Investor Presentation - January, 2019 - Mexichem

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Investor Presentation January, 2019

Forward-Looking Statements

In addition to historical information, this presentation Mexichem has implemented a Code of Ethics that rules its

contains "forward-looking" statements that reflect relationships with its employees, clients, suppliers and

management's expectations for the future. The words general groups. Mexichem’s Code of Ethics is available for

“anticipate,” “believe,” “expect,” “hope,” “have the intention consulting in the following link:

of,” “might,” “plan,” “should” and similar expressions http://www.mexichem.com/Codigo_de_etica.html.

generally indicate comments on expectations. The final

results may be materially different from current expectations Additionally, according to the terms contained in the

due to several factors, which include, but are not limited to, Securities Exchange Act No 42, Mexichem Audit Committee

global and local changes in politics, the economy, business, established a mechanism of contact, which allows that any

competition, market and regulatory factors, cyclical trends in person that knows the un-fulfilment of operational and

relevant sectors; as well as other factors that are highlighted accounting records guidelines and lack of internal controls of

under the title “Risk Factors” on the annual report submitted the Code of Ethics, from the Company itself or from the

by Mexichem to the Mexican National Banking and subsidiaries that this controls, file a complaint which is

Securities Commission (CNBV). anonymously guaranteed. The whistleblower program is

facilitated by a third party. The telephone number in Mexico

The forward-looking statements included herein represent

is 01-800-062-12-03.

Mexichem’s views as of the date of this press release.

Mexichem undertakes no obligation to revise or update The website is: http://www.ethic-line.com/mexichem and

publicly any forward-looking statement for any reason unless contact e-mail is: mexichem@ethic-line.com.

required by law.”

Mexichem’s Audit Committee will be notified of all complaints

for immediate investigation.

2

Mexichem’s Growth Strategy

Mexichem at a Glance pg. 4

Adding Specialty Products and M&A pg. 12

Acquisition for the Fluent Business Group

Acquisition for the Vinyl Business Group

Margin Growth vs Organic Volume Growth pg. 20

Backward Integration to Reduce Cost of Production pg. 24

Vinyl and Fluor Business Group Outlook pg. 28

Improving Outlook for PVC

Fluor Business Group

NAFTA impact on Mexichem pg. 34

Lower Capex Cycle and Solid Balance Sheet pg. 37

Mexichem of the Future pg. 40

Management Team pg. 45

3

Mexichem at a Glance 4

Business Snapshot

Operations

41 countries

Sales

>22,000

employees

>100 countries

>$6.7 billion*

Consolidated Annual

137 Revenues

production plants

17 2

R&D labs fluorite mines

* Note: Includes sales of Netafim as of 2017 (Proforma). All numbers includes Netafim figures

5 .

A major transformation over the past 15 years...

2003 TODAY

Revenues(1)

$312 million 21x Consolidated Revenues

$6.7 billion*

EBITDA(1)

$50 million

24x Adjusted EBITDA

$1.2 billion*

Market Cap(2) Market Cap(2)

$167 million 32x $5.4 billion

Notes:

1) Reported figures under Mexican GAAP and converted into dollars using an FX of 10.8 MXN/USD

2) 2003 market cap figures as of 12/31/2003; Market cap as of 01/07/2019. *All figures are as of 2017 and includes the integration of Netafim (Proforma)

8

Strong Track Record of Disciplined Acquisitions

(27 acquisitions since 2003)

4

Sylvin Technologies

Specialty PVC resins

Fluorita de Mexico

Camesa trade name becomes Mexichem

43% of Mexichem (Camesa subsidiary)

Quimica Fluor

Fluorita de Rio Verde 1

2 1,405

1,106

830 962 899 910 926

818

645

392 472 457

189 228

50 72

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 LTM 3Q'18

1.9x 2.5x 0.5x 0.7x 1.6x 1.2x 1.0x 1.3x 1.1x 0.7x 1.0x 2.2x 1.0x 1.8x 1.2x 1.91x

Success at integrating new acquisitions has boosted sales and EBITDA and has made EBITDA (US$mm)

Mexichem a leader within the industries it operates 3

Net debt/EBITDA

Source: Company filings. 1) 3Q18 considers Netafim’s integration since February 7th, 2018. 2) Figures for 2017 do not consider EBITDA from Netafim.

3) Net debt in 3Q’18 and 2017 includes US$0.6 million and US$0.9mm, respectively; in 2016 includes US$1.4mm and in 2015 US$21.4mm,

7 corresponding to letters of credit and suppliers’ credits exceeding 180 days, which, only for the purposes of the covenants of the Cebures and our

revolving credit facility, are considered financial debt, although they are not recorded as debt in our balance sheet 4) Acquired in 2018.

