Four Trends Re-Shaping Investment Management - Economic ...

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Citi Markets & Securities Services – Business Advisory Services

10th January 2019

Four Trends Re-Shaping Investment Management

Presentation for the Economic Club of Florida

For Institutional Clients Only

Citi Business Advisory Services Global: Sandy Kaul, 212-723-5118 Sandy.Kaul@citi.com

EMEA: Robert Crossley, +44 (0) 207 986 9255 Robert.Crossley@citi.com

US: Matt Kummell, 212-723-2848 Matt.Kummell@citi.com

Strictly Private and ConfidentialAgenda

Improved Factor Understanding Drives New Thinking About Portfolio Construction

Investors Demonstrate a Significant Shift to Passive Over Actively Managed Funds

Actively Managed Funds Re-Align to High Conviction, Thematic & Alternatives

Emerging Technologies Offer Potential to Democratize Access to Real Assets

2

1Rethinking Asset Class Diversification

Since the late 1950s, investors have sought to build diversified portfolios of asset class

exposures that seek to balance risk and reward, but our understanding of risk is evolving

Evolving Understanding of Portfolio Diversification

Real Assets Real Assets

Alternatives Private Equity Common Factor

Rates Exposures

Hedge Funds Inflation

Growth

Rates Liquidity

Currency

Exposure to

Bonds Geography

Diversified Companies Sector

Asset Credit

Companies

Class

Exposures

Common Factor

Exposures

Volatility

Inflation

Equities Equities

Growth

Momentum

Geography

Sector

• By diversifying across asset • Asset classes are not mutually exclusive units • Real assets and rate-linked

classes, investors should be investments also share many

able to find the best possible • Many are comprised of exposure to a set of common risk factors, several of which

return for the least possible risk companies that share common risks overlap with company risk factors

Source: Citi Business Advisory Services

3

2Risk Balancing

To ensure diversification without disrupting their existing fund allocation, some institutions go long

or short specific factor exposures outside their desired range to balance their portfolio holdings

Adjusting for Factor Exposures at a Portfolio Level

Asset Class Fund Allocations Under- Factor Exposures Over-

Exposed 0 Exposed

Alternatives

Volatility

Inflation

Bonds Growth

Momentum

Aggregate

Exposures Liquidity

Duration

Credit Risk

Equities

Real Rates

Emerging

Markets

• Many sophisticated institutional investors look to manage their unintended Desired Range

factor exposures, but there is significant debate as to whether this practice Buy Sell

undermines the value of the core allocations Exposure Exposure

Source: Citi Business Advisory Services

4

3Re-Categorizing Allocations Based on Return Profile

Other investors are re-thinking whether asset classes are the best way to categorize and diversify

their portfolio—many are beginning to re-assign strategies based on their return profile

Re-Assigning Strategies Based on their Return Profile • A wide variety of sub-strategies can be

found within the Equity, Bond and

Asset Class Return Profile Alternatives buckets

Systematic Illiquid • Sub-strategies offer highly divergent

Alternatives Macro Limited return profiles:

Mark-to- •

Market • ,Some align to low volatility bond-

Returns like returns

Distressed

Bonds • Some align to higher volatility

Bonds

Higher equity-like returns and

G-10 Volatility

Rates Equity- • Others are illiquid and very long-

Fund Like term in nature and are thus only

Returns occasionally marked-to-market to

track their contribution

Emerging

Markets • Some institutions have now begun to re-

Low

Equities Equity categorize these various sub-strategies

Volatility

Bond- and group them more effectively to reflect

Quant the types of risks and return streams they

Long- Like

Returns offer to the portfolio

Short EQ

• This is seen as helping ensure better

diversification and more effective risk

control according to participants in

proprietary Citi surveys

Source: Citi Business Advisory Services

4Re-Thinking Sources of Investment Returns

Improved risk technologies allow investors to slice and dice portfolios to look more deeply into

what is the driver of returns and thus better isolate and target the specific sources of returns

Fund or Portfolio Sources of Investment Returns

Return Attribution

Asset Idiosyncratic

Selection Exposures

& Capacity

Momentum Technical

Volatility

Duration

Factors:

Liquidity etc.

Growth Style

Value

Quality

Factors

Credit Grade etc.

Interest Rate Sensitivity Risk

Credit Risk—Ability to Repay

Factors

Equity Risk—Earnings on Cash

Inflation Sensitivity etc.

Financials

Sector

Automotive

Energy Exposures

Consumer Goods etc.

