A CAPTIVE PRIMER: WHAT THEY ARE AND HOW THEY WORK - EDUCATE - EVALUATE - ELEVATE - INLIGHT RISK MANAGEMENT

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

A Captive Primer:

What they are and how they work

Educate – Evaluate – Elevate

2018

1

Do It Right, Or Don’t Do It At All

At Elevate, we passionately believe in what we do. We are conservative and

focus on insurance, risk financing, and risk management strategies to mitigate

your risk over the long term.

It’s imperative you understand the captive strategy and how it works for your

organization – we do not believe in a “one size fits all” captive approach.

This presentation is a summary only and not a replacement for a full captive

feasibility study. Nothing contained in this presentation should be deemed an

offer to sell insurance or offer legal or tax advice.

2

Elevate Captives

Jerry has over 34 years experience in the insurance and alternative risk transfer

industry and serves as CEO for Elevate Captives. In his position with Elevate, he

is an approved captive manager in multiple jurisdictions, both onshore and off.

Jerry is the Founding President of the Oklahoma Captive Insurance Association,

member of the Captive Insurance Committee of the Self Insurance Institute of

America (SIIA) and is an active speaker with industry trade groups. Jerry is an

accredited Associate in Captive Insurance with ICCIE and an Adjunct Professor

with Clear Law and Lawline.

Ryan serves as Managing Director of Risk Management for Elevate Captives.

Ryan performs the Elevate “CORE™ Review” for clients and his experience

includes being the Director of Risk and creating captives for Boing, Whirlpool,

and Koch Industries.

Ryan has participated on many insurance and reinsurance company advisory

boards and is a frequent speaker at RIMS (Risk & Insurance Management

Society) and CICA (Captive Insurance Company Association), where he currently

serves on the Board

3

What Are We Talking About Today?

A Little About Elevate

ü Create/manage captives to provide

long-term solutions for enterprise

risk management A Lot About Captives

ü Domiciles: Arizona, Delaware,

Hawaii, New York, Oklahoma, ü History

Texas ü Types

ü Our goal is to provide the best ü Structures

captive administrative service in ü What they’re used for (and what

the industry and to do so with the they shouldn’t be used for)

highest integrity ü Who makes a good captive

candidate

ü The captive formation process

Captive Examples

ü Single Parent with Mixed P/C

and Employee Benefits

ü Expense Profile

4

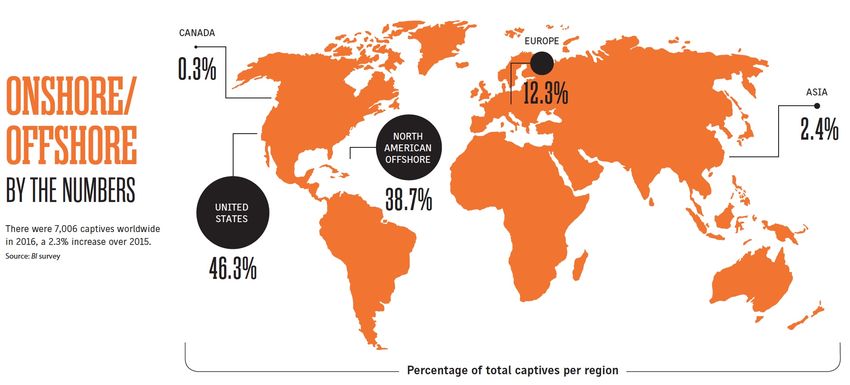

Onshore/Offshore Captives

as of 12.31.16 (Business Insurance)

7,006

CAPTIVES

WORLDWIDE

5

Captive’s Ranked by State

as of 12.31.16 (Business Insurance)

6

Definition/History of Captives

Definition by Captive.com: A captive insurer is generally defined as an insurance

company that is owned and controlled by its insureds.

Captives first used in 1700’s in Europe

Ø Lloyd’s Café (the ship-owners meeting…thereby creating Lloyd’s of London)

Ø Apple ($99 AppleCare)

Ø Federal Express (”check the box”)

Ø Allstate (Sears)

Three main markets that host captives:

Ø Europe (Isle of Man, Guernsey, Luxembourg, etc.)

