mood has been putting us at risk to be deterred to take the steps to understand what is going on, because the taste of the analysis was so bitter. But anyway, the best to do was to face things as they are. To try, at least. And meanwhile, during August, things have turned around significantly, hence what comes next is the big question. 1.2 COMMENTS ON CRYPTO ASSETS MARKETS 1.2.1 Prices observation In one word: what a depression. This is hard to believe that prices have been cut in 2 or sometimes in 3, 4 or more, just to stay there and fail completely to pick up during over 2 months. The technical analysis has been extremely ugly this summer. Now as of end of August, things look somewhat stabilized. The mood of fear is somewhat gone, though it is not far to be found; the trauma experienced by the variety of players should not be underestimated, as it will have impressed people a lot. It might have hardened some, and disgusted others; it exposed everyone to reality of crypto volatility, and uncertainty. Strictly speaking, a scenario “à la 2013” is still not ruled out, even if it came close of breaking it. At the end of this report, we shall study what are the likeliness and the possible extent of what we could call a “crypto-autumn”, in the sense of November 2013 and December 2017 that see huge spike before triggering terrible bear markets. 1.2.2 Correlations Recently correlation of cryptos with stocks or precious metals have gone down to negative, despite they had gone in an increasing trend during the last years. 1.2.3 Exchange volumes and liquidity Volumes have decreased to very low levels. What does it mean in this context? Probably that people have taken their side for the next weeks/months, and are not interested any more in daily surveillance… It can mean that a significant price movement is looming, but fear in which direction it might go. 1.2.4 Volatility [Nothing new to report in this section this quarter.] 1.3 HYPE LEVEL Hype is calmed down, significantly. The press is quiet again, after a peak in May on the crypto topics. It looks very much like we are in the middle of nowhere. A feeling that we never had before. Lassitude, while in the same time so much is going on, so much competition between protocols, projects, companies who still do not know what to do, regulators who also do not know how to handle it, divides in fashion to treat it by states, by bankers, etc…

Juncker Alexandre Blockchain Quarterly – August 2021 8/40 What a weird moment. Like something could be brewing. 1.4 INTERACTION WITH MACROECONOMICS AND THE GLOBAL ECONOMIC SITUATION Let’s study two major aspects of the global economy of the next years: (1) the reality of an energy supply stress on the economy; (2) the dynamic of economic activity level in the world likely given the particular post-pandemic fiscal and monetary policy context. 1.4.1 Looming energy crisis Let’s start with the energy crisis that is awaiting us. May it be artificially for climate-friendly policies, or due to physical shortage of resources on the planet (“peak oil” is now behind us), the cost of burning fossil fuels is going to increase drastically in the future. So-called sustainable means of power production are nowhere close to offering the same value, which means that we engage in a path where energy availability will shrink, at a moment when global population is still growing fast, and expects life conditions improvement. Logically, the first effect to be felt should be that the cost of operating machines will increase: gas price is already being significantly impacted, and this is merely a start. Producing machines is going to be all the more expensive, too. In practice, given the high level of mecanisation of industries (which was itself the productivity gains that allowed us to enjoy so much growth), everything will become more expensive – more scarce, in fact. Some sectors are more crucial than others: think of food production. Cement will be among the hardest hit, for different reasons, impacting housing and infrastructure constructions; traveling will be widely impaired, of course. Consequently to this mega trend, human labor will become cheaper with respect to machine work. Meanwhile, the overall output will decrease, if measured in terms of items of any thing we may want to consider. Mechanism is simple: the more energy-intensive is a product, the more expensive it shall become, hence the lower the equilibrating demand will be given the constrained offer curve. If one product is marginally free of machine work (energy), like for instance one hour of massage, then relative to the rest, this is likely to become more affordable. Logically, in order to take advantage of this, one should hence invest today into items that are energy- intensive. Bags of cement, metallic aluminum, energy storage devices, batteries. Native tokens of PoW blockchains would qualify as well, according to this point of view. From a wider macroeconomic point of view, as far as asset prices cycles are concerned, this will have long term impacts that we might want to discuss in next issue of this report. For now in the short run, crypto asset prices evolutions do not depend from it. 1.4.2 Impact of fiscal and monetary policies for- and post- Covid The second aspect to study is about reflecting what is the likely development of economic activities given the very accommodating fiscal and monetary policies conducted in response to the pandemic. Academics and observers reckon that the “sustainable” level of debt by the rich countries states might be high enough, that there is quite some margin still. In the context of pandemics and uncertainties, confidence in the states might not be too much questioned. But even if so, not all countries are in the same point, and some like Italy are much closer to potential collapse than others. Future cannot be predicted, the fate of the Wuhan’s coronavirus evolutions are uncertain. If all goes well, vaccine shall keep being efficient against further mutations, it finishes being rolled out, and we will be gradually through it at measure that countries reach collective immunity. If things go in the worst, it could be that one mutation after the others prevents reopening of borders, permanently stranding recreational businesses and crippling a number of others, forcing states to step in strongly again, stretching their monetary credibility to a breaking point… In lack of new catastrophe meanwhile (war, natural disasters, new viruses), and if central banks play their “modern role” well, we might go through with simply people accepting that goods prices have gone up, they need to go back to work to afford the same, but that is all. If the debt level of states is high, then the central bank is just buying it back issuing paper money, like they have always done. So prices of goods will have gone up, salaries will follow “reluctantly”, people on average will have gone poorer – relatively speaking – it is kind of mechanically necessary since output has been