Local Market

Developed Markets Geographic

Emerging Markets Exposures

Specific Countries etc.

Source: Citi Business Advisory Services

5Increasing Use of Index Exposures in Portfolio Construction

A more precise view of the various sources of return for the portfolio allows investors to replace

many expensive active managers with low cost indices for much of their exposures

Traditional Approach Shifting Approach to Portfolio Construction Emerging Approach

EQ B A External

Idiosyncratic

Active

Exposures

Managers

Technical

Factors

External

Active

Managers Style

Factors

Active

Index

Risk

Selection

Factors

Sector

Exposures

Asset Geographic

Allocation Exposures

Source: Citi Business Advisory Services

6Agenda

Improved Factor Understanding Drives New Thinking About Portfolio Construction

Investors Demonstrate a Significant Shift to Passive Over Actively Managed Funds

Actively Managed Funds Re-Align to High Conviction, Thematic & Alternatives

Emerging Technologies Offer Potential to Democratize Access to Real Assets

7Impact of Rising Index Offerings

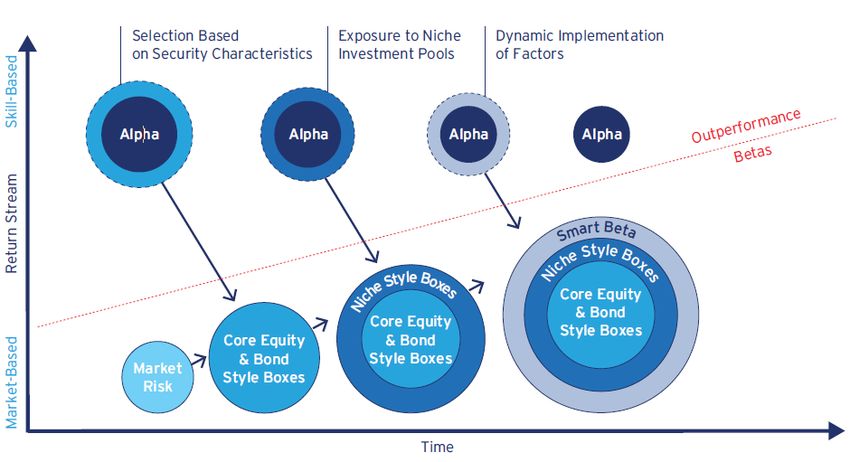

Technology is enabling managers to dynamically identify and construct indices or baskets of

securities to provide exposure to specific factors, shifting factor-related returns from alpha to beta

Reclassification of Outperformance to Beta

*1995: 32 Stocks to

Each Tradable Index

2016: 1.2 Tradable Indices

To Each Stock

• The ever-expanding variety of tradable index offerings are allowing investors to directly access sources of return

that used to only be available through active management and that were considered to be “outperformance”

• Now those return sources can be captured as an alternate type of market return or “beta”, helping to explain why

increasingly, investors are only viewing idiosyncratic returns as alpha-generating

Source: Citi Business Advisory Services. *“What’s Behind the Falling Number of Public Companies?”, Vanguard.com,

https://advisors.vanguard.com/VGApp/iip/site/advisor/researchcommentary/article/IWE_InvResBhndFallPublCompanies

8Drivers of New Portfolio Construction Approach

The number of index offerings increased 4.5X between 2007 and 2017—the growing variety of

index offerings and cost advantage is helping drive the move away from actively managed funds

Growth in Number of Passive Fund Offerings Actively Managed vs. Passive Fund Fees

ETFs & US Index Funds Actual Paid by Institutional Investors: 2016

Basis Points

70

7,593

Number of Funds

8000

59

60

7000

50

6000

+4.5x 37

40

5000

30 28

4000 AUM Growth by Category

2007-Q3 2018: 20

14

3000

Equity ETFs: +5.7X $3.9T

1,667 Bond ETFs: +13.4X $823B 10

4

6 6

4

2000

Int’l ETFs: +7.2X $767B

0

1000 Asian ETFs: +8.6X $508B US Large Cap US Small/Mid Non-US EQ US FI (Core)

US Index MFs: +3.9x $3.4T* Cap

0

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 Active Managers Passive Funds

• The number of passive fund offerings has expanded • Fee advantages are a major reason that many investors

dramatically in the past decade are choosing to utilize low-cost ETFs and indices

