ABACC - Accounting & Tax Update - Fran Brown, Partner Dave Moja, Partner CapinCrouse LLP

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

ABACC – Accounting & Tax Update Fran Brown, Partner Dave Moja, Partner CapinCrouse LLP

Accounting & Financial Reporting

ASUs We Will Be Covering Today • 2014-15 Going concern • 2015-01 Extraordinary items • 2015-03 Debt interest • 2015-11 Inventory • 2016-18 Restricted Cash • 2017-02 Consolidation guidance • 2017-07 Compensation retirement benefits

ASUs We Will Be Covering — At a High Level • 2016-14 NFP Financial Statements • 2016-02 Leases • 2014-09 Rev rec • 2015-07 NAV disclosures • Proposed ASU – Grants and Contracts

ASU 2014-15, Disclosure of Uncertainties about an Entity’s Ability to Continue as a Going Concern

Disclosures

• Disclosure is required when “substantial

doubt” exists

• “… when conditions and events, considered in the

aggregate, indicate that it is probable that the entity

will be unable to meet its obligations as they become

due within one year after the date that the financial

statements are issued…”

• Current auditing standards don’t give a definition of

“substantial doubt”

Triggers

Other

Negative indications

Internal External

financial of

matters matters

trends financial

difficulties

Time Horizon

3/1/20X3

• FASB Requirement:

12/31/20X2 One Year from

FS Issuance Date

• Prior Auditing

3/1/20X2 Standard

Requirement: One

• FS Issuance Date Year from Balance

12/31/20X1 Sheet Date

• Balance Sheet DateDisclosures

• Principal conditions or events

• Management’s evaluation

• Management’s plan

• Statement that there is “substantial doubt”

about the entity’s ability to continue as a going

concern

• This is only necessary when management’s plans

do not alleviate concernEffective Date • For annual periods ending after December 15, 2016 • How does this impact debt covenant waivers?

ASU 2015-01, Eliminating the Concept of Extraordinary Items

OLD RULES – Extraordinary Items • Criteria to be met to qualify as extraordinary: • Unusual in nature • Infrequency of occurrence • Both had to be met

NEW RULES – Nothing • Does not exist

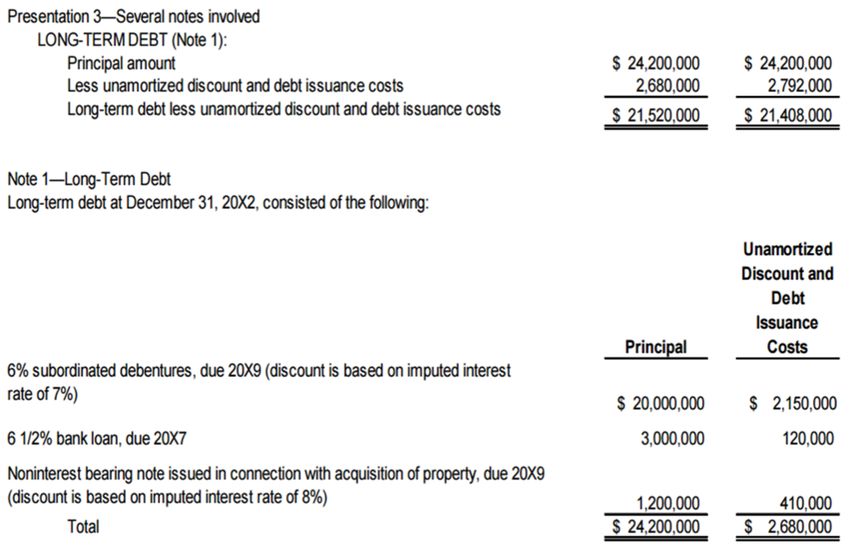

ASU 2015-03, Simplifying the Presentation of Debt Issuance Costs

Update

Debt issuance costs

related to a recognized

debt liability should be Recognition and

presented in the measurement guidance

balance sheet as a for debt issuance costs

direct deduction from are not affected

the carrying amount of

that debt liabilityEffective Date • Effective for fiscal years beginning after December 15, 2015