Mexichem Business Groups

Global Leader in Plastics and Chemicals

Fluor Ethylene

Value Chain Value Chain

Fluorspar Pipes and fittings

PVC & Specialty Resins

Hydrofluoric acid Irrigation systems

Compounds &

Refrigerants Plasticizers Datacom

Aluminum fluoride Derivatives Geosynthetics

JV with

Revenues: $830 mm Revenues: $2,476 mm Revenues: $4,158 mm

EBITDA: $351 mm EBITDA: $614 mm EBITDA: $534 mm

LTM 3Q18 EBITDA margin: 24.8% EBITDA margin: 12.8%

EBITDA margin: 42.3%

Proforma 24% of consolidated EBITDA 43% of consolidated EBITDA 38% of consolidated

Specialty products EBITDA 13% of Specialty products EBITDA 12% EBITDA

Consolidated of Consolidated

Note: Revenues and adjusted EBITDA margin correspond to LTM 3Q18. All figures are before intercompany eliminations.

* Includes Netafim figures proforma (12 months of results). For statutory purposes, Netafim is consolidated since February 7th, 2018.

8

Vertical Integration

Ensuring Supply to Mitigate Volatility & Increase Cost Competitiveness

Ethylene Chain Overview

- One of the largest PVC resin and leading player in piping worldwide

Compounds

Chlorine &

Salt

Caustic

PVC Resin

VCM

Sylvin Technologies 63% of LTM

Specialty Resin

consolidated

Ethane Ethylene

proforma EBITDA* in

Fluent 3Q’18

Mexichem products On-going joint ventures

VOLATILITY

+ VERTICAL INTEGRATION THROUGHOUT THE VALUE CHAIN

–

Commodity companies trade at an average Specialty material companies trade at an

EV/EBITDA multiple of 5.8x to 8.0x average EV/EBITDA multiple of 9.0x to 13.8x

9

Vertical Integration: Fluor Business Group

40% Sold to Market 100% Sold to Market

Sulphuric

Acid

HF Refrigerant

Gases

Fluorspar

Aluminum Strategy:

Fluoride Downstream integration to

higher value added

60% Sold to Market products

100% Sold to Market

+ VOLATILITY

VERTICAL INTEGRATION THROUGHOUT THE VALUE CHAIN

–

Commodity/Chemical Companies trade at an

average EV/EBITDA multiple of 9.0x to 11.0x

Source: Company filings

10Mexichem’s Markets and Product Categories

Netafim’s contribution

BUSINESS UNITS MARKETS SERVED PRODUCT CATEGORIES EXAMPLES

Others Pipes & Fittings (PVC,

Infrastructure

Energy

10% Polyethylene, Polypropylene)

4% 15%

Telecom Geosynthetics (woven &

12% non-woven)

32% Datacom & Infrastructure

Agricultural Irrigation systems

27% Housing

From 3% to 27% if we Driplines, sprinklers and

FLUENT were to include other irrigation products

Netafim

Others 3% Automotive 3%

Industrial 5% Base Chemicals

Wire & Medical 4% Specialty Resins

Cable Home, lawn &

20% PVC Resins

Garden 4%

Compounds

PA & Plasticizers

60% Phosphates

Building &

VINYL Construction Other Chemicals

Technical

Propellants Aluminium

Fluorspar Met Grade

8% 5% Building and

Construction Fluorspar Acid Grade

Air Conditioning 14%

Chemicals

Hydrofluoric Acid

3%

26% Anhydrite

*1% Aluminum Fluoride

26% corresponds to Refrigerants

FLUOR 17%

Energy Medical propellants

Refrigeration Medicals

Technical Propellants

Source: Company fillings, Markets as % of pro forma 2017 revenues of combined entity

Note: Netafim’s agricultural contribution includes Landscape (c.1%) and Mining (c.1%)

11Adding Specialty Products

M&A

12Acquisitions for Fluent Business Group

Wavin and Dura-Line

Wavin EBITDA Margin (1) Dura-Line EBITDA Margin (1)

(% of Total Revenue) (% of Total Revenue)

20.0% 25.0%

22.4%

14.3% 20.0% 17.3%

15.0% 13.7% 17.2%

12.0% Margin 2018 = 16.5%

10.3% 10.9% Margin 2018 = 12.5% 15.0% 14.8% 14.0% 13.5% Margin 2015 = 14.8%

9.7% 13.3%

10.0% 9.2% Margin 2013 = 9.3% 9.7%

10.0%

4.3%

5.0%

5.0%

0.0%

0.0%

1Q 2Q 3Q 4Q

1Q 2Q 3Q 4Q

2013 2014 2015 2016 2017 2108 2015 2016 2017 2018

Note:* Includes Wavin Africa, Overseas, China, Australia and Middle East Note:* Includes USA, Canada, Oman, Mexico, South Africa and Czech Republic

(1) (1) The 4Q15 EBITDA figure includes the effect of discontinued operations

EBITDA figures exclude restructuring costs and a benefit of US$17MM in 4Q13

A global leader in the supply of plastic pipe A global leader in high-density polyethylene

systems and solutions for both, above, and conduit duct and pressure pipe solutions.

below ground applications. Allows for expansion in Telecom, Datacom and

Has close to $1.3 billion in annual revenue. Energy Piping markets.