• Growth has occurred across a wide range of categories, • The largest institutional investors that can command the

boosting the variety of indices that investors can choose lowest fees paid between 14 bps for US Core Fixed

to gain exposure Income and 59 bps for US Small/Mid-Cap actively

managed funds in 2016 according to Callan

• Smart Beta funds that isolate specific technical and style

factors are further expanding investor options • By contrast, the range for passive funds was 4-6 bps

*Data as of 2017. Sources: Left-hand Chart: Citi Business Advisory Services analysis based on proprietary data subscriptions to SimFund and eVestment. US Mutual fund data from

www.ici.org. Right hand chart: Callan 2017 Investment Management Fee Survey. Active fees are for the largest category of investor (cheapest fees) and passive fees represent average

9

across all investor bands. https://www.callan.com/wp-content/uploads/2017/10/Callan-2017-Investment-Manager-Fee-Survey.pdfDecisive Shift to Passive Fund Exposures

Since 2011,net new investor flows into passive funds has outstripped flows into actively managed

funds by nearly 5X – with flows into active managers showing a net negative since 2015

Comparison of Net New Flows into Actively Managed vs. Passive Funds

2,000 Passive

Active

1,500 Passive Funds

1,263 2011-H1 2018 : $5.2T

1,000 515 2015-H1 2018: +$3.1T

Investor Flows

(USD billions)

461 564

500 647 927

786 640 679

424 531

282 Active Funds

190

0 37 2011-H1 2018: +$1.1T

-145

-432 -549 2015-H1 2018: -$447B

(500) -290

(1,000)

2011 2012 2013 2014 2015 2016 2017 1H18

• Net investor flows into passive funds topped $5.0 trillion between 2011 and H1 2018, a figure 4.7X larger than the

net new flows into actively managed funds

• Active fund managers have in particular struggled since 2015 as both the financial press and global regulators have

been vocal in their views about how fees negatively impact long-term returns. Since 2015, actively managed funds

have registered outflows of $447 billion through H1 2018

Source: Citi Business Advisory Services based on proprietary data subscriptions to Morningstar, eVestment and Simfund

10Agenda Improved Factor Understanding Drives New Thinking About Portfolio Construction Investors Demonstrate a Significant Shift to Passive Over Actively Managed Funds Actively Managed Funds Re-Align to High Conviction, Thematic & Alternatives Emerging Technologies Offer Potential to Democratize Access to Real Assets 11

Shifting Goals for Actively Managed Funds

Active managers with returns too close to a benchmark that can be replicated through a cheaper

index fund are becoming more active in their security selection to generate differentiated returns

Traditional Active Funds High Conviction Funds Thematic Funds

Performance Performance

Performance / Benchmark Benchmark

Benchmark

Universe

Full Set of Securities High Conviction Sub-Set Benchmark

Universe Select

Cross-

Universe

Benchmark Securities

Benchmark Universe Benchmark Universe Universe

• Traditional actively managed funds • High conviction funds choose a sub-set • Thematic funds choose securities

overweight or underweight securities of securities, concentrating their bets across several benchmark universes,

across the entire benchmark universe to across a fewer number of names so uniting those choices by a common

outperform—this makes for returns that correct choices can outperform the characteristic in the pursuit of

tightly clustered around the benchmark benchmark by a more significant degree uncorrelated opportunistic returns

Actively-Managed More Actively-Managed

Source: Citi Business Advisory Services

12Growth Accelerates in New Active Fund Categories

Though AUM in traditional long only active core funds rose over the past decade, the pace of

growth trailed those funds that offer more specialized or thematic strategies

AUM Growth 2008 to H1 2018 Market Share Changes • Specialty long funds that include

2008 to H1 2018 high conviction strategies added

+48% +115% 100%

9000 nearly as much AUM as active

90%

Billions of Dollars

8000 27% 35% core funds over the past decade

+$8.6T 80%

7000 70%

+$7.6T • Specialty long funds grew by

6000 60%

50% 115% between 2008 and H1

5000

40% 2018,rising from $6.6 trillion to

4000 73% 65%

30% $14.2 trillion and gaining 8%

3000 market share over active core

20%

2000 10%

1000 0% • Active core grew 47.5% in the

0 2008 H1 2018 corresponding period from $18.0

Active Core Specialty Long (Ex- to $26.6 trillion—losing 8% share

Active Core Specialty Long (ex-ESG)

ESG)