Ø Offshore Financial Centers (OFC’s – Bermuda, Cayman, Nevis, etc.)

Ø USA (Vermont, Delaware, North Carolina, etc.)

Ø Over 7,000 captives worldwide and growing rapidly

30+ states currently have captive legislation:

Ø In US, first captive formed for “captive” coal mines named/owned by Fred Reiss, an

insurance agent in Ohio in 1951

Ø Delaware/Vermont have over 1,000+ each

Ø Most have specialties like series captives, medical stop-loss, XXX and AXXX

7

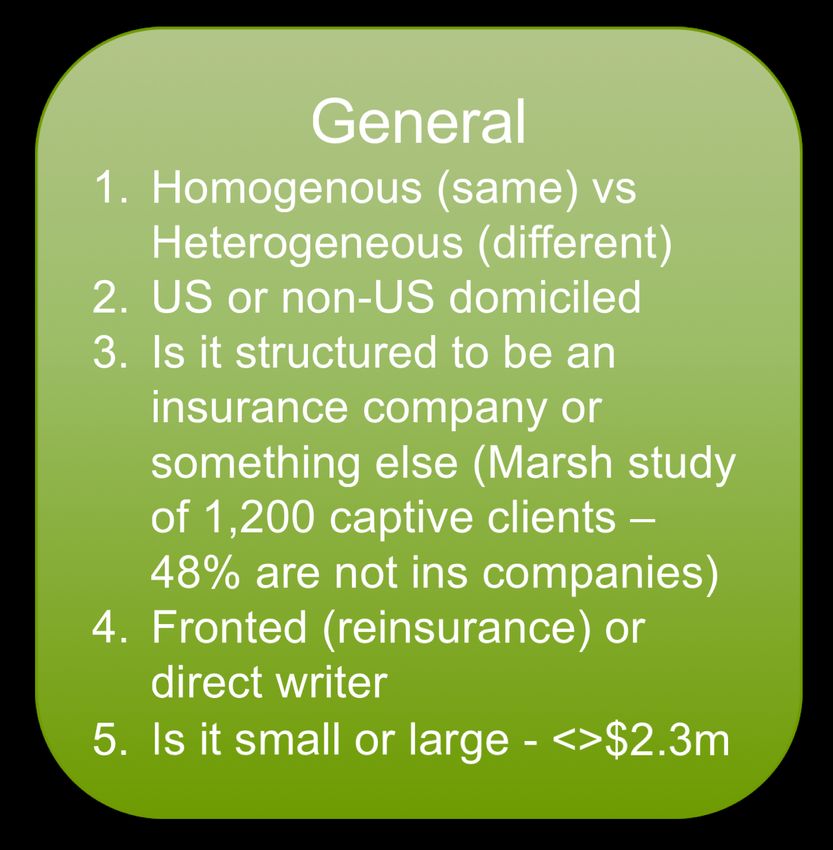

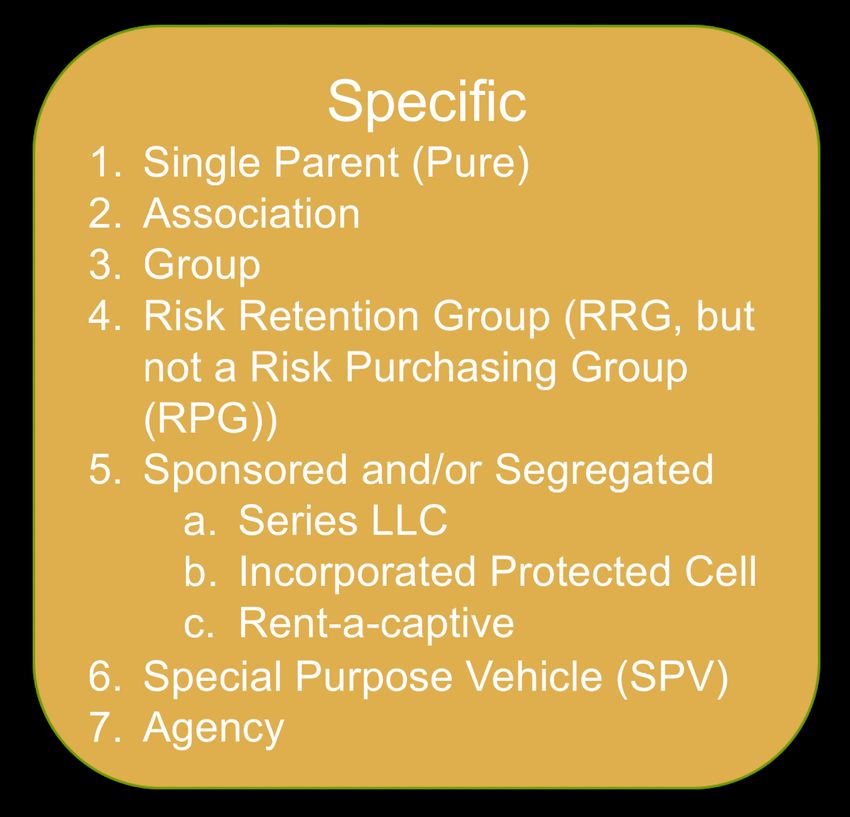

Mix and Match Types of Captives

“Small, fronted, protected cell, US-based, homogenous group captive”

8

2 Most Common Captive Types

• Single Parent Captive: A single owner for whom the captive provides

insurance protection. Also known as a “Pure Captive” representing over

60% of all captives. Can also be a protected cell or series captive

insurance company.

• Group Captive: Formed by a group of individual companies that

typically own the captive. A group captive can also be started/owned by

an association (aka “Sponsor”) and come in the form of a risk retention

group (RRG), reciprocal group captive, or group reinsurance captive

where a fronting company is involved.

9

The Large Captive

Over $2.3m in Premium

(The limit is indexed to inflation or $50,000, whichever is less)

Historically, a “large captive” has been defined as anything over the limit within the

831b election (currently $2.3m). You typically see these as single parent (pure)

captives owned by medium-to-large companies or some smaller-to-medium sized

businesses. For example, a $150m company writing a large workers compensation

deductible reimbursement policy or large healthcare systems writing medical

malpractice and general liability.