ASU 2015-11, Simplifying the Subsequent Measurement of Inventory

Concepts • Measure inventory at the lower of cost and net realizable value • Net realizable value is the estimated selling price in the ordinary course of business, less reasonably predictable costs of completion, disposal, and transportation • Not in scope – LIFO or Retail Inventory Method

Effective Date • Fiscal years beginning after December 15, 2016 • Prospective application

ASU 2016-18, Restricted Cash

Update • Statements of cash flows explain the change during the period in the total of cash, cash equivalents, and amounts generally described as restricted cash or restricted cash equivalents • Transfers between cash, cash equivalents, and restricted cash or restricted cash equivalents are not reported as cash flows activities • Disclose in a narrative or tabular format the amounts, disaggregated by line item, that sum to the total amount shown in the SOCF

Effective Date • For fiscal years beginning after December 15, 2018

ASU 2017-02, Clarifying When a Not-for-Profit Entity That Is a General Partner or a Limited Partner Should Consolidate a For-Profit Limited Partnership or Similar Entity

Update

• This ASU was issued to clarify when a NFP that is

the General Partner or a Limited Partner should

consolidate a For-Profit Limited Partner or similar

entity

• Retains the consolidation guidance that was in

Subtopic 810-20 for NFPs by including it within

Subtopic 958-810

• Adds guidance to Subtopic 958-810 on when an

NFP limited partner should consolidate a for-profit

limited partnershipEffective Date

• Fiscal years beginning after December 15, 2016

• NFPs need to adopt ASU 2017-02 at the same time

they adopt ASU 2015-02 and should apply the same

transaction method elected for the application of

ASU 2015-02

• For NFPs that have already adopted 2015-02, will

need to be applied retrospectively for all relevant

periods beginning with the fiscal year in which

2015-02 was initially appliedASU 2017-07, Improving the Presentation of Net Periodic Pension Cost & Net Periodic Benefit Cost

Update

• Requires that an employer report the service cost

component in the same line item or items as other

compensation costs arising from services rendered by

the pertinent employees during the period

• The other components of net benefit cost are required to

be presented in the income statement separately from

the service cost component and outside a subtotal of

income from operations, if one is presented

• Only the service cost component is eligible for

capitalization when applicable (for example, as a cost of

internally manufactured inventory or a self-constructed

asset)Effective Date • Fiscal years beginning after December 15, 2018

ASUs We Will Be Covering — At a High Level • 2016-14 NFP Financial Statements • 2016-02 Leases • 2014-09 Rev rec • 2015-07 NAV disclosures • Proposed ASU-Grants and Contracts

ASU 2016-14, NFP Financial Statement

Final Words

• Implementing the ASU can take longer than you

think

• Start working on Expense Analysis by natural and

function and work through the format issues sooner

rather than later

• Assess your cost allocation methods – contact IT now if

you currently don’t allocate

• Attempt to construct the Board Designation before

doing the Liquidity & Availability disclosures

• Beginning sooner rather than later will make final

implementation so much easier.ASU 2016-02, Leases

Update

Recognition &

Lease Classification

New Definition Measurement

of a Lease Finance Lease

Right of Use Asset

Operating Lease

Lease Liability

Subsequent Short-Term Lease

Measurement ExceptionEffective Date

NFP entities that have issued, For All Other Entities

or are conduit bond obligators

for, securities that are traded,

listed, or quoted on an

exchange or an OTC market

Fiscal years Fiscal years

beginning after beginning after

December 15, 2018 December 15, 2019ASU 2017-09 Revenue From Contracts with Customers (“Topic 606”)