Juncker Alexandre Blockchain Quarterly – August 2021 9/40 impaired at least punctually (but significantly). In short, the demand side has been sustained, but not so much the offer side that is in very different shapes depending the industries. If people go unemployed, it seems that the states’ logic is now to pay whatever it takes to avoid unrests. Unfortunately, this is likely to reinforce the problem in a loop. Said differently, the pending catastrophe will only accumulate steam, but it will seem OK until it blows in the form of social inequalities confrontations. Only if the offer side is built fast enough back, and people pushed to work, it could be avoided. Now, is there a risk in the stock exchange, in this context? Stock exchange crashes if the expectations of future cash flow of companies drops. In a given sector, bad business perspectives are killing; in the perspective of inflation, inflated future prices inflate stock prices on the way. Dropping consumption has immediate effect on stocks, obviously, due to dropping prices of goods. Increase of central bank interest rates has the same effect by “eating” in capital cost a fraction of the margins of companies. What we are saying is that in the near future, next 18-24 months, one can expect central banks and governments to make money available to “people who need it”; even if that makes everyone together poorer transitorily, that will push prices up, hence stocks up, hence dope the offer side. All depends on the offer side to give jobs to people. There are two path of thoughts. If central banks “play well their role” in the sense of mitigating debt crisis created by governments and in good intelligence with finance ministers, then this managed flow of liquidities shall allow people to cope with hardness and shall not prevent output to be deficient (otherwise there would not be the need for this) – but pushing prices up more than would be in a sane equilibrium situation. Still, at a given moment there will be social disequilibrium between the haves and the subsidized have-nots because assets prices will have gone up significantly. Otherwise if central banks and governments screw things up, then situation gets out of control earlier. In case of serious social unrest, there is cut of activities, which has to reflect in consumption, which impacts stock prices. Another way to wonder is, what could push prices down? Industrialization and efficiency gains are among them. Apart from robotization, data analysis is rather making things more expensive and more marketing/advertising intensive. Impoverishment of people without financial help would also; this we have ruled that out above for the short term, but in the mid term it might be difficult to sustain. Conclusion: we should expect wealth gaps to widen, and then social unrest to strengthen, leading to disruptions, themselves impacting stock prices. Meanwhile, as long as central banks pump money into people’s pockets, prices of assets including cryptocurrencies should rise. 1.4.3 Concretely in the short term In the short term, economy is picking up in USA, which is still leading the western financial mood. In practice, this means that unemployment is curbed, companies’ order books are full, and output is recovering fast. Generalized vaccination is within reach in rich countries, giving hopes. News often talk of lots of jobs finding no talent to match. Virus propagation is a chain reaction, just like in the nuclear sense. So one characteristic of it is, it cannot be very bad and very long. If it is bad, then it finishes rather fast (e.g. India), but if it is long then it does not hurt much (Western Europe). The only thing one can do is to choose one model to reach immunity: either get the disease, or get vaccination. This being said, countries who locked down completely and hence are now much more vulnerable still have significant way to go before opening. Some regions still are under heavy measures, Latin America in particular. Vaccine seem also not to be preventing so high fraction of population to get sick. Variants will continue to emerge. So we are far from out of the woods. Still, in the mid term it looks like the economy will recover, in a mostly positive dynamic, a priori masking the catastrophic situation of some other sectors. The characteristics of the dynamic itself is the thing that nobody really knows, given the unprecedented case, the huge amount of money poured, not to mention potential exogenous factors that progressed uncovered during the whole time. Federal Reserve is even considering raising interest rates if the take off confirms being too fast, and this has already been a major shock to markets at large, and cryptos in particular. There are a lot of opposite energies in the reactor, so it can be very rocky. For cryptocurrencies, the notion of increased volatility in the wide economy is annoying, because it is very sufficiently volatile itself. But then it might appear itself less volatile comparatively speaking…? Otherwise, there is a possibility that stock exchanges can hold still until end of the year. If not,

Juncker Alexandre Blockchain Quarterly – August 2021 10/40 decorrelation of crypto assets prices moves is an argument, if you want to believe in it, but an additional risk if you do not.