What are some of the benefits? The same as a Small

Captive, plus:

ü You tend to have greater flexibility in writing on a direct basis

ü You can take advantage of a net-operating-loss carryforward

ü All expenses, including administration, risk management, and any

claims themselves, are deductible within the captive, thereby

allowing for the potential of the premiums paid and all operating

expense to be deductible

10The Small Captive

Under $2.3m in Premium

A captive is a real insurance company the insured ultimately owns and controls. The

small captive model can be used for low-frequency/ high severity risk.

The captive also exists to cover gaps in commercial policies while protecting against

risk where no coverage exists at all. It doesn’t replace the commercial insurance

program, it ENHANCES it.

What are some of the benefits?

ü It creates significant SAVINGS on commercial premiums

ü Allows for GREATER protection using difference-in-conditions polices

ü The underwriting profit is not taxed, thereby allowing an accelerated

build-up of surplus. This allows you to take even more risk down the

road.

11Small or Large - Key Ingredients

Legitimate

Business

Reason

(Real Risk)

Pay Claims (Formal Legitimate Asset Investment

TPA Process)

Domicile Credibility

Adequate Capital What is a

Must Have

Captive Must Have

Transfer Insurance Distribution

Company?

Quality Reinsurance

Legitimate Governance

Credible Service Providers –

CANNOT Conservative Parental

be just for

actuary, tax, audit, legal, Tax Guarantees or Loan Backs(?)

captive manager Benefit!!

12The 831b Tax Election

The IRS provides a special election for insurance companies

collecting less than $2.3m in premium…it’s known as the 831b

election.