Scope

• This FASB ASU applies when an entity

• enters into contracts with customers to

transfer goods or services; or

• enters into contracts for the transfer of

nonfinancial assets

• Unless those contracts fall within the scope

of other standards, such as insurance, lease

contracts, or guarantees within the scope of

Topic 460Overview

Addresses

concerns Supersedes

regarding or amends

Joint Creates a

the existing

convergence new Topic in

complexity revenue

project the

and lack of recognition

between the Codification

consistency requirement

FASB and the

surrounding ASC 606 s (will

IASB

the replace ASC

accounting 605)

for revenueOverview (continued)

Eliminates

Avoids

transaction Provides more

inconsistencies

and industry- useful

Provides a of accounting

specific information

principles- treatment

revenue through

based across

recognition enhanced

approach different

guidance disclosure

geographies

under current requirements

and industries

GAAPGuidance • Recognize revenue to depict the transfer of promised goods or service to customers in an amount that reflects the considerations to which the entity expects to be entitled in exchange for these goods and services

Key Terms

Transfer Amount

Reflects

Transfer of promised consideration

goods and services expects to receive5-Step Process 1. Identify contracts 2. Identify performance obligations (PO) 3. Determine transaction price 4. Allocate transaction price 5. Recognize revenue when PO is satisfied

Application for Recognition Steps to apply the core principle:

Implementation Guidance

• Performance obligations • Licensing

satisfied over time • Repurchase agreements

• Methods for measuring • Consignment arrangements

progress

• Bill-and-hold arrangements

• Sale with a right of return

• Customer acceptance

• Warranties

• Disclosure of disaggregated

• Principal versus agent revenue

considerations

• Customer options for

additional goods or services

• Customers’ unexercised

rights

• Nonrefundable upfront feesConsiderations for NFPs • Contributions (out of scope) • Bifurcation (combination of exchange and contribution) • Membership Dues • Tuition and Fees • Licenses and Royalties

Effective Date

• For a public entity (including NFP entities that

have issued or are conduit bond obligors for

securities that are traded, listed, or quoted on

an exchange or OTC market)

• For annual reporting periods beginning after

December 15, 2017

• For all other entities

• For annual reporting periods beginning after

December 15, 2018AICPA Rev Rec Task Forces

• The AICPA has formed 16 industry task forces to help

develop a new accounting guide on revenue recognition

that will provide illustrative examples for how to apply

the new standard — one is for NFPs

• Implementation issues — finalized and included in AICPA

Revenue Recognition Guide:

• Tuition and housing revenues for NFP higher eds

• Contributions

• Bifurcation of Transactions Between Contribution and Exchange

Components

• Implementation issue — out for exposure

• Subscription and membership duesASU 2017-07 Disclosures for Investments in Certain Entities That Calculate NAV (or its equivalent)

Update • Removes the requirement to categorize within the fair value hierarchy all investments for which fair value is measured using the net asset value per share practical expedient