Targeting opportunities in Europe, Asia Adds presence in India, South Africa and the

Pacific and Middle East. Middle East.

13Acquisition for Fluent Business Group

Netafim to incorporate ~higher value-added products

A global leader of technologically

advanced irrigation solutions.

Transformational acquisition in specialty products

and industrial solutions with specific expertise in

water.

Leader in advanced technology irrigation

solutions.

Consistent with the company’s growth strategy

into higher value-added products, increasing

Fluent’s portfolio of specialty products.

Expands global footprint by strengthening

presence in key markets such as U.S., India, and

LatAm, and opens new regions such as Middle

East, Africa and Australia.

Revenues in 2017 were close to $950 million and

EBITDA Margin of 14%.

Brings strong R&D and technically advanced

capabilities.

14Acquisition for Vinyl Business Group

Vestolit

Vestolit EBITDA Margin

(% of Total Revenue)

16.0% 14.4%

14.5%

14.0%

Margin 2018 = 12.4%

11.6% 11.2%

12.0%

10.1%

10.0% 8.4% 8.8% Margin 2015 = 8.8%

7.8%

8.0%

6.0%

4.0%

2.0%

0.0%

1Q 2Q 3Q 4Q

2015 2016 2017 2018

Europe’s 6th largest PVC manufacturer.

Europe’s only manufacturer of High Impact Suspension PVC (HIS-PVC) for

weather-resistant windows and is Europe’s Third-largest producer of

paste PVC for floors and wallpapers.

Keeping with the strategy of becoming a global, vertically integrated

company with a focus on high-end, specialized products.

Expands European footprint by entering a new market segment and

acquire new technology.

15Building Mexichem’s Specialty Products Portfolio

Specialty PVC Resins Producers Worldwide (Kton)

500

400

CAPACITY (KMT)

300

200

100

-

Mexichem Westlake Formosa Hanwha INEOS LG Group ChemChina Saint-Gobain Alain de Open Gate

Group Group Krassny Capital

Source: IHS 2017

16Acquisition for Vinyl Business Group

Vinyl Compounds to incorporate ~40 m in sales to Compounds Business Unit

U.K. leading supplier of PVC compounds

Adds scale to Mexichem’s U.K. operations.

Targeting opportunities in India and Southeast Asia.

Expands the portfolio of specialty products.

Enabled further vertical integration of Compound Business through stabilizer technologies

and recycled PVC capabilities.

Brings synergies to Vinyl Business group through Vinyl Compounds’ PVC resins and

plasticizers.

Key drivers for the demand are related to:

o Building & Construction

o Consumer Goods

o Footwear

17Acquisition for Vinyl Business Group

Sylvin Technologies Inc. ~29 m in sales to Compounds Business Unit

A niche PVC compounds manufacturer based in Denver, Pennsylvania

Customer-focused business model.

Serving a broad range of industries, such as: automotive, general purpose/industrial,

specialty, medical, building and construction and wire and cable market.

A strong team and application development capabilities.

Sylvin’s key raw materials are PVC resin, plasticizers and stabilizers, which should bring

synergies to Mexichem’s Vinyl operations.

18Improvement of Profitability Ratios

Mexichem WACC ~7.5%

ROE (%) 15.2%

ROIC (%)

Mexichem Group Mexichem Group

9.5%

8.2%

9.8%

6.5% 6.7%

8.7%

7.0%

2015 2016 2017 LTM Sep 2018 2015 2016 2017 LTM Sep 2018

ROE: Income from continuing operations / Adjusted Average Equity from continuing operations.

ROIC: Adjusted NOPAT for continuing operations/Adjusted Equity from continuing operations + Liabilities with cost – Cash.

Income from continuing operations and NOPAT (EBIT-taxes) consider trailing twelve months.

19Margin Growth vs Organic

Volume Growth

20Driving Margin Growth Vs. Volume Growth

Closer To Our End Consumers -Fluent

Chlorine &

Salt

Caustic PVC Resin

VCM Compounds Fluent

Specialty

Ethane Ethylene

21

21Focus on Higher Margin Products

In 2016 we discontinued operations of pressure pipes and shifted that capacity

to Datacom pipes

Datacom pipes have higher

margins than pressure pipes

22Cross selling of Products (Netafim, Fluorspar in

Brazil, HIS-PVC in Latam)

The company cross sells products

with attractive margins in other

regions, among others:

1) Fluorspar and refrigerant gases

in Brazil,

2) HIS-PVC (high impact modified

polyvinylchloride copolymer) a

Vestolit product in LatAm, and,

3) Expects to sell PVC pipes to

Netafim.

The broad high vale-added portfolio

product is expected to expand with the

acquisition of Netafim.