Ø Any underwriting profit is not taxed (only taxed on investment income)

Ø Designed for low frequency/ high severity risk models

Ø Captive assets may be invested per regulatory guidelines

Ø It does have limitations: No NOL carry forward, no claim or operating expense

deductions (except expenses related to investments)

Ø Effective May 1, 2017, certain captives and their owners that elect 831b tax treatment

must disclose this interest as a Transaction of Interest and file Form 8886

Ø This election is only considered after all aspects of the risk have been reviewed, not

before

In our opinion, the 831b election has been abused by certain promoters that

exclusively push the tax benefits of the captive. They are not focused on the

insurance and risk management aspects of the captive and they will not stand up

to audit.

13Benefits, Uses, and

Coverage

Educate – Evaluate – Elevate

14What We Hear…

I keep paying premiums year-after-year and NEVER

have any claims…

I know if I turn these small claims in, I’ll be cancelled or

they’ll raise my premiums, so I just pay them out of my

pocket…

On the one claim I did turn in, they denied it, so why

pay for insurance…

The quote seemed really expensive and I don’t

typically have claims anyway, so…

15Who can benefit from a Captive?

Those who have strong financial statements and wish to have ultimate control

over their insurance and risk management programs – “Seller of Risk”

Those who have a clear understanding of their own risk & loss history:

Ø Sufficient operational exposures (employee benefits, fleets, property, business interruption,

supply chain, etc.)

Ø Quality exposure and loss data (or ”shadow price”) demonstrating profit over time

Ø Strong financial statements showing sufficient net income

Ø Committed to risk management and cost containment programs

Owners committed to paying appropriate premiums for multiple years:

Ø Captives are seldom short-term solutions

Ø How much is the minimum? About $400,000 captive premium due to the fixed expense ratio.

Those wanting ultimate control over:

- Consistent Premium - Underwriting Profit

- Claims Management - Investment Return

- Risk Management - Cost Containment Programs

16How is a Captive Used?

Deductible Reimbursement & Difference in Conditions (DIC):

Ø Raise deductibles and retentions to retain more profit & cut commercial insurance

premiums

Ø DIC - covers exclusions, deductibles & excess protection with your commercial

policies

Risk that is too expensive, not available in the commercial market, or is currently

uninsured (whether you know it or not):

Ø Medical Stop-loss

Ø Property, Hurricane (Named storm), Wind, Flood, DIC

Ø Key Contract/Key Employee (expense reimbursement)

Ø Business Litigation, Business Income (Interruption)

Ø Product Recall, Reputation, Crisis Management

Ø Employee Related Practice Liability/Directors & Officers

Ø Supply Chain Risk

Enhance business planning (Enterprise Risk Management)

17Risk Financing Continuum

HIGH

Cell or Single Parent Captive

• Complete assumption of risk on

primary layer

What happens to the premium

• Subject to Regulatory Oversight

as the retentions go up?