Effective Date

• Retrospective application

NFP Entities

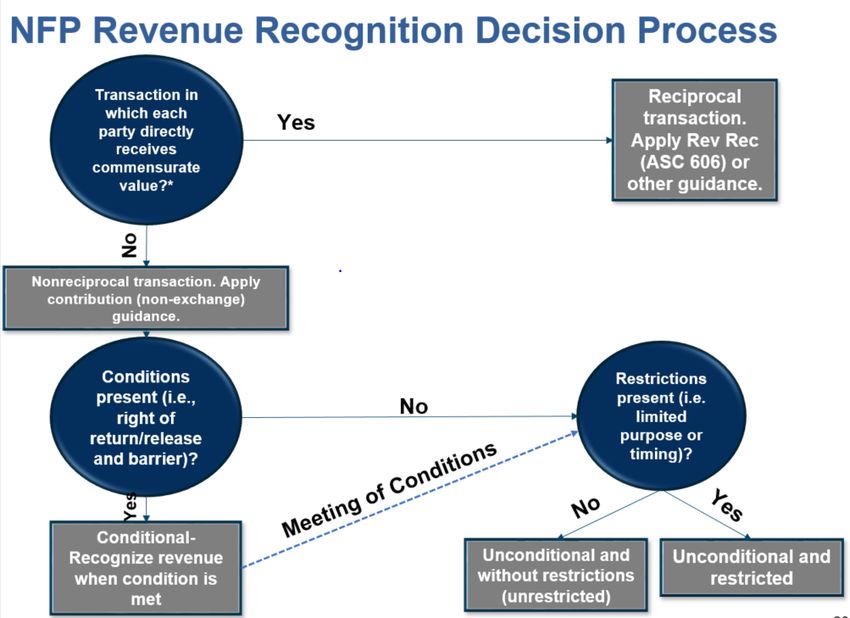

Fiscal years beginning after December 15, 2016Proposed ASU – Clarifying the Scope and Guidance for Contributions Received and Contributions Made

Proposed Accounting & Reporting

Proposed Accounting & Reporting • Applies to both contributions received and made • Proposed ASU requires: • A right of return or release must exist, and • The agreement must include a barrier

Indicators To Determine A Barrier

Including But Not Limited To:

• Inclusion of a measurable performance-

related barrier

• Whether a stipulation is related to the

purpose of the agreement

• The extent to which a stipulation limits

discretion by the recipient

• The extent to which a stipulation requires an

additional action or actionsProposed Effective Dates The effective date is the same as the new Revenue Recognition standard (Topic 606), but allows for early implementation.

Tax Update Tax Update

Tax Reform – Higher Education

• Excise Tax on Some Private Colleges &

Universities

• Each Unrelated Business Activity Stands Alone

with Respect to Profit/Loss

• Excess Compensation Excise Tax

• College Athletic Event Seating Rights

• UBIT on Certain Fringe Benefits

• Repeal of Advance Refunding BondsTax Reform – Higher Education • Whew! The provision that made “logo and name” licensing fees automatically (“per se”) unrelated business income did not make it out of the Senate. Thus, we escaped without this rule in the new law.

Tax Reform: On-premises Athletic Facilities = UBIT • Section 13703 of the new law contains a provision whereby the market value of providing exercise facilities (and specific other fringes) to staff and faculty would be considered unrelated business income and required to be reported on Form 990-T.

Tax Reform: On-premises

Athletic Facilities = UBIT

• “Unrelated business taxable income of an organization shall be

increased by any amount for which a deduction is not

allowable under this chapter by reason of section 274 and

which is paid or incurred by such organization for any qualified

transportation fringe (as defined in section 132(f)), any

parking facility used in connection with qualified parking (as

defined in section 132(f)(5)(C)), or any on-premises athletic

facility (as defined in section 132(j)(4)(B)).”

• “The Secretary shall issue such regulations or other guidance

as may be necessary or appropriate to carry out the purposes

of this paragraph, including regulations or other guidance

providing for the appropriate allocation of depreciation and

other costs with respect to facilities used for parking or for

onpremises athletic facilities.”Tax Reform: Moving Expense

Deductions Suspended

• Sections 11048 and 11049 of the new law suspend the

exclusion from income tax for qualified moving expense

reimbursements AND the deduction for moving expenses

through December 31, 2025 (except in the case of a

member of the Armed Forces of the United States on

active duty who moves pursuant to a military).

• Thus, IRC Section 217 has been amended by adding at

the end the following new subsection:

• “(k) SUSPENSION OF DEDUCTION FOR TAXABLE YEARS

2018 THROUGH 2025.”Tax Reform: Athletic Tickets Deduction Suspended • College Athletic Event Seating Rights. Historically, special rules applied to certain payments to institutions of higher education in exchange for which the donor/payor who met certain criteria received the right to purchase tickets or seating at an athletic event. Specifically, the donor/payor could treat 80 percent of a payment as a charitable contribution. The new law includes a denial of this deduction for periods after December 31, 2017.