Juncker Alexandre Blockchain Quarterly – August 2021 11/40 2. Review by actors 2.1 GOVERNMENTS & REGULATORS (LEGAL ASPECTS) 2.1.1 Regulation on offerings of crypto assets [Also refer to the paragraph concerning Ownership crypto-asset class] Now the status for offering of crypto assets is largely clarified throughout jurisdictions. Securities are securities, commodities are commodities, real estate is real estate, art is art, and the rules that were applicable before DLTs are applicable for DLT-recorded asset ownership titles. Exotic vehicles such as 2017’s ICOs are practically cut from mainstream fundraising, which solves any problem altogether. The remainder are tokens that choose to get issued on decentralized platforms by nature cannot be prosecuted. In this case the concern of authorities may not be the so much about protection of investors, but rather about tax compliance; but this shall not be a valid ground to shut down the businesses. 2.1.2 KYC / AML / CFT There is not necessarily anything new regarding KYC / AML / CFT, all the considerations have already been exposed and reflected upon extensively in the last issues of this quarterly, but we cannot refrain from pausing a moment in front of this very central point for cryptos. KYC and tax enforcement is the easy way for public administrations to crackdown on cryptocurrencies when they want to do it and do not have any good reason or way to do so. Then the exchanges and holders are attacked as they are the weak point. There is no shortage of administrations putting pressures right now, even in a context of depressed cryptocurrencies prices. One consequence is that compliance in its complexity of global jurisdictions is getting enforced strongly on the given exchanges, and that people who want to earn money with decentralized applications do everything directly on-chain. So the fight is a fight of giants, and KYC is just the first easy battlefield. 2.1.3 Taxes enforcement Strong news of strong crypto taxes enforcement are many. Just to quote tue USA, Biden projects to earn several tens of billions USD by running more seriously after it. No surprise, as stated above! But one interesting point of view to look at is reverse: if cryptocurrencies succeed, then taxation and anti money laundering itself might have just to change. After all, the tax systems are very old and do not necessarily make any global sense. Does an added value tax make any sense? An income tax? How to enforce it when it becomes very easy for individuals to just avoid it? Could it be envisioned that states altogether become weaker because more and more things get privatized, due to the fact that states will have less and less financial means, and would deliver services and benefits as a society to which one would choose to belong or not? Clearly, not all states will willingfully go that way! The problem is on how to manage services that are “absolute”, like security/military; justice; police; legislation, etc. Healthcare, education, culture, retirement, these can be managed by non-compulsory mutuallisation bodies. Well, this is very forward looking, but just to highlight that in the big war ahead, it might not be states winning, it might be distributed applications undermining them until their scope of control de facto decreases and they are replaced by alternative societies and service providers that get funded differently. It will be a tough world, probably… But personally, we would bet on that, as our social welfare approach is under threat anyway due to shortage in resources.

Juncker Alexandre Blockchain Quarterly – August 2021 12/40

2.1.4 Battle between permissionless pure cryptocurrencies vs official fiats

Here is arguably the greatest news of the quarter: the progress of BTC as a legal tender in Latin

America. Quite an unexpected move, actually, if we recall the previous considerations in this review: so

far we had in the radar only the expected huge fight back of “big” currencies against Bitcoin.

But now, some countries, even if small ones, have decided to embrace Bitcoin as an official currency.

This is such a huge move that we have to stop and look at it very closely. We need to figure out:

- Why are those countries doing this, what they are trying to achieve? And then can these

elements be extended to other countries, to picture a wider embrace worldwide?

- What are potential consequences on the global monetary system depending on the share of

global GDP officially allowing use of cryptocurrencies?

- What are the possible consequences for cryptocurrencies prices, on the short, mid and long

term? According to which mechanisms?

- How can we project the next steps for this trend, in terms of operational risks and especially

reaction from the part of major reserve currencies states?

A nice program: two years ago we had Libra who posed nice questions too, this is of the same

magnitude at least.