Group Captive

Program Control

• Pooling of Risk with Participants subject

to Corporate Governance

Deductible Policy

• Significant/complete risk assumption in exchange

for deductible credit

Retro Policy

• Assumption of limited risk in exchange for potential return premium

• Deferred “pay-in” premium

Guaranteed Cost

• Complete transfer of risk

• Commercial insurance with little-to-no deductible

LOW HIGH

Financial Control

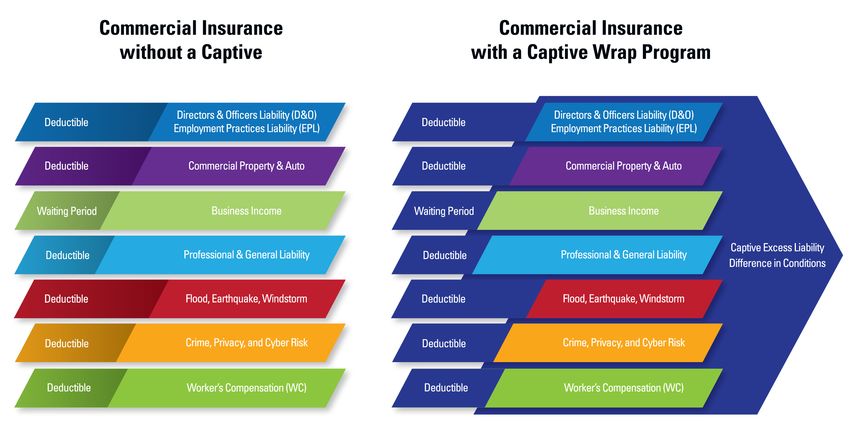

18The Captive Wrap Program™

Stand-alone and Difference-in-Conditions Policies

19Coverage Examples

Medical Stop-loss Political Risk

Professional Liability DIC* Coverage HIPAA/Billing Audit Liability

Contractual Liability Cyber Liability

Business Litigation DIC Business Interruption/DIC

Environmental Liability/Excess Employment Practices/DIC

Labor Strike Reimbursement Employee Dishonesty

Patent Infringement/Intellectual Property General Liability DIC

Property Management Professional Professional Misconduct

Errors & Omissions Liability DIC Administrative Actions

Product Liability/Recall DIC Directors & Officers Liability

Loss of Key Employee Wind Deductibles on Property

Wage & Hour Liability Inland Marine DIC

Credit Default Trade Credit

Medical Malpractice/DIC Regulatory Change

Subcontractor Performance “Fat Finger” Insurance

Reputational Risk Adverse Party Legal Risk

*Difference in Conditions

20Stop Loss

Insurance

Funding Medical Stop Loss

Captive Layer

Self-Insured

5315%(

Retention

Savings

Medical(

Stop(Loss(in(

How it Works Captive

Ø Medical stop loss may be funded in a captive as a direct reimbursement policy, or as

reinsurance behind a regular carrier (“fronted”)

Ø The captive layer typically sits above a self-insured retention of $25 - $100K

Ø Specific and aggregate stop loss may be purchased above the captive layer to cap losses

Ø Captive layers are often funded at 125% of expected losses, based on an actuarial calculation

Ø Employer may fund the captive layer with their own funds and avoid complicated ERISA issues

(by using employee funds, but not applicable in Hawaii)

Ø Purchasing stop loss from a captive insurer is functionally the same as from a commercial

insurer and can be structured to have no impact on plan participants

Ø Employers with smaller populations can participate in a group medical stop loss captive

Ø Subject to regulatory approval, medical stop loss policies may be funded in existing P&C

captives

21What Do the Structures

Look Like?

Educate – Evaluate – Elevate

22International Risk Insurance Company (IRIC)

Delaware-domiciled Series Captive Insurance Company (SCIC)

IRIC

Contractual Relationship “Administrative Core”

Series Captive “A” Series Captive “B” Series Captive “C”

Min $100k Capital Min $100k Capital Min $100k Capital

Own FEIN

Own Board

Own Assets

23Single Parent (Pure) Structure

Why a holding company?

1. Not regulated, so no

NAIC bio or D&O issues

Holding 2. Flexible ownership

Company changes

Ownership of 3. Used in ”Golden

Holding Company Handcuff” structure

will typically mirror 4. Some cash flow benefits

Insurance

that of Insured

Company

Insured

24Group Captive with Fronting Company

Funding Model

Three Funding

Capital Loan Repayments Phases:

1. Feasibility

or Dividends 2. Statutory Capital

3. Growth Capital

Insured A

Capital Holding

Insured B Loans or Company

Investments

Insured C

100% Capitalization Surplus Note

Fronting Group Captive

Premium Company (Insurance Company)

25Captive Examples and

Expense Examples

Educate – Evaluate – Elevate

26Single Parent Captive Example

(Mixed P&C – Stop Loss)

Commercial renewal in 2013

(without a captive):

• $840,000 premium

Holding Company

• $250k SIR on commercial policy Coverage Examples

• Fully-insured on health plan

• Multiple gaps/exclusions

Loss of Key Contract Reputational Risk

Commercial renewal in 2017 Captive with

(with a captive): Hedge Fund E&O Loss of Key

$250,000 in

• $515,000 premium DIC Employee

Statutory Capital

• $500,000 SIR on commercial

“Fat Finger” Network/Cyber

policy Endorsement Liability

• $30,000 Spec Ded ($10,000

excess $20,000 in captive)