Tax Reform: Private College/University Endowment Excise Tax • Excise Tax on some Private Colleges and Universities. There is a 1.4% excise tax on the net investment income (to be defined) of private colleges and universities that are “applicable educational institutions” (AEIs) — generally meaning the school has at least 500 students and 50% of its students are located in the U.S. The “threshold” computation applies to AEIs with an aggregate fair market value of the assets at the end of the preceding taxable year (other than those assets that are used directly in carrying out the institution’s exempt purpose) of at least $500,000 per student.

Tax Reform: What did not make it in? • Political Campaign Activity. The current “Johnson Amendment,” which prohibits any political activity by 501(c)(3) organizations, is not affected. • Private Foundation Taxes. The current 1% or 2% structure for taxes on investment income of private foundations is not changed from current law. • Tuition Reduction/Remission Rules Not Affected. Qualified tuition reductions will remain non-taxable. • Employer-Provided Educational Assistance Intact. The Section 127 provision for the non-taxability of certain employer educational assistance is not repealed.

Tax Reform: What did not make it in? • Housing for the Convenience of the Employer. The House bill contained a provision to provide limits on the amount that could be excluded from an employee’s income for employer-provided housing. This provision is not in the final bill. • UBIT on Research Activities. The House bill included a modification that subjected income from research activities whose results were not publicly available to unrelated business income taxes. The final bill does not include this provision. • Donor-Advised Fund Reporting. The final bill does not incorporate the House provision to increase reporting and disclosure of donor-advised funds.

Tax Reform: What did not make it in? • Private Activity Bonds. The House bill included a provision to make interest on private activity bonds taxable. This provision is not included in the final bill. • Inflation Adjustment for Charitable Mileage Deduction. The House proposed a provision to repeal the statutory charitable mileage rate and provide instead that the standard mileage rate used for determining the charitable contribution deduction shall be a rate which takes into account the variable costs of operating an automobile. This is not included in the final bill.

Tax Reform – Other Issues

• Repeal and replacement of the Affordable Care

Act – Not really

• Repeal of the “Johnson Amendment” – No!

• Excess benefit taxes and “rebuttable

presumption”

• Corporate tax rate (flat) – 21%

• Perceived effects on charitable givingPerceived Effects on Charitable

Giving

• For 100 years, our tax code has been a powerful

tool to encourage and empower Americans to

support their communities through charitable

giving.

• Tax reform provides a unique opportunity to explore policies

that could increase charitable investment in local

communities.

• The charitable deduction has been included in current tax

reform proposals, but efforts to increase the standard

deduction and lower rates have the unintended consequences

of limiting the effect of the charitable deduction and reducing

giving.Perceived Effects on Charitable

Giving

• A recent study by Independent Sector and Indiana

University indicates that current tax reform

proposals would reduce charitable giving.

• The study finds that doubling the standard deduction and

reducing the top rate to 35% could reduce charitable giving

by up to $13 billion per year.

• The Independent Sector/Indiana University study also found

that when those proposals incorporated an expanded

charitable deduction for all taxpayers, including people who

do not currently itemize on their taxes, charitable giving

would actually increase by an estimated $4.8 billion.Pouring Agreements Update • The 2016 snapshot entitled “Advertising or Qualified Sponsorship Payments?” still left hanging the situation of a “pouring agreement” whereby a donor/sponsor/partner makes a contribution to a college under an agreement that stipulates the college will only serve (“pour”) that donor/sponsor/partner’s soft drinks. It can be argued that this type of payment would not be deemed as “sponsoring” an event. However, the snapshot states, “The Regulations apply to all forms of corporate sponsorship activities and not just single events. Sponsored activities may include a single event, a series of related events, an activity of extended or indefinite duration, and/or continuing support of an exempt organization’s operation. A payment may be a qualified sponsorship payment regardless of whether the sponsored activity is related or unrelated to the organization’s exempt purpose(s).””