So, to start with, why are those countries doing it? And first: what exactly is happening, in which

countries? El Salvador (population 6,5 millions) is in the frontline: early June, 62 out of 84 members of

parliament voted a law to make BTC a legal tender with effect in September. This has a lot to do with

the BTC-prone character of Nayib Bukele, the Salvadorian president. A lot of ink flew to comment this

event: to see how the country was trying to become a BTC hub, some fearing the pressure it should

put on the BTC network (ignoring that its local adoption is mostly thanks to a lightning network app).

The previous statu quo in El Salvador was one of no local currency existing, a de-facto dollarization,

but in principle a choice left for buyer and seller to agree on any currency of their preference to settle.

Now with the Bitcoin law, Salvadorians will be forced to accept BTC as payment medium, and this is

quite an incredible move. Subsequent, el Salvador asked the World Bank its help to deploy the BTC

adoption, but World Bank declined. El Salvador also is under discussion with IMF on a 1 billion USD

financing plan, and the BTC adoption has triggered concerns from IMF, which claims to be discussing

them with El Salvador; USA and the legacy monetary system obviously have by there a clear pressure

mean against BTC adoption by countries.

Meanwhile, other Latin American countries experience similar movements. Paraguay (population 7

millions) presents a similar bill on July 14th; it is well known that hyperinflation in Venezuela and

Argentina push populations to turn to cryptocurrencies to transact and store value; Brazil launched a

BTC ETF; lawmakers in Panama and Mexico also showed support to promote and propose a legal

framework for crypto assets, even if it did not develop so far. In the latest news, Cuba is also taking

steps to recognize BTC as a payment mean, “for reasons of socio-economic interest” (dixit the central

bank), that is recognizing a phenomenon that is already a reality anyway.

So, while there are signs of progress in various countries especially in Latin America, only El Salvador

has gone through so far, and it may remain alone for some time. People will be watching what benefits

or problems may happen there, before embracing (or not) cryptocurrencies as legal tenders.

Which leads us to precisely that: what may happen, good or bad, in El Salvador upon adoption of BTC

as legal tender in competition with USD? This is a small economy, of GDP 25 billion CHF, even if

growing. Out of a global output yearly of 80 000 billion CHF, we are talking of merely 0,03% of the

global economy. Now if we consider 20 trillion CHF of “running money supply” worldwide, and we take

this same fraction, then we reach a “need” for around 6 billion CHF worth of bitcoin. So this is really just

a drop in the ocean of even the current depressed bitcoin marketcap of 600 billion CHF. To have an

impact, it should be a country ten times bigger, and maybe a bit richer: that could be Argentina,

typically. But so, for El Salvador, their recognition per se will not move the BTC price, it can only have a

marginal stabilization effect, and only its advertising effect can play a role.

On the effects within a country like El Salvador, we can list:

- The easier remittance effect from the diaspora.

- The banking inclusion even in the countryside.Juncker Alexandre Blockchain Quarterly – August 2021 13/40

- The potential drawbacks of easier (or new channels for) money laundering.

- Enrichment by the people if price goes up; no real empoverishment if it goes down. In all cases,

large exposure to volatility in price of the crypto asset that may hurt the economy.

- Attraction of businesses linked to crypto.

- Potential difficulties to connect to legacy global monetary systems.

- Potential freedom from the USA’s monetary policy.

All of this shall depend largely from the depth of adoption, of course.

The major risk / consequence of all this is the potential construction of a BTC-based global settlement

system that would get cut-off from a USD/fiat-based existing settlement system. It will comes down

to the question of KYCs.

Then the case of El Salvador who does not have a native fiat currency is hardly so easily replicable

elsewhere where there are incumbent central banks with the attached power. Failed economies such

as Venezuela, Argentina, Cambodia, Nigeria maybe will be eligible lands, but it is rather by reason of

catastrophe than by real motivated choice.

As of end August 2021, El Salvador announces that they are building the infrastructure to support the

BTC acceptance, in particular thanks to a network of BTC ATMs to allow for the most seamless

conversion possible. A 140 million CHF fund will be also available for commerces who wish to avoid

exposure to bitcoin to immediately convert their BTC to USD.

2.1.5 Smart-contracts legal recognition

Iowa state now fully recognizes smart-contracts as legal law enforcement medium. Quite positive

comments have been expressed at that occasion.

2.1.6 Conclusion on Global evolution of governmental positions and worldwide regulatory

coordination

The situation is very mixed, torn, and overall definitely worrisome. Most autocracies consider, with

reason, that cryptocurrencies put in danger their control over their population, and democracies fail to

issue any clear opinion, except isolated threats and bad declarations. Countries with positive views are

in minority, and most if not all of them are small. Overall, with cryptocurrencies reaching their current

levels, the regulatory pressure is immense and bound to increase even more.