23Backward Integration to

Reduce Production Cost

24Vertical Integration: Ethylene

Ethylene is our Most Important Raw Material

Ethylene Price Components

Polyethylene’s Cost Structure

December 2014 PE Pipe Cost Structure

Ethane Others Ethylene Margin Others

27% 10% 63% Ethylene 82% 18%

PVC’s Cost Structure

PVC Pipe Cost Structure

Others

Ethylene 29% 71%

December 2017

Ethane Others Ethylene Margin

38% 22% PVC Resin Cost Structure

39% Others

Ethylene 39% 61%

Ethylene Cracker (JV w/ OXY) =

VCM Cost Structure

• ~70% of the Vinyl’s Group ethylene needs. Ethylene 49%

Others

51%

• ~90% of the NA Vinyl’s Group ethylene

needs.

Source: Company fillings,

*Once Ethylene cracker is fully operational.

25Vertical Integration: Ethylene

Estimated PVC Cost-Curve by Region, USD/Metric ton and million metric tons

Europe Northeast Asia (KTJ) Middle East Northeast Asia (China) Former USSR

South America North America Africa Asia and Pacific

Global demand:

~48 MM metric tons

Cash cost per ton Acetylene based (2021)

1,000

800

600

Before

400

200

0

The cracker positions Mexichem on the lowest part of the cost-curve globally

Source: McKinsey petrochemical models, IHS

1 2021 capacity are estimates from HIS. 2 Effective capacity is given as 90% of nameplate capacity

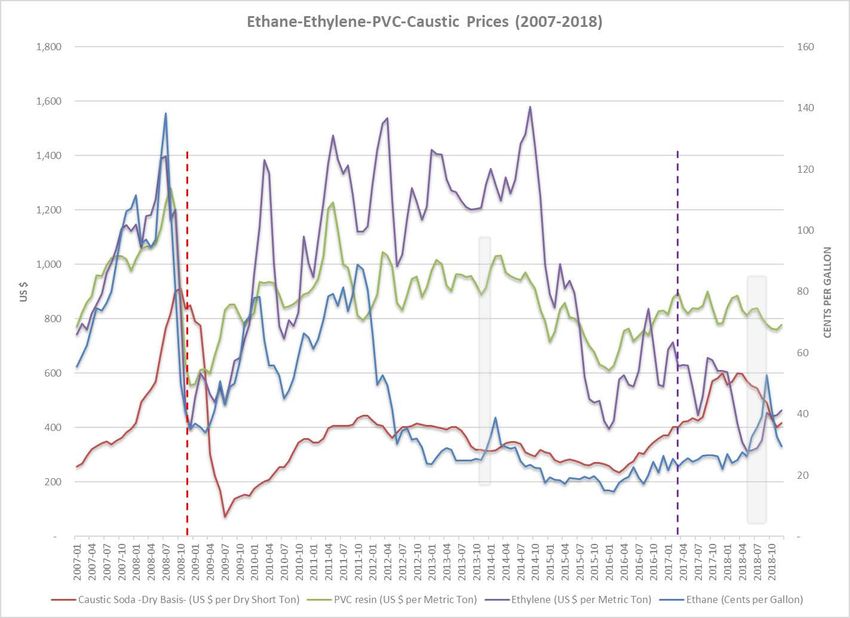

26Ethylene, Ethane, Caustic soda & PVC resin prices

Source: IHS

27Vinyl and Fluor Business

Group Outlook

28Improving Outlook for PVC

Global Supply, Demand and Operating Rate

70,000 100

90

60,000

80

50,000 70

(‘000 MT)

60

40,000

50

30,000

40

20,000 30

20

10,000

10

0 0

2011 2012 2013 2014 2015 2016 2017 2018E 2019E 2020E

Total Capacity ('000 MT) Total Demand ('000 MT) Operating rate (%)

Source: IHS

29Improving Outlook for PVC

There is limited additional global PVC capacity being built in the next 4 years

~4.5 million metric tons

PVC Global Capacity Expansions

5.0

4.0 India,

China,

Million Metric Tons

3.0

China, Philippines,

India Egypt China,

2.0 Egypt,

Baltics

1.0

0.0

-1.0

-2.0

11 12 13 14 15 16 17 18 19 20 21

North America Northeast Asia ROW Hypothetical NAM Hypothetical Europe

30 Source: IHSImproving Outlook for PVC

PVC is the third most popular plastic in the world and the largest sourced

material in the Building & Construction market, followed by PE & PP

Building &

19.7%

Construction

Packaging 39.9%

Automotive 8.9%

Electrical &

5.8%

Electronic

Others 25.7%

31 Source: Plastics - The facts 2016 by PlasticsEuropeImproving Outlook for PVC

China’s Share of Global Capacity is 44%

PVC Capacity

70,000

60,000

50,000

(‘000 MT)

40,000

30,000

20,000

10,000

0

2010 2011 2012 2013 2014 2015 2016 2017 2018E 2019E 2020E

Worldwide China

Source: IHS

32U.S. International Trade Commission decision and

Price Behavior

After a year-long investigation process by the U.S. Department of Commerce, on

February 22, 2017 they announced that R-134a from China were being dumped in the

U.S. market at prices below fair value and prescribed antidumping duties ranging from

148.79% to 167.02%.