EPLI/D&O Crisis Management

• $1m DIC limit with Zero SIR in

captive

• $5.3m in captive assets Business

Business Litigation

Interruption

• $4.3m in premium deductions

• $325,000 in annual premium

savings, $1.6m total so far 27Reinsurance - Why you might need or want it

Ground-up Quota-share

Purpose 1M Limit –

Ø Protect captive against Quota-share

significant loss

Ø Preserve capital 49% 51%

Your Captive of of

Ø Risk transfer

prem. prem.

Ø Risk distribution kept in for

51% of the 51% of

Structure Premium/Risk Captive Limit

Ø Quota-share

Ø 49/51% Ratio

Ø 2.5% Cost Reinsurance

Captive

Participants

Captive

Participants Captive

Participants

285-year Financial Overview

Pure Captive with Reinsurance

Available

Loss Ratio Paid Claims

Captive Assets

5% 486,500 10,028,386

• Expense ratio should be much lower than commercial at 35%+

25% 2,342,500 7,917,147

• Reduction in commercial premium due to retentions (10-20%+)

• Claims are paid to owner (they do not come out of your cash flow) 50% 4,685,000 5,278,098

• Highly efficient regardless of tax election 80% 7,496,000 2,111,239

This table reflects a 35% loss ratio, 2% ROI, WITH reinsurance:

Year 1 Year 2 Year 3 Year 4 Year 5 Total

Premium 2,000,000 2,000,000 2,000,000 2,000,000 2,000,000 10,000,000

Admin/Operational (est.) 75,000 75,000 75,000 75,000 75,000 375,000

Reinsurance 51,000 51,000 51,000 51,000 51,000 255,000

Paid Claims 655,900 655,900 655,900 655,900 655,900 3,279,500

EBITDA 1,218,100 1,218,100 1,218,100 1,218,100 1,218,100 6,090,500

Investment Inc (net of tax) 48,724 99,397 152,097 206,905 263,905 771,027

Net Profit 1,266,824 1,317,497 1,370,197 1,425,005 1,482,005 6,861,527

Available Captive Assets 1,266,824 2,584,321 3,954,518 5,379,523 6,861,527 29Actual Claim Examples

Ø Wage & Hour: $480,000 due to allegations the insured didn’t follow strict

guidelines on breaks, lunchtimes, and overtime rules. Excluded from

commercial EPLI/D&O policy.

Ø Trade Credit: $260,000 due to large client (of the insured) filing bankruptcy and

continuing to use security services. Insured’s IT system failed to flag

nonpayment’s. Commercial policy declined claim due to “prior acts” date on

policy.

Ø Reputational Risk (Headline): $63,000 due to homicide investigation of elder

death. Nurse falsified medical records. Hiring of PR firm not covered under

General Liability policy and claim denied due to ”actual or alleged” wording in

commercial policy.

Ø Sexual Abuse Allegation: $140,000 due to defense of Owner by previous

employee alleging sexual abuse. Commercial carrier declined due to retro-date.

Defense verdict and insured fully reimbursed.

30Risk and Insurance Review

Process & Foundations

Educate – Evaluate – Elevate

31Elevate CORE™ Review

Coordinated Overview

of Risk and Exposure

32The Captive Creation Process

Step I: Step II: Step III:

CORE™ Regulatory Funding &

Process Filing COA

Insurance Regulator Receipt of Cert

review discussion of Authority

Actuarial rates Corporate Capitalize

structure

Captive lines of creation Fund Premium

insurance

Bank accounts Policy Issuance

Loss projections

Investment plan Implement

Domicile and investment plan

Service provider Business plan

Governance

Go/no go File plan

30 Days 15 Days 30 Days

33Questions and Answers

Our family is blessed to do what we do, and we love doing it.

Thank you for allowing us to visit with you today.

Jerry D. Messick, ACI

CEO

Elevate Captives

M: 405.550.2651

jm@elevatecaptives.com

34You can also read