Growth in ESG / Impact Funds

• The most widely recognized category of thematic funds are those 1,550

Billions of Dollars

$1.4T

that isolate companies that lead their industries in environmental,

1,350

societal or governance practices (aka ESG or impact funds)

1,150

• Total AUM has more than doubled in these funds over the past 950

decade, rising to $1.4 trillion in H1 2018

750 $639B

• In our proprietary surveys, Institutional investors cite their belief that 550

these companies will outperform their peers over time due to already

existing practices and investments whereas retail and wealth 350

investors focus on these funds as a way of impacting the world with

their investment dollars

Sources: Top charts: Citi Business Advisory Services analysis based on the Boston Consulting Group Global Asset Management Study 2018, https://www.bcg.com/en-

13 us/publications/2018/global-asset-management-2018-digital-metamorphosis.aspx Bottom Chart: Citi Business Advisory Services analysis based on proprietary data subscriptions to

Morningstar and eVestmentMore Opportunities & Interest in Private Markets

More foundational issues exist in the publicly traded markets beyond a shifting approach to active

management and the move to passive--more and more activity is occurring in the private markets

Dry Powder in Private Equity Investments Downward trend in US & European IPOs

• Ready availability of private capital is allowing more companies to forego the public markets – especially small firms

with valuations below $50 million; more growth opportunities are now only to be found in the private markets

• Many private companies express concern about short-termism in the public markets; institutional investors also see the

focus on short-term financial results as out of sync with what is required to sustain long-term growth

• While cash may be available, staying private makes it harder for their employees to monetize their wealth tied up in

these companies and boxes investors unable to meet suitability thresholds out of many growth opportunities

Source Left Hand Chart: Citi Business Advisory Services Analysis based on proprietary subscription to Preqin. Source Right Hand Chart: Citi Business Advisory Services based on

Dealogic data to 30 June 2017

14Alternative Flows Dominate, Focus on Most Illiquid

Net inflows into Alternative products outstripped passive flows in recent years with 79% of that

money going to the industry’s most illiquid assets in private equity, real estate & infrastructure

Total Industry Net Flows: Active, Passive & Alternative Breakdown of Inflows into Alternatives

2014 to H1 2018 2014 - 1H18 ($4.1Tn)

3,000

Alternatives: +$4.1T

Passive: +$3.8T 1,043 79%

2,000 Active: -$257B Infrastructure

& Real Estate

(USD Billions)

Private Equity $1,221 B

880 812 1,263 30%

907 $2,006 B

1,000 49%

647 927 433 Private Debt

640 679 $467 B

190 282 12%

0 -145

-432 -549

Hedge Funds Liquid Alts

$58 B $323 B

-1,000 1% 8%

2014 2015 2016 2017 1H18

• Global flow data shows that investors have moved into • Flows have not just been directed to alternatives as a

illiquid funds and private markets in their search for yield whole, but into the two most illiquid portions of the

and diversification alternatives space

• While flows into passively traded funds from 2014 to H1 • Private equity inflows totaled $2.0 trillion between 2014

2018 totaled $3.8 trillion, alternative fund flows were +8% and H1 2018 (49%) and real estate and infrastructure

larger at $4.1 trillion in the corresponding period. These accounted for $1.2 trillion (30%)

figures compare to a net outflow of -$257 billion from

actively managed funds

Source left hand chart: Citi Business Advisory Services based on proprietary data subscriptions to Morningstar, eVestment, Simfund, HFR, and Preqin.

15 Right hand chart: Citi Business Advisory Services based on proprietary data subscriptions to Simfund, Preqin and HFR..Demographic Challenges for Industry

Accelerating Baby Boomer retirements are shifting the industry to one where individuals will be

left to manage more of their own money, resulting in less robust and diverse portfolios

Assets Managed for Institutions Less 2017 Portfolio Allocation

Assets Managed for Individuals (US) U.S. Corporate & Public DB Plans vs. IRAs

$7 $6.6T 100%

Baby Boomer Retirements

16.9%

$6 22.2%

$5.3T

$5 Individuals limited

to equity & bonds

$4 50% 97%

Cash

80.1%

74.2%

$3

Alternatives

$2.1T

$2

Equities & Bonds

$1 0%

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 Corp DB Public DB IRAs

• The bulk of professionally managed U.S. assets are • Institutional investors have shifted a significant share of

invested on behalf of institutions that can use their their portfolio into alternative investments

more sophisticated status to access a wider array of • These alternative investments offer both an illiquidity

illiquid and sophisticated investment options premium and the potential to access cash flows