Pouring Agreements Update • “An exclusive provider arrangement limits the sale, distribution, availability, or use of competing products, services, or facilities in connection with an exempt organization’s activity. An exclusive provider arrangement generally results in a substantial return benefit to the payor. Thus, only the portion of the payment that exceeds the fair market value of the exclusive provider arrangement and any other benefit(s) received is a qualified sponsorship payment that does not constitute receipt of income from an unrelated trade or business.”

Pouring Agreements Update • “A payment that does not meet the criteria as a qualified sponsorship payment is not automatically subject to UBIT. Rather, the unrelated business income tax treatment of such unqualified payment is determined under the existing principles and rules found in IRC Sections 512, 513, and 514. Treas. Reg. Section 1.513-4(d)(1)(i).”

Minister’s Housing Allowance

• In November 2013, a federal judge held that the

minister’s housing allowance (under IRC section

107(2)) was unconstitutional because it “violates

the establishment clause of the First Amendment”

• This was in response to a case filed by a

foundation that sued because it did not believe its

officers could utilize this tax benefit

• The judge delayed the implementation of the ruling

until appeals had run their courseMinister’s Housing Allowance

• In 2014, the Seventh Circuit Court overturned the

lower court judge’s ruling

• However, the reversal was not based upon the

merits of the case, but on the “standing” of the

plaintiffs

• Ultimately, the officers of the foundation had not

had the IRS deny the minister’s housing

allowances claimed on their individual tax returnsMinister’s Housing Allowance

• In 2016, the foundation filed a new court case —

because its officers paid taxes on the housing

allowances apparently claimed on their individual

returns

• In August 2016, the federal government made its first

filing in this new case. In the government’s filing, it

conceded that, based upon their understanding of the

facts, the foundation’s officers have the legal standing

to challenge the housing allowance exclusion.

• The government maintained that the plaintiffs did not

have standing to challenge the parsonage exclusion –

IRC section 107(1)Minister’s Housing Allowance

• In October 2017, the District Court (Judge Crabb) held

that the Section 107(2) minister rental allowance

violates the First Amendment

• Previously dismissed case against Section 107(1)

• After the foundation’s executives — following the

directions of the Court of Appeals — filed individual tax

returns with housing allowances and had them denied

by the IRS, the judge found that they had standing to

challenge Section 107(2)

• On to the Court of Appeals… and beyond?!Department of Treasury Priority

Guidance Plan – Dual Use

Current language in the regulations – allocate

between the two uses “on a reasonable basis.”

• For the 14/15 year and 15/16 year and 16/17

year and 17/18 year, the Priority Guidance Plan

has listed:

• Guidance under §512 regarding methods of

allocating expenses relating to dual use

facilities.Dual Use Facilities and Cost

Allocation

• A dual use facility is used for both

exempt and nonexempt purposes.

• Examples:

• College athletic stadium used for concerts

• Charity’s community fitness center also used

by the public

• University golf courseMethods of Allocation • Reasonable given all facts/circumstances • Space-based methods • Time-based methods • Unit-based methods

Cost Allocations – Unit-based • College Y is a public charity in accordance with Internal Revenue Code sections 501(c)(3) and 170(b)(1)(A)(ii). In the past year, a donor gave Y a golf course. So now Y runs a golf operation that is used by students, faculty, alumni, and the general public. Fees charged are as follows: • General public $30 • Alumni $25 • Faculty $10 • Students $10

Cost Allocations – Unit-based

• The accounting team at Y knows that they have unrelated

business income for the greens fees paid by the general

public and alumni (but not students and faculty). They

have allocated expenses to the unrelated business income

on a “gross-to-gross” (gross revenue for unrelated golfers

over total gross revenue). So, for example, if each of the

four “types” of golfers above accounted for 250 rounds

per year, the expense allocation would look as follows:

($30 x 250 = 7,500) + ($25 x 250 = 6,250) =

13,750 / 18,750 = 73.33%Cost Allocations – Unit-based

• The IRS EO Examinations team prescribed a “unit-

based” allocation method modeled after NUMBER OF

ROUNDS as follows:

Number of unrelated (alumni & general public) rounds

of golf (numerator) / Total number of rounds of golf

(denominator)

= % of expenses allocable to unrelated business

income from golf fees

• This would result in a much lower expense allocation

percentage at:

500 rounds / 1,000 total rounds = 50.00%Form 1098-T Box 1 Only!