Let us make no mistakes. The fight of titans that is due concerns the privilege to coin money by states

versus the open approach championned by Bitcoin & co – and nothing else, the disputes over taxes,

money laundering or investors protection are only side-battles. States cannot and will not let this go

without fierce and huge resistance. It is unclear who might win in fact, because on the one hand states

have with them all the power of institutions, armies, polices, law enforcement. But on the other hand

now, this is not like in the 1990’s: cryptocurrencies will not disappear, they just cannot be shutdown –

and this is the very reason of their success. How to better stress it? The next downturn of crypto will be

due to states taking very strong measures to (more or less openly) wipe out Bitcoin. What may happen,

is that they will ultimately fail, but it will take bitcoin down, and create further opportunities to

speculate on it – that is definitely worth pointing out.

To the question of what states might do in effect to preserve their position to dictate what is money

and what is not, there is KYC and tax enforcement for sure; in democracies it seems complicated, at

least out of a state of emergency, to forbid the ownership and commerce of cryptocurrencies. But if

things go bad, it might very well come, so we should be cautious of acknowledging whenever

countries arrive in such situations, like Turkey has already (and even if El Salvador shows that it can go

either way!). Then, forbidding mining activities out of the excuse that it pollutes is also a big threat, but

difficult to enforce in democratic courts still. So in the short term, what will happen is a question of

legislative fight in democracies, and executive imposition in autocracies.Juncker Alexandre Blockchain Quarterly – August 2021 14/40 2.2 VALIDATORS: MINERS, STAKERS, ETC 2.2.1 Proof of Work miners 2.2.1.1 Market growth and profitability Consequent to disappearance of large mining facilities in China, the hashrate of Bitcoin collapsed by half (180mTh/s in mid-May to 86 early July). Even if news of emergency shipments to alternative locations have been reported, and hence there is hope for relatively quick ramp-up back of the hashing power, the shock has been a particularly rude one, including difficulty adjustment back down by the protocol. We have gone down back to the summer 2019 level, so that is two years hashrate progression erased in shocking few weeks. The short-term consequence is that for operators established out of China, the business enjoys a boom in profitability. In the same time, as the production cost of Bitcoin has been cut in two, it does explain at least part of the price crash of BTC and other cryptos. On the mid-term, relocated mining rigs (for the ones that can afford it) may be forced to operate at a premium cost of electricity, so supposing that most of the hashing power comes back on line in the next weeks, it shall bring back difficulty to roughly its previous level, but with a somewhat higher production cost. This, all the more that the pressure for “clean” origin of energy is high on the industry: a comparatively higher cost to support with respect to coal energy. Curve of hash power seems to have bottomed now. It is hard to see it going even lower than that, and miners’ cash needs might also come to some end sooner than later, so that this mess of selling pressure is behind us. Because let’s reckon it: the May-June dip is probably mostly due to miners movements and demonstrate that hashrate and price in effect always move together. As of end of August, the hashrate has somewhat recovered and is fluctuating between 120 and 150 Th/s. This is still 25% lower than before the events, but up some 75% since the low level of June. If one consider the instantaneous minimum of as law as 52TH/s, this is almost a tripling of the mining power – mostly showing, again, the violence of the shock that called for a fast rebound. Difficulty adjustment also climbs back. Blockstream, a mining company, has merged with a special acquisition vehicle, bringing it on the public stock exchange with a valuation of 3 billion CHF. In the middle of the mining migration, this is presented as a success; but compared to big mineral mining companies (counting in the hundreds of billions), this remains a reasonable size for a company. 2.2.1.2 Material For Chinese players, this unprecedented attack has been devastating. Gigawatts of machines have been unplugged, many of which are still in hangars due to the lack of suitable electricity sources anywhere on the planet. ASICs production is halted; the market passed from tense supply chain to huge overcapacity, overnight. 2.2.1.3 Hash power concentration With crack down on crypto mining in China, one consequence at least is the complete disappearance of the Chinese concentration of hash power (estimated at 65% in April). All in all, the fact that China hardly can do any damage any more now is sort of good news. A regime change would be now just an opportunity, just as it would be if India opens up. 2.2.1.4 Environmental issue – electricity consumption It is like for plane transport vs automotive transport: safety pressure is much higher for planes, so the fact that they forced to so high standards helped. Same here for sourcing of energy: crypto mining is forced to become the cleanest and it will be an asset on the long run.

You can also read