The American HFC Coalition believes the decision is fully supported by :1) The

industry developed R-134a to succeed earlier-generation refrigerants without any

negative impact on the ozone layer, 2) The industry invested substantial sums to

manufacture R-134a in the U.S. for automotive air-conditioning, stationary air-

conditioning, and other applications.

As a result of the dumped imports, the U.S. industry has suffered persistently low

price levels and poor operating results.

The imposition of antidumping duties is a positive step to restore conditions of fair

trade in this market.

As a consequence of the above mentioned R-134a refrigerant gas prices increased

approximately by 25% on average in 2017.

33NAFTA Impact on Mexichem 34

U.S. Fluorspar Demand – Supply Summary

U.S. Fluorspar Demand 2014 – 2017 U.S. Acidspar Supply

2014 2015 2016 2017

Spain /

Metspar 108 90 55 70 Others

China 3%

19%

Acidspar 291 331 310 330

Total 399 421 365 400

Fluorspar Vietnam

8%

Mexichem

• Metspar: 100% used as a fluxer in the steel South 58%

industry, particularly for stainless and Africa

specialty steels. 11%

Mexico

(Others)

• Acidspar: Aprox. 90% used for HF 1%

production (Honeywell, Chemours) and

10% for other applications. • Metspar: Mexichem is currently supplying

99% of total consumption (2016-2017).

• The U.S. does not produce Metspar and

has some small Acidspar mines (Hastie) • Acidspar: Mexichem supplies approx. 58%

that have not been producing in the last few of the US consumption. Other sources are

years, but are still in development. from Mexico (Muzquiz), Vietnam, South

Africa, China.

Source: Roskill, IM,USGS, Trademap Internal Analysis

35Mexichem’s Fluor exports/Vinyl’s imports to the U.S.

NAFTA tariffs and MFN tariffs from WTO (World Trade Organization)

Exports (MX-USA) Sales in 2017

Product Name NAFTA MFN USA US (MM)

Acid grade fluorspar low arsenic Ex. 3.70% N.A

Acid grade fluorspar (ceramic, fine and standard) Ex. Ex. $ 43.1

Aluminum fluoride Ex. 3.70% $ 17.5

HF Ex. Ex. N.A

Anhydrous HF Ex. Ex. $ 104.7

Metallurgic fluorspar (lamas, big stone, standard) Ex. Ex. $ 15.6

Sulfuric acid Ex. Ex. N.A

Total Sales to the USA $ 180.9

As % of 2017 total consolidated sales 3.1%

Imports (USA-MX) Purchases in 2017

Product Name NAFTA MFN USA US (MM)

Vinyl Chlorine Monomer (VCM) Ex. Ex. $ 364.9

Source: WTO and Company Filings.

36Lower Capex Cycle and Solid

Balance Sheet

37Ending a Capital Cycle

(in USD terms)

Capex

666

460

414

302 289

253 251

199

2011 2012 2013 2014 2015 2016 2017 9 M1 8

2018e figure includes CAPEX for NETAFIM.

38Manageable Debt Profile & Long-Term Maturity Profile Investment Grade

Fitch Ratings BBB

S&P BBB-

Moody’s Baa3

Long-Term Debt Schedule

US$MM, as of September 30th, 2018 Debt Average Life

14.1 years

Weighted Average

Cost of Debt 5.09%

Most Debt at Hold Co Level Alignment of Debt to Revenue Currency Conservative Leverage Ratios

Debt by Division (3Q18) Debt by Currency (Swapped, 3Q18)

1% 6% 3% Total Debt / EBITDA Net Debt / EBITDA

3%

3.0x 2.9x

24% 2.6x 2.6x 2.5x

2.4x

2.0x 1.9x 1.8x 1.9x

1.2x

90% 73% 1.0x

Holding Vinyl Fluor Fluent US$ Euro Others

2013 2014 2015 2016 2017 3Q18

US$1.5B revolving credit facility

Source: Company filings (100% available)

39 Third Quarter 2018 EarningsMexichem of the Future 40

We Have Created The World’s First Agricultural Brain

Based on 50 Years of Agricultural and Hydraulic Knowledge, NetBeat™ is the World’s First Automated Precision Irrigation System

NetBeat™ combines real-time

data with Dynamic Crop Models™

to personalize irrigation while minimizing water

programs and optimize yields and resource useNetafim

• Please see video (NetBeat and Ramthal Community in India)

- NetBeat™ - the first irrigation system with a brain!

https://www.netafim.com/49a475/globalassets/digital-farming/netbeat/netbeat_online_07.mp4

- Ramthal Community

https://www.netafim.com/48e8ab/globalassets/demo/homepage/empowering-regional-

prosperity-through-a-multi-stakeholder-agro-water-management-project.mp4

4244

Management Team 45

Executive Leadership Team (ELT)