• The 2015 PATH Act contained a provision that eliminated

the option for educational institutions to either report on

Form 1098-T payments received (Box 1) or amounts

billed (Box 2).

• For forms required to be filed for 2016 and 2017, the IRS

announced that it would not impose penalties if an

institution reported the aggregate amount billed for the

calendar year for expenses paid (Box 2).

• Ultimately, the relief extended the rules in effect prior to

the PATH Act. However, in 2017 the IRS announced that

no further “Box 1” relief would be granted after 2017.Rebuttable Presumption of Reasonableness • Treas. Reg. 53.4958-6 • Approval by Independent Board (Committee) • Use of reasonable comparable data • Documentation of decision

Form 990 Reporting and ASU 2016-14

2018 Standard Mileage Rates • The 2018 optional mileage rates are as follows: Type Rate Business travel 54.5¢ per mile Medical & moving travel 18¢ per mile Charitable mileage travel 14¢ per mile**

Form 990 Extension Changes • A review of the new Form 8868 for 2017 reveals no Part II. Further, the draft instructions (under “What’s New”) state: There is now an automatic 6-month extension of time to file instead of the previous 3-month automatic extension and subsequent request for an additional 3-month extension. The form and instructions have been revised accordingly.

IRS – Issue Snapshots

• Knowledge Management (KM)

• Knowledge Networks (K-Nets)

• In 2016 EO completed 8 Issue Snapshots

• In 2017 EO completed 8 Issue Snapshots

• K-Nets will continue to prepare and post technical Issue

Snapshots for EO employees and the general public

• The TE/GE “Issue Snapshots” may be found at

www.irs.gov/government-entities/tax-exempt-and-

government-entities-issue-snapshotsIRS – Issue Snapshots – UBIT

• Advertising or Qualified Sponsorship

Payments? (9/29/16)

• Volunteer Labor Exclusion from Unrelated

Trade or Business (5/12/17)

• Identification and Treatment of Income from

Mailing Lists (5/24/17)

• Exclusive Provider Arrangement within

Qualified Sponsorship Agreements (6/16/17)IRS – Issue Snapshots – UBIT • Exclusion of Bingo from Unrelated Business Activity (10/18/17) • Rents from Personal Property, “Mixed Leases,” and the Rental Exclusion from UBTI (10/18/17) • Exclusion of Rent from Real Property from Unrelated Business Taxable Income (10/18/17)

IRS “Case Selection Model”

• “Data-Driven Decision Making”

• 200 – 250 “Queries”

• R.A.A.S. (Research, Applied Analytics &

Statistics)

• 2017 – 6,100 Examinations

• College & University Compliance Program

• Employment Tax AuditsIRA Charitable Rollover Made

Permanent (2015)

• For taxpayers 70.5 years of age

• Up to $100,000

• Direct distribution to a public charity

• PERMANENT

• No changes (i.e. higher limit, DAFs, 59.5 years

old)

• Tax reform?2018 – Other Matters of Interest • Coaches’ Apparel • Fuel Credits • QSEHRA (Small Institutions) • UBIT: The Required Minimum Level of Knowledge

Questions?

Thank you. Fran Brown, Partner Dave Moja, Partner CapinCrouse LLP CapinCrouse LLP fbrown@capincrouse.com dmoja@capincrouse.com 617.535.7534 321.258.9907

You can also read