• With Baby Boomers retiring and pulling their money uncorrelated to listed companies

out of defined benefit and defined contribution plans, • Individuals are limited to such public companies in their

there is a shift underway—by the early 2020s, more investment options and most are over-exposed to only

of the industry’s assets are going to be managed on one real asset—their home

behalf of individuals, not institutions

Sources: Left hand chart: Citi Business Advisory Services analysis based on proprietary data subscription to Cerrulli Associates. Right hand chart: Citi Business Advisory Services analysis

based on proprietary data subscription to Cerulli Associates and on Willis Towers Watson Global Pension Assets Study 2017, https://www.willistowerswatson.com/en/insights/2017/01/global-

16

pensions-asset-study-2017, proprietary subscriptions to Hedge Fund Research (HFR), Morningstar, eVestment, SimFund, and Preqin, http://investments.yale.edu/about-the-yio/Agenda Improved Factor Understanding Drives New Thinking About Portfolio Construction Investors Demonstrate a Significant Shift to Passive Over Actively Managed Funds Actively Managed Funds Re-Align to High Conviction, Thematic & Alternatives Emerging Technologies Offer Potential to Democratize Access to Real Assets 17

Understanding the Architecture Underlying Digital Assets

Early digital assets such as Bit Coin have been greeted with widespread skepticism by many but

the architecture underlying such assets may help democratize access to alternative investments

Digital Assets & their Underlying Architecture

• New digital assets have garnered many headlines and

resulted in highly volatile and unregulated parallel capital

New Products

markets activity

• Regulators are looking into establishing rules for these

Cryptocurrencies Coin Offerings markets, but their future is uncertain

• The architecture that these products are built upon,

however, can be levered to create registered investment

products that may democratize access to alternatives

• Big Data & AI Analytics: New technologies developed

by Google allow for the processing of huge, unstructured

Big Data & AI Analytics data sets and the application of “smart” toolkits such as

machine learning and natural language processing

Product Architecture

• Smart Contracts: New digital contracts code in the

terms of execution, link such terms to specific data-driven

triggers that can be monitored using Big Data & AI

Smart Contracts analytics and allow for the self-execution of those terms

when a trigger is activated

• Distributed Ledgers: Distributed ledgers record

transactions but have 3 advantages over traditional

ledgers: 1) all interested parties can simultaneously see

Blockchain / Distributed Ledgers transactions; 2) each transaction is secured by two

independently verified crypto-keys; 3) the entire history of

each transaction is contained in each entry

Source: Citi Business Advisory Services

18New Shared Ownership Models for Access to Real Assets

Tokenization might enable today’s models around crowd-investing and unitization for ownership of

real assets to extend to a more democratized set of investors with smaller liquidity thresholds

Carve Out Minority Divide Minority Access Natural

Share of a Real Share of Asset Up Level of Demand by

Asset into Individual Units Fractionalizing Unit

• Co-investing in real assets • Unitizing assets entails • Tokenizing each investable unit

features a majority asset owner breaking up the shared allows demand be adjusted down

“sharing” their ownership investable pool into a pre- to fractional bits that can meet

stake with either an outside determined number of fixed trading interest from both large

entity or the crowd pieces and small investors

FRACTIONAL UNITS

TOKENS OF

REAL ASSET

OWNERSHIP

MINORITY MINORITY UNITS OF

SHARE OF SHARE OF REAL ASSET IDENTICAL

REAL ASSET REAL ASSET OWNERSHIP SMART

MAJORTY CONTRACTS

SHARE OF DESCRIBING

REAL ASSET BLOCKCHAIN LEDGER

OWNERSHIP

RIGHTS

SEPARATE ABILITY TO REASSEMBLE

CONTRACT FRACTIONAL UNITS BACK

DESCRIBING SEPARATE STANDARDIZED TO ORIGINAL WHOLE

MINORITY CONTRACTS DESCRIBING

OWNERSHIP RIGHTS UNIT OWNERSHIP RIGHTS

Source: Citi Business Advisory Services

19Opportunity for Financial Instrument Innovation

Survey participants in our Industry Revolution report envision new real asset models and the

blueprint underlying cryptocurrencies to create a new investment instrument--Ownits

New Solution:

• Expand the “shared ownership” model to a broad set of

real assets

• Make this approach affordable by dividing these assets up

into units

New Liquid

• Create a new registered digital token using smart

contracts that define the rights of the unit owners and embed Ownership Units

the contracts into the blockchain (Ownits)