Rodrigo Guzmán Perera Paresh Chari Ran Maidan, Carlos Manrique Rocha

Chief Financial Officer (CFO) President, Fluent Business Group President and CEO,Netafim Ltd President, Vinyl Business Group

Daniel Martínez Valle Sameer S. Bharadwaj

President, Compounds Business Unit

Alejandra Rodríguez Sáenz

Corporate Vice-President, Human Capital

Pedro Martínez Puig

Corporate Vice-President, IT

Francisco Hernández

Corporate Vice-President, Legal

Chief Executive Officer President, Fluor Business Group

(CEO)

Mary Gorges Cristina Gil Jorge Luis Guzmán Mejía

Vice-president of Corporate Communications Director Corporate Affairs Corporate Vice-President, Internal Audit

46Thank You 47

APPENDIX 48

Brief Summary of Results (Q3 2018)

1 2 EBITDA by quarter (US mm)

mm US$ Third Quarter

Financial Highlights 2018 2017 %Var.

Net sales 1,785 1,503 19%

Operating income 270 201 34%

EBITDA 375 299 25%

EBITDA margin 21.0% 19.9% 107 bps

Net majority income 82 61 34%

Cash Flow before dividends 157 151 4%

Q'1 Q'2 Q'3 Q'4

Free cash flow 83 71 17%

2013 2014 2015 2016 2017 2018

Quarter Sales EBITDA

3 mm US$ 3Q18 3Q17 %Var. 3Q18 3Q17 %Var.

Vinyl 621 579 7% 151 133 14%

Fluent 1,003 785 28% 140 107 31%

Fluor 210 177 19% 94 68 38%

Eliminations/ Holding (49) (38) 29% (10) (9) 11%

Mexichem Consolidated 1,785 1,503 19% 375 299 25%

49 Third Quarter 2018 EarningsSales by Region Destination 50 Third Quarter 2018 Earnings

Strong Performance by Business Group X% EBITDA margin

Vinyl Fluent Fluor 5,509 Vinyl Fluent Fluor

26% 644 * Constant currency & 9% 4,771

Revenues

4,360 Organic Revenue Growth 4,360

630

495 495

19%

3,093 8%

1,785 2,257 2,257 2,416

1,503 1,503 1,623

210 210

177 177

785 1,003 1,908 785 839 1,861

1,749 1,749

579 621 579 623

3Q'17 3Q'18 9M'17 9M'18 3Q'17 3Q'18 9M'17 9M'18

* Constant currency &

EBITDA Organic EBITDA Growth

20.5%

Vinyl Fluent Fluor Vinyl Fluent Fluor 21.6%

36% 1,128 24%

1,029

19.0% 44.1% 19.1%

284 22.0% 832

25% 829 18% 277 44.0%

20.1% 192

21.0% 192 38.8% 38.8%

19.9% 423 13.7% 337

375 44.8% 357 44.8% 13.9%

299 38.4% 309 13.7%

302 38.4% 312 13.8%

94 14.0% 94 14.7%

68 13.6% 68 14.0%

107 140 20.4% 464 24.3% 110 123 357 20.4% 458 24.6%

24.3% 357 24.2%

23.0% 23.0% 151

133 151 133

3Q'17 3Q'18 9M'17 9M'18 3Q'17 3Q'18 9M'17 9M'18

Note: Breakdowns consider figures before eliminations. Total figures consider eliminations.

Organic = means that it will exclude: i) Netafim´s results for the quarter; ii) CADE and Netafim Ltd. Acquisition related expenses; iii) Brazil Tax legal settlement benefit, and iv) FX translation effects without consider

any positive or negative effect from Venezuela.

51 Third Quarter 2018 EarningsEBITDA Evolution

55% 60%

of Group EBITDA of Group EBITDA

produced in Specialty produced in Specialty

Products Products

52 Third Quarter 2018 EarningsStrong Cash Generation Despite Seasonality

Third Quarter January - September

2018 2017 %Var. 2018 2017 % Var.

mm US$

EBITDA 375 299 25% 1,128 829 36%

Taxes paid (58) (34) 71% (190) (104) 83%

Net interest paid (49) (35) 40% (143) (107) 34%

Bank commissions (7) (8) -13% (30) (21) 43%

Exchange rate gains (losses) (8) (5) 60% (40) (17) 135%

Change in trade working capital (1) (2) (33) 0 N/A (294) (208) 41% 1) PMV's insurance A/R is not

Operating cash flow before capex 220 217 1% 431 372 16% included in trade working

capital calculation.

CAPEX (Organic) (61) (54) 13% (186) (149) 25%

CAPEX (Total JV) (2) (19) -89% (13) (105) -88% 2) Trade working capital

variation (Sep 18 vs Dec 17)

CAPEX JV (OXY share) - 6 -100% - 45 -100%

includes Netafim’s proforma

NET CAPEX JV (2) (13) -85% (13) (59) -78% results for comparative

purposes.

Total CAPEX (organic & JV) (63) (66) -5% (199) (208) -4%

Cash flow before dividends 157 151 4% 232 164 41%

Shareholders' dividend (74) (80) -8% (210) (132) 59%

Free cash flow 83 71 17% 22 32 -31%

PMV's insurance A/R - - 268 -

Free cash flow after Insurance 83 71 17% 290 32 806%

53 Third Quarter 2018 EarningsUSD in millions

Balance Sheet Balance sheet Sep 2018 Dec 2017

Total assets 10,318 9,759

Cash and temporary investments 879 1,900

Receivables 1,349 975

Inventories 904 675

Others current assets 310 403

Property, plant and equipment, Net 3,482 3,626

Intangible assets and Goodwill 3,137 1,910

Long term assets 257 270

Total liabilities 6,814 6,078

Current portion of long-term debt 368 45

Suppliers 1,449 1,362

Other current liabilities 930 723

Long-term debt 3,267 3,210

Long-term employee benefits 185 186

Long-Term deferred tax liabilities 197 231

Other long-term liabilities 418 321

Consolidated shareholders'equity 3,504 3,681

Minority shareholders' equity 889 878

Majority shareholders' equity 2,615 2,803

Total liabilities & shareholders' equity 10,318 9,759

54 Third Quarter 2018 EarningsIncome Statement

Third Quarter January - September

USD in millions

Income Statement 2018 2017 % 2018 2017 %

Net sales 1,785 1,503 19% 5,509 4,360 26%

Cost of sales 1,289 1,129 14% 3,964 3,289 21%

Gross profit 497 374 33% 1,545 1,071 44%

Operating expenses 227 173 31% 732 525 39%

Operating income (loss) 270 201 34% 813 546 49%

Interest expenses (income) & bank commisions 57 43 33% 173 129 34%

Exchange rate, net 12 3 300% 43 38 13%

Monetary position 20 (2) N/A (6) (4) 50%

Financial Costs 89 44 102% 210 163 29%

Equity in income of associated entity (2) (1) 100% (4) (1) 300%

Income (loss) from continuing operations

183 157 17% 607 385 58%

before income tax

Cash tax 54 34 59% 168 104 62%

Deferred taxes 8 28 -71% 22 47 -53%

Income tax 62 62 0% 190 150 27%

Income (loss) from continuing operations 120 95 26% 417 234 78%

Discontinued operations (1) (4) -75% 19 1 1800%

Consolidated net income (loss) 120 91 32% 437 236 85%

Minority stockholders 37 30 23% 113 56 102%

Net income (loss) 82 61 34% 323 180 79%

EBITDA 375 299 25% 1,128 829 36%

55 Third Quarter 2018 EarningsResults by Business Group

Third Quarter January - September

mm US$

Vinyl 2018 2017 %Var. 2018 2017 % Var.

Volume (K tons) 646 635 2% 1,944 1,916 1%

Total sales* 621 579 7% 1,908 1,749 9%

Operating income 99 84 18% 315 227 39%

EBITDA 151 133 14% 464 357 30%

*Intercompany sales were $48 million and $37 million in 3Q18 and 3Q17, respectively. And as of September 2018 and 2017

were $135 million and $134 million, respectively.

Third Quarter January - September

mm US$

Fluor 2018 2017 %Var. 2018 2017 % Var.

Sales 210 177 19% 644 495 30%

Operating income 82 56 46% 247 153 61%

EBITDA 94 68 38% 284 192 48%

56 Third Quarter 2018 EarningsResults by Business Group

Third Quarter January - September

mm US$

Fluent 2018 2017 %Var. 2018 2017 % Var.