• Facilitate fractionalization and secondary liquidity

• Leverage existing primary and secondary market

transmission mechanisms

Source: Citi Business Advisory Services

20Ownits as New Investment Vehicles

Ownits would create the ability to have a listed ownership unit that offers the owner both financial

and non-financial rights to the underlying asset as well as a set of utilization rights

Model of an Ownit

Ownits may offer a series of financial and non-

financial rights in the underlying asset:

• Financial Rights: Total return investment,

including both cash flow participation and

long-term appreciation of the underlying

asset

• Ownership Rights: The Ownit owner can list

Ownits on their financial statement, pass the

Ownit on to their heirs or choose to transfer

ownership to another holder

• Utilization Rights: Ownit holders could partake

in the utilization of their asset via incentives

such as discounted rates and preferential

consideration for use or access

Source: Citi Business Advisory Services

21Ownits Might Be Used to Solve Many Investor Problems

Both institutional and individual investors may find benefits through the use of real asset tokens

that could both democratize access to new types of investments and support more localization

Use Cases to Highlight Potential of New Investment Template

Pension Plan Supplements Individual Business Owner

Institutional Investor

Liability Shortfall via Finances Capital

Frees Up Liquidity in

Extension of Improvements Through

Existing Real Asset Holding

Utilization Rights Shared Ownership Model

• Problem: Institutional investor • Problem: Pension does not have • Problem: Individual owner

currently owns a real asset such as a sufficient assets to meet their full needs capital to expand or

shopping mall but they need some liability to members improve their business but does

liquidity and do not wish to sell their not want to take on additional

entire stake and/or other investors are • Solution: Pension might invest in debt or partners

against any overall asset sale an asset that individuals could

utilize such as a housing • Solution: Individual could allow

• Solution: Investor might carve out a community and offer members local institutions or a pool of

minority share of their investment and “credits” via tokens to use the individuals to take on a minority

sell the right to participate in their asset/ live in the community to ownership in their business via a

investment to the crowd via a offset owed liabilities tokenized offering

tokenized offering

• Benefit: Long-term asset that • Benefit: Incoming cash for the

• Benefit: Incoming cash for the should generate income and individual business owner and an

institution and an ability for individuals appreciate for pension fund and incentivized pool of local owners

to both own a portion of the property utilization benefit for retired to support their business and

and participate in its revenue- pension member to offset any exposure to a new asset and

generation and appreciation benefit shortfall potential cash flow for investors

Source: Citi Business Advisory Services

22Disclaimer

This communication is provided by a member of the Business Advisory Services Group of Citigroup Global Markets Inc. (together with its affiliates,

"Citi"). For important disclosures and disclaimers please see https://icg.citi.com/icg/data/documents/ST_ExternalDiscl.pdf. This message is for the

internal use of the intended recipients and may contain information proprietary to Citi which may not be reproduced, redistributed, or copied in whole or

in part without Citi's prior consent.

The information contained in this communication is for discussion purposes only. Information provided does not constitute or include professional legal

and tax or any other form of advice and should not be relied on as such.

Information is provided to the recipient solely on the basis that the recipient will make all decisions, regardless of their nature, based on its own

independent evaluation and judgment regarding their appropriateness for the recipient's own business. Any decisions made by the recipient will be

made independently and separate from this communication and any other material provided by Citi, and in reliance on the advice of its other

professional advisors as the recipient may deem necessary and not in reliance on any communication whether written or oral from Citi. Though Citi

hopes its services will be helpful, Citi is not acting as investment advisor or fiduciary to the recipient or its clients, and the recipient's clients are not

third-party beneficiaries of Citi's services. No communication whether written or oral will be understood to be an assurance or guarantee of results.

This communication is provided by Citi on a confidential basis for the recipient's use and may not be publicly disclosed. The information contained

herein (a) is for informational purposes only and may not be publicly disclosed, (b) is not an offer to buy or sell any securities or service, and (c) may

contain estimates and projections which may be incomplete or condensed and may be inaccurate. No representation or warranty, express or implied,

is made as to the accuracy or completeness of the information and nothing herein is, or shall be relied upon as, a representation. Citi has no obligation

to update or otherwise revise any such information.

© 2019 Citigroup Global Markets Inc. Member SIPC. All rights reserved. Citi and Arc Design are trademarks and service marks of Citigroup Inc. or its

affiliates and are used and registered throughout the world.

23You can also read