Sales 1,003 785 28% 3,093 2,257 37%

Fluent LatAm 270 279 -3% 816 818 0%

Fluent Europe 349 357 -2% 1,086 1,006 8%

Fluent USA & Canada 152 120 27% 415 341 22%

Fluent AMEA 35 34 3% 118 108 9%

Netafim 206 - 669 -

Intercompany eliminations (8) (5) 60% (11) (15) -27%

Operating income 95 71 34% 297 203 46%

EBITDA 140 107 31% 423 309 37%

57 Third Quarter 2018 EarningsRevenues & EBITDA wo FX effect

3Q17 3Q18 3Q18 3Q18/3Q17

mm US$

Sales Sales FX Total % Var

579 Vinyl 621 2 623 8%

785 Fluent 1,003 52 1,055 34%

1,364 Ethylene (Vinyl + Fluent) 1,624 54 1,678 23%

177 Fluor 210 - 210 19%

(38) Eliminations / Holding (49) - (49) 29%

1,503 Total 1,785 54 1,839 22%

3Q17 3Q18 3Q18 3Q18/3Q17

mm US$

EBITDA EBITDA FX Total % Var

133 Vinyl 151 - 151 14%

107 Fluent 140 7 147 37%

240 Ethylene (Vinyl + Fluent) 291 7 298 24%

68 Fluor 94 - 94 38%

(9) Eliminations / Holding (10) - (10) 11%

299 Total 375 7 382 28%

58 Third Quarter 2018 EarningsRevenues wo FX effect - Fluent

3Q17 3Q18 3Q18 3Q18/3Q17

mm US$

Sales Sales FX Total % Var

279 Fluent LatAm 270 30 300 8%

357 Fluent Europe 349 10 359 1%

120 Fluent US/Canada 152 - 152 27%

34 Fluent AMEA 35 2 37 9%

- Netafim 206 10 216

(5) Intercompany Eliminations (8) - (8) 60%

785 Total 1,003 52 1,055 34%

59 Third Quarter 2018 EarningsIn 2017 We Achieved Record Results and Expect Another Year of

Strong Growth in 2018

In 2017 we met high-end of EBITDA guidance range

For 2018 we expect an EBITDA growth to be between 25%-30%

Revenue ($mm) Adj EBITDA ($mm) and Margin (%)

19.0%

16.0% 16.7%

$5,485 $5,584 $5,828 14.8%

$5,344 $1,106

$814 $895 $895

EBITDA

Margin

+9% +223bps

2014 2015 2016 2017 2014 2015 2016 2017

EBITDA1 – non-M&A capex ($mm) and Conversion (%)2

78.0%

74.0% 74%

69.7%

$817

Our cash conversión is above 70%

$722 asd

$657 $634

In 2017 FCF increased 123% from

(EBITDA – non

M&A capex) / $90m to $201m

EBITDA

2014 2015 2016 2017

60 Third Quarter 2018 EarningsCloser to Our End Customers Chlorine &

Housing Catalogue in Brazil: Salt

Caustic

VCM

PVC Resin

Compounds Fluent

Specialty

Ethane Ethylene

WATER FLOW SOLUTIONS WATER STORAGE SOLUTIONS

ACCESORIES

GAS SOLUTIONS

ELECTRIC SOLUTIONS

61

61Closer to Our End Customers Chlorine &

Infrastructure Catalogue in Brazil: Salt

Caustic

VCM

PVC Resin

Compounds Fluent

Specialty

Ethane Ethylene

SEWAGE SYSTEM SOLUTIONS HYDRAULIC SOLUTIONS

62

62Vertical Integration Tested in 4Q14

Prices of oil and ethylene falling rapidly

Chlorine &

Salt

Caustic

USD/ ton USD/ barrel VCM

PVC Resin

Compounds Fluent

Specialty

2,000 120 Ethane Ethylene

100

1,500

80

1,000 60

40

500

20

0 0

Jan-2010

Sep-2010

Jan-2011

Sep-2011

Jan-2012

Sep-2012

Jan-2013

Sep-2013

Jan-2014

Sep-2014

Jan-2015

Sep-2015

Jul-2010

Jul-2011

Jul-2012

Jul-2013

Jul-2014

Jul-2015

Mar-2010

May-2010

Mar-2011

May-2011

Mar-2012

May-2012

Mar-2013

May-2013

Mar-2014

May-2014

Mar-2015

May-2015

Nov-2010

Nov-2011

Nov-2012

Nov-2013

Nov-2014

Nov-2015

Ethylene-Spot USA (Left) PVC Export USA (Left) Crude Oil WTI (Right)

Source: IHS (formerly CMAI)

Vinyl Business Group Fluent Business Group

* EBITDA USD$MM * EBITDA USD$MM

8%

14% 10% 66

64

66% 5% ~30M USD 48

59%

22

4Q13 4Q14 4Q13 4Q14

* EBITDA without FX in 4Q14, and non recurrent effects of 4Q13

63Margin Expansions in 4Q15

Prices of oil, ethylene and PVC resins

Chlorine &

Salt

Caustic

USD/ ton USD/ barrel VCM

PVC Resin

Compounds Fluent

Specialty

2,000 120 Ethane Ethylene

100

1,500

80

1,000 60

40

500

20

0 0

Jan-2010

Sep-2010

Jan-2011

Sep-2011

Jan-2012

Sep-2012

Jan-2013

Sep-2013

Jan-2014

Sep-2014

Jan-2015

Sep-2015

Jul-2010

Jul-2011

Jul-2012

Jul-2013

Jul-2014

Jul-2015

Mar-2010

May-2010

Mar-2011

May-2011

Mar-2012

May-2012

Mar-2013

May-2013

Mar-2014

May-2014

Mar-2015

May-2015

Nov-2010

Nov-2011

Nov-2012

Nov-2013

Nov-2014

Nov-2015

Ethylene-Spot USA (Left) PVC Export USA (Left) Crude Oil WTI (Right)

Source: IHS (formerly CMAI)

Vinyl Business Group Fluent Business Group

Positive performance on PMV + Resins, compounds & derivatives Amid FX fluctuations, EBITDA margin expansions

EBITDA USD$MM

15% EBITDA USD$MM 12%

100

244% 74

100 8% 26% 83

66

5%

22

0 0

4Q14 4Q15 4Q14 4Q15

64Thank You 65

